Management Accounting Systems and Techniques: A Detailed Report

VerifiedAdded on 2023/01/04

|16

|4514

|71

Report

AI Summary

This report delves into the realm of management accounting, providing a detailed analysis of various systems and techniques employed by businesses. It begins with an introduction to the importance of effective management accounting in today's market, highlighting its role in monitoring and evaluating financial information for strategic decision-making. The report then explores different types of management accounting systems, such as inventory control, cost accounting, job costing, and price optimization systems, and discusses their benefits. Furthermore, it examines various management accounting reports, including budget reports, cost reports, performance reports, and accounts receivable aging reports, explaining their uses and significance. The report also covers a range of management accounting techniques, such as absorption costing and marginal costing, along with the application of material variances and reconciliation statements. Through the analysis of these elements, the report provides a comprehensive understanding of how management accounting supports organizational efficiency, financial planning, and performance evaluation. The report uses KEF LTD as a case study to illustrate the concepts discussed and how different frameworks help support the business strategy.

Management Accounting

Systems & Techniques

Systems & Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Different type of management accounting system................................................................3

P2 Different type of management accounting reports.................................................................5

TASK 2............................................................................................................................................5

P3. Range of management accounting techniques......................................................................5

TASK 3............................................................................................................................................9

P4.Planning tools used in management accounting.....................................................................9

P5. Comparison of organisations adapting management accounting to respond to financial

problems....................................................................................................................................10

CONCLUSION..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Different type of management accounting system................................................................3

P2 Different type of management accounting reports.................................................................5

TASK 2............................................................................................................................................5

P3. Range of management accounting techniques......................................................................5

TASK 3............................................................................................................................................9

P4.Planning tools used in management accounting.....................................................................9

P5. Comparison of organisations adapting management accounting to respond to financial

problems....................................................................................................................................10

CONCLUSION..............................................................................................................................12

INTRODUCTION

There is a critical need for an effective professional management structure in the current market

situation that can monitor the valuable activity of the organisation to improve business

productivity (Collis and Hussey, 2017). Management accounting is define as an important

system for evaluating, monitoring, and handling valuable financial information within a system

in order to achieve a strategic choice by some company president to improve and grow profits

over a given period of time. The entire expense or management accounting process begins with

the compilation, reporting, estimation, evaluation, review and distribution of useful business

financial information that helps reach the required objectives over a predetermined amount of

time. To better explain the meaning of accounting administration, KEF LTD, a production firm,

is chosen.

This research illustrates understanding of multiple processes and reports, estimates the

cost of output per unit, budget period P&L accounts, etc. by applying useful valuation models. In

addition, the study further explores the use of multiple forecasting tools used in reporting for

management and how different frameworks help support the business strategy.

TASK 1

P1. Different type of management accounting system

The principle of MA is known to become an internally fitting method in the company

sense that facilitates the estimation or evaluation of the total output of various groups inside the

company. Typically, supervisors set criteria for performance assessment, evaluating several

methods that promote the accomplishment of established targets also help to determine real

explanations for variations from the current plan (Schaltegger, Burritt and Petersen, 2017). In

corporate words, MA typically provides the management and then all organisation personnel

with the non-financial as well as financial evidence that allows them create the most correct

decisions to maximise revenue, competitiveness and meet targets. There have been numerous

important managerial accounting systems that support KEF Ltd's management, which are listed

below:

Inventory control system: This program provides handle company stock in the

necessary quantities, transacted products and final product. There have been different methods

such as FIFO, LIFO and Average methodologies for regulating company shares which provide

There is a critical need for an effective professional management structure in the current market

situation that can monitor the valuable activity of the organisation to improve business

productivity (Collis and Hussey, 2017). Management accounting is define as an important

system for evaluating, monitoring, and handling valuable financial information within a system

in order to achieve a strategic choice by some company president to improve and grow profits

over a given period of time. The entire expense or management accounting process begins with

the compilation, reporting, estimation, evaluation, review and distribution of useful business

financial information that helps reach the required objectives over a predetermined amount of

time. To better explain the meaning of accounting administration, KEF LTD, a production firm,

is chosen.

This research illustrates understanding of multiple processes and reports, estimates the

cost of output per unit, budget period P&L accounts, etc. by applying useful valuation models. In

addition, the study further explores the use of multiple forecasting tools used in reporting for

management and how different frameworks help support the business strategy.

TASK 1

P1. Different type of management accounting system

The principle of MA is known to become an internally fitting method in the company

sense that facilitates the estimation or evaluation of the total output of various groups inside the

company. Typically, supervisors set criteria for performance assessment, evaluating several

methods that promote the accomplishment of established targets also help to determine real

explanations for variations from the current plan (Schaltegger, Burritt and Petersen, 2017). In

corporate words, MA typically provides the management and then all organisation personnel

with the non-financial as well as financial evidence that allows them create the most correct

decisions to maximise revenue, competitiveness and meet targets. There have been numerous

important managerial accounting systems that support KEF Ltd's management, which are listed

below:

Inventory control system: This program provides handle company stock in the

necessary quantities, transacted products and final product. There have been different methods

such as FIFO, LIFO and Average methodologies for regulating company shares which provide

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the confidence of the business process. In KEF Ltd the FIFO approach is used though they are

necessary to eliminate old products using this approach and thus reduce damage due to defective

products. First of all, KEF Ltd helps KEF Ltd to produce products according to markets and

customer likes and dislikes, helping to increase profit.

Essential requirements: The manager establishes supplies and storage of commodities

through a coordinated supply chain structure with KEF Ltd. This relationship aims to effectively

and effectively reduce the costs for repair and marketing of goods.

System of cost accounting: This is used to calculate the cost of that same total

manufacturing of specific company’s products. It essentially entails multi-level gross costs which

also requires fixed costs that help decide the benefit. Useful accounting expense approaches such

as median and absorption costing, lean costing, operation as well as the regular costing approach

are applicable. ABC stock valuation technique is used in the respective firm that basically

allocates overall cost to items related to the production of goods (Humphrey, C. and Miller,

2012).

Essential requirements: This measure is helpful for the management of KEF Ltd as it

will determine products that are more costly again and determine whether they really worth a

huge amount or if they should obtain meaningful market shares.

Job Coasting system: This approach primarily records the costs associated with the

production of good management within the company. It helps to delegate production costs to

every other commodity, and the product manager and auditor have proof of each given product

category. This system also supports the calculation of the cost of different products produced by

the company over the same amount of time. In KEF Ltd, therefore this system helps to assess

and evaluate the cost of different helpful company’s products to reach the demand of the

consumers.

Essential requirements: This MA scheme is needed to monitor the expenses of works

with HEF ltd along with wrapping and delivery, through Innocent items. The organisation

employs cost-per-take methods to calculate its expenditures.

Price optimization system: This is regarded to just be the company's greatest system as

it helps to understand the consumer's response to the manufacturing sales volumes fixed by the

organization. Used by managers to set decent product prices that will make customers happy as

necessary to eliminate old products using this approach and thus reduce damage due to defective

products. First of all, KEF Ltd helps KEF Ltd to produce products according to markets and

customer likes and dislikes, helping to increase profit.

Essential requirements: The manager establishes supplies and storage of commodities

through a coordinated supply chain structure with KEF Ltd. This relationship aims to effectively

and effectively reduce the costs for repair and marketing of goods.

System of cost accounting: This is used to calculate the cost of that same total

manufacturing of specific company’s products. It essentially entails multi-level gross costs which

also requires fixed costs that help decide the benefit. Useful accounting expense approaches such

as median and absorption costing, lean costing, operation as well as the regular costing approach

are applicable. ABC stock valuation technique is used in the respective firm that basically

allocates overall cost to items related to the production of goods (Humphrey, C. and Miller,

2012).

Essential requirements: This measure is helpful for the management of KEF Ltd as it

will determine products that are more costly again and determine whether they really worth a

huge amount or if they should obtain meaningful market shares.

Job Coasting system: This approach primarily records the costs associated with the

production of good management within the company. It helps to delegate production costs to

every other commodity, and the product manager and auditor have proof of each given product

category. This system also supports the calculation of the cost of different products produced by

the company over the same amount of time. In KEF Ltd, therefore this system helps to assess

and evaluate the cost of different helpful company’s products to reach the demand of the

consumers.

Essential requirements: This MA scheme is needed to monitor the expenses of works

with HEF ltd along with wrapping and delivery, through Innocent items. The organisation

employs cost-per-take methods to calculate its expenditures.

Price optimization system: This is regarded to just be the company's greatest system as

it helps to understand the consumer's response to the manufacturing sales volumes fixed by the

organization. Used by managers to set decent product prices that will make customers happy as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

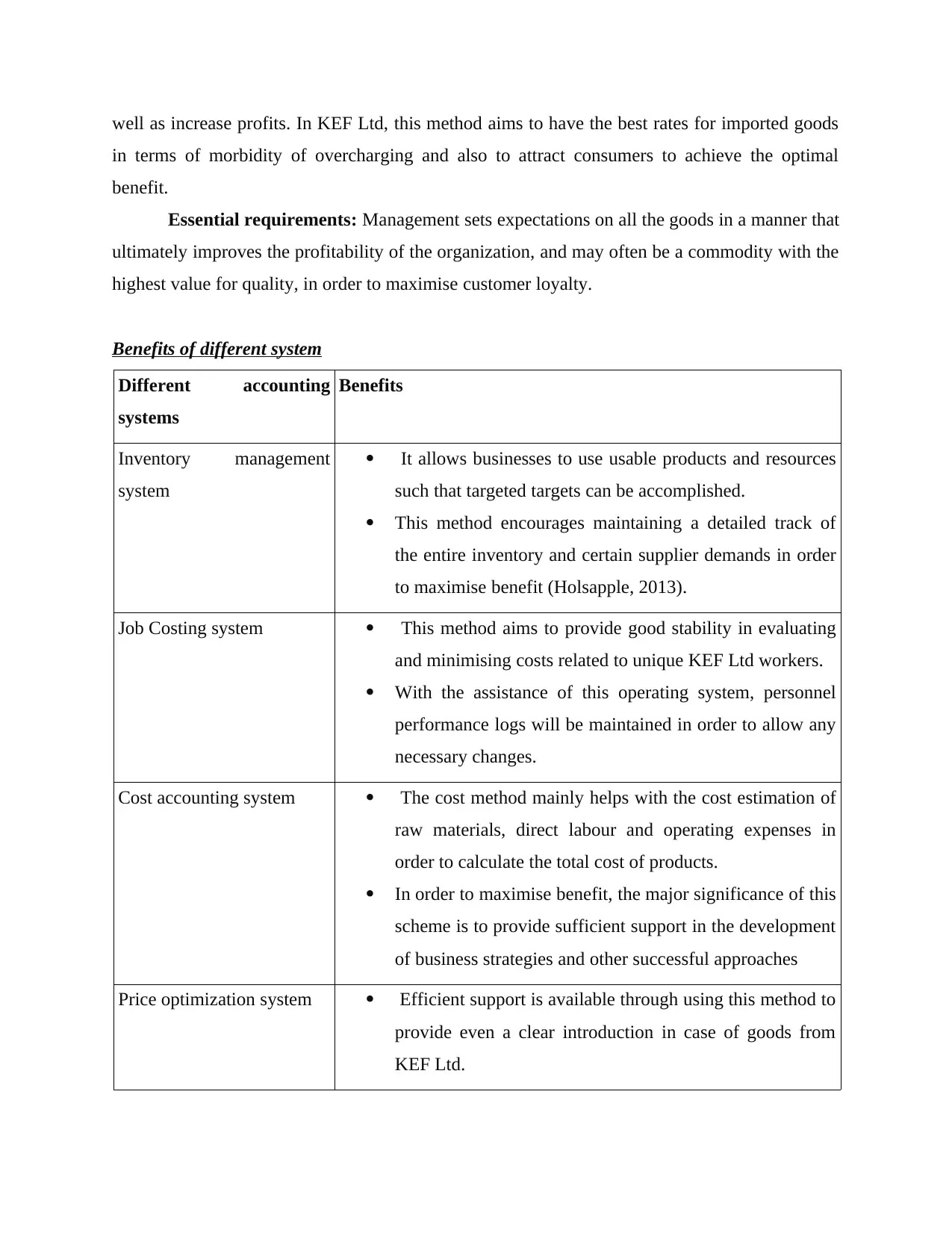

well as increase profits. In KEF Ltd, this method aims to have the best rates for imported goods

in terms of morbidity of overcharging and also to attract consumers to achieve the optimal

benefit.

Essential requirements: Management sets expectations on all the goods in a manner that

ultimately improves the profitability of the organization, and may often be a commodity with the

highest value for quality, in order to maximise customer loyalty.

Benefits of different system

Different accounting

systems

Benefits

Inventory management

system

It allows businesses to use usable products and resources

such that targeted targets can be accomplished.

This method encourages maintaining a detailed track of

the entire inventory and certain supplier demands in order

to maximise benefit (Holsapple, 2013).

Job Costing system This method aims to provide good stability in evaluating

and minimising costs related to unique KEF Ltd workers.

With the assistance of this operating system, personnel

performance logs will be maintained in order to allow any

necessary changes.

Cost accounting system The cost method mainly helps with the cost estimation of

raw materials, direct labour and operating expenses in

order to calculate the total cost of products.

In order to maximise benefit, the major significance of this

scheme is to provide sufficient support in the development

of business strategies and other successful approaches

Price optimization system Efficient support is available through using this method to

provide even a clear introduction in case of goods from

KEF Ltd.

in terms of morbidity of overcharging and also to attract consumers to achieve the optimal

benefit.

Essential requirements: Management sets expectations on all the goods in a manner that

ultimately improves the profitability of the organization, and may often be a commodity with the

highest value for quality, in order to maximise customer loyalty.

Benefits of different system

Different accounting

systems

Benefits

Inventory management

system

It allows businesses to use usable products and resources

such that targeted targets can be accomplished.

This method encourages maintaining a detailed track of

the entire inventory and certain supplier demands in order

to maximise benefit (Holsapple, 2013).

Job Costing system This method aims to provide good stability in evaluating

and minimising costs related to unique KEF Ltd workers.

With the assistance of this operating system, personnel

performance logs will be maintained in order to allow any

necessary changes.

Cost accounting system The cost method mainly helps with the cost estimation of

raw materials, direct labour and operating expenses in

order to calculate the total cost of products.

In order to maximise benefit, the major significance of this

scheme is to provide sufficient support in the development

of business strategies and other successful approaches

Price optimization system Efficient support is available through using this method to

provide even a clear introduction in case of goods from

KEF Ltd.

The key advantages of the pricing system are the

availability of a mechanism which encourages the setting

of the cheapest rates for the good.

P2 Different type of management accounting reports.

Mainly four types of reports are made, which are as follows.

Budget report: Budget report helps in doing business analysis of small type of business.

According to the period it is based on prior actual expenses. It compares expenses and revenue

activities among themselves. The report includes all accounts that have revenue and expenditure

related activities. No account related to profit and loss will be included in the report. The use of

this report is determined by which expenditure is much higher than its fixed level. So that the

amount spent on expenditure can be included in the performance of the budget. The same report

is used to make transactions on the financial results of the business. And this report proves very

beneficial for the business.

Cost report: The cost report covers all the facts related to material labour and overhead.

Inventory waste, hourly labour costs, and overhead costs are also part of cost managerial

accounting reports. They provide an exact understanding of all expenses, which is essential for

better optimization of resources among all departments. Cost Reports help management

managers to compute costs of items that are produced through unprocessed data.

Performance reports: Performance reports are created to review the performance of a company

as a whole as good as for each employees at the end of a term. Departmental performance reports

are also generated in very large organizations. Managers use these performance reports to make

key strategic decisions about the future of the organization. Individuals are often awarded for

their commitment to the organization and under performers are laid off or dealt with as required.

Performance-related managerial accounting reports also offer deep insight into the working of a

company. If company think that company should be performing in a certain capacity but

somehow that is not happening, these reports can point company towards flaws in the setup. The

role of performance reports is vital for any company to keep an accurate measure of their

strategy towards their mission.

4. Account Receivable Aging Reports: Tracking Company AR aging report in a regular

cadence Weekly/monthly will help company identify concerns before they become a cash-flow

availability of a mechanism which encourages the setting

of the cheapest rates for the good.

P2 Different type of management accounting reports.

Mainly four types of reports are made, which are as follows.

Budget report: Budget report helps in doing business analysis of small type of business.

According to the period it is based on prior actual expenses. It compares expenses and revenue

activities among themselves. The report includes all accounts that have revenue and expenditure

related activities. No account related to profit and loss will be included in the report. The use of

this report is determined by which expenditure is much higher than its fixed level. So that the

amount spent on expenditure can be included in the performance of the budget. The same report

is used to make transactions on the financial results of the business. And this report proves very

beneficial for the business.

Cost report: The cost report covers all the facts related to material labour and overhead.

Inventory waste, hourly labour costs, and overhead costs are also part of cost managerial

accounting reports. They provide an exact understanding of all expenses, which is essential for

better optimization of resources among all departments. Cost Reports help management

managers to compute costs of items that are produced through unprocessed data.

Performance reports: Performance reports are created to review the performance of a company

as a whole as good as for each employees at the end of a term. Departmental performance reports

are also generated in very large organizations. Managers use these performance reports to make

key strategic decisions about the future of the organization. Individuals are often awarded for

their commitment to the organization and under performers are laid off or dealt with as required.

Performance-related managerial accounting reports also offer deep insight into the working of a

company. If company think that company should be performing in a certain capacity but

somehow that is not happening, these reports can point company towards flaws in the setup. The

role of performance reports is vital for any company to keep an accurate measure of their

strategy towards their mission.

4. Account Receivable Aging Reports: Tracking Company AR aging report in a regular

cadence Weekly/monthly will help company identify concerns before they become a cash-flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

crunch to company business. This is a periodic report that categorizes a company's accounts

receivable according to the length of time an invoice has been outstanding. It is used as a gauge

to determine the financial health of a company's customers. If a particular customer is paying late

more often, company can evaluate your payment terms and conditions and bring about necessary

changes. It will also help company withhold product/service offerings until the amount is paid by

the customer on the specific due date.

The most important information which is required by the manager is to analyse the current

operation of company and the total revenues and expenses made on such operations to gain the

desired results.

Mostly this useful information is required by the internal managers who always worry to make

important plans in order to increase the company performance and make plan to increase profit

margin.

The collected information is required on regular basis mainly at the end of a working day so that

managers can make out the overall productivity and mark the areas which needed improvement

for future.

The main sources of information are the regular report prepare by the internal staff members and

the executive those are part of different external operation.

TASK 2

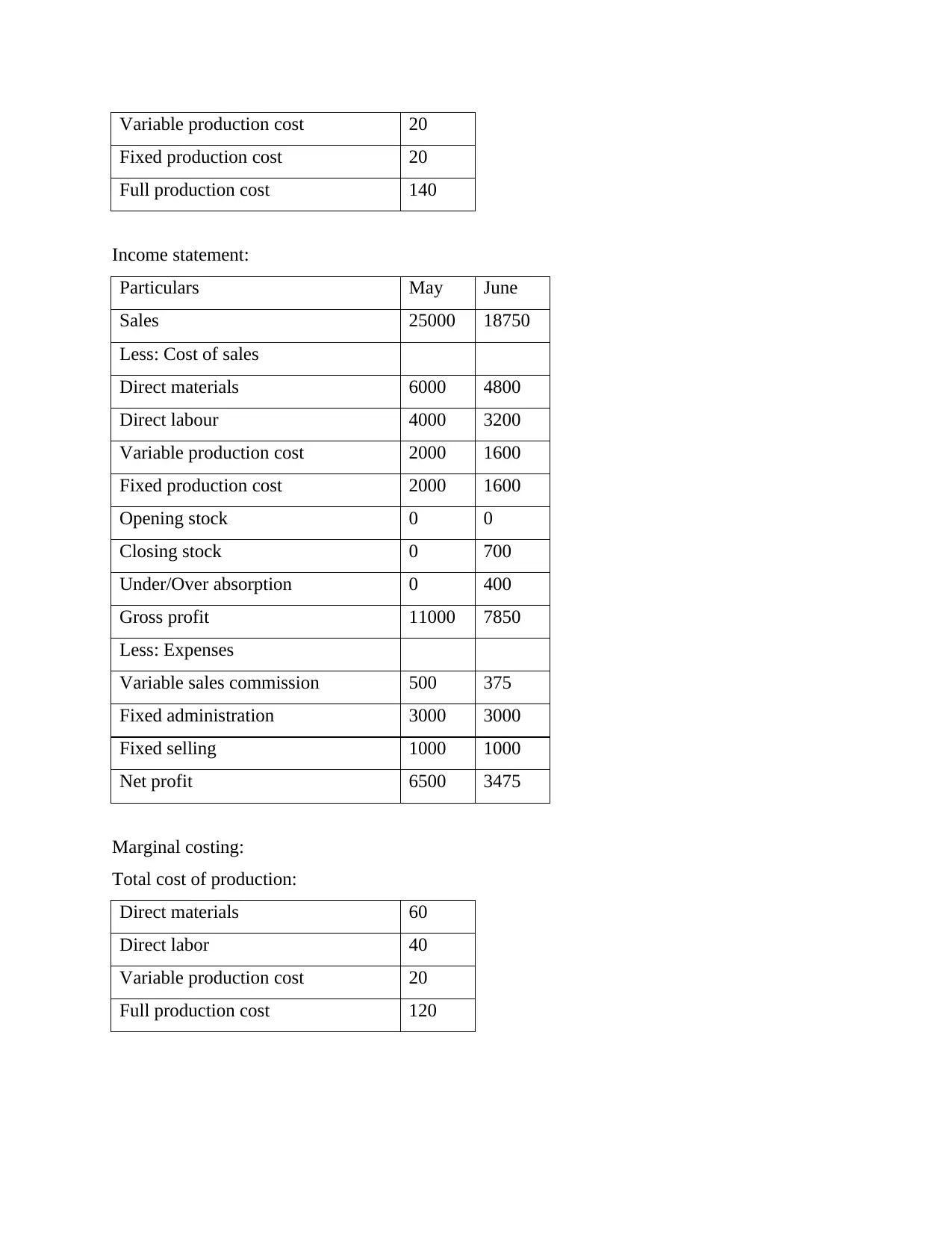

P3. Range of management accounting techniques.

Cost of absorption: This essentially means acquiring or absorbing something related to a

specific goal. It primarily involves all the costs involved in the production of a particular unit of

product. This system's key downside is that it offers the overall output expense but does not help

the decision-making process (Grabner and Moers, 2013).

Marginal costing: It is characterised as the increased costs imposed by firms to obtain an

additional item that helps to boost the amount of performance. Only contingent costs are used in

this inventory valuation while fixed costs are now measured against investment.

The income statement of Capital Joinery Ltd by using both the methods are shown below:

Total cost of production:

Direct materials 60

Direct labour 40

receivable according to the length of time an invoice has been outstanding. It is used as a gauge

to determine the financial health of a company's customers. If a particular customer is paying late

more often, company can evaluate your payment terms and conditions and bring about necessary

changes. It will also help company withhold product/service offerings until the amount is paid by

the customer on the specific due date.

The most important information which is required by the manager is to analyse the current

operation of company and the total revenues and expenses made on such operations to gain the

desired results.

Mostly this useful information is required by the internal managers who always worry to make

important plans in order to increase the company performance and make plan to increase profit

margin.

The collected information is required on regular basis mainly at the end of a working day so that

managers can make out the overall productivity and mark the areas which needed improvement

for future.

The main sources of information are the regular report prepare by the internal staff members and

the executive those are part of different external operation.

TASK 2

P3. Range of management accounting techniques.

Cost of absorption: This essentially means acquiring or absorbing something related to a

specific goal. It primarily involves all the costs involved in the production of a particular unit of

product. This system's key downside is that it offers the overall output expense but does not help

the decision-making process (Grabner and Moers, 2013).

Marginal costing: It is characterised as the increased costs imposed by firms to obtain an

additional item that helps to boost the amount of performance. Only contingent costs are used in

this inventory valuation while fixed costs are now measured against investment.

The income statement of Capital Joinery Ltd by using both the methods are shown below:

Total cost of production:

Direct materials 60

Direct labour 40

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable production cost 20

Fixed production cost 20

Full production cost 140

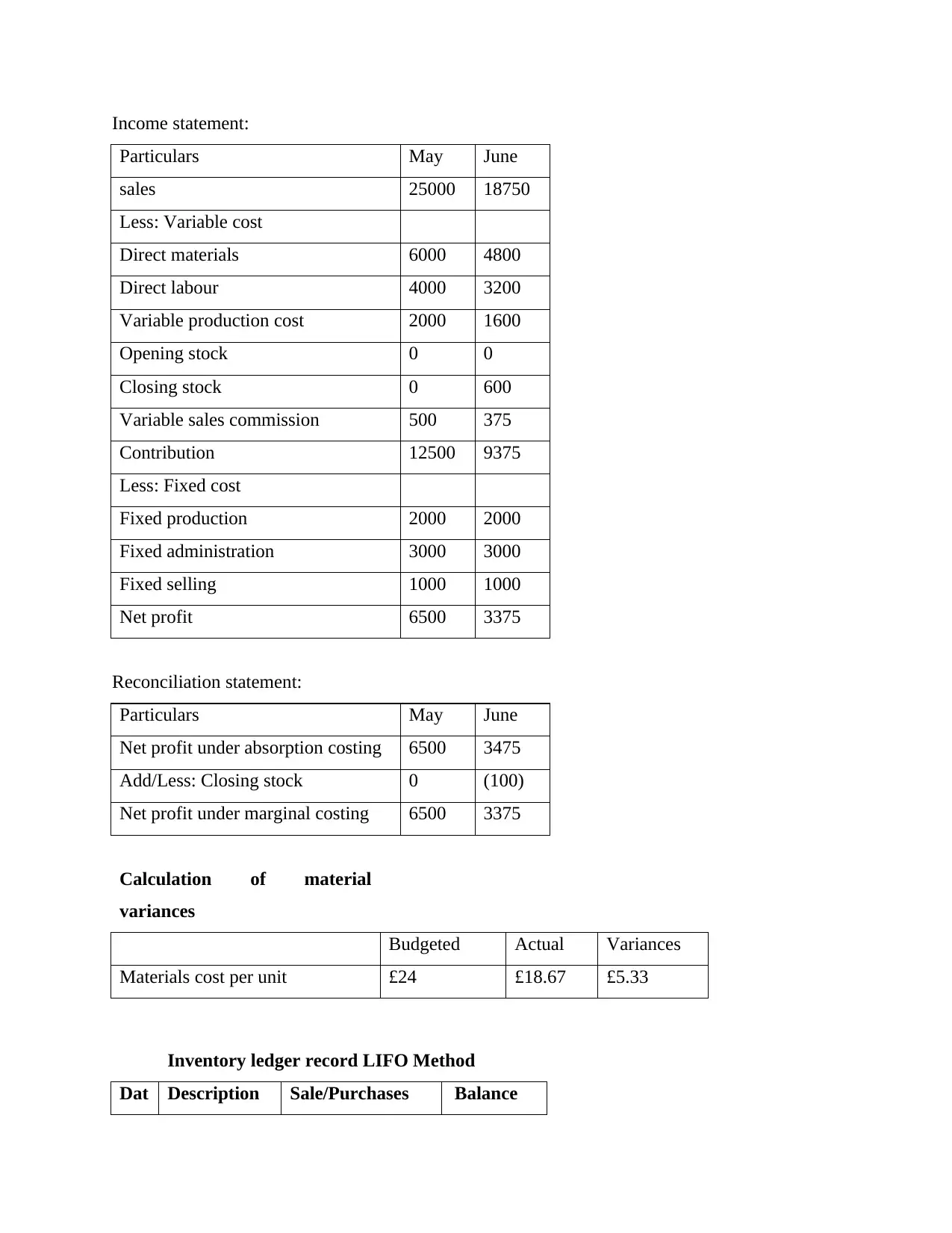

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

Total cost of production:

Direct materials 60

Direct labor 40

Variable production cost 20

Full production cost 120

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

Total cost of production:

Direct materials 60

Direct labor 40

Variable production cost 20

Full production cost 120

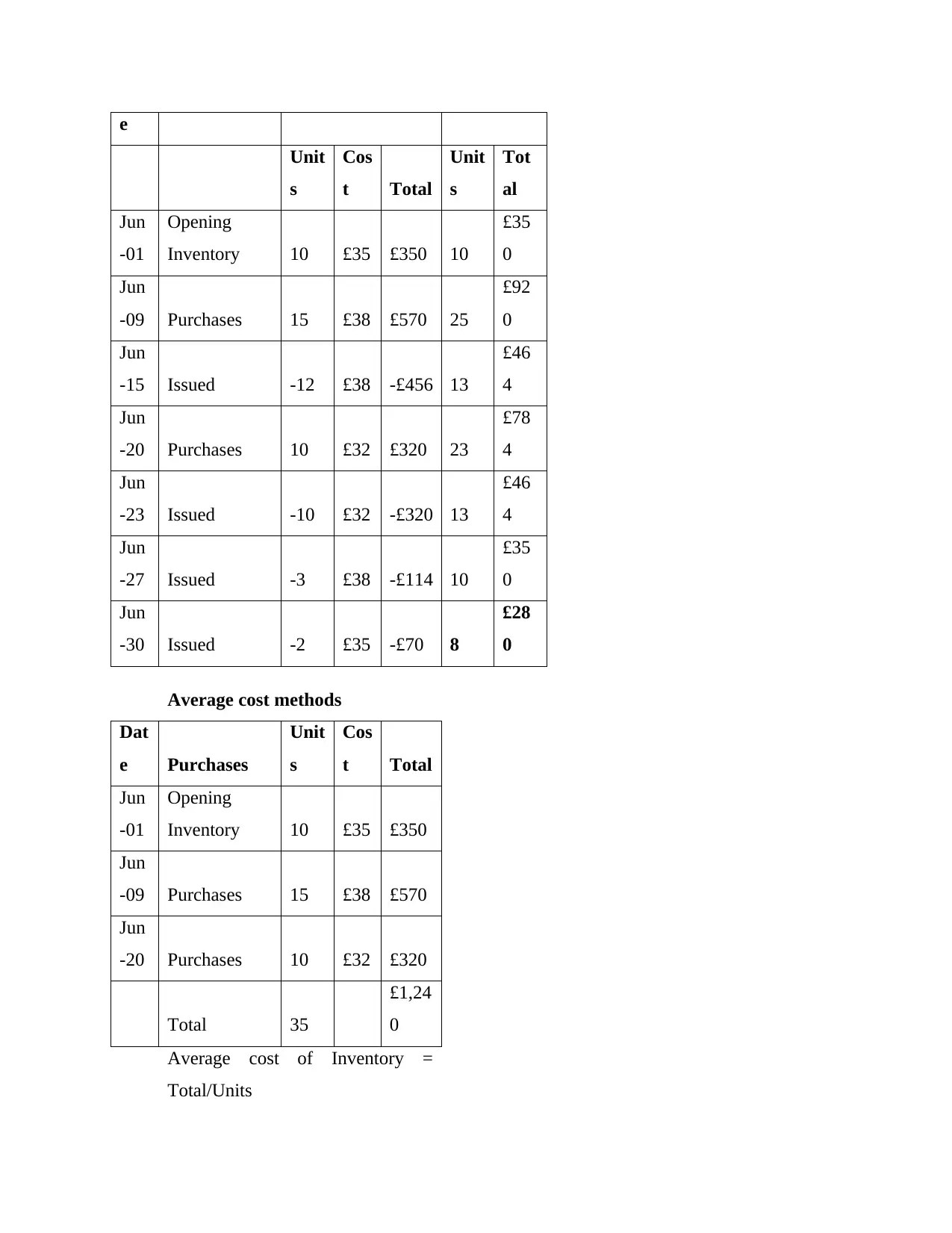

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement:

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat Description Sale/Purchases Balance

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Reconciliation statement:

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventory ledger record LIFO Method

Dat Description Sale/Purchases Balance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

e

Unit

s

Cos

t Total

Unit

s

Tot

al

Jun

-01

Opening

Inventory 10 £35 £350 10

£35

0

Jun

-09 Purchases 15 £38 £570 25

£92

0

Jun

-15 Issued -12 £38 -£456 13

£46

4

Jun

-20 Purchases 10 £32 £320 23

£78

4

Jun

-23 Issued -10 £32 -£320 13

£46

4

Jun

-27 Issued -3 £38 -£114 10

£35

0

Jun

-30 Issued -2 £35 -£70 8

£28

0

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun

-01

Opening

Inventory 10 £35 £350

Jun

-09 Purchases 15 £38 £570

Jun

-20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

Unit

s

Cos

t Total

Unit

s

Tot

al

Jun

-01

Opening

Inventory 10 £35 £350 10

£35

0

Jun

-09 Purchases 15 £38 £570 25

£92

0

Jun

-15 Issued -12 £38 -£456 13

£46

4

Jun

-20 Purchases 10 £32 £320 23

£78

4

Jun

-23 Issued -10 £32 -£320 13

£46

4

Jun

-27 Issued -3 £38 -£114 10

£35

0

Jun

-30 Issued -2 £35 -£70 8

£28

0

Average cost methods

Dat

e Purchases

Unit

s

Cos

t Total

Jun

-01

Opening

Inventory 10 £35 £350

Jun

-09 Purchases 15 £38 £570

Jun

-20 Purchases 10 £32 £320

Total 35

£1,24

0

Average cost of Inventory =

Total/Units

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 1240/35

= 35.42857143

TASK 3

P4.Planning tools used in management accounting.

In business terms, expenditures plan are described as a continuous and valuable report that

perhaps a company typically intends to build useful forecasts within a particular time period of

total revenue and expenditures. This is a comprehensive way of planning a budget which helps

KEF Ltd in decision-making, like:

Dependent on the essence of the market climate, the very first phase is concerned with

filtering assumptions.

The though is to discuss the challenges that can impede progress in results and effect.

Suitable time periods are fixed, such as yearly, weekly, etc.

Each category of costing is calculated, such as revenues and expenses.

For the time span, gross income is reported and real outcomes are contrasted against the

budgeted outcomes (Morden, 2016).

The challenges and disadvantages are discussed in addition to making the review of

future spending more credible.

It is reported that the key justification for budget planning is to decrease the risk prospects for

companies which may exist due to discrepancies between real and normal budget performance.

There are different kinds of expenditures plan that are develop by KEF Ltd as a forecasting

mechanism to simplify the budget management process. Under, these would be characterised:

Flexible budgets: Because of any disaster or confusion that cannot function as per old funding

levels, this programme is useful in changing the business’ financial budgets. This budget aims to

provide fresh spending that can be created by any potential scenario in KEF Ltd but also aims to

systematically document new opportunities to increase profit in a financial year. KEF Ltd's

adjustable budget is based on modifications resulting from new in semi-variable, production

overheads. The following are the various benefits and drawbacks of this approach:

Benefits:

= 35.42857143

TASK 3

P4.Planning tools used in management accounting.

In business terms, expenditures plan are described as a continuous and valuable report that

perhaps a company typically intends to build useful forecasts within a particular time period of

total revenue and expenditures. This is a comprehensive way of planning a budget which helps

KEF Ltd in decision-making, like:

Dependent on the essence of the market climate, the very first phase is concerned with

filtering assumptions.

The though is to discuss the challenges that can impede progress in results and effect.

Suitable time periods are fixed, such as yearly, weekly, etc.

Each category of costing is calculated, such as revenues and expenses.

For the time span, gross income is reported and real outcomes are contrasted against the

budgeted outcomes (Morden, 2016).

The challenges and disadvantages are discussed in addition to making the review of

future spending more credible.

It is reported that the key justification for budget planning is to decrease the risk prospects for

companies which may exist due to discrepancies between real and normal budget performance.

There are different kinds of expenditures plan that are develop by KEF Ltd as a forecasting

mechanism to simplify the budget management process. Under, these would be characterised:

Flexible budgets: Because of any disaster or confusion that cannot function as per old funding

levels, this programme is useful in changing the business’ financial budgets. This budget aims to

provide fresh spending that can be created by any potential scenario in KEF Ltd but also aims to

systematically document new opportunities to increase profit in a financial year. KEF Ltd's

adjustable budget is based on modifications resulting from new in semi-variable, production

overheads. The following are the various benefits and drawbacks of this approach:

Benefits:

It helps internal management to take the right cost reduction steps because it is fundamentally

positioned for the new industry dynamics (Siverbo, 2014). This budget assists managers of KEF

Ltd in order to allow possible improvements and modifications to the overall expense and in

order to raise the profitability within different operations.

Disadvantage:

This kind of budget is complicated and dynamic in nature involving professional labour. It takes

additional effort and resources, lacks motivation for the worker of KEF Ltd which force to

implement more cost on hiring highly talented staff.

Zero-based budgeting: It is considered the most efficient budgetary control technique that

facilitates the process of creating new expenditures plan without taking related legislation into

account. ZBB's procedure creates re-evaluating each item inside the working capital but also

justifying the extra fees invested by various areas. In KEF Ltd, the whole budget helps to

estimate the whole expenses associated with producing luxury items accrued based on the

current costs of past information. There are different benefits and drawbacks that are described

below:

Benefits:

This plan enables to provide efficiency, precision and outcomes because each component of

working capital is re-evaluated. Basically, ZBB offers better and transparent communication

between different departments in order to make decisions more reliably and with accurate results

(Booth, 2018). This budget is of primary importance and helps to reduce the multiple features of

KEF Ltd in order to maximize revenue.

Disadvantage:

The big issue that needs skilled labour and much more period to predict outcomes. Such

expenditures plan also lack the skills necessary to prepare a budget. As a result company have to

arrange regular meeting for the staff to understand the working of this budget which increase the

external expenditure and impact the profit in adverse manner.

P5. Comparison of organisations adapting management accounting to respond to financial

problems.

Nowadays, each particular company faces various kinds of challenges in the corporate

environment, because of which it is crucial to decrease whole operating and commercial

activities. There are different negatives to the financial position, including the failure to produce

positioned for the new industry dynamics (Siverbo, 2014). This budget assists managers of KEF

Ltd in order to allow possible improvements and modifications to the overall expense and in

order to raise the profitability within different operations.

Disadvantage:

This kind of budget is complicated and dynamic in nature involving professional labour. It takes

additional effort and resources, lacks motivation for the worker of KEF Ltd which force to

implement more cost on hiring highly talented staff.

Zero-based budgeting: It is considered the most efficient budgetary control technique that

facilitates the process of creating new expenditures plan without taking related legislation into

account. ZBB's procedure creates re-evaluating each item inside the working capital but also

justifying the extra fees invested by various areas. In KEF Ltd, the whole budget helps to

estimate the whole expenses associated with producing luxury items accrued based on the

current costs of past information. There are different benefits and drawbacks that are described

below:

Benefits:

This plan enables to provide efficiency, precision and outcomes because each component of

working capital is re-evaluated. Basically, ZBB offers better and transparent communication

between different departments in order to make decisions more reliably and with accurate results

(Booth, 2018). This budget is of primary importance and helps to reduce the multiple features of

KEF Ltd in order to maximize revenue.

Disadvantage:

The big issue that needs skilled labour and much more period to predict outcomes. Such

expenditures plan also lack the skills necessary to prepare a budget. As a result company have to

arrange regular meeting for the staff to understand the working of this budget which increase the

external expenditure and impact the profit in adverse manner.

P5. Comparison of organisations adapting management accounting to respond to financial

problems.

Nowadays, each particular company faces various kinds of challenges in the corporate

environment, because of which it is crucial to decrease whole operating and commercial

activities. There are different negatives to the financial position, including the failure to produce

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.