Management Accounting Systems: Techniques, Reporting & Adaptations

VerifiedAdded on 2024/06/04

|22

|4524

|272

Report

AI Summary

This report provides a comprehensive overview of management accounting, emphasizing its crucial role in modern businesses. It explores various management techniques, cost accounting methods, and budgetary control techniques, illustrating their application within the context of Zylla Ltd. The report details the essential requirements for different types of management accounting, including cost management, inventory management, and price optimization systems. Furthermore, it discusses different methods used for management accounting reporting, such as budget reports, performance reports, and cost reports, highlighting their integration in improving planning quality, cost control, performance evaluation, and interdepartmental coordination. The analysis also addresses financial problems encountered by Zylla Ltd and proposes solutions to achieve sustainable success through effective management accounting practices, including variance analysis and other planning tools.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:....................................................................................................................................3

Task 1:.............................................................................................................................................4

P1: Explain management accounting and give the essential requirements for different types of

management accounting..............................................................................................................4

P2: Explain different methods used for management accounting reporting................................9

M2 &D1: apply management techniques and reporting documents. How management

accounting and reporting is integrated processes......................................................................10

Task 2.............................................................................................................................................11

P3: describe marginal and absorption costing:..........................................................................11

M2: apply techniques and produce financial reporting documents...........................................11

D2: interpretation of data:..........................................................................................................13

Task 3:...........................................................................................................................................14

P4: Explain the advantages and disadvantages of different types of planning tools used in the

budgetary control.......................................................................................................................14

M3: You should analyse the use of different planning tools and their application for preparing

and forecasting budgets.............................................................................................................16

Task4:............................................................................................................................................17

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................17

M4 & D3: how responding to financial problems, management accounting can lead

organisations to sustainable success..........................................................................................18

Conclusion:....................................................................................................................................19

References:....................................................................................................................................20

2

Introduction:....................................................................................................................................3

Task 1:.............................................................................................................................................4

P1: Explain management accounting and give the essential requirements for different types of

management accounting..............................................................................................................4

P2: Explain different methods used for management accounting reporting................................9

M2 &D1: apply management techniques and reporting documents. How management

accounting and reporting is integrated processes......................................................................10

Task 2.............................................................................................................................................11

P3: describe marginal and absorption costing:..........................................................................11

M2: apply techniques and produce financial reporting documents...........................................11

D2: interpretation of data:..........................................................................................................13

Task 3:...........................................................................................................................................14

P4: Explain the advantages and disadvantages of different types of planning tools used in the

budgetary control.......................................................................................................................14

M3: You should analyse the use of different planning tools and their application for preparing

and forecasting budgets.............................................................................................................16

Task4:............................................................................................................................................17

P5. Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................17

M4 & D3: how responding to financial problems, management accounting can lead

organisations to sustainable success..........................................................................................18

Conclusion:....................................................................................................................................19

References:....................................................................................................................................20

2

Introduction:

As a key to success, management accounting is playing a crucial role in modern businesses.

Currently, the discussion is based on the features of management accounting to discuss that, “is

management accounting is really beneficial for businesses and if yes how?” In context with the

business of Zylla Ltd, the report includes the explanation about different management

techniques, cost techniques and budgetary control techniques to give an understanding about

these techniques so that the senior management of Zylla Ltd. can adopt these systems to gain

sustainable success for the company. Additionally, some financial problems of Zylla Ltd which

are found during the analysis of company management system and way to remove them are also

going to be discussed in this report so that the financial director of Zylla can make suitable

changes.

3

As a key to success, management accounting is playing a crucial role in modern businesses.

Currently, the discussion is based on the features of management accounting to discuss that, “is

management accounting is really beneficial for businesses and if yes how?” In context with the

business of Zylla Ltd, the report includes the explanation about different management

techniques, cost techniques and budgetary control techniques to give an understanding about

these techniques so that the senior management of Zylla Ltd. can adopt these systems to gain

sustainable success for the company. Additionally, some financial problems of Zylla Ltd which

are found during the analysis of company management system and way to remove them are also

going to be discussed in this report so that the financial director of Zylla can make suitable

changes.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1:

P1: Explain management accounting and give the essential requirements for different types

of management accounting.

As a group of some analysis and reporting techniques, management accounting is a assistance for

the company managers in the decision-making process so that they can understand the internal

situation of company and external situation of the market and take gainful decisions during the

preparation of future strategy (Butterfield, 2016). It can be also defined as a set of rules which

reduces the risk of inappropriate decision-making and supports strategy making process from

start to end as an additional management specialist.

Management accounting is different from financial accounting and key differences are as

follows:

No. Management accounting financial accounting

1. Reports generated under management

accounting does not need to be

published

Financial statements made under financial

accounting are published for the use of

external parties.

2. It is used by only internal management

to understand and managethe business

situation (Wiedemann, 2014).

External and internal both parties use it to

understand the monetary situation of the

company.

4

P1: Explain management accounting and give the essential requirements for different types

of management accounting.

As a group of some analysis and reporting techniques, management accounting is a assistance for

the company managers in the decision-making process so that they can understand the internal

situation of company and external situation of the market and take gainful decisions during the

preparation of future strategy (Butterfield, 2016). It can be also defined as a set of rules which

reduces the risk of inappropriate decision-making and supports strategy making process from

start to end as an additional management specialist.

Management accounting is different from financial accounting and key differences are as

follows:

No. Management accounting financial accounting

1. Reports generated under management

accounting does not need to be

published

Financial statements made under financial

accounting are published for the use of

external parties.

2. It is used by only internal management

to understand and managethe business

situation (Wiedemann, 2014).

External and internal both parties use it to

understand the monetary situation of the

company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting is a continuous process which is run by the management within an

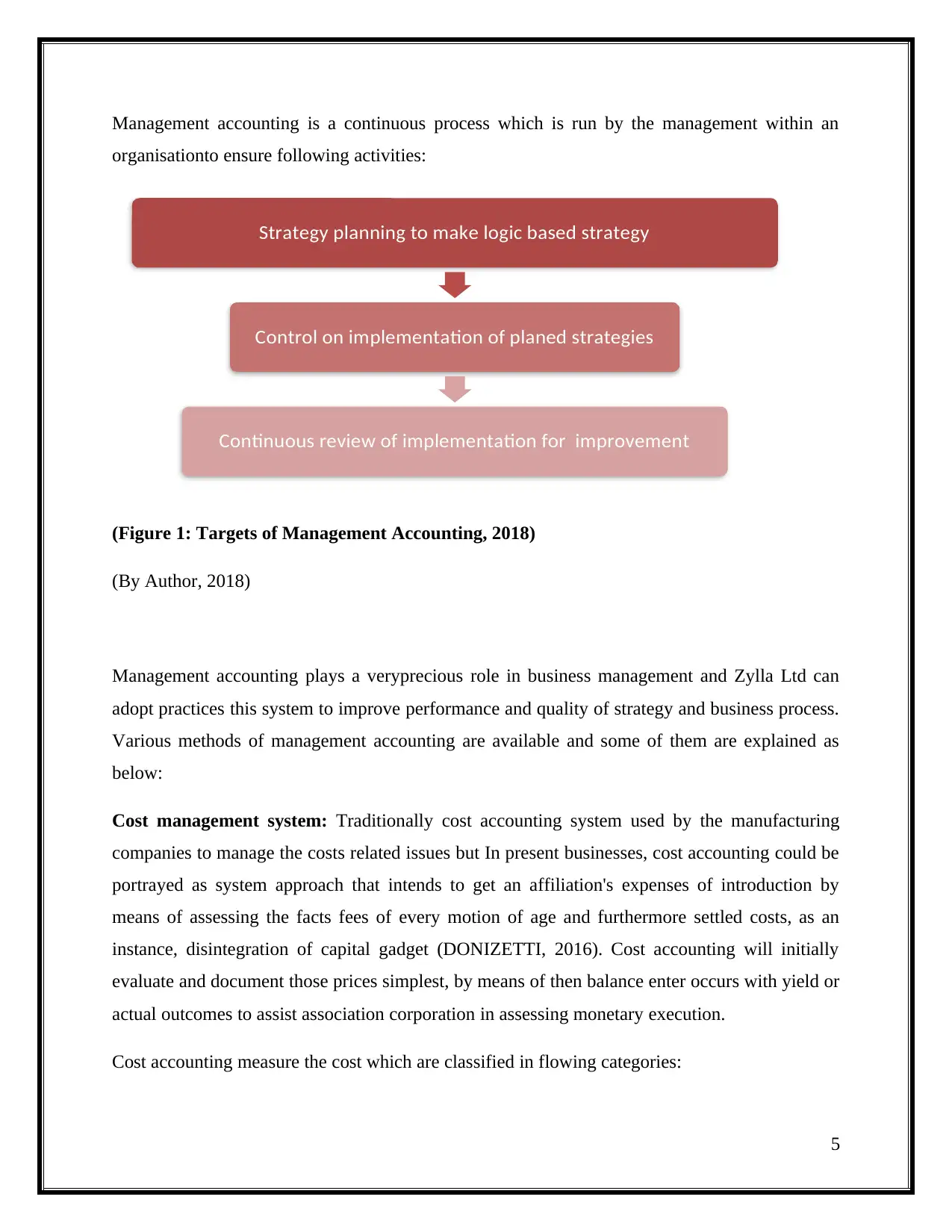

organisationto ensure following activities:

(Figure 1: Targets of Management Accounting, 2018)

(By Author, 2018)

Management accounting plays a veryprecious role in business management and Zylla Ltd can

adopt practices this system to improve performance and quality of strategy and business process.

Various methods of management accounting are available and some of them are explained as

below:

Cost management system: Traditionally cost accounting system used by the manufacturing

companies to manage the costs related issues but In present businesses, cost accounting could be

portrayed as system approach that intends to get an affiliation's expenses of introduction by

means of assessing the facts fees of every motion of age and furthermore settled costs, as an

instance, disintegration of capital gadget (DONIZETTI, 2016). Cost accounting will initially

evaluate and document those prices simplest, by means of then balance enter occurs with yield or

actual outcomes to assist association corporation in assessing monetary execution.

Cost accounting measure the cost which are classified in flowing categories:

5

Strategy planning to make logic based strategy

Control on implementation of planed strategies

Continuous review of implementation for improvement

organisationto ensure following activities:

(Figure 1: Targets of Management Accounting, 2018)

(By Author, 2018)

Management accounting plays a veryprecious role in business management and Zylla Ltd can

adopt practices this system to improve performance and quality of strategy and business process.

Various methods of management accounting are available and some of them are explained as

below:

Cost management system: Traditionally cost accounting system used by the manufacturing

companies to manage the costs related issues but In present businesses, cost accounting could be

portrayed as system approach that intends to get an affiliation's expenses of introduction by

means of assessing the facts fees of every motion of age and furthermore settled costs, as an

instance, disintegration of capital gadget (DONIZETTI, 2016). Cost accounting will initially

evaluate and document those prices simplest, by means of then balance enter occurs with yield or

actual outcomes to assist association corporation in assessing monetary execution.

Cost accounting measure the cost which are classified in flowing categories:

5

Strategy planning to make logic based strategy

Control on implementation of planed strategies

Continuous review of implementation for improvement

(Figure 2: Targets of Management Accounting, 2018)

(By Author, 2018)

Some requirements of this system:

Recording of each cost occurs with appropriate classification because various cost

determination techniques are used in cost accounting (Savić, et. al., 2014).

If a company is engaged in job or batch process, cost data according to each job.

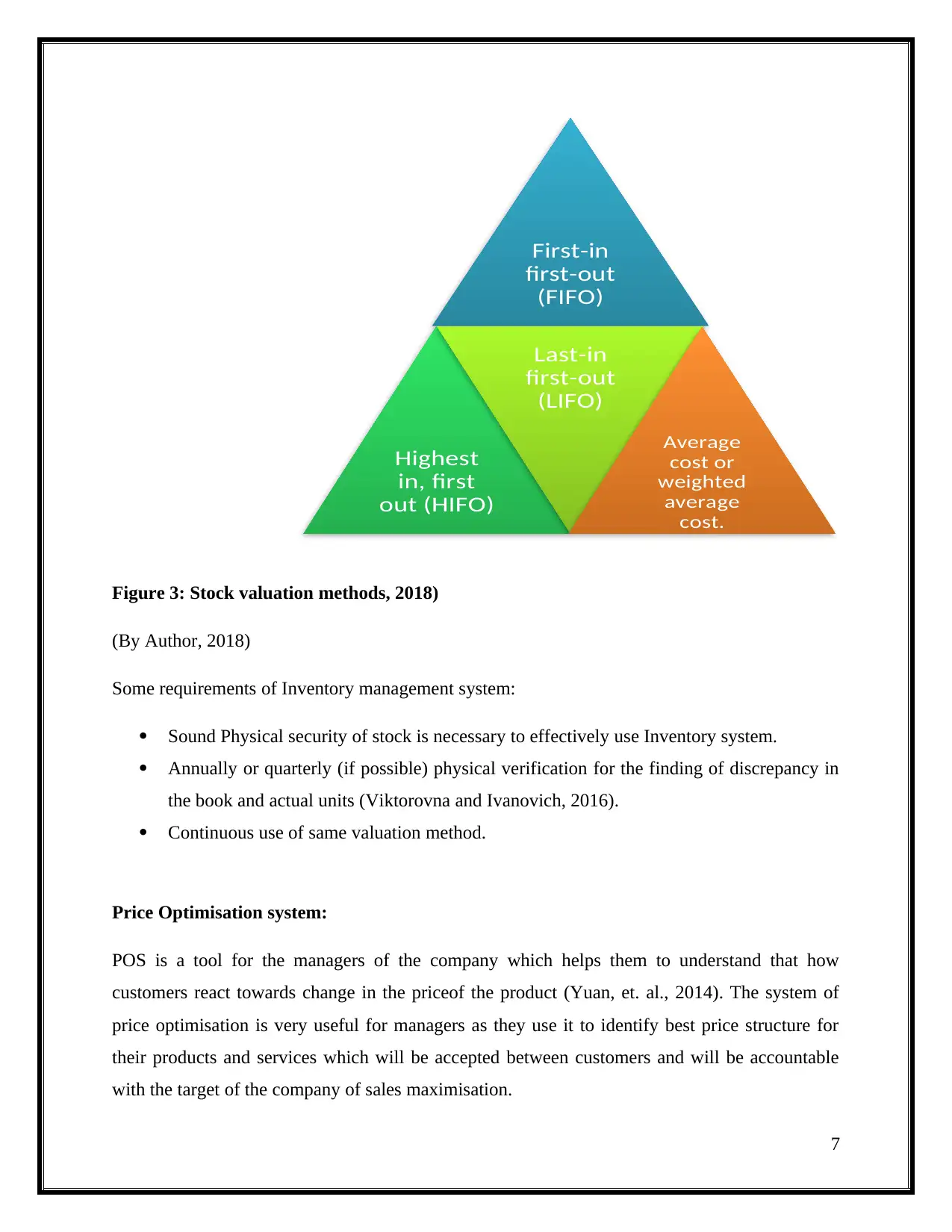

Inventory management system:

A combination of some techniques which is put to use to manage and control the stock items is

known as inventory management system. In modern businesses, inventory management system

can be defined as a mixture of some software, hardware and financial management rules which

are applied within an organisation to maintain the stock items at an appropriate level because it is

necessery to run a business without any interruption (Shen, et. al., 2014). To value the stock

following methods are used under Inventory system:

6

Types of

Costs

Fixed costs

Operating cost

Direct Costs

Variable costs

(By Author, 2018)

Some requirements of this system:

Recording of each cost occurs with appropriate classification because various cost

determination techniques are used in cost accounting (Savić, et. al., 2014).

If a company is engaged in job or batch process, cost data according to each job.

Inventory management system:

A combination of some techniques which is put to use to manage and control the stock items is

known as inventory management system. In modern businesses, inventory management system

can be defined as a mixture of some software, hardware and financial management rules which

are applied within an organisation to maintain the stock items at an appropriate level because it is

necessery to run a business without any interruption (Shen, et. al., 2014). To value the stock

following methods are used under Inventory system:

6

Types of

Costs

Fixed costs

Operating cost

Direct Costs

Variable costs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 3: Stock valuation methods, 2018)

(By Author, 2018)

Some requirements of Inventory management system:

Sound Physical security of stock is necessary to effectively use Inventory system.

Annually or quarterly (if possible) physical verification for the finding of discrepancy in

the book and actual units (Viktorovna and Ivanovich, 2016).

Continuous use of same valuation method.

Price Optimisation system:

POS is a tool for the managers of the company which helps them to understand that how

customers react towards change in the priceof the product (Yuan, et. al., 2014). The system of

price optimisation is very useful for managers as they use it to identify best price structure for

their products and services which will be accepted between customers and will be accountable

with the target of the company of sales maximisation.

7

First-in

first-out

(FIFO)

Highest

in, first

out (HIFO)

Last-in

first-out

(LIFO)

Average

cost or

weighted

average

cost.

(By Author, 2018)

Some requirements of Inventory management system:

Sound Physical security of stock is necessary to effectively use Inventory system.

Annually or quarterly (if possible) physical verification for the finding of discrepancy in

the book and actual units (Viktorovna and Ivanovich, 2016).

Continuous use of same valuation method.

Price Optimisation system:

POS is a tool for the managers of the company which helps them to understand that how

customers react towards change in the priceof the product (Yuan, et. al., 2014). The system of

price optimisation is very useful for managers as they use it to identify best price structure for

their products and services which will be accepted between customers and will be accountable

with the target of the company of sales maximisation.

7

First-in

first-out

(FIFO)

Highest

in, first

out (HIFO)

Last-in

first-out

(LIFO)

Average

cost or

weighted

average

cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Some requirements of POS structure:

Market trend analysis report to understand the situation of market that it is highly

growing, stable or crises (Vives, et. al., 2014).

Study of customer base and product nature to find that is company have any monopoly

related tothe product?

Information about past experiences in the context of sales and prices.

8

Market trend analysis report to understand the situation of market that it is highly

growing, stable or crises (Vives, et. al., 2014).

Study of customer base and product nature to find that is company have any monopoly

related tothe product?

Information about past experiences in the context of sales and prices.

8

P2: Explain different methods used for management accounting reporting

Management reporting works to provide useful information to the business managers to support

them in planning and decision-making process. Zylla Ltd can use it to improve its internal

information flow system. Following reports can be made by Zylla Ltd under management

reporting:

Budget reports:

The budgetreport is one of the most important reports which are made under management

accounting. Historical data of company operation and, estimations according to the market

situation is used to prepare budgets, and all items of revenue and expense are included in it to

make a plan for future activities (Sullivan, 2018).

Performance report:

It is used by the enterprise clerks to examine noticeable utilization and earnings to entirety that

has been allotted. The distinctions are organized and tested to support in selecting new spending

designs. The information in association with those wholes is sorted out with the assistance of

execution reports. These reviews are enrolled every year despite the way that there are

associations that need month to month or quarterly reviews. An official requires similar reports

to empower them to test and select the prospect of the association to the volume augments in

charges and respectively age increases.

Cost Reports:

Cost Reports assist organization clerks to enlist prices of things which are made via ordinary

statistics. Such information joins the price of factors, overheads, paintings and a few specific

expenses (Jokinen, 2017). Cost reports are a kind of organization accounting reports which have

to seem, and used to layout and watching net incomes.

9

Management reporting works to provide useful information to the business managers to support

them in planning and decision-making process. Zylla Ltd can use it to improve its internal

information flow system. Following reports can be made by Zylla Ltd under management

reporting:

Budget reports:

The budgetreport is one of the most important reports which are made under management

accounting. Historical data of company operation and, estimations according to the market

situation is used to prepare budgets, and all items of revenue and expense are included in it to

make a plan for future activities (Sullivan, 2018).

Performance report:

It is used by the enterprise clerks to examine noticeable utilization and earnings to entirety that

has been allotted. The distinctions are organized and tested to support in selecting new spending

designs. The information in association with those wholes is sorted out with the assistance of

execution reports. These reviews are enrolled every year despite the way that there are

associations that need month to month or quarterly reviews. An official requires similar reports

to empower them to test and select the prospect of the association to the volume augments in

charges and respectively age increases.

Cost Reports:

Cost Reports assist organization clerks to enlist prices of things which are made via ordinary

statistics. Such information joins the price of factors, overheads, paintings and a few specific

expenses (Jokinen, 2017). Cost reports are a kind of organization accounting reports which have

to seem, and used to layout and watching net incomes.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2 &D1: apply management techniques and reporting documents. How management

accounting and reporting is integrated processes.

Management techniques have a very important role in modern business which produces a lot of

benefits if it is applied effectively. Zylla Ltd can use gain following benefits from management

system by applying techniques accurately.

Quality of planning: management system and reporting allow the managers to make sound

planning for future business activities by providing useful information. Good planning is must to

manage the business in a gainful manner (Watts, et. al., 2014). In this way, it improves the

quality of planning.

Proficient control on cost: as a main element of finance, cost control is a very important matter

for every business. Management accounting has different techniques gives depth knowledge

about the occurring structure of costs and manager of Zylla can apply this to ensure proficient

control of costs and expenses.

Performance evaluation: Management accounting and reporting involve complete information

about the efficiency of staff. Managers of Zylla Ltd can use these reports to evaluate the

proficiency of labour so that they can take action on performance below standards.

Coordination between different units: Management accounting generates a two-way

communication which enables the managers of different departments to share their data with

each other so that business can be managed effectively (Lopez-Valeiras, et. al., 2014). For

example, by studying sales report, production manager can understand the sales structure and can

manage production accordingly.

10

accounting and reporting is integrated processes.

Management techniques have a very important role in modern business which produces a lot of

benefits if it is applied effectively. Zylla Ltd can use gain following benefits from management

system by applying techniques accurately.

Quality of planning: management system and reporting allow the managers to make sound

planning for future business activities by providing useful information. Good planning is must to

manage the business in a gainful manner (Watts, et. al., 2014). In this way, it improves the

quality of planning.

Proficient control on cost: as a main element of finance, cost control is a very important matter

for every business. Management accounting has different techniques gives depth knowledge

about the occurring structure of costs and manager of Zylla can apply this to ensure proficient

control of costs and expenses.

Performance evaluation: Management accounting and reporting involve complete information

about the efficiency of staff. Managers of Zylla Ltd can use these reports to evaluate the

proficiency of labour so that they can take action on performance below standards.

Coordination between different units: Management accounting generates a two-way

communication which enables the managers of different departments to share their data with

each other so that business can be managed effectively (Lopez-Valeiras, et. al., 2014). For

example, by studying sales report, production manager can understand the sales structure and can

manage production accordingly.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 2

P3: describe marginal and absorption costing:

Marginal costing:

A system of cost measuring which is applied to find the cost of the product by including only

variable cost as the primary cost is known as marginal costing system. In this system, the only

variable cost is included in the cost of the product and fixed cost occurs are charged over the

complete period. For example, cost of direct material, labour and overhead (variable) are charged

as cost of the product and fixed overhead costs are charged as a period cost (Aurora, 2013).

Absorption costing: also it is a cost measuring method but with different assumptions.

Absorption costing involves all fixed and variable expenses as the primary cost of the product. It

means that fixed overhead costs along with variable costs are charged at the cost of the product.

Marginal costing Absorption costing

Only variable cost as product cost Variable and fixed both costs as product cost

Not acceptable as per GAAP Acceptable as per GAAP rules

Useful in budgetary control It shows the impact of Fixed cost.

M2: apply techniques and produce financial reporting documents.

Particulars ₤ amount

Material cost per unit 10

Labour cost per unit 5

variable overhead 10

fixed overhead 15

Fixed production overhead incurred 20000

Selling and administration (Fixed) 18000

Budgeted production (units) 20000

Actual production (units) 5000

Selling price ₤ 50

11

P3: describe marginal and absorption costing:

Marginal costing:

A system of cost measuring which is applied to find the cost of the product by including only

variable cost as the primary cost is known as marginal costing system. In this system, the only

variable cost is included in the cost of the product and fixed cost occurs are charged over the

complete period. For example, cost of direct material, labour and overhead (variable) are charged

as cost of the product and fixed overhead costs are charged as a period cost (Aurora, 2013).

Absorption costing: also it is a cost measuring method but with different assumptions.

Absorption costing involves all fixed and variable expenses as the primary cost of the product. It

means that fixed overhead costs along with variable costs are charged at the cost of the product.

Marginal costing Absorption costing

Only variable cost as product cost Variable and fixed both costs as product cost

Not acceptable as per GAAP Acceptable as per GAAP rules

Useful in budgetary control It shows the impact of Fixed cost.

M2: apply techniques and produce financial reporting documents.

Particulars ₤ amount

Material cost per unit 10

Labour cost per unit 5

variable overhead 10

fixed overhead 15

Fixed production overhead incurred 20000

Selling and administration (Fixed) 18000

Budgeted production (units) 20000

Actual production (units) 5000

Selling price ₤ 50

11

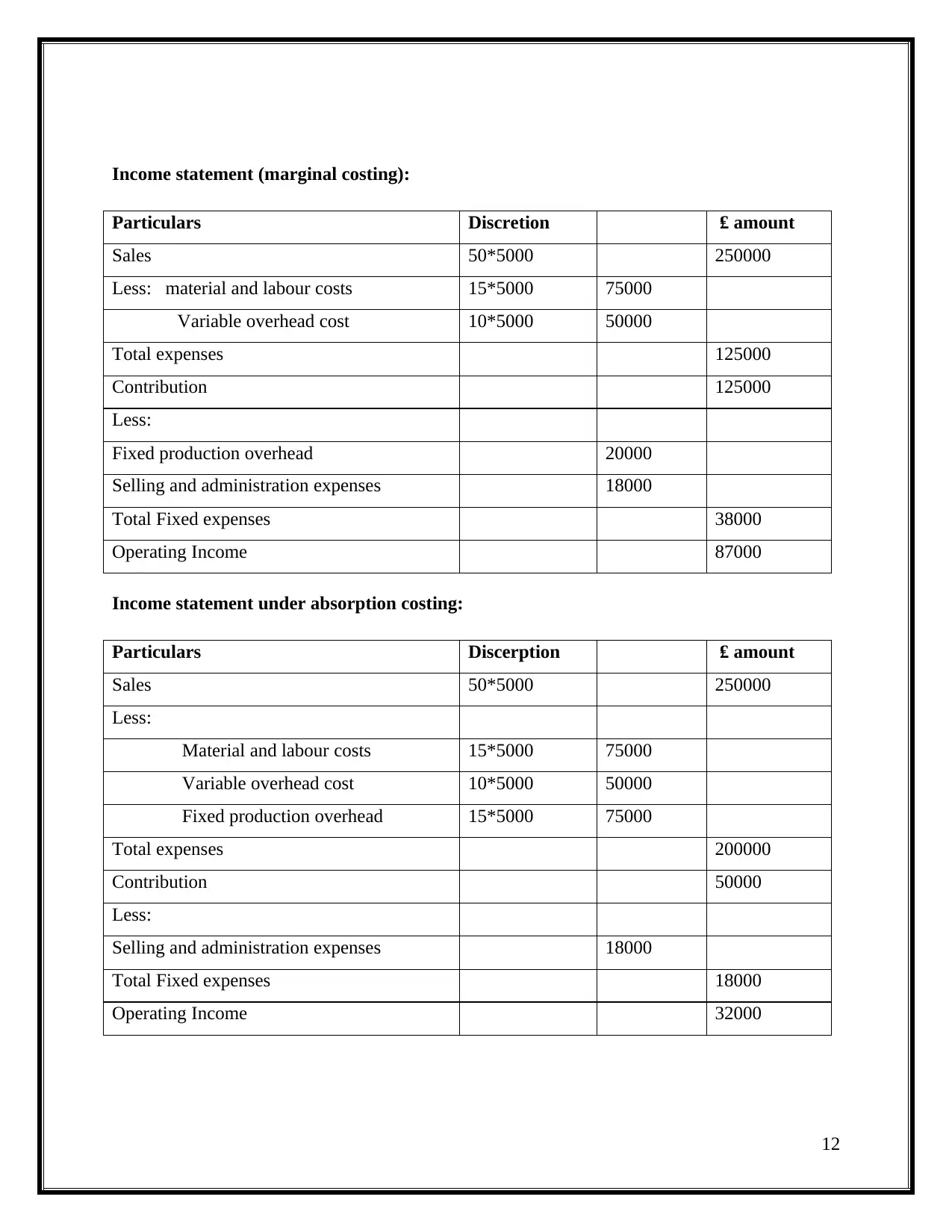

Income statement (marginal costing):

Particulars Discretion ₤ amount

Sales 50*5000 250000

Less: material and labour costs 15*5000 75000

Variable overhead cost 10*5000 50000

Total expenses 125000

Contribution 125000

Less:

Fixed production overhead 20000

Selling and administration expenses 18000

Total Fixed expenses 38000

Operating Income 87000

Income statement under absorption costing:

Particulars Discerption ₤ amount

Sales 50*5000 250000

Less:

Material and labour costs 15*5000 75000

Variable overhead cost 10*5000 50000

Fixed production overhead 15*5000 75000

Total expenses 200000

Contribution 50000

Less:

Selling and administration expenses 18000

Total Fixed expenses 18000

Operating Income 32000

12

Particulars Discretion ₤ amount

Sales 50*5000 250000

Less: material and labour costs 15*5000 75000

Variable overhead cost 10*5000 50000

Total expenses 125000

Contribution 125000

Less:

Fixed production overhead 20000

Selling and administration expenses 18000

Total Fixed expenses 38000

Operating Income 87000

Income statement under absorption costing:

Particulars Discerption ₤ amount

Sales 50*5000 250000

Less:

Material and labour costs 15*5000 75000

Variable overhead cost 10*5000 50000

Fixed production overhead 15*5000 75000

Total expenses 200000

Contribution 50000

Less:

Selling and administration expenses 18000

Total Fixed expenses 18000

Operating Income 32000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.