Analysis of Management Accounting Systems for Tata Motors Company

VerifiedAdded on 2023/03/20

|15

|4159

|100

Report

AI Summary

This report provides an introduction to management accounting, emphasizing its role in financial resource management and organizational stability. It explores the importance of accounting in identifying financial performance and areas for improvement, particularly within the context of Tata Motors. The report delves into key concepts such as cost accounting, job costing, and process costing, highlighting their application in reducing operational costs and tracking production activities. It also examines various management accounting reporting methods, including budget reporting, job costing reports, and financial reports, and their significance in planning, performance assessment, and decision-making. Furthermore, the report analyzes income statements using marginal and absorption costing methodologies, offering a comprehensive understanding of their impact on profitability analysis within the company.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Accounting is defines as the procedure of managing the financial resources of a company.

It assists manager in controlling the flow of finance. Accounting method also help business

entity in maintaining the financial stability and ensuring effective as well as efficient utilization

of resources. It includes the several activities such as recording of tractions, and other monetary

records. Accounting statement is used by the management team in an organisation for identifying

the financial performance of the company and recognizing the area of improvement. Financial

records also assist manager in identifying the income earned and expenses incurred during the

particular financial year. Accounting also assists management team in analyzing several financial

issues and finding the appropriate solution for the same.

The purpose of the report is to develop the understanding about the accounting system

and analysing its importance in an organization. It also has focus on highlighting the major issues

in accounting problems and identifying the appropriate solution for the same in context of Tata

motor company.

1

Accounting is defines as the procedure of managing the financial resources of a company.

It assists manager in controlling the flow of finance. Accounting method also help business

entity in maintaining the financial stability and ensuring effective as well as efficient utilization

of resources. It includes the several activities such as recording of tractions, and other monetary

records. Accounting statement is used by the management team in an organisation for identifying

the financial performance of the company and recognizing the area of improvement. Financial

records also assist manager in identifying the income earned and expenses incurred during the

particular financial year. Accounting also assists management team in analyzing several financial

issues and finding the appropriate solution for the same.

The purpose of the report is to develop the understanding about the accounting system

and analysing its importance in an organization. It also has focus on highlighting the major issues

in accounting problems and identifying the appropriate solution for the same in context of Tata

motor company.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

P.1.Explain management accounting and essential requirements of different types of

management accounting system

Management accounting is the approach which defines about preparing a proper

management reports in the organisation in order to management of all financial accounting

information in case of reduction of costing in business efficiently. Financial accounting refer to

the preparation of annual reports majorly for external stakeholders and management accounting

is a monthly reports which is made of internal performance assessment of company.

Management accounting reports are prepared by internal management team and accounting

executives for gaining financial reports in relevant form (Smith, Brännström and Jansson, 2015).

These reports are typically showed the amount of available in cash, sales revenue generated,

amount orders in hands, state of accounts payable and accounts receivable, outstanding debts and

raw materials etc. management accounting is most necessary for Tata organisational manager

which assist them to making proper decision in the company in respect to minimise the costing

and expenses of the company in the industry efficiently.

Cost accounting system: Cost accounting system is also one of the effective management

accounting approach in order to making proper management of monetary terms of the company

in the industry sufficiently. These are in tow form in the business which is job order costing and

process costing, both costing systems are being utilised by Tata company's manager in terms of

reducing several functionalities and manufacturing costing in the company in relevant manner.

Moreover, the cost accounting systems are being utilised by its manager in terms of proper

recording of production activities at the workplace efficiently (Kumarasiri and Jubb, 2016). This

could be used by organisational manager in order to appropriate tracking a raw material as they

go through the production stages of various car products at the manufacturing plant in the firm

effectively. When in the business, raw materials are used for manufacturing input then

immediately record the use of the materials by crediting the raw materials accounts for debiting

the goods in process accounts efficiently. This is also useful approach for Tata auto-mobile

organisation in order to recording of costing of each manufacturing activities which are being

done at the plant efficiently. This costing system can reduce the operational costing of the

company which is running in their production plant in the industry sufficiently.

2

P.1.Explain management accounting and essential requirements of different types of

management accounting system

Management accounting is the approach which defines about preparing a proper

management reports in the organisation in order to management of all financial accounting

information in case of reduction of costing in business efficiently. Financial accounting refer to

the preparation of annual reports majorly for external stakeholders and management accounting

is a monthly reports which is made of internal performance assessment of company.

Management accounting reports are prepared by internal management team and accounting

executives for gaining financial reports in relevant form (Smith, Brännström and Jansson, 2015).

These reports are typically showed the amount of available in cash, sales revenue generated,

amount orders in hands, state of accounts payable and accounts receivable, outstanding debts and

raw materials etc. management accounting is most necessary for Tata organisational manager

which assist them to making proper decision in the company in respect to minimise the costing

and expenses of the company in the industry efficiently.

Cost accounting system: Cost accounting system is also one of the effective management

accounting approach in order to making proper management of monetary terms of the company

in the industry sufficiently. These are in tow form in the business which is job order costing and

process costing, both costing systems are being utilised by Tata company's manager in terms of

reducing several functionalities and manufacturing costing in the company in relevant manner.

Moreover, the cost accounting systems are being utilised by its manager in terms of proper

recording of production activities at the workplace efficiently (Kumarasiri and Jubb, 2016). This

could be used by organisational manager in order to appropriate tracking a raw material as they

go through the production stages of various car products at the manufacturing plant in the firm

effectively. When in the business, raw materials are used for manufacturing input then

immediately record the use of the materials by crediting the raw materials accounts for debiting

the goods in process accounts efficiently. This is also useful approach for Tata auto-mobile

organisation in order to recording of costing of each manufacturing activities which are being

done at the plant efficiently. This costing system can reduce the operational costing of the

company which is running in their production plant in the industry sufficiently.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: This is also crucial approach of management accounting costing

system by which could assist Tata company's manager to keep track all activities and each job of

the company which is being operated and keep record each job expenses in the company

properly. This is used for those manufacturing companies in the industry which is usually

measured by the numbers of completed job in the industry in relevant manner (Budding, Grossi

and Tagesson, 2014). The each job costing is recorded by management accounting officer of the

company on a ledger throughout the entire job process and are included to the ultimate balance

statement, when preparing for job costing and batch statements at the workplace in effective

manner. There are numbers of jobs are being done while manufacturing works are being done in

several production phases of auto case making process, so varied of activities must be recorded

by its manager at the workplace and as per gathered data, they need to assess the costing of

production process each job effectively, and with the help of tools and techniques of job costing

system, the manager of Tata organisation could reduce the job costing at the workplace. This

approach must give benefits for the business in effective way, because they can reduce costing of

each job as per job costing system mechanisms process effectively and raise the profitability of

the company in the industry in proper way.

Process costing system: This is also one of the appropriate management accounting

costing system, which could be used for the firm's manager in respect to making proper

assessment of process which is being done while manufacturing activities are being done in the

plant effectively. This is an approach which is mostly used by manufacturing companies in the

world effectively and they can accumulate costs while large number of identical units are being

produced at the workplace properly (Haskin, 2010). In such circumstances, it is mostly useful for

the company in order to accumulate costing at an aggregate level for a large batch of production

in order to making allocate them to the individual units has been produces in the plant relevantly.

Various types of such activities are being done in manufacturing plant of the company and its

manager require to utilisation of several kinds of process costing system in terms of assessment

of process costing which is being produced in the company at mass level and as per its tool and

techniques, its manager can reduce the costing of manufacturing phase of the firm appropriately.

This might be also most beneficial for the business in respect to reducing the cost of production

and other several expenses in the firm sufficiently. Some costing occurs in the business such as

Direct material costs, Direct labour costs and overhead costs etc. all these costing might be

3

system by which could assist Tata company's manager to keep track all activities and each job of

the company which is being operated and keep record each job expenses in the company

properly. This is used for those manufacturing companies in the industry which is usually

measured by the numbers of completed job in the industry in relevant manner (Budding, Grossi

and Tagesson, 2014). The each job costing is recorded by management accounting officer of the

company on a ledger throughout the entire job process and are included to the ultimate balance

statement, when preparing for job costing and batch statements at the workplace in effective

manner. There are numbers of jobs are being done while manufacturing works are being done in

several production phases of auto case making process, so varied of activities must be recorded

by its manager at the workplace and as per gathered data, they need to assess the costing of

production process each job effectively, and with the help of tools and techniques of job costing

system, the manager of Tata organisation could reduce the job costing at the workplace. This

approach must give benefits for the business in effective way, because they can reduce costing of

each job as per job costing system mechanisms process effectively and raise the profitability of

the company in the industry in proper way.

Process costing system: This is also one of the appropriate management accounting

costing system, which could be used for the firm's manager in respect to making proper

assessment of process which is being done while manufacturing activities are being done in the

plant effectively. This is an approach which is mostly used by manufacturing companies in the

world effectively and they can accumulate costs while large number of identical units are being

produced at the workplace properly (Haskin, 2010). In such circumstances, it is mostly useful for

the company in order to accumulate costing at an aggregate level for a large batch of production

in order to making allocate them to the individual units has been produces in the plant relevantly.

Various types of such activities are being done in manufacturing plant of the company and its

manager require to utilisation of several kinds of process costing system in terms of assessment

of process costing which is being produced in the company at mass level and as per its tool and

techniques, its manager can reduce the costing of manufacturing phase of the firm appropriately.

This might be also most beneficial for the business in respect to reducing the cost of production

and other several expenses in the firm sufficiently. Some costing occurs in the business such as

Direct material costs, Direct labour costs and overhead costs etc. all these costing might be

3

reduced at the workplace in effective form in case of using this costing system in the firm

effectively.

P.2. Explain different method used for management accounting reporting

Management accounting reporting is also one of the crucial part of accounting system in

order to making proper assessment of organisation's performance and this is also assists company

to making use of some accounting period which is needed most. This is depends on the types of

quality of the project which is being implemented on the business process in order to completion

of various activities at the workplace efficiently (McLellan and Moustafa, 2011). Tata company's

manager may need to prepare management accounting reporting at the workplace as per,

projection requirements for reports quarterly, monthly and weekly at the workplace properly.

There are different kinds of management accounting techniques are presented here, which might

be utilised by company's manager in terms of proper planning for their various projections which

is being operated upon the business sufficiently.

Budget reporting: Budget reporting is also necessary terms for Tata organisation in order

to proper planning for their budget on each project which occurs in the business in future

effectively. Budget reporting could be utilised by Tata company's manager in effectively assess]

of the company performance and also analyse the departmental performances efficiently, it could

assist the firm's manger in case of proper controlling of costing on all expenses on various

projections in the efficiently. The company's manager prepare this budget on the basis on the

actual expenses form prior years properly. This must be in accurate form in the future in order to

trim various costs of the company in the industry sufficiently (Roslender and Hart, 2010).

Moreover, budget reporting also making use of some customers in case of generating more

revenue from the market in case of generating more revenue from the market in sufficient form,

so that efficient development could be gained in more relevant form. Budgeting reporting of

sales data, fixed data collection of the data and net worth of the entire organisation in their

common section of budget. This is helpful for the company in order to meeting employees of

specific financial goals of the business in the industry sufficiently. This is totally made on

estimation at the workplace, so its manager need to make more efforts to meet to budget

expected goals within given time period efficiently.

Job costing reports: This is also another essential management accounting reporting

approaches at the workplace which could be used by its manager in case of accumulating various

4

effectively.

P.2. Explain different method used for management accounting reporting

Management accounting reporting is also one of the crucial part of accounting system in

order to making proper assessment of organisation's performance and this is also assists company

to making use of some accounting period which is needed most. This is depends on the types of

quality of the project which is being implemented on the business process in order to completion

of various activities at the workplace efficiently (McLellan and Moustafa, 2011). Tata company's

manager may need to prepare management accounting reporting at the workplace as per,

projection requirements for reports quarterly, monthly and weekly at the workplace properly.

There are different kinds of management accounting techniques are presented here, which might

be utilised by company's manager in terms of proper planning for their various projections which

is being operated upon the business sufficiently.

Budget reporting: Budget reporting is also necessary terms for Tata organisation in order

to proper planning for their budget on each project which occurs in the business in future

effectively. Budget reporting could be utilised by Tata company's manager in effectively assess]

of the company performance and also analyse the departmental performances efficiently, it could

assist the firm's manger in case of proper controlling of costing on all expenses on various

projections in the efficiently. The company's manager prepare this budget on the basis on the

actual expenses form prior years properly. This must be in accurate form in the future in order to

trim various costs of the company in the industry sufficiently (Roslender and Hart, 2010).

Moreover, budget reporting also making use of some customers in case of generating more

revenue from the market in case of generating more revenue from the market in sufficient form,

so that efficient development could be gained in more relevant form. Budgeting reporting of

sales data, fixed data collection of the data and net worth of the entire organisation in their

common section of budget. This is helpful for the company in order to meeting employees of

specific financial goals of the business in the industry sufficiently. This is totally made on

estimation at the workplace, so its manager need to make more efforts to meet to budget

expected goals within given time period efficiently.

Job costing reports: This is also another essential management accounting reporting

approaches at the workplace which could be used by its manager in case of accumulating various

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costs of materials, labour and overhead for particular job in the company in relevant form.

However, this method is an excellent tool for tracing particular costing to separated jobs ad

assessing them to see if the costs could be reduced in later jobs in the industry in relevant form.

Job costing approach is used by Tata organisational manager in order to accumulating small level

of production in the company, job costing reporting is inclusion of several kinds of costing at the

workplace in effective form, so that sufficient outcomes could be gain effectively (Dekker,

2016). Job costing includes materials costing, variety of raw materials are being utilised in the

company in their auto-mobile production process and they need various components for

producing it and some labour and overhead costs are also being included in case of preparation

of job costing in the business in relevant ways. The organisational manager could use of this

reporting process at the workplace in order to examining of each jobs which is being done in the

company in proper manner.

Financial reports: This is also one of the effective reporting system which could be used

by accounting manager of Tata company in order to assessment of various financial transaction

of the company within specific time period efficiently. Financial reports assist the business

manager in case of utilisation of proper financial information which assist them to ascertain the

company's performance in give time period properly (Youssef, 2013). The business accounting

officer need to proper profit and loss statements of the firm in a specific time period, which gives

proper information about how mush company has been earned ad in which section of the

company is giving negative performance in the company in sufficient form. The company's final

financial report, balance sheet defines about how much Tata company has been earned during the

year and how much they have gained losses in the company effectively. This reporting useful for

Tata organisational manager in terms of determination of profit and loss section of the business

in the industry and as per its information, manager could make proper decision about to making

improvement in such areas of business which is giving negative performance in the firm

effectively.

TASK 2

P.3. Income statements using marginal and absorption costing methodologies

5

However, this method is an excellent tool for tracing particular costing to separated jobs ad

assessing them to see if the costs could be reduced in later jobs in the industry in relevant form.

Job costing approach is used by Tata organisational manager in order to accumulating small level

of production in the company, job costing reporting is inclusion of several kinds of costing at the

workplace in effective form, so that sufficient outcomes could be gain effectively (Dekker,

2016). Job costing includes materials costing, variety of raw materials are being utilised in the

company in their auto-mobile production process and they need various components for

producing it and some labour and overhead costs are also being included in case of preparation

of job costing in the business in relevant ways. The organisational manager could use of this

reporting process at the workplace in order to examining of each jobs which is being done in the

company in proper manner.

Financial reports: This is also one of the effective reporting system which could be used

by accounting manager of Tata company in order to assessment of various financial transaction

of the company within specific time period efficiently. Financial reports assist the business

manager in case of utilisation of proper financial information which assist them to ascertain the

company's performance in give time period properly (Youssef, 2013). The business accounting

officer need to proper profit and loss statements of the firm in a specific time period, which gives

proper information about how mush company has been earned ad in which section of the

company is giving negative performance in the company in sufficient form. The company's final

financial report, balance sheet defines about how much Tata company has been earned during the

year and how much they have gained losses in the company effectively. This reporting useful for

Tata organisational manager in terms of determination of profit and loss section of the business

in the industry and as per its information, manager could make proper decision about to making

improvement in such areas of business which is giving negative performance in the firm

effectively.

TASK 2

P.3. Income statements using marginal and absorption costing methodologies

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

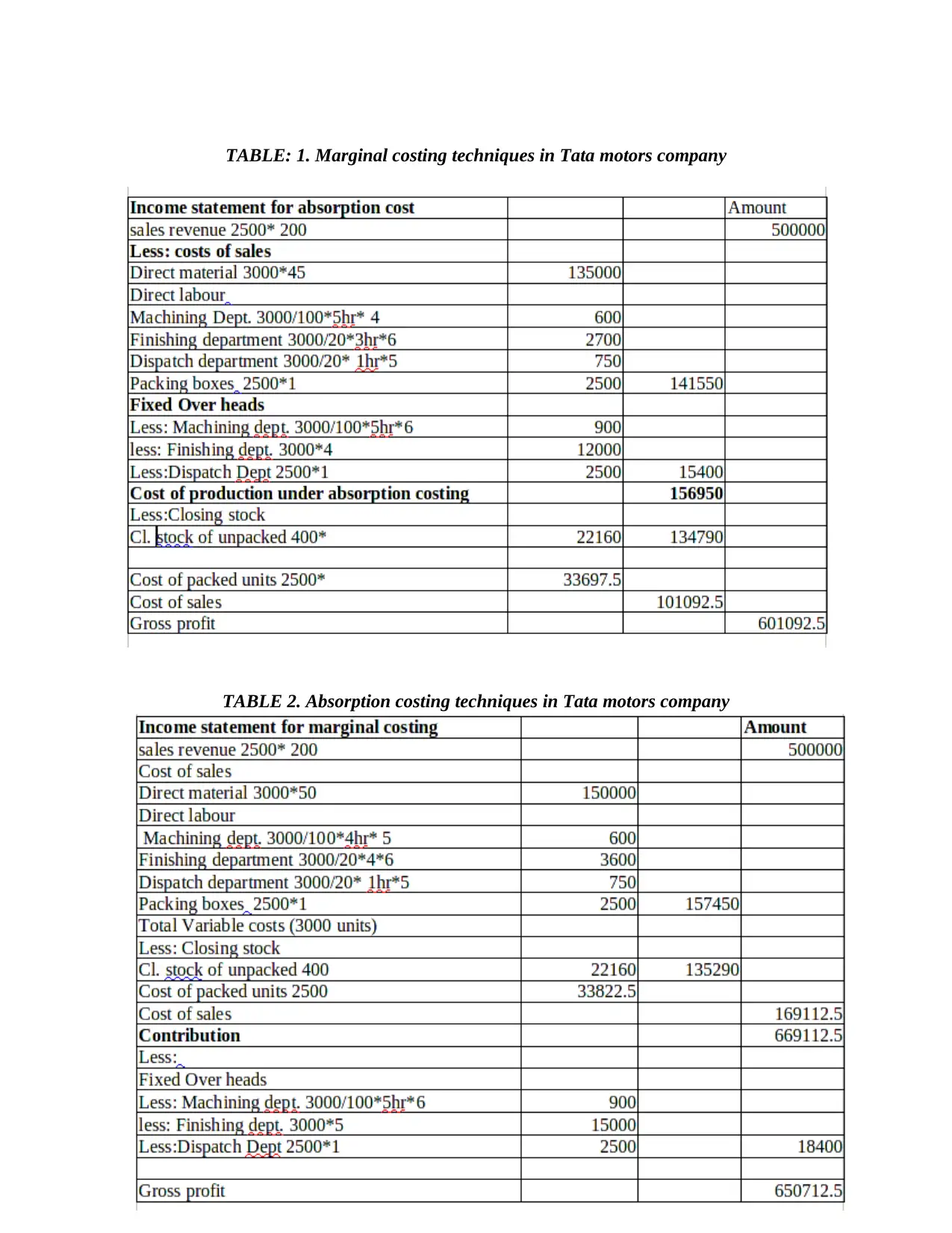

TABLE: 1. Marginal costing techniques in Tata motors company

TABLE 2. Absorption costing techniques in Tata motors company

6

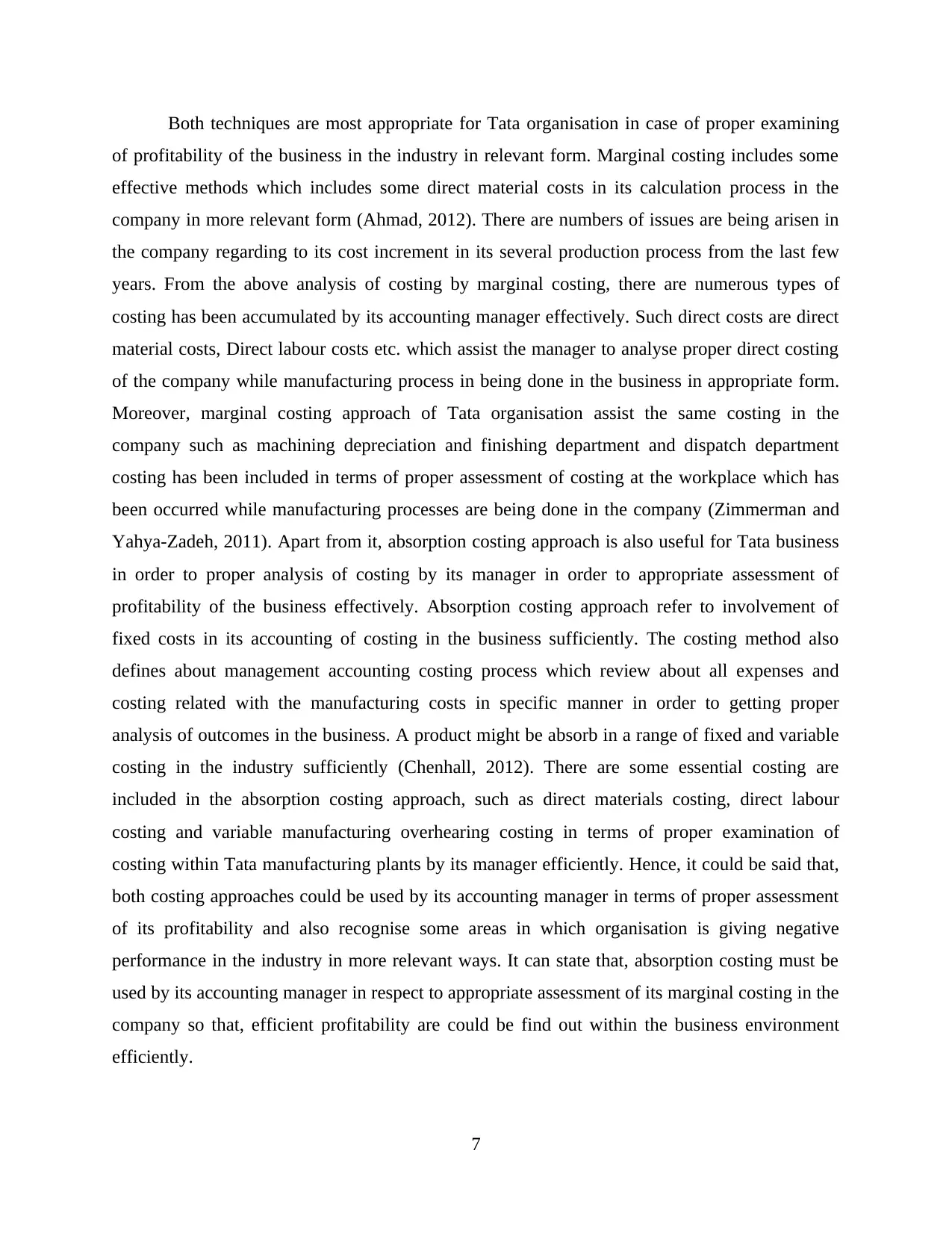

TABLE 2. Absorption costing techniques in Tata motors company

6

Both techniques are most appropriate for Tata organisation in case of proper examining

of profitability of the business in the industry in relevant form. Marginal costing includes some

effective methods which includes some direct material costs in its calculation process in the

company in more relevant form (Ahmad, 2012). There are numbers of issues are being arisen in

the company regarding to its cost increment in its several production process from the last few

years. From the above analysis of costing by marginal costing, there are numerous types of

costing has been accumulated by its accounting manager effectively. Such direct costs are direct

material costs, Direct labour costs etc. which assist the manager to analyse proper direct costing

of the company while manufacturing process in being done in the business in appropriate form.

Moreover, marginal costing approach of Tata organisation assist the same costing in the

company such as machining depreciation and finishing department and dispatch department

costing has been included in terms of proper assessment of costing at the workplace which has

been occurred while manufacturing processes are being done in the company (Zimmerman and

Yahya-Zadeh, 2011). Apart from it, absorption costing approach is also useful for Tata business

in order to proper analysis of costing by its manager in order to appropriate assessment of

profitability of the business effectively. Absorption costing approach refer to involvement of

fixed costs in its accounting of costing in the business sufficiently. The costing method also

defines about management accounting costing process which review about all expenses and

costing related with the manufacturing costs in specific manner in order to getting proper

analysis of outcomes in the business. A product might be absorb in a range of fixed and variable

costing in the industry sufficiently (Chenhall, 2012). There are some essential costing are

included in the absorption costing approach, such as direct materials costing, direct labour

costing and variable manufacturing overhearing costing in terms of proper examination of

costing within Tata manufacturing plants by its manager efficiently. Hence, it could be said that,

both costing approaches could be used by its accounting manager in terms of proper assessment

of its profitability and also recognise some areas in which organisation is giving negative

performance in the industry in more relevant ways. It can state that, absorption costing must be

used by its accounting manager in respect to appropriate assessment of its marginal costing in the

company so that, efficient profitability are could be find out within the business environment

efficiently.

7

of profitability of the business in the industry in relevant form. Marginal costing includes some

effective methods which includes some direct material costs in its calculation process in the

company in more relevant form (Ahmad, 2012). There are numbers of issues are being arisen in

the company regarding to its cost increment in its several production process from the last few

years. From the above analysis of costing by marginal costing, there are numerous types of

costing has been accumulated by its accounting manager effectively. Such direct costs are direct

material costs, Direct labour costs etc. which assist the manager to analyse proper direct costing

of the company while manufacturing process in being done in the business in appropriate form.

Moreover, marginal costing approach of Tata organisation assist the same costing in the

company such as machining depreciation and finishing department and dispatch department

costing has been included in terms of proper assessment of costing at the workplace which has

been occurred while manufacturing processes are being done in the company (Zimmerman and

Yahya-Zadeh, 2011). Apart from it, absorption costing approach is also useful for Tata business

in order to proper analysis of costing by its manager in order to appropriate assessment of

profitability of the business effectively. Absorption costing approach refer to involvement of

fixed costs in its accounting of costing in the business sufficiently. The costing method also

defines about management accounting costing process which review about all expenses and

costing related with the manufacturing costs in specific manner in order to getting proper

analysis of outcomes in the business. A product might be absorb in a range of fixed and variable

costing in the industry sufficiently (Chenhall, 2012). There are some essential costing are

included in the absorption costing approach, such as direct materials costing, direct labour

costing and variable manufacturing overhearing costing in terms of proper examination of

costing within Tata manufacturing plants by its manager efficiently. Hence, it could be said that,

both costing approaches could be used by its accounting manager in terms of proper assessment

of its profitability and also recognise some areas in which organisation is giving negative

performance in the industry in more relevant ways. It can state that, absorption costing must be

used by its accounting manager in respect to appropriate assessment of its marginal costing in the

company so that, efficient profitability are could be find out within the business environment

efficiently.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P.4. Explain the advantage and disadvantages of different types of planning tools used for

budgetary control in Tata motors

This is also most necessary part of the business in case of preparation of proper budgeting

for Tata Motors company in order to proper distribution of funds of its various parts in the

company in sufficient form in case of running of its varied of function in the industry in relevant

manner (Adams and Drtina, 2010).

Internal rate of return: This is also useful terms for Tata Motors company in order to

preparation of capital budgeting at the workplace effectively. This approach could be used by

Tata company junior management accountant in order to making forecast of profitability on its

potential investments of the company on given time period efficiently (Abdel-Kader, ed., 2011).

This is a discount rate of the company, that represent the net present value(NPV) of all cash

flows of the company which has been made on specific projection of the company appropriately.

Advantages:

Internal rate of return considers the times value of the money in the business on the

annual cash inflow is equal or unequal in the firm effectively.

This budget approach is totally easy to understand values in the business properly so, that

could effectively present in the company. This is helpful for the organisation in respect to maximise the profitability of the business

in the industry in relevant manner (Hammad, Jusoh and Yen Nee Oon, 2010).

Disadvantages:

This approach defines about earning and make reinvestment at the internal rate of return

for the remaining life of the project is essential for the project of company and in this

case, if the average rate of return gain by the firm in not closed to the internal rate of

return, then the business could not get proper profitability in the business

efficiently(Cokins, 2013).

It has tedious calculation method which is very lengthy approach and time consuming

system for its business manager.

Zero base budgeting: This is also necessary for Tata Motors company, which defines

that, zero base budgeting start in the firm from zero base and it is method of budgeting by which

its manager need to all expenses must be justified for each new period of the business. This

budget begins from the zero base in the business sufficiently.

8

budgetary control in Tata motors

This is also most necessary part of the business in case of preparation of proper budgeting

for Tata Motors company in order to proper distribution of funds of its various parts in the

company in sufficient form in case of running of its varied of function in the industry in relevant

manner (Adams and Drtina, 2010).

Internal rate of return: This is also useful terms for Tata Motors company in order to

preparation of capital budgeting at the workplace effectively. This approach could be used by

Tata company junior management accountant in order to making forecast of profitability on its

potential investments of the company on given time period efficiently (Abdel-Kader, ed., 2011).

This is a discount rate of the company, that represent the net present value(NPV) of all cash

flows of the company which has been made on specific projection of the company appropriately.

Advantages:

Internal rate of return considers the times value of the money in the business on the

annual cash inflow is equal or unequal in the firm effectively.

This budget approach is totally easy to understand values in the business properly so, that

could effectively present in the company. This is helpful for the organisation in respect to maximise the profitability of the business

in the industry in relevant manner (Hammad, Jusoh and Yen Nee Oon, 2010).

Disadvantages:

This approach defines about earning and make reinvestment at the internal rate of return

for the remaining life of the project is essential for the project of company and in this

case, if the average rate of return gain by the firm in not closed to the internal rate of

return, then the business could not get proper profitability in the business

efficiently(Cokins, 2013).

It has tedious calculation method which is very lengthy approach and time consuming

system for its business manager.

Zero base budgeting: This is also necessary for Tata Motors company, which defines

that, zero base budgeting start in the firm from zero base and it is method of budgeting by which

its manager need to all expenses must be justified for each new period of the business. This

budget begins from the zero base in the business sufficiently.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages:

With the help of zero base budgeting in the company, its manager can save the inefficient

costing which occurs in its operational level in the firm effectively (Hopper and Bui,

2016). The junior management account of the company can easily review about clear picture to

the extent of finance present in the business and also helps to raise finance in the

company sufficiently.

Disadvantages:

In case of Tata business, its manager ned to make large number of decision packages

within the firm in this budgeting and it includes variety of expenses in the business

appropriately (France, 2010).

Various kinds of expertise is needed for preparation of Zero base budgeting at the

workplace effectively, which is required to high expenses in the business sufficiently.

P5 Management accounting system for the resolution of financial problems.

Lean Accounting- lean accounting refers that the general changes in the company for

controlling, measurement and management process. The lean accounting is the business

management tools that focus on reducing waste from production process. The purpose of lean

accounting is to support lean enterprise as a business strategy. It seeks to move form traditional

accounting method to a system that measure and motivate excellent business practice in a lean

enterprise. Lean accounting refers that reducing extra cost of goods and services witch is

provided to customers. The lean accounting describe that any organization they are used to

reduced the unnecessary row material to the products and removing the waste material from the

products. This process benefited for organization because they control cost of the products and it

help for avoiding problems of the products.

Process costing- Process costing is the method for collecting and assigning

manufacturing cost of the products. Process costing is type of operation costing which is use for

maintain the products manufacturing cost. Process costing use where the mass production of

similar products. The cost of each products is assumed to be the same as the cost of the other

products. The process costing involve that process where the process are under manufacturing

period. Process costing is the only reasonable approach to determining product cost many

industries . Is uses most of the same journal entries found in a job costing environment, so there

9

With the help of zero base budgeting in the company, its manager can save the inefficient

costing which occurs in its operational level in the firm effectively (Hopper and Bui,

2016). The junior management account of the company can easily review about clear picture to

the extent of finance present in the business and also helps to raise finance in the

company sufficiently.

Disadvantages:

In case of Tata business, its manager ned to make large number of decision packages

within the firm in this budgeting and it includes variety of expenses in the business

appropriately (France, 2010).

Various kinds of expertise is needed for preparation of Zero base budgeting at the

workplace effectively, which is required to high expenses in the business sufficiently.

P5 Management accounting system for the resolution of financial problems.

Lean Accounting- lean accounting refers that the general changes in the company for

controlling, measurement and management process. The lean accounting is the business

management tools that focus on reducing waste from production process. The purpose of lean

accounting is to support lean enterprise as a business strategy. It seeks to move form traditional

accounting method to a system that measure and motivate excellent business practice in a lean

enterprise. Lean accounting refers that reducing extra cost of goods and services witch is

provided to customers. The lean accounting describe that any organization they are used to

reduced the unnecessary row material to the products and removing the waste material from the

products. This process benefited for organization because they control cost of the products and it

help for avoiding problems of the products.

Process costing- Process costing is the method for collecting and assigning

manufacturing cost of the products. Process costing is type of operation costing which is use for

maintain the products manufacturing cost. Process costing use where the mass production of

similar products. The cost of each products is assumed to be the same as the cost of the other

products. The process costing involve that process where the process are under manufacturing

period. Process costing is the only reasonable approach to determining product cost many

industries . Is uses most of the same journal entries found in a job costing environment, so there

9

is no need to restructure the chart of account to any significant degree , this make it easy to job

costing system from a process costing one if the need arises, or to adopt hybrid approach that

uses portion of both system.

Through put accounting system- The through accounting (TA) refers that it is simple

accounting based system. Through put accounting system makes growth- driven management

and decision making system that understandable for all peoples. This method is most accurate

and most fast in using. This is provide accurate financial problems and solve them. The through

put accounting system is based on through put analyzing. Through refers as the rate of a

producing goals units and translate as a revenue or sales minus totally variable expenses in

accounting terms. Some of the important points through put analysis needed to including:

Manage and make decision in a growth oriented and ToC way.

Allow faster reporting and near to real-time figure based management.

Helping of people to understand the basics of accounting.

Transfer Pricing- The transfer pricing means the price changing by one company to

another company according to the organization. This can include sales or products. Transfer

pricing is important for assessing the performance of business units of multinational and the

mangers of those units. In the simple way transfer pricing is the process who adopts every

company, those companies are changes products price according to there strategies. The

multinational companies who adopts this process they have to paying tax for this process

regarding.

Conclusion

From the above concluded that, management accounting is the most appropriate system

that assist the SME in managing its critical business. Management accounting is the approach

which defines about preparing a proper management reports in the organisation in order to

management of all financial accounting information in case of reduction of costing in business

efficiently. Further it is concluded that This is also useful terms for Tata Motors company in

order to preparation of capital budgeting at the workplace effectively. lean accounting refers that

the general changes in the company for controlling, measurement and management process. The

lean accounting is the business management tools that focus on reducing waste from production

process. Financial reporting is also one of the effective reporting system which could be used by

10

costing system from a process costing one if the need arises, or to adopt hybrid approach that

uses portion of both system.

Through put accounting system- The through accounting (TA) refers that it is simple

accounting based system. Through put accounting system makes growth- driven management

and decision making system that understandable for all peoples. This method is most accurate

and most fast in using. This is provide accurate financial problems and solve them. The through

put accounting system is based on through put analyzing. Through refers as the rate of a

producing goals units and translate as a revenue or sales minus totally variable expenses in

accounting terms. Some of the important points through put analysis needed to including:

Manage and make decision in a growth oriented and ToC way.

Allow faster reporting and near to real-time figure based management.

Helping of people to understand the basics of accounting.

Transfer Pricing- The transfer pricing means the price changing by one company to

another company according to the organization. This can include sales or products. Transfer

pricing is important for assessing the performance of business units of multinational and the

mangers of those units. In the simple way transfer pricing is the process who adopts every

company, those companies are changes products price according to there strategies. The

multinational companies who adopts this process they have to paying tax for this process

regarding.

Conclusion

From the above concluded that, management accounting is the most appropriate system

that assist the SME in managing its critical business. Management accounting is the approach

which defines about preparing a proper management reports in the organisation in order to

management of all financial accounting information in case of reduction of costing in business

efficiently. Further it is concluded that This is also useful terms for Tata Motors company in

order to preparation of capital budgeting at the workplace effectively. lean accounting refers that

the general changes in the company for controlling, measurement and management process. The

lean accounting is the business management tools that focus on reducing waste from production

process. Financial reporting is also one of the effective reporting system which could be used by

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.