Analysis of Management Accounting Systems and Application for KEF

VerifiedAdded on 2020/12/09

|16

|4236

|451

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and their practical applications within KEF Ltd. It begins by defining management accounting and highlighting the significance of various systems, including inventory management, job costing, price optimization, and cost accounting. The report then delves into different management accounting reporting methods, such as budget reports, account receivable reports, job cost reports, and inventory and manufacturing reports. An evaluation of the advantages and disadvantages of these systems is presented, along with their specific applications within KEF Ltd. The report further explores the integration of management accounting reporting and systems, providing insights into how these elements work together to support decision-making and financial management. The report also includes calculations using absorption and marginal costing methods, and discusses the benefits and drawbacks of various planning tools under budgetary control, analyzing their usage in KEF's budget preparation and forecasting. Finally, the report examines how KEF can leverage management accounting to address financial problems and achieve sustainable growth, using planning tools to resolve financial issues and move towards long-term financial stability.

Management accounting

System and its application

System and its application

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Explaining the concept of management accounting and the significance of various systems....1

Presenting various methods of management accounting reporting............................................2

Evaluation of the advantages and disadvantage of the management accounting systems and

their application in KEF..............................................................................................................3

Integration of the management accounting reporting and management accounting systems...5

TASK 2............................................................................................................................................5

Calculations under Absorption costing and marginal costing ....................................................5

TASK 3............................................................................................................................................7

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Explaining the concept of management accounting and the significance of various systems....1

Presenting various methods of management accounting reporting............................................2

Evaluation of the advantages and disadvantage of the management accounting systems and

their application in KEF..............................................................................................................3

Integration of the management accounting reporting and management accounting systems...5

TASK 2............................................................................................................................................5

Calculations under Absorption costing and marginal costing ....................................................5

TASK 3............................................................................................................................................7

Presenting benefits and drawbacks of various types of planning tools under budgetary control

.....................................................................................................................................................7

Analysing the usage and application of planning tools by KEF in preparation and forecasting

of budgets....................................................................................................................................8

TASK 4............................................................................................................................................9

Comparing the adopting management accounting system for responding to financial problem

by KEF .......................................................................................................................................9

Presenting the fact that dealing with financial problem through management accounting

system leads KEF to sustainable growth...................................................................................10

Use of planning tools for resolving financial issues and heading towards sustainable growth 10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

.....................................................................................................................................................7

Analysing the usage and application of planning tools by KEF in preparation and forecasting

of budgets....................................................................................................................................8

TASK 4............................................................................................................................................9

Comparing the adopting management accounting system for responding to financial problem

by KEF .......................................................................................................................................9

Presenting the fact that dealing with financial problem through management accounting

system leads KEF to sustainable growth...................................................................................10

Use of planning tools for resolving financial issues and heading towards sustainable growth 10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a provision of financial and statistical data of an organisation

which is used by the business in decision making process and development of the company.

This scope of management accounting revolve around the management decision making,

devising planning and performance management systems along with providing expertise in

financial reporting. In the present report different sections under management accounting are

discussed. This includes presenting management amounting systems, their advantages with

presenting different methods of accounting reporting to KDF Ltd. For the new product launching

calculation are presented by using absorption as well as marginal method of costing. The

application of various planning tool in the management accounting is done explaining their use.

In the lase section of the report the ways in which KEF can use the management accounting in

for responding to financial problem of the business are presented.

TASK 1

Explaining the concept of management accounting and the significance of various systems

Management accounting is the application of the professional knowledge and the skill in

preparing accounting information in a manner that enables the management of the KEF Ltd in

formulating its policies and strategies. It also helps in effective planning and the controlling of

operations within an organization. In management accounting, both financial and the non

financial information is been presented in a regular interval of time such as weekly reports,

monthly etc. It includes the forecast, in-depth analysis and the budgets. Management accounting

ensure preparation of various charts for the performance and the forecast analysis which in turn

helps the managers of the company in making the best possible decisions (Novas, Alves, C. G.

and Sousa, 2017). Management accounting is not been regulated by law so at the time of making

the analysis no standards had to be followed as like in financial accounting. In other words

management accounting refers to the process for framing the management reports and the

accounts which facilitates accurate statistical and financial information which in turn helps

managers in making long and short term decisions.

There are various systems of the management accounting that are important for the company to

adopt as follows-

1

Management accounting is a provision of financial and statistical data of an organisation

which is used by the business in decision making process and development of the company.

This scope of management accounting revolve around the management decision making,

devising planning and performance management systems along with providing expertise in

financial reporting. In the present report different sections under management accounting are

discussed. This includes presenting management amounting systems, their advantages with

presenting different methods of accounting reporting to KDF Ltd. For the new product launching

calculation are presented by using absorption as well as marginal method of costing. The

application of various planning tool in the management accounting is done explaining their use.

In the lase section of the report the ways in which KEF can use the management accounting in

for responding to financial problem of the business are presented.

TASK 1

Explaining the concept of management accounting and the significance of various systems

Management accounting is the application of the professional knowledge and the skill in

preparing accounting information in a manner that enables the management of the KEF Ltd in

formulating its policies and strategies. It also helps in effective planning and the controlling of

operations within an organization. In management accounting, both financial and the non

financial information is been presented in a regular interval of time such as weekly reports,

monthly etc. It includes the forecast, in-depth analysis and the budgets. Management accounting

ensure preparation of various charts for the performance and the forecast analysis which in turn

helps the managers of the company in making the best possible decisions (Novas, Alves, C. G.

and Sousa, 2017). Management accounting is not been regulated by law so at the time of making

the analysis no standards had to be followed as like in financial accounting. In other words

management accounting refers to the process for framing the management reports and the

accounts which facilitates accurate statistical and financial information which in turn helps

managers in making long and short term decisions.

There are various systems of the management accounting that are important for the company to

adopt as follows-

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system- It refers to the management of the current assets which

relates in maintaining the optimum level of the inventory and ensuring effective control in order

to minimize the cost of the total inventory. It is the system which plays a vital role in the KEF

Ltd as it helps in maintaining the adequate inventory so that smooth functioning of the

production and the selling activities can be attained. It enables the firm in minimizing the

investments in its inventory so that higher profitability can be gained (Hoozée and Mitchell,

2018). As the company deals in the manufacturing activity, this system helps in avoiding the

problem of the stock out and also helps in producing the proper level of inventory.

Job costing system- It is the method of recording cost that involved in the manufacturing

activity of the firm. Through the job costing system, managers can keep the track record

regarding the cost incurred in each job and maintains the data which is essential or relevant for

the operations of business. The information provided by this system is essential as to determine

the accuracy in the estimating system of the enterprise and also in assigning the correct cost in

manufacturing the goods.

Price optimization system- It is the method that defines the preferred set of the prices in

relation to the products offered. KEF Ltd by using this can create sales model and the cost model

that helps it in knowing the true demand for the product (Chenhall and Moers, 2015). This in

turn assist the firm in evaluating the cost spending and the sales target that need to be met for

gaining higher margins.

Cost accounting system- It is the system of management accounting that accumulates and

assigns the cost to each activity within the organization. Cost accounting system helps in

improving the allocation and the planning of the resources as to attain efficiency in the cost.

Presenting various methods of management accounting reporting

Under the management accounting a major section is related with preparation and presentation

of the reports for various activities and task undertake by the company. These reports are crucial

parts of the business organisation KEF to make sure that a complete picture how the business is

operating (Shields, 2015). There are various reports that are produced in KEF for protecting the

business, and managerial accounting reports assist the management of the KEF to analyses the

business performance in context of different activities and jobs undertaken by the company.

The several kinds of managerial accounting reports that are prepared by KEF includes:

Budget reports:

2

relates in maintaining the optimum level of the inventory and ensuring effective control in order

to minimize the cost of the total inventory. It is the system which plays a vital role in the KEF

Ltd as it helps in maintaining the adequate inventory so that smooth functioning of the

production and the selling activities can be attained. It enables the firm in minimizing the

investments in its inventory so that higher profitability can be gained (Hoozée and Mitchell,

2018). As the company deals in the manufacturing activity, this system helps in avoiding the

problem of the stock out and also helps in producing the proper level of inventory.

Job costing system- It is the method of recording cost that involved in the manufacturing

activity of the firm. Through the job costing system, managers can keep the track record

regarding the cost incurred in each job and maintains the data which is essential or relevant for

the operations of business. The information provided by this system is essential as to determine

the accuracy in the estimating system of the enterprise and also in assigning the correct cost in

manufacturing the goods.

Price optimization system- It is the method that defines the preferred set of the prices in

relation to the products offered. KEF Ltd by using this can create sales model and the cost model

that helps it in knowing the true demand for the product (Chenhall and Moers, 2015). This in

turn assist the firm in evaluating the cost spending and the sales target that need to be met for

gaining higher margins.

Cost accounting system- It is the system of management accounting that accumulates and

assigns the cost to each activity within the organization. Cost accounting system helps in

improving the allocation and the planning of the resources as to attain efficiency in the cost.

Presenting various methods of management accounting reporting

Under the management accounting a major section is related with preparation and presentation

of the reports for various activities and task undertake by the company. These reports are crucial

parts of the business organisation KEF to make sure that a complete picture how the business is

operating (Shields, 2015). There are various reports that are produced in KEF for protecting the

business, and managerial accounting reports assist the management of the KEF to analyses the

business performance in context of different activities and jobs undertaken by the company.

The several kinds of managerial accounting reports that are prepared by KEF includes:

Budget reports:

2

The budget reports are the fundamental report under management accounting which

assist the owners and managers of KEF in understanding the cost which is spread through out

entity (Ax and Greve, 2017). The cost identification is regarding each of the department and for

every job of KEF. The company evaluates the expenses of the previous years and then makes

the estimated budgets for the following years and find out the places of cost cutting.

Account receivable reports:

This report is prepared by KEF for determining the extent of credits given to the

consumers and how much is still due to be received (Bromwich and Scapens, 2016). This report

provide an overview of the credit balances as per the level of business and amount of due to be

received. This assist the management of KEF to adjust the credit policies to make them align

with the repayment capabilities of the consumers.

Job cost reports:

The Job cost report is prepared by KEF to determine the expenses and cost incurred on

each of the job undertaken by the business. This present a side by side view of the total cost

accrued on a single job as compared to the expected revenues yielded by that job (Hopper and

Bui, 2016). This reports aid the management of KEF to evaluate the contribution made by each

particular activity in the profits of the company. The reports lead the management to evaluate the

profitably of each specific job or activity and optimise their operation by putting focus on those

job which are more profitable.

Inventory and manufacturing report:

KEF produces a physical products and is indulged in manufacturing activities

primarily. This type of organisation have a low tolerance regarding any fault in the inventory as

this can lead to major losses and fall back in the productions (.Messner, 2016). For this the

inventory and manufacturing reports are of high value. This also assist in centralising the data

related with inventory cost, labour and other overhead which are incurred in the production

process with presenting a raw data for optimizing the cost.

Evaluation of the advantages and disadvantage of the management accounting systems and their

application in KEF

Inventory management system:

The advantage of the inventory management system is that is tracks the supplies and

present the information related with inquiry , work orders inputs and outputs, bills and others to

3

assist the owners and managers of KEF in understanding the cost which is spread through out

entity (Ax and Greve, 2017). The cost identification is regarding each of the department and for

every job of KEF. The company evaluates the expenses of the previous years and then makes

the estimated budgets for the following years and find out the places of cost cutting.

Account receivable reports:

This report is prepared by KEF for determining the extent of credits given to the

consumers and how much is still due to be received (Bromwich and Scapens, 2016). This report

provide an overview of the credit balances as per the level of business and amount of due to be

received. This assist the management of KEF to adjust the credit policies to make them align

with the repayment capabilities of the consumers.

Job cost reports:

The Job cost report is prepared by KEF to determine the expenses and cost incurred on

each of the job undertaken by the business. This present a side by side view of the total cost

accrued on a single job as compared to the expected revenues yielded by that job (Hopper and

Bui, 2016). This reports aid the management of KEF to evaluate the contribution made by each

particular activity in the profits of the company. The reports lead the management to evaluate the

profitably of each specific job or activity and optimise their operation by putting focus on those

job which are more profitable.

Inventory and manufacturing report:

KEF produces a physical products and is indulged in manufacturing activities

primarily. This type of organisation have a low tolerance regarding any fault in the inventory as

this can lead to major losses and fall back in the productions (.Messner, 2016). For this the

inventory and manufacturing reports are of high value. This also assist in centralising the data

related with inventory cost, labour and other overhead which are incurred in the production

process with presenting a raw data for optimizing the cost.

Evaluation of the advantages and disadvantage of the management accounting systems and their

application in KEF

Inventory management system:

The advantage of the inventory management system is that is tracks the supplies and

present the information related with inquiry , work orders inputs and outputs, bills and others to

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management of KEF. This system directly assist the business is controlling the cost by cutting

down the extra cost by not stuffing up the storage space with unnecessary supplies. It also

enhance the efficiency in operating performance leading to higher productivity (Quattrone,

2016). The disadvantage associated with this system is that the this system requires specific

software which are high in cost and being a medium size enterprise the cost is high for KEF.

Also this system in time consuming and requires a skilled person to operate the system. The

application of inventory management system can be be seen in KEF as keeping the record of all

the units manufactures. This includes maintaining records of opening and closing stock, along

with production and sales units.

Job costing system:

The benefit of job costing system is that costs are ascertained at any stage of completion

of a job. This gives scope for control of costs by taking suitable steps to KEF. The profits earned

from each job is known separately (Maas, Schaltegger and Crutzen, 2016). The actual costs of

previous job can be compared with present job executed. Drawbacks related with this system is

that there is no standardization of this system and more clerical work is required to maintain the

detailed information. Also this is expensive for KEF.

The application of this system in KEF is that for a each of job related with the

productions of goods in KEF separate details are maintained with keeping a track of expenses

incurred, unit manufactured and issued to sales.

Price optimisation system:

The pros related with price optimisation system for KEF are that with optimizing the

prices the organisation can significantly reduce the internal manual resources devoted to price

setting. It is that strategy where KEF arrive to a decision on how much business they can obtain

within defined profitability levels after understanding how sensitive their existing clients are to

changes in product prices (Otley, 2016). The cons of this system for KEF is that there is huge

possibility that the demands and trends can be identified not to the optimal level which can lead

to set the wrong prices. It is time consuming and required indulgence of more human resources

of KEF.

The application of this system in KEF can be seen through as determining the actual

prices of each of the product manufactured in KEF which is desirable to consumer to pay. The

4

down the extra cost by not stuffing up the storage space with unnecessary supplies. It also

enhance the efficiency in operating performance leading to higher productivity (Quattrone,

2016). The disadvantage associated with this system is that the this system requires specific

software which are high in cost and being a medium size enterprise the cost is high for KEF.

Also this system in time consuming and requires a skilled person to operate the system. The

application of inventory management system can be be seen in KEF as keeping the record of all

the units manufactures. This includes maintaining records of opening and closing stock, along

with production and sales units.

Job costing system:

The benefit of job costing system is that costs are ascertained at any stage of completion

of a job. This gives scope for control of costs by taking suitable steps to KEF. The profits earned

from each job is known separately (Maas, Schaltegger and Crutzen, 2016). The actual costs of

previous job can be compared with present job executed. Drawbacks related with this system is

that there is no standardization of this system and more clerical work is required to maintain the

detailed information. Also this is expensive for KEF.

The application of this system in KEF is that for a each of job related with the

productions of goods in KEF separate details are maintained with keeping a track of expenses

incurred, unit manufactured and issued to sales.

Price optimisation system:

The pros related with price optimisation system for KEF are that with optimizing the

prices the organisation can significantly reduce the internal manual resources devoted to price

setting. It is that strategy where KEF arrive to a decision on how much business they can obtain

within defined profitability levels after understanding how sensitive their existing clients are to

changes in product prices (Otley, 2016). The cons of this system for KEF is that there is huge

possibility that the demands and trends can be identified not to the optimal level which can lead

to set the wrong prices. It is time consuming and required indulgence of more human resources

of KEF.

The application of this system in KEF can be seen through as determining the actual

prices of each of the product manufactured in KEF which is desirable to consumer to pay. The

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

price is set such which is affordable to consumers and also gives profits to the company while

considering trends and demand of customer.

Cost accounting system:

The advantages of the cost accounting system can be outlined as the the cost pertaining

to each job can be easily identified. This gives a opportunity to management of KEF to conduct

a comparison of the current cost with the past records to establish a controlling measure for cost

control (Kaplan and Atkinson, 2015). The disadvantages of this system is that it is time

consuming as to determine the cost for each activity is cumbersome as there are lots of processes

for production of a single units only. A wrong detection of the cost can lead to misallocation of

the resources and can hamper the performance efficiency.

The application of this system in KEF can be stated as cost related with each activity of

manufacturing of different product is determined. This is done by identifying the expenses done

both direct and indirect and then sales prices is decided after adding the profit margin required by

KEF.

Integration of the management accounting reporting and management accounting systems

The management accounting system are related with presenting a full system to manage

the activity of the business rather the reports under management accounting are prepared to

detect the performance of the business and its related activities (Key Advantages &

Disadvantages of Using a Static Budget, 2019). The integration can be seen as both falls under

the scope of management accounting one is related with stating system to conduct the operation

of the business of KEF and the other is related with detecting and evaluation of the performance

and each setting the goals fro each of the activity of the business.

TASK 2

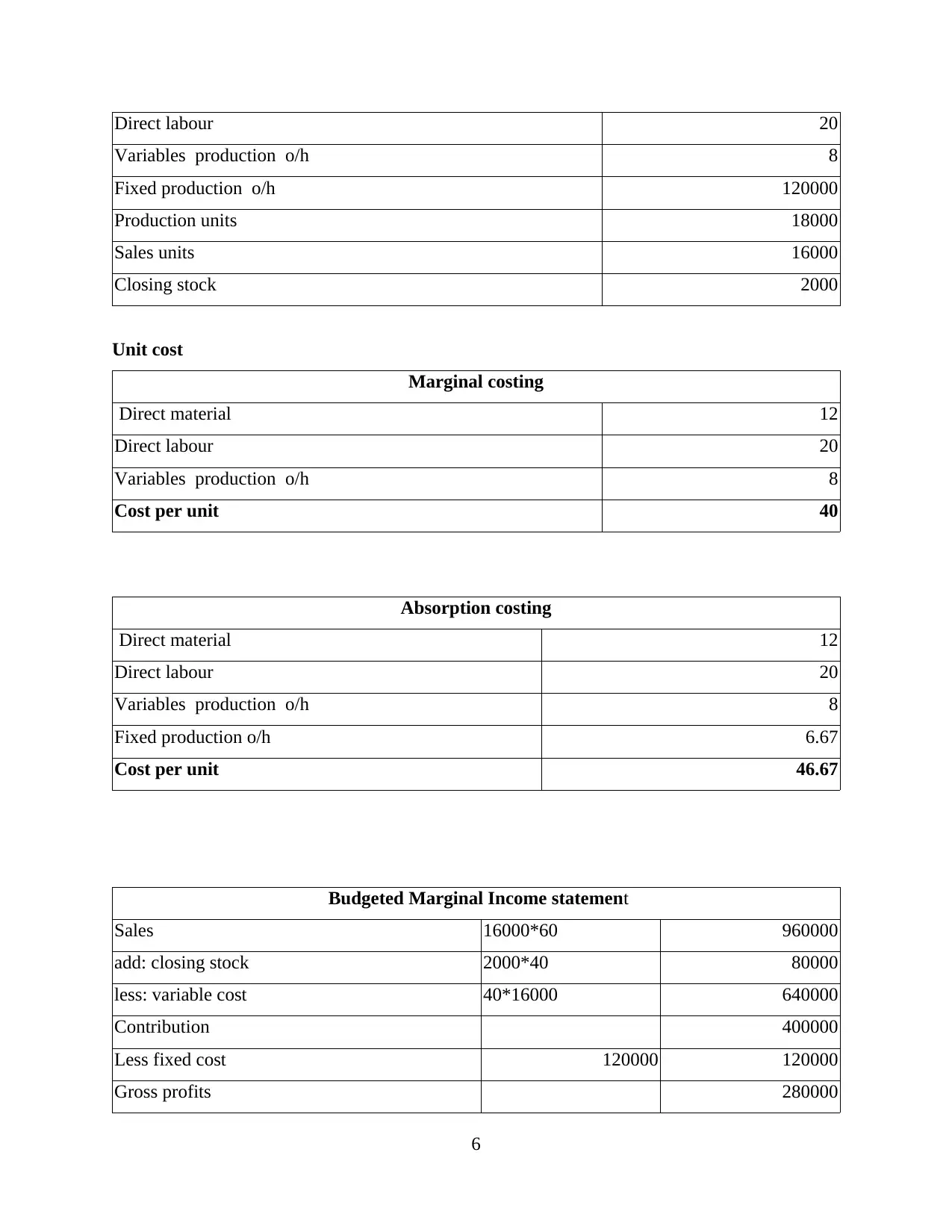

Calculations under Absorption costing and marginal costing

Marginal costing:

Given details

Sales prices 60

Direct material 12

5

considering trends and demand of customer.

Cost accounting system:

The advantages of the cost accounting system can be outlined as the the cost pertaining

to each job can be easily identified. This gives a opportunity to management of KEF to conduct

a comparison of the current cost with the past records to establish a controlling measure for cost

control (Kaplan and Atkinson, 2015). The disadvantages of this system is that it is time

consuming as to determine the cost for each activity is cumbersome as there are lots of processes

for production of a single units only. A wrong detection of the cost can lead to misallocation of

the resources and can hamper the performance efficiency.

The application of this system in KEF can be stated as cost related with each activity of

manufacturing of different product is determined. This is done by identifying the expenses done

both direct and indirect and then sales prices is decided after adding the profit margin required by

KEF.

Integration of the management accounting reporting and management accounting systems

The management accounting system are related with presenting a full system to manage

the activity of the business rather the reports under management accounting are prepared to

detect the performance of the business and its related activities (Key Advantages &

Disadvantages of Using a Static Budget, 2019). The integration can be seen as both falls under

the scope of management accounting one is related with stating system to conduct the operation

of the business of KEF and the other is related with detecting and evaluation of the performance

and each setting the goals fro each of the activity of the business.

TASK 2

Calculations under Absorption costing and marginal costing

Marginal costing:

Given details

Sales prices 60

Direct material 12

5

Direct labour 20

Variables production o/h 8

Fixed production o/h 120000

Production units 18000

Sales units 16000

Closing stock 2000

Unit cost

Marginal costing

Direct material 12

Direct labour 20

Variables production o/h 8

Cost per unit 40

Absorption costing

Direct material 12

Direct labour 20

Variables production o/h 8

Fixed production o/h 6.67

Cost per unit 46.67

Budgeted Marginal Income statement

Sales 16000*60 960000

add: closing stock 2000*40 80000

less: variable cost 40*16000 640000

Contribution 400000

Less fixed cost 120000 120000

Gross profits 280000

6

Variables production o/h 8

Fixed production o/h 120000

Production units 18000

Sales units 16000

Closing stock 2000

Unit cost

Marginal costing

Direct material 12

Direct labour 20

Variables production o/h 8

Cost per unit 40

Absorption costing

Direct material 12

Direct labour 20

Variables production o/h 8

Fixed production o/h 6.67

Cost per unit 46.67

Budgeted Marginal Income statement

Sales 16000*60 960000

add: closing stock 2000*40 80000

less: variable cost 40*16000 640000

Contribution 400000

Less fixed cost 120000 120000

Gross profits 280000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

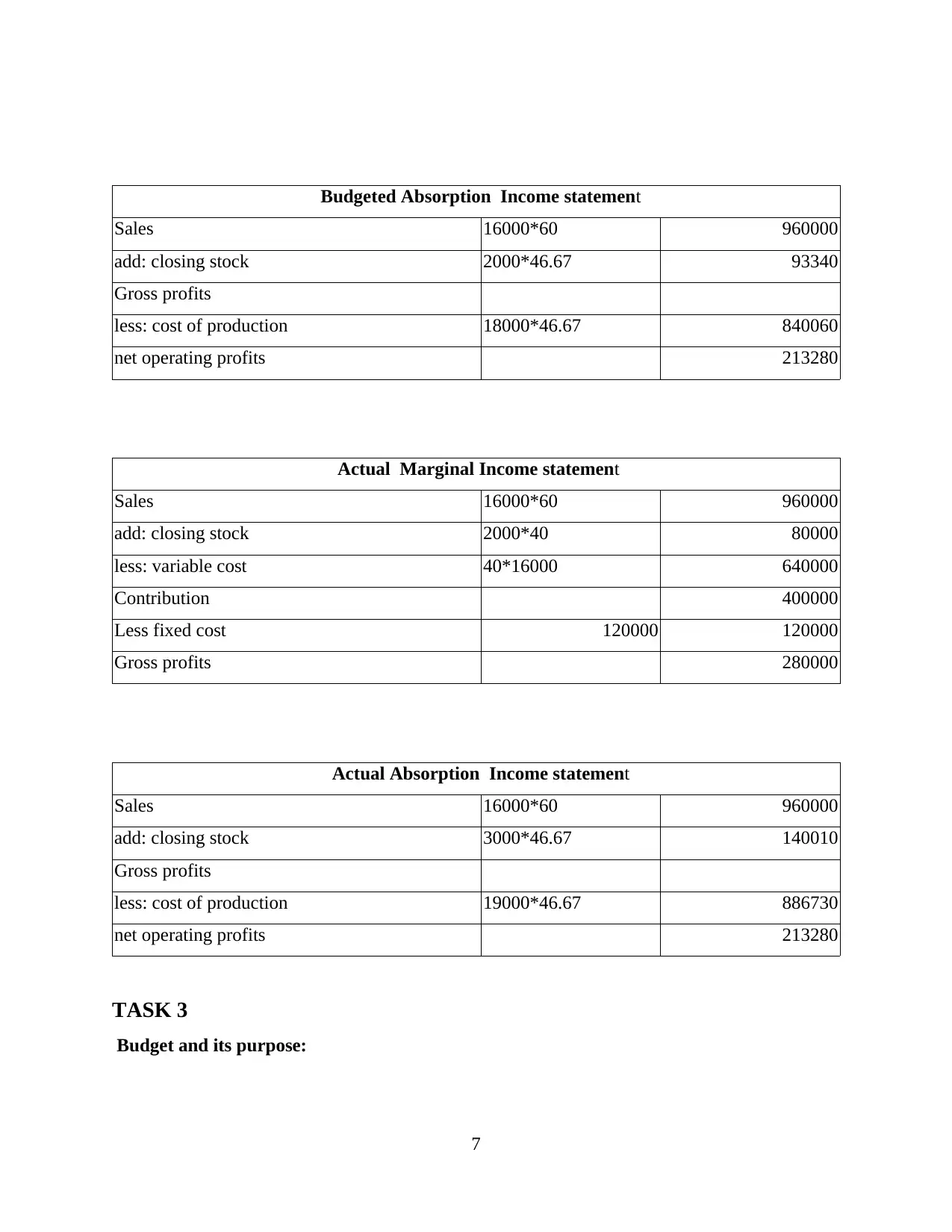

Budgeted Absorption Income statement

Sales 16000*60 960000

add: closing stock 2000*46.67 93340

Gross profits

less: cost of production 18000*46.67 840060

net operating profits 213280

Actual Marginal Income statement

Sales 16000*60 960000

add: closing stock 2000*40 80000

less: variable cost 40*16000 640000

Contribution 400000

Less fixed cost 120000 120000

Gross profits 280000

Actual Absorption Income statement

Sales 16000*60 960000

add: closing stock 3000*46.67 140010

Gross profits

less: cost of production 19000*46.67 886730

net operating profits 213280

TASK 3

Budget and its purpose:

7

Sales 16000*60 960000

add: closing stock 2000*46.67 93340

Gross profits

less: cost of production 18000*46.67 840060

net operating profits 213280

Actual Marginal Income statement

Sales 16000*60 960000

add: closing stock 2000*40 80000

less: variable cost 40*16000 640000

Contribution 400000

Less fixed cost 120000 120000

Gross profits 280000

Actual Absorption Income statement

Sales 16000*60 960000

add: closing stock 3000*46.67 140010

Gross profits

less: cost of production 19000*46.67 886730

net operating profits 213280

TASK 3

Budget and its purpose:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A budget is the forecast of the spending and revenue for a business for a specific time

period. The forecast is related with income and expenditure and there by the profitability and

this is a tool for decision making and this monitor a business (Maas, Schaltegger and Crutzen,

2016). The purpose of budget is to present a estimated expenses to the business where the

activities are to be undertaken under allocated funds and resources.

Presenting benefits and drawbacks of various types of planning tools under budgetary control

Zero based budget:

The advantage of preparing this type of budget is that it ensures the mangers of KEF

think about how everts penny of the organisation is spent (Quattrone, 2016). All the operating

expenses are justified and its considers all those areas of the KEF which are generating revenues.

The disadvantages of this type of budget is that its takes lots of time in preparation as all

the expenses are required to be justified for each budging period. This budget rewards short term

thinking were the resources are shifted to those areas of KEF which generated more revenues.

Fixed budget:

The benefits of the fixed budget are that once after its establishment KEF follows it and

keeps the record of actual spending. This is easy to implement and does not require any updates

through out the budgeting period. This allowed KEF to see whether it might be overestimating or

underestimating the expenses.

The drawbacks related to fixed budget is that it lacks flexibility. Once established no changes are

made in the budget by KEF with changes in sales volume or other changes. KEF can not allocate

additional resources to keep up with the changes as well. Also, KEF, static budgets are based on

previous data of KEF, newer businesses may have more difficulty establishing and implementing

them.

Operating budget:

Pros of the operation budget for KEF are related with keeping a track of all the activities

of the business (Messner, 2016). This indicates both money that is spend and the revenues that

can be generated.

Another benefit is that by showing this to the potential investors the operating cost of the KEF

the investors can make a informed decision to invest in KEF.

The cons of operating budget is that its is rigid in nature and does not allow any changes

in it during the financial year. This budget do not assist the management in reduction of the

8

period. The forecast is related with income and expenditure and there by the profitability and

this is a tool for decision making and this monitor a business (Maas, Schaltegger and Crutzen,

2016). The purpose of budget is to present a estimated expenses to the business where the

activities are to be undertaken under allocated funds and resources.

Presenting benefits and drawbacks of various types of planning tools under budgetary control

Zero based budget:

The advantage of preparing this type of budget is that it ensures the mangers of KEF

think about how everts penny of the organisation is spent (Quattrone, 2016). All the operating

expenses are justified and its considers all those areas of the KEF which are generating revenues.

The disadvantages of this type of budget is that its takes lots of time in preparation as all

the expenses are required to be justified for each budging period. This budget rewards short term

thinking were the resources are shifted to those areas of KEF which generated more revenues.

Fixed budget:

The benefits of the fixed budget are that once after its establishment KEF follows it and

keeps the record of actual spending. This is easy to implement and does not require any updates

through out the budgeting period. This allowed KEF to see whether it might be overestimating or

underestimating the expenses.

The drawbacks related to fixed budget is that it lacks flexibility. Once established no changes are

made in the budget by KEF with changes in sales volume or other changes. KEF can not allocate

additional resources to keep up with the changes as well. Also, KEF, static budgets are based on

previous data of KEF, newer businesses may have more difficulty establishing and implementing

them.

Operating budget:

Pros of the operation budget for KEF are related with keeping a track of all the activities

of the business (Messner, 2016). This indicates both money that is spend and the revenues that

can be generated.

Another benefit is that by showing this to the potential investors the operating cost of the KEF

the investors can make a informed decision to invest in KEF.

The cons of operating budget is that its is rigid in nature and does not allow any changes

in it during the financial year. This budget do not assist the management in reduction of the

8

debts of the KEF. This also do not used through out the years without any assumptions and

charges in consideration.

Analysing the usage and application of planning tools by KEF in preparation and forecasting of

budgets

Zero based budget:

This is the budget which is made under accounting practices where concept of tradition

budget overruled. Under this budget KEF prepare the budgets from the base zero for every

expenses which means no refereed from past budgets are taken (Hopper and Bui, 2016). Each

new budget is made from a zero base and the management of KEF is required to justify each

expense before it to new budget.

Fixed budget:

It is also termed as static budget. The fixed budget is used by KEF as an essential tool for

measuring the success of the business. This assist business in taking both long term and short

term goal (Bromwich and Scapens, 2015). The fixed budget is prepared for certain expenses

where no changes are made in the budgets and used by the KEF to operate activities in

specified budget.

Operating budget:

The operating budgets are prepared by KEF to plan the day to day expenses and

operation of the business in order to prevent a financial ditch (Ax and Greve, 2017). The

management of KEF uses this budget to track as well as charting growth and addressing any of

the issues of the business. The operating budget possess a potential to to attract investment into

the company.

TASK 4

Comparing the adopting management accounting system for responding to financial problem by

KEF

The decision making process of a business is related with making choices by

identification of a decision with getting information and assessing alternate resolution . This is

process of making decisions step by steps that help KEF to make more deliberate, thoughtful

decisions by organizing relevant information and defining alternatives. A business faces various

issues and for this a decisions are required to be taken. The following tables depicts the same:

9

charges in consideration.

Analysing the usage and application of planning tools by KEF in preparation and forecasting of

budgets

Zero based budget:

This is the budget which is made under accounting practices where concept of tradition

budget overruled. Under this budget KEF prepare the budgets from the base zero for every

expenses which means no refereed from past budgets are taken (Hopper and Bui, 2016). Each

new budget is made from a zero base and the management of KEF is required to justify each

expense before it to new budget.

Fixed budget:

It is also termed as static budget. The fixed budget is used by KEF as an essential tool for

measuring the success of the business. This assist business in taking both long term and short

term goal (Bromwich and Scapens, 2015). The fixed budget is prepared for certain expenses

where no changes are made in the budgets and used by the KEF to operate activities in

specified budget.

Operating budget:

The operating budgets are prepared by KEF to plan the day to day expenses and

operation of the business in order to prevent a financial ditch (Ax and Greve, 2017). The

management of KEF uses this budget to track as well as charting growth and addressing any of

the issues of the business. The operating budget possess a potential to to attract investment into

the company.

TASK 4

Comparing the adopting management accounting system for responding to financial problem by

KEF

The decision making process of a business is related with making choices by

identification of a decision with getting information and assessing alternate resolution . This is

process of making decisions step by steps that help KEF to make more deliberate, thoughtful

decisions by organizing relevant information and defining alternatives. A business faces various

issues and for this a decisions are required to be taken. The following tables depicts the same:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.