Management Accounting Systems & Reporting for Tata Motors Ltd

VerifiedAdded on 2024/05/20

|7

|1384

|404

Report

AI Summary

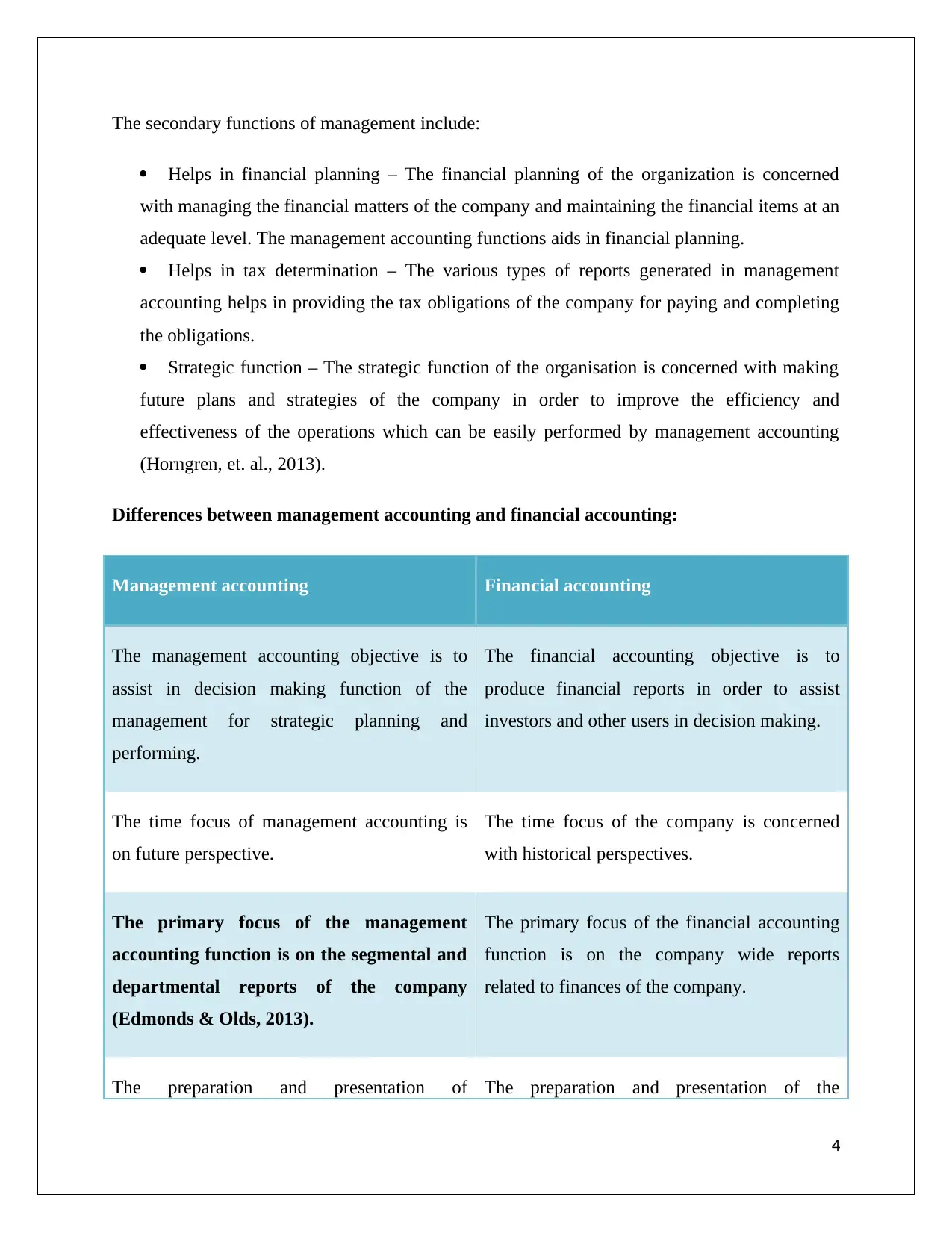

This report provides an overview of management accounting and its application within Tata Motors. It defines management accounting as a function involving planning, organizing, and controlling company activities through the use of relevant information and reports. The report highlights the primary and secondary functions of management accounting, including providing accounting information, assisting in managerial activities, financial planning, tax determination, and strategic planning. It differentiates management accounting from financial accounting, emphasizing their distinct objectives and focuses. Furthermore, the report discusses various management accounting systems relevant to Tata Motors, such as cost accounting, inventory management, and price optimization systems, outlining their essential requirements. Finally, it explains different management accounting reporting methods, including budgeting reports, cost and revenue reports, and investment appraisal reports, along with the benefits of implementing these systems within Tata Motors, such as cost reduction, innovation, and improved operational efficiency. Desklib offers a wealth of similar resources for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.