Management Accounting Systems and Financial Problem Responses

VerifiedAdded on 2023/06/08

|17

|4758

|478

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on cost analysis, budgetary control, and financial problem responses within organizations like Rite Track. It explains management accounting principles, essential requirements of different management accounting systems, and methods used for reporting, including performance, cost, budget, and inventory management reports. The report estimates costs using marginal and absorption costing techniques to prepare income statements and discusses the benefits and drawbacks of various planning techniques for budgetary control. Furthermore, it compares how organizations adapt their management accounting systems to respond to financial challenges, offering insights into practical applications and strategic decision-making. Desklib offers more solved assignments and study resources to help students excel.

Management

accounting

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1 Explain management accounting and also provide essential requirements of different types

of management accounting system.............................................................................................3

P2. Different methods that are exploited for the purposes of management accounting

reporting......................................................................................................................................4

P3 Estimate costs by utilising proper techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................6

P4 Explain the benefits and drawbacks of different kinds of planning techniques utilised for

budgetary control........................................................................................................................9

P5. Comparing how organisations adapts management accounting systems to respond to

financial problems.....................................................................................................................12

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1 Explain management accounting and also provide essential requirements of different types

of management accounting system.............................................................................................3

P2. Different methods that are exploited for the purposes of management accounting

reporting......................................................................................................................................4

P3 Estimate costs by utilising proper techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................6

P4 Explain the benefits and drawbacks of different kinds of planning techniques utilised for

budgetary control........................................................................................................................9

P5. Comparing how organisations adapts management accounting systems to respond to

financial problems.....................................................................................................................12

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is a concept which is preferred by each and every organisation

in order to make a number of reports by accessing the financial information of the organisation.

Rite Track was established in year 1993, it is a leader in aggregate sales and support solutions for

the semiconductor industry's most popular mature production coat and develop tools and water

carrier inspection systems. By initiating best practices and performing with honesty Rite Track

try to accomplish duties towards the environment, providing dependable and innovative

commodities that represents commitment of Rite Track towards wastage, energy saving ,

reduction in level of noise and purify air (Alsaid and Mutiganda, 2020). The report consists of

two parts. The first part includes the role and principle of management accounting and its

systems which are explained in detail using the techniques and method of marginal and

absorption costing. Further, the part is summed up by describing the integration and benefits of it

in the entity. The second part takes into consideration the different planning tools. Also the

financial problems of Rite Track are discussed in the following report.

MAIN BODY

P1 Explain management accounting and also provide essential requirements of different types of

management accounting system.

Management Accounting

It is also defined as managerial accounting. It is a method of accounting that helps in

creation of statements, reports and documents or papers that assist management in the procedure

of decision making which are incidental to the performance of entity. It is basically used for

internal operations of an enterprise. It helps the management to execute all its functions

including planning, organizing, staffing, directing and controlling (Aslanertik and Yardımcı,

2019).

Functions of management accounting and its systems

It defines to an procedure that generally focuses about perceiving and estimating

stratified goals to refer individual monetary and non-monetary information to superior

governing authority of a business concern. Administrators can utilise this data for preparing

various financial plans and execution of reports. The executive accounting is certainly have more

unexpected content as compared to organised summaries of budget. Important difference

Management accounting is a concept which is preferred by each and every organisation

in order to make a number of reports by accessing the financial information of the organisation.

Rite Track was established in year 1993, it is a leader in aggregate sales and support solutions for

the semiconductor industry's most popular mature production coat and develop tools and water

carrier inspection systems. By initiating best practices and performing with honesty Rite Track

try to accomplish duties towards the environment, providing dependable and innovative

commodities that represents commitment of Rite Track towards wastage, energy saving ,

reduction in level of noise and purify air (Alsaid and Mutiganda, 2020). The report consists of

two parts. The first part includes the role and principle of management accounting and its

systems which are explained in detail using the techniques and method of marginal and

absorption costing. Further, the part is summed up by describing the integration and benefits of it

in the entity. The second part takes into consideration the different planning tools. Also the

financial problems of Rite Track are discussed in the following report.

MAIN BODY

P1 Explain management accounting and also provide essential requirements of different types of

management accounting system.

Management Accounting

It is also defined as managerial accounting. It is a method of accounting that helps in

creation of statements, reports and documents or papers that assist management in the procedure

of decision making which are incidental to the performance of entity. It is basically used for

internal operations of an enterprise. It helps the management to execute all its functions

including planning, organizing, staffing, directing and controlling (Aslanertik and Yardımcı,

2019).

Functions of management accounting and its systems

It defines to an procedure that generally focuses about perceiving and estimating

stratified goals to refer individual monetary and non-monetary information to superior

governing authority of a business concern. Administrators can utilise this data for preparing

various financial plans and execution of reports. The executive accounting is certainly have more

unexpected content as compared to organised summaries of budget. Important difference

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

between them is that the first one is ready in association with inner cycles on the contrast the last

one is brought up for outsiders such as investors. It usually help in anticipating future patterns

and revenues of business operation which also suggests in making plans incidental to to expense.

The accounting framework is a method of controlling and effecting workers like

different costs which are basically for fulfilling initial goals. Mandatory execution of the

accounting framework in Rite Track is advantageous as it supply's different experiences which

assist in directing and organising processes (Booth, 2018).

Some Management accounting systems are as follows:

Cost accounting model is a important strategy which helps company in evaluating

product cost for performing beneficial examination and evaluation of stock. It is

advantageous for Rite Track as it helps in identification of items that are beneficial for

workings of business. This system in addition of these also help accountants of

foundation in preparing fiscal report. It contains job request and cycle costing strategies.

Stock administration system is conscious about valuing and accounting variations in

stock at any stage of organisation. Rite Track incorporates this model to grow its deals

and upsurge net revenues. Stock of business are of three kinds, to be specific, unrefined

element, ongoing work and acquired commodities. Its action is generally needed in

entities to upsurge functional capability and duration of business projects. It aid Rite

Track in diversifying direct costs associated with acquisition and troughing away

personalisation. It also helps organisations in holding additional stock which assist in

occurrence of insufficiency (Bourmistrov, Grossi and Haldma, 2019).

Cost streamlining system is a numerical model which helps an entity in falling down and

estimating how request differ with respect to the modification in stage of value of item

or administration. Data gathered by this model is accumulated with cost and stock at

suggestions of costs that recommends in further growth of the productivity. Rite Track

involves this system for gathering data about the trends of market, demands of consumer

and tendency to carry out its operations effectively.

Job costing model is a procedure of gathering various data about subsequent and

disjoining cost with selected work or task. It needs to occupy differential data in terms of

direct material, cost and upward. Rite Track involves this system in order to determine

quality of its estimating system which helps in providing estimations of items of cost. It

one is brought up for outsiders such as investors. It usually help in anticipating future patterns

and revenues of business operation which also suggests in making plans incidental to to expense.

The accounting framework is a method of controlling and effecting workers like

different costs which are basically for fulfilling initial goals. Mandatory execution of the

accounting framework in Rite Track is advantageous as it supply's different experiences which

assist in directing and organising processes (Booth, 2018).

Some Management accounting systems are as follows:

Cost accounting model is a important strategy which helps company in evaluating

product cost for performing beneficial examination and evaluation of stock. It is

advantageous for Rite Track as it helps in identification of items that are beneficial for

workings of business. This system in addition of these also help accountants of

foundation in preparing fiscal report. It contains job request and cycle costing strategies.

Stock administration system is conscious about valuing and accounting variations in

stock at any stage of organisation. Rite Track incorporates this model to grow its deals

and upsurge net revenues. Stock of business are of three kinds, to be specific, unrefined

element, ongoing work and acquired commodities. Its action is generally needed in

entities to upsurge functional capability and duration of business projects. It aid Rite

Track in diversifying direct costs associated with acquisition and troughing away

personalisation. It also helps organisations in holding additional stock which assist in

occurrence of insufficiency (Bourmistrov, Grossi and Haldma, 2019).

Cost streamlining system is a numerical model which helps an entity in falling down and

estimating how request differ with respect to the modification in stage of value of item

or administration. Data gathered by this model is accumulated with cost and stock at

suggestions of costs that recommends in further growth of the productivity. Rite Track

involves this system for gathering data about the trends of market, demands of consumer

and tendency to carry out its operations effectively.

Job costing model is a procedure of gathering various data about subsequent and

disjoining cost with selected work or task. It needs to occupy differential data in terms of

direct material, cost and upward. Rite Track involves this system in order to determine

quality of its estimating system which helps in providing estimations of items of cost. It

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

also helps organisation in creation of a reasonable benefits. Initial requirement of this

model is an entity is constant observation of creation process which helps with

recognition of challenges and making adaption in order to attempt not to hamper any

circumstances (Datar and Rajan, 2018).

P2. Different methods that are exploited for the purposes of management accounting reporting.

It is utilised for designing, controlling, decision making intention and evaluation of

performance. These reports are constantly prepared through the accounting and auditing period

according to requirements. The results of management accounting is in form of periodic reports

for the entity's department executives and CEO. For example, existing generation of sales

revenue, the existing position or situation of the organisation's accounts payable and accounts

receivables etc. Management reporting looks in the business in a more detailed way and shows

results from various sections. Despite on focusing on the whole organisation, management

reports focuses on a particular job, department or team.

Techniques utilised for management accounting reporting are:

Performance report: It can be termed as a detailed report which estimates outcomes of

particular workings which is related to the growth of organisation at any given point of time.

Management accountants of Rite Track, making best utilisation of budgets for making

comparison between actual expenses with incomes which are reliable on budgeted variables and

them list or updating information on grounds of performance of report. When a report is made,

executives design the demand of its future for customers and the need of a product in market and

in accordance of that modifications in prices are being made (Eaton, Grenier and Layman,

2019).

Cost report: While operating in Rite Track, management accounting analysis a number

of costs of manufacturing goods. On this basis, cost report is prepared in Rite track as it

examines all labour costs, raw material along with any type of additional cost in accordance to

sustain reporting of management accounting. The entire data is then adequately merged with the

cost report. And therefore, the method helps in monitoring and planning profit margins.

Budget report: This particular method plays a vital role in management accounting in

Rite Track for communicating as it focuses on preparation and diverging the budgets with

various departments of organisation. The report of budget emphasis on execution of Rite Track,

model is an entity is constant observation of creation process which helps with

recognition of challenges and making adaption in order to attempt not to hamper any

circumstances (Datar and Rajan, 2018).

P2. Different methods that are exploited for the purposes of management accounting reporting.

It is utilised for designing, controlling, decision making intention and evaluation of

performance. These reports are constantly prepared through the accounting and auditing period

according to requirements. The results of management accounting is in form of periodic reports

for the entity's department executives and CEO. For example, existing generation of sales

revenue, the existing position or situation of the organisation's accounts payable and accounts

receivables etc. Management reporting looks in the business in a more detailed way and shows

results from various sections. Despite on focusing on the whole organisation, management

reports focuses on a particular job, department or team.

Techniques utilised for management accounting reporting are:

Performance report: It can be termed as a detailed report which estimates outcomes of

particular workings which is related to the growth of organisation at any given point of time.

Management accountants of Rite Track, making best utilisation of budgets for making

comparison between actual expenses with incomes which are reliable on budgeted variables and

them list or updating information on grounds of performance of report. When a report is made,

executives design the demand of its future for customers and the need of a product in market and

in accordance of that modifications in prices are being made (Eaton, Grenier and Layman,

2019).

Cost report: While operating in Rite Track, management accounting analysis a number

of costs of manufacturing goods. On this basis, cost report is prepared in Rite track as it

examines all labour costs, raw material along with any type of additional cost in accordance to

sustain reporting of management accounting. The entire data is then adequately merged with the

cost report. And therefore, the method helps in monitoring and planning profit margins.

Budget report: This particular method plays a vital role in management accounting in

Rite Track for communicating as it focuses on preparation and diverging the budgets with

various departments of organisation. The report of budget emphasis on execution of Rite Track,

firm and is conserved in an entity. Report represents executives the manner to rearrange terms

with suppliers and marketer, better worker incentives and cutting down the cost on goods.

Directors also work for increasing the demand in sales and declining the expenses which leads to

saving of money (Heiling, 2020).

Inventory management report: It is an abstract of unfinished stock and information of

such amount of stock is accessible, products that are sold the most and quickest, category

performance etc. joined to status altogether with presentation of goods. For beneficial

development of Rite Track, it is important for management inventory level in sufficient and

ideally manner as possible. It is capability of purchase manager of the organisation to confirm

that correct stock levels are consistent for producing and marketing of various kinds of goods.

The informatory method that records all types of agreements which are incidental to

modification of inventory to various sections and their end results.

P3 Estimate costs by utilising proper techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost: It can be determined as an amount which can be paid despite of getting product or service.

In accordance with business, cost is estimation of money with sources, risk acquired,

opportunities forgone, materials, consumption of time and utilities in producing with product

delivery or any services. For analysing cost of preparation of income statement, financial

analysts uses various types of techniques and methods.

Absorption Costing: In this technique, managers uses a method for preparing external financial

as well as recording of income tax also. Analysing of techniques incidental to cost acquires all

cost which is associated with production or selling a product (Heinzelmann, 2018).

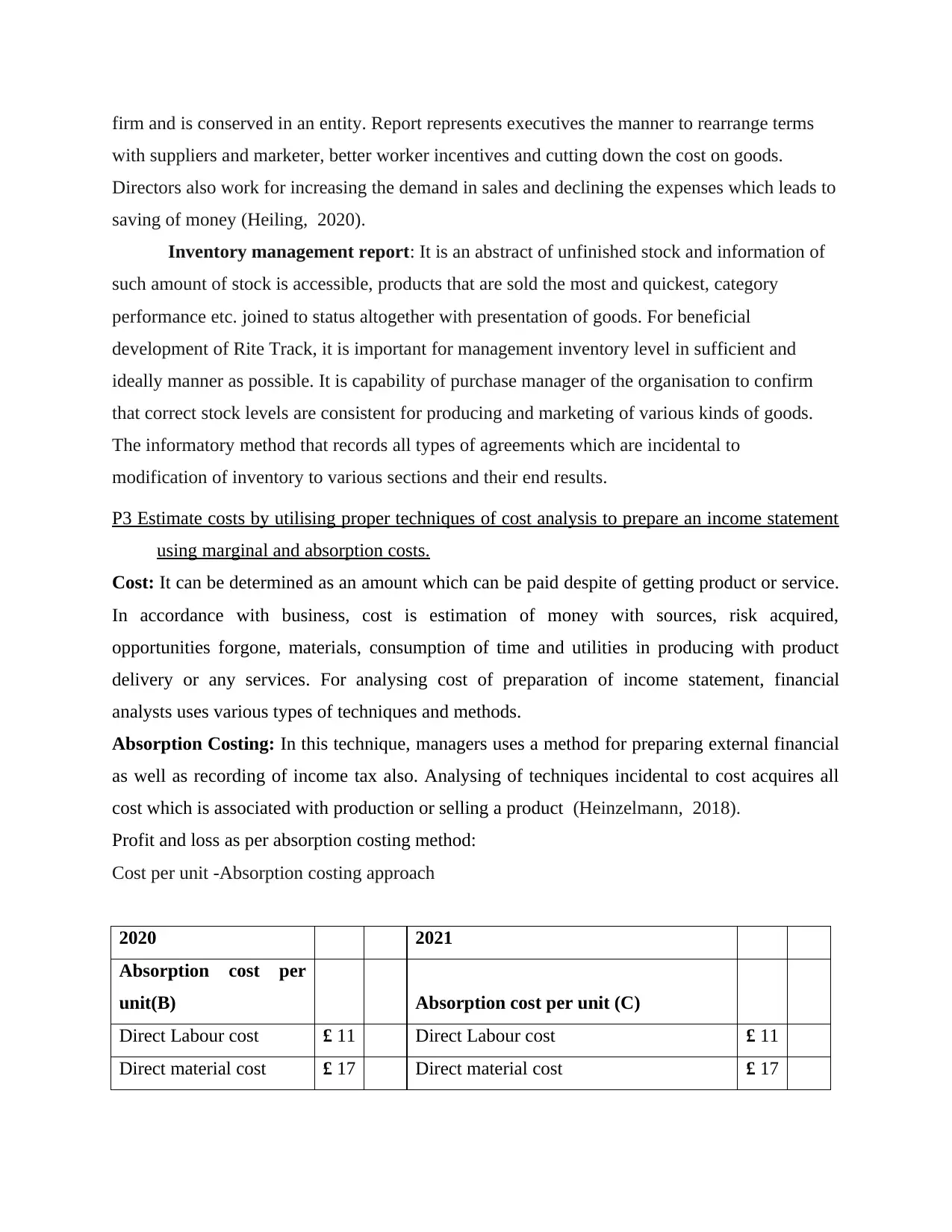

Profit and loss as per absorption costing method:

Cost per unit -Absorption costing approach

2020 2021

Absorption cost per

unit(B) Absorption cost per unit (C)

Direct Labour cost £ 11 Direct Labour cost £ 11

Direct material cost £ 17 Direct material cost £ 17

with suppliers and marketer, better worker incentives and cutting down the cost on goods.

Directors also work for increasing the demand in sales and declining the expenses which leads to

saving of money (Heiling, 2020).

Inventory management report: It is an abstract of unfinished stock and information of

such amount of stock is accessible, products that are sold the most and quickest, category

performance etc. joined to status altogether with presentation of goods. For beneficial

development of Rite Track, it is important for management inventory level in sufficient and

ideally manner as possible. It is capability of purchase manager of the organisation to confirm

that correct stock levels are consistent for producing and marketing of various kinds of goods.

The informatory method that records all types of agreements which are incidental to

modification of inventory to various sections and their end results.

P3 Estimate costs by utilising proper techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost: It can be determined as an amount which can be paid despite of getting product or service.

In accordance with business, cost is estimation of money with sources, risk acquired,

opportunities forgone, materials, consumption of time and utilities in producing with product

delivery or any services. For analysing cost of preparation of income statement, financial

analysts uses various types of techniques and methods.

Absorption Costing: In this technique, managers uses a method for preparing external financial

as well as recording of income tax also. Analysing of techniques incidental to cost acquires all

cost which is associated with production or selling a product (Heinzelmann, 2018).

Profit and loss as per absorption costing method:

Cost per unit -Absorption costing approach

2020 2021

Absorption cost per

unit(B) Absorption cost per unit (C)

Direct Labour cost £ 11 Direct Labour cost £ 11

Direct material cost £ 17 Direct material cost £ 17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

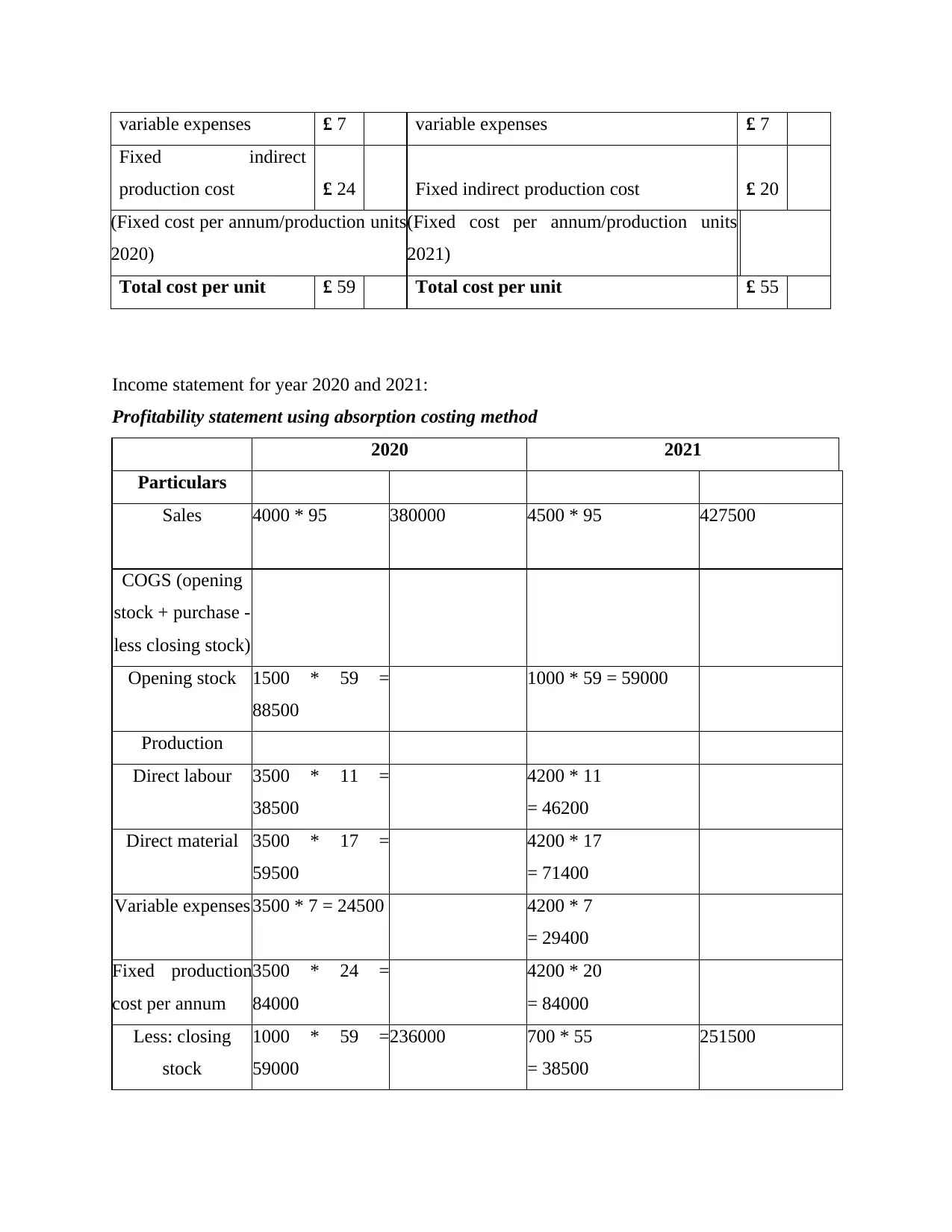

variable expenses £ 7 variable expenses £ 7

Fixed indirect

production cost £ 24 Fixed indirect production cost £ 20

(Fixed cost per annum/production units

2020)

(Fixed cost per annum/production units

2021)

Total cost per unit £ 59 Total cost per unit £ 55

Income statement for year 2020 and 2021:

Profitability statement using absorption costing method

2020 2021

Particulars

Sales 4000 * 95 380000 4500 * 95 427500

COGS (opening

stock + purchase -

less closing stock)

Opening stock 1500 * 59 =

88500

1000 * 59 = 59000

Production

Direct labour 3500 * 11 =

38500

4200 * 11

= 46200

Direct material 3500 * 17 =

59500

4200 * 17

= 71400

Variable expenses 3500 * 7 = 24500 4200 * 7

= 29400

Fixed production

cost per annum

3500 * 24 =

84000

4200 * 20

= 84000

Less: closing

stock

1000 * 59 =

59000

236000 700 * 55

= 38500

251500

Fixed indirect

production cost £ 24 Fixed indirect production cost £ 20

(Fixed cost per annum/production units

2020)

(Fixed cost per annum/production units

2021)

Total cost per unit £ 59 Total cost per unit £ 55

Income statement for year 2020 and 2021:

Profitability statement using absorption costing method

2020 2021

Particulars

Sales 4000 * 95 380000 4500 * 95 427500

COGS (opening

stock + purchase -

less closing stock)

Opening stock 1500 * 59 =

88500

1000 * 59 = 59000

Production

Direct labour 3500 * 11 =

38500

4200 * 11

= 46200

Direct material 3500 * 17 =

59500

4200 * 17

= 71400

Variable expenses 3500 * 7 = 24500 4200 * 7

= 29400

Fixed production

cost per annum

3500 * 24 =

84000

4200 * 20

= 84000

Less: closing

stock

1000 * 59 =

59000

236000 700 * 55

= 38500

251500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

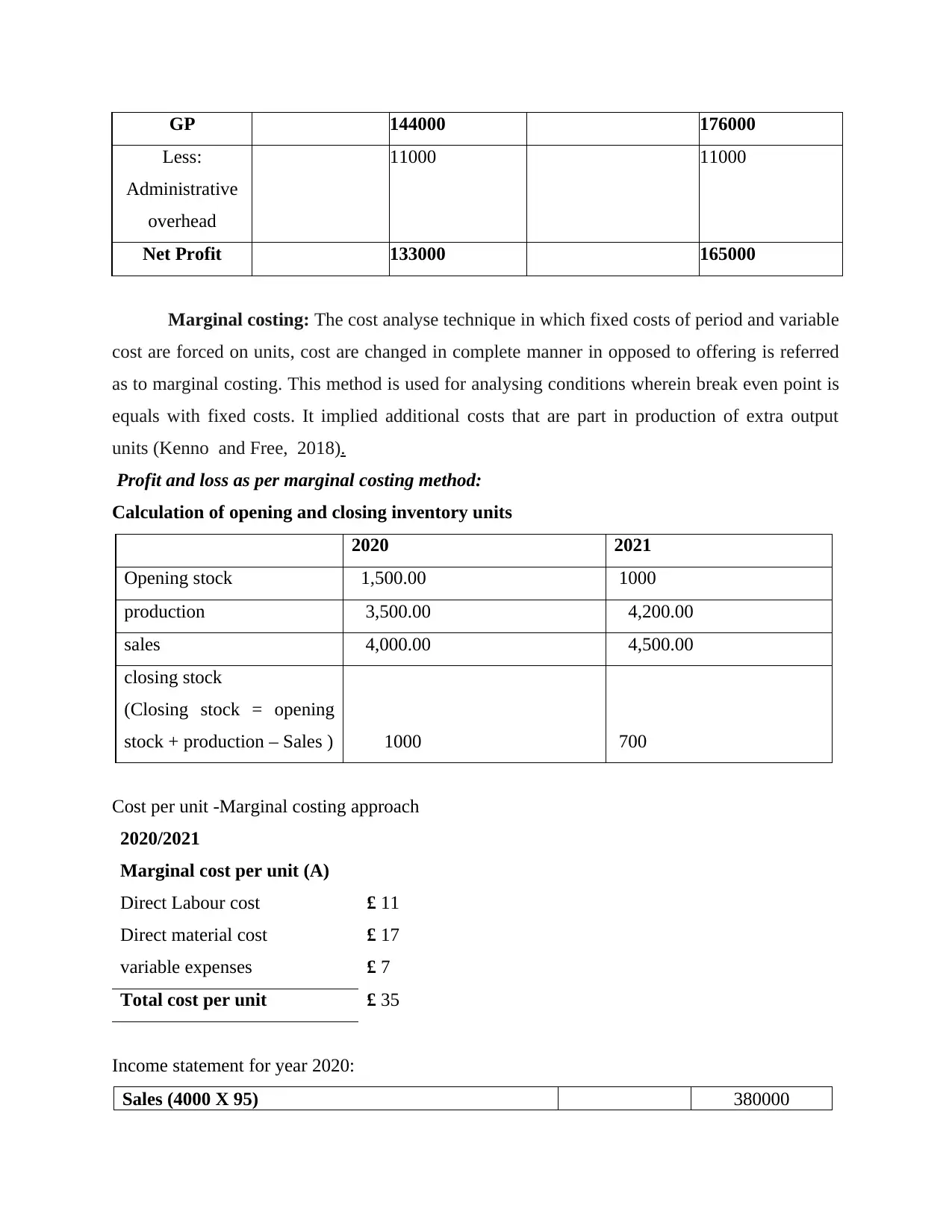

GP 144000 176000

Less:

Administrative

overhead

11000 11000

Net Profit 133000 165000

Marginal costing: The cost analyse technique in which fixed costs of period and variable

cost are forced on units, cost are changed in complete manner in opposed to offering is referred

as to marginal costing. This method is used for analysing conditions wherein break even point is

equals with fixed costs. It implied additional costs that are part in production of extra output

units (Kenno and Free, 2018).

Profit and loss as per marginal costing method:

Calculation of opening and closing inventory units

2020 2021

Opening stock 1,500.00 1000

production 3,500.00 4,200.00

sales 4,000.00 4,500.00

closing stock

(Closing stock = opening

stock + production – Sales ) 1000 700

Cost per unit -Marginal costing approach

2020/2021

Marginal cost per unit (A)

Direct Labour cost £ 11

Direct material cost £ 17

variable expenses £ 7

Total cost per unit £ 35

Income statement for year 2020:

Sales (4000 X 95) 380000

Less:

Administrative

overhead

11000 11000

Net Profit 133000 165000

Marginal costing: The cost analyse technique in which fixed costs of period and variable

cost are forced on units, cost are changed in complete manner in opposed to offering is referred

as to marginal costing. This method is used for analysing conditions wherein break even point is

equals with fixed costs. It implied additional costs that are part in production of extra output

units (Kenno and Free, 2018).

Profit and loss as per marginal costing method:

Calculation of opening and closing inventory units

2020 2021

Opening stock 1,500.00 1000

production 3,500.00 4,200.00

sales 4,000.00 4,500.00

closing stock

(Closing stock = opening

stock + production – Sales ) 1000 700

Cost per unit -Marginal costing approach

2020/2021

Marginal cost per unit (A)

Direct Labour cost £ 11

Direct material cost £ 17

variable expenses £ 7

Total cost per unit £ 35

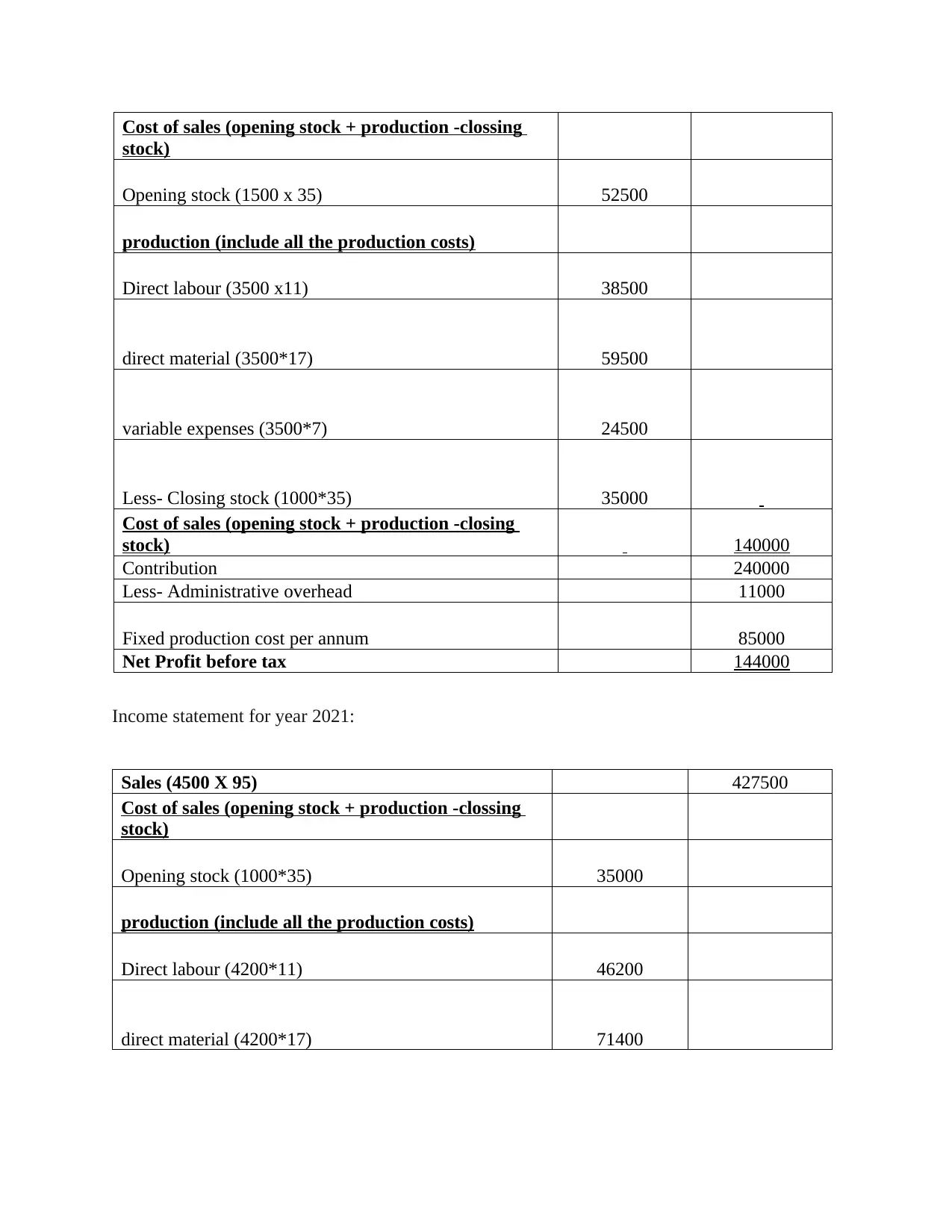

Income statement for year 2020:

Sales (4000 X 95) 380000

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1500 x 35) 52500

production (include all the production costs)

Direct labour (3500 x11) 38500

direct material (3500*17) 59500

variable expenses (3500*7) 24500

Less- Closing stock (1000*35) 35000

Cost of sales (opening stock + production -closing

stock) 140000

Contribution 240000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 144000

Income statement for year 2021:

Sales (4500 X 95) 427500

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1000*35) 35000

production (include all the production costs)

Direct labour (4200*11) 46200

direct material (4200*17) 71400

stock)

Opening stock (1500 x 35) 52500

production (include all the production costs)

Direct labour (3500 x11) 38500

direct material (3500*17) 59500

variable expenses (3500*7) 24500

Less- Closing stock (1000*35) 35000

Cost of sales (opening stock + production -closing

stock) 140000

Contribution 240000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 144000

Income statement for year 2021:

Sales (4500 X 95) 427500

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1000*35) 35000

production (include all the production costs)

Direct labour (4200*11) 46200

direct material (4200*17) 71400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

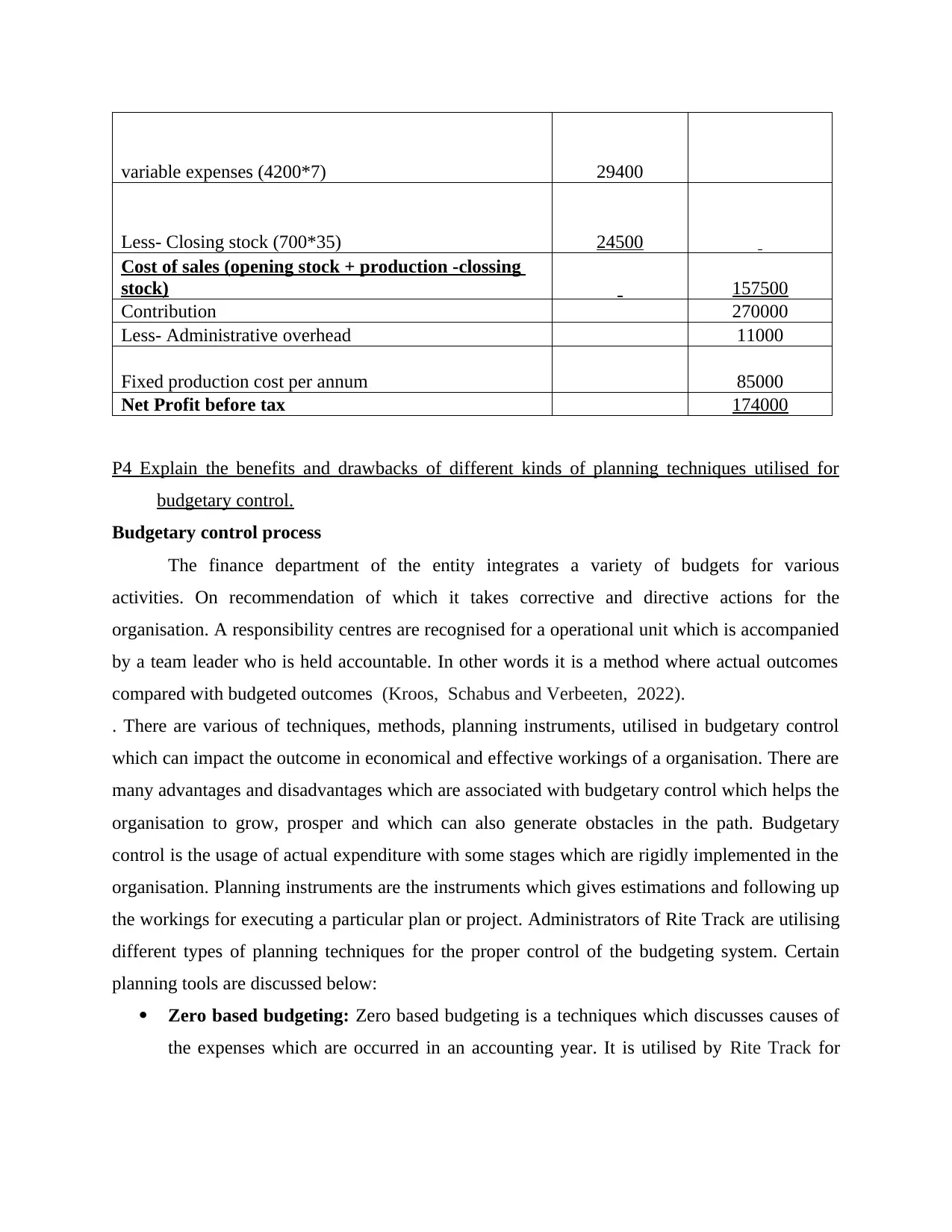

variable expenses (4200*7) 29400

Less- Closing stock (700*35) 24500

Cost of sales (opening stock + production -clossing

stock) 157500

Contribution 270000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 174000

P4 Explain the benefits and drawbacks of different kinds of planning techniques utilised for

budgetary control.

Budgetary control process

The finance department of the entity integrates a variety of budgets for various

activities. On recommendation of which it takes corrective and directive actions for the

organisation. A responsibility centres are recognised for a operational unit which is accompanied

by a team leader who is held accountable. In other words it is a method where actual outcomes

compared with budgeted outcomes (Kroos, Schabus and Verbeeten, 2022).

. There are various of techniques, methods, planning instruments, utilised in budgetary control

which can impact the outcome in economical and effective workings of a organisation. There are

many advantages and disadvantages which are associated with budgetary control which helps the

organisation to grow, prosper and which can also generate obstacles in the path. Budgetary

control is the usage of actual expenditure with some stages which are rigidly implemented in the

organisation. Planning instruments are the instruments which gives estimations and following up

the workings for executing a particular plan or project. Administrators of Rite Track are utilising

different types of planning techniques for the proper control of the budgeting system. Certain

planning tools are discussed below:

Zero based budgeting: Zero based budgeting is a techniques which discusses causes of

the expenses which are occurred in an accounting year. It is utilised by Rite Track for

Less- Closing stock (700*35) 24500

Cost of sales (opening stock + production -clossing

stock) 157500

Contribution 270000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 174000

P4 Explain the benefits and drawbacks of different kinds of planning techniques utilised for

budgetary control.

Budgetary control process

The finance department of the entity integrates a variety of budgets for various

activities. On recommendation of which it takes corrective and directive actions for the

organisation. A responsibility centres are recognised for a operational unit which is accompanied

by a team leader who is held accountable. In other words it is a method where actual outcomes

compared with budgeted outcomes (Kroos, Schabus and Verbeeten, 2022).

. There are various of techniques, methods, planning instruments, utilised in budgetary control

which can impact the outcome in economical and effective workings of a organisation. There are

many advantages and disadvantages which are associated with budgetary control which helps the

organisation to grow, prosper and which can also generate obstacles in the path. Budgetary

control is the usage of actual expenditure with some stages which are rigidly implemented in the

organisation. Planning instruments are the instruments which gives estimations and following up

the workings for executing a particular plan or project. Administrators of Rite Track are utilising

different types of planning techniques for the proper control of the budgeting system. Certain

planning tools are discussed below:

Zero based budgeting: Zero based budgeting is a techniques which discusses causes of

the expenses which are occurred in an accounting year. It is utilised by Rite Track for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

analysing the best possible utilisation of resources allocated at different places. There are

some advantages and disadvantages for Rite Track:

Advantage Disadvantages

This technique helps Rite Track in considering

the fields which assists in generation of profits

and the operational activities in which it is

used. This supply's a better, transparent and

more reliable information for determining the

operations of organisation and examining of

business performance that would helps in

management of the budgets and have a

adequate control over them.

It is considered as a difficult, time consuming

and an costly procedure. It is determined as

difficult project to elaborated the utilisation of

expenses and generation of profit in budgets.

Any deduction in the profit margin or revenue

of the organisation can impact the brand image

of the organisation (Meiryani, Susanto and

Warganegara, 2019).

Operating budget: It can be determined as a budget which is according to all the

operating incomes and activities incidental to expense as well. Executives of Rite Track

this budget for supervising and controlling expense incidental to activities in association

to business. It also helps in prediction of challenges which are related to future

occurrence, expenses and take precautionary course of actions in advance. There are three

major factors of operating budget which can be referred as revenue, variable costs, fixed

costs (O’Dwyer, 2021). There are certain merits and demerits for Rite Track:

Merits Demerits

It can have a advantageous outcome in

Rite Track for estimating costs and

management on expenses of the

business operational activities for

achieving the main objective of

company in the long period of time.

This technique can helps in making the

best available chances to expand

It is not reliable for Rite Track as it do not promotes

any help for evaluating the difference between

standard and actual costs. This technique is not

considered appropriate and is not flexible in nature and

operations. Variations cannot be made in policies

which are made during the year.

some advantages and disadvantages for Rite Track:

Advantage Disadvantages

This technique helps Rite Track in considering

the fields which assists in generation of profits

and the operational activities in which it is

used. This supply's a better, transparent and

more reliable information for determining the

operations of organisation and examining of

business performance that would helps in

management of the budgets and have a

adequate control over them.

It is considered as a difficult, time consuming

and an costly procedure. It is determined as

difficult project to elaborated the utilisation of

expenses and generation of profit in budgets.

Any deduction in the profit margin or revenue

of the organisation can impact the brand image

of the organisation (Meiryani, Susanto and

Warganegara, 2019).

Operating budget: It can be determined as a budget which is according to all the

operating incomes and activities incidental to expense as well. Executives of Rite Track

this budget for supervising and controlling expense incidental to activities in association

to business. It also helps in prediction of challenges which are related to future

occurrence, expenses and take precautionary course of actions in advance. There are three

major factors of operating budget which can be referred as revenue, variable costs, fixed

costs (O’Dwyer, 2021). There are certain merits and demerits for Rite Track:

Merits Demerits

It can have a advantageous outcome in

Rite Track for estimating costs and

management on expenses of the

business operational activities for

achieving the main objective of

company in the long period of time.

This technique can helps in making the

best available chances to expand

It is not reliable for Rite Track as it do not promotes

any help for evaluating the difference between

standard and actual costs. This technique is not

considered appropriate and is not flexible in nature and

operations. Variations cannot be made in policies

which are made during the year.

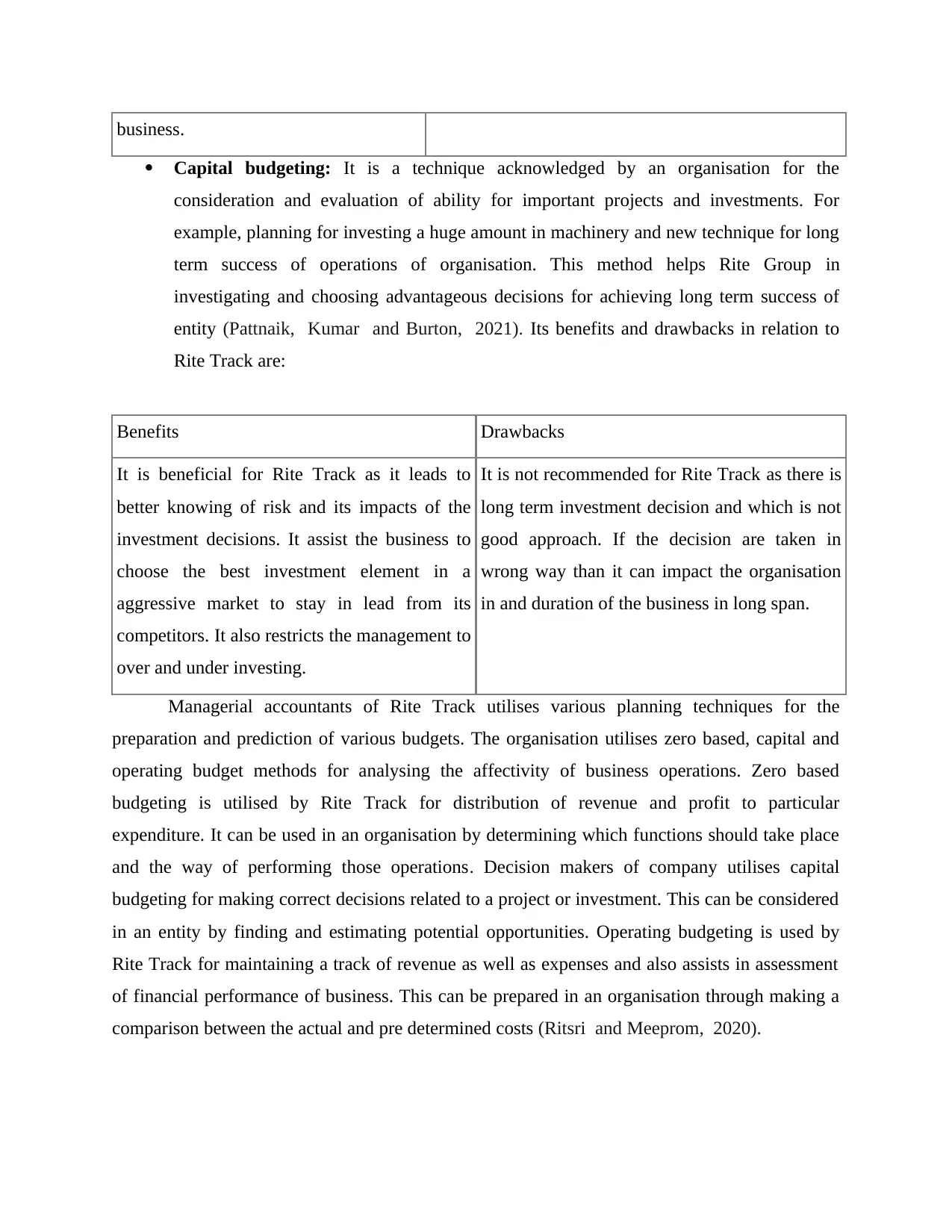

business.

Capital budgeting: It is a technique acknowledged by an organisation for the

consideration and evaluation of ability for important projects and investments. For

example, planning for investing a huge amount in machinery and new technique for long

term success of operations of organisation. This method helps Rite Group in

investigating and choosing advantageous decisions for achieving long term success of

entity (Pattnaik, Kumar and Burton, 2021). Its benefits and drawbacks in relation to

Rite Track are:

Benefits Drawbacks

It is beneficial for Rite Track as it leads to

better knowing of risk and its impacts of the

investment decisions. It assist the business to

choose the best investment element in a

aggressive market to stay in lead from its

competitors. It also restricts the management to

over and under investing.

It is not recommended for Rite Track as there is

long term investment decision and which is not

good approach. If the decision are taken in

wrong way than it can impact the organisation

in and duration of the business in long span.

Managerial accountants of Rite Track utilises various planning techniques for the

preparation and prediction of various budgets. The organisation utilises zero based, capital and

operating budget methods for analysing the affectivity of business operations. Zero based

budgeting is utilised by Rite Track for distribution of revenue and profit to particular

expenditure. It can be used in an organisation by determining which functions should take place

and the way of performing those operations. Decision makers of company utilises capital

budgeting for making correct decisions related to a project or investment. This can be considered

in an entity by finding and estimating potential opportunities. Operating budgeting is used by

Rite Track for maintaining a track of revenue as well as expenses and also assists in assessment

of financial performance of business. This can be prepared in an organisation through making a

comparison between the actual and pre determined costs (Ritsri and Meeprom, 2020).

Capital budgeting: It is a technique acknowledged by an organisation for the

consideration and evaluation of ability for important projects and investments. For

example, planning for investing a huge amount in machinery and new technique for long

term success of operations of organisation. This method helps Rite Group in

investigating and choosing advantageous decisions for achieving long term success of

entity (Pattnaik, Kumar and Burton, 2021). Its benefits and drawbacks in relation to

Rite Track are:

Benefits Drawbacks

It is beneficial for Rite Track as it leads to

better knowing of risk and its impacts of the

investment decisions. It assist the business to

choose the best investment element in a

aggressive market to stay in lead from its

competitors. It also restricts the management to

over and under investing.

It is not recommended for Rite Track as there is

long term investment decision and which is not

good approach. If the decision are taken in

wrong way than it can impact the organisation

in and duration of the business in long span.

Managerial accountants of Rite Track utilises various planning techniques for the

preparation and prediction of various budgets. The organisation utilises zero based, capital and

operating budget methods for analysing the affectivity of business operations. Zero based

budgeting is utilised by Rite Track for distribution of revenue and profit to particular

expenditure. It can be used in an organisation by determining which functions should take place

and the way of performing those operations. Decision makers of company utilises capital

budgeting for making correct decisions related to a project or investment. This can be considered

in an entity by finding and estimating potential opportunities. Operating budgeting is used by

Rite Track for maintaining a track of revenue as well as expenses and also assists in assessment

of financial performance of business. This can be prepared in an organisation through making a

comparison between the actual and pre determined costs (Ritsri and Meeprom, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.