Management Accounting Systems & Techniques Report - BTEC Unit 5

VerifiedAdded on 2023/01/03

|18

|4050

|81

Report

AI Summary

This report analyzes management accounting systems and techniques through the case study of Capital Joinery Limited. It explores the meaning and requirements of management accounting, detailing various systems like cost accounting, price optimization, inventory management, and job costing. The report examines different modules such as performance reports, cost reports, budget reports, and accounts receivable reports. It also calculates costs using absorption and marginal costing techniques, along with material variances and inventory valuation methods like LIFO and average cost methods. Furthermore, the report discusses the benefits of managerial accounting systems and the relevance of integrating them with managerial reports. It evaluates the advantages and disadvantages of planning tools, including budgetary techniques and activity-based budgeting, and analyzes their use in preparing budgets. Finally, the report compares different management accounting tools used to solve financial problems and evaluates the application of planning tools in this context.

Management Accounting Systems &

Techniques

Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Brief explanation regarding meaning of management accounting and requirement of

different accounting system.........................................................................................................3

P2 Explanation of different modules use for management accounting system...........................4

M1 Benefits of using different kinds of managerial accounting system.....................................5

D1 Evaluation of relevance of integration of management accounting system with managerial

reports..........................................................................................................................................6

TASK 2............................................................................................................................................7

P3Calcluation of cost by using managerial accounting technique..............................................7

M2Breif description regarding production of finance report.....................................................10

D2Fiananacil report which help in applying accurate data........................................................10

TASK 3..........................................................................................................................................10

P4Explanation of advantage & disadvantage of various types of planning tools......................10

M3Aanayisis use of planning tools for prepare budget.............................................................12

TASK 4..........................................................................................................................................12

P5 Comparison of different management accounting tools how they use for solve financial

problems.....................................................................................................................................12

M4 Use of management accounting tools to solve financial problem.......................................15

D3 Evaluation how planning tools are used to solve financial problems.................................15

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Brief explanation regarding meaning of management accounting and requirement of

different accounting system.........................................................................................................3

P2 Explanation of different modules use for management accounting system...........................4

M1 Benefits of using different kinds of managerial accounting system.....................................5

D1 Evaluation of relevance of integration of management accounting system with managerial

reports..........................................................................................................................................6

TASK 2............................................................................................................................................7

P3Calcluation of cost by using managerial accounting technique..............................................7

M2Breif description regarding production of finance report.....................................................10

D2Fiananacil report which help in applying accurate data........................................................10

TASK 3..........................................................................................................................................10

P4Explanation of advantage & disadvantage of various types of planning tools......................10

M3Aanayisis use of planning tools for prepare budget.............................................................12

TASK 4..........................................................................................................................................12

P5 Comparison of different management accounting tools how they use for solve financial

problems.....................................................................................................................................12

M4 Use of management accounting tools to solve financial problem.......................................15

D3 Evaluation how planning tools are used to solve financial problems.................................15

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is part of accounting approach which organizations use for

analysing, recording managing and controlling their accounting information in systematic way.

Which useful in take essential business decision by representing accounting information as per

the norms of accounting standard. To understand this concept Capital joinery limited has been

taken. It is medium size organization. This report has been define use of different types of

management accounting system which useful in decision making. Relevance of management

account report and technique use for determine cost as well as usefulness of planning tool for

recognize issue arising of financial problem and use of benchmarking, balance scorecard through

which they can resolve problem. All theses information has been describe in systematic manner.

TASK 1

P1 Brief explanation regarding meaning of management accounting and requirement of different

accounting system.

Management accounting: This term is combination of two essential norms of business.

The first one is management , which refer as an art of getting things and activities done by other

personal by influencing them. The other one is accounting which means process of identifying ,

analysing, recording and presenting data in effective way. Management accounting is

combination of theses word which means managing accounting record in a way which help in

influencing people and took decision by representing accounting data in systematic manner.

There are various system has been used while applying management accounting approach

following are define below

Cost accounting system: It is consider as essential system of management accounting

approach. There are various technique has been used by organizations through which

they can able to find out value of cost as well as profit. In context with Capital joinery

limited, they used cost accounting system through which they can manage all the relevant

cost, of raw materiel, process costing and cost incurred for distributing products.

Manager of cost accounting use this system to determine cost required for manufacturing

their business products which include, furniture, door, table etc (Quattrone, 2016).

Management accounting is part of accounting approach which organizations use for

analysing, recording managing and controlling their accounting information in systematic way.

Which useful in take essential business decision by representing accounting information as per

the norms of accounting standard. To understand this concept Capital joinery limited has been

taken. It is medium size organization. This report has been define use of different types of

management accounting system which useful in decision making. Relevance of management

account report and technique use for determine cost as well as usefulness of planning tool for

recognize issue arising of financial problem and use of benchmarking, balance scorecard through

which they can resolve problem. All theses information has been describe in systematic manner.

TASK 1

P1 Brief explanation regarding meaning of management accounting and requirement of different

accounting system.

Management accounting: This term is combination of two essential norms of business.

The first one is management , which refer as an art of getting things and activities done by other

personal by influencing them. The other one is accounting which means process of identifying ,

analysing, recording and presenting data in effective way. Management accounting is

combination of theses word which means managing accounting record in a way which help in

influencing people and took decision by representing accounting data in systematic manner.

There are various system has been used while applying management accounting approach

following are define below

Cost accounting system: It is consider as essential system of management accounting

approach. There are various technique has been used by organizations through which

they can able to find out value of cost as well as profit. In context with Capital joinery

limited, they used cost accounting system through which they can manage all the relevant

cost, of raw materiel, process costing and cost incurred for distributing products.

Manager of cost accounting use this system to determine cost required for manufacturing

their business products which include, furniture, door, table etc (Quattrone, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimization system: This system is used for determine price of relevant product.

Success of business entity depend on the strategy they use for select particular price.

Price skimming, penetration, premium and price formulation of particular rate all these

are strategies regarding price which manager can adopt. Capital joinery limited, use

skimping price policy which help in provides satisfaction to customers as well as help in

gain profits. Price of Capital joinery limited, set on the basis of expectation and market

demand of customers. Price optimization system beneficial for internal as well as external

stockholders as this will useful in attain business profits.

Inventory management system: Management accounting is useful for maintain level of

stock. Stock management system is help in recognize maximum, minimum and

dangerous level of stock on the basis of that management department formulate policies t

control cost of managing and storing inventory. Capital joinery limited, apply technique

used in stock management system which includes, FIFO, LIFO, JIT, ABC analysing, all

theses are help in recording inventory in effective manner. This will useful for Capital

joinery limited, to recognize value of under stock (Guinea, 2016).

Job costing system: This system is used to determine value of job order, this system help

in recognize the cost incurred for complete or fulfil requirement of their clients. as

different customer according to their needs take order and measured value of rational job.

Capital joinery limited, use job costing system through which they can able to find out

cost required for running business activities. Theses information are useful for finance

manager on the basis of that they formulate their trading statement.

P2 Explanation of different modules use for management accounting system

Report: The term report has been consider as document which help in defining all the

summery and information of business activities in systematic manner. It is record of all business

transactions which are essential. Following are types of report which management department of

Capital joinery limited, has been formulated

Performance report: This report is consider as combination of all the reports as it

proved base for measuring performance of each department. This report gives

information regarding the overall performance, target achieved by departments as well as

individual performance of workforce. Capital joinery limited, formulate performance

Success of business entity depend on the strategy they use for select particular price.

Price skimming, penetration, premium and price formulation of particular rate all these

are strategies regarding price which manager can adopt. Capital joinery limited, use

skimping price policy which help in provides satisfaction to customers as well as help in

gain profits. Price of Capital joinery limited, set on the basis of expectation and market

demand of customers. Price optimization system beneficial for internal as well as external

stockholders as this will useful in attain business profits.

Inventory management system: Management accounting is useful for maintain level of

stock. Stock management system is help in recognize maximum, minimum and

dangerous level of stock on the basis of that management department formulate policies t

control cost of managing and storing inventory. Capital joinery limited, apply technique

used in stock management system which includes, FIFO, LIFO, JIT, ABC analysing, all

theses are help in recording inventory in effective manner. This will useful for Capital

joinery limited, to recognize value of under stock (Guinea, 2016).

Job costing system: This system is used to determine value of job order, this system help

in recognize the cost incurred for complete or fulfil requirement of their clients. as

different customer according to their needs take order and measured value of rational job.

Capital joinery limited, use job costing system through which they can able to find out

cost required for running business activities. Theses information are useful for finance

manager on the basis of that they formulate their trading statement.

P2 Explanation of different modules use for management accounting system

Report: The term report has been consider as document which help in defining all the

summery and information of business activities in systematic manner. It is record of all business

transactions which are essential. Following are types of report which management department of

Capital joinery limited, has been formulated

Performance report: This report is consider as combination of all the reports as it

proved base for measuring performance of each department. This report gives

information regarding the overall performance, target achieved by departments as well as

individual performance of workforce. Capital joinery limited, formulate performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

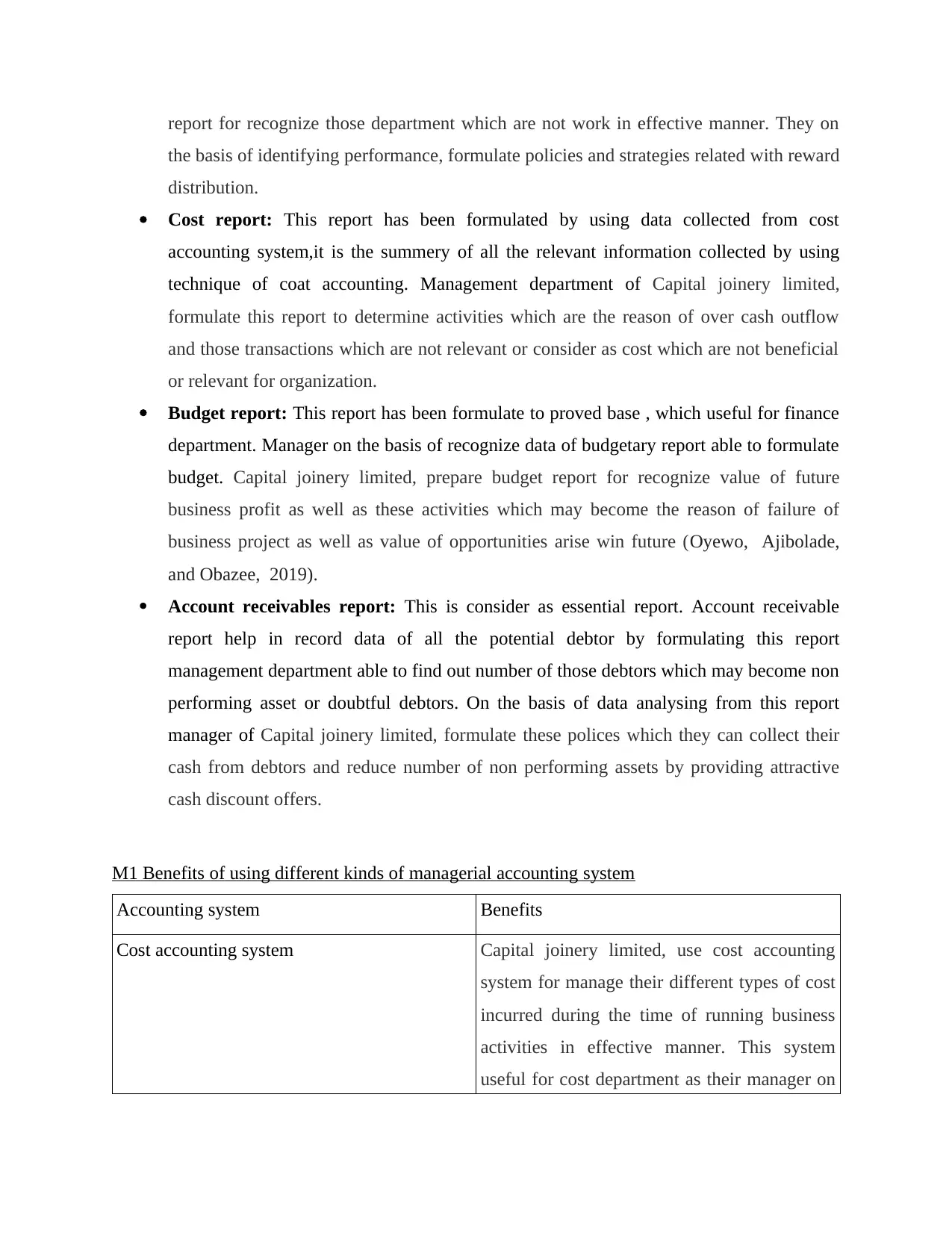

report for recognize those department which are not work in effective manner. They on

the basis of identifying performance, formulate policies and strategies related with reward

distribution.

Cost report: This report has been formulated by using data collected from cost

accounting system,it is the summery of all the relevant information collected by using

technique of coat accounting. Management department of Capital joinery limited,

formulate this report to determine activities which are the reason of over cash outflow

and those transactions which are not relevant or consider as cost which are not beneficial

or relevant for organization.

Budget report: This report has been formulate to proved base , which useful for finance

department. Manager on the basis of recognize data of budgetary report able to formulate

budget. Capital joinery limited, prepare budget report for recognize value of future

business profit as well as these activities which may become the reason of failure of

business project as well as value of opportunities arise win future (Oyewo, Ajibolade,

and Obazee, 2019).

Account receivables report: This is consider as essential report. Account receivable

report help in record data of all the potential debtor by formulating this report

management department able to find out number of those debtors which may become non

performing asset or doubtful debtors. On the basis of data analysing from this report

manager of Capital joinery limited, formulate these polices which they can collect their

cash from debtors and reduce number of non performing assets by providing attractive

cash discount offers.

M1 Benefits of using different kinds of managerial accounting system

Accounting system Benefits

Cost accounting system Capital joinery limited, use cost accounting

system for manage their different types of cost

incurred during the time of running business

activities in effective manner. This system

useful for cost department as their manager on

the basis of identifying performance, formulate policies and strategies related with reward

distribution.

Cost report: This report has been formulated by using data collected from cost

accounting system,it is the summery of all the relevant information collected by using

technique of coat accounting. Management department of Capital joinery limited,

formulate this report to determine activities which are the reason of over cash outflow

and those transactions which are not relevant or consider as cost which are not beneficial

or relevant for organization.

Budget report: This report has been formulate to proved base , which useful for finance

department. Manager on the basis of recognize data of budgetary report able to formulate

budget. Capital joinery limited, prepare budget report for recognize value of future

business profit as well as these activities which may become the reason of failure of

business project as well as value of opportunities arise win future (Oyewo, Ajibolade,

and Obazee, 2019).

Account receivables report: This is consider as essential report. Account receivable

report help in record data of all the potential debtor by formulating this report

management department able to find out number of those debtors which may become non

performing asset or doubtful debtors. On the basis of data analysing from this report

manager of Capital joinery limited, formulate these polices which they can collect their

cash from debtors and reduce number of non performing assets by providing attractive

cash discount offers.

M1 Benefits of using different kinds of managerial accounting system

Accounting system Benefits

Cost accounting system Capital joinery limited, use cost accounting

system for manage their different types of cost

incurred during the time of running business

activities in effective manner. This system

useful for cost department as their manager on

the basis of information collected from this

system use to formulate policies and strategies

which help in reduce cost of product produce

by Capital joinery limited.

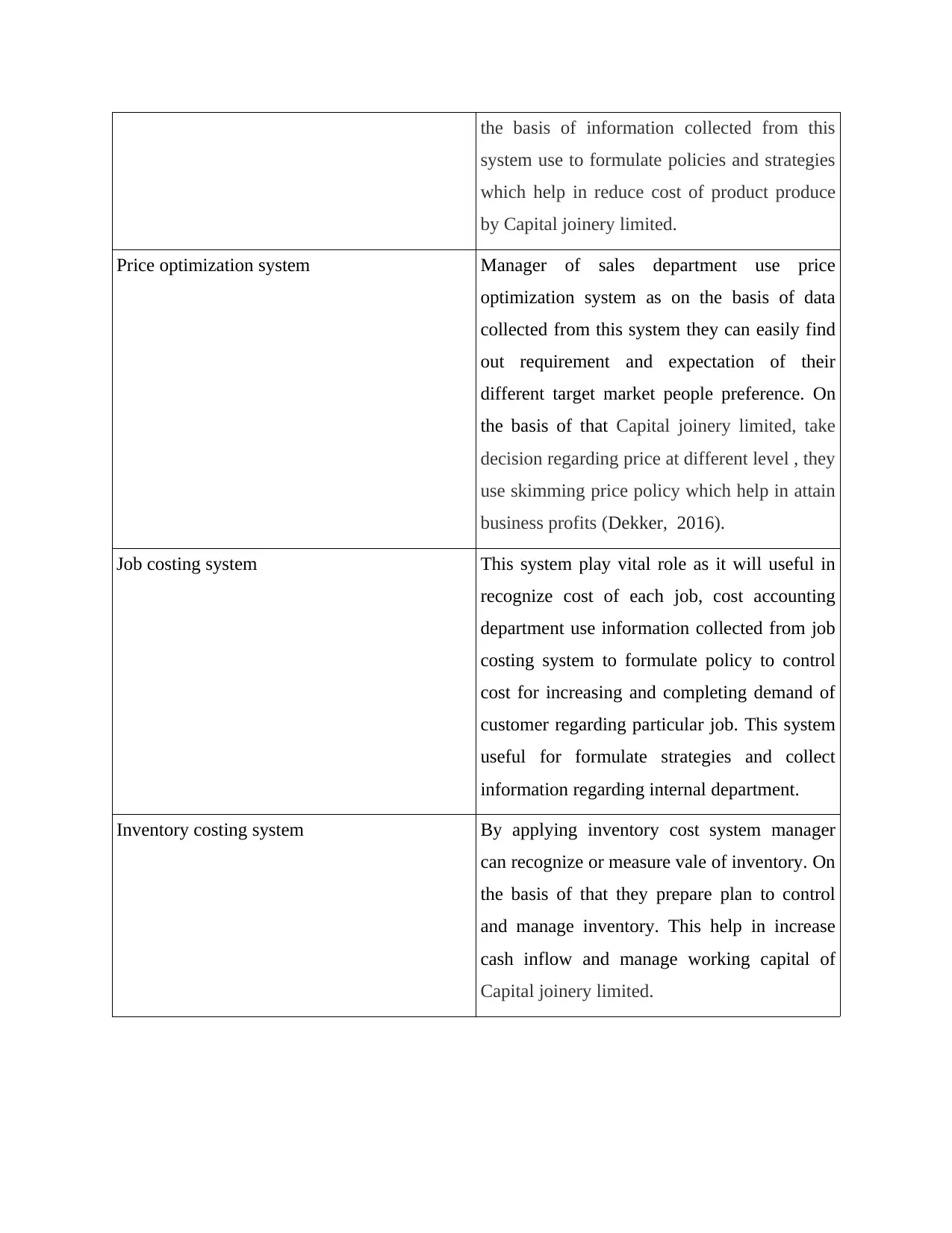

Price optimization system Manager of sales department use price

optimization system as on the basis of data

collected from this system they can easily find

out requirement and expectation of their

different target market people preference. On

the basis of that Capital joinery limited, take

decision regarding price at different level , they

use skimming price policy which help in attain

business profits (Dekker, 2016).

Job costing system This system play vital role as it will useful in

recognize cost of each job, cost accounting

department use information collected from job

costing system to formulate policy to control

cost for increasing and completing demand of

customer regarding particular job. This system

useful for formulate strategies and collect

information regarding internal department.

Inventory costing system By applying inventory cost system manager

can recognize or measure vale of inventory. On

the basis of that they prepare plan to control

and manage inventory. This help in increase

cash inflow and manage working capital of

Capital joinery limited.

system use to formulate policies and strategies

which help in reduce cost of product produce

by Capital joinery limited.

Price optimization system Manager of sales department use price

optimization system as on the basis of data

collected from this system they can easily find

out requirement and expectation of their

different target market people preference. On

the basis of that Capital joinery limited, take

decision regarding price at different level , they

use skimming price policy which help in attain

business profits (Dekker, 2016).

Job costing system This system play vital role as it will useful in

recognize cost of each job, cost accounting

department use information collected from job

costing system to formulate policy to control

cost for increasing and completing demand of

customer regarding particular job. This system

useful for formulate strategies and collect

information regarding internal department.

Inventory costing system By applying inventory cost system manager

can recognize or measure vale of inventory. On

the basis of that they prepare plan to control

and manage inventory. This help in increase

cash inflow and manage working capital of

Capital joinery limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

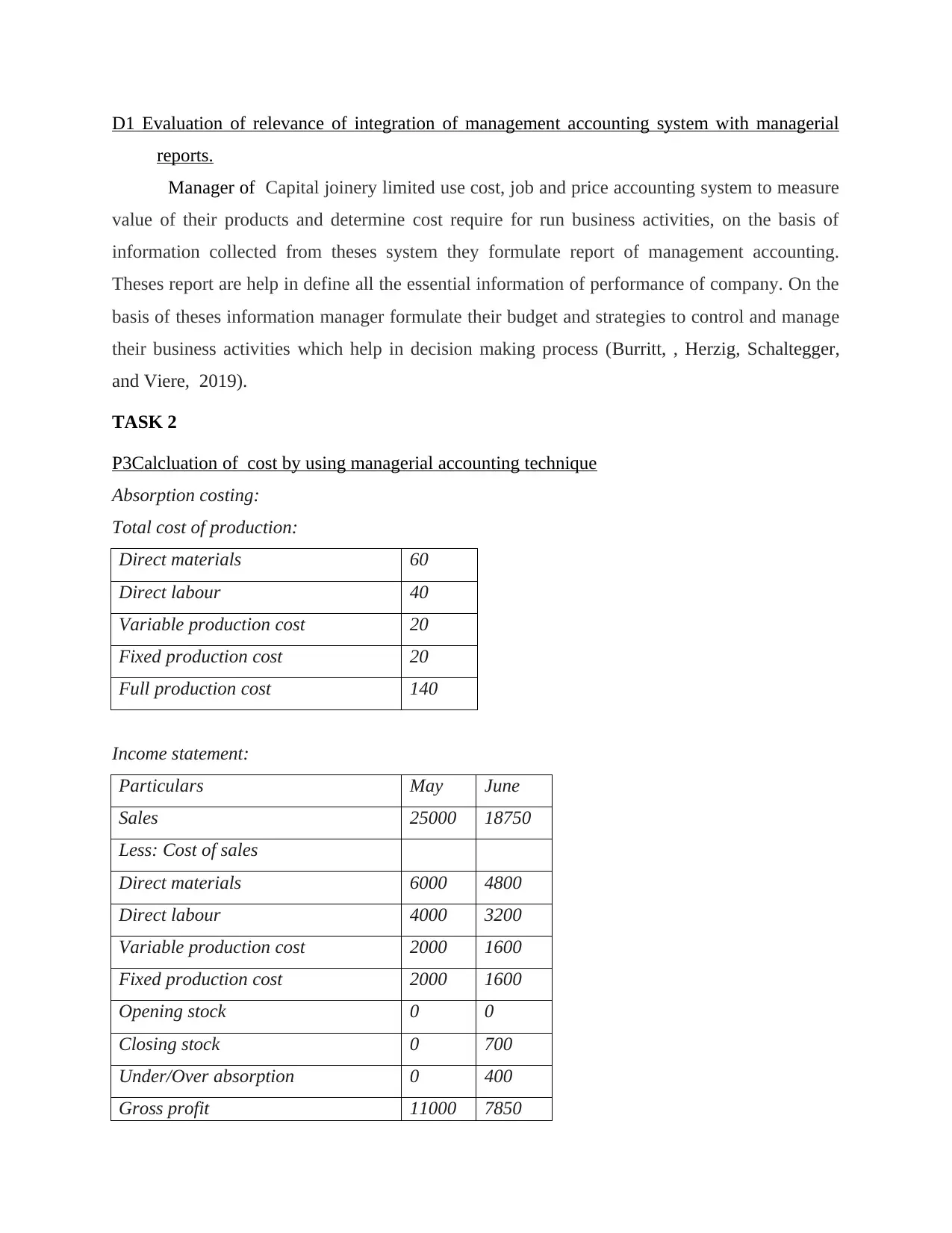

D1 Evaluation of relevance of integration of management accounting system with managerial

reports.

Manager of Capital joinery limited use cost, job and price accounting system to measure

value of their products and determine cost require for run business activities, on the basis of

information collected from theses system they formulate report of management accounting.

Theses report are help in define all the essential information of performance of company. On the

basis of theses information manager formulate their budget and strategies to control and manage

their business activities which help in decision making process (Burritt, , Herzig, Schaltegger,

and Viere, 2019).

TASK 2

P3Calcluation of cost by using managerial accounting technique

Absorption costing:

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

reports.

Manager of Capital joinery limited use cost, job and price accounting system to measure

value of their products and determine cost require for run business activities, on the basis of

information collected from theses system they formulate report of management accounting.

Theses report are help in define all the essential information of performance of company. On the

basis of theses information manager formulate their budget and strategies to control and manage

their business activities which help in decision making process (Burritt, , Herzig, Schaltegger,

and Viere, 2019).

TASK 2

P3Calcluation of cost by using managerial accounting technique

Absorption costing:

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Fixed production cost 20

Full production cost 140

Income statement:

Particulars May June

Sales 25000 18750

Less: Cost of sales

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Fixed production cost 2000 1600

Opening stock 0 0

Closing stock 0 700

Under/Over absorption 0 400

Gross profit 11000 7850

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

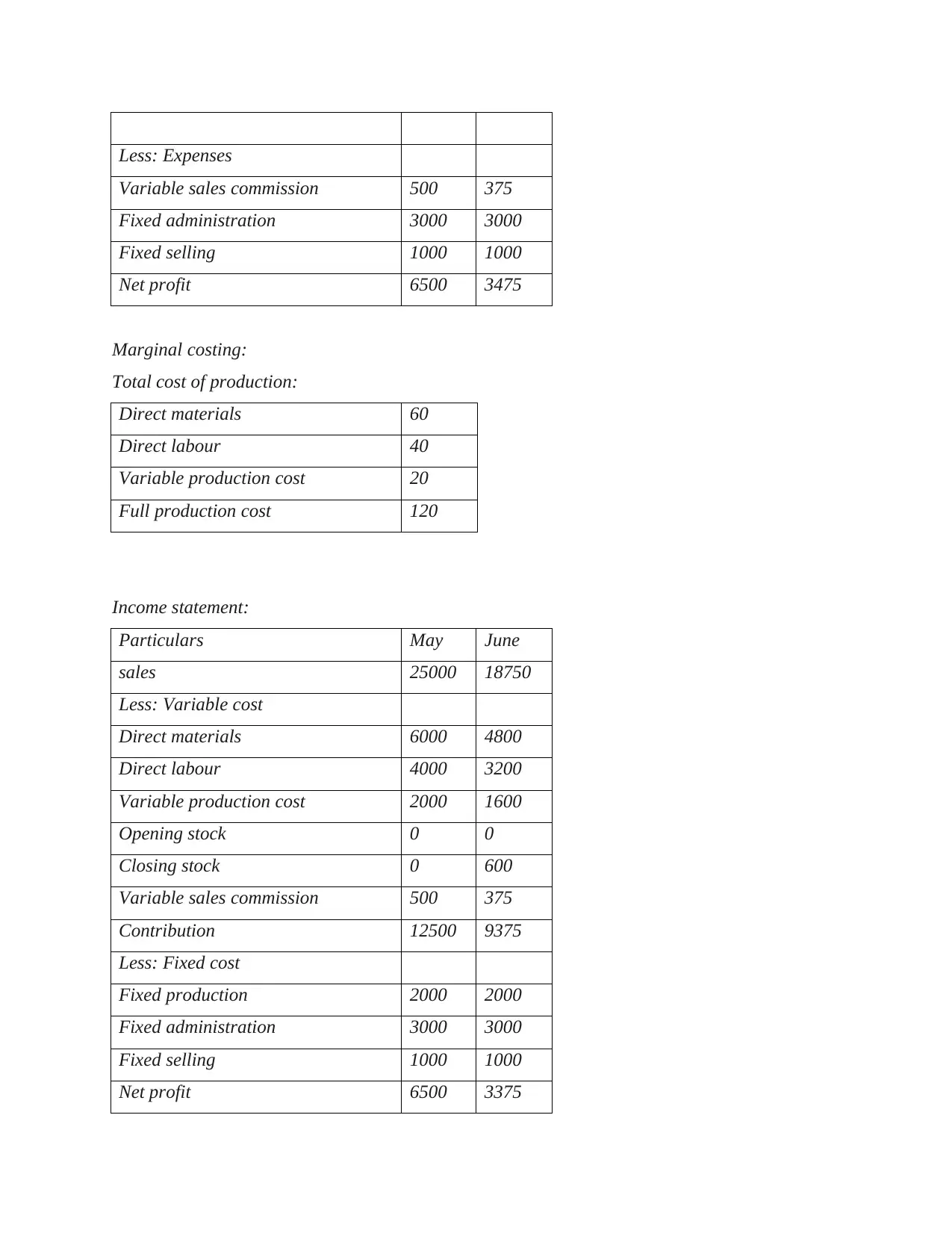

Less: Expenses

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

Variable sales commission 500 375

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3475

Marginal costing:

Total cost of production:

Direct materials 60

Direct labour 40

Variable production cost 20

Full production cost 120

Income statement:

Particulars May June

sales 25000 18750

Less: Variable cost

Direct materials 6000 4800

Direct labour 4000 3200

Variable production cost 2000 1600

Opening stock 0 0

Closing stock 0 600

Variable sales commission 500 375

Contribution 12500 9375

Less: Fixed cost

Fixed production 2000 2000

Fixed administration 3000 3000

Fixed selling 1000 1000

Net profit 6500 3375

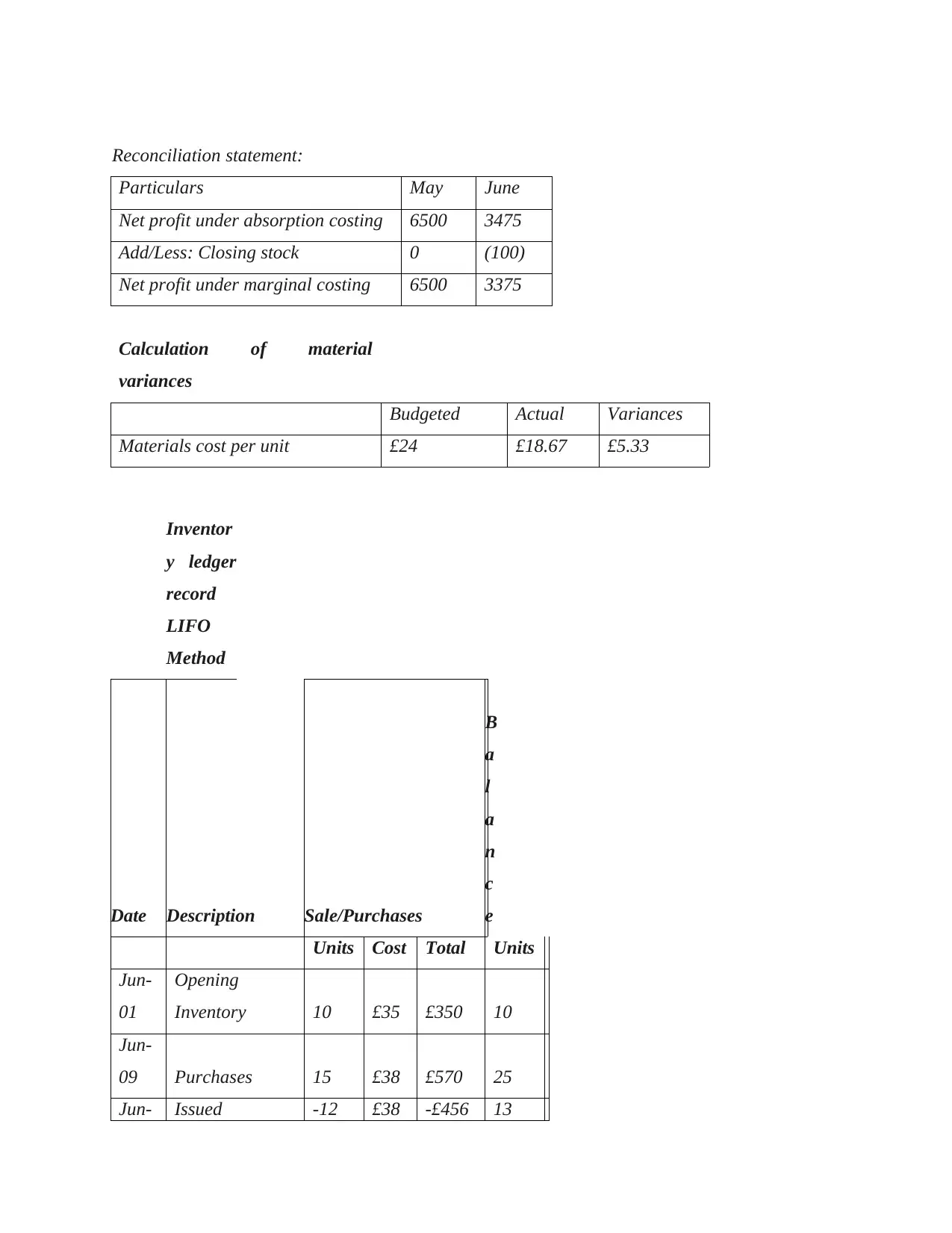

Reconciliation statement:

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventor

y ledger

record

LIFO

Method

Date Description Sale/Purchases

B

a

l

a

n

c

e

Units Cost Total Units

Jun-

01

Opening

Inventory 10 £35 £350 10

Jun-

09 Purchases 15 £38 £570 25

Jun- Issued -12 £38 -£456 13

Particulars May June

Net profit under absorption costing 6500 3475

Add/Less: Closing stock 0 (100)

Net profit under marginal costing 6500 3375

Calculation of material

variances

Budgeted Actual Variances

Materials cost per unit £24 £18.67 £5.33

Inventor

y ledger

record

LIFO

Method

Date Description Sale/Purchases

B

a

l

a

n

c

e

Units Cost Total Units

Jun-

01

Opening

Inventory 10 £35 £350 10

Jun-

09 Purchases 15 £38 £570 25

Jun- Issued -12 £38 -£456 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

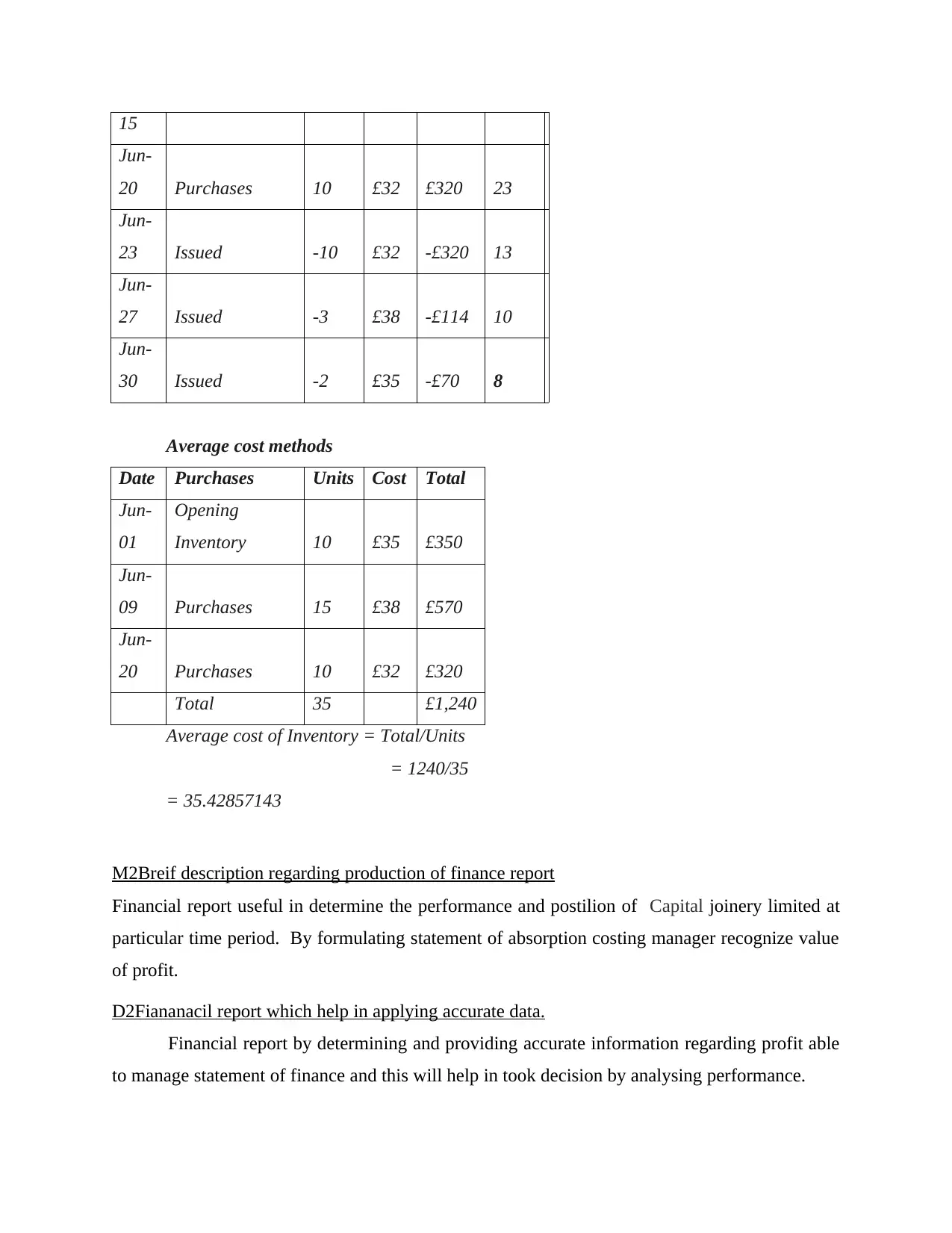

15

Jun-

20 Purchases 10 £32 £320 23

Jun-

23 Issued -10 £32 -£320 13

Jun-

27 Issued -3 £38 -£114 10

Jun-

30 Issued -2 £35 -£70 8

Average cost methods

Date Purchases Units Cost Total

Jun-

01

Opening

Inventory 10 £35 £350

Jun-

09 Purchases 15 £38 £570

Jun-

20 Purchases 10 £32 £320

Total 35 £1,240

Average cost of Inventory = Total/Units

= 1240/35

= 35.42857143

M2Breif description regarding production of finance report

Financial report useful in determine the performance and postilion of Capital joinery limited at

particular time period. By formulating statement of absorption costing manager recognize value

of profit.

D2Fiananacil report which help in applying accurate data.

Financial report by determining and providing accurate information regarding profit able

to manage statement of finance and this will help in took decision by analysing performance.

Jun-

20 Purchases 10 £32 £320 23

Jun-

23 Issued -10 £32 -£320 13

Jun-

27 Issued -3 £38 -£114 10

Jun-

30 Issued -2 £35 -£70 8

Average cost methods

Date Purchases Units Cost Total

Jun-

01

Opening

Inventory 10 £35 £350

Jun-

09 Purchases 15 £38 £570

Jun-

20 Purchases 10 £32 £320

Total 35 £1,240

Average cost of Inventory = Total/Units

= 1240/35

= 35.42857143

M2Breif description regarding production of finance report

Financial report useful in determine the performance and postilion of Capital joinery limited at

particular time period. By formulating statement of absorption costing manager recognize value

of profit.

D2Fiananacil report which help in applying accurate data.

Financial report by determining and providing accurate information regarding profit able

to manage statement of finance and this will help in took decision by analysing performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4Explanation of advantage & disadvantage of various types of planning tools.

Planning tool: T hoes technique or tools which help manager to formulate plan are known

as planning tools. Difference kind of tools which Capital joinery limited, use are define below

Budgetary techniques: The term budget is define as numerical statement which is

formulated to define value of future profit and loss. There are various way through which

manager can formulate their budget all theses are define below

Activity based budgeting: This is consider as type of budget in which all the information are

collected on the basis of allocation of record, cost incurred for particular time period. Thus it is

known as activity based budget:

Advantage:

Activity based budget help in allocate resource in effective manner, and by formulating

this budget manager able to find out accurate result (Ghasemi, Mohamad, Karami, Bajuri, and

Asgharizade, 2016).

This budget is useful in providing accurate business information.

Disadvantage

Activity based budget is time consuming budget as well a it also cost incurred activity.

Formulate budget by using this method is complex procedure.

Zero based budgeting: In this type of planning tool, budget are prepared from zero or

initial level. Manager not use previous data to formulate this budget, thus it is known as zero

based budget.

Advantage:

This method of budget is useful for newly set up business entities a information are

accurate and reliable.

Zero based budget useful in cut throat redundant business activities. And help in

coordinated and communication process (Cescon, Costantini, and Grassetti, 2016).

Disadvantage

It is not useful for multinational organization as it took time for formulate budget by using

initial level information.

For formulating zero based budget cost as well as requirement of manpower is

comparatively high.

P4Explanation of advantage & disadvantage of various types of planning tools.

Planning tool: T hoes technique or tools which help manager to formulate plan are known

as planning tools. Difference kind of tools which Capital joinery limited, use are define below

Budgetary techniques: The term budget is define as numerical statement which is

formulated to define value of future profit and loss. There are various way through which

manager can formulate their budget all theses are define below

Activity based budgeting: This is consider as type of budget in which all the information are

collected on the basis of allocation of record, cost incurred for particular time period. Thus it is

known as activity based budget:

Advantage:

Activity based budget help in allocate resource in effective manner, and by formulating

this budget manager able to find out accurate result (Ghasemi, Mohamad, Karami, Bajuri, and

Asgharizade, 2016).

This budget is useful in providing accurate business information.

Disadvantage

Activity based budget is time consuming budget as well a it also cost incurred activity.

Formulate budget by using this method is complex procedure.

Zero based budgeting: In this type of planning tool, budget are prepared from zero or

initial level. Manager not use previous data to formulate this budget, thus it is known as zero

based budget.

Advantage:

This method of budget is useful for newly set up business entities a information are

accurate and reliable.

Zero based budget useful in cut throat redundant business activities. And help in

coordinated and communication process (Cescon, Costantini, and Grassetti, 2016).

Disadvantage

It is not useful for multinational organization as it took time for formulate budget by using

initial level information.

For formulating zero based budget cost as well as requirement of manpower is

comparatively high.

Pricing strategies: This is consider as essential tool of planning. By using pricing

strategies manager able to determine price and they formulate plan through which they can

generate business profit. There are various strategies which can apply by organization,

skimming, penetration, discounting business entity according t their needs select pricing strategy.

Advantage:

Theses strategies useful in generate business revenue.

Pricing strategy help in attain competitive business advantage by providing satisfaction to

organization's relevant customer.

Disadvantage

Future business policies are made on the basis of price element and value of price are not

constant thus it is not essential that theses strategies provide accurate business result.

Selection of price required expertise who have great knowledge regarding the market area.

Costing techniques: Theses technique are use to identify the value of cost incurred for

each business activity. By using marginal, standard as well as absorption costing method , these

methods are help in determine cost.

Advantage:

Costing technique help in reduce cost incurred on wastage businesses activities by identify

those business activities which may cause of incurring high cost.

Manager take investment decision on the basis of measuring cost of each investment.

Disadvantage

Organization need to hire person who have special degree in the field of finance or account

as well as have knowledge regarding working in corporate sector.

Other strategical tools: By using environment scanning techniques organization able to

formulate business plan. Theses consider SWOT, PESTLE, Porter's 5 model. All these are useful

in determine future opportunities (Abbasi, Khanmohammadi, Moradi, and Mahmoodiyan,

2019).

Advantage:

Strategic planning tool help in identify opportunity and market threat by using SWOT, and

PESTLE technique.

strategies manager able to determine price and they formulate plan through which they can

generate business profit. There are various strategies which can apply by organization,

skimming, penetration, discounting business entity according t their needs select pricing strategy.

Advantage:

Theses strategies useful in generate business revenue.

Pricing strategy help in attain competitive business advantage by providing satisfaction to

organization's relevant customer.

Disadvantage

Future business policies are made on the basis of price element and value of price are not

constant thus it is not essential that theses strategies provide accurate business result.

Selection of price required expertise who have great knowledge regarding the market area.

Costing techniques: Theses technique are use to identify the value of cost incurred for

each business activity. By using marginal, standard as well as absorption costing method , these

methods are help in determine cost.

Advantage:

Costing technique help in reduce cost incurred on wastage businesses activities by identify

those business activities which may cause of incurring high cost.

Manager take investment decision on the basis of measuring cost of each investment.

Disadvantage

Organization need to hire person who have special degree in the field of finance or account

as well as have knowledge regarding working in corporate sector.

Other strategical tools: By using environment scanning techniques organization able to

formulate business plan. Theses consider SWOT, PESTLE, Porter's 5 model. All these are useful

in determine future opportunities (Abbasi, Khanmohammadi, Moradi, and Mahmoodiyan,

2019).

Advantage:

Strategic planning tool help in identify opportunity and market threat by using SWOT, and

PESTLE technique.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.