Tech Ltd Management Accounting: Decision Making and Financial Issues

VerifiedAdded on 2020/12/09

|17

|3900

|177

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices relevant to Tech Ltd, a company specializing in mobile phone chargers. The report begins by defining management accounting and differentiating it from financial accounting, emphasizing its role in internal decision-making. It then explores the importance of management accounting information for Tech Ltd, covering areas such as make-or-buy decisions, cash flow forecasting, variance analysis, and resource allocation. Various management accounting systems, including cost accounting, inventory management, and job costing, are examined with their respective advantages and disadvantages. The report further illustrates how managerial reporting aids in decision-making through job cost reports, inventory reports, accounts receivable ageing reports, and budget/performance reports. It also explains the significance of understandability in managerial reports. The report includes a profitability statement prepared using both marginal and absorption costing methods, along with an interpretation of the results. Finally, the report discusses different types of budgets, their advantages and disadvantages, and the budget preparation process, highlighting their importance as decision-making tools. The report concludes with a comparison of how organizations adapt management accounting to respond to financial problems, offering valuable insights for Tech Ltd to improve its financial performance and decision-making processes.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a....................................................................................................................................................3

1. Defining management accounting and differentiating it from financial.................................3

2. Presenting the importance of management accounting information as a decision making tool

.....................................................................................................................................................4

3. Cost accounting system...........................................................................................................5

4. Inventory management system................................................................................................6

5. Job costing system...................................................................................................................6

B...................................................................................................................................................7

1. Presenting the manner in which managerial reporting aid in decision making.......................7

2. Stating reasons behind the inclusion of understand-ability characteristics in managerial

reports..........................................................................................................................................8

TASK 2............................................................................................................................................8

Preparation of profitability statement as per marginal and absorption costing method..............8

Presenting different kinds of budgets and their advantages and disadvantages........................10

Describing budget preparation process and costing system that can be used for taking pricing

decisions....................................................................................................................................12

Stating the importance of budget as a decision making tool.....................................................13

TASK 4..........................................................................................................................................13

Comparing the manner in which organisations use adapt management accounting for

responding financial problems...................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

a....................................................................................................................................................3

1. Defining management accounting and differentiating it from financial.................................3

2. Presenting the importance of management accounting information as a decision making tool

.....................................................................................................................................................4

3. Cost accounting system...........................................................................................................5

4. Inventory management system................................................................................................6

5. Job costing system...................................................................................................................6

B...................................................................................................................................................7

1. Presenting the manner in which managerial reporting aid in decision making.......................7

2. Stating reasons behind the inclusion of understand-ability characteristics in managerial

reports..........................................................................................................................................8

TASK 2............................................................................................................................................8

Preparation of profitability statement as per marginal and absorption costing method..............8

Presenting different kinds of budgets and their advantages and disadvantages........................10

Describing budget preparation process and costing system that can be used for taking pricing

decisions....................................................................................................................................12

Stating the importance of budget as a decision making tool.....................................................13

TASK 4..........................................................................................................................................13

Comparing the manner in which organisations use adapt management accounting for

responding financial problems...................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting tools are widely used by the business organization around the

globe. In the recent times, both profit and non-profit making organizations, undertake managerial

accounting tools for making effectual use of financial resources. Moreover, it renders

information about day to day activities as well as operations and thereby aid in decision making

aspects. The present report is based on the case scenario of Tech ltd which provides customers

with special chargers for the mobile phone. Business entity of Tech Ltd owns & operates retail

outlets in UK and now concerned about making improvement in the decision making aspect as

well as overall performance. In this, report will describe different type of management

accounting systems along with the essential requirements. Further, report will present the manner

in which different types of accounting system aid in managerial decision making.

TASK 1

a.

1. Defining management accounting and differentiating it from financial

Management accounting lays emphasis on analyzing and evaluating monetary

information related to the internal operations. Such field of accounting provides manager with

appropriate cost information for planning, controlling and decision-making purpose.

On the contrary to MA, financial accounting focuses on providing information about

business transactions to both internal and external stakeholders (Hilton and Platt, 2013). Hence,

financial accounting places emphasis on recording, summarizing and presenting information

about business transactions over the time frame.

Difference between management and financial accounting can be presented on the basis of

following aspects:

Basis of difference Management accounting Financial accounting

Management accounting tools are widely used by the business organization around the

globe. In the recent times, both profit and non-profit making organizations, undertake managerial

accounting tools for making effectual use of financial resources. Moreover, it renders

information about day to day activities as well as operations and thereby aid in decision making

aspects. The present report is based on the case scenario of Tech ltd which provides customers

with special chargers for the mobile phone. Business entity of Tech Ltd owns & operates retail

outlets in UK and now concerned about making improvement in the decision making aspect as

well as overall performance. In this, report will describe different type of management

accounting systems along with the essential requirements. Further, report will present the manner

in which different types of accounting system aid in managerial decision making.

TASK 1

a.

1. Defining management accounting and differentiating it from financial

Management accounting lays emphasis on analyzing and evaluating monetary

information related to the internal operations. Such field of accounting provides manager with

appropriate cost information for planning, controlling and decision-making purpose.

On the contrary to MA, financial accounting focuses on providing information about

business transactions to both internal and external stakeholders (Hilton and Platt, 2013). Hence,

financial accounting places emphasis on recording, summarizing and presenting information

about business transactions over the time frame.

Difference between management and financial accounting can be presented on the basis of

following aspects:

Basis of difference Management accounting Financial accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

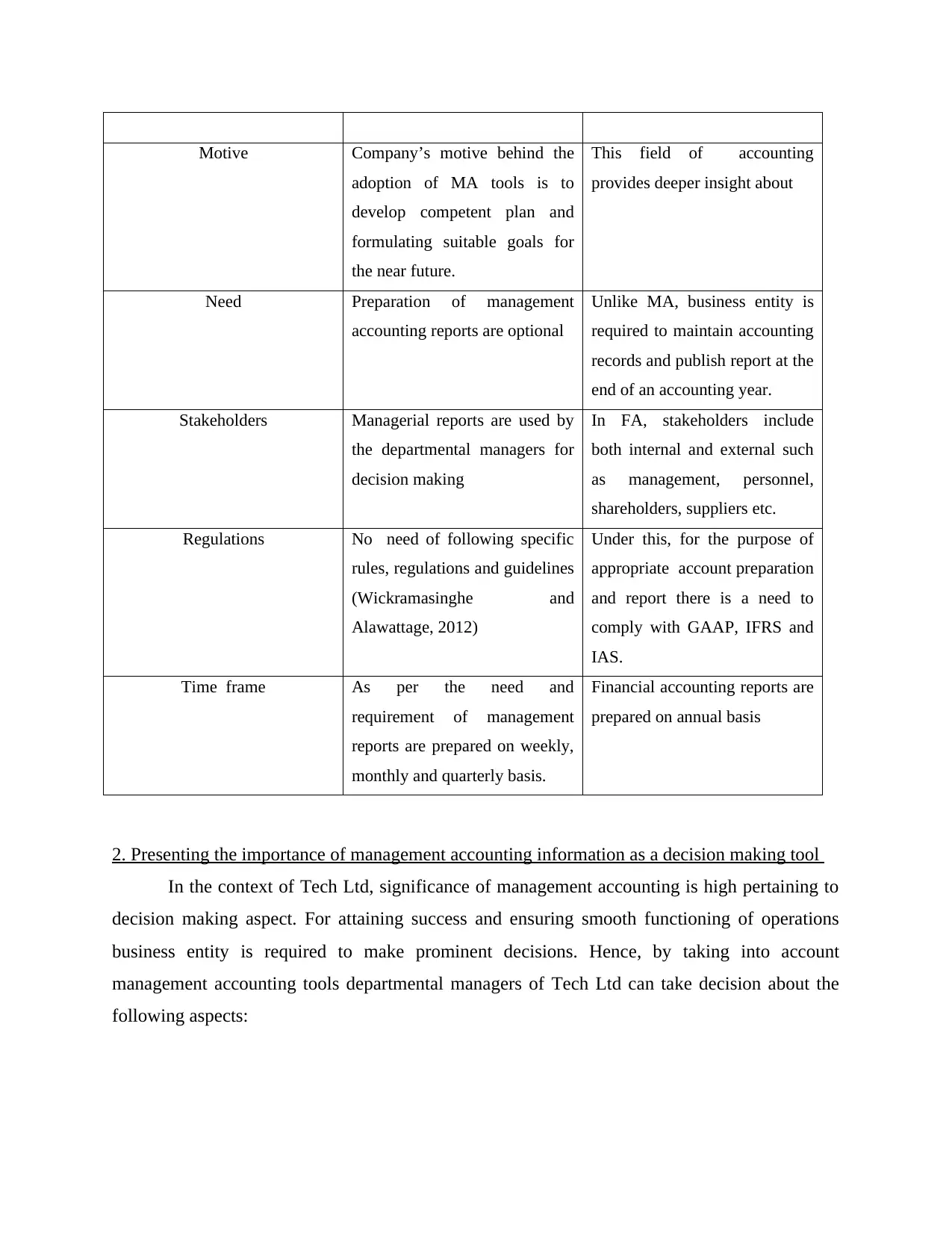

Motive Company’s motive behind the

adoption of MA tools is to

develop competent plan and

formulating suitable goals for

the near future.

This field of accounting

provides deeper insight about

Need Preparation of management

accounting reports are optional

Unlike MA, business entity is

required to maintain accounting

records and publish report at the

end of an accounting year.

Stakeholders Managerial reports are used by

the departmental managers for

decision making

In FA, stakeholders include

both internal and external such

as management, personnel,

shareholders, suppliers etc.

Regulations No need of following specific

rules, regulations and guidelines

(Wickramasinghe and

Alawattage, 2012)

Under this, for the purpose of

appropriate account preparation

and report there is a need to

comply with GAAP, IFRS and

IAS.

Time frame As per the need and

requirement of management

reports are prepared on weekly,

monthly and quarterly basis.

Financial accounting reports are

prepared on annual basis

2. Presenting the importance of management accounting information as a decision making tool

In the context of Tech Ltd, significance of management accounting is high pertaining to

decision making aspect. For attaining success and ensuring smooth functioning of operations

business entity is required to make prominent decisions. Hence, by taking into account

management accounting tools departmental managers of Tech Ltd can take decision about the

following aspects:

adoption of MA tools is to

develop competent plan and

formulating suitable goals for

the near future.

This field of accounting

provides deeper insight about

Need Preparation of management

accounting reports are optional

Unlike MA, business entity is

required to maintain accounting

records and publish report at the

end of an accounting year.

Stakeholders Managerial reports are used by

the departmental managers for

decision making

In FA, stakeholders include

both internal and external such

as management, personnel,

shareholders, suppliers etc.

Regulations No need of following specific

rules, regulations and guidelines

(Wickramasinghe and

Alawattage, 2012)

Under this, for the purpose of

appropriate account preparation

and report there is a need to

comply with GAAP, IFRS and

IAS.

Time frame As per the need and

requirement of management

reports are prepared on weekly,

monthly and quarterly basis.

Financial accounting reports are

prepared on annual basis

2. Presenting the importance of management accounting information as a decision making tool

In the context of Tech Ltd, significance of management accounting is high pertaining to

decision making aspect. For attaining success and ensuring smooth functioning of operations

business entity is required to make prominent decisions. Hence, by taking into account

management accounting tools departmental managers of Tech Ltd can take decision about the

following aspects:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Make or buy decision: MA field helps in ascertaining the cost of manufacturing chargers

in house as well as outsourcing. This in turn helps managers is taking suitable decision

from the perspective of cost saving and profit maximization.

Cash flow forecasting: Management accounting facilitates forecasting of cash flows and

thereby helps in taking suitable decisions. In other words, through the means of

budgeting tools and techniques Tech Ltd’s manager can make estimation about income

and expenses.

Assists in understanding performance variances: Departmental manager can assess and

evaluate performance of each department with the help of variance analysis (Fullerton,

Kennedy and Widener, 2014). Thus, by identifying deviations firm can take corrective

action within the suitable time frame.

Helps in analyzing rate of return: MA assists in finding best option out of several which

is offering high returns on the investment over others.

Facilitates cost control: Departmental managers can avoid redundant business activities

with the help of MA tools and thereby becomes able to control cost.

Optimal allocation of resources: MA helps in identifying profitable operations and helps

in making allocation of resources in the suitable activities.

3. Cost accounting system

This accounting system is used by the business organizations such as Tech ltd for making

estimation about the cost of products or services for profitability analysis. It mainly includes

normal and standard costing system which firm can use for evaluation purpose. Normal costing

system is highly effectual which in turn helps in valuing manufactured products on the basis of

predetermined rate (Christ and Burritt, 2013). Further, standard costing system helps in

evaluating or comparing actual income as well as expenses with the budgeted figures. Hence, by

assessing deviations Tech Ltd can strategic decision for improvement within the suitable time

frame.

Advantages

Cost accounting system provides assistance in eliminating wastage, losses and

inefficiencies to a great extent

in house as well as outsourcing. This in turn helps managers is taking suitable decision

from the perspective of cost saving and profit maximization.

Cash flow forecasting: Management accounting facilitates forecasting of cash flows and

thereby helps in taking suitable decisions. In other words, through the means of

budgeting tools and techniques Tech Ltd’s manager can make estimation about income

and expenses.

Assists in understanding performance variances: Departmental manager can assess and

evaluate performance of each department with the help of variance analysis (Fullerton,

Kennedy and Widener, 2014). Thus, by identifying deviations firm can take corrective

action within the suitable time frame.

Helps in analyzing rate of return: MA assists in finding best option out of several which

is offering high returns on the investment over others.

Facilitates cost control: Departmental managers can avoid redundant business activities

with the help of MA tools and thereby becomes able to control cost.

Optimal allocation of resources: MA helps in identifying profitable operations and helps

in making allocation of resources in the suitable activities.

3. Cost accounting system

This accounting system is used by the business organizations such as Tech ltd for making

estimation about the cost of products or services for profitability analysis. It mainly includes

normal and standard costing system which firm can use for evaluation purpose. Normal costing

system is highly effectual which in turn helps in valuing manufactured products on the basis of

predetermined rate (Christ and Burritt, 2013). Further, standard costing system helps in

evaluating or comparing actual income as well as expenses with the budgeted figures. Hence, by

assessing deviations Tech Ltd can strategic decision for improvement within the suitable time

frame.

Advantages

Cost accounting system provides assistance in eliminating wastage, losses and

inefficiencies to a great extent

It lays emphasis on undertaking cost effectual methods of production. This in turn leads

cost reduction and profit maximization.

This managerial accounting system helps in identifying reasons behind profit or loss.

Disadvantages

Cost accounting system furnishes information about past performance whereas

management is concerned in relation to taking decision about future

Involves issue regarding under or over absorption of overhead

Installation regarding cost accounting system imposes high monetary expenses in front of

the firm. Moreover, it demands for the maintenance of many costing records.

4. Inventory management system

In the context of business unit, inventory management is highly vital for managing cost

and ensuring the smooth functioning of operations. There are several methods which can be used

by Tech Ltd for inventory management and valuation such as FIFO, LIFO, perpetual etc. By

employing FIFO method business unit can avoid the risk of obsolescence to the significant level

through selling firstly purchased or manufactured products on prior basis (Banerjee, 2012). In

addition to this, economic order quantity, just in time etc methods helps in making proper

inventory management. EOQ helps in assessing the number of raw and finished units need to be

maintained within the firm for ensuring smooth functioning of operations.

Advantages

Helps in avoiding wastage and losses Assists in reducing the level of production bottlenecks

Disadvantages

Time intensive exercise

Inventory software installation and training of personnel imposes cost in front of Tech

Ltd

cost reduction and profit maximization.

This managerial accounting system helps in identifying reasons behind profit or loss.

Disadvantages

Cost accounting system furnishes information about past performance whereas

management is concerned in relation to taking decision about future

Involves issue regarding under or over absorption of overhead

Installation regarding cost accounting system imposes high monetary expenses in front of

the firm. Moreover, it demands for the maintenance of many costing records.

4. Inventory management system

In the context of business unit, inventory management is highly vital for managing cost

and ensuring the smooth functioning of operations. There are several methods which can be used

by Tech Ltd for inventory management and valuation such as FIFO, LIFO, perpetual etc. By

employing FIFO method business unit can avoid the risk of obsolescence to the significant level

through selling firstly purchased or manufactured products on prior basis (Banerjee, 2012). In

addition to this, economic order quantity, just in time etc methods helps in making proper

inventory management. EOQ helps in assessing the number of raw and finished units need to be

maintained within the firm for ensuring smooth functioning of operations.

Advantages

Helps in avoiding wastage and losses Assists in reducing the level of production bottlenecks

Disadvantages

Time intensive exercise

Inventory software installation and training of personnel imposes cost in front of Tech

Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. Job costing system

It implies for the specific costing system which is used when production carried out in

accordance with the customer’s requirements. Under job costing method, manufacturing

expenses are assigned to the individual product or services (Job costing, 2018). Hence, Tech Ltd

can assess cost and take suitable pricing decision by undertaking job costing system. For

instance: Manufacturing cost in relation to 100 units of charger implies for £20000. In this, per

unit manufacturing cost can be assessed in the following way:

Unit cost of charger: 20000 / 100

= £200

Advantages

Helps in making estimation about the cost of similar jobs

Job costing method facilitates detailed evaluation of labour, material and overhead cost.

Assists in undertaking budgetary control tool for performance evaluation

Disadvantages

This costing method demands for more clerical work

Highly expensive in nature because records need to be kept at the every step of order.

B.

1. Presenting the manner in which managerial reporting aid in decision making

Manager of Tech Ltd places high level of emphasis on undertaking managerial reports for

getting information about internal operations and taking decision about future growth or success.

Hence, specifically there are mainly four managerial reports which Tech Ltd can prepare for

effective decision making.

Job cost report: Manager of Tech Ltd can assess cost associated with the specific project

by using such report. Job cost report offers opportunity to the manager to evaluate

profitability by doing comparison with the budgeted figures. Using job cost report, Tech

Ltd’s manager can assess high performing areas and thereby become able to focusing

efforts into the same. In addition to this, manager can assess projects

It implies for the specific costing system which is used when production carried out in

accordance with the customer’s requirements. Under job costing method, manufacturing

expenses are assigned to the individual product or services (Job costing, 2018). Hence, Tech Ltd

can assess cost and take suitable pricing decision by undertaking job costing system. For

instance: Manufacturing cost in relation to 100 units of charger implies for £20000. In this, per

unit manufacturing cost can be assessed in the following way:

Unit cost of charger: 20000 / 100

= £200

Advantages

Helps in making estimation about the cost of similar jobs

Job costing method facilitates detailed evaluation of labour, material and overhead cost.

Assists in undertaking budgetary control tool for performance evaluation

Disadvantages

This costing method demands for more clerical work

Highly expensive in nature because records need to be kept at the every step of order.

B.

1. Presenting the manner in which managerial reporting aid in decision making

Manager of Tech Ltd places high level of emphasis on undertaking managerial reports for

getting information about internal operations and taking decision about future growth or success.

Hence, specifically there are mainly four managerial reports which Tech Ltd can prepare for

effective decision making.

Job cost report: Manager of Tech Ltd can assess cost associated with the specific project

by using such report. Job cost report offers opportunity to the manager to evaluate

profitability by doing comparison with the budgeted figures. Using job cost report, Tech

Ltd’s manager can assess high performing areas and thereby become able to focusing

efforts into the same. In addition to this, manager can assess projects

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory report: By undertaking such report, Tech Ltd can make manufacturing process

more efficient and smoother. Stock report provides information about wastage, hourly

labour and per unit overhead cost (Figge and Hahn, 2013). Hence, this report assists

manager in doing comparison of different assembly lines and assessing best performing

departments. Thus, inventory report enables business unit to find out the most effectual

ways of performing activities and thereby exerts control on cost level.

Accounts receivable ageing report: Tech Ltd can ensure prominent cash flow

management by using accounts receivable ageing report. Concerned report is highly

suitable for the companies which grant credit to their customers. Receivable report

presents the time frame for which customers are taking products or services on credit

basis. Hence, problems which take place in the monetary collection process can easily be

assessed through receivable reports. Thus, by assessing the capacity of debtor in relation

to making payment on time Tech Ltd can decide whether it should tighten credit policies

or not.

Budget or performance report: This report enables manager to analyze departmental and

thereby overall company’s performance. Budget report furnishes information about the

extent to which actual expenses incurred and revenue generated is in line with the

budgeted figures. Thus, referring performance report manager of Tech Ltd can set

suitable standards for the near future. Besides this, it also helps in ascertaining feasible

ways to trim cost and setting incentive plans for each department.

2. Stating reasons behind the inclusion of understand-ability characteristics in managerial reports

Tech Ltd prepares managerial report with the motive to take effectual decisions which

makes contribution in the attainment of organizational goals and objectives. Hence, management

accounting team needs to ensure that report contains the feature of reliability, comparability and

understand-ability (Caglio and Ditillo, 2012). In other words, it can be depicted that team of

management accounting reports about cost, departmental performance etc should be presented in

a clear & precise way that manager can easily understand and thereby becomes able to take

appropriate decisions.

more efficient and smoother. Stock report provides information about wastage, hourly

labour and per unit overhead cost (Figge and Hahn, 2013). Hence, this report assists

manager in doing comparison of different assembly lines and assessing best performing

departments. Thus, inventory report enables business unit to find out the most effectual

ways of performing activities and thereby exerts control on cost level.

Accounts receivable ageing report: Tech Ltd can ensure prominent cash flow

management by using accounts receivable ageing report. Concerned report is highly

suitable for the companies which grant credit to their customers. Receivable report

presents the time frame for which customers are taking products or services on credit

basis. Hence, problems which take place in the monetary collection process can easily be

assessed through receivable reports. Thus, by assessing the capacity of debtor in relation

to making payment on time Tech Ltd can decide whether it should tighten credit policies

or not.

Budget or performance report: This report enables manager to analyze departmental and

thereby overall company’s performance. Budget report furnishes information about the

extent to which actual expenses incurred and revenue generated is in line with the

budgeted figures. Thus, referring performance report manager of Tech Ltd can set

suitable standards for the near future. Besides this, it also helps in ascertaining feasible

ways to trim cost and setting incentive plans for each department.

2. Stating reasons behind the inclusion of understand-ability characteristics in managerial reports

Tech Ltd prepares managerial report with the motive to take effectual decisions which

makes contribution in the attainment of organizational goals and objectives. Hence, management

accounting team needs to ensure that report contains the feature of reliability, comparability and

understand-ability (Caglio and Ditillo, 2012). In other words, it can be depicted that team of

management accounting reports about cost, departmental performance etc should be presented in

a clear & precise way that manager can easily understand and thereby becomes able to take

appropriate decisions.

TASK 2

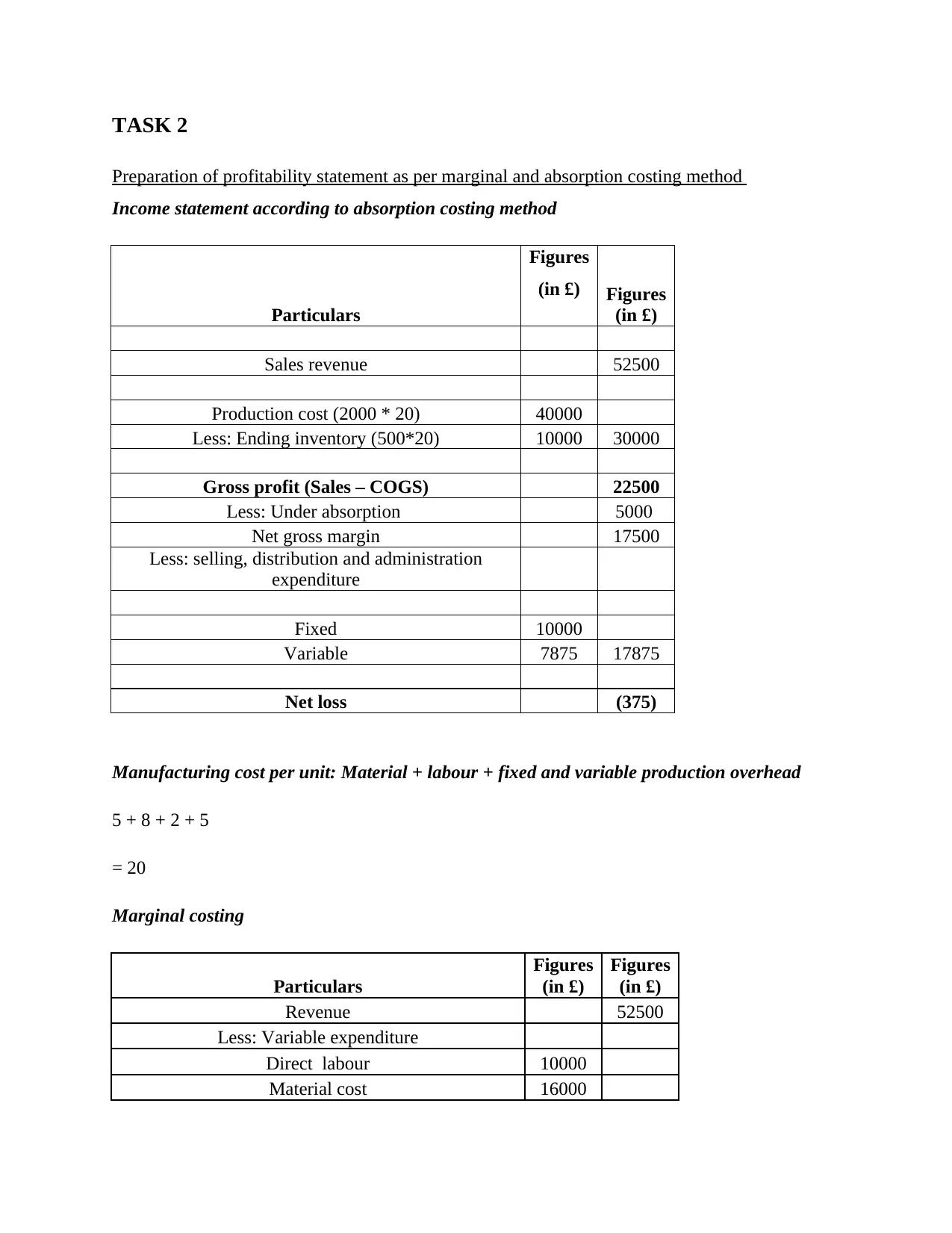

Preparation of profitability statement as per marginal and absorption costing method

Income statement according to absorption costing method

Particulars

Figures

(in £) Figures

(in £)

Sales revenue 52500

Production cost (2000 * 20) 40000

Less: Ending inventory (500*20) 10000 30000

Gross profit (Sales – COGS) 22500

Less: Under absorption 5000

Net gross margin 17500

Less: selling, distribution and administration

expenditure

Fixed 10000

Variable 7875 17875

Net loss (375)

Manufacturing cost per unit: Material + labour + fixed and variable production overhead

5 + 8 + 2 + 5

= 20

Marginal costing

Particulars

Figures

(in £)

Figures

(in £)

Revenue 52500

Less: Variable expenditure

Direct labour 10000

Material cost 16000

Preparation of profitability statement as per marginal and absorption costing method

Income statement according to absorption costing method

Particulars

Figures

(in £) Figures

(in £)

Sales revenue 52500

Production cost (2000 * 20) 40000

Less: Ending inventory (500*20) 10000 30000

Gross profit (Sales – COGS) 22500

Less: Under absorption 5000

Net gross margin 17500

Less: selling, distribution and administration

expenditure

Fixed 10000

Variable 7875 17875

Net loss (375)

Manufacturing cost per unit: Material + labour + fixed and variable production overhead

5 + 8 + 2 + 5

= 20

Marginal costing

Particulars

Figures

(in £)

Figures

(in £)

Revenue 52500

Less: Variable expenditure

Direct labour 10000

Material cost 16000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

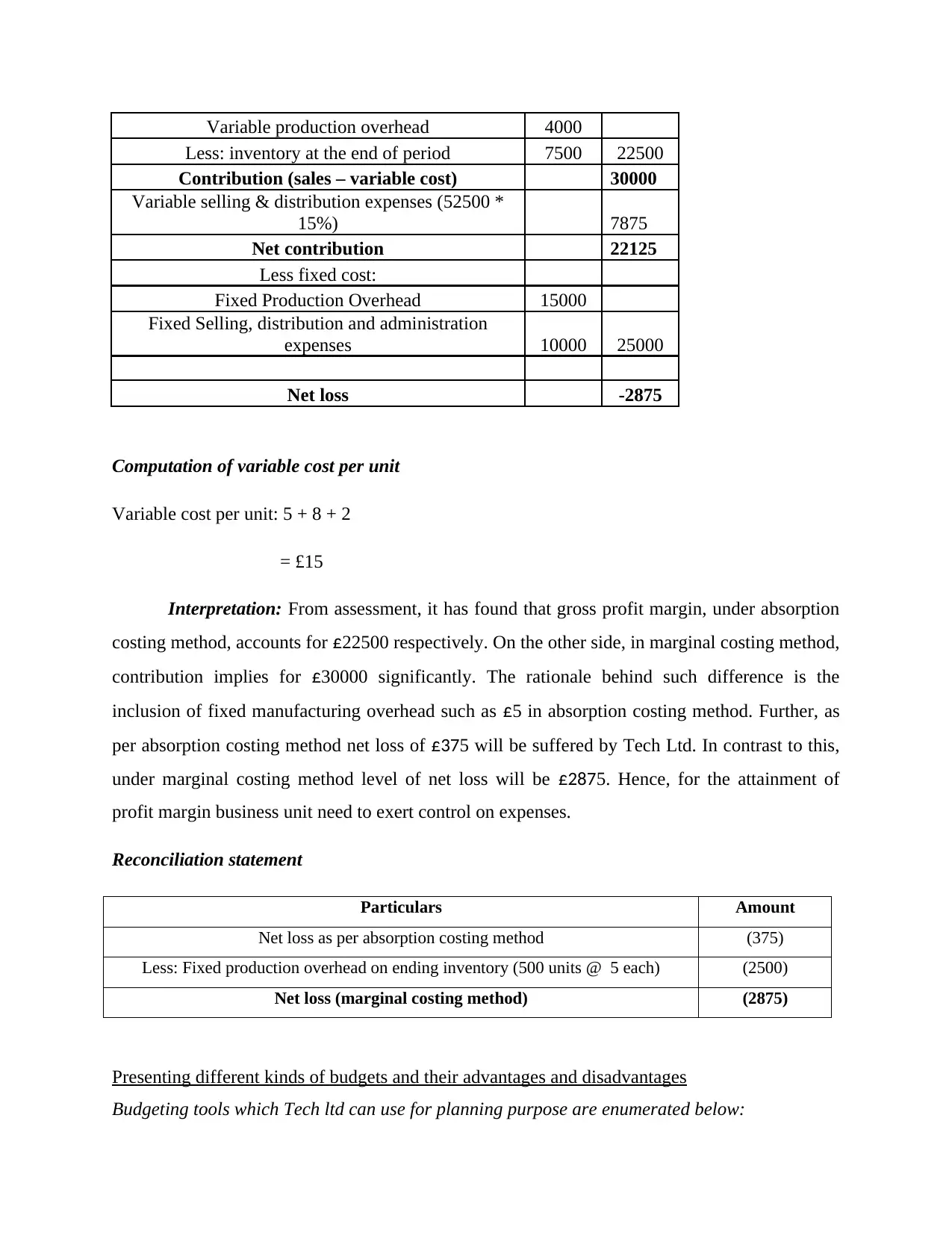

Variable production overhead 4000

Less: inventory at the end of period 7500 22500

Contribution (sales – variable cost) 30000

Variable selling & distribution expenses (52500 *

15%) 7875

Net contribution 22125

Less fixed cost:

Fixed Production Overhead 15000

Fixed Selling, distribution and administration

expenses 10000 25000

Net loss -2875

Computation of variable cost per unit

Variable cost per unit: 5 + 8 + 2

= £15

Interpretation: From assessment, it has found that gross profit margin, under absorption

costing method, accounts for £22500 respectively. On the other side, in marginal costing method,

contribution implies for £30000 significantly. The rationale behind such difference is the

inclusion of fixed manufacturing overhead such as £5 in absorption costing method. Further, as

per absorption costing method net loss of £375 will be suffered by Tech Ltd. In contrast to this,

under marginal costing method level of net loss will be £2875. Hence, for the attainment of

profit margin business unit need to exert control on expenses.

Reconciliation statement

Particulars Amount

Net loss as per absorption costing method (375)

Less: Fixed production overhead on ending inventory (500 units @ 5 each) (2500)

Net loss (marginal costing method) (2875)

Presenting different kinds of budgets and their advantages and disadvantages

Budgeting tools which Tech ltd can use for planning purpose are enumerated below:

Less: inventory at the end of period 7500 22500

Contribution (sales – variable cost) 30000

Variable selling & distribution expenses (52500 *

15%) 7875

Net contribution 22125

Less fixed cost:

Fixed Production Overhead 15000

Fixed Selling, distribution and administration

expenses 10000 25000

Net loss -2875

Computation of variable cost per unit

Variable cost per unit: 5 + 8 + 2

= £15

Interpretation: From assessment, it has found that gross profit margin, under absorption

costing method, accounts for £22500 respectively. On the other side, in marginal costing method,

contribution implies for £30000 significantly. The rationale behind such difference is the

inclusion of fixed manufacturing overhead such as £5 in absorption costing method. Further, as

per absorption costing method net loss of £375 will be suffered by Tech Ltd. In contrast to this,

under marginal costing method level of net loss will be £2875. Hence, for the attainment of

profit margin business unit need to exert control on expenses.

Reconciliation statement

Particulars Amount

Net loss as per absorption costing method (375)

Less: Fixed production overhead on ending inventory (500 units @ 5 each) (2500)

Net loss (marginal costing method) (2875)

Presenting different kinds of budgets and their advantages and disadvantages

Budgeting tools which Tech ltd can use for planning purpose are enumerated below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital expenditure budget: It helps in assessing the amount of cash which business unit

will invest in projects and long-term assets. Hence, it clearly presents time and amount when

fixed assets will be purchased.

Advantages

Facilitates effective cash management

Assists in making plan about fixed assets investment (Capital expenditure budget, 2018)

Disadvantages

Includes more numeric assessments

Time intensive activity

Operational or functional budget: For the purpose of effective financial planning Tech

Ltd can prepare operational or functional budget. As it helps in assessing expected income and

expenses over a particular time period (Operating budget, 2018).

Advantages

Exerts control on undesirable spending

Assists in managing the growth of business

Disadvantages

Time-consuming

Expensive exercise

Cash flow budget: Tech Ltd’s manager can make proper estimation about inflow and

outflow by preparing cash budget. Hence, using cash budget manager can do panning about

further investment projects. Cash budget has following advantages and disadvantages such as:

Advantages

Cash budget helps management in concentrating their attention on significant or

relevant matters

Facilitates co-ordination among the activities of all departments

will invest in projects and long-term assets. Hence, it clearly presents time and amount when

fixed assets will be purchased.

Advantages

Facilitates effective cash management

Assists in making plan about fixed assets investment (Capital expenditure budget, 2018)

Disadvantages

Includes more numeric assessments

Time intensive activity

Operational or functional budget: For the purpose of effective financial planning Tech

Ltd can prepare operational or functional budget. As it helps in assessing expected income and

expenses over a particular time period (Operating budget, 2018).

Advantages

Exerts control on undesirable spending

Assists in managing the growth of business

Disadvantages

Time-consuming

Expensive exercise

Cash flow budget: Tech Ltd’s manager can make proper estimation about inflow and

outflow by preparing cash budget. Hence, using cash budget manager can do panning about

further investment projects. Cash budget has following advantages and disadvantages such as:

Advantages

Cash budget helps management in concentrating their attention on significant or

relevant matters

Facilitates co-ordination among the activities of all departments

Assists in improving communication and developing harmonious relationship among the

personnel

Disadvantages

Cash budget includes subjective estimation

It takes longer time period to achieve the goals

Negatively impacts employee productivity and morale when targets are not realistic in

nature

Master budget: It is the aggregation of all the lower-level budgets produced by the

various functional areas of business organization. Such budgeting framework is the central

planning tool which manager of Tech Ltd can use to direct the activities of business unit.

Advantages

Master budget provides high level of assistance in identifying problems and planning for

the near future.

Provides overall overview of firm’s budget ( Income and expenses of all the

departments)

Disadvantages

Lack of specificity

Difficult to update because master budget includes several financial frameworks such as

production, sales, cash etc.

Describing budget preparation process and costing system that can be used for taking pricing

decisions

Budget preparation process in the context of Tech Ltd is as follows:

First stage of budgeting process includes making estimation about cash inflows and

outflows.

Once estimation has been done thereafter manager submits financial plan to committee

for approval.

personnel

Disadvantages

Cash budget includes subjective estimation

It takes longer time period to achieve the goals

Negatively impacts employee productivity and morale when targets are not realistic in

nature

Master budget: It is the aggregation of all the lower-level budgets produced by the

various functional areas of business organization. Such budgeting framework is the central

planning tool which manager of Tech Ltd can use to direct the activities of business unit.

Advantages

Master budget provides high level of assistance in identifying problems and planning for

the near future.

Provides overall overview of firm’s budget ( Income and expenses of all the

departments)

Disadvantages

Lack of specificity

Difficult to update because master budget includes several financial frameworks such as

production, sales, cash etc.

Describing budget preparation process and costing system that can be used for taking pricing

decisions

Budget preparation process in the context of Tech Ltd is as follows:

First stage of budgeting process includes making estimation about cash inflows and

outflows.

Once estimation has been done thereafter manager submits financial plan to committee

for approval.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.