Management Accounting Systems: Methods, Benefits, and Reporting

VerifiedAdded on 2021/01/01

|27

|7745

|354

Report

AI Summary

This report provides a comprehensive overview of management accounting, detailing its definition, purpose, and essential requirements within a business context. It explores various management accounting systems, including cost accounting, inventory management, and job costing, outlining their key functionalities and benefits. The report further delves into different management accounting reporting methods such as oral, written, and graphical presentations, evaluating their advantages and applications. It also examines the integration of these systems within an organization, emphasizing their role in enhancing efficiency, financial control, and profitability. Additionally, the report discusses the application of planning tools like budgetary control and how management accounting systems can address various financial challenges, ultimately aiming to assist managers in making informed decisions for sustained business success. The document includes detailed explanations of various costing techniques and their application in preparing financial reports. The content is based on the assignment brief provided. The report concludes with a discussion on the adoption of management accounting systems to respond to financial problems and provides a list of references.

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P 1 management accounting system and its essential requirements in business.........................1

P 2 Different methods of management accounting reporting.....................................................3

M1 Benefits of different management accounting systems and their applications in the

organisation.................................................................................................................................4

P3 Different types of costs and costing techniques and calculation of various costs to analyse

and interpret different costing techniques and preparing income statements.............................6

M2 Description of costing techniques and using these for preparation of financial reporting

documents.................................................................................................................................10

P4 advantages and disadvantages of different planning tools of budgetary control.................16

P5 Adoption of management accounting systems to respond various financial problems. .....18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................1

P 1 management accounting system and its essential requirements in business.........................1

P 2 Different methods of management accounting reporting.....................................................3

M1 Benefits of different management accounting systems and their applications in the

organisation.................................................................................................................................4

P3 Different types of costs and costing techniques and calculation of various costs to analyse

and interpret different costing techniques and preparing income statements.............................6

M2 Description of costing techniques and using these for preparation of financial reporting

documents.................................................................................................................................10

P4 advantages and disadvantages of different planning tools of budgetary control.................16

P5 Adoption of management accounting systems to respond various financial problems. .....18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION

Management accounting is the systematic presentation of financial activities in such a

manner that provides useful information to manager in taking rationale decisions. The purpose of

this accounting is to assist internal management in forming policies and strategies. The present

report will cover meaning, advantages and requirements of management accounting system. The

report will also shown the calculation of budgeted and actual costs by using different costing

techniques. Further, use of planning tools in management accounting for maintaining

profitability and sustainability of company will be discussed.

P 1 management accounting system and its essential requirements in business

Management accounting

Management accounting is a branch of accounting which helps the management in

taking managerial decision relating to the financial position of the company (Akhmetshin, E. M.

and Osadchy, E. A., 2015). It can be defined as applying the professional knowledge and skills in

preparation of the financial statements of the company so that they could provide relevant

information to the mangers in taking appropriate decisions and formulate the best policies for the

enhancement of business and increasing the financial position of the company.

Management accounting system

Management accounting system is a system of accounting which deals with the analysing

and controlling the internal system of the business including various resources of the business are

needed to operate the regular operations of the company. Management accounting system helps

the management in enhancing the overall capacity of the business in order to enhance its

efficiency and profitability.

Requirements of management accounting system

Management accounting system plays a vital role in the success of the company. Each

firm needs inclusion of a better management accounting system in order to enhance its financial

position over a time.

Types of management accounting system and their requirements

Cost accounting system, inventory accounting systems, job costing systems, price

optimization system, etc. are the various types of management accounting systems which could

1

Management accounting is the systematic presentation of financial activities in such a

manner that provides useful information to manager in taking rationale decisions. The purpose of

this accounting is to assist internal management in forming policies and strategies. The present

report will cover meaning, advantages and requirements of management accounting system. The

report will also shown the calculation of budgeted and actual costs by using different costing

techniques. Further, use of planning tools in management accounting for maintaining

profitability and sustainability of company will be discussed.

P 1 management accounting system and its essential requirements in business

Management accounting

Management accounting is a branch of accounting which helps the management in

taking managerial decision relating to the financial position of the company (Akhmetshin, E. M.

and Osadchy, E. A., 2015). It can be defined as applying the professional knowledge and skills in

preparation of the financial statements of the company so that they could provide relevant

information to the mangers in taking appropriate decisions and formulate the best policies for the

enhancement of business and increasing the financial position of the company.

Management accounting system

Management accounting system is a system of accounting which deals with the analysing

and controlling the internal system of the business including various resources of the business are

needed to operate the regular operations of the company. Management accounting system helps

the management in enhancing the overall capacity of the business in order to enhance its

efficiency and profitability.

Requirements of management accounting system

Management accounting system plays a vital role in the success of the company. Each

firm needs inclusion of a better management accounting system in order to enhance its financial

position over a time.

Types of management accounting system and their requirements

Cost accounting system, inventory accounting systems, job costing systems, price

optimization system, etc. are the various types of management accounting systems which could

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

be adopted by the company in order to enhance its capacity and efficiency at various departments

of the business. Key requirements of these management accounting system are as under:

cost accounting system

Cost accounting system deals with the analysing the cost efficiency of the business and

developing plans for the company in order to make it more cost efficien (Doluwarawaththa

Gamage, S. D. and Gooneratne, T., 2017)t. Management can identify cost incurred by the firm

on each product manufactured by the company. It helps in determining the selling price of the

product as well.

Requirements

This system of management accounting is required by the company as it helps

them in having better control over the cost of the company.

With the help of cost accounting system, business can determine cost incurred at

each level of production. It helps managers in identifying the wastage of cost at

each level and eliminate them.

This system helps in determining the cost of each product incurred by the firm.

Managers can determine the selling price of each product after adding set profit to

be earned by the company.

Inventory management system

It is the system which deals with the planning and controlling the inventory of the

company (Bedford, D. S., 2015). With the help of it, company can record the flow and

requirement of inventory in the firm. By maintaining the inventory accordingly company can

reduce the risk of insufficiency of the stock in the business.

Requirement

It leads it proper maintenance of record of the inventory.

This system is required by the manufacturing concerns, as with the help of it they can

identify the minimum requirement of the business to held the inventory for

eliminating the insufficiency or excess of the stock with the company.

Through inventory management system, business can record each movement of

inventory, whether it is within the business of outside the business. It results in

enhancement of efficiency of the company in context with the inventory.

Job costing system

2

of the business. Key requirements of these management accounting system are as under:

cost accounting system

Cost accounting system deals with the analysing the cost efficiency of the business and

developing plans for the company in order to make it more cost efficien (Doluwarawaththa

Gamage, S. D. and Gooneratne, T., 2017)t. Management can identify cost incurred by the firm

on each product manufactured by the company. It helps in determining the selling price of the

product as well.

Requirements

This system of management accounting is required by the company as it helps

them in having better control over the cost of the company.

With the help of cost accounting system, business can determine cost incurred at

each level of production. It helps managers in identifying the wastage of cost at

each level and eliminate them.

This system helps in determining the cost of each product incurred by the firm.

Managers can determine the selling price of each product after adding set profit to

be earned by the company.

Inventory management system

It is the system which deals with the planning and controlling the inventory of the

company (Bedford, D. S., 2015). With the help of it, company can record the flow and

requirement of inventory in the firm. By maintaining the inventory accordingly company can

reduce the risk of insufficiency of the stock in the business.

Requirement

It leads it proper maintenance of record of the inventory.

This system is required by the manufacturing concerns, as with the help of it they can

identify the minimum requirement of the business to held the inventory for

eliminating the insufficiency or excess of the stock with the company.

Through inventory management system, business can record each movement of

inventory, whether it is within the business of outside the business. It results in

enhancement of efficiency of the company in context with the inventory.

Job costing system

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is the system with the help of which company can determine cost incurred by the

company in performing each job or manufacturing a particular lot of the product or services.

Requirement

Job costing system is required by those companies which are engaged with

manufacturing the product or services as per the requirement of its customers.

Business concerns required this system of accounting if they want to determine the

cost of each type of product of services manufactured by them.

With the help of this system they can also determine the selling price of the

customised product or services by additing the set profit of the company in order to

achieve the organisational objective of gaining profit from the products.

Critical evaluation of management accounting system and reporting

From the above analysis, it can be evaluated that involvement of management accounting

system can help the company in maintaining an effective control over all the financial transations

of the business. Although, for the purpose of adopting management accounting system, the

business needs to involve huge cost in the business.

Further, maintenance of management accounting reports could help the managers in

effectively analysing the actual position of the business and developing their strategies and plans

accordingly. On the other hand, for preparing the management accounting reports, company

needs to appoint professional accountants, that may increase the cost of company.

In this order, a company should adopt management accounting systems and maintain its

reports as well. As, although both involves a huge cost, but the company can recover the cost and

generate additional profits with effective management.

P 2 Different methods of management accounting reporting

Management reporting

Management reporting is a process of management in which deals with

documentation of all the relevant information to the managers including finacial reports and

reports of different accounting systems of the business (Collis, J. and Hussey, R., 2017).

Management reporting helps the management in financial control, project management,

presentation of business in business meetings, etc.

Methods of management reporting

3

company in performing each job or manufacturing a particular lot of the product or services.

Requirement

Job costing system is required by those companies which are engaged with

manufacturing the product or services as per the requirement of its customers.

Business concerns required this system of accounting if they want to determine the

cost of each type of product of services manufactured by them.

With the help of this system they can also determine the selling price of the

customised product or services by additing the set profit of the company in order to

achieve the organisational objective of gaining profit from the products.

Critical evaluation of management accounting system and reporting

From the above analysis, it can be evaluated that involvement of management accounting

system can help the company in maintaining an effective control over all the financial transations

of the business. Although, for the purpose of adopting management accounting system, the

business needs to involve huge cost in the business.

Further, maintenance of management accounting reports could help the managers in

effectively analysing the actual position of the business and developing their strategies and plans

accordingly. On the other hand, for preparing the management accounting reports, company

needs to appoint professional accountants, that may increase the cost of company.

In this order, a company should adopt management accounting systems and maintain its

reports as well. As, although both involves a huge cost, but the company can recover the cost and

generate additional profits with effective management.

P 2 Different methods of management accounting reporting

Management reporting

Management reporting is a process of management in which deals with

documentation of all the relevant information to the managers including finacial reports and

reports of different accounting systems of the business (Collis, J. and Hussey, R., 2017).

Management reporting helps the management in financial control, project management,

presentation of business in business meetings, etc.

Methods of management reporting

3

There are various ways to present the management reports like, written, oral, graphical,

group discussions, etc. managers can make their management report using any of these methods.

Oral reporting

It is the simplest method of transforming informations of business. In this method of

reporting, managers transfers all the informations in verbal form. Group discussions, meetings,

conversations are different ways to present the management reports in oral form. In addition, as

there is no proper record of these informations, theses are comparatively more flexible and easy

to change.

This method of reporting is the most cost efficient method among all the methods of

management accounting reporting. It also takes less time in conveying the information to the

audience. Further, managers can determine the response of the audience for they report through

their facial expressions.

Written reporting

It could be termed as the best method of reporting (Christopher, M., 2016). It is also most

common method of presenting the management reports. With the help of this method, company

can maintain all these reports for a period of long time. It also helps in maintain all the records

for the legal purpose as well.

Financial statements, income statements, balance sheets, cash flow statements, fund flow

statements etc. are various forms of maintaining the reports in written format. Written reports can

show the proper information about the business financial position, efficiency and all other

relevant informations which could help the managers in taking their managerial decisions.

There are various types of written reports like:

Accounts receivable reports: In these reports, the informations relating to all the unpaid

customers of the company. For example, With the help of these reports, the managers

can analyse the amount of debts over the business. In this regard, they can maintain

sufficiency of fund in the firm.

Budget reports: From these reports, managers can analyse the estimated operations of

the business. For example, It helps the managers in detecting various needs of the

business and maintaining the smooth running of all the operations as well.

4

group discussions, etc. managers can make their management report using any of these methods.

Oral reporting

It is the simplest method of transforming informations of business. In this method of

reporting, managers transfers all the informations in verbal form. Group discussions, meetings,

conversations are different ways to present the management reports in oral form. In addition, as

there is no proper record of these informations, theses are comparatively more flexible and easy

to change.

This method of reporting is the most cost efficient method among all the methods of

management accounting reporting. It also takes less time in conveying the information to the

audience. Further, managers can determine the response of the audience for they report through

their facial expressions.

Written reporting

It could be termed as the best method of reporting (Christopher, M., 2016). It is also most

common method of presenting the management reports. With the help of this method, company

can maintain all these reports for a period of long time. It also helps in maintain all the records

for the legal purpose as well.

Financial statements, income statements, balance sheets, cash flow statements, fund flow

statements etc. are various forms of maintaining the reports in written format. Written reports can

show the proper information about the business financial position, efficiency and all other

relevant informations which could help the managers in taking their managerial decisions.

There are various types of written reports like:

Accounts receivable reports: In these reports, the informations relating to all the unpaid

customers of the company. For example, With the help of these reports, the managers

can analyse the amount of debts over the business. In this regard, they can maintain

sufficiency of fund in the firm.

Budget reports: From these reports, managers can analyse the estimated operations of

the business. For example, It helps the managers in detecting various needs of the

business and maintaining the smooth running of all the operations as well.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job cost reports: This reports are prepared by those businesses that provides customised

goods and services to the customers. It helps the managers in setting the appropriate price

of the products and generate profit as per the objectives of the company. Inventory management reports : Inventory reports helps the managers in tracking the

flow of inventory in the business. With the help of these reports, the managers can detect

the need of inventories for maintaining the sufficiency. Further, with the help of theses

reports, the company can also eliminate the inventory wastage in the business.

Graphical reporting

In this method of reporting, informations of the business are presented in the form of

charts, diagrams, pictures, etc. (Gooneratne, T.N. and Hoque, Z., 2016). it could be termed as the

most attractive way or presenting the management reports. Further, this method of reporting also

leads in better understanding a better transforming the informations to the users.

It is the method which is used by the professionals in order to show their reports and

transfer all the informations to the audience. It also eliminates the confusion about the

information that need to be provided through this method. Bar diagrams, Pie charts, Break even

charts, flow charts, etc. are the most common ways of graphical presentation.

M1 Benefits of different management accounting systems and their applications in the

organisation

Integration of management accounting system

Management accounting system is important to be included in the managerial system of

the company. Cost accounting system, job costing system, inventory management systems,etc.

are various types of management accounting system. This system of management helps the

managers in having better control over the various departments and enhance their efficiency of

performance. Managerial accounting system also helps in properly detecting the inefficiency of

the business and its each departments as well.

Integration of management accounting system is important as it results in elimination of

all the inefficiency of the business by detecting them and developing managerial strategies and

plans accordingly (Ansoff, H.I. and et.al., 2019). Hence, by integrating management accounting

system in the business, managers can enhance the efficiency of the business, make the financial

position better and increase the profit generation capacity of the business.

5

goods and services to the customers. It helps the managers in setting the appropriate price

of the products and generate profit as per the objectives of the company. Inventory management reports : Inventory reports helps the managers in tracking the

flow of inventory in the business. With the help of these reports, the managers can detect

the need of inventories for maintaining the sufficiency. Further, with the help of theses

reports, the company can also eliminate the inventory wastage in the business.

Graphical reporting

In this method of reporting, informations of the business are presented in the form of

charts, diagrams, pictures, etc. (Gooneratne, T.N. and Hoque, Z., 2016). it could be termed as the

most attractive way or presenting the management reports. Further, this method of reporting also

leads in better understanding a better transforming the informations to the users.

It is the method which is used by the professionals in order to show their reports and

transfer all the informations to the audience. It also eliminates the confusion about the

information that need to be provided through this method. Bar diagrams, Pie charts, Break even

charts, flow charts, etc. are the most common ways of graphical presentation.

M1 Benefits of different management accounting systems and their applications in the

organisation

Integration of management accounting system

Management accounting system is important to be included in the managerial system of

the company. Cost accounting system, job costing system, inventory management systems,etc.

are various types of management accounting system. This system of management helps the

managers in having better control over the various departments and enhance their efficiency of

performance. Managerial accounting system also helps in properly detecting the inefficiency of

the business and its each departments as well.

Integration of management accounting system is important as it results in elimination of

all the inefficiency of the business by detecting them and developing managerial strategies and

plans accordingly (Ansoff, H.I. and et.al., 2019). Hence, by integrating management accounting

system in the business, managers can enhance the efficiency of the business, make the financial

position better and increase the profit generation capacity of the business.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages of each management accounting systems

Cost accounting, inventory management, job costing, etc. are various types of

management accounting system. There advantages are:

cost accounting system

This system provides various tools to mangers through which managers can have better

control over the cost of business like marginal costing, budgetary control, standard costing, etc.

Advantages

Majorly this method is helpful for the manufacturing concerns as through this system

they can evaluate cost incurred by each department at each level of production for the

purpose of detecting cost wastage.

It also helps in determining the future cost of the business which may help managers in

maintaining sufficiency of cash in the company.

This method helps in determining the price of each product as it could help in

determining each product's cost of the business.

Inventory management system

This system helps in effectively managing the stock in the company. In this system

managers can get the proper record of purchase, use and selling of inventory in the business

organisation.

Advantages

With this method, company can determine the minimum stock requirement of the

business (Otley, D., 2015). Maintaining at least that level of stock can eliminate the

probability of insufficiency of the inventory in business.

It enhances the efficiency of flow of inventory in the firm.

Further, this system also makes the company more cost effective.

Job costing system

This technique is mostly used by those business concerns which are engaged in

manufacturing the products or services as per the requirement of customers of which produces

the customised products.

Advantages

It helps in calculating the cost incurred for each type of product manufactured.

6

Cost accounting, inventory management, job costing, etc. are various types of

management accounting system. There advantages are:

cost accounting system

This system provides various tools to mangers through which managers can have better

control over the cost of business like marginal costing, budgetary control, standard costing, etc.

Advantages

Majorly this method is helpful for the manufacturing concerns as through this system

they can evaluate cost incurred by each department at each level of production for the

purpose of detecting cost wastage.

It also helps in determining the future cost of the business which may help managers in

maintaining sufficiency of cash in the company.

This method helps in determining the price of each product as it could help in

determining each product's cost of the business.

Inventory management system

This system helps in effectively managing the stock in the company. In this system

managers can get the proper record of purchase, use and selling of inventory in the business

organisation.

Advantages

With this method, company can determine the minimum stock requirement of the

business (Otley, D., 2015). Maintaining at least that level of stock can eliminate the

probability of insufficiency of the inventory in business.

It enhances the efficiency of flow of inventory in the firm.

Further, this system also makes the company more cost effective.

Job costing system

This technique is mostly used by those business concerns which are engaged in

manufacturing the products or services as per the requirement of customers of which produces

the customised products.

Advantages

It helps in calculating the cost incurred for each type of product manufactured.

6

With the helps of it management can also determine the efficiency of budgetary control

system of the company.

Company can also determine different prices of different products as per their

manufacturing process and pricing strategy of the whole organisation.

Price optimising system

This system of management accounting helps in determining the best price of any

product after analysing and comparing the pricing strategy of the organisation and the customers'

attitude for towards the product.

Advantages

It helps in setting up the best price of product which customer will pay happily and

through which organisation will achieve its objectives effectively as well.

This system also provides various alternatives to determine the bets price of the product

or services.

P3 Different types of costs and costing techniques and calculation of various costs to analyse and

interpret different costing techniques and preparing income statements

Cost

In terms of business, cost is the amount incurred by the business to manufacture any

product or getting any product or service for the purpose of further sales or to procure any

product for using it in the normal course of business (Mohamed, I.A., Kerosi, E. and Tirimba,

O.I., 2016). For example, material, labour, overheads, etc. Are the main costs of each company.

Role of costing

costing plays an important role in any business organisation like:

The main role of costing in the business is to determine the actual cost incurred by the

business during a period in order to calculate the actual profit of the company.

Costing also helps the managers in determining the optimistic price of the product so that

customers could be satisfied with it and company could achieve its profit earning goals as

well.

Further, it also helps managers in maintaining cost efficiency of the business concern.

It helps in determining the actual financial position of the firm to take appropriate

decisions for it.

Different types of costs

7

system of the company.

Company can also determine different prices of different products as per their

manufacturing process and pricing strategy of the whole organisation.

Price optimising system

This system of management accounting helps in determining the best price of any

product after analysing and comparing the pricing strategy of the organisation and the customers'

attitude for towards the product.

Advantages

It helps in setting up the best price of product which customer will pay happily and

through which organisation will achieve its objectives effectively as well.

This system also provides various alternatives to determine the bets price of the product

or services.

P3 Different types of costs and costing techniques and calculation of various costs to analyse and

interpret different costing techniques and preparing income statements

Cost

In terms of business, cost is the amount incurred by the business to manufacture any

product or getting any product or service for the purpose of further sales or to procure any

product for using it in the normal course of business (Mohamed, I.A., Kerosi, E. and Tirimba,

O.I., 2016). For example, material, labour, overheads, etc. Are the main costs of each company.

Role of costing

costing plays an important role in any business organisation like:

The main role of costing in the business is to determine the actual cost incurred by the

business during a period in order to calculate the actual profit of the company.

Costing also helps the managers in determining the optimistic price of the product so that

customers could be satisfied with it and company could achieve its profit earning goals as

well.

Further, it also helps managers in maintaining cost efficiency of the business concern.

It helps in determining the actual financial position of the firm to take appropriate

decisions for it.

Different types of costs

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mainly cost are of 3 types namely fixed costs, variable costs and semi variable costs.

Fixed costs

Those costs which do not vary with the variation of production of number of goods or

services. Company incurs these periodically (Kwarteng, A., 2018). They do not depend upon the

volume of production of the business. Rent, office salaries, etc. are the fixed cost of any business

concern.

Variable cost

These costs are also termed as per unit cost of the company, as they incurred by the firm

on per unit basis (Alami, S. and Boussetta, M., 2018). The total amount of variable costs varies

with the variation in the volume of production or services by the business. Direct material,

labour, packing costs, etc. are the various variable cost of a company.

Semi variable cost

These costs are the combination of both fixed and variable costs. Part of these costs

remains same periodically and other part keeps changing as per the change in the volume of the

production of company.

Product cost

Those costs which could be directly associated with the production of the company can

be termed as product cost (Walker, R.L. and et.al., 2016). It includes those costs which are

incurred directly to the product in the manufacturing process. For example, direct material, direct

labour, etc.

Period cost

Period costs are those which do not incur directly for the business. Rather, these costs are

associated with the period. Therefore, these are charged against the expenses of the company.

Selling expenses, advertisement expenses, etc. are the examples of period cost.

Marginal cost

Marginal cost can be defined as cost that would need to be incurred by the for

manufacturing one extra unit of the output.

Contribution

Contribution can be termed as the amount earned by the business by selling its product or

services after deducting all the direct costs incurred by it.

Absorption cost

8

Fixed costs

Those costs which do not vary with the variation of production of number of goods or

services. Company incurs these periodically (Kwarteng, A., 2018). They do not depend upon the

volume of production of the business. Rent, office salaries, etc. are the fixed cost of any business

concern.

Variable cost

These costs are also termed as per unit cost of the company, as they incurred by the firm

on per unit basis (Alami, S. and Boussetta, M., 2018). The total amount of variable costs varies

with the variation in the volume of production or services by the business. Direct material,

labour, packing costs, etc. are the various variable cost of a company.

Semi variable cost

These costs are the combination of both fixed and variable costs. Part of these costs

remains same periodically and other part keeps changing as per the change in the volume of the

production of company.

Product cost

Those costs which could be directly associated with the production of the company can

be termed as product cost (Walker, R.L. and et.al., 2016). It includes those costs which are

incurred directly to the product in the manufacturing process. For example, direct material, direct

labour, etc.

Period cost

Period costs are those which do not incur directly for the business. Rather, these costs are

associated with the period. Therefore, these are charged against the expenses of the company.

Selling expenses, advertisement expenses, etc. are the examples of period cost.

Marginal cost

Marginal cost can be defined as cost that would need to be incurred by the for

manufacturing one extra unit of the output.

Contribution

Contribution can be termed as the amount earned by the business by selling its product or

services after deducting all the direct costs incurred by it.

Absorption cost

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is the total amount incurred by the business in the production process including all the

indirect and direct expenses of the company for turning the raw materials into finished products.

Under absorption of overhead

Under absorption is a situation where overhead actually incurred by the company are

more than the amount of overheads predicted by the managers (Christian, D., 2018). This

situation indicated the inefficiency of the organisation.

Over absorption of overhead

This situation occurs when the actual overheads are incurred less than the amount

predicted by the managers. It shows the enhancement of efficiency of the business.

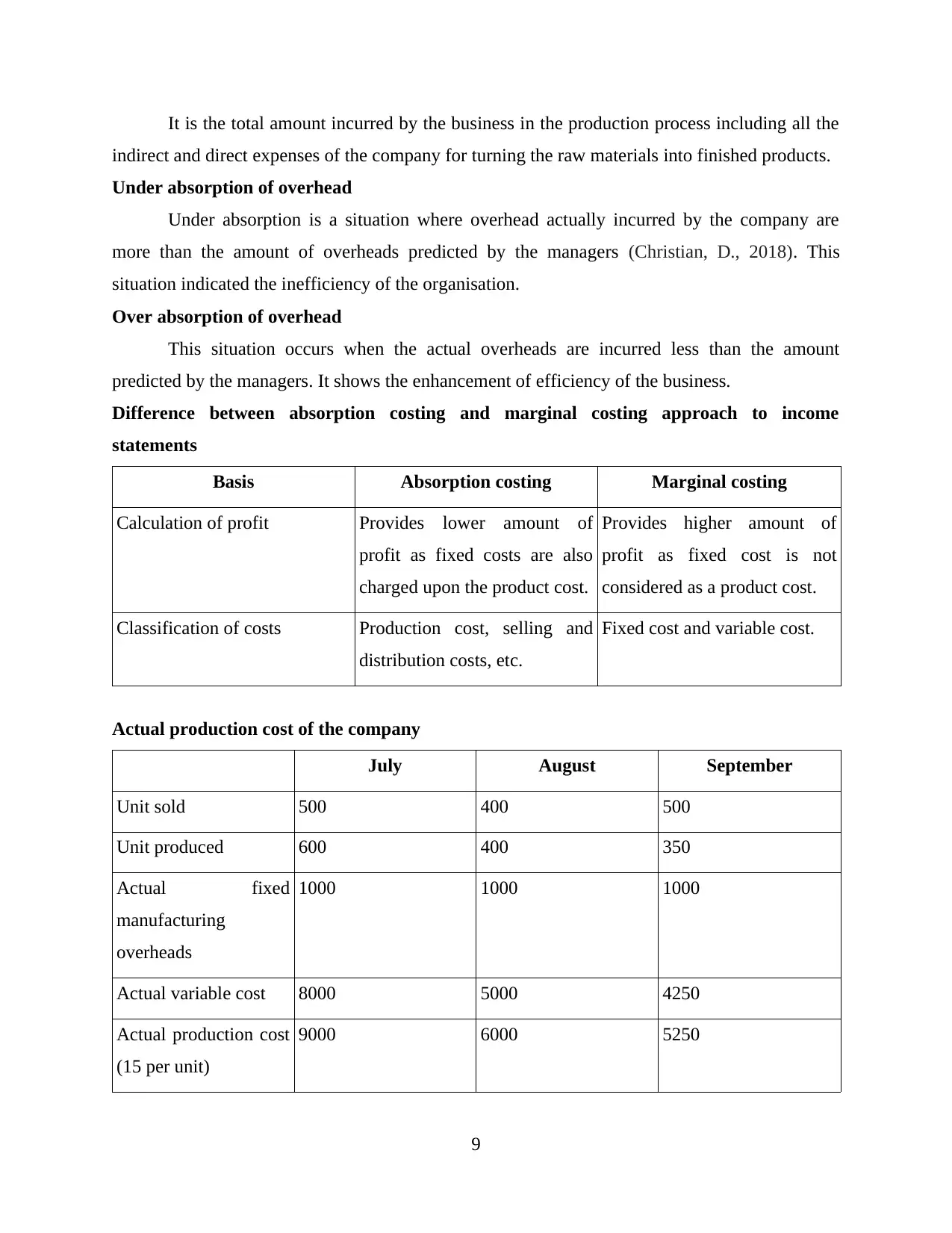

Difference between absorption costing and marginal costing approach to income

statements

Basis Absorption costing Marginal costing

Calculation of profit Provides lower amount of

profit as fixed costs are also

charged upon the product cost.

Provides higher amount of

profit as fixed cost is not

considered as a product cost.

Classification of costs Production cost, selling and

distribution costs, etc.

Fixed cost and variable cost.

Actual production cost of the company

July August September

Unit sold 500 400 500

Unit produced 600 400 350

Actual fixed

manufacturing

overheads

1000 1000 1000

Actual variable cost 8000 5000 4250

Actual production cost

(15 per unit)

9000 6000 5250

9

indirect and direct expenses of the company for turning the raw materials into finished products.

Under absorption of overhead

Under absorption is a situation where overhead actually incurred by the company are

more than the amount of overheads predicted by the managers (Christian, D., 2018). This

situation indicated the inefficiency of the organisation.

Over absorption of overhead

This situation occurs when the actual overheads are incurred less than the amount

predicted by the managers. It shows the enhancement of efficiency of the business.

Difference between absorption costing and marginal costing approach to income

statements

Basis Absorption costing Marginal costing

Calculation of profit Provides lower amount of

profit as fixed costs are also

charged upon the product cost.

Provides higher amount of

profit as fixed cost is not

considered as a product cost.

Classification of costs Production cost, selling and

distribution costs, etc.

Fixed cost and variable cost.

Actual production cost of the company

July August September

Unit sold 500 400 500

Unit produced 600 400 350

Actual fixed

manufacturing

overheads

1000 1000 1000

Actual variable cost 8000 5000 4250

Actual production cost

(15 per unit)

9000 6000 5250

9

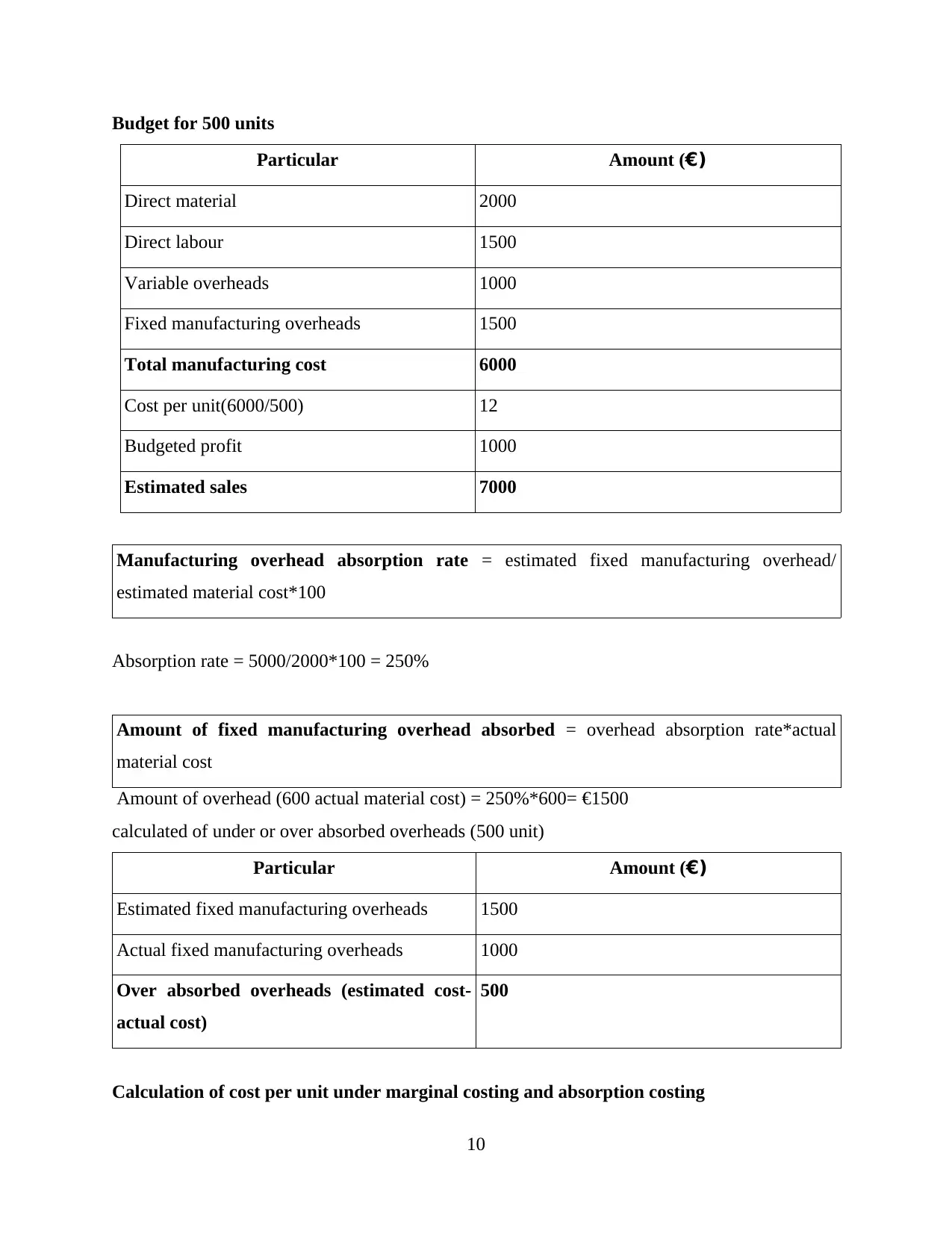

Budget for 500 units

Particular Amount (€)

Direct material 2000

Direct labour 1500

Variable overheads 1000

Fixed manufacturing overheads 1500

Total manufacturing cost 6000

Cost per unit(6000/500) 12

Budgeted profit 1000

Estimated sales 7000

Manufacturing overhead absorption rate = estimated fixed manufacturing overhead/

estimated material cost*100

Absorption rate = 5000/2000*100 = 250%

Amount of fixed manufacturing overhead absorbed = overhead absorption rate*actual

material cost

Amount of overhead (600 actual material cost) = 250%*600= €1500

calculated of under or over absorbed overheads (500 unit)

Particular Amount (€)

Estimated fixed manufacturing overheads 1500

Actual fixed manufacturing overheads 1000

Over absorbed overheads (estimated cost-

actual cost)

500

Calculation of cost per unit under marginal costing and absorption costing

10

Particular Amount (€)

Direct material 2000

Direct labour 1500

Variable overheads 1000

Fixed manufacturing overheads 1500

Total manufacturing cost 6000

Cost per unit(6000/500) 12

Budgeted profit 1000

Estimated sales 7000

Manufacturing overhead absorption rate = estimated fixed manufacturing overhead/

estimated material cost*100

Absorption rate = 5000/2000*100 = 250%

Amount of fixed manufacturing overhead absorbed = overhead absorption rate*actual

material cost

Amount of overhead (600 actual material cost) = 250%*600= €1500

calculated of under or over absorbed overheads (500 unit)

Particular Amount (€)

Estimated fixed manufacturing overheads 1500

Actual fixed manufacturing overheads 1000

Over absorbed overheads (estimated cost-

actual cost)

500

Calculation of cost per unit under marginal costing and absorption costing

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.