Management Accounting Systems, Applications, and KEF Limited Report

VerifiedAdded on 2023/01/19

|17

|4225

|89

Report

AI Summary

This report provides a comprehensive overview of Management Accounting Systems (MAS) and their applications within a business context, using KEF Limited as a case study. It begins with an introduction to MA, defining its role and principles, and differentiating it from financial accounting. The report then delves into various MAS, including cost accounting, inventory management, job costing, and price optimization systems, highlighting their benefits and importance. The second task focuses on cost accounting techniques, detailing absorption and marginal costing methods, and demonstrating their application through profit and loss statements. Finally, the report explores the advantages and disadvantages of budgetary control as a planning tool, providing a complete analysis of MAS and its impact on business operations. The report concludes with a discussion of the importance of reliable, up-to-date, and accurate financial information. The report is a contribution to Desklib, a platform providing study resources.

Management

Accounting Systems

And It's Applications

Accounting Systems

And It's Applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3..........................................................................................................................................13

TASK 4 .........................................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3..........................................................................................................................................13

TASK 4 .........................................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

The term management accounting (MA) is a way of accounting in which

companies all kind of transactions' information including monetary and non monetary

aspects is recorded in a systematic manner (Yigitbasioglu, 2017). Under this accounting

the purpose of recording these information is to produce internal reports that may help

to management department in effective decision making regards to different context.

The aim of project report is to spread out information about role of MA for business

entities. For better understanding a company has been selected that is KEF limited. The

company operates in manufacture sector. The report covers detailed information about

various management accounting systems (MAS), MA reports and planning tools. Along

with role of MAS in sorting monetary issues is also described under the report.

TASK 1

Introduction of MA:

MA and its definition.

MA – This accounting is a systematic process of recording and presenting quantitative

& qualitative information in the form of internal reports. It is not essential for companies

to apply this accounting in their operations.

Definition of MA:

According to Charted Institute of Management Accountants (CIMA), MA is “the way of

identify, analyse, producing, interpretation of information that is needed by managers in

order to plan and control in a business entity.”

MAS – The term MAS can be defined as those accounting systems which aligns with

business operations and provide framework to managers in effective management

(Nielsen, 2015).

Importance to integrate MAS with organisations:

The term management accounting (MA) is a way of accounting in which

companies all kind of transactions' information including monetary and non monetary

aspects is recorded in a systematic manner (Yigitbasioglu, 2017). Under this accounting

the purpose of recording these information is to produce internal reports that may help

to management department in effective decision making regards to different context.

The aim of project report is to spread out information about role of MA for business

entities. For better understanding a company has been selected that is KEF limited. The

company operates in manufacture sector. The report covers detailed information about

various management accounting systems (MAS), MA reports and planning tools. Along

with role of MAS in sorting monetary issues is also described under the report.

TASK 1

Introduction of MA:

MA and its definition.

MA – This accounting is a systematic process of recording and presenting quantitative

& qualitative information in the form of internal reports. It is not essential for companies

to apply this accounting in their operations.

Definition of MA:

According to Charted Institute of Management Accountants (CIMA), MA is “the way of

identify, analyse, producing, interpretation of information that is needed by managers in

order to plan and control in a business entity.”

MAS – The term MAS can be defined as those accounting systems which aligns with

business operations and provide framework to managers in effective management

(Nielsen, 2015).

Importance to integrate MAS with organisations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is important for businesses to integrate different accounting systems with

their operations and activities. Such as for finance department, it is important to link cost

accounting system so that expenses can be controlled. As well as for production

department, inventory management system can guide in order to manage overall stock.

Like in KEF limited company, they are using these accounting systems in their different

operations and activities.

Principles, role and origin of MA:

Principles- There are mainly four kind of principles of MA and each business entity is

needed to comply with these principles:

Influence- This principle of MA defines that it is important to communicate

accounting information among managers so that they can take corrective actions.

Relevance- In addition, this principle states that MA evaluates the key

information that can be helpful for better decision making in companies

operations (Cazier, Tian and Wilson, 2015).

Value- This principle of MA states that it links the company's process to its key

models and demands of the wide economic environment.

Credibility–According to this principle, if companies apply the MA in their

operations and activities then it becomes easier for shareholders to relay on

financial outcomes.

Role - The role of MA is too crucial and important for businesses. This is so because it

provides essential framework to users in order to manage different aspects. Like the

above KEF limited company is using this accounting system for gaining competitive

advantage over their rivalry firms.

Origin- The MA evolved after financial accounting and its origin can be traced before

300 years ago. This accounting was firstly used during industrial revolution in the aspect

of European merchant trading ventures.

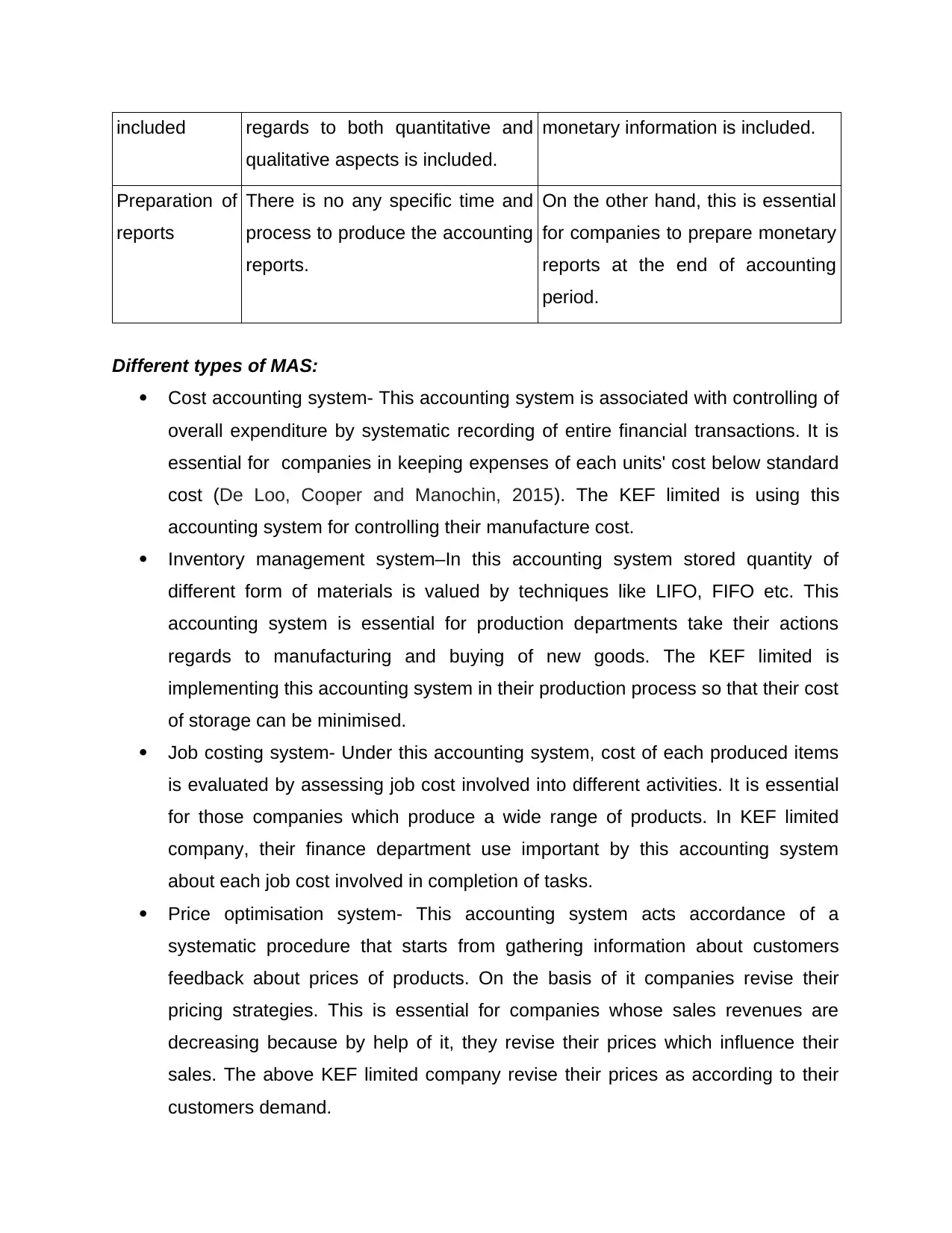

Difference between management and financial accounting:

Basis MA Financial accounting

Information Under this accounting information While in this accounting only

their operations and activities. Such as for finance department, it is important to link cost

accounting system so that expenses can be controlled. As well as for production

department, inventory management system can guide in order to manage overall stock.

Like in KEF limited company, they are using these accounting systems in their different

operations and activities.

Principles, role and origin of MA:

Principles- There are mainly four kind of principles of MA and each business entity is

needed to comply with these principles:

Influence- This principle of MA defines that it is important to communicate

accounting information among managers so that they can take corrective actions.

Relevance- In addition, this principle states that MA evaluates the key

information that can be helpful for better decision making in companies

operations (Cazier, Tian and Wilson, 2015).

Value- This principle of MA states that it links the company's process to its key

models and demands of the wide economic environment.

Credibility–According to this principle, if companies apply the MA in their

operations and activities then it becomes easier for shareholders to relay on

financial outcomes.

Role - The role of MA is too crucial and important for businesses. This is so because it

provides essential framework to users in order to manage different aspects. Like the

above KEF limited company is using this accounting system for gaining competitive

advantage over their rivalry firms.

Origin- The MA evolved after financial accounting and its origin can be traced before

300 years ago. This accounting was firstly used during industrial revolution in the aspect

of European merchant trading ventures.

Difference between management and financial accounting:

Basis MA Financial accounting

Information Under this accounting information While in this accounting only

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

included regards to both quantitative and

qualitative aspects is included.

monetary information is included.

Preparation of

reports

There is no any specific time and

process to produce the accounting

reports.

On the other hand, this is essential

for companies to prepare monetary

reports at the end of accounting

period.

Different types of MAS:

Cost accounting system- This accounting system is associated with controlling of

overall expenditure by systematic recording of entire financial transactions. It is

essential for companies in keeping expenses of each units' cost below standard

cost (De Loo, Cooper and Manochin, 2015). The KEF limited is using this

accounting system for controlling their manufacture cost.

Inventory management system–In this accounting system stored quantity of

different form of materials is valued by techniques like LIFO, FIFO etc. This

accounting system is essential for production departments take their actions

regards to manufacturing and buying of new goods. The KEF limited is

implementing this accounting system in their production process so that their cost

of storage can be minimised.

Job costing system- Under this accounting system, cost of each produced items

is evaluated by assessing job cost involved into different activities. It is essential

for those companies which produce a wide range of products. In KEF limited

company, their finance department use important by this accounting system

about each job cost involved in completion of tasks.

Price optimisation system- This accounting system acts accordance of a

systematic procedure that starts from gathering information about customers

feedback about prices of products. On the basis of it companies revise their

pricing strategies. This is essential for companies whose sales revenues are

decreasing because by help of it, they revise their prices which influence their

sales. The above KEF limited company revise their prices as according to their

customers demand.

qualitative aspects is included.

monetary information is included.

Preparation of

reports

There is no any specific time and

process to produce the accounting

reports.

On the other hand, this is essential

for companies to prepare monetary

reports at the end of accounting

period.

Different types of MAS:

Cost accounting system- This accounting system is associated with controlling of

overall expenditure by systematic recording of entire financial transactions. It is

essential for companies in keeping expenses of each units' cost below standard

cost (De Loo, Cooper and Manochin, 2015). The KEF limited is using this

accounting system for controlling their manufacture cost.

Inventory management system–In this accounting system stored quantity of

different form of materials is valued by techniques like LIFO, FIFO etc. This

accounting system is essential for production departments take their actions

regards to manufacturing and buying of new goods. The KEF limited is

implementing this accounting system in their production process so that their cost

of storage can be minimised.

Job costing system- Under this accounting system, cost of each produced items

is evaluated by assessing job cost involved into different activities. It is essential

for those companies which produce a wide range of products. In KEF limited

company, their finance department use important by this accounting system

about each job cost involved in completion of tasks.

Price optimisation system- This accounting system acts accordance of a

systematic procedure that starts from gathering information about customers

feedback about prices of products. On the basis of it companies revise their

pricing strategies. This is essential for companies whose sales revenues are

decreasing because by help of it, they revise their prices which influence their

sales. The above KEF limited company revise their prices as according to their

customers demand.

Benefits of MAS:

Role of cost accounting- This helps in reducing unnecessary costs from

operations and activities by effective management. The above KEF limited

company's overall operational cost is decreasing that is helping them in

generating higher revenues.

Role of inventory management system- It benefits to companies in keeping cost

of inventory lower so that overall cost can be reduced (Charifzadeh and

Taschner, 2017). The above company is using this accounting that helping their

manufacturers in producing products as per market demand.

Role of Job costing system- As above stated, it helps in computing each units'

cost. In KEF limited company, their accountants evaluates manufactured outputs

cost by calculating each job cost.

Role of price optimisation system- On the basis of this accounting system, prices

of products are revised and set according customers feedback. The sales

department of above company utilise key information about demand of their

products in market and after that set the price.

Presenting financial information:

Reason for which information should be reliable, up to date and accurate- This is

important that financial information should have below mentioned features:

Relevant- The monetary information should be relevant as accordance to

companies operations. This is so because in the absence of it, accountants can

not produce accurate reports.

Up to date- In addition, financial information should be up to date because

companies do the transactions on regular basis. If information will be updated

that current performance can be evaluated.

Accurate- The financial information is needed to be error free so that correct

decisions can be taken by companies about different aspects (Vann, 2016).

Understandable- Along with the monetary information should be understandable

for all users, specially for managers so that they can prepare futuristic strategies.

Role of cost accounting- This helps in reducing unnecessary costs from

operations and activities by effective management. The above KEF limited

company's overall operational cost is decreasing that is helping them in

generating higher revenues.

Role of inventory management system- It benefits to companies in keeping cost

of inventory lower so that overall cost can be reduced (Charifzadeh and

Taschner, 2017). The above company is using this accounting that helping their

manufacturers in producing products as per market demand.

Role of Job costing system- As above stated, it helps in computing each units'

cost. In KEF limited company, their accountants evaluates manufactured outputs

cost by calculating each job cost.

Role of price optimisation system- On the basis of this accounting system, prices

of products are revised and set according customers feedback. The sales

department of above company utilise key information about demand of their

products in market and after that set the price.

Presenting financial information:

Reason for which information should be reliable, up to date and accurate- This is

important that financial information should have below mentioned features:

Relevant- The monetary information should be relevant as accordance to

companies operations. This is so because in the absence of it, accountants can

not produce accurate reports.

Up to date- In addition, financial information should be up to date because

companies do the transactions on regular basis. If information will be updated

that current performance can be evaluated.

Accurate- The financial information is needed to be error free so that correct

decisions can be taken by companies about different aspects (Vann, 2016).

Understandable- Along with the monetary information should be understandable

for all users, specially for managers so that they can prepare futuristic strategies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MA reports:

Inventory report- Under this report information about how much quantity of

material is being purchased, sold and utilised for production during a particular

time period. The above KEF limited company's accountants are preparing this

report for managing storage cost and for better utilisation of all materials.

Performance report- It is a kind of report that contains information regards to

actual outcome and estimated outcome as well as variation between these. On

the basis of it, managers take decision about progress of employees and

business entity. In above company, this report is being used in order to manage

performance of each aspects.

Account receivable ageing report- The report consists information about those

debtors whose amount is due even after the predetermined date. On the basis of

it, finance department makes plan about sources of fund. In the above company,

this report helps in keeping debtors collection period lower.

TASK 2

Cost- This can be defined as an overall expenditures which occur in process of

completing different operations and tasks. There are different kind of costs such

as direct material cost, labour cost, indirect cost and many more.

Fixed cost- Fixed cost is a type of cost which does not effect due to change in level of

production.

Variable cost- While the variable cost is a kind of cost that flex as accordance of

change in production.

Direct cost- It can be defined as a type of cost that is directly accountable to a

specific cost objective.

Indirect cost- This is a kinds of cost which is not directly linked o a specific cost

objective.

Different costing techniques:

Inventory report- Under this report information about how much quantity of

material is being purchased, sold and utilised for production during a particular

time period. The above KEF limited company's accountants are preparing this

report for managing storage cost and for better utilisation of all materials.

Performance report- It is a kind of report that contains information regards to

actual outcome and estimated outcome as well as variation between these. On

the basis of it, managers take decision about progress of employees and

business entity. In above company, this report is being used in order to manage

performance of each aspects.

Account receivable ageing report- The report consists information about those

debtors whose amount is due even after the predetermined date. On the basis of

it, finance department makes plan about sources of fund. In the above company,

this report helps in keeping debtors collection period lower.

TASK 2

Cost- This can be defined as an overall expenditures which occur in process of

completing different operations and tasks. There are different kind of costs such

as direct material cost, labour cost, indirect cost and many more.

Fixed cost- Fixed cost is a type of cost which does not effect due to change in level of

production.

Variable cost- While the variable cost is a kind of cost that flex as accordance of

change in production.

Direct cost- It can be defined as a type of cost that is directly accountable to a

specific cost objective.

Indirect cost- This is a kinds of cost which is not directly linked o a specific cost

objective.

Different costing techniques:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

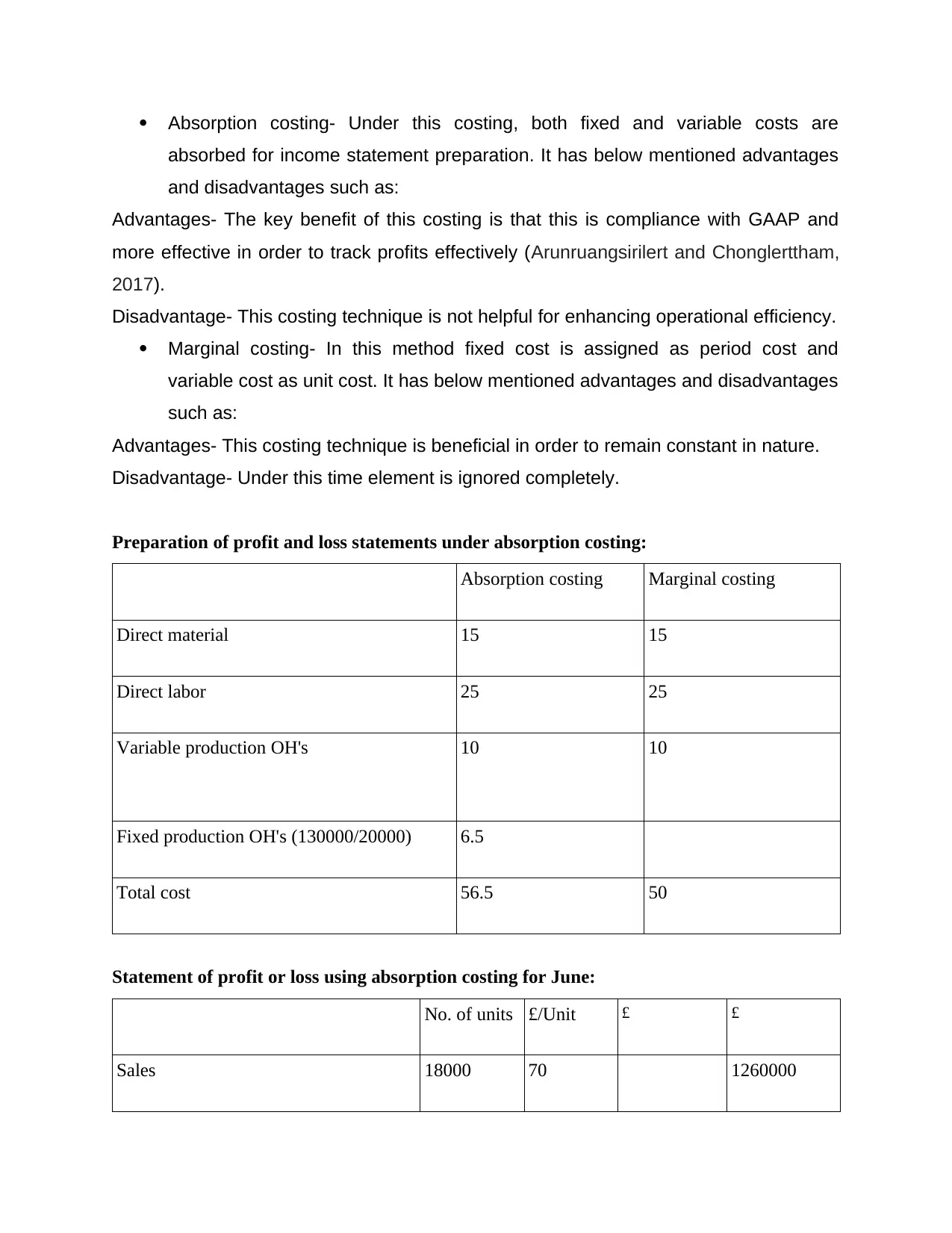

Absorption costing- Under this costing, both fixed and variable costs are

absorbed for income statement preparation. It has below mentioned advantages

and disadvantages such as:

Advantages- The key benefit of this costing is that this is compliance with GAAP and

more effective in order to track profits effectively (Arunruangsirilert and Chonglerttham,

2017).

Disadvantage- This costing technique is not helpful for enhancing operational efficiency.

Marginal costing- In this method fixed cost is assigned as period cost and

variable cost as unit cost. It has below mentioned advantages and disadvantages

such as:

Advantages- This costing technique is beneficial in order to remain constant in nature.

Disadvantage- Under this time element is ignored completely.

Preparation of profit and loss statements under absorption costing:

Absorption costing Marginal costing

Direct material 15 15

Direct labor 25 25

Variable production OH's 10 10

Fixed production OH's (130000/20000) 6.5

Total cost 56.5 50

Statement of profit or loss using absorption costing for June:

No. of units £/Unit £ £

Sales 18000 70 1260000

absorbed for income statement preparation. It has below mentioned advantages

and disadvantages such as:

Advantages- The key benefit of this costing is that this is compliance with GAAP and

more effective in order to track profits effectively (Arunruangsirilert and Chonglerttham,

2017).

Disadvantage- This costing technique is not helpful for enhancing operational efficiency.

Marginal costing- In this method fixed cost is assigned as period cost and

variable cost as unit cost. It has below mentioned advantages and disadvantages

such as:

Advantages- This costing technique is beneficial in order to remain constant in nature.

Disadvantage- Under this time element is ignored completely.

Preparation of profit and loss statements under absorption costing:

Absorption costing Marginal costing

Direct material 15 15

Direct labor 25 25

Variable production OH's 10 10

Fixed production OH's (130000/20000) 6.5

Total cost 56.5 50

Statement of profit or loss using absorption costing for June:

No. of units £/Unit £ £

Sales 18000 70 1260000

Cost of sales: 0 56.5 0

Opening stock 19000 56.5 1073500

Add- Production 1073500

Less- Closing stock 1000 56.5 56500 -1017000

Profit 243000

Less- Under absorption 13000

Reconciled profit with the marginal

costing

230000

Statement of profit or loss using marginal costing for June:

No. of units £/Unit £ £

Sales 18000 70 1260000

Prime cost:

Opening stock 0 50 0

Add- Production 19000 50 950000

Less- Closing stock 1000 50 50000 -900000

Contribution 360000

Less- Fixed production cost -130000

Profit 230000

Opening stock 19000 56.5 1073500

Add- Production 1073500

Less- Closing stock 1000 56.5 56500 -1017000

Profit 243000

Less- Under absorption 13000

Reconciled profit with the marginal

costing

230000

Statement of profit or loss using marginal costing for June:

No. of units £/Unit £ £

Sales 18000 70 1260000

Prime cost:

Opening stock 0 50 0

Add- Production 19000 50 950000

Less- Closing stock 1000 50 50000 -900000

Contribution 360000

Less- Fixed production cost -130000

Profit 230000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

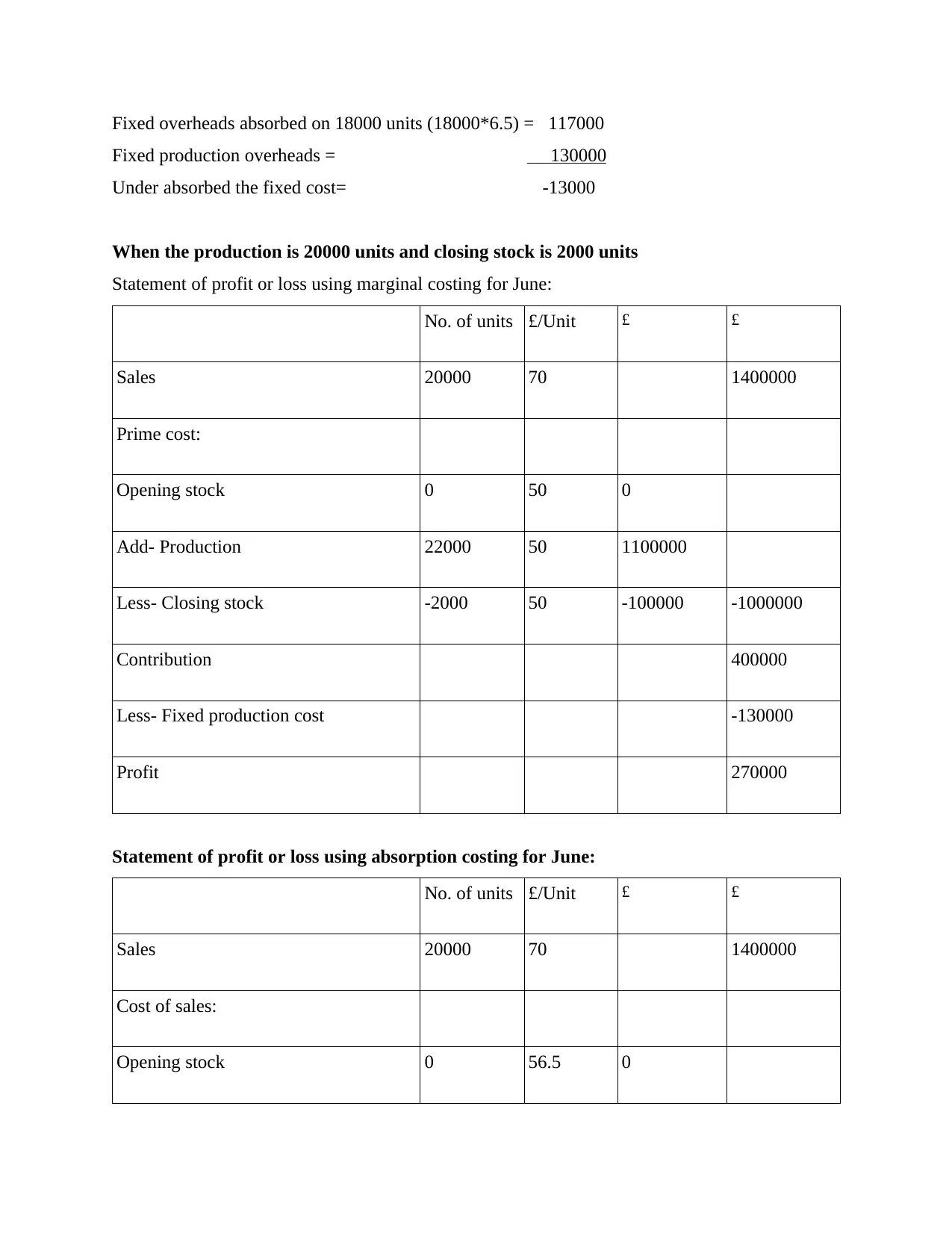

Fixed overheads absorbed on 18000 units (18000*6.5) = 117000

Fixed production overheads = 130000

Under absorbed the fixed cost= -13000

When the production is 20000 units and closing stock is 2000 units

Statement of profit or loss using marginal costing for June:

No. of units £/Unit £ £

Sales 20000 70 1400000

Prime cost:

Opening stock 0 50 0

Add- Production 22000 50 1100000

Less- Closing stock -2000 50 -100000 -1000000

Contribution 400000

Less- Fixed production cost -130000

Profit 270000

Statement of profit or loss using absorption costing for June:

No. of units £/Unit £ £

Sales 20000 70 1400000

Cost of sales:

Opening stock 0 56.5 0

Fixed production overheads = 130000

Under absorbed the fixed cost= -13000

When the production is 20000 units and closing stock is 2000 units

Statement of profit or loss using marginal costing for June:

No. of units £/Unit £ £

Sales 20000 70 1400000

Prime cost:

Opening stock 0 50 0

Add- Production 22000 50 1100000

Less- Closing stock -2000 50 -100000 -1000000

Contribution 400000

Less- Fixed production cost -130000

Profit 270000

Statement of profit or loss using absorption costing for June:

No. of units £/Unit £ £

Sales 20000 70 1400000

Cost of sales:

Opening stock 0 56.5 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Add- Production 22000 56.5 1243000

Less- Closing stock -2000 56.5 -113000 -1130000

Profit 270000

From the above mentioned costing systems, this can be suggested to above company that they

should make focus on implementation of absorption costing system.

Other techniques:

Apart from above mentioned techniques there are some other techniques such

as ABC, standard costing and many more that can produce accurate results in an

effective manner.

TASK 3

Advantage and disadvantage of planning tools of budgetary control.

Budgeting- It is a type of technique which is associated with process of setting futuristic

monetary goals in order to measure actual performance (Rubin, 2019). In simple term,

this is linked with making financial plan so that it can be determined whether companies

have enough amount of fund to operate various activities or not. This is beneficial for

business entities due to following reasons:

It is beneficial for companies in order to make better control over available

amount of funds.

In addition, it plays a significant role in identifying total number of spendings and

savings.

It helps in determining how much amount of debt can be opt out business entities

(Wildavsky, 2017).

Less- Closing stock -2000 56.5 -113000 -1130000

Profit 270000

From the above mentioned costing systems, this can be suggested to above company that they

should make focus on implementation of absorption costing system.

Other techniques:

Apart from above mentioned techniques there are some other techniques such

as ABC, standard costing and many more that can produce accurate results in an

effective manner.

TASK 3

Advantage and disadvantage of planning tools of budgetary control.

Budgeting- It is a type of technique which is associated with process of setting futuristic

monetary goals in order to measure actual performance (Rubin, 2019). In simple term,

this is linked with making financial plan so that it can be determined whether companies

have enough amount of fund to operate various activities or not. This is beneficial for

business entities due to following reasons:

It is beneficial for companies in order to make better control over available

amount of funds.

In addition, it plays a significant role in identifying total number of spendings and

savings.

It helps in determining how much amount of debt can be opt out business entities

(Wildavsky, 2017).

Budgetary control – It can be defined as a type of method that is related with managing

monetary outcomes in an effective manner by help of vital range of budgets. In KEF

limited company, they are using different kind of budgets such as:

Cash budget – It is a kind of financial plan under which information regards to

activities of in and out of cash. This budget is prepared in those business entities

wherein cash regarding activities are done on a regular basis. In the above

company, their managers use key information from this budget in order to

manage working capital requirement. It has some advantages and disadvantages

like:

Advantages- This budget helps to companies in identifying deficits on priority basis.

Disadvantage- Due to this budget, managers can not utilise fund as accordance of

business need. They tends to follow the cash budgets' activities.

Rolling budget- This is a type of budget, that is rolled out soon after end of

previous years' accounting period (Murthy and Rooney, 2018). The KEF limited

company is using this budget as after end of their accounting period.

Advantage – This is beneficial for becoming responsive to users in order to adjust

unexpected changes in an effective manner.

Disadvantage- This budget is not suitable for those companies wherein activities

change year by year.

Production budget- It is a budget in which estimation of activities regards to

materials and funds needed for production is included. The KEF limited

company, is preparing this budget for their manufacturing process.

Advantage- This is helpful for companies to make their production cost effectively.

Disadvantage- In some cases, wrong estimation of needed quantity of material or fund

may lead to huge financial lose.

Balance scorecard- It can be defined as a kinds of performance measurement

framework which is linked with process of finding and enhancing different business

monetary outcomes in an effective manner by help of vital range of budgets. In KEF

limited company, they are using different kind of budgets such as:

Cash budget – It is a kind of financial plan under which information regards to

activities of in and out of cash. This budget is prepared in those business entities

wherein cash regarding activities are done on a regular basis. In the above

company, their managers use key information from this budget in order to

manage working capital requirement. It has some advantages and disadvantages

like:

Advantages- This budget helps to companies in identifying deficits on priority basis.

Disadvantage- Due to this budget, managers can not utilise fund as accordance of

business need. They tends to follow the cash budgets' activities.

Rolling budget- This is a type of budget, that is rolled out soon after end of

previous years' accounting period (Murthy and Rooney, 2018). The KEF limited

company is using this budget as after end of their accounting period.

Advantage – This is beneficial for becoming responsive to users in order to adjust

unexpected changes in an effective manner.

Disadvantage- This budget is not suitable for those companies wherein activities

change year by year.

Production budget- It is a budget in which estimation of activities regards to

materials and funds needed for production is included. The KEF limited

company, is preparing this budget for their manufacturing process.

Advantage- This is helpful for companies to make their production cost effectively.

Disadvantage- In some cases, wrong estimation of needed quantity of material or fund

may lead to huge financial lose.

Balance scorecard- It can be defined as a kinds of performance measurement

framework which is linked with process of finding and enhancing different business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.