Management Accounting Techniques and Systems: MVMT Watches Analysis

VerifiedAdded on 2023/01/09

|20

|5451

|90

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and techniques applied within MVMT Watches. It begins by defining management accounting and its importance in decision-making, then explores various management accounting systems such as cost accounting, inventory management, job costing, and price optimization, detailing their essential requirements and benefits. The report also examines different methods used for management accounting reporting, including inventory management reports, departmental reports, operating budget reports, and product profitability reports, highlighting their significance in providing insights for managers. Furthermore, it delves into the calculation of costs using techniques like marginal costing and absorption costing, illustrating their application with numerical examples and reconciliation statements. The analysis includes the calculation of break-even points and margin of safety, offering a detailed perspective on cost-volume-profit relationships. The report emphasizes the advantages and integration of these systems within organizational processes, ultimately providing a critical evaluation of their role in enhancing decision-making and financial performance at MVMT Watches. Desklib offers a platform to access similar solved assignments and study resources for students.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting refers to the use of different types of techniques to analyse and

interpret the financial data and information available in order to take the correct decisions

(Armitage, Webb and Glynn, 2016). If the managers use its provisions in the correct manner then

it can result in taking of such decisions which can likely create a strong impact on the working

pattern and the functioning of the company. For using it the managers are required to have sound

knowledge of the different types of financial concepts and must be able to perform a deep

analysis on the financial data of the company in an accurate manner to get the desired outcomes.

For this report MVMT Watches has been chosen. This company has headquarters in Los Angels,

United States. In this assignment, detailed focus will be made on demonstration of understanding

of management accounting systems, application of a range of its techniques. Additionally,

explanation of the use of planning tools and comparison of ways in which companies are using it

to respond to financial problems will be discussed as a part of this project.

TASK 1

P1: Management Accounting Systems

Management Accounting refers to making the use of different types of financial

provisions in an effective manner so that the managers are able to take the right decisions

effectively and efficiently without problems and issues. Therefore the managers of Innocent

Drinks should be able to make the correct use of it for taking of short-term and long-term

decisions. If they make the right use of its methods and techniques then they will be able to attain

the goals and objectives in the future time period.

There are different types of management accounting systems (Bui and De Villiers, 2017).

These are explained as follows-

Cost Accounting System- This system is basically meant to identify the various costs

which can be incurred within an organization. Using it, the companies like MVMT Watches can

make sure that they are able to identify and reduce the costs effectively and efficiently.

Essential requirements-

In a Cost Accounting System there must be a methodology which can be used for

identifying and segregating the costs and overheads of different types of departments in

the company.

1

Management Accounting refers to the use of different types of techniques to analyse and

interpret the financial data and information available in order to take the correct decisions

(Armitage, Webb and Glynn, 2016). If the managers use its provisions in the correct manner then

it can result in taking of such decisions which can likely create a strong impact on the working

pattern and the functioning of the company. For using it the managers are required to have sound

knowledge of the different types of financial concepts and must be able to perform a deep

analysis on the financial data of the company in an accurate manner to get the desired outcomes.

For this report MVMT Watches has been chosen. This company has headquarters in Los Angels,

United States. In this assignment, detailed focus will be made on demonstration of understanding

of management accounting systems, application of a range of its techniques. Additionally,

explanation of the use of planning tools and comparison of ways in which companies are using it

to respond to financial problems will be discussed as a part of this project.

TASK 1

P1: Management Accounting Systems

Management Accounting refers to making the use of different types of financial

provisions in an effective manner so that the managers are able to take the right decisions

effectively and efficiently without problems and issues. Therefore the managers of Innocent

Drinks should be able to make the correct use of it for taking of short-term and long-term

decisions. If they make the right use of its methods and techniques then they will be able to attain

the goals and objectives in the future time period.

There are different types of management accounting systems (Bui and De Villiers, 2017).

These are explained as follows-

Cost Accounting System- This system is basically meant to identify the various costs

which can be incurred within an organization. Using it, the companies like MVMT Watches can

make sure that they are able to identify and reduce the costs effectively and efficiently.

Essential requirements-

In a Cost Accounting System there must be a methodology which can be used for

identifying and segregating the costs and overheads of different types of departments in

the company.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A Cost Accounting System must be able to make sure that the correct techniques can be

used by the companies so that they are able to reduce the costs and overheads to

maximize their level of profits.

Inventory Management System- In this system a company aims to properly manage the

level of stock. The firms like MVMT Watches can use this system so that they are able to

achieve the desired level of efficiency and effectiveness in the management of stock level in the

organization. If the company makes use of methods like LIFO, FIFO, Weighted Average Cost in

a correct manner then this will make sure that the company is able to properly track its level of

inventory.

Essential requirements-

In a good Inventory Management System it is required that the right measures are used to

value the level of stock.

In an Inventory Management System there should be proper maintenance of records of

inflows and outflows of the stock.

Job Costing System- In it, there is a particular system which is used in order to track the

different types of job orders (Cooper, Ezzamel and Qu, 2017). Using it, the managers of MVMT

Watches can track and manage their job orders. This will help not only in reducing the costs

incurred in these orders but also in maximizing the level of profits.

Essential requirements-

A good Job Costing System is the one which is able to track the inwards and outwards

movement of job orders. In this way it makes sure that the company becomes efficient in

dealing with these orders.

In a Job Costing System there must be a particular focus which must be put on

application of the techniques in order to reduce the overall level of costs.

Price Optimization System- In this system, there are various techniques which can be

used in order to forecast the overall demand of the products as well as services (Gibassier and

Alcouffe, 2018). The management of MVMT Watches can use it so that they are able to set a

right price which will enable the company to earn higher level of profits.

Essential requirements-

In a Price Optimization System there are techniques which must be used in order to set

the right price in the organization.

2

used by the companies so that they are able to reduce the costs and overheads to

maximize their level of profits.

Inventory Management System- In this system a company aims to properly manage the

level of stock. The firms like MVMT Watches can use this system so that they are able to

achieve the desired level of efficiency and effectiveness in the management of stock level in the

organization. If the company makes use of methods like LIFO, FIFO, Weighted Average Cost in

a correct manner then this will make sure that the company is able to properly track its level of

inventory.

Essential requirements-

In a good Inventory Management System it is required that the right measures are used to

value the level of stock.

In an Inventory Management System there should be proper maintenance of records of

inflows and outflows of the stock.

Job Costing System- In it, there is a particular system which is used in order to track the

different types of job orders (Cooper, Ezzamel and Qu, 2017). Using it, the managers of MVMT

Watches can track and manage their job orders. This will help not only in reducing the costs

incurred in these orders but also in maximizing the level of profits.

Essential requirements-

A good Job Costing System is the one which is able to track the inwards and outwards

movement of job orders. In this way it makes sure that the company becomes efficient in

dealing with these orders.

In a Job Costing System there must be a particular focus which must be put on

application of the techniques in order to reduce the overall level of costs.

Price Optimization System- In this system, there are various techniques which can be

used in order to forecast the overall demand of the products as well as services (Gibassier and

Alcouffe, 2018). The management of MVMT Watches can use it so that they are able to set a

right price which will enable the company to earn higher level of profits.

Essential requirements-

In a Price Optimization System there are techniques which must be used in order to set

the right price in the organization.

2

A good Price Optimization System should be able to make sure that the company earns

higher level of profits in the future time period to get a strategic edge over the

competitors.

P2: Methods used for Management Accounting Reporting

Management Accounting Reports are useful for the managers to get insights in their

business operations. Some of these reports are as follows-

Inventory Management Report- In this report, a focus is made on the detailed aspects

of the level of inventory (Hall, 2016). The managers of MVMT Watches can use these

reports so that they are able to bring the required level of efficiency as well as

effectiveness in their inventory management. With it, they can make specific analysis and

give their detailed viewpoints on the improvements which can be done to rectify the

different types of deviations and variances which can occur so that desired outcomes can

be achieved. For using them correctly proper cooperation and coordination is required

within the company.

Departmental Report- There can be different types of departments in an organization

(Honggowati and et.al., 2017). These are Production, Finance, HR, Marketing and Sales.

There are reports which are prepared on them so that specific analysis on each one of

them can be made by the departmental managers. This helps in promoting the

specialization within the organizational processes and its way of functioning. In the

context of MVMT Watches it can be crucial for the managers to identify the problems

and issues facing the departments so that the rectifying measures are taken to sort them

out. If this report has to be used to provide the required results then the managers should

be able to rightly make use of the available data.

Operating Budget Report- In this report, focus is made particularly on operating budget

of the organization (Hopper and Bui, 2016). Thus once it has been made then this report

is prepared so that the correct viewpoints of the managers can be recorded for taking

crucial decisions in the future time period. For the managers of MVMT Watches, use of

these reports becomes quite crucial so that they are able to make the necessary

judgements. Using it, the managers can make detailed plans of the procedures to be

undertaken to improve the operating profit of the organization so that an overall level of

efficiency and effectiveness may be raised.

3

higher level of profits in the future time period to get a strategic edge over the

competitors.

P2: Methods used for Management Accounting Reporting

Management Accounting Reports are useful for the managers to get insights in their

business operations. Some of these reports are as follows-

Inventory Management Report- In this report, a focus is made on the detailed aspects

of the level of inventory (Hall, 2016). The managers of MVMT Watches can use these

reports so that they are able to bring the required level of efficiency as well as

effectiveness in their inventory management. With it, they can make specific analysis and

give their detailed viewpoints on the improvements which can be done to rectify the

different types of deviations and variances which can occur so that desired outcomes can

be achieved. For using them correctly proper cooperation and coordination is required

within the company.

Departmental Report- There can be different types of departments in an organization

(Honggowati and et.al., 2017). These are Production, Finance, HR, Marketing and Sales.

There are reports which are prepared on them so that specific analysis on each one of

them can be made by the departmental managers. This helps in promoting the

specialization within the organizational processes and its way of functioning. In the

context of MVMT Watches it can be crucial for the managers to identify the problems

and issues facing the departments so that the rectifying measures are taken to sort them

out. If this report has to be used to provide the required results then the managers should

be able to rightly make use of the available data.

Operating Budget Report- In this report, focus is made particularly on operating budget

of the organization (Hopper and Bui, 2016). Thus once it has been made then this report

is prepared so that the correct viewpoints of the managers can be recorded for taking

crucial decisions in the future time period. For the managers of MVMT Watches, use of

these reports becomes quite crucial so that they are able to make the necessary

judgements. Using it, the managers can make detailed plans of the procedures to be

undertaken to improve the operating profit of the organization so that an overall level of

efficiency and effectiveness may be raised.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Product Profitability Report- In this report, the profitability of a particular product in a

market can be determined (Kastberg and Siverbo, 2016). In the context of the managers

of MVMT Watches, preparation of these reports is quite crucial because using it they will

be able to determine the products which will provide them with maximum profits. Thus

specific attention can be given to them and the right plan can be made for the purpose of

their marketing and promotion. The products of the company must be segregated and

detailed analysis should be made on the profits which have been earned due to them in

the last 5 years. Thereafter, the products with maximum profitability must be selected and

plans must be made so that some improvements can be made in them so that they can

satisfy the customers and continue to be profitable for the organization.

M1: Benefits of Management Accounting Systems

Cost Accounting System can help the organizations like MVMT Watches so that they are

able to identify and segregate their various costs and can make use of rectifying techniques to

reduce them. Inventory Management Systems offers the benefits of better tracking and better

usage of the stock. Job Costing System helps the companies so that they are able to identify the

job orders and also allows it to track these job orders. Price Optimization System can be used to

forecast the prices and optimize them to suit the needs and requirements of the companies.

D1: Critical evaluation of Management Accounting Systems and their Integration within

Organizational Processes

Cost Accounting System can be integrated within the organizational processes of MVMT

Watches by identifying and segregating the costs. Inventory Management System can be

integrated by identification and management of the stock levels. Job Costing System can be

integrated by actively tracking the inwards and outwards movement of the job orders. Price

Optimization System can be integrated by forecasting the demand data of the products and

services and setting the price accordingly. Thus in this way all of them can be successfully

integrated within the organizational processes. This will ensure that the correct decisions can be

taken within the context of the organization without problems and issues.

TASK 2

P3: Calculation of costs using appropriate techniques

4

market can be determined (Kastberg and Siverbo, 2016). In the context of the managers

of MVMT Watches, preparation of these reports is quite crucial because using it they will

be able to determine the products which will provide them with maximum profits. Thus

specific attention can be given to them and the right plan can be made for the purpose of

their marketing and promotion. The products of the company must be segregated and

detailed analysis should be made on the profits which have been earned due to them in

the last 5 years. Thereafter, the products with maximum profitability must be selected and

plans must be made so that some improvements can be made in them so that they can

satisfy the customers and continue to be profitable for the organization.

M1: Benefits of Management Accounting Systems

Cost Accounting System can help the organizations like MVMT Watches so that they are

able to identify and segregate their various costs and can make use of rectifying techniques to

reduce them. Inventory Management Systems offers the benefits of better tracking and better

usage of the stock. Job Costing System helps the companies so that they are able to identify the

job orders and also allows it to track these job orders. Price Optimization System can be used to

forecast the prices and optimize them to suit the needs and requirements of the companies.

D1: Critical evaluation of Management Accounting Systems and their Integration within

Organizational Processes

Cost Accounting System can be integrated within the organizational processes of MVMT

Watches by identifying and segregating the costs. Inventory Management System can be

integrated by identification and management of the stock levels. Job Costing System can be

integrated by actively tracking the inwards and outwards movement of the job orders. Price

Optimization System can be integrated by forecasting the demand data of the products and

services and setting the price accordingly. Thus in this way all of them can be successfully

integrated within the organizational processes. This will ensure that the correct decisions can be

taken within the context of the organization without problems and issues.

TASK 2

P3: Calculation of costs using appropriate techniques

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

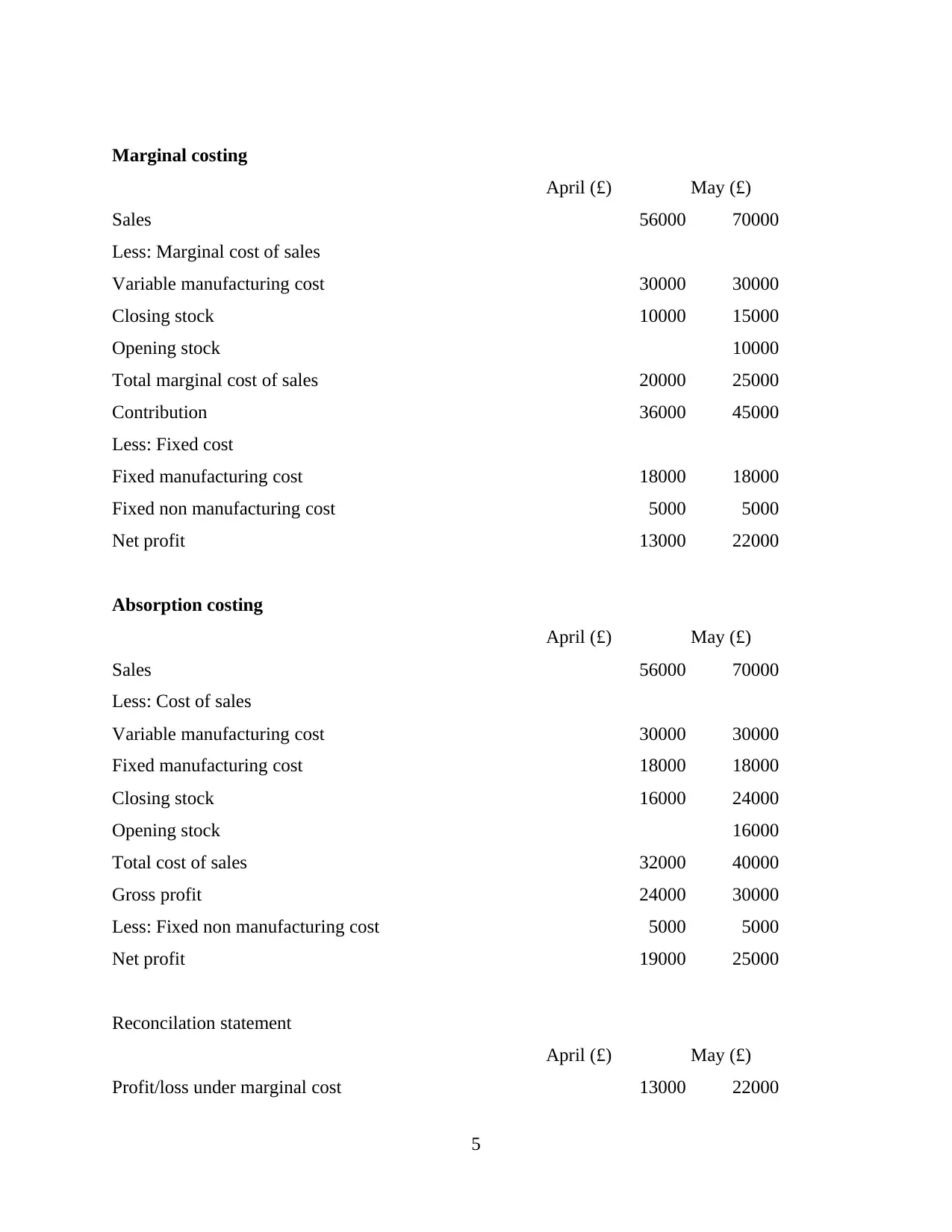

Marginal costing

April (£) May (£)

Sales 56000 70000

Less: Marginal cost of sales

Variable manufacturing cost 30000 30000

Closing stock 10000 15000

Opening stock 10000

Total marginal cost of sales 20000 25000

Contribution 36000 45000

Less: Fixed cost

Fixed manufacturing cost 18000 18000

Fixed non manufacturing cost 5000 5000

Net profit 13000 22000

Absorption costing

April (£) May (£)

Sales 56000 70000

Less: Cost of sales

Variable manufacturing cost 30000 30000

Fixed manufacturing cost 18000 18000

Closing stock 16000 24000

Opening stock 16000

Total cost of sales 32000 40000

Gross profit 24000 30000

Less: Fixed non manufacturing cost 5000 5000

Net profit 19000 25000

Reconcilation statement

April (£) May (£)

Profit/loss under marginal cost 13000 22000

5

April (£) May (£)

Sales 56000 70000

Less: Marginal cost of sales

Variable manufacturing cost 30000 30000

Closing stock 10000 15000

Opening stock 10000

Total marginal cost of sales 20000 25000

Contribution 36000 45000

Less: Fixed cost

Fixed manufacturing cost 18000 18000

Fixed non manufacturing cost 5000 5000

Net profit 13000 22000

Absorption costing

April (£) May (£)

Sales 56000 70000

Less: Cost of sales

Variable manufacturing cost 30000 30000

Fixed manufacturing cost 18000 18000

Closing stock 16000 24000

Opening stock 16000

Total cost of sales 32000 40000

Gross profit 24000 30000

Less: Fixed non manufacturing cost 5000 5000

Net profit 19000 25000

Reconcilation statement

April (£) May (£)

Profit/loss under marginal cost 13000 22000

5

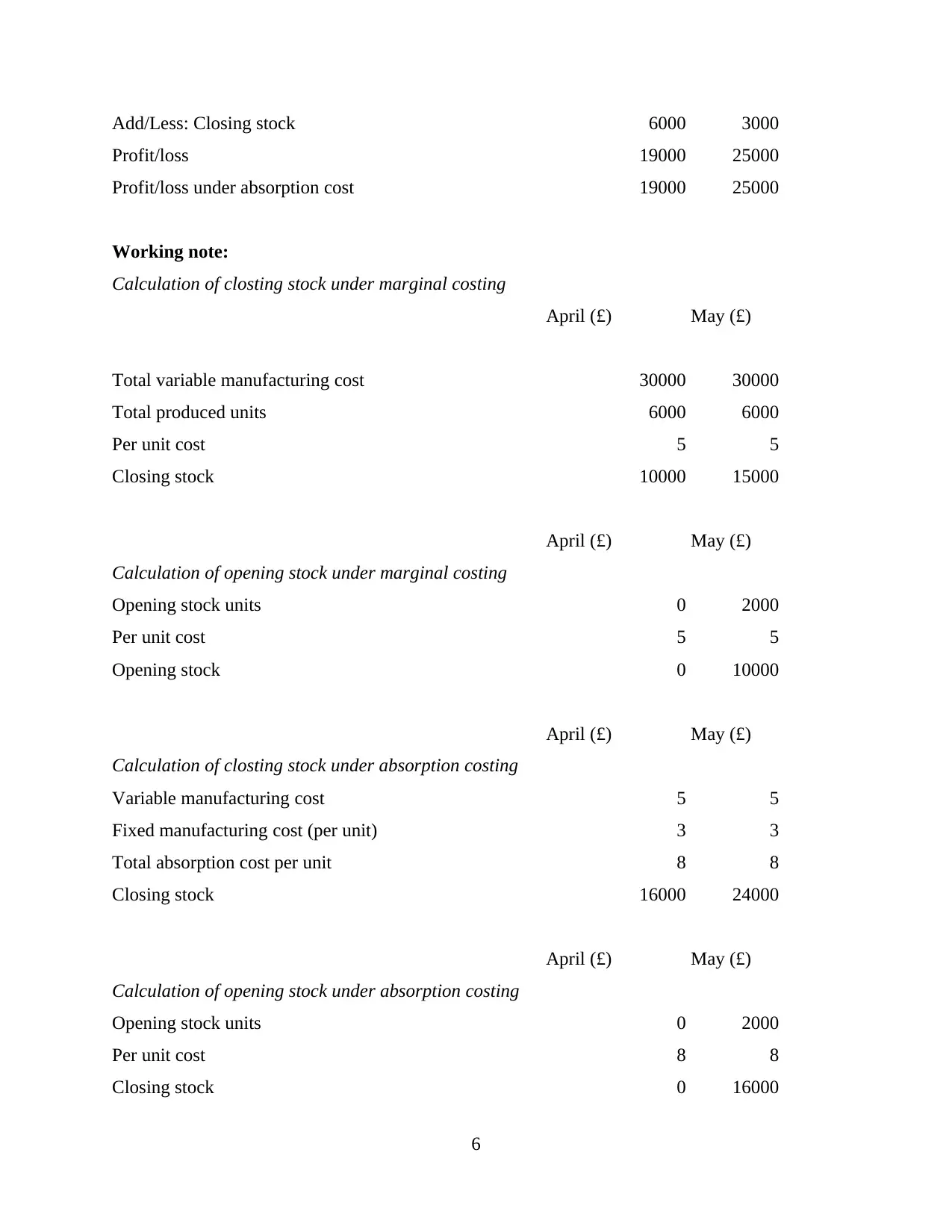

Add/Less: Closing stock 6000 3000

Profit/loss 19000 25000

Profit/loss under absorption cost 19000 25000

Working note:

Calculation of closting stock under marginal costing

April (£) May (£)

Total variable manufacturing cost 30000 30000

Total produced units 6000 6000

Per unit cost 5 5

Closing stock 10000 15000

April (£) May (£)

Calculation of opening stock under marginal costing

Opening stock units 0 2000

Per unit cost 5 5

Opening stock 0 10000

April (£) May (£)

Calculation of closting stock under absorption costing

Variable manufacturing cost 5 5

Fixed manufacturing cost (per unit) 3 3

Total absorption cost per unit 8 8

Closing stock 16000 24000

April (£) May (£)

Calculation of opening stock under absorption costing

Opening stock units 0 2000

Per unit cost 8 8

Closing stock 0 16000

6

Profit/loss 19000 25000

Profit/loss under absorption cost 19000 25000

Working note:

Calculation of closting stock under marginal costing

April (£) May (£)

Total variable manufacturing cost 30000 30000

Total produced units 6000 6000

Per unit cost 5 5

Closing stock 10000 15000

April (£) May (£)

Calculation of opening stock under marginal costing

Opening stock units 0 2000

Per unit cost 5 5

Opening stock 0 10000

April (£) May (£)

Calculation of closting stock under absorption costing

Variable manufacturing cost 5 5

Fixed manufacturing cost (per unit) 3 3

Total absorption cost per unit 8 8

Closing stock 16000 24000

April (£) May (£)

Calculation of opening stock under absorption costing

Opening stock units 0 2000

Per unit cost 8 8

Closing stock 0 16000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

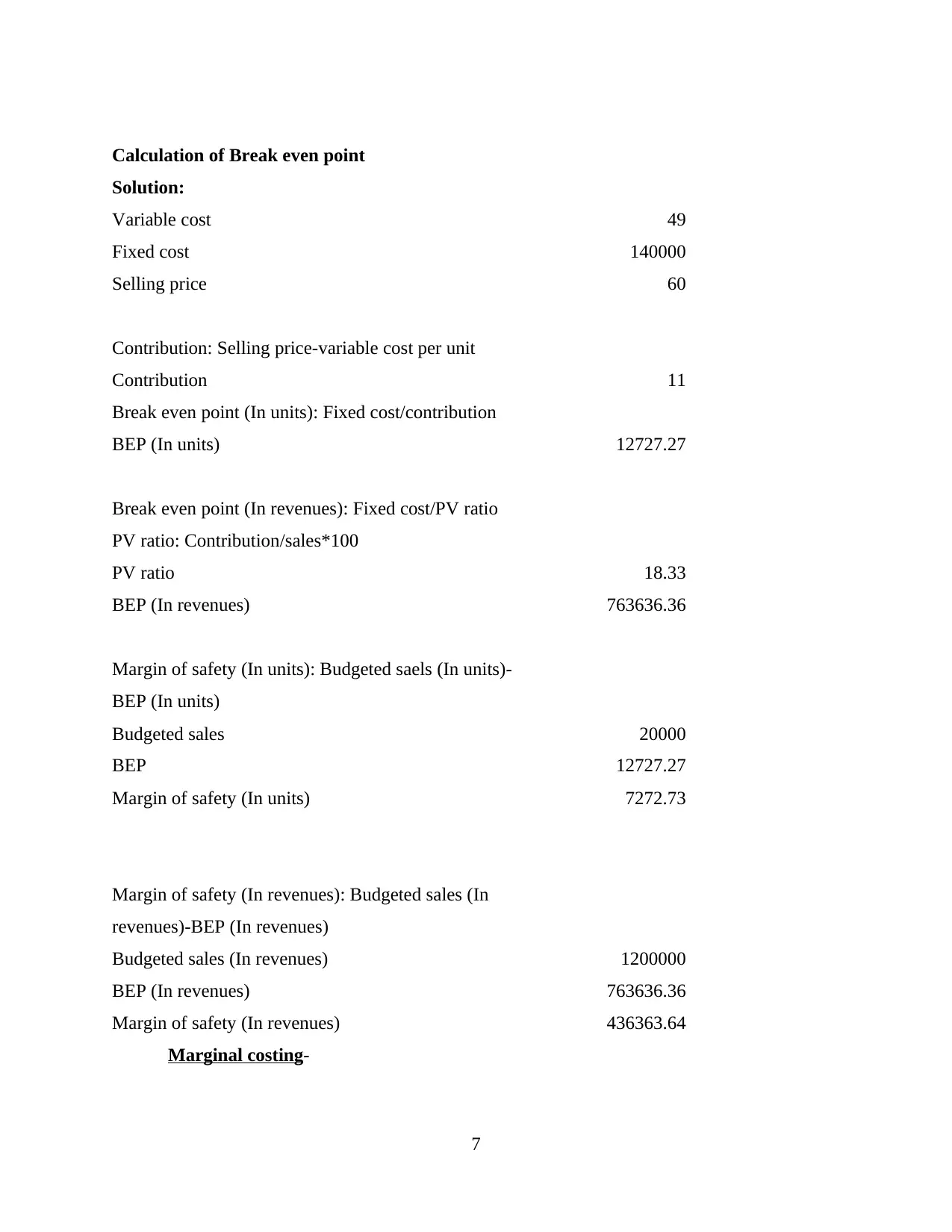

Calculation of Break even point

Solution:

Variable cost 49

Fixed cost 140000

Selling price 60

Contribution: Selling price-variable cost per unit

Contribution 11

Break even point (In units): Fixed cost/contribution

BEP (In units) 12727.27

Break even point (In revenues): Fixed cost/PV ratio

PV ratio: Contribution/sales*100

PV ratio 18.33

BEP (In revenues) 763636.36

Margin of safety (In units): Budgeted saels (In units)-

BEP (In units)

Budgeted sales 20000

BEP 12727.27

Margin of safety (In units) 7272.73

Margin of safety (In revenues): Budgeted sales (In

revenues)-BEP (In revenues)

Budgeted sales (In revenues) 1200000

BEP (In revenues) 763636.36

Margin of safety (In revenues) 436363.64

Marginal costing-

7

Solution:

Variable cost 49

Fixed cost 140000

Selling price 60

Contribution: Selling price-variable cost per unit

Contribution 11

Break even point (In units): Fixed cost/contribution

BEP (In units) 12727.27

Break even point (In revenues): Fixed cost/PV ratio

PV ratio: Contribution/sales*100

PV ratio 18.33

BEP (In revenues) 763636.36

Margin of safety (In units): Budgeted saels (In units)-

BEP (In units)

Budgeted sales 20000

BEP 12727.27

Margin of safety (In units) 7272.73

Margin of safety (In revenues): Budgeted sales (In

revenues)-BEP (In revenues)

Budgeted sales (In revenues) 1200000

BEP (In revenues) 763636.36

Margin of safety (In revenues) 436363.64

Marginal costing-

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is a technique which is used to find out the profitability level (Kostyukova and et.al.,

2018). In it the variable cost is charged to the units while the fixed cost is written off against the

contribution. Using it, the managers of Innocent Drinks can take the required decisions easily.

Thus it is a very valuable technique for the management. It helps a lot in the determination of

Break-Even Point which is where the companies neither earn profit nor incur losses.

Advantages-

The technique of Marginal Costing is very simple to use as well as understand. This

creates an advantage for the managers of Innocent Drinks as it can be applied effectively

in the processes of the organization without issues and problems.

The Marginal Costing Technique helps a lot to the organizations so that they are able to

maintain cost control. For Innocent Drinks, this creates an advantage.

Disadvantages-

It makes use of certain types of assumptions. If these assumptions are wrong then this can

create problems as it will lead to inaccuracy. For Innocent Drinks this creates a

disadvantage.

All costs cannot be divided into fixed and variable costs. Therefore some of the costs are

semi-variable in nature. If all the costs are segregated into fixed and variable then this can

give inaccurate results leading to disadvantage for Innocent Drinks.

Absorption Costing-

It is a method in which the costs are calculated by identifying the details of full cost of

manufacturing the product (Kumarasiri and Jubb, 2016). Using it the managers of Innocent

Drinks can make sure that they are able to make use of its correct techniques to find out the

profits. Thus in this way the managers will be able to make sure that they can find out the profits

and can perform the required analysis and interpretation using different methods.

Advantages-

Absorption Costing technique helps a lot in identifying the full cost which is associated

with the production. The management of Innocent Drinks can use it so that they are able

to get details on their overall costs.

This technique is helpful for the management as it Cadburyshows less fluctuation in

profits in the case of constant production but fluctuating sales. In the context of Innocent

Drinks, this can help the managers a lot.

8

2018). In it the variable cost is charged to the units while the fixed cost is written off against the

contribution. Using it, the managers of Innocent Drinks can take the required decisions easily.

Thus it is a very valuable technique for the management. It helps a lot in the determination of

Break-Even Point which is where the companies neither earn profit nor incur losses.

Advantages-

The technique of Marginal Costing is very simple to use as well as understand. This

creates an advantage for the managers of Innocent Drinks as it can be applied effectively

in the processes of the organization without issues and problems.

The Marginal Costing Technique helps a lot to the organizations so that they are able to

maintain cost control. For Innocent Drinks, this creates an advantage.

Disadvantages-

It makes use of certain types of assumptions. If these assumptions are wrong then this can

create problems as it will lead to inaccuracy. For Innocent Drinks this creates a

disadvantage.

All costs cannot be divided into fixed and variable costs. Therefore some of the costs are

semi-variable in nature. If all the costs are segregated into fixed and variable then this can

give inaccurate results leading to disadvantage for Innocent Drinks.

Absorption Costing-

It is a method in which the costs are calculated by identifying the details of full cost of

manufacturing the product (Kumarasiri and Jubb, 2016). Using it the managers of Innocent

Drinks can make sure that they are able to make use of its correct techniques to find out the

profits. Thus in this way the managers will be able to make sure that they can find out the profits

and can perform the required analysis and interpretation using different methods.

Advantages-

Absorption Costing technique helps a lot in identifying the full cost which is associated

with the production. The management of Innocent Drinks can use it so that they are able

to get details on their overall costs.

This technique is helpful for the management as it Cadburyshows less fluctuation in

profits in the case of constant production but fluctuating sales. In the context of Innocent

Drinks, this can help the managers a lot.

8

Disadvantages-

Absorption Costing technique does not helps the managers to take decisions. For the

managers of Innocent Drinks this can create a disadvantage.

It ignores the CVP analysis which helps in the calculation of Break-Even Point which is

the point at which a company does not earns profits but neither incurs a loss. In the

context of Innocent Drinks this is a disadvantage.

Justification- Both Marginal Costing and Absorption Costing Technique can be used by

the organizations so that they are able to find out the profitability. Companies like Innocent

Drinks can make sure that they can use both these techniques to achieve the desired results.

M2: Accurate application of the techniques

The techniques of marginal and absorption costing can be used by the organizations like

Innocent Drinks to get an overview of their financial position. By applying them in the correct

manner the management is able to make sure that it will raise the standards for the achievement

of aims and targets in the future time period. If the company has to get a strategic edge over its

competitors then it will certainly target the areas where it requires improvement and will use

rectifying techniques for improving. This will increase the chances of attaining the level of

sustainable success which is desired.

D2: Producing of financial reports for accurate application and interpretation of data

The financial reports are useful for the management because they help them a lot. These

are Cash Flow Statement, Income Statement and Balance Sheet. If the managers of the company

use them in the right manner they will be able to draw the right conclusions and

recommendations. This will help in taking the right decisions for growth in the future time

period. Thus the managers of Innocent Drinks should make sure that they are able to achieve the

goals and objectives through analysing and interpreting them.

TASK 3

P3: Advantages and Disadvantages of Planning Tools for Budgetary Control

Cash Budget-

9

Absorption Costing technique does not helps the managers to take decisions. For the

managers of Innocent Drinks this can create a disadvantage.

It ignores the CVP analysis which helps in the calculation of Break-Even Point which is

the point at which a company does not earns profits but neither incurs a loss. In the

context of Innocent Drinks this is a disadvantage.

Justification- Both Marginal Costing and Absorption Costing Technique can be used by

the organizations so that they are able to find out the profitability. Companies like Innocent

Drinks can make sure that they can use both these techniques to achieve the desired results.

M2: Accurate application of the techniques

The techniques of marginal and absorption costing can be used by the organizations like

Innocent Drinks to get an overview of their financial position. By applying them in the correct

manner the management is able to make sure that it will raise the standards for the achievement

of aims and targets in the future time period. If the company has to get a strategic edge over its

competitors then it will certainly target the areas where it requires improvement and will use

rectifying techniques for improving. This will increase the chances of attaining the level of

sustainable success which is desired.

D2: Producing of financial reports for accurate application and interpretation of data

The financial reports are useful for the management because they help them a lot. These

are Cash Flow Statement, Income Statement and Balance Sheet. If the managers of the company

use them in the right manner they will be able to draw the right conclusions and

recommendations. This will help in taking the right decisions for growth in the future time

period. Thus the managers of Innocent Drinks should make sure that they are able to achieve the

goals and objectives through analysing and interpreting them.

TASK 3

P3: Advantages and Disadvantages of Planning Tools for Budgetary Control

Cash Budget-

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.