Management Accounting Project: Analysis of Costing Systems & Reports

VerifiedAdded on 2021/02/20

|13

|4272

|33

Project

AI Summary

This project report delves into the realm of management accounting, focusing on its application within a medium-sized UK manufacturing company, Roberts Metal Packaging. The report explores various aspects of management accounting, including cost accounting systems, job costing, and inventory management, highlighting their essential requirements and benefits. It examines different methods for management accounting reporting, such as budget reports, account receivable reports, cost managerial accounting reports, and performance reports, detailing their advantages and applicability within an organization. The report further evaluates the integration of management accounting systems and reporting within organizational processes, emphasizing the interrelation between cost accounting and budget reports. The project also includes calculations and analysis of financial statements within variable costing, as well as marginal and absorption costing under income statements, providing a comprehensive overview of management accounting practices and their impact on business decision-making.

PROJECT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS.................................................................................................................1

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

Part 1...........................................................................................................................................2

Part 2...........................................................................................................................................7

TASK 2............................................................................................................................................8

Part 1...........................................................................................................................................8

Part 2...........................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

1

TABLE OF CONTENTS.................................................................................................................1

INTRODUCTION...........................................................................................................................2

TASK 1............................................................................................................................................2

Part 1...........................................................................................................................................2

Part 2...........................................................................................................................................7

TASK 2............................................................................................................................................8

Part 1...........................................................................................................................................8

Part 2...........................................................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

1

INTRODUCTION

Management accounting is a tool of accounting which is prepared for the internal users

for executing critical decision making in business (Dyckman and Zeff, 2015). This report will lay

focus on medium sized manufacturing company of UK which is Roberts Metal Packaging. This

company provides metal packaging such as aluminium jars, lids, bottles, screw tops to clients of

Fast moving consumer goods. Roberts Metal Packaging employs 75 employees in their company

which holds plant of 30,000 square foot. This report will lay emphasis on management

accounting and essential requirement of management accounting of certain types like cost

account system, job costing system, etc.

The report will determine about methods which will be use by management accounting

reporting. These reports depict performance of company and their operations like budget report,

cost managerial accounting report, etc. Benefits of different system of management accounting

and their applicability in context of organisation will also be discussed. The evaluation of

management accounting system and management accounting reporting will be elaborated in this

report for integration of organisational process. Three different planning tools will be focused

which is used in management accounting. Portfolio of calculation along with financial

statements within variable costing will be calculated in this report. Marginal and absorption

costing under income statement will be disclose in the report.

TASK 1

Part 1

A. About management accounting and their essential requirements of different types of

management accounting.

Management accounting – The accounts prepared under management accounting is for

providing help to internal management of a company to analyse financial statements which

further assist them in executing decision making for a longer period in business (Parker and

Northcott, 2016). This concept enables effective planning for selecting the best alternative

activities for an organisation. Management accounting not only helps in decision making process

but also they help in controlling activities and performance evaluation.

Financial accounting – The financial accounting is different from management

accounting because it is prepared for the purpose of satisfying interest of external users like

2

Management accounting is a tool of accounting which is prepared for the internal users

for executing critical decision making in business (Dyckman and Zeff, 2015). This report will lay

focus on medium sized manufacturing company of UK which is Roberts Metal Packaging. This

company provides metal packaging such as aluminium jars, lids, bottles, screw tops to clients of

Fast moving consumer goods. Roberts Metal Packaging employs 75 employees in their company

which holds plant of 30,000 square foot. This report will lay emphasis on management

accounting and essential requirement of management accounting of certain types like cost

account system, job costing system, etc.

The report will determine about methods which will be use by management accounting

reporting. These reports depict performance of company and their operations like budget report,

cost managerial accounting report, etc. Benefits of different system of management accounting

and their applicability in context of organisation will also be discussed. The evaluation of

management accounting system and management accounting reporting will be elaborated in this

report for integration of organisational process. Three different planning tools will be focused

which is used in management accounting. Portfolio of calculation along with financial

statements within variable costing will be calculated in this report. Marginal and absorption

costing under income statement will be disclose in the report.

TASK 1

Part 1

A. About management accounting and their essential requirements of different types of

management accounting.

Management accounting – The accounts prepared under management accounting is for

providing help to internal management of a company to analyse financial statements which

further assist them in executing decision making for a longer period in business (Parker and

Northcott, 2016). This concept enables effective planning for selecting the best alternative

activities for an organisation. Management accounting not only helps in decision making process

but also they help in controlling activities and performance evaluation.

Financial accounting – The financial accounting is different from management

accounting because it is prepared for the purpose of satisfying interest of external users like

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

creditors, shareholders, etc (Correa and Larrinaga, 2015). The concept of financial accounting is

an accounting branch which track transactions of business.

The different types of management accounting system and their essential requirements

will be expressed as follows :

Cost accounting system – The cost accounting system is adopted by many firms in order

to estimate their products cost and profitability. This system assists companies by making track

of their raw materials till they are converted into finished goods. The company Roberts Metal

Packaging also used this accounting system to analyse their cost of inventories as well as

profitability. Also, the Roberts Metal Packaging company by executing accounting entry from

the beginning of purchasing of raw material till final production. Company in order to aligning

cost accounting credits immediately purchase of raw material and debit goods in progress. There

are certain types of cost which considers in cost accounting system. They are :

Direct cost is related with production of products and services in a company. Along with

it, this cost includes all the labour cost as well as distribution cost within it as these cost are

highly associated with production process (Nakajima, Kimura and Wagner, 2015). Also,

production cost is considers in this accounting system. The another cost which is considers in

cost accounting system is accounting standard cost. This cost is evaluated by figuring out the

difference within budgeted and actual cost. This cost compares estimated performance of a

business with the planned ones. The variance observed under this cost is the difference which

need to be cover for equating actual with budgeted.

Inventory management system – This system uses supply chain of business as a tracking

element. In inventory management system all the activities which are part of inventories are

included such as warehousing, shipping, retail, production, etc. Inventory management system

enables supervision of stock and inventories. They use three methods for the management of

inventory which is FIFO, LIFO and Weighted Average. The acronym of FIFO is First in first

out. As the name suggest, the inventories of business is valued at very first inventory and

recorded first. Like wise, LIFO is Last in first out (Farrell and Gallagher, 2015) . This method

of inventory management is concerned with last inventory which is arrived at company is to be

valued and recorded at first while Weighted average method is different from all. This includes

average production cost in which they assume valuation of inventories simultaneously.

3

an accounting branch which track transactions of business.

The different types of management accounting system and their essential requirements

will be expressed as follows :

Cost accounting system – The cost accounting system is adopted by many firms in order

to estimate their products cost and profitability. This system assists companies by making track

of their raw materials till they are converted into finished goods. The company Roberts Metal

Packaging also used this accounting system to analyse their cost of inventories as well as

profitability. Also, the Roberts Metal Packaging company by executing accounting entry from

the beginning of purchasing of raw material till final production. Company in order to aligning

cost accounting credits immediately purchase of raw material and debit goods in progress. There

are certain types of cost which considers in cost accounting system. They are :

Direct cost is related with production of products and services in a company. Along with

it, this cost includes all the labour cost as well as distribution cost within it as these cost are

highly associated with production process (Nakajima, Kimura and Wagner, 2015). Also,

production cost is considers in this accounting system. The another cost which is considers in

cost accounting system is accounting standard cost. This cost is evaluated by figuring out the

difference within budgeted and actual cost. This cost compares estimated performance of a

business with the planned ones. The variance observed under this cost is the difference which

need to be cover for equating actual with budgeted.

Inventory management system – This system uses supply chain of business as a tracking

element. In inventory management system all the activities which are part of inventories are

included such as warehousing, shipping, retail, production, etc. Inventory management system

enables supervision of stock and inventories. They use three methods for the management of

inventory which is FIFO, LIFO and Weighted Average. The acronym of FIFO is First in first

out. As the name suggest, the inventories of business is valued at very first inventory and

recorded first. Like wise, LIFO is Last in first out (Farrell and Gallagher, 2015) . This method

of inventory management is concerned with last inventory which is arrived at company is to be

valued and recorded at first while Weighted average method is different from all. This includes

average production cost in which they assume valuation of inventories simultaneously.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing systems – The method of job costing is a procedure which is followed at the

time of information accumulation. The production cost along with cost of service is associated

with this system. The direct labour, direct material and overhead are kinds in which job costing

system can be executed in business entity. This system brings accuracy within business to

estimate system of company.

Thus, all this management accounting system is essential for the smooth functioning of

the company.

B. Different methods for management accounting reporting.

The management accounting reports are generated through period of book keeping and

accounting. These reports are use for regulating, planning, performance measurement and

decision making. By the help of these report, the managers in the company able to highlight

certain pattern and also convert them in useful information. The methods in which management

accounting reports is prepared are budget report, account receivable report, cost managerial

accounting report and performance report.

Budget report – This kind of reports are essential for every business entity as it assists

them in measuring their performance. Different department within a company prepared this

report individually to manage their activities and investment. This helps them in managing

functions of different department in a particular manner with aligned budget. The budget report

is helpful in an organisation for comparison and performing according to planned budget. Also,

the businesses by identifying the variance takes corrective measures for eliminate deviations

within it. Along with it, this budget also considers expenses and income in accordance with

budget prepared. This report is useful for internal interest users of business like owners,

employees, managers, etc. because they are responsible for investment and other operating

expenses within businesses.

Some advantages of budget report in context of business entity are as follows :

This report enables investors to decide about their investment which is wholly based on

performance of business.

The budget report provides aid in executing corrective actions for the deviations.

Budget report is a tool which is used to measure business financial performance. Also, it is helpful in ascertaining risk in organisation and also prepare the company for

any future financial uncertainty.

4

time of information accumulation. The production cost along with cost of service is associated

with this system. The direct labour, direct material and overhead are kinds in which job costing

system can be executed in business entity. This system brings accuracy within business to

estimate system of company.

Thus, all this management accounting system is essential for the smooth functioning of

the company.

B. Different methods for management accounting reporting.

The management accounting reports are generated through period of book keeping and

accounting. These reports are use for regulating, planning, performance measurement and

decision making. By the help of these report, the managers in the company able to highlight

certain pattern and also convert them in useful information. The methods in which management

accounting reports is prepared are budget report, account receivable report, cost managerial

accounting report and performance report.

Budget report – This kind of reports are essential for every business entity as it assists

them in measuring their performance. Different department within a company prepared this

report individually to manage their activities and investment. This helps them in managing

functions of different department in a particular manner with aligned budget. The budget report

is helpful in an organisation for comparison and performing according to planned budget. Also,

the businesses by identifying the variance takes corrective measures for eliminate deviations

within it. Along with it, this budget also considers expenses and income in accordance with

budget prepared. This report is useful for internal interest users of business like owners,

employees, managers, etc. because they are responsible for investment and other operating

expenses within businesses.

Some advantages of budget report in context of business entity are as follows :

This report enables investors to decide about their investment which is wholly based on

performance of business.

The budget report provides aid in executing corrective actions for the deviations.

Budget report is a tool which is used to measure business financial performance. Also, it is helpful in ascertaining risk in organisation and also prepare the company for

any future financial uncertainty.

4

Account receivable report – The report of account receivable relies on credit extension

within businesses. The credit amount offer to customers for a specific time given to customer’s

is recorded in account receivable report. This provide assist to managers of company to identify

defaulters which can increase their balance amount which they offer on credit. Defaulters are

those which have the least possibility of repayment of amount for the product they purchased.

The account receivable report is helpful for business personnel in ascertaining defaulters for the

adaption in their credit policy (Ahmad, 2017). Also, this report provides aid to managers in

changing existing credit policies and reform new ones by comprehending the whole report.

Benefits which account receivable report offers are as follows :

The account receivable report helps managers in determining period of collection from

creditors.

Also, the internal users of company is able to make decisions regarding credit extension

for making changes in different strategies. This report is helpful in company to decide the appropriate credit policy and mode of

restructuring for them.

Cost managerial accounting report – This report is associated with cost of raw materials,

labour, overheads, and any other additional cost. The cost managerial accounting report provide

capacity of cost price realisation with that of selling price. Under this report, the margins of cost

are estimated and monitored by depicted a clear picture which went into procurement of

company. This report provides an exact comprehension on expenses which is important for

optimization in better way for the resources in all the department.

Some advantages of cost managerial report will be depicted as :

This report enables control among cost of products and services in efficient and effective

manner. The cost managerial accounting report help company in evaluating income as well as

expense of company by taking actions which lead to business development and growth.

Performance report – This report is appropriate for company in analysis and

reassessment of performance of company. The members of staff working in company be a part of

appraisals and promotions according to proper analysis of this report by department head. This

report is mainly prepared in large organisation because it is not possible for managers to measure

performance of every staff member verbally. So, they prepare report to analyse their

5

within businesses. The credit amount offer to customers for a specific time given to customer’s

is recorded in account receivable report. This provide assist to managers of company to identify

defaulters which can increase their balance amount which they offer on credit. Defaulters are

those which have the least possibility of repayment of amount for the product they purchased.

The account receivable report is helpful for business personnel in ascertaining defaulters for the

adaption in their credit policy (Ahmad, 2017). Also, this report provides aid to managers in

changing existing credit policies and reform new ones by comprehending the whole report.

Benefits which account receivable report offers are as follows :

The account receivable report helps managers in determining period of collection from

creditors.

Also, the internal users of company is able to make decisions regarding credit extension

for making changes in different strategies. This report is helpful in company to decide the appropriate credit policy and mode of

restructuring for them.

Cost managerial accounting report – This report is associated with cost of raw materials,

labour, overheads, and any other additional cost. The cost managerial accounting report provide

capacity of cost price realisation with that of selling price. Under this report, the margins of cost

are estimated and monitored by depicted a clear picture which went into procurement of

company. This report provides an exact comprehension on expenses which is important for

optimization in better way for the resources in all the department.

Some advantages of cost managerial report will be depicted as :

This report enables control among cost of products and services in efficient and effective

manner. The cost managerial accounting report help company in evaluating income as well as

expense of company by taking actions which lead to business development and growth.

Performance report – This report is appropriate for company in analysis and

reassessment of performance of company. The members of staff working in company be a part of

appraisals and promotions according to proper analysis of this report by department head. This

report is mainly prepared in large organisation because it is not possible for managers to measure

performance of every staff member verbally. So, they prepare report to analyse their

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance along with it the strengths and areas of improvement is also measured with an ease

under this report. Thus, this report is helpful for both businesses purpose as well as individual

purpose. The higher authority provide guidance to employees on initial stage of project in order

to foster them to perform their best.

The performance report is helpful in providing various benefits which are as follows :

This report is helpful for individual growth and development of employees as they are

guided by their superior by analysing weaknesses through report.

The performance under this report is measured by actual with planned which help them in

taking corrective measures to attain success and organisational goal.

C. The benefits of different management accounting system and their application in context

of business.

Benefits and application of different management accounting system in context of

organisation are as follows :

Cost accounting system – The cost accounting system enables company like Roberts

Metal Packaging to measure and improve their performance by ascertaining cost and decline

amount of wastage. Along with it, cost accounting provide guidance to management of Roberts

Metal to deriving production cost for which they able to execute decisions regarding use of

labour or machinery for their production of metal packaging.

Inventory management system – This system is helpful in achievement of productivity

and efficiency in operations (Langfield - Smith and et.al., 2017). Company Roberts Metal

Packaging by adopting this inventory system is able to save their time as well as money by

tracking on products and services company rendered to their customer’s.

Job costing systems – For Roberts Metal Packaging this system found very profitable

because by job costing system company is able to estimate the similar cost job which will be

taken in the future. The efficiency of plant of metal packaging also regulated by attention at the

cost which is related to job of individual. Along with it, by this system company is able to

analyse in detail about labour, overhead and material for each job.

D. Evaluation of management accounting system and reporting which is integrated in

process of organisation.

Management accounting system focus on preparation of financial information of

company for internal and or confidential purpose which is used by managers which enhances

6

under this report. Thus, this report is helpful for both businesses purpose as well as individual

purpose. The higher authority provide guidance to employees on initial stage of project in order

to foster them to perform their best.

The performance report is helpful in providing various benefits which are as follows :

This report is helpful for individual growth and development of employees as they are

guided by their superior by analysing weaknesses through report.

The performance under this report is measured by actual with planned which help them in

taking corrective measures to attain success and organisational goal.

C. The benefits of different management accounting system and their application in context

of business.

Benefits and application of different management accounting system in context of

organisation are as follows :

Cost accounting system – The cost accounting system enables company like Roberts

Metal Packaging to measure and improve their performance by ascertaining cost and decline

amount of wastage. Along with it, cost accounting provide guidance to management of Roberts

Metal to deriving production cost for which they able to execute decisions regarding use of

labour or machinery for their production of metal packaging.

Inventory management system – This system is helpful in achievement of productivity

and efficiency in operations (Langfield - Smith and et.al., 2017). Company Roberts Metal

Packaging by adopting this inventory system is able to save their time as well as money by

tracking on products and services company rendered to their customer’s.

Job costing systems – For Roberts Metal Packaging this system found very profitable

because by job costing system company is able to estimate the similar cost job which will be

taken in the future. The efficiency of plant of metal packaging also regulated by attention at the

cost which is related to job of individual. Along with it, by this system company is able to

analyse in detail about labour, overhead and material for each job.

D. Evaluation of management accounting system and reporting which is integrated in

process of organisation.

Management accounting system focus on preparation of financial information of

company for internal and or confidential purpose which is used by managers which enhances

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

their decision making ability whereas management accounting reporting is helpful to monitor

business performance. These reports are prepared on frequent basis as and when needed. The

managerial reports and management accounting system are inter - related .

Cost accounting system is followed under Roberts Metal Packaging company in which

they able to ascertain their cost of product as well as profitability. But for determining the cost a

budget is prepared from budget report in production department for which the company able to

determine their allocation of amount (Krishnan, 2015). Any deviation in budget report lead to

disbursement of this accounting system. Thus, cost accounting system and budget report is inter -

related. Like wise, inventory management is system is related with budget report and cost

managerial accounting report. As it includes cost of labour, raw material, etc. which enhances

overall cost. This influences not only pre set budget but also inventory management system

affects with it as they both are concerned on tracking of productivity and profitability of

company Roberts Metal Packaging.

Part 2

Analyse different planning tools which is used in management accounting.

The different planning tools which is adopting in management accounting as ass follows :

Activity based costing – This method of costing is assigns to indirect cost activities and

products which is based on usage of activities on each products. It identifies activities which

generates and assigns costs to activities. Costing based on activity is observed a more accurate

method of product and service costing and helps the company to take pricing decisions more

effectively. This method enables challenge operating cost to better way of eliminating and

allocating overheads. This method is also helpful in improvement of customer’s and products in

analysing profitability. Also, it provides support to techniques of performance management.

The activity based costing depicts an accurate information as company Roberts Metal

Packaging able to determine activities and cost of activity. It helps the company in identify their

cost of activities. This method help marketing personnel in providing accurate cost of products

for decisions about price and also the products which are not profitable eliminates.

Benchmarking – The benchmarking method is a measurement of internal performance

and process of organisation and lays a comparison with related and comparative companies

(Saleem Salem Alzoubi, 2016). The managers of a company compares performance of their

products with that of products of external rivalry firms. The company operates this method to

7

business performance. These reports are prepared on frequent basis as and when needed. The

managerial reports and management accounting system are inter - related .

Cost accounting system is followed under Roberts Metal Packaging company in which

they able to ascertain their cost of product as well as profitability. But for determining the cost a

budget is prepared from budget report in production department for which the company able to

determine their allocation of amount (Krishnan, 2015). Any deviation in budget report lead to

disbursement of this accounting system. Thus, cost accounting system and budget report is inter -

related. Like wise, inventory management is system is related with budget report and cost

managerial accounting report. As it includes cost of labour, raw material, etc. which enhances

overall cost. This influences not only pre set budget but also inventory management system

affects with it as they both are concerned on tracking of productivity and profitability of

company Roberts Metal Packaging.

Part 2

Analyse different planning tools which is used in management accounting.

The different planning tools which is adopting in management accounting as ass follows :

Activity based costing – This method of costing is assigns to indirect cost activities and

products which is based on usage of activities on each products. It identifies activities which

generates and assigns costs to activities. Costing based on activity is observed a more accurate

method of product and service costing and helps the company to take pricing decisions more

effectively. This method enables challenge operating cost to better way of eliminating and

allocating overheads. This method is also helpful in improvement of customer’s and products in

analysing profitability. Also, it provides support to techniques of performance management.

The activity based costing depicts an accurate information as company Roberts Metal

Packaging able to determine activities and cost of activity. It helps the company in identify their

cost of activities. This method help marketing personnel in providing accurate cost of products

for decisions about price and also the products which are not profitable eliminates.

Benchmarking – The benchmarking method is a measurement of internal performance

and process of organisation and lays a comparison with related and comparative companies

(Saleem Salem Alzoubi, 2016). The managers of a company compares performance of their

products with that of products of external rivalry firms. The company operates this method to

7

improve their performance and incorporation of best practises into their business through

innovation.

The company Roberts Metal Packaging use this method for improve their operational

efficiency and product efficiency. Also, the benchmarking enables company to reveal their cost

position and opportunities for the improvement. In addition to this, benchmarking also bring new

ideas in the business and enables sharing of experience.

Break even analysis – This is a technique which is widely adopted by management

accounting and production department. The break even analysis relies between variable cost and

fixed cost. The fixed cost is not directly associated with production or output level. This means

that even at zero output the fixed cost remains same while variable cost changes with level of

production. When there is break even point, the revenue is equal to summation of variable cost

and fixed cost.

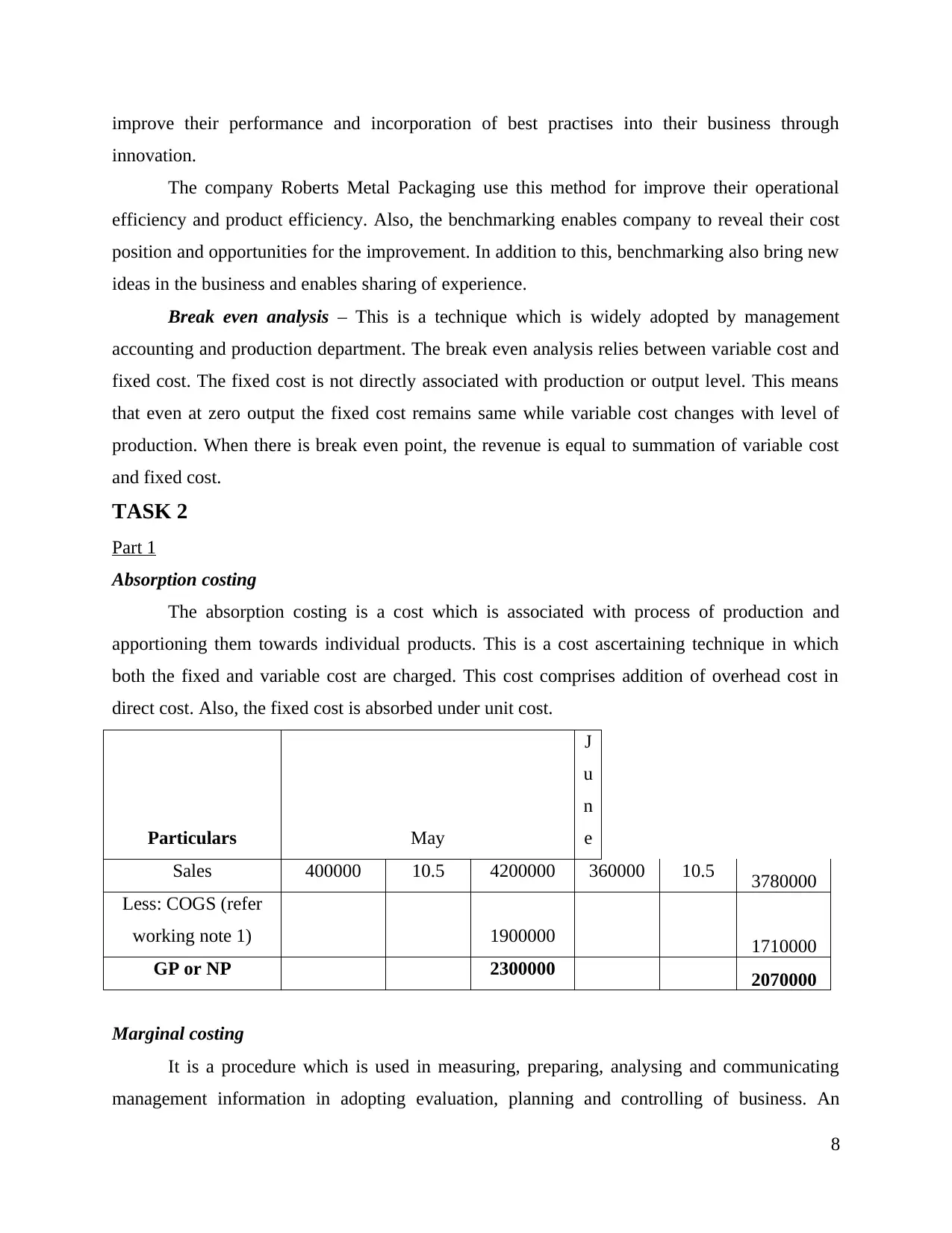

TASK 2

Part 1

Absorption costing

The absorption costing is a cost which is associated with process of production and

apportioning them towards individual products. This is a cost ascertaining technique in which

both the fixed and variable cost are charged. This cost comprises addition of overhead cost in

direct cost. Also, the fixed cost is absorbed under unit cost.

Particulars May

J

u

n

e

Sales 400000 10.5 4200000 360000 10.5 3780000

Less: COGS (refer

working note 1) 1900000 1710000

GP or NP 2300000 2070000

Marginal costing

It is a procedure which is used in measuring, preparing, analysing and communicating

management information in adopting evaluation, planning and controlling of business. An

8

innovation.

The company Roberts Metal Packaging use this method for improve their operational

efficiency and product efficiency. Also, the benchmarking enables company to reveal their cost

position and opportunities for the improvement. In addition to this, benchmarking also bring new

ideas in the business and enables sharing of experience.

Break even analysis – This is a technique which is widely adopted by management

accounting and production department. The break even analysis relies between variable cost and

fixed cost. The fixed cost is not directly associated with production or output level. This means

that even at zero output the fixed cost remains same while variable cost changes with level of

production. When there is break even point, the revenue is equal to summation of variable cost

and fixed cost.

TASK 2

Part 1

Absorption costing

The absorption costing is a cost which is associated with process of production and

apportioning them towards individual products. This is a cost ascertaining technique in which

both the fixed and variable cost are charged. This cost comprises addition of overhead cost in

direct cost. Also, the fixed cost is absorbed under unit cost.

Particulars May

J

u

n

e

Sales 400000 10.5 4200000 360000 10.5 3780000

Less: COGS (refer

working note 1) 1900000 1710000

GP or NP 2300000 2070000

Marginal costing

It is a procedure which is used in measuring, preparing, analysing and communicating

management information in adopting evaluation, planning and controlling of business. An

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

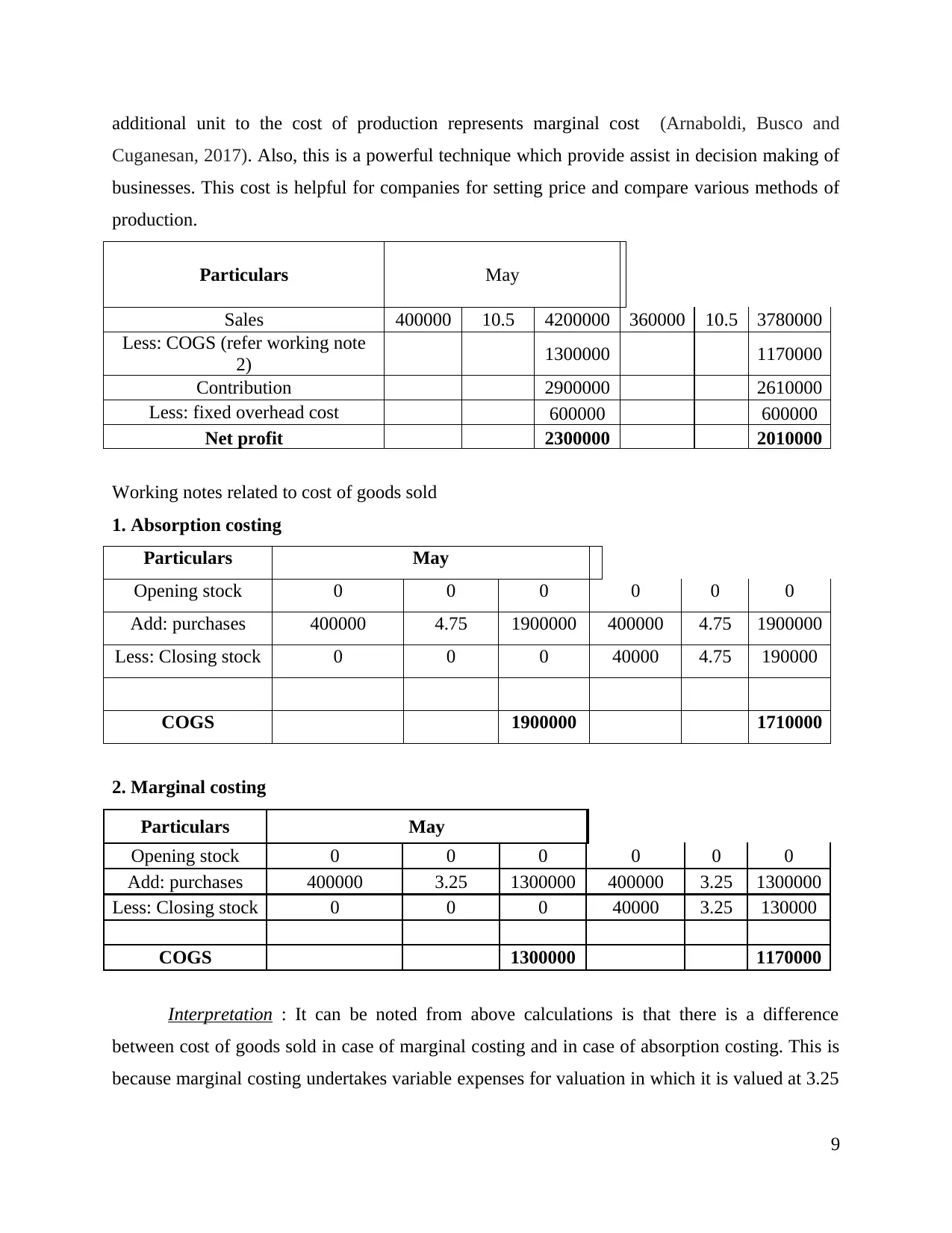

additional unit to the cost of production represents marginal cost (Arnaboldi, Busco and

Cuganesan, 2017). Also, this is a powerful technique which provide assist in decision making of

businesses. This cost is helpful for companies for setting price and compare various methods of

production.

Particulars May

Sales 400000 10.5 4200000 360000 10.5 3780000

Less: COGS (refer working note

2) 1300000 1170000

Contribution 2900000 2610000

Less: fixed overhead cost 600000 600000

Net profit 2300000 2010000

Working notes related to cost of goods sold

1. Absorption costing

Particulars May

Opening stock 0 0 0 0 0 0

Add: purchases 400000 4.75 1900000 400000 4.75 1900000

Less: Closing stock 0 0 0 40000 4.75 190000

COGS 1900000 1710000

2. Marginal costing

Particulars May

Opening stock 0 0 0 0 0 0

Add: purchases 400000 3.25 1300000 400000 3.25 1300000

Less: Closing stock 0 0 0 40000 3.25 130000

COGS 1300000 1170000

Interpretation : It can be noted from above calculations is that there is a difference

between cost of goods sold in case of marginal costing and in case of absorption costing. This is

because marginal costing undertakes variable expenses for valuation in which it is valued at 3.25

9

Cuganesan, 2017). Also, this is a powerful technique which provide assist in decision making of

businesses. This cost is helpful for companies for setting price and compare various methods of

production.

Particulars May

Sales 400000 10.5 4200000 360000 10.5 3780000

Less: COGS (refer working note

2) 1300000 1170000

Contribution 2900000 2610000

Less: fixed overhead cost 600000 600000

Net profit 2300000 2010000

Working notes related to cost of goods sold

1. Absorption costing

Particulars May

Opening stock 0 0 0 0 0 0

Add: purchases 400000 4.75 1900000 400000 4.75 1900000

Less: Closing stock 0 0 0 40000 4.75 190000

COGS 1900000 1710000

2. Marginal costing

Particulars May

Opening stock 0 0 0 0 0 0

Add: purchases 400000 3.25 1300000 400000 3.25 1300000

Less: Closing stock 0 0 0 40000 3.25 130000

COGS 1300000 1170000

Interpretation : It can be noted from above calculations is that there is a difference

between cost of goods sold in case of marginal costing and in case of absorption costing. This is

because marginal costing undertakes variable expenses for valuation in which it is valued at 3.25

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

whereas opening and closing stock under absorption costing is valued at the rate of 4.75. As this

costing considers both costs that is variable and fixed cost in identification of cost of goods sold.

Part 2

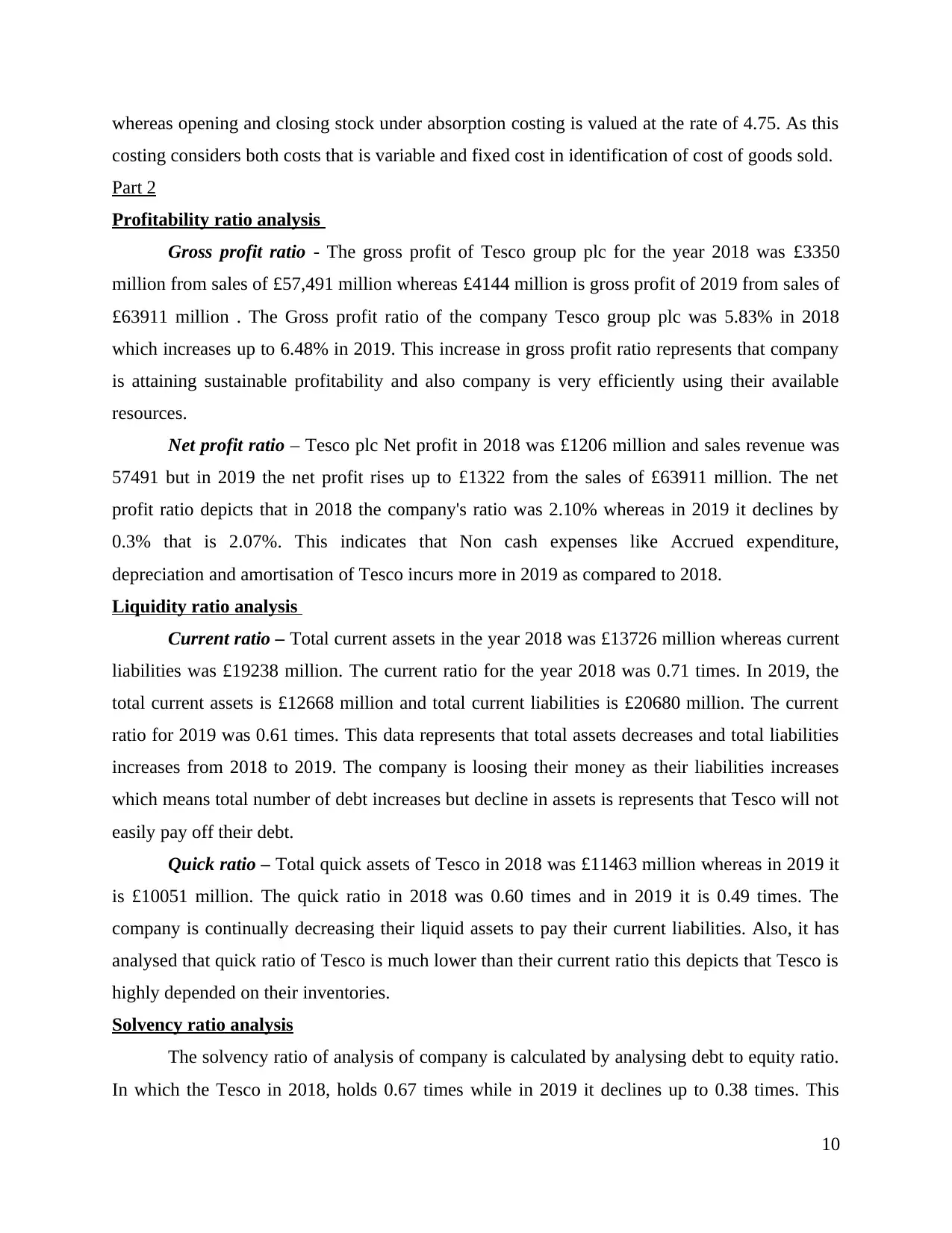

Profitability ratio analysis

Gross profit ratio - The gross profit of Tesco group plc for the year 2018 was £3350

million from sales of £57,491 million whereas £4144 million is gross profit of 2019 from sales of

£63911 million . The Gross profit ratio of the company Tesco group plc was 5.83% in 2018

which increases up to 6.48% in 2019. This increase in gross profit ratio represents that company

is attaining sustainable profitability and also company is very efficiently using their available

resources.

Net profit ratio – Tesco plc Net profit in 2018 was £1206 million and sales revenue was

57491 but in 2019 the net profit rises up to £1322 from the sales of £63911 million. The net

profit ratio depicts that in 2018 the company's ratio was 2.10% whereas in 2019 it declines by

0.3% that is 2.07%. This indicates that Non cash expenses like Accrued expenditure,

depreciation and amortisation of Tesco incurs more in 2019 as compared to 2018.

Liquidity ratio analysis

Current ratio – Total current assets in the year 2018 was £13726 million whereas current

liabilities was £19238 million. The current ratio for the year 2018 was 0.71 times. In 2019, the

total current assets is £12668 million and total current liabilities is £20680 million. The current

ratio for 2019 was 0.61 times. This data represents that total assets decreases and total liabilities

increases from 2018 to 2019. The company is loosing their money as their liabilities increases

which means total number of debt increases but decline in assets is represents that Tesco will not

easily pay off their debt.

Quick ratio – Total quick assets of Tesco in 2018 was £11463 million whereas in 2019 it

is £10051 million. The quick ratio in 2018 was 0.60 times and in 2019 it is 0.49 times. The

company is continually decreasing their liquid assets to pay their current liabilities. Also, it has

analysed that quick ratio of Tesco is much lower than their current ratio this depicts that Tesco is

highly depended on their inventories.

Solvency ratio analysis

The solvency ratio of analysis of company is calculated by analysing debt to equity ratio.

In which the Tesco in 2018, holds 0.67 times while in 2019 it declines up to 0.38 times. This

10

costing considers both costs that is variable and fixed cost in identification of cost of goods sold.

Part 2

Profitability ratio analysis

Gross profit ratio - The gross profit of Tesco group plc for the year 2018 was £3350

million from sales of £57,491 million whereas £4144 million is gross profit of 2019 from sales of

£63911 million . The Gross profit ratio of the company Tesco group plc was 5.83% in 2018

which increases up to 6.48% in 2019. This increase in gross profit ratio represents that company

is attaining sustainable profitability and also company is very efficiently using their available

resources.

Net profit ratio – Tesco plc Net profit in 2018 was £1206 million and sales revenue was

57491 but in 2019 the net profit rises up to £1322 from the sales of £63911 million. The net

profit ratio depicts that in 2018 the company's ratio was 2.10% whereas in 2019 it declines by

0.3% that is 2.07%. This indicates that Non cash expenses like Accrued expenditure,

depreciation and amortisation of Tesco incurs more in 2019 as compared to 2018.

Liquidity ratio analysis

Current ratio – Total current assets in the year 2018 was £13726 million whereas current

liabilities was £19238 million. The current ratio for the year 2018 was 0.71 times. In 2019, the

total current assets is £12668 million and total current liabilities is £20680 million. The current

ratio for 2019 was 0.61 times. This data represents that total assets decreases and total liabilities

increases from 2018 to 2019. The company is loosing their money as their liabilities increases

which means total number of debt increases but decline in assets is represents that Tesco will not

easily pay off their debt.

Quick ratio – Total quick assets of Tesco in 2018 was £11463 million whereas in 2019 it

is £10051 million. The quick ratio in 2018 was 0.60 times and in 2019 it is 0.49 times. The

company is continually decreasing their liquid assets to pay their current liabilities. Also, it has

analysed that quick ratio of Tesco is much lower than their current ratio this depicts that Tesco is

highly depended on their inventories.

Solvency ratio analysis

The solvency ratio of analysis of company is calculated by analysing debt to equity ratio.

In which the Tesco in 2018, holds 0.67 times while in 2019 it declines up to 0.38 times. This

10

analysis depicts that company is not taking any benefit of their increased profits which is brought

by financial leverage. Also, company is decreasing their long term debt by the analysis of 2018

and 2019. Tesco is increasing their equities which represents that they are increasing their

financially strong and attains a huge amount of profitability.

Efficiency ratio analysis

Ratio analysis in terms of efficiency for the company Tesco group is showing increasing

trend as the stock turnover ratio from 2018 to 2019 increases by 0.76 times. Also, total assets

turnover ratio increases by 0.09 times and fixed asset turnover ratio from 2018 increases by 0.02

times. This indicates that company is using their available resources efficiently. Also, they are

attaining success in their business operations due to efficiently management of their assets and

investments.

Investment ratio analysis

The investment ratio is analysed through dividend per share and earning per share. The

earning per share of Tesco is depicting a decreasing trend of 0.03% whereas dividend per share

is increasing from 2018 to 2019 by 0.08%. The increasing trend of dividend per share indicates

that company is sure about their future earning and distributes dividend more in 2019 as

compared to 2018.

CONCLUSION

This report was all about management accounting for the company Roberts Metal

Packaging. The report was begun with a brief explanation of management accounting and

essential requirements of different kinds of management accounting such as cost account system,

job costing system , and inventory management system. This report also describe about certain

methods adopted by management accounting reporting like budget report, cost report,

performance report and account receivable report. The benefits of different management

accounting system were described under this report along with their applicability in context of

Roberts Metal Packaging. Also, the management accounting system and reporting were

elaborated in report for expressing relationship between them during process of organisation.

Three planning tools were also be discussed which is adopted by management accounting was

explained in this report. At last, a portfolio of financial statement were calculated along with it

ratio analysis of Tesco group plc were calculated and interpreted in this report.

11

by financial leverage. Also, company is decreasing their long term debt by the analysis of 2018

and 2019. Tesco is increasing their equities which represents that they are increasing their

financially strong and attains a huge amount of profitability.

Efficiency ratio analysis

Ratio analysis in terms of efficiency for the company Tesco group is showing increasing

trend as the stock turnover ratio from 2018 to 2019 increases by 0.76 times. Also, total assets

turnover ratio increases by 0.09 times and fixed asset turnover ratio from 2018 increases by 0.02

times. This indicates that company is using their available resources efficiently. Also, they are

attaining success in their business operations due to efficiently management of their assets and

investments.

Investment ratio analysis

The investment ratio is analysed through dividend per share and earning per share. The

earning per share of Tesco is depicting a decreasing trend of 0.03% whereas dividend per share

is increasing from 2018 to 2019 by 0.08%. The increasing trend of dividend per share indicates

that company is sure about their future earning and distributes dividend more in 2019 as

compared to 2018.

CONCLUSION

This report was all about management accounting for the company Roberts Metal

Packaging. The report was begun with a brief explanation of management accounting and

essential requirements of different kinds of management accounting such as cost account system,

job costing system , and inventory management system. This report also describe about certain

methods adopted by management accounting reporting like budget report, cost report,

performance report and account receivable report. The benefits of different management

accounting system were described under this report along with their applicability in context of

Roberts Metal Packaging. Also, the management accounting system and reporting were

elaborated in report for expressing relationship between them during process of organisation.

Three planning tools were also be discussed which is adopted by management accounting was

explained in this report. At last, a portfolio of financial statement were calculated along with it

ratio analysis of Tesco group plc were calculated and interpreted in this report.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.