Management Accounting Systems, Techniques and Reporting- BTEC HND

VerifiedAdded on 2023/01/13

|15

|4058

|33

Report

AI Summary

This report provides a detailed analysis of management accounting (MA) systems and techniques, focusing on their application within an organization that produces designer furniture. It begins by defining MA and outlining its essential functions, including financial management, auditing, planning, cost accounting, controlling, and decision-making. The report differentiates between management and financial accounting, highlighting the importance of cost accounting, inventory management, job costing, and price accounting systems. It discusses various methods of MA reporting, such as inventory management, accounts receivable aging, and performance reports, emphasizing their benefits and integration with organizational processes. The report also includes the preparation of income statements using marginal and absorption costing schemes, along with a discussion of different planning tools for budgetary control. Finally, it compares organizations regarding their use of MA systems to solve problems, concluding with the significance of MA in enhancing decision-making and overall efficiency.

Management Accounting

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P1 MA and essential requirement of 4 MA system....................................................................1

P2. Various method of management accounting reporting.........................................................3

TASK 2............................................................................................................................................4

P3. Preparation of income statements with different costing scheme.........................................4

TASK 3............................................................................................................................................7

P4 Advantages and disadvantages of different planning tools used for budgetary control .......7

TASK 4............................................................................................................................................9

P5. Comparison between organisations regarding using of MA system to solve problems. .....9

CONCLUSION..............................................................................................................................10

REFERENCES .............................................................................................................................12

P2. Various method of management accounting reporting.........................................................3

TASK 2............................................................................................................................................4

P3. Preparation of income statements with different costing scheme.........................................4

TASK 3............................................................................................................................................7

P4 Advantages and disadvantages of different planning tools used for budgetary control .......7

TASK 4............................................................................................................................................9

P5. Comparison between organisations regarding using of MA system to solve problems. .....9

CONCLUSION..............................................................................................................................10

REFERENCES .............................................................................................................................12

INTRODUCTION

The methodology related with determining the important and useful financial and non

financial information into proper record to make valuable decisions is known as Management

accounting (Carlsson-Wall, Kraus and Karlsson, 2017). It is a detailed process in which different

types of MA system are applied by the manager of company to prepare important report which

help in assessing the main information at different business situation. The report in based on

Katie Walker Furniture that use to produce designer furniture in UK.

In this report, different sort of MA system and their effective benefits are defined which

are used to prepare several important reports which are also discussed in this report. Report also

cover different costing techniques which is used to prepare income statements and most

importantly various planning tool is used within organisation to prepare budgets. In addition,

MA system are used detect and overcome several financial problems faced by company.

TASK 1

P1 MA and essential requirement of 4 MA system.

“Management accounting inform the elaborated and regular financial strength and status

of company to leading parties” (Management accounting, 2020).

“Management accounting is a procedure of setting up management accounts and reports

that give faithful and punctual non-financial and statistical data to administrator to form short

and long term decisions”.

From the above two definition, it has been clearly started that MA is a method which is

related with forming of crucial report that hold detail information about monetary and non

monetary aspect of business in order to make better decision (Goh and Scerri, 2016). There are 6

important function of MA that are discussed underneath:

Financial management: The finance manager must organize and adjust the necessary

elements of the P&L report, income statement. Of instance the information are provided

to finance manager in a most comprehensible manner, which simplifies in managing the

financial information throughout the year.

Auditing: The data presented is needed to be modified by the manager according to the

expectation which help in auditing. In order to complete the audit process manager use to

1

The methodology related with determining the important and useful financial and non

financial information into proper record to make valuable decisions is known as Management

accounting (Carlsson-Wall, Kraus and Karlsson, 2017). It is a detailed process in which different

types of MA system are applied by the manager of company to prepare important report which

help in assessing the main information at different business situation. The report in based on

Katie Walker Furniture that use to produce designer furniture in UK.

In this report, different sort of MA system and their effective benefits are defined which

are used to prepare several important reports which are also discussed in this report. Report also

cover different costing techniques which is used to prepare income statements and most

importantly various planning tool is used within organisation to prepare budgets. In addition,

MA system are used detect and overcome several financial problems faced by company.

TASK 1

P1 MA and essential requirement of 4 MA system.

“Management accounting inform the elaborated and regular financial strength and status

of company to leading parties” (Management accounting, 2020).

“Management accounting is a procedure of setting up management accounts and reports

that give faithful and punctual non-financial and statistical data to administrator to form short

and long term decisions”.

From the above two definition, it has been clearly started that MA is a method which is

related with forming of crucial report that hold detail information about monetary and non

monetary aspect of business in order to make better decision (Goh and Scerri, 2016). There are 6

important function of MA that are discussed underneath:

Financial management: The finance manager must organize and adjust the necessary

elements of the P&L report, income statement. Of instance the information are provided

to finance manager in a most comprehensible manner, which simplifies in managing the

financial information throughout the year.

Auditing: The data presented is needed to be modified by the manager according to the

expectation which help in auditing. In order to complete the audit process manager use to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

modify the data according to accounting principle and standards which help in making

useful decision.

Planning: The business advisor provides sufficient information to help determine the

company's future. Including administrators of all company prediction details for business

purposes.

Cost accounting: Comparative and can size statements are structured to make effective

representation results. Such as executives of organization use the ratio to predict the

patterns in cost and make certain polices to reduce and lower the cost to increase

profitability.

Controlling: This is the main function of MA is related with controlling the company

resources and performance of employees and worker. Like manager use to control and

manage the valuable resources which support in better functioning of operations. Decision making: In last the useful data and relevant information is communicated and

distributed to employees to maximise the results and make valuable decision for

increasing the overall efficiency and affectivity (West, 2018). In respective firm modified

data is given to each member at different level in order to increase the total profit and

make judgement to improve customer base.

Difference between Management accounting and financial accounting.

Financial accounting Management accounting

In this process reports are formulated which

are used by external parties like stakeholders,

investors etc.

It is related to preparation of reports which are

used by internal manager to make better and

sound decision.

Financial accounting is primarily concerned

with reporting for the company as a whole.

Managerial accounting forces much more on

the parts, or segments, of a company.

Management accounting consists of multiple systems that help fulfil multiple

management and accounting standards for successful decision-making purposes. These are

detailed discussed underneath:

Cost Accounting system: It is also regarded as a commodity pricing method which is

utilizes by company for estimating cost of their products that help in cost regulation, profitability

assessment and product assessment. In Katie Walker Furniture, this system can be used to

2

useful decision.

Planning: The business advisor provides sufficient information to help determine the

company's future. Including administrators of all company prediction details for business

purposes.

Cost accounting: Comparative and can size statements are structured to make effective

representation results. Such as executives of organization use the ratio to predict the

patterns in cost and make certain polices to reduce and lower the cost to increase

profitability.

Controlling: This is the main function of MA is related with controlling the company

resources and performance of employees and worker. Like manager use to control and

manage the valuable resources which support in better functioning of operations. Decision making: In last the useful data and relevant information is communicated and

distributed to employees to maximise the results and make valuable decision for

increasing the overall efficiency and affectivity (West, 2018). In respective firm modified

data is given to each member at different level in order to increase the total profit and

make judgement to improve customer base.

Difference between Management accounting and financial accounting.

Financial accounting Management accounting

In this process reports are formulated which

are used by external parties like stakeholders,

investors etc.

It is related to preparation of reports which are

used by internal manager to make better and

sound decision.

Financial accounting is primarily concerned

with reporting for the company as a whole.

Managerial accounting forces much more on

the parts, or segments, of a company.

Management accounting consists of multiple systems that help fulfil multiple

management and accounting standards for successful decision-making purposes. These are

detailed discussed underneath:

Cost Accounting system: It is also regarded as a commodity pricing method which is

utilizes by company for estimating cost of their products that help in cost regulation, profitability

assessment and product assessment. In Katie Walker Furniture, this system can be used to

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

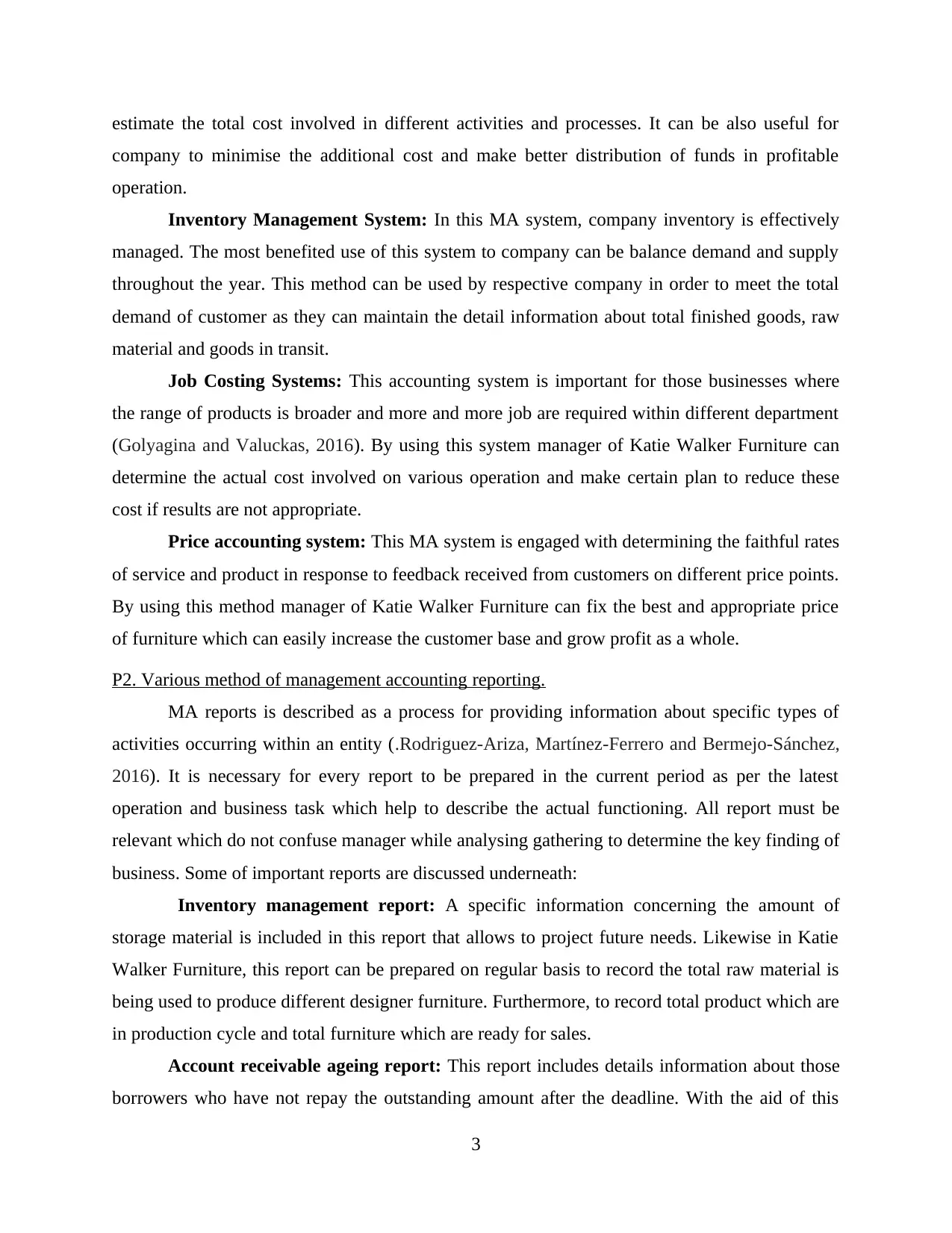

estimate the total cost involved in different activities and processes. It can be also useful for

company to minimise the additional cost and make better distribution of funds in profitable

operation.

Inventory Management System: In this MA system, company inventory is effectively

managed. The most benefited use of this system to company can be balance demand and supply

throughout the year. This method can be used by respective company in order to meet the total

demand of customer as they can maintain the detail information about total finished goods, raw

material and goods in transit.

Job Costing Systems: This accounting system is important for those businesses where

the range of products is broader and more and more job are required within different department

(Golyagina and Valuckas, 2016). By using this system manager of Katie Walker Furniture can

determine the actual cost involved on various operation and make certain plan to reduce these

cost if results are not appropriate.

Price accounting system: This MA system is engaged with determining the faithful rates

of service and product in response to feedback received from customers on different price points.

By using this method manager of Katie Walker Furniture can fix the best and appropriate price

of furniture which can easily increase the customer base and grow profit as a whole.

P2. Various method of management accounting reporting.

MA reports is described as a process for providing information about specific types of

activities occurring within an entity (.Rodriguez-Ariza, Martínez-Ferrero and Bermejo-Sánchez,

2016). It is necessary for every report to be prepared in the current period as per the latest

operation and business task which help to describe the actual functioning. All report must be

relevant which do not confuse manager while analysing gathering to determine the key finding of

business. Some of important reports are discussed underneath:

Inventory management report: A specific information concerning the amount of

storage material is included in this report that allows to project future needs. Likewise in Katie

Walker Furniture, this report can be prepared on regular basis to record the total raw material is

being used to produce different designer furniture. Furthermore, to record total product which are

in production cycle and total furniture which are ready for sales.

Account receivable ageing report: This report includes details information about those

borrowers who have not repay the outstanding amount after the deadline. With the aid of this

3

company to minimise the additional cost and make better distribution of funds in profitable

operation.

Inventory Management System: In this MA system, company inventory is effectively

managed. The most benefited use of this system to company can be balance demand and supply

throughout the year. This method can be used by respective company in order to meet the total

demand of customer as they can maintain the detail information about total finished goods, raw

material and goods in transit.

Job Costing Systems: This accounting system is important for those businesses where

the range of products is broader and more and more job are required within different department

(Golyagina and Valuckas, 2016). By using this system manager of Katie Walker Furniture can

determine the actual cost involved on various operation and make certain plan to reduce these

cost if results are not appropriate.

Price accounting system: This MA system is engaged with determining the faithful rates

of service and product in response to feedback received from customers on different price points.

By using this method manager of Katie Walker Furniture can fix the best and appropriate price

of furniture which can easily increase the customer base and grow profit as a whole.

P2. Various method of management accounting reporting.

MA reports is described as a process for providing information about specific types of

activities occurring within an entity (.Rodriguez-Ariza, Martínez-Ferrero and Bermejo-Sánchez,

2016). It is necessary for every report to be prepared in the current period as per the latest

operation and business task which help to describe the actual functioning. All report must be

relevant which do not confuse manager while analysing gathering to determine the key finding of

business. Some of important reports are discussed underneath:

Inventory management report: A specific information concerning the amount of

storage material is included in this report that allows to project future needs. Likewise in Katie

Walker Furniture, this report can be prepared on regular basis to record the total raw material is

being used to produce different designer furniture. Furthermore, to record total product which are

in production cycle and total furniture which are ready for sales.

Account receivable ageing report: This report includes details information about those

borrowers who have not repay the outstanding amount after the deadline. With the aid of this

3

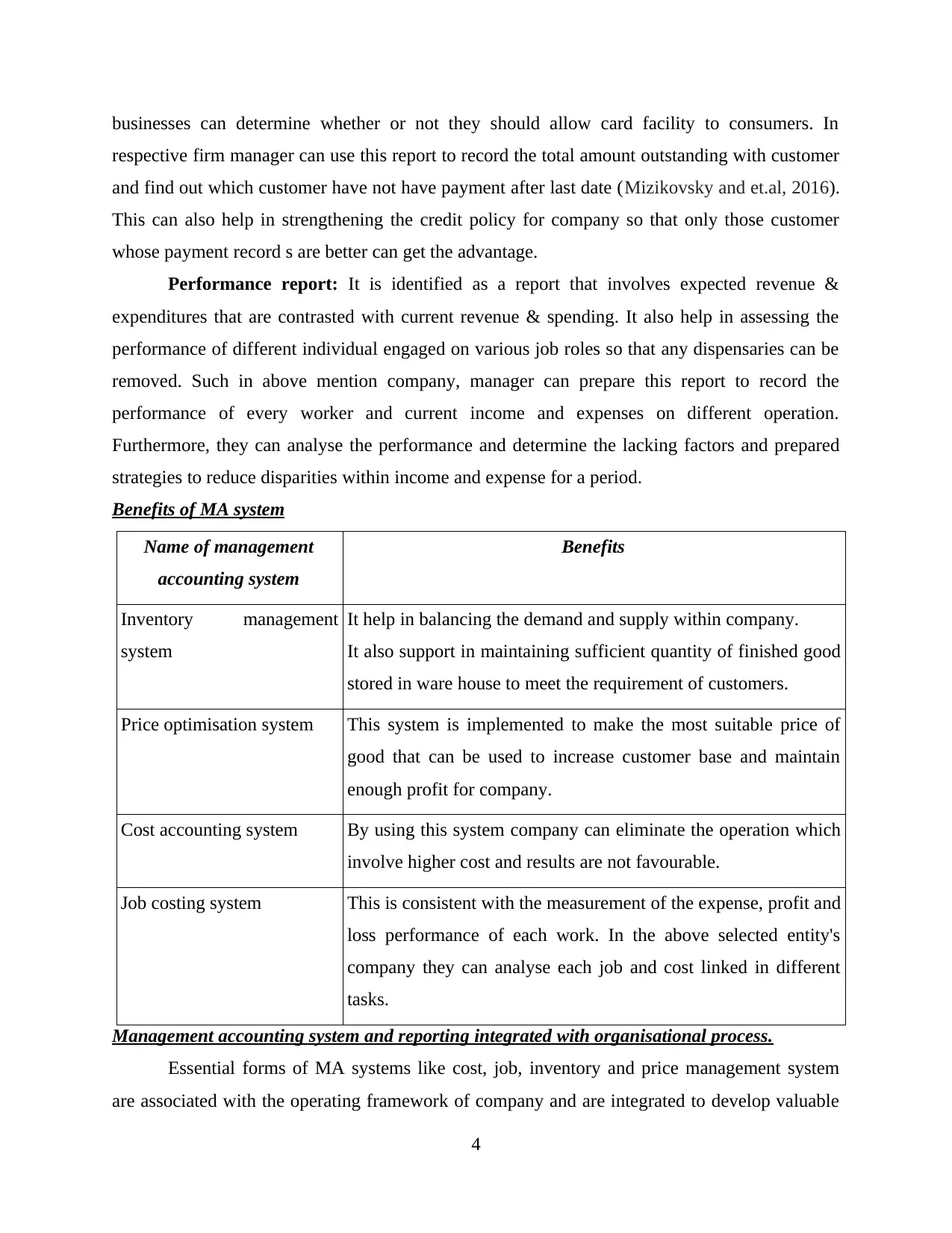

businesses can determine whether or not they should allow card facility to consumers. In

respective firm manager can use this report to record the total amount outstanding with customer

and find out which customer have not have payment after last date (Mizikovsky and et.al, 2016).

This can also help in strengthening the credit policy for company so that only those customer

whose payment record s are better can get the advantage.

Performance report: It is identified as a report that involves expected revenue &

expenditures that are contrasted with current revenue & spending. It also help in assessing the

performance of different individual engaged on various job roles so that any dispensaries can be

removed. Such in above mention company, manager can prepare this report to record the

performance of every worker and current income and expenses on different operation.

Furthermore, they can analyse the performance and determine the lacking factors and prepared

strategies to reduce disparities within income and expense for a period.

Benefits of MA system

Name of management

accounting system

Benefits

Inventory management

system

It help in balancing the demand and supply within company.

It also support in maintaining sufficient quantity of finished good

stored in ware house to meet the requirement of customers.

Price optimisation system This system is implemented to make the most suitable price of

good that can be used to increase customer base and maintain

enough profit for company.

Cost accounting system By using this system company can eliminate the operation which

involve higher cost and results are not favourable.

Job costing system This is consistent with the measurement of the expense, profit and

loss performance of each work. In the above selected entity's

company they can analyse each job and cost linked in different

tasks.

Management accounting system and reporting integrated with organisational process.

Essential forms of MA systems like cost, job, inventory and price management system

are associated with the operating framework of company and are integrated to develop valuable

4

respective firm manager can use this report to record the total amount outstanding with customer

and find out which customer have not have payment after last date (Mizikovsky and et.al, 2016).

This can also help in strengthening the credit policy for company so that only those customer

whose payment record s are better can get the advantage.

Performance report: It is identified as a report that involves expected revenue &

expenditures that are contrasted with current revenue & spending. It also help in assessing the

performance of different individual engaged on various job roles so that any dispensaries can be

removed. Such in above mention company, manager can prepare this report to record the

performance of every worker and current income and expenses on different operation.

Furthermore, they can analyse the performance and determine the lacking factors and prepared

strategies to reduce disparities within income and expense for a period.

Benefits of MA system

Name of management

accounting system

Benefits

Inventory management

system

It help in balancing the demand and supply within company.

It also support in maintaining sufficient quantity of finished good

stored in ware house to meet the requirement of customers.

Price optimisation system This system is implemented to make the most suitable price of

good that can be used to increase customer base and maintain

enough profit for company.

Cost accounting system By using this system company can eliminate the operation which

involve higher cost and results are not favourable.

Job costing system This is consistent with the measurement of the expense, profit and

loss performance of each work. In the above selected entity's

company they can analyse each job and cost linked in different

tasks.

Management accounting system and reporting integrated with organisational process.

Essential forms of MA systems like cost, job, inventory and price management system

are associated with the operating framework of company and are integrated to develop valuable

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

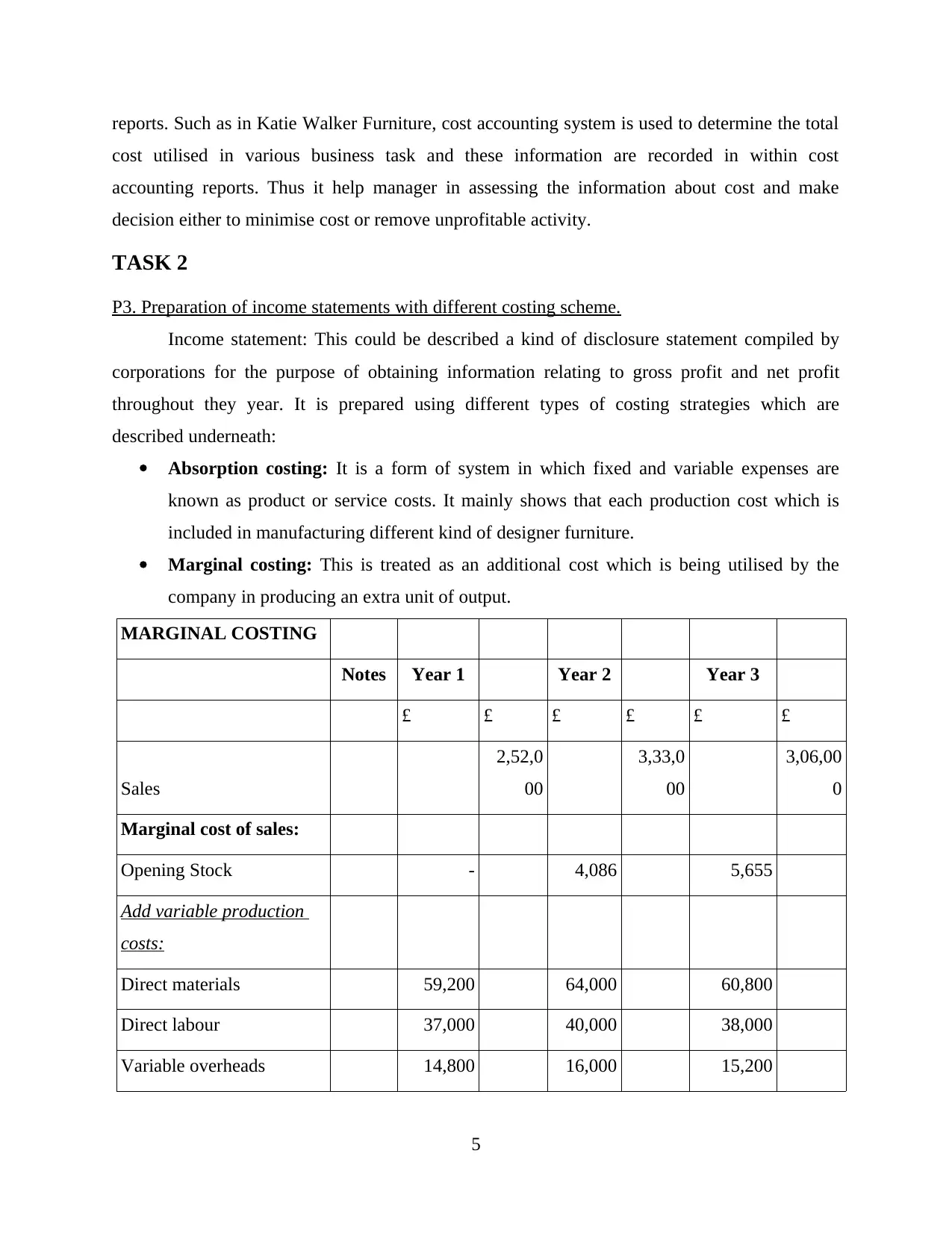

reports. Such as in Katie Walker Furniture, cost accounting system is used to determine the total

cost utilised in various business task and these information are recorded in within cost

accounting reports. Thus it help manager in assessing the information about cost and make

decision either to minimise cost or remove unprofitable activity.

TASK 2

P3. Preparation of income statements with different costing scheme.

Income statement: This could be described a kind of disclosure statement compiled by

corporations for the purpose of obtaining information relating to gross profit and net profit

throughout they year. It is prepared using different types of costing strategies which are

described underneath:

Absorption costing: It is a form of system in which fixed and variable expenses are

known as product or service costs. It mainly shows that each production cost which is

included in manufacturing different kind of designer furniture.

Marginal costing: This is treated as an additional cost which is being utilised by the

company in producing an extra unit of output.

MARGINAL COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,00

0

Marginal cost of sales:

Opening Stock - 4,086 5,655

Add variable production

costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

5

cost utilised in various business task and these information are recorded in within cost

accounting reports. Thus it help manager in assessing the information about cost and make

decision either to minimise cost or remove unprofitable activity.

TASK 2

P3. Preparation of income statements with different costing scheme.

Income statement: This could be described a kind of disclosure statement compiled by

corporations for the purpose of obtaining information relating to gross profit and net profit

throughout they year. It is prepared using different types of costing strategies which are

described underneath:

Absorption costing: It is a form of system in which fixed and variable expenses are

known as product or service costs. It mainly shows that each production cost which is

included in manufacturing different kind of designer furniture.

Marginal costing: This is treated as an additional cost which is being utilised by the

company in producing an extra unit of output.

MARGINAL COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,00

0

Marginal cost of sales:

Opening Stock - 4,086 5,655

Add variable production

costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

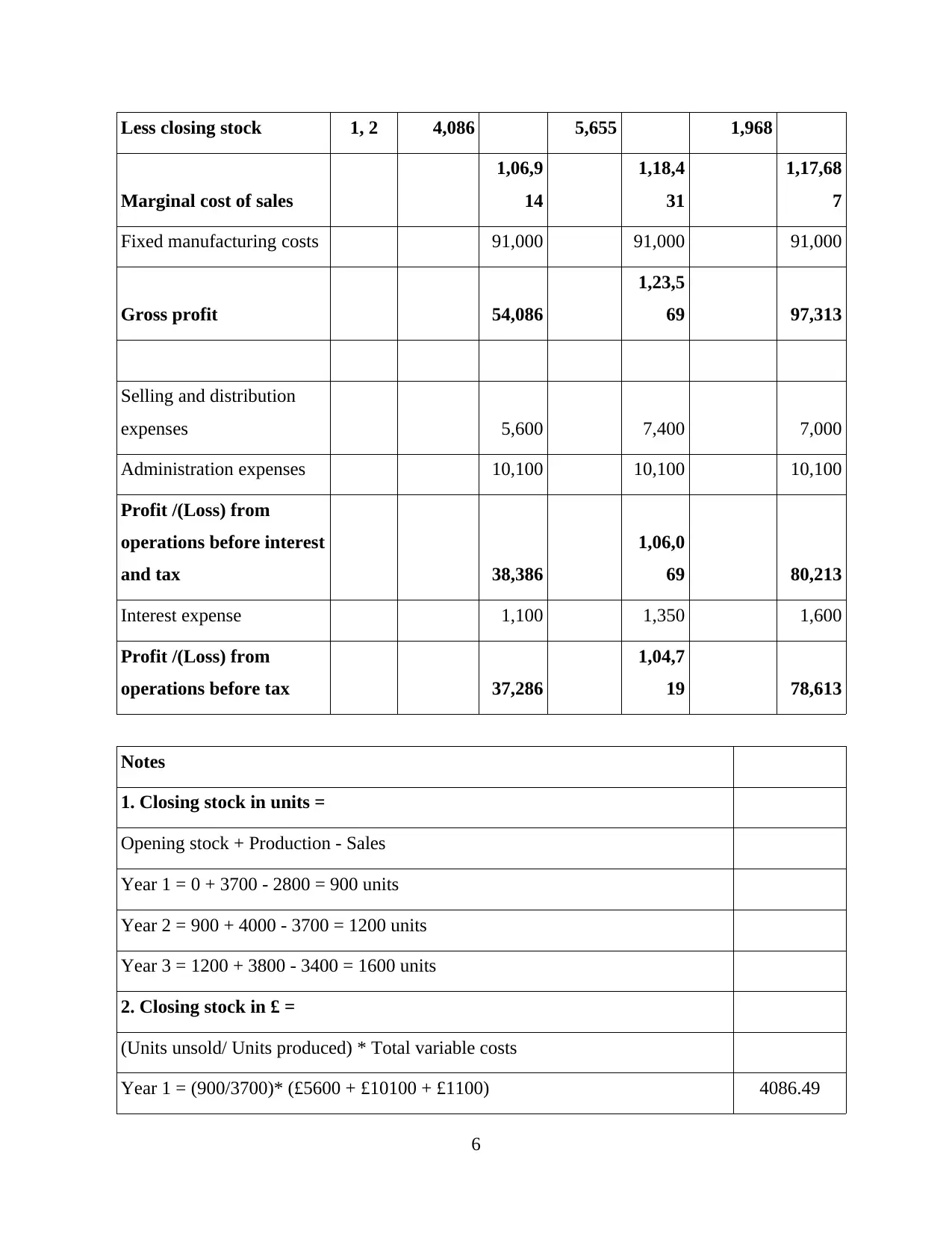

Less closing stock 1, 2 4,086 5,655 1,968

Marginal cost of sales

1,06,9

14

1,18,4

31

1,17,68

7

Fixed manufacturing costs 91,000 91,000 91,000

Gross profit 54,086

1,23,5

69 97,313

Selling and distribution

expenses 5,600 7,400 7,000

Administration expenses 10,100 10,100 10,100

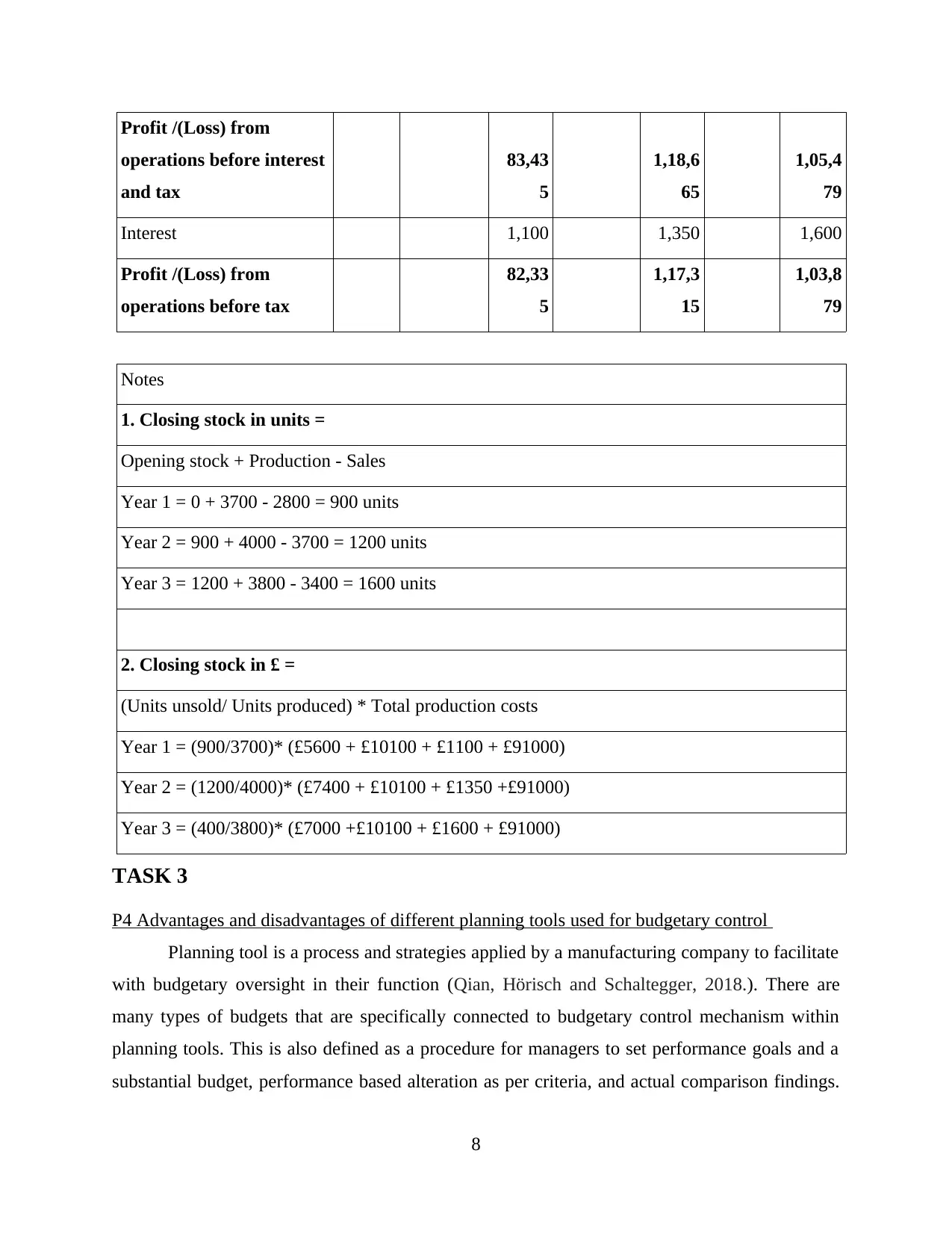

Profit /(Loss) from

operations before interest

and tax 38,386

1,06,0

69 80,213

Interest expense 1,100 1,350 1,600

Profit /(Loss) from

operations before tax 37,286

1,04,7

19 78,613

Notes

1. Closing stock in units =

Opening stock + Production - Sales

Year 1 = 0 + 3700 - 2800 = 900 units

Year 2 = 900 + 4000 - 3700 = 1200 units

Year 3 = 1200 + 3800 - 3400 = 1600 units

2. Closing stock in £ =

(Units unsold/ Units produced) * Total variable costs

Year 1 = (900/3700)* (£5600 + £10100 + £1100) 4086.49

6

Marginal cost of sales

1,06,9

14

1,18,4

31

1,17,68

7

Fixed manufacturing costs 91,000 91,000 91,000

Gross profit 54,086

1,23,5

69 97,313

Selling and distribution

expenses 5,600 7,400 7,000

Administration expenses 10,100 10,100 10,100

Profit /(Loss) from

operations before interest

and tax 38,386

1,06,0

69 80,213

Interest expense 1,100 1,350 1,600

Profit /(Loss) from

operations before tax 37,286

1,04,7

19 78,613

Notes

1. Closing stock in units =

Opening stock + Production - Sales

Year 1 = 0 + 3700 - 2800 = 900 units

Year 2 = 900 + 4000 - 3700 = 1200 units

Year 3 = 1200 + 3800 - 3400 = 1600 units

2. Closing stock in £ =

(Units unsold/ Units produced) * Total variable costs

Year 1 = (900/3700)* (£5600 + £10100 + £1100) 4086.49

6

Year 2 = (1200/4000)* (£7400 + £10100 + £1350) 5655

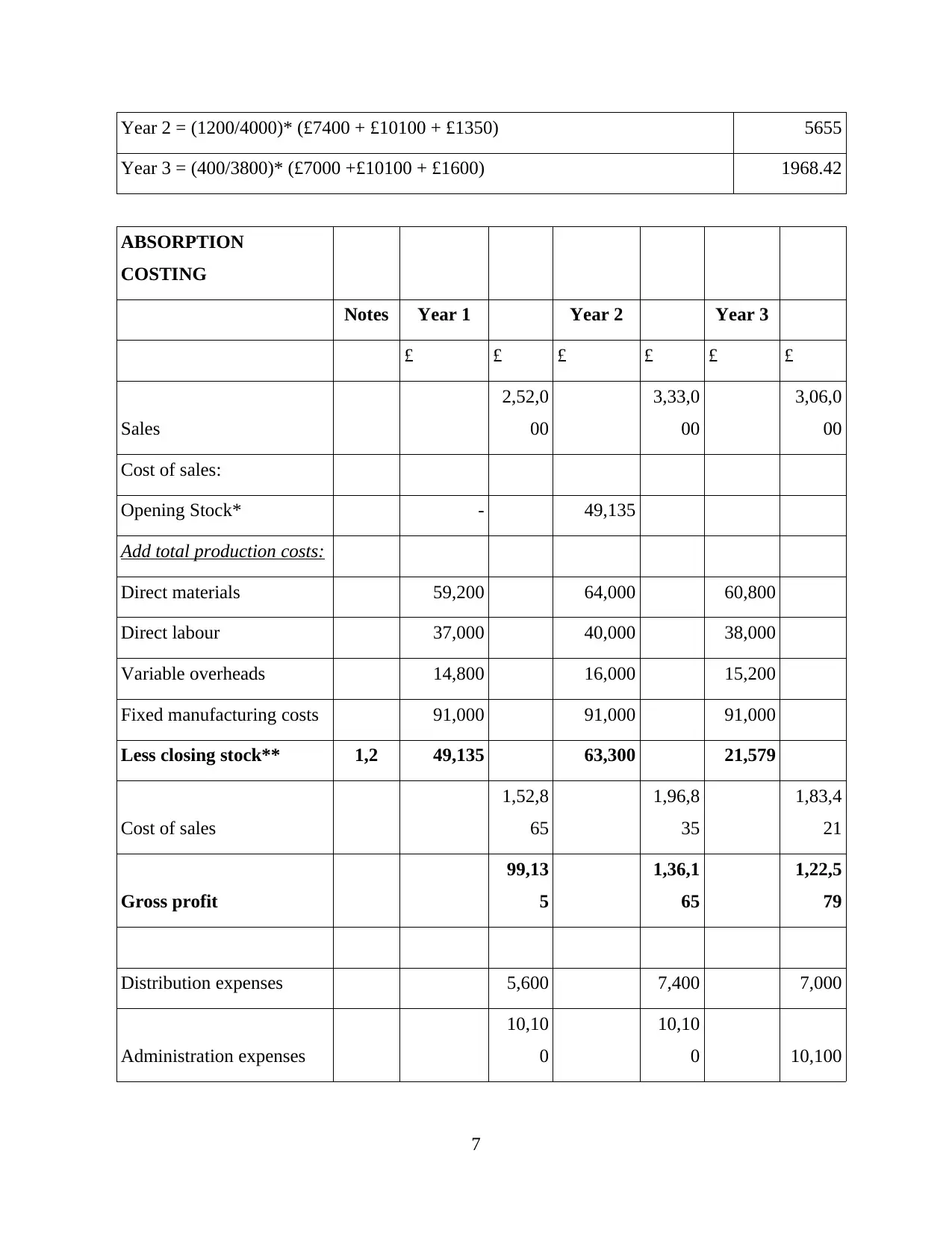

Year 3 = (400/3800)* (£7000 +£10100 + £1600) 1968.42

ABSORPTION

COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,0

00

Cost of sales:

Opening Stock* - 49,135

Add total production costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Fixed manufacturing costs 91,000 91,000 91,000

Less closing stock** 1,2 49,135 63,300 21,579

Cost of sales

1,52,8

65

1,96,8

35

1,83,4

21

Gross profit

99,13

5

1,36,1

65

1,22,5

79

Distribution expenses 5,600 7,400 7,000

Administration expenses

10,10

0

10,10

0 10,100

7

Year 3 = (400/3800)* (£7000 +£10100 + £1600) 1968.42

ABSORPTION

COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,0

00

Cost of sales:

Opening Stock* - 49,135

Add total production costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Fixed manufacturing costs 91,000 91,000 91,000

Less closing stock** 1,2 49,135 63,300 21,579

Cost of sales

1,52,8

65

1,96,8

35

1,83,4

21

Gross profit

99,13

5

1,36,1

65

1,22,5

79

Distribution expenses 5,600 7,400 7,000

Administration expenses

10,10

0

10,10

0 10,100

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit /(Loss) from

operations before interest

and tax

83,43

5

1,18,6

65

1,05,4

79

Interest 1,100 1,350 1,600

Profit /(Loss) from

operations before tax

82,33

5

1,17,3

15

1,03,8

79

Notes

1. Closing stock in units =

Opening stock + Production - Sales

Year 1 = 0 + 3700 - 2800 = 900 units

Year 2 = 900 + 4000 - 3700 = 1200 units

Year 3 = 1200 + 3800 - 3400 = 1600 units

2. Closing stock in £ =

(Units unsold/ Units produced) * Total production costs

Year 1 = (900/3700)* (£5600 + £10100 + £1100 + £91000)

Year 2 = (1200/4000)* (£7400 + £10100 + £1350 +£91000)

Year 3 = (400/3800)* (£7000 +£10100 + £1600 + £91000)

TASK 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

Planning tool is a process and strategies applied by a manufacturing company to facilitate

with budgetary oversight in their function (Qian, Hörisch and Schaltegger, 2018.). There are

many types of budgets that are specifically connected to budgetary control mechanism within

planning tools. This is also defined as a procedure for managers to set performance goals and a

substantial budget, performance based alteration as per criteria, and actual comparison findings.

8

operations before interest

and tax

83,43

5

1,18,6

65

1,05,4

79

Interest 1,100 1,350 1,600

Profit /(Loss) from

operations before tax

82,33

5

1,17,3

15

1,03,8

79

Notes

1. Closing stock in units =

Opening stock + Production - Sales

Year 1 = 0 + 3700 - 2800 = 900 units

Year 2 = 900 + 4000 - 3700 = 1200 units

Year 3 = 1200 + 3800 - 3400 = 1600 units

2. Closing stock in £ =

(Units unsold/ Units produced) * Total production costs

Year 1 = (900/3700)* (£5600 + £10100 + £1100 + £91000)

Year 2 = (1200/4000)* (£7400 + £10100 + £1350 +£91000)

Year 3 = (400/3800)* (£7000 +£10100 + £1600 + £91000)

TASK 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

Planning tool is a process and strategies applied by a manufacturing company to facilitate

with budgetary oversight in their function (Qian, Hörisch and Schaltegger, 2018.). There are

many types of budgets that are specifically connected to budgetary control mechanism within

planning tools. This is also defined as a procedure for managers to set performance goals and a

substantial budget, performance based alteration as per criteria, and actual comparison findings.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Some description of these references together with some benefits and drawbacks are provided

below:-

Zero based Budgeting – It is planning tool that, while designing budget, takes zero as a

basis. In zero-based approach, it ensures that no prior data will be considered by the management

planning the budget when preparing the budget. This method of budgeting allows organization

manager to take decisions quickly without any prior data being involved. Based on current case

manager, often find fresh assumptions which do not include any previous theories or

information.

Advantages: It is a effective tool which is beneficial in making short term valuable

decision. This also help manager to set a new budget every time easily as they do not

have to consider previous budget information. Disadvantages: As the budget is prepared on yearly basis so many time create

difficulties for the team member to make decision (Saleem Salem Alzoubi, 2016).

Operating budget: This is a beneficial planning tool since all the small detail about

companies operation and activity are included in operating budget. This can be said in short that

the respective budget provides the facility to carry out all significant business task in one spot. In

addition, all sub- or divisional should prepare during preparation of the operation budget.

Advantages: This budget help the manager of respective company to make a decision in

more cosine manner about business task and activity as detail information is included in

operating budget.

Disadvantages: Expertise is needed to plan operating budget that essentially means

manager require proper ability and capability to plan spending.

Cash budget: It is a budget that plans as per a company's financial needs and give detail

predicted information related with cash inflows and outflows. In Katie Walker Furniture, this

budget can be used to estimate the total cash requirement to run production function and

manager can record the total cash inflows form selling process.

Advantages : This budget can support for respective company by providing actual

liquidity and cash detail from various operation (.Höglund and Sundvik, 2016). Disadvantages: The major limitation was that the calculation resulting in loss can not be

extended due to firms.

Different planning tools used in preparing and forecasting of budget.

9

below:-

Zero based Budgeting – It is planning tool that, while designing budget, takes zero as a

basis. In zero-based approach, it ensures that no prior data will be considered by the management

planning the budget when preparing the budget. This method of budgeting allows organization

manager to take decisions quickly without any prior data being involved. Based on current case

manager, often find fresh assumptions which do not include any previous theories or

information.

Advantages: It is a effective tool which is beneficial in making short term valuable

decision. This also help manager to set a new budget every time easily as they do not

have to consider previous budget information. Disadvantages: As the budget is prepared on yearly basis so many time create

difficulties for the team member to make decision (Saleem Salem Alzoubi, 2016).

Operating budget: This is a beneficial planning tool since all the small detail about

companies operation and activity are included in operating budget. This can be said in short that

the respective budget provides the facility to carry out all significant business task in one spot. In

addition, all sub- or divisional should prepare during preparation of the operation budget.

Advantages: This budget help the manager of respective company to make a decision in

more cosine manner about business task and activity as detail information is included in

operating budget.

Disadvantages: Expertise is needed to plan operating budget that essentially means

manager require proper ability and capability to plan spending.

Cash budget: It is a budget that plans as per a company's financial needs and give detail

predicted information related with cash inflows and outflows. In Katie Walker Furniture, this

budget can be used to estimate the total cash requirement to run production function and

manager can record the total cash inflows form selling process.

Advantages : This budget can support for respective company by providing actual

liquidity and cash detail from various operation (.Höglund and Sundvik, 2016). Disadvantages: The major limitation was that the calculation resulting in loss can not be

extended due to firms.

Different planning tools used in preparing and forecasting of budget.

9

Budgetary control planning techniques comprise of various types of budgets like cash

operating and ZBB budget and many more. Such as cash budget provide the information about

total cash inflows and outflows, operational budget gives detail about actual business process and

task in a period. That's because such planning instruments comprise of financial data which can

be a reliable structure for future earnings and expenditure prediction.

TASK 4

P5. Comparison between organisations regarding using of MA system to solve problems.

A kind of issue that comes up because of lack of sufficient financial means which can

reduce the overall functioning and profitability of business activity is knows as financial

problems (Jefrey, 2018). Through there is no particular reason why the financial problem occurs

but some reason specific this like increasing operating cost, more spending than earning, lack of

money management etc. There are different MA tool which can be effectively used by the Katie

Walker Furniture to detect the financial problems. Some of these are discussed underneath:

KPI: Key performance measurement was the tool that helps the market company to

assess both financial and non-financial results. In respective firm this tool can be

implemented to analyse the performance of staff and operation at different level so that

problem of weak performance can be determined.

Benchmarking: It was described as a technique of attributing the practices, techniques

and financial results of an organization with that of another same industry company. With

the help of this tool real problem of businesses are figuring out in different aspects. In

Katie Walker Furniture manager can use this tool to detect the issues of increasing cost

with other company dealing in furniture business in a year (Aouni, McGillis and

Abdulkarim, 2017).

Financial governance: This method acts as a surveillance approach for firms in

overcoming financial problems. It was defined as a sort of tool that systematically gathers and

manages all business transactions of corporations. Such as in above mention company financial

governance can be used to improve the performance of weak member by putting additional

training support. Similarly it can be used to increase productivity of operation by making smaller

projects so that each activity is monitored in well manner.

10

operating and ZBB budget and many more. Such as cash budget provide the information about

total cash inflows and outflows, operational budget gives detail about actual business process and

task in a period. That's because such planning instruments comprise of financial data which can

be a reliable structure for future earnings and expenditure prediction.

TASK 4

P5. Comparison between organisations regarding using of MA system to solve problems.

A kind of issue that comes up because of lack of sufficient financial means which can

reduce the overall functioning and profitability of business activity is knows as financial

problems (Jefrey, 2018). Through there is no particular reason why the financial problem occurs

but some reason specific this like increasing operating cost, more spending than earning, lack of

money management etc. There are different MA tool which can be effectively used by the Katie

Walker Furniture to detect the financial problems. Some of these are discussed underneath:

KPI: Key performance measurement was the tool that helps the market company to

assess both financial and non-financial results. In respective firm this tool can be

implemented to analyse the performance of staff and operation at different level so that

problem of weak performance can be determined.

Benchmarking: It was described as a technique of attributing the practices, techniques

and financial results of an organization with that of another same industry company. With

the help of this tool real problem of businesses are figuring out in different aspects. In

Katie Walker Furniture manager can use this tool to detect the issues of increasing cost

with other company dealing in furniture business in a year (Aouni, McGillis and

Abdulkarim, 2017).

Financial governance: This method acts as a surveillance approach for firms in

overcoming financial problems. It was defined as a sort of tool that systematically gathers and

manages all business transactions of corporations. Such as in above mention company financial

governance can be used to improve the performance of weak member by putting additional

training support. Similarly it can be used to increase productivity of operation by making smaller

projects so that each activity is monitored in well manner.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.