Management Accounting Report: Analysis of Tech (UK) Limited's Finances

VerifiedAdded on 2024/05/21

|28

|4253

|242

Report

AI Summary

This management accounting report focuses on Tech (UK) Limited, providing a comprehensive analysis of various management accounting principles and their application within the organization. It covers the essential requirements of a management accounting system, including the difference between management and financial accounting, and the use of management accounting as a decision-making tool. The report evaluates the benefits of management accounting systems and their integration within organizational processes. It also includes a detailed cost analysis using marginal and absorption costing techniques to prepare an income statement, discusses different types of budgets and their advantages and disadvantages, and examines the budget preparation process. Furthermore, the report analyzes the use of planning tools for preparing and forecasting budgets and evaluates how management accounting can lead organizations to sustainable success, including a discussion on the balanced scorecard approach. The study is aimed at providing a clear understanding of how effective management accounting practices can contribute to the financial health and strategic decision-making of Tech (UK) Limited.

Management Accounting report for Tech (UK) Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:....................................................................................................................................4

Task 1...............................................................................................................................................5

a) Explanation of management accounting and the essential requirements of management

accounting system........................................................................................................................5

b) Presenting financial information.............................................................................................9

M1 Evaluate the benefits of management accounting systems and their application within an

organizational context................................................................................................................10

D1 critically evaluates how management accounting systems and management accounting

reporting is integrated within organizational processes.............................................................11

Task 2.............................................................................................................................................12

a) Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs..........................................................................................12

M2 accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents:..................................................................................................14

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities:....................................................................................................................................15

Task 3.............................................................................................................................................16

a) Different kinds of budgets and their advantages and disadvantages.....................................16

b) The budget preparation process including determination of pricing and different costing

systems that can be used............................................................................................................19

c) The importance of budget as a tool for planning and control purposes.................................20

Introduction:....................................................................................................................................4

Task 1...............................................................................................................................................5

a) Explanation of management accounting and the essential requirements of management

accounting system........................................................................................................................5

b) Presenting financial information.............................................................................................9

M1 Evaluate the benefits of management accounting systems and their application within an

organizational context................................................................................................................10

D1 critically evaluates how management accounting systems and management accounting

reporting is integrated within organizational processes.............................................................11

Task 2.............................................................................................................................................12

a) Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs..........................................................................................12

M2 accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents:..................................................................................................14

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities:....................................................................................................................................15

Task 3.............................................................................................................................................16

a) Different kinds of budgets and their advantages and disadvantages.....................................16

b) The budget preparation process including determination of pricing and different costing

systems that can be used............................................................................................................19

c) The importance of budget as a tool for planning and control purposes.................................20

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets....................................................................................................................21

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organizations to sustainable success..............................................................22

Task 4.............................................................................................................................................23

a) Balance scorecard approach..................................................................................................23

M4 Analyse how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................24

Conclusion:....................................................................................................................................26

References......................................................................................................................................27

forecasting budgets....................................................................................................................21

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organizations to sustainable success..............................................................22

Task 4.............................................................................................................................................23

a) Balance scorecard approach..................................................................................................23

M4 Analyse how, in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................24

Conclusion:....................................................................................................................................26

References......................................................................................................................................27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction:

Management accounting is the subject of managing all managerial things sophisticatedly in order

to achieve some goals and make arrangements for further targets. This report study will revolve

around management studies and their evaluation related to Tech UK Ltd. to analyse each and

every phase of management accounting and their significance in the decision-making process.

This report will include a brief description of costing techniques in order to understand each

situation and management & financial changes within the management. It will reveal about cost

analysis process budgetary control process via analysing various planking tools as budget. This

report will include an explanation of marginal and absorption costing to monitor business

activities and managerial tasks within the organisation.

Management accounting is the subject of managing all managerial things sophisticatedly in order

to achieve some goals and make arrangements for further targets. This report study will revolve

around management studies and their evaluation related to Tech UK Ltd. to analyse each and

every phase of management accounting and their significance in the decision-making process.

This report will include a brief description of costing techniques in order to understand each

situation and management & financial changes within the management. It will reveal about cost

analysis process budgetary control process via analysing various planking tools as budget. This

report will include an explanation of marginal and absorption costing to monitor business

activities and managerial tasks within the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 1

a) Explanation of management accounting and the essential requirements of management

accounting system.

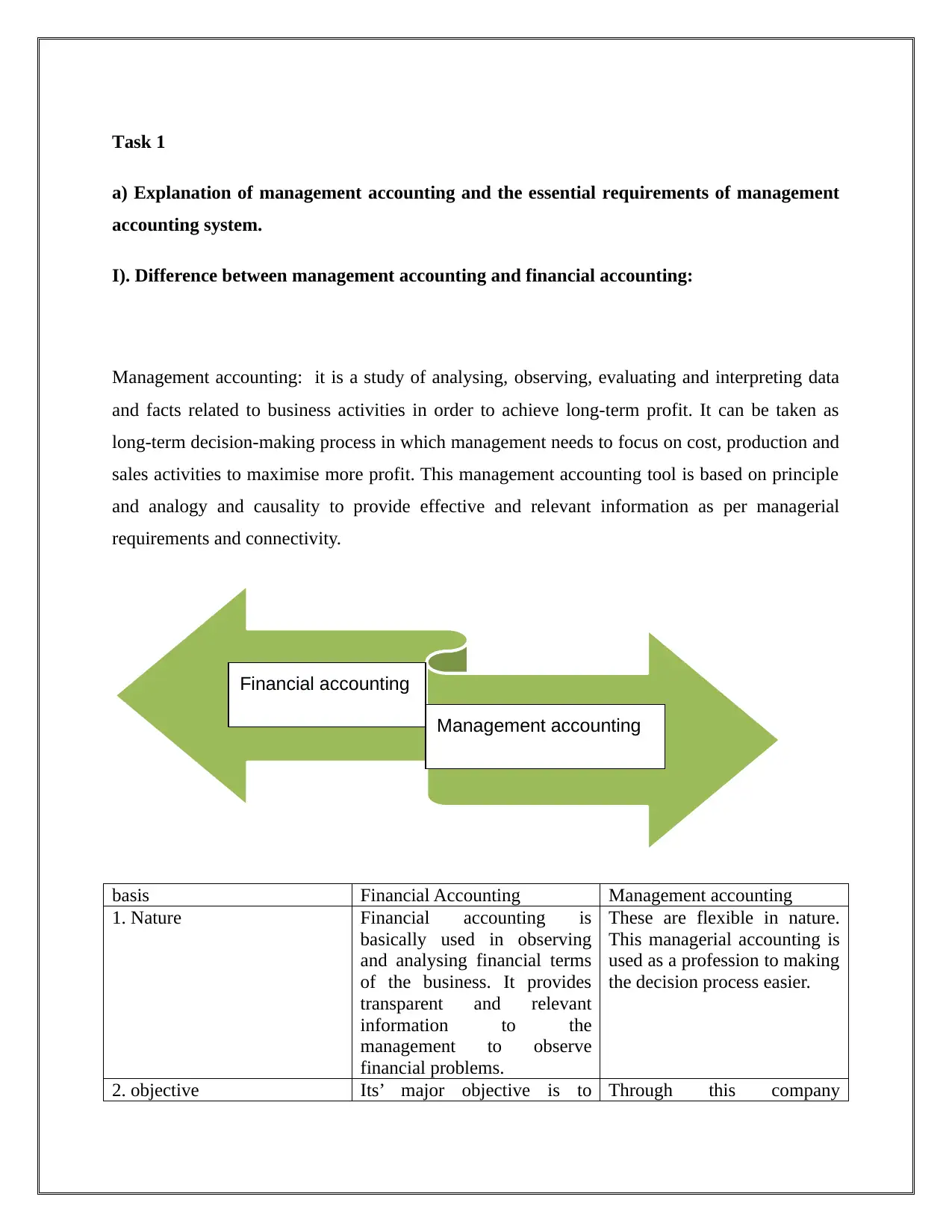

I). Difference between management accounting and financial accounting:

Management accounting: it is a study of analysing, observing, evaluating and interpreting data

and facts related to business activities in order to achieve long-term profit. It can be taken as

long-term decision-making process in which management needs to focus on cost, production and

sales activities to maximise more profit. This management accounting tool is based on principle

and analogy and causality to provide effective and relevant information as per managerial

requirements and connectivity.

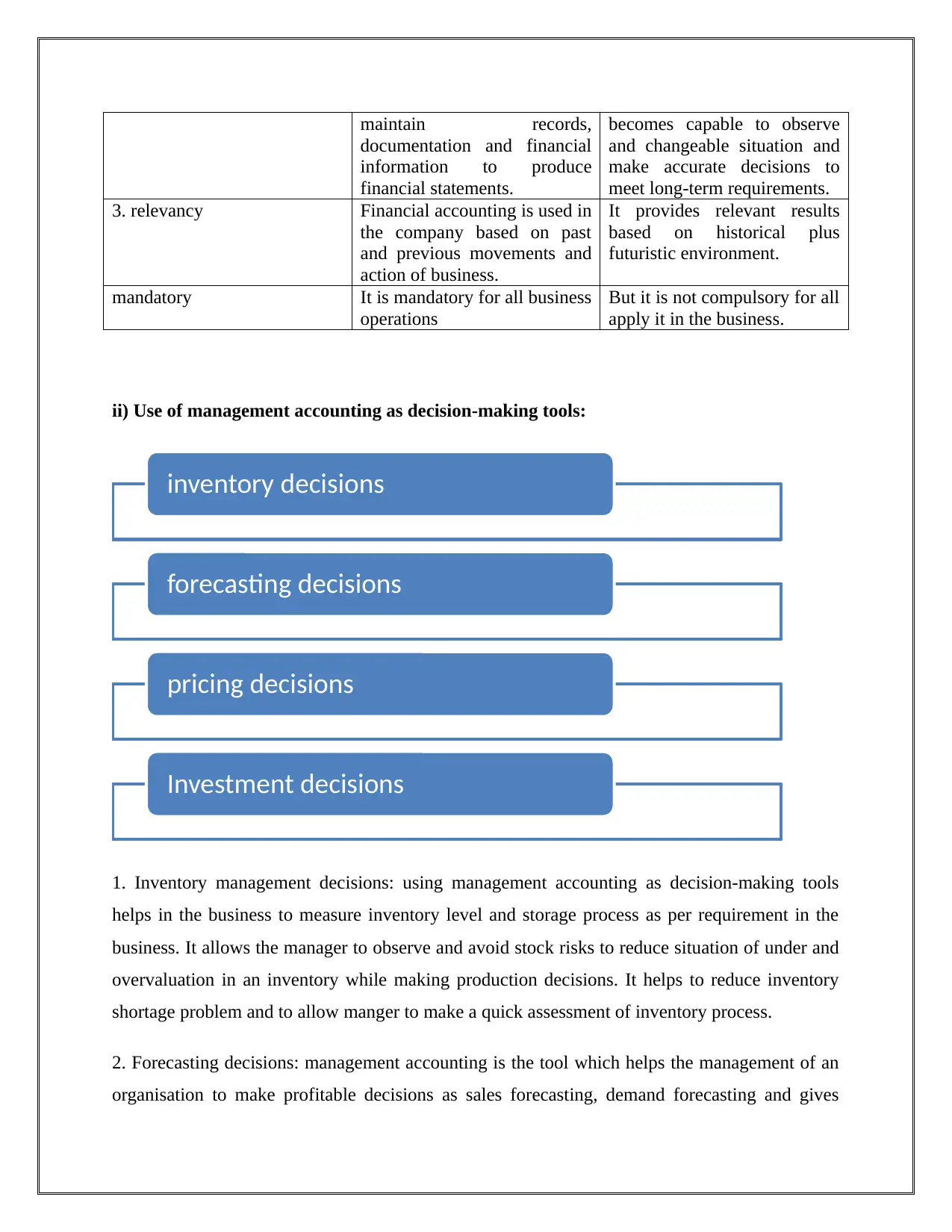

basis Financial Accounting Management accounting

1. Nature Financial accounting is

basically used in observing

and analysing financial terms

of the business. It provides

transparent and relevant

information to the

management to observe

financial problems.

These are flexible in nature.

This managerial accounting is

used as a profession to making

the decision process easier.

2. objective Its’ major objective is to Through this company

Financial accounting

Management accounting

a) Explanation of management accounting and the essential requirements of management

accounting system.

I). Difference between management accounting and financial accounting:

Management accounting: it is a study of analysing, observing, evaluating and interpreting data

and facts related to business activities in order to achieve long-term profit. It can be taken as

long-term decision-making process in which management needs to focus on cost, production and

sales activities to maximise more profit. This management accounting tool is based on principle

and analogy and causality to provide effective and relevant information as per managerial

requirements and connectivity.

basis Financial Accounting Management accounting

1. Nature Financial accounting is

basically used in observing

and analysing financial terms

of the business. It provides

transparent and relevant

information to the

management to observe

financial problems.

These are flexible in nature.

This managerial accounting is

used as a profession to making

the decision process easier.

2. objective Its’ major objective is to Through this company

Financial accounting

Management accounting

maintain records,

documentation and financial

information to produce

financial statements.

becomes capable to observe

and changeable situation and

make accurate decisions to

meet long-term requirements.

3. relevancy Financial accounting is used in

the company based on past

and previous movements and

action of business.

It provides relevant results

based on historical plus

futuristic environment.

mandatory It is mandatory for all business

operations

But it is not compulsory for all

apply it in the business.

ii) Use of management accounting as decision-making tools:

1. Inventory management decisions: using management accounting as decision-making tools

helps in the business to measure inventory level and storage process as per requirement in the

business. It allows the manager to observe and avoid stock risks to reduce situation of under and

overvaluation in an inventory while making production decisions. It helps to reduce inventory

shortage problem and to allow manger to make a quick assessment of inventory process.

2. Forecasting decisions: management accounting is the tool which helps the management of an

organisation to make profitable decisions as sales forecasting, demand forecasting and gives

inventory decisions

forecasting decisions

pricing decisions

Investment decisions

documentation and financial

information to produce

financial statements.

becomes capable to observe

and changeable situation and

make accurate decisions to

meet long-term requirements.

3. relevancy Financial accounting is used in

the company based on past

and previous movements and

action of business.

It provides relevant results

based on historical plus

futuristic environment.

mandatory It is mandatory for all business

operations

But it is not compulsory for all

apply it in the business.

ii) Use of management accounting as decision-making tools:

1. Inventory management decisions: using management accounting as decision-making tools

helps in the business to measure inventory level and storage process as per requirement in the

business. It allows the manager to observe and avoid stock risks to reduce situation of under and

overvaluation in an inventory while making production decisions. It helps to reduce inventory

shortage problem and to allow manger to make a quick assessment of inventory process.

2. Forecasting decisions: management accounting is the tool which helps the management of an

organisation to make profitable decisions as sales forecasting, demand forecasting and gives

inventory decisions

forecasting decisions

pricing decisions

Investment decisions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accurate information about changes in balance sheets, changes in equity and managerial

profitability.

3. Investment decisions: investment decisions are depended on reliability and accuracy of the

financial projections in which company is going to invest. Management accounting helps the

company to make effective investment policies based accounting norms and principles. It creates

a solution by which and where the company could invest to get maximum returns and higher

ROE%.

4. Pricing decisions: management accounting uses various kinds of tools such as cost analysis,

pricing determination activities to help the management to make an effective decision regarding

prices for their products. It helps sales and production department to make an effective analysis

of the market and set the price of their product to make a higher profit.

Types of management accounting systems:

1. Inventory management systems: Inventory management systems are those systems that are

utilised in the management of control inventory storage procedure to understand the production

an inventory level of the company. The company manages their profit as per requirements and

Inventory managment system

Job cost system

Cost managment system

profitability.

3. Investment decisions: investment decisions are depended on reliability and accuracy of the

financial projections in which company is going to invest. Management accounting helps the

company to make effective investment policies based accounting norms and principles. It creates

a solution by which and where the company could invest to get maximum returns and higher

ROE%.

4. Pricing decisions: management accounting uses various kinds of tools such as cost analysis,

pricing determination activities to help the management to make an effective decision regarding

prices for their products. It helps sales and production department to make an effective analysis

of the market and set the price of their product to make a higher profit.

Types of management accounting systems:

1. Inventory management systems: Inventory management systems are those systems that are

utilised in the management of control inventory storage procedure to understand the production

an inventory level of the company. The company manages their profit as per requirements and

Inventory managment system

Job cost system

Cost managment system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production level to analyse the effectiveness of inventory to increase the productivity level and

accuracy to avoid stock risk. This system is utilised to manage and take quick decisions

regarding management in case of under and overvaluation of inventory.

2. Job cost systems: Job cost systems are those systems which are applied in the management in

order possess and regulate each and every cost of job orders by tracing those projects. The

company are allowed to keep tracing their works and jobs in order to maintain the level of cost-

effectiveness and efficiency as per requirements and demand for all projects (Strelnik, et. al.,

2015).

3. Cost management systems: cost management systems are also known as product assessing

systems. These systems provide a platform for the company to regulate and control over their

cost by making effective assessment procedure of each project and product. This system is used

or adopted by the management to measure the cost-effectiveness of each cost such as

administrative, production and selling cost to operate the business properly by managing such

effectively. It is a medium of observing and evaluating sales and revenue related to maximising

profitability.

accuracy to avoid stock risk. This system is utilised to manage and take quick decisions

regarding management in case of under and overvaluation of inventory.

2. Job cost systems: Job cost systems are those systems which are applied in the management in

order possess and regulate each and every cost of job orders by tracing those projects. The

company are allowed to keep tracing their works and jobs in order to maintain the level of cost-

effectiveness and efficiency as per requirements and demand for all projects (Strelnik, et. al.,

2015).

3. Cost management systems: cost management systems are also known as product assessing

systems. These systems provide a platform for the company to regulate and control over their

cost by making effective assessment procedure of each project and product. This system is used

or adopted by the management to measure the cost-effectiveness of each cost such as

administrative, production and selling cost to operate the business properly by managing such

effectively. It is a medium of observing and evaluating sales and revenue related to maximising

profitability.

b) Presenting financial information.

Tech UK uses to prepare various kinds of a report for measuring business performance.

These reports are:

1. Budgets: Budgets are prepared in the company as a major financial report to produce financial

plans, implement them for making improvement in financial performance of the company. It is

basically utilised to enhance the financial performance of the company by measuring expenses,

budgeted cost etc. it provides effective results by making a comparison between estimated and

planned behaviour.

2. Sales report: Sales reports are produced by the company as per sales requirements and market

demands. Tech UK uses to make sales report to analyse sales volume of the company by

measuring the relationship between sales and revenue. Sales report allows the company to

understand changes and increase their sales and productivity by making changes in sales plans

and strategies (Strelnik, et. al., 2015).

3. Performance report: Performance report is produced to measure performance criteria for the

management. These performance records are based on sales, production and other activities and

utilities. This report defines company’s accuracy and liquidity level that how much it is capable

to meet its requirements and obligations.

Tech UK uses to prepare various kinds of a report for measuring business performance.

These reports are:

1. Budgets: Budgets are prepared in the company as a major financial report to produce financial

plans, implement them for making improvement in financial performance of the company. It is

basically utilised to enhance the financial performance of the company by measuring expenses,

budgeted cost etc. it provides effective results by making a comparison between estimated and

planned behaviour.

2. Sales report: Sales reports are produced by the company as per sales requirements and market

demands. Tech UK uses to make sales report to analyse sales volume of the company by

measuring the relationship between sales and revenue. Sales report allows the company to

understand changes and increase their sales and productivity by making changes in sales plans

and strategies (Strelnik, et. al., 2015).

3. Performance report: Performance report is produced to measure performance criteria for the

management. These performance records are based on sales, production and other activities and

utilities. This report defines company’s accuracy and liquidity level that how much it is capable

to meet its requirements and obligations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1 Evaluate the benefits of management accounting systems and their application within

an organizational context.

Management accounting is taken as a study of management activities based on business

management and operation criteria. It is used as a decision-making tool to analyse needs of

accurate information, data to provide it to the company at the time of making decisions such as

cost analysis, forecasting decision etc. UK Tech company can be utilised make cost-effective and

productive decision by using management accounting systems and prepare accounting report for

managing flexibility. Application of such systems in the Tech UK Ltd will provide accurate and

flexible information and allow the company to deal with future changes and obstacles.

an organizational context.

Management accounting is taken as a study of management activities based on business

management and operation criteria. It is used as a decision-making tool to analyse needs of

accurate information, data to provide it to the company at the time of making decisions such as

cost analysis, forecasting decision etc. UK Tech company can be utilised make cost-effective and

productive decision by using management accounting systems and prepare accounting report for

managing flexibility. Application of such systems in the Tech UK Ltd will provide accurate and

flexible information and allow the company to deal with future changes and obstacles.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1 critically evaluates how management accounting systems and management accounting

reporting is integrated within organizational processes.

Management accounting systems and preparation of management reports are interrelated to

management work and organisational process in order to manage whole work and make proper

management strategies to get relevant results. Management accounting systems are effectively

used and adopted by the company to convert managerial plans into reality. It allows the

management to measure and track organisational tasks and works by analysing cost, maintain

budget and accounts to reduce disorders and run business in a stable manner with competitive

strategies. Management reports help to trace and keeping records of all activities in an efficient

manner to make productive results and decisions by observing the financial health of the

company (Lavia López and Hiebl, 2014).

reporting is integrated within organizational processes.

Management accounting systems and preparation of management reports are interrelated to

management work and organisational process in order to manage whole work and make proper

management strategies to get relevant results. Management accounting systems are effectively

used and adopted by the company to convert managerial plans into reality. It allows the

management to measure and track organisational tasks and works by analysing cost, maintain

budget and accounts to reduce disorders and run business in a stable manner with competitive

strategies. Management reports help to trace and keeping records of all activities in an efficient

manner to make productive results and decisions by observing the financial health of the

company (Lavia López and Hiebl, 2014).

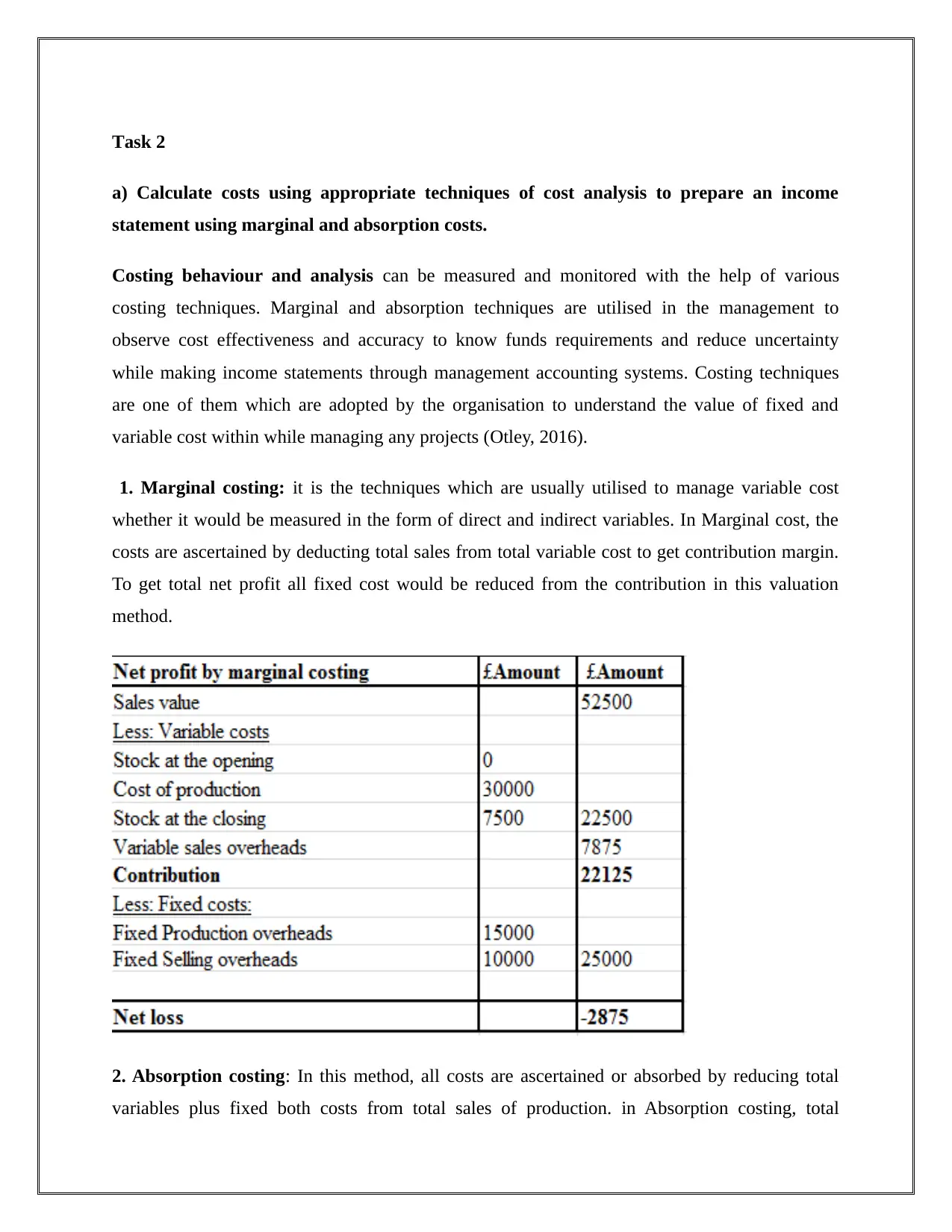

Task 2

a) Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Costing behaviour and analysis can be measured and monitored with the help of various

costing techniques. Marginal and absorption techniques are utilised in the management to

observe cost effectiveness and accuracy to know funds requirements and reduce uncertainty

while making income statements through management accounting systems. Costing techniques

are one of them which are adopted by the organisation to understand the value of fixed and

variable cost within while managing any projects (Otley, 2016).

1. Marginal costing: it is the techniques which are usually utilised to manage variable cost

whether it would be measured in the form of direct and indirect variables. In Marginal cost, the

costs are ascertained by deducting total sales from total variable cost to get contribution margin.

To get total net profit all fixed cost would be reduced from the contribution in this valuation

method.

2. Absorption costing: In this method, all costs are ascertained or absorbed by reducing total

variables plus fixed both costs from total sales of production. in Absorption costing, total

a) Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

Costing behaviour and analysis can be measured and monitored with the help of various

costing techniques. Marginal and absorption techniques are utilised in the management to

observe cost effectiveness and accuracy to know funds requirements and reduce uncertainty

while making income statements through management accounting systems. Costing techniques

are one of them which are adopted by the organisation to understand the value of fixed and

variable cost within while managing any projects (Otley, 2016).

1. Marginal costing: it is the techniques which are usually utilised to manage variable cost

whether it would be measured in the form of direct and indirect variables. In Marginal cost, the

costs are ascertained by deducting total sales from total variable cost to get contribution margin.

To get total net profit all fixed cost would be reduced from the contribution in this valuation

method.

2. Absorption costing: In this method, all costs are ascertained or absorbed by reducing total

variables plus fixed both costs from total sales of production. in Absorption costing, total

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.