Management Accounting: Systems, Reporting, and Techniques Report

VerifiedAdded on 2023/01/10

|15

|3812

|89

Report

AI Summary

This report delves into the core concepts of management accounting, exploring various systems and their benefits, including cost accounting, inventory management, and job costing. It examines different reporting methods such as inventory reports, budget reports, and job cost reports, providing insights into their application within organizations. The report critically evaluates management accounting systems and reporting, demonstrating their role in organizational success and financial problem-solving. It analyzes the application of techniques like marginal and absorption costing, including detailed calculations and interpretations. Furthermore, the report discusses planning tools for budgetary control, comparing how organizations adapt management accounting systems to address financial challenges and achieve sustainable success. The analysis also considers the break-even point and margin of safety. Finally, the report concludes with a summary of the key findings and their implications for effective financial management within organizations. This report is a comprehensive resource for students, offering a detailed overview of management accounting principles and their practical applications.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

P1 Different management accounting systems and their benefits...............................................1

P2 Different methods used for MA reporting .............................................................................3

M1 & D1 Critical evaluation of MA system and reporting along with application....................4

P3 Application of different types of management accounting techniques..................................5

P4 Types of planning tools for exercising budgetary control......................................................9

P5 & M4 Comparing organisation adapting the MA systems for responding to financial

problems and leading organisation towards success. ................................................................10

D3 Evaluating planning tool for resolving financial issues for sustainable success. ................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

P1 Different management accounting systems and their benefits...............................................1

P2 Different methods used for MA reporting .............................................................................3

M1 & D1 Critical evaluation of MA system and reporting along with application....................4

P3 Application of different types of management accounting techniques..................................5

P4 Types of planning tools for exercising budgetary control......................................................9

P5 & M4 Comparing organisation adapting the MA systems for responding to financial

problems and leading organisation towards success. ................................................................10

D3 Evaluating planning tool for resolving financial issues for sustainable success. ................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

MA can be defined as accounting process including combination of the non financial and

financial statements to enable organisations for making effective decisions. The information

generated by the managers to take different activities and operations for controlling the costs.

Next Plc is international footwear, clothing and the home product retailer which is

headquartered at Enderby, Leicestershire. It has nearly nearly 700 stores and around 500 are

located in UK and 200 in Asia, Europe and Middle east. It is largest retailer of clothes by sales in

UK. Company is listed in London Stock exchange. Report will provide about the MA concepts

and systems used by managers. It will also include the MA reporting systems and different types

of costing techniques used. Further it will provide about the budgetary planning tools and use of

different tools in solving the financial problems.

MAIN BODY

P1 Different management accounting systems and their benefits.

MA refers to process involving presentation of the financial information regarding the

different operations of business to manage the internal working of organisation. It involves

application of professional & knowledge skills for formulating the accounting and financial

information that helps the management of company for planning, framing policies, strategies,

and to control operations of enterprise. MA enables management to take decisions that are most

beneficial for the entity.

Difference between management and financial accounting

MA is of internal use of company to take business decisions where financial accounting

aims at providing information to external users of the business such as stakeholders.

Organisation is not required to follow any set standard in MA reports while financial accounting

reports are prepared using set standards (Jermias, Gani and Juliana, 2018). MA reports are for

internal use therefore no audit where financial reports are required to be audited before they are

issued for public use.

Different MA systems and essential requirements

Cost Accounting systems

This refers to MA systems that keep record of all the transactions carried out by the

organisation related with production. The system helps company in tracing the costs related with

1

MA can be defined as accounting process including combination of the non financial and

financial statements to enable organisations for making effective decisions. The information

generated by the managers to take different activities and operations for controlling the costs.

Next Plc is international footwear, clothing and the home product retailer which is

headquartered at Enderby, Leicestershire. It has nearly nearly 700 stores and around 500 are

located in UK and 200 in Asia, Europe and Middle east. It is largest retailer of clothes by sales in

UK. Company is listed in London Stock exchange. Report will provide about the MA concepts

and systems used by managers. It will also include the MA reporting systems and different types

of costing techniques used. Further it will provide about the budgetary planning tools and use of

different tools in solving the financial problems.

MAIN BODY

P1 Different management accounting systems and their benefits.

MA refers to process involving presentation of the financial information regarding the

different operations of business to manage the internal working of organisation. It involves

application of professional & knowledge skills for formulating the accounting and financial

information that helps the management of company for planning, framing policies, strategies,

and to control operations of enterprise. MA enables management to take decisions that are most

beneficial for the entity.

Difference between management and financial accounting

MA is of internal use of company to take business decisions where financial accounting

aims at providing information to external users of the business such as stakeholders.

Organisation is not required to follow any set standard in MA reports while financial accounting

reports are prepared using set standards (Jermias, Gani and Juliana, 2018). MA reports are for

internal use therefore no audit where financial reports are required to be audited before they are

issued for public use.

Different MA systems and essential requirements

Cost Accounting systems

This refers to MA systems that keep record of all the transactions carried out by the

organisation related with production. The system helps company in tracing the costs related with

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

each product being manufactured. It is essential for the business to evaluate costs to determine

the profit margins and costs of products.

Requirements

Cost accounting system is required for tracing the costs that are incurred at different

stages of manufacturing the product. The system enables managers in producing goods and

services at minimum cost and adequate profits.

Benefits

Managers could identify productive and unproductive exercises of processes.

Cost information provides the managers to make important strategic and operational

decisions. Cost accounting allows company to exercise control over increasing costs applying cost

efficient techniques.

Application

This system is applied by the manufacturing concerns to appropriately and effectively

record and implement the various costs in relation with the business production of goods and

services.

Inventory Management System

The system looks over each item of the stock. It plays essential role to assess needs

regarding the raw materials and other components used to produce the goods and

services(Abernethy and Wallis, 2019). This system provides a defined framework regarding the

management of inventory of the organisation.

Requirements

IMS is essential for the management to have record of each and every inventory items

from capital assets, raw material to other supplies of the company. It has automated the process

of ordering.

Benefits

It assists in managing the inventory stocks of company adequately.

Management could identify the frequency of inventory movement to make future

forecasting. It helps the company in saving and reducing its carrying cost of inventory.

Application

2

the profit margins and costs of products.

Requirements

Cost accounting system is required for tracing the costs that are incurred at different

stages of manufacturing the product. The system enables managers in producing goods and

services at minimum cost and adequate profits.

Benefits

Managers could identify productive and unproductive exercises of processes.

Cost information provides the managers to make important strategic and operational

decisions. Cost accounting allows company to exercise control over increasing costs applying cost

efficient techniques.

Application

This system is applied by the manufacturing concerns to appropriately and effectively

record and implement the various costs in relation with the business production of goods and

services.

Inventory Management System

The system looks over each item of the stock. It plays essential role to assess needs

regarding the raw materials and other components used to produce the goods and

services(Abernethy and Wallis, 2019). This system provides a defined framework regarding the

management of inventory of the organisation.

Requirements

IMS is essential for the management to have record of each and every inventory items

from capital assets, raw material to other supplies of the company. It has automated the process

of ordering.

Benefits

It assists in managing the inventory stocks of company adequately.

Management could identify the frequency of inventory movement to make future

forecasting. It helps the company in saving and reducing its carrying cost of inventory.

Application

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The system is applied in the organisation to have complete record of all the inventories

and their consumption in the process. This is required for maintaining safety stock and making

timely orders.

Job Costing System

JC system refers to practice of gathering the information regarding the costs associated

with specific job or the production. The information related to cost of producing particular job is

required by the business on special orders from customers. JC system is very useful system as it

enables the company to identify the costs related to each costs separately.

Requirements

The systems is very essential for the organisation as it provides detailed information

regarding each cost of job such as raw materials, labour and overheads. It enables the company

to quote price of each job separately.

Benefits

It supports the business to assist costs of every job individually.

This helps the company to determine the cost margins and profit levels. The systems helps management in allocating the cost to different accounts and jobs

specifically and appropriately.

Application

JC system is applied by the organisation for identifying the cost of producing a specific

job on special requirements of the client. It determines the prices to be charged over specific

jobs.

P2 Different methods used for MA reporting

There are different types of MA reports that are used by the organisation for providing

information related to different operations.

Inventory Report

The report contains information regarding all the inventory stocks of business. It

provided complete information regarding the quantity of purchases, frequency of purchases and

the rates at which inventory is purchased. Management analyses the inventory stocks are capable

to meet the requirement of specified period or not. The information provided by the inventory

reports enables the management in taking future decisions (Bui and De Villiers, 2017). It also

3

and their consumption in the process. This is required for maintaining safety stock and making

timely orders.

Job Costing System

JC system refers to practice of gathering the information regarding the costs associated

with specific job or the production. The information related to cost of producing particular job is

required by the business on special orders from customers. JC system is very useful system as it

enables the company to identify the costs related to each costs separately.

Requirements

The systems is very essential for the organisation as it provides detailed information

regarding each cost of job such as raw materials, labour and overheads. It enables the company

to quote price of each job separately.

Benefits

It supports the business to assist costs of every job individually.

This helps the company to determine the cost margins and profit levels. The systems helps management in allocating the cost to different accounts and jobs

specifically and appropriately.

Application

JC system is applied by the organisation for identifying the cost of producing a specific

job on special requirements of the client. It determines the prices to be charged over specific

jobs.

P2 Different methods used for MA reporting

There are different types of MA reports that are used by the organisation for providing

information related to different operations.

Inventory Report

The report contains information regarding all the inventory stocks of business. It

provided complete information regarding the quantity of purchases, frequency of purchases and

the rates at which inventory is purchased. Management analyses the inventory stocks are capable

to meet the requirement of specified period or not. The information provided by the inventory

reports enables the management in taking future decisions (Bui and De Villiers, 2017). It also

3

presents the consumption and wastage figures in production so that adequate steps could be

taken by the entity and for framing the strategies to reduce the costs and wastage.

Budget Report

Budget report could be stated as one of the important report for the management. It could

be defined as standard document containing all the information regarding income and

expenditures of the specific period. Budget report is prepared by company analysing the previous

trends and reviewing the previous budgets and making adjustments related to the current

situation. It is used by the management for comparing the actual and budgeted figures of the

organisation and to identify the variances (Endrikat, Hartmann and Schreck, 2017). On the basis

of variances effective control procedures are adopted for reducing the variances from the

organisation.

Job Cost Report

The report is used to evaluate projects of company against set standards. The work

includes evaluation of total cost in a specified project as against the estimated revenues. The

reports of job costing are used for evaluating profitability associated with every job undertaken.

It helps Next plc in identifying jobs that are profitable for the entity so that it could pay attention

over such jobs. Report provides all the information related to different jobs performed by the

organisation.

M1 & D1 Critical evaluation of MA system and reporting along with application.

Various systems of MA are used by company to help them in running operations

smoothly and effectively. MA systems enables firm to assist the organisation to attain the desired

goals and objectives of earning adequate profits at minimum cost. Integration of the MA systems

& reporting results in integrated system that enables the management in having effective

management of various operations and assessing the success achieved using information

provided by MA reports. It provides information of MA systems and its effectiveness in

achieving the organisational goals. The information provided by the systems helps in evaluating

efficiency and productivity of the organisation related to different operations undertaken by

company. MA report enable the management to give direction to different processes carried out

by organisation (Herschung, Mahlendorf and Weber, 2018). It is essential for the business to

make effective utilisation of the resources of the entity using different systems and reports.

4

taken by the entity and for framing the strategies to reduce the costs and wastage.

Budget Report

Budget report could be stated as one of the important report for the management. It could

be defined as standard document containing all the information regarding income and

expenditures of the specific period. Budget report is prepared by company analysing the previous

trends and reviewing the previous budgets and making adjustments related to the current

situation. It is used by the management for comparing the actual and budgeted figures of the

organisation and to identify the variances (Endrikat, Hartmann and Schreck, 2017). On the basis

of variances effective control procedures are adopted for reducing the variances from the

organisation.

Job Cost Report

The report is used to evaluate projects of company against set standards. The work

includes evaluation of total cost in a specified project as against the estimated revenues. The

reports of job costing are used for evaluating profitability associated with every job undertaken.

It helps Next plc in identifying jobs that are profitable for the entity so that it could pay attention

over such jobs. Report provides all the information related to different jobs performed by the

organisation.

M1 & D1 Critical evaluation of MA system and reporting along with application.

Various systems of MA are used by company to help them in running operations

smoothly and effectively. MA systems enables firm to assist the organisation to attain the desired

goals and objectives of earning adequate profits at minimum cost. Integration of the MA systems

& reporting results in integrated system that enables the management in having effective

management of various operations and assessing the success achieved using information

provided by MA reports. It provides information of MA systems and its effectiveness in

achieving the organisational goals. The information provided by the systems helps in evaluating

efficiency and productivity of the organisation related to different operations undertaken by

company. MA report enable the management to give direction to different processes carried out

by organisation (Herschung, Mahlendorf and Weber, 2018). It is essential for the business to

make effective utilisation of the resources of the entity using different systems and reports.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

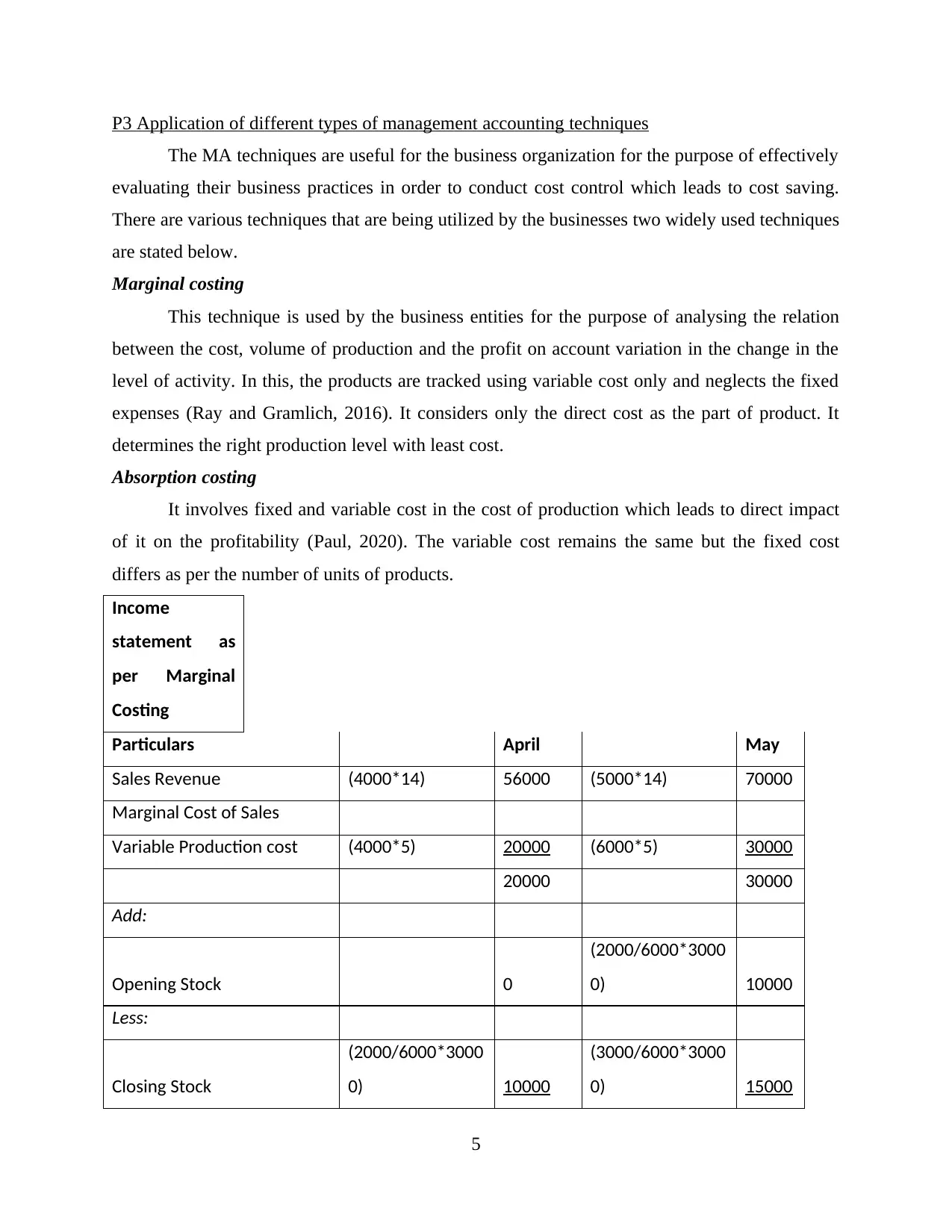

P3 Application of different types of management accounting techniques

The MA techniques are useful for the business organization for the purpose of effectively

evaluating their business practices in order to conduct cost control which leads to cost saving.

There are various techniques that are being utilized by the businesses two widely used techniques

are stated below.

Marginal costing

This technique is used by the business entities for the purpose of analysing the relation

between the cost, volume of production and the profit on account variation in the change in the

level of activity. In this, the products are tracked using variable cost only and neglects the fixed

expenses (Ray and Gramlich, 2016). It considers only the direct cost as the part of product. It

determines the right production level with least cost.

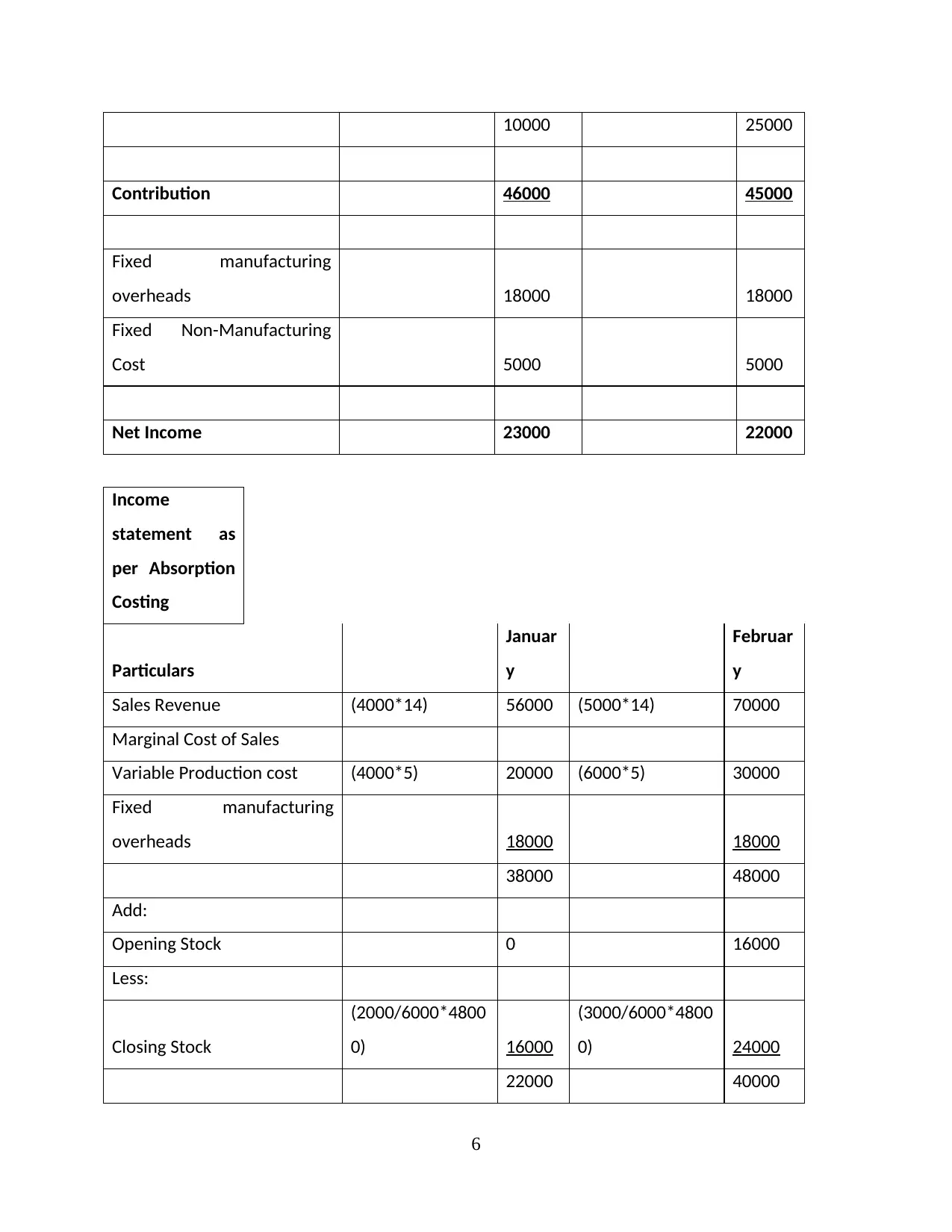

Absorption costing

It involves fixed and variable cost in the cost of production which leads to direct impact

of it on the profitability (Paul, 2020). The variable cost remains the same but the fixed cost

differs as per the number of units of products.

Income

statement as

per Marginal

Costing

Particulars April May

Sales Revenue (4000*14) 56000 (5000*14) 70000

Marginal Cost of Sales

Variable Production cost (4000*5) 20000 (6000*5) 30000

20000 30000

Add:

Opening Stock 0

(2000/6000*3000

0) 10000

Less:

Closing Stock

(2000/6000*3000

0) 10000

(3000/6000*3000

0) 15000

5

The MA techniques are useful for the business organization for the purpose of effectively

evaluating their business practices in order to conduct cost control which leads to cost saving.

There are various techniques that are being utilized by the businesses two widely used techniques

are stated below.

Marginal costing

This technique is used by the business entities for the purpose of analysing the relation

between the cost, volume of production and the profit on account variation in the change in the

level of activity. In this, the products are tracked using variable cost only and neglects the fixed

expenses (Ray and Gramlich, 2016). It considers only the direct cost as the part of product. It

determines the right production level with least cost.

Absorption costing

It involves fixed and variable cost in the cost of production which leads to direct impact

of it on the profitability (Paul, 2020). The variable cost remains the same but the fixed cost

differs as per the number of units of products.

Income

statement as

per Marginal

Costing

Particulars April May

Sales Revenue (4000*14) 56000 (5000*14) 70000

Marginal Cost of Sales

Variable Production cost (4000*5) 20000 (6000*5) 30000

20000 30000

Add:

Opening Stock 0

(2000/6000*3000

0) 10000

Less:

Closing Stock

(2000/6000*3000

0) 10000

(3000/6000*3000

0) 15000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10000 25000

Contribution 46000 45000

Fixed manufacturing

overheads 18000 18000

Fixed Non-Manufacturing

Cost 5000 5000

Net Income 23000 22000

Income

statement as

per Absorption

Costing

Particulars

Januar

y

Februar

y

Sales Revenue (4000*14) 56000 (5000*14) 70000

Marginal Cost of Sales

Variable Production cost (4000*5) 20000 (6000*5) 30000

Fixed manufacturing

overheads 18000 18000

38000 48000

Add:

Opening Stock 0 16000

Less:

Closing Stock

(2000/6000*4800

0) 16000

(3000/6000*4800

0) 24000

22000 40000

6

Contribution 46000 45000

Fixed manufacturing

overheads 18000 18000

Fixed Non-Manufacturing

Cost 5000 5000

Net Income 23000 22000

Income

statement as

per Absorption

Costing

Particulars

Januar

y

Februar

y

Sales Revenue (4000*14) 56000 (5000*14) 70000

Marginal Cost of Sales

Variable Production cost (4000*5) 20000 (6000*5) 30000

Fixed manufacturing

overheads 18000 18000

38000 48000

Add:

Opening Stock 0 16000

Less:

Closing Stock

(2000/6000*4800

0) 16000

(3000/6000*4800

0) 24000

22000 40000

6

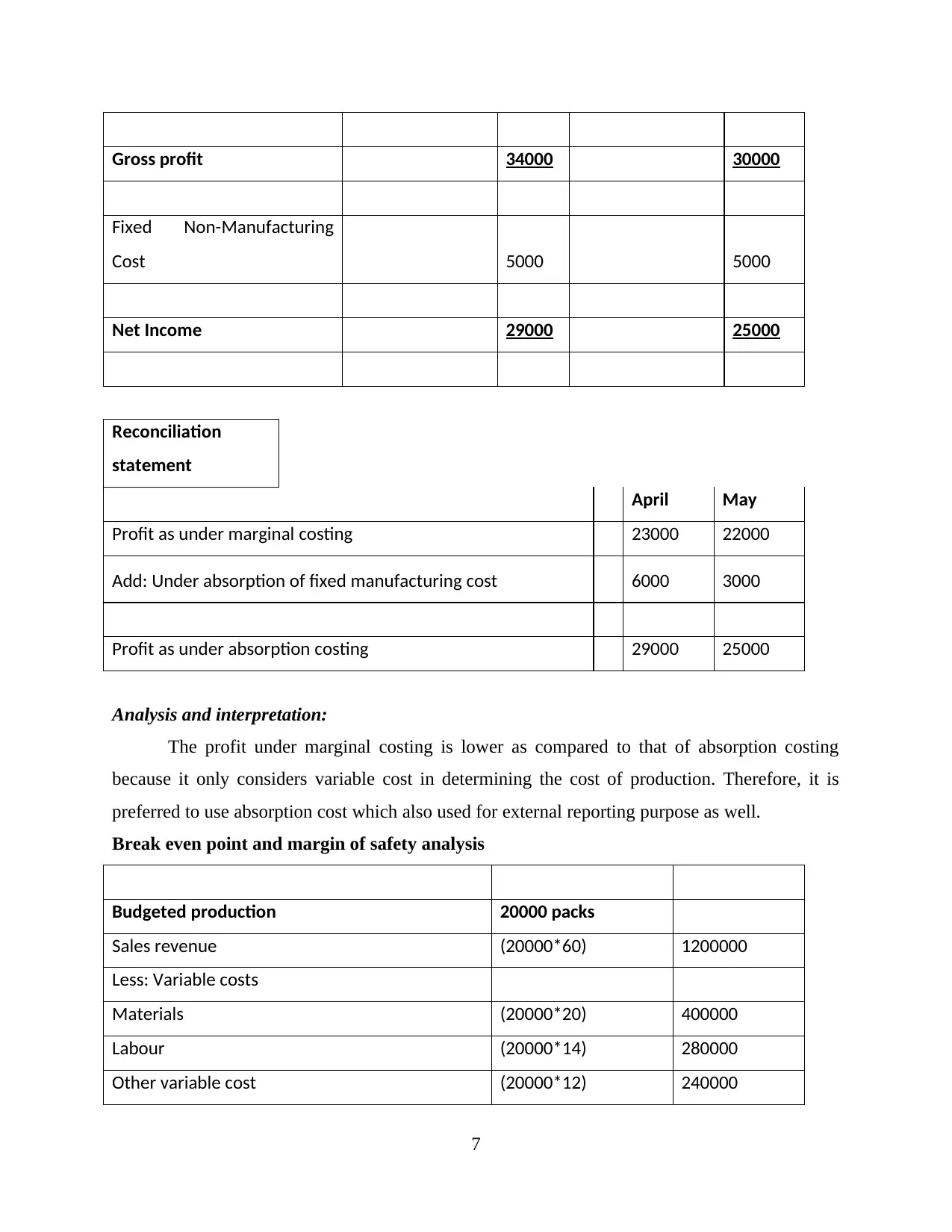

Gross profit 34000 30000

Fixed Non-Manufacturing

Cost 5000 5000

Net Income 29000 25000

Reconciliation

statement

April May

Profit as under marginal costing 23000 22000

Add: Under absorption of fixed manufacturing cost 6000 3000

Profit as under absorption costing 29000 25000

Analysis and interpretation:

The profit under marginal costing is lower as compared to that of absorption costing

because it only considers variable cost in determining the cost of production. Therefore, it is

preferred to use absorption cost which also used for external reporting purpose as well.

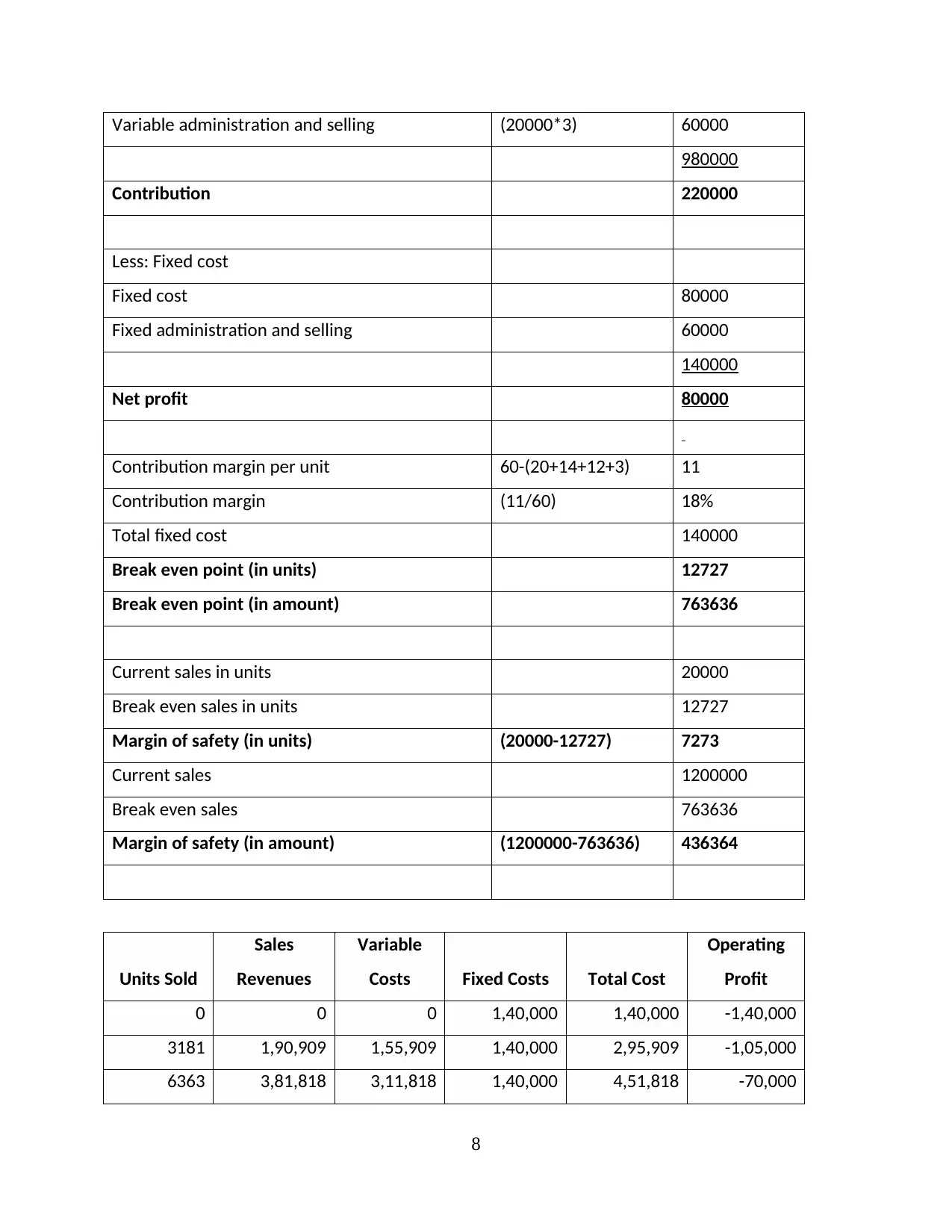

Break even point and margin of safety analysis

Budgeted production 20000 packs

Sales revenue (20000*60) 1200000

Less: Variable costs

Materials (20000*20) 400000

Labour (20000*14) 280000

Other variable cost (20000*12) 240000

7

Fixed Non-Manufacturing

Cost 5000 5000

Net Income 29000 25000

Reconciliation

statement

April May

Profit as under marginal costing 23000 22000

Add: Under absorption of fixed manufacturing cost 6000 3000

Profit as under absorption costing 29000 25000

Analysis and interpretation:

The profit under marginal costing is lower as compared to that of absorption costing

because it only considers variable cost in determining the cost of production. Therefore, it is

preferred to use absorption cost which also used for external reporting purpose as well.

Break even point and margin of safety analysis

Budgeted production 20000 packs

Sales revenue (20000*60) 1200000

Less: Variable costs

Materials (20000*20) 400000

Labour (20000*14) 280000

Other variable cost (20000*12) 240000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variable administration and selling (20000*3) 60000

980000

Contribution 220000

Less: Fixed cost

Fixed cost 80000

Fixed administration and selling 60000

140000

Net profit 80000

Contribution margin per unit 60-(20+14+12+3) 11

Contribution margin (11/60) 18%

Total fixed cost 140000

Break even point (in units) 12727

Break even point (in amount) 763636

Current sales in units 20000

Break even sales in units 12727

Margin of safety (in units) (20000-12727) 7273

Current sales 1200000

Break even sales 763636

Margin of safety (in amount) (1200000-763636) 436364

Units Sold

Sales

Revenues

Variable

Costs Fixed Costs Total Cost

Operating

Profit

0 0 0 1,40,000 1,40,000 -1,40,000

3181 1,90,909 1,55,909 1,40,000 2,95,909 -1,05,000

6363 3,81,818 3,11,818 1,40,000 4,51,818 -70,000

8

980000

Contribution 220000

Less: Fixed cost

Fixed cost 80000

Fixed administration and selling 60000

140000

Net profit 80000

Contribution margin per unit 60-(20+14+12+3) 11

Contribution margin (11/60) 18%

Total fixed cost 140000

Break even point (in units) 12727

Break even point (in amount) 763636

Current sales in units 20000

Break even sales in units 12727

Margin of safety (in units) (20000-12727) 7273

Current sales 1200000

Break even sales 763636

Margin of safety (in amount) (1200000-763636) 436364

Units Sold

Sales

Revenues

Variable

Costs Fixed Costs Total Cost

Operating

Profit

0 0 0 1,40,000 1,40,000 -1,40,000

3181 1,90,909 1,55,909 1,40,000 2,95,909 -1,05,000

6363 3,81,818 3,11,818 1,40,000 4,51,818 -70,000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

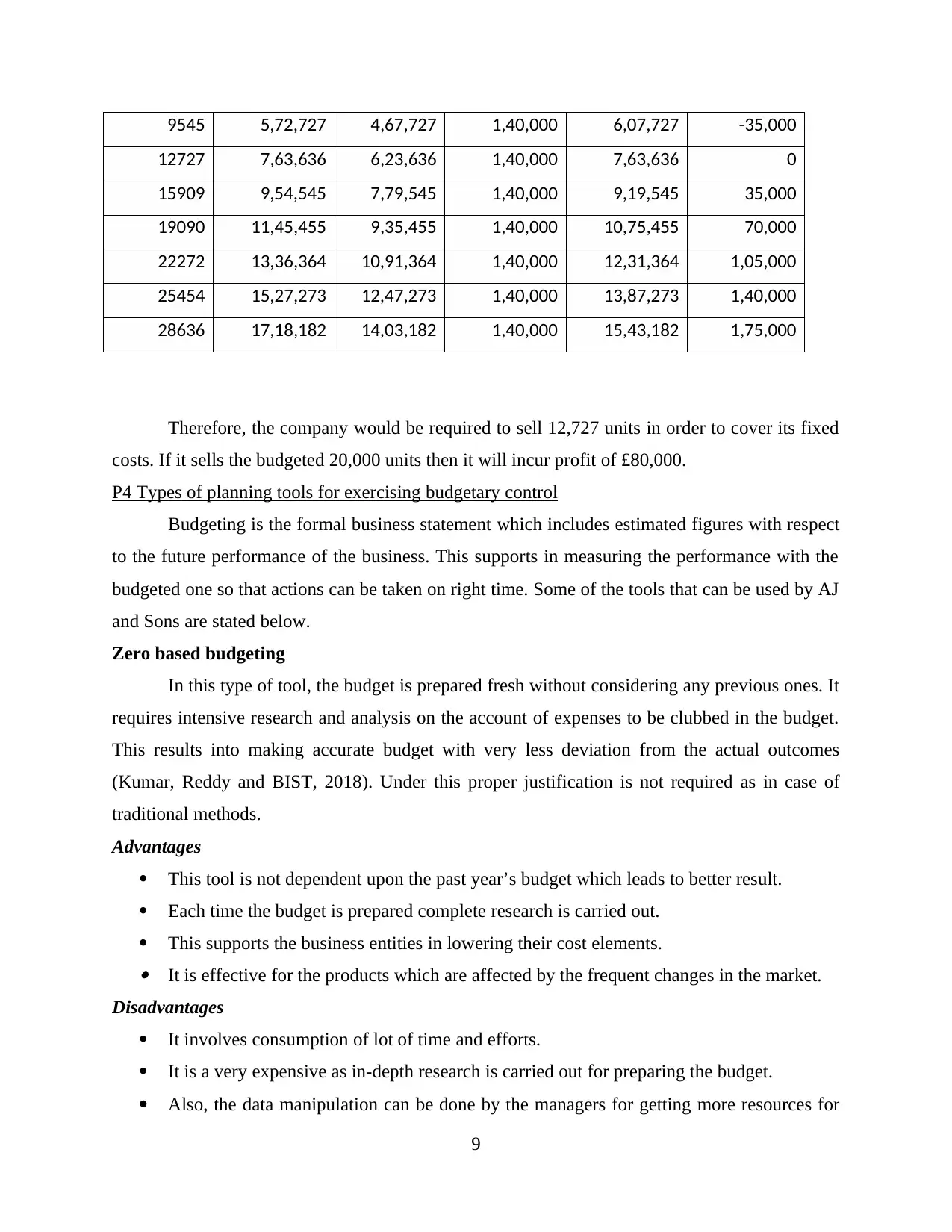

9545 5,72,727 4,67,727 1,40,000 6,07,727 -35,000

12727 7,63,636 6,23,636 1,40,000 7,63,636 0

15909 9,54,545 7,79,545 1,40,000 9,19,545 35,000

19090 11,45,455 9,35,455 1,40,000 10,75,455 70,000

22272 13,36,364 10,91,364 1,40,000 12,31,364 1,05,000

25454 15,27,273 12,47,273 1,40,000 13,87,273 1,40,000

28636 17,18,182 14,03,182 1,40,000 15,43,182 1,75,000

Therefore, the company would be required to sell 12,727 units in order to cover its fixed

costs. If it sells the budgeted 20,000 units then it will incur profit of £80,000.

P4 Types of planning tools for exercising budgetary control

Budgeting is the formal business statement which includes estimated figures with respect

to the future performance of the business. This supports in measuring the performance with the

budgeted one so that actions can be taken on right time. Some of the tools that can be used by AJ

and Sons are stated below.

Zero based budgeting

In this type of tool, the budget is prepared fresh without considering any previous ones. It

requires intensive research and analysis on the account of expenses to be clubbed in the budget.

This results into making accurate budget with very less deviation from the actual outcomes

(Kumar, Reddy and BIST, 2018). Under this proper justification is not required as in case of

traditional methods.

Advantages

This tool is not dependent upon the past year’s budget which leads to better result.

Each time the budget is prepared complete research is carried out.

This supports the business entities in lowering their cost elements. It is effective for the products which are affected by the frequent changes in the market.

Disadvantages

It involves consumption of lot of time and efforts.

It is a very expensive as in-depth research is carried out for preparing the budget.

Also, the data manipulation can be done by the managers for getting more resources for

9

12727 7,63,636 6,23,636 1,40,000 7,63,636 0

15909 9,54,545 7,79,545 1,40,000 9,19,545 35,000

19090 11,45,455 9,35,455 1,40,000 10,75,455 70,000

22272 13,36,364 10,91,364 1,40,000 12,31,364 1,05,000

25454 15,27,273 12,47,273 1,40,000 13,87,273 1,40,000

28636 17,18,182 14,03,182 1,40,000 15,43,182 1,75,000

Therefore, the company would be required to sell 12,727 units in order to cover its fixed

costs. If it sells the budgeted 20,000 units then it will incur profit of £80,000.

P4 Types of planning tools for exercising budgetary control

Budgeting is the formal business statement which includes estimated figures with respect

to the future performance of the business. This supports in measuring the performance with the

budgeted one so that actions can be taken on right time. Some of the tools that can be used by AJ

and Sons are stated below.

Zero based budgeting

In this type of tool, the budget is prepared fresh without considering any previous ones. It

requires intensive research and analysis on the account of expenses to be clubbed in the budget.

This results into making accurate budget with very less deviation from the actual outcomes

(Kumar, Reddy and BIST, 2018). Under this proper justification is not required as in case of

traditional methods.

Advantages

This tool is not dependent upon the past year’s budget which leads to better result.

Each time the budget is prepared complete research is carried out.

This supports the business entities in lowering their cost elements. It is effective for the products which are affected by the frequent changes in the market.

Disadvantages

It involves consumption of lot of time and efforts.

It is a very expensive as in-depth research is carried out for preparing the budget.

Also, the data manipulation can be done by the managers for getting more resources for

9

their department.

Activity Based Budgeting

This budget created which is dependent upon the activities being carried out by the

business organization. It is completely based on the estimation in respect to the resources to be

used and production level to be generated (Cokins and Dybvig, 2018). The activity-based

budgeting helps in identifying the different types of costs and expenditures that may be incurred

in relation to the various business activities which is conducted in the manufacturing process.

Advantages

This tool is very simple to be implemented as it requires less time.

It provides support to the management in identifying any discrepancies in the production

activities and processes. This budget is prepared without considering any of the previous year’s budgets.

Disadvantages

For preparing this budget requires exercising professional knowledge and skills.

It is very costly at the time of implementation.

It is useful for the businesses where various activities are carried out.

Operational Budgets

This budget only involves the operational activities of the business. Estimated values are

provided taking into account the past year’s budget. It provides an estimated amount of income

and expenditure and other relevant cost in relation to operational activities. This tool provides

support to the organization for the purpose of effective allocation of financial resources among

the different functional units or departments of the organization.

Advantages

This budget can be easily created and also it is simple to understand.

Useful in appropriate distribution of the financial resources, resulting exercising control

over cost. Based on the set targets, the effective actions can eb taken to ensure that all the

requirements can be easily met.

Disadvantages

The operational budge is based on the previous year budget which leads to increase in

chances of errors and inaccurate figures.

10

Activity Based Budgeting

This budget created which is dependent upon the activities being carried out by the

business organization. It is completely based on the estimation in respect to the resources to be

used and production level to be generated (Cokins and Dybvig, 2018). The activity-based

budgeting helps in identifying the different types of costs and expenditures that may be incurred

in relation to the various business activities which is conducted in the manufacturing process.

Advantages

This tool is very simple to be implemented as it requires less time.

It provides support to the management in identifying any discrepancies in the production

activities and processes. This budget is prepared without considering any of the previous year’s budgets.

Disadvantages

For preparing this budget requires exercising professional knowledge and skills.

It is very costly at the time of implementation.

It is useful for the businesses where various activities are carried out.

Operational Budgets

This budget only involves the operational activities of the business. Estimated values are

provided taking into account the past year’s budget. It provides an estimated amount of income

and expenditure and other relevant cost in relation to operational activities. This tool provides

support to the organization for the purpose of effective allocation of financial resources among

the different functional units or departments of the organization.

Advantages

This budget can be easily created and also it is simple to understand.

Useful in appropriate distribution of the financial resources, resulting exercising control

over cost. Based on the set targets, the effective actions can eb taken to ensure that all the

requirements can be easily met.

Disadvantages

The operational budge is based on the previous year budget which leads to increase in

chances of errors and inaccurate figures.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.