Detailed Report on Management Accounting for Tech (UK) Limited

VerifiedAdded on 2024/05/31

|23

|5759

|427

Report

AI Summary

This report provides a comprehensive analysis of management accounting techniques within the context of Tech (UK) Limited, a manufacturer of mobile chargers and gadgets. It differentiates between management and financial accounting, highlighting the importance of management accounting in business decision-making. The report explores cost accounting systems, inventory management, and job costing, alongside various management accounting reports like budgets, sales reports, production reports, and variance analysis. It further examines absorption and marginal costing methods, providing calculations and income statements for Tech (UK) Limited. The document also discusses budgeting processes, pricing strategies, and the role of budgets in planning and control, concluding with an explanation of the Balanced Scorecard approach and its implementation for performance measurement. Desklib provides access to this and many other solved assignments for students.

MANAGEMENT ACCOUNTING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of content

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

I. Difference between management and financial accounting.........................................................3

II. Importance of management accounting in making business decision........................................4

III. Cost accounting system.............................................................................................................5

IV. Inventory management system..................................................................................................5

V. Job costing system......................................................................................................................5

B. Presentation of financial information..........................................................................................6

I. Various types of management accounting reports.......................................................................6

II. Why presenting management accounting information in an understandable manner is

important..........................................................................................................................................7

Task 2...............................................................................................................................................7

I. Absorption costing.......................................................................................................................7

II. Marginal costing.........................................................................................................................8

Task 3.............................................................................................................................................10

a. Different categories of budget along with their advantages and disadvantages........................10

b. Process or steps involved in budget preparation and determination of pricing and different

costing systems..............................................................................................................................12

C. Importance of budget as a tool for planning and controlling....................................................13

Task 4.............................................................................................................................................16

A) Explain what a Balance Score Card approach is and describe how the implementation of a

balanced score card can deliver a range of performance measures (financial and non-financial)16

Conclusion.....................................................................................................................................19

Reference list.................................................................................................................................20

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

I. Difference between management and financial accounting.........................................................3

II. Importance of management accounting in making business decision........................................4

III. Cost accounting system.............................................................................................................5

IV. Inventory management system..................................................................................................5

V. Job costing system......................................................................................................................5

B. Presentation of financial information..........................................................................................6

I. Various types of management accounting reports.......................................................................6

II. Why presenting management accounting information in an understandable manner is

important..........................................................................................................................................7

Task 2...............................................................................................................................................7

I. Absorption costing.......................................................................................................................7

II. Marginal costing.........................................................................................................................8

Task 3.............................................................................................................................................10

a. Different categories of budget along with their advantages and disadvantages........................10

b. Process or steps involved in budget preparation and determination of pricing and different

costing systems..............................................................................................................................12

C. Importance of budget as a tool for planning and controlling....................................................13

Task 4.............................................................................................................................................16

A) Explain what a Balance Score Card approach is and describe how the implementation of a

balanced score card can deliver a range of performance measures (financial and non-financial)16

Conclusion.....................................................................................................................................19

Reference list.................................................................................................................................20

2

Introduction

Nowadays, in the complicated business environment, management accounting is the backbone of

the organization. It is a very simple system, but it takes care of several activities of business. The

procedure under management accounting is very suitable for the complicated business

environment. It makes the overall business activities simpler by applying different suitable

techniques. In this study, the importance and application of management accounting techniques

will be shown in the business context of Tech (UK) Limited, which manufactures special mobile

charger and other carry-on-gadgets for the retailers. Here, focus will be made on different

systems and techniques used by the organizations under the management accounting system.

Task 1

To

Director of Finance

Tech (UK) Limited

Date: ____________________

Subject: Regarding the importance of management accounting

I. Difference between management and financial accounting

In the introductory part, management accounting has been considered as a simple procedure that

makes operational activities simpler. Sometimes, people cannot differentiate management

accounting from the financial accounting system (Hansen, 2011). However, in practical, there are

several differences that exist between these two parts of organizational systems. The differences

have been noted below:

Management accounting Financial accounting

Management accounting is a broader part of

organization that deals with non-financial as

well as financial activities or transactions

Financial accounting is comparatively smaller

part of the organization that deals only with the

financial activities or transactions.

3

Nowadays, in the complicated business environment, management accounting is the backbone of

the organization. It is a very simple system, but it takes care of several activities of business. The

procedure under management accounting is very suitable for the complicated business

environment. It makes the overall business activities simpler by applying different suitable

techniques. In this study, the importance and application of management accounting techniques

will be shown in the business context of Tech (UK) Limited, which manufactures special mobile

charger and other carry-on-gadgets for the retailers. Here, focus will be made on different

systems and techniques used by the organizations under the management accounting system.

Task 1

To

Director of Finance

Tech (UK) Limited

Date: ____________________

Subject: Regarding the importance of management accounting

I. Difference between management and financial accounting

In the introductory part, management accounting has been considered as a simple procedure that

makes operational activities simpler. Sometimes, people cannot differentiate management

accounting from the financial accounting system (Hansen, 2011). However, in practical, there are

several differences that exist between these two parts of organizational systems. The differences

have been noted below:

Management accounting Financial accounting

Management accounting is a broader part of

organization that deals with non-financial as

well as financial activities or transactions

Financial accounting is comparatively smaller

part of the organization that deals only with the

financial activities or transactions.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Hittet al., 2012).

Management accounting prepares the reports

for internal use of the business

Financial accounting prepares reports for the

internal as well as external uses of the

business.

Management accounting does not follow any

specific rules or structure. It is much flexible in

nature.

Financial accounting follows some specific

rules and structure and it is conservative in

nature (Indounas, 2016).

Management accounting is not mandatory for

the business, but it is importance for the

company

Financial accounting is mandatory as well as

important for the business.

II. Importance of management accounting in making business decision

The previous discussion is indicating that management accounting differs from financial

accounting. At the same time, it has also been noticed that management accounting is much

broader than financial accounting. In the business context of Tech (UK) Limited, it can be stated

that the management can develop better decisions following management accounting system.

Under management accounting, the personnel in Tech (UK) Limited get the chance to perform

critical analysis on different activities of the firm. For instance, while developing plans for

business improvement, respective personnel in Tech (UK) Limited can analyze the performance

from different aspects like, cost, income, inventory, resource base and environmental. These

analyses make decision-making procedure concrete (Kaplan and Atkinson, 2015). The higher

authority of Tech (UK) Limited can avoid several risks using the system of management

accounting, which enhances quality of organizational decisions. At the same time, it also

improves or increase possibilities of business success in the particular accounting year. These

analyses help the personnel understanding the gaps in company’s performance, which influences

in making better controlling decisions (Nyaga and Muema, 2017). Higher authority can guide the

junior employees regarding use of resources, improvement in performance quality and many

other areas. Decision regarding resource allocation becomes also easier under this system of

business.

4

Management accounting prepares the reports

for internal use of the business

Financial accounting prepares reports for the

internal as well as external uses of the

business.

Management accounting does not follow any

specific rules or structure. It is much flexible in

nature.

Financial accounting follows some specific

rules and structure and it is conservative in

nature (Indounas, 2016).

Management accounting is not mandatory for

the business, but it is importance for the

company

Financial accounting is mandatory as well as

important for the business.

II. Importance of management accounting in making business decision

The previous discussion is indicating that management accounting differs from financial

accounting. At the same time, it has also been noticed that management accounting is much

broader than financial accounting. In the business context of Tech (UK) Limited, it can be stated

that the management can develop better decisions following management accounting system.

Under management accounting, the personnel in Tech (UK) Limited get the chance to perform

critical analysis on different activities of the firm. For instance, while developing plans for

business improvement, respective personnel in Tech (UK) Limited can analyze the performance

from different aspects like, cost, income, inventory, resource base and environmental. These

analyses make decision-making procedure concrete (Kaplan and Atkinson, 2015). The higher

authority of Tech (UK) Limited can avoid several risks using the system of management

accounting, which enhances quality of organizational decisions. At the same time, it also

improves or increase possibilities of business success in the particular accounting year. These

analyses help the personnel understanding the gaps in company’s performance, which influences

in making better controlling decisions (Nyaga and Muema, 2017). Higher authority can guide the

junior employees regarding use of resources, improvement in performance quality and many

other areas. Decision regarding resource allocation becomes also easier under this system of

business.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

III. Cost accounting system

Cost accounting is a part of management accounting that is required to be followed for better

management of operational and other costs of the business. Cost accounting is nothing but

developing better strategies for cost reduction after analyzing the current cost structure (Otley

and Emmanuel, 2013). Cost accounting system can be followed by adopting any of the available

costing techniques like, actual costing, normal costing and standard costing. Actual costing and

normal costing are almost same, in which total cost is derived by summing up the actual costs for

materials, labor and overheads. On the other hand, if the higher authority of Tech (UK) Limited

decides to follow the standard costing method, they need to set the standard costs for each

activity of the business. At the end of the financial year, management will review the actual

performance on the basis of the previously set standard(Perkinset al., 2014). Gaps between the

two performances are known as variance. Adopting any of the costing method, company can

reduce its level of costs very effectively.

IV. Inventory management system

Inventory management system is followed to maintain standard level of stock in company’s

warehouse, so that proper flow of sales can be maintained. Inventory management aims to

control flow of inventory in the business (Reason, 2016). For managing inventory at the required

level, the company may follow a particular technique of inventory management. The available

alternatives for inventory management are – FIFO, LIFO and AVCO methods. Each method is

different from the other methods. Among the three available inventory management methods,

AVCO method is critical than the other two methods. FIFO and LIFO methods are just opposite

to each other. In the FIFO method, the stock or inventory that comes first in the storage is sold

out at first (Salako and Yusuf, 2016). On the other hand, in the case of LIFO method, the stock

or inventory that comes last in the storage is sold out at first.

V. Job costing system

Job costing is another method of costing that can be followed in the business context of Tech

(UK) Limited. Job costing is followed in the business, where companies need to produce in bulk

(Alviniussen and Jankensgard, 2015). Following the system of job costing, Tech (UK) Limited’s

personnel can divide overall production process in to small jobs, so that handling overall

5

Cost accounting is a part of management accounting that is required to be followed for better

management of operational and other costs of the business. Cost accounting is nothing but

developing better strategies for cost reduction after analyzing the current cost structure (Otley

and Emmanuel, 2013). Cost accounting system can be followed by adopting any of the available

costing techniques like, actual costing, normal costing and standard costing. Actual costing and

normal costing are almost same, in which total cost is derived by summing up the actual costs for

materials, labor and overheads. On the other hand, if the higher authority of Tech (UK) Limited

decides to follow the standard costing method, they need to set the standard costs for each

activity of the business. At the end of the financial year, management will review the actual

performance on the basis of the previously set standard(Perkinset al., 2014). Gaps between the

two performances are known as variance. Adopting any of the costing method, company can

reduce its level of costs very effectively.

IV. Inventory management system

Inventory management system is followed to maintain standard level of stock in company’s

warehouse, so that proper flow of sales can be maintained. Inventory management aims to

control flow of inventory in the business (Reason, 2016). For managing inventory at the required

level, the company may follow a particular technique of inventory management. The available

alternatives for inventory management are – FIFO, LIFO and AVCO methods. Each method is

different from the other methods. Among the three available inventory management methods,

AVCO method is critical than the other two methods. FIFO and LIFO methods are just opposite

to each other. In the FIFO method, the stock or inventory that comes first in the storage is sold

out at first (Salako and Yusuf, 2016). On the other hand, in the case of LIFO method, the stock

or inventory that comes last in the storage is sold out at first.

V. Job costing system

Job costing is another method of costing that can be followed in the business context of Tech

(UK) Limited. Job costing is followed in the business, where companies need to produce in bulk

(Alviniussen and Jankensgard, 2015). Following the system of job costing, Tech (UK) Limited’s

personnel can divide overall production process in to small jobs, so that handling overall

5

production process becomes easier. In this context, it must be noted that job costing helps in

reducing cost level of the firm by eliminating unnecessary costs (Aminbakhsh et al., 2015).

B. Presentation of financial information

I. Various types of management accounting reports

Management accounting controls overall activities of the firm by using different reports. Reports

are prepared for each activity or department. For example, if the case study of Tech (UK)

Limited is considered, it is noticeable that as a manufacturing firm, the business includes several

departments and under management accounting, every department needs to prepare separate

reports. Various types of reports under management accounting system are stated below:

Budgets – Budgets can be considered as the most important management accounting report that

shows plans for the business in the coming years. This report is not only important for systematic

operations of the business, but it is also important for proper allocation of resources

(Belleflamme and Peitz, 2015). Budgets are prepared by analyzing the past and present

performance of the business critically. Along with that analyzing the current resource base of the

business is very important.

Sales report – This report focuses on the value and volume of sales in an organization. It means

the report deals with the sales department of the company. In the sales report, the detailed

information regarding the revenue and direct and indirect costs of the business is available (Binti,

2016). Preparing sales report, the higher authority can easily understand changes in revenue level

of the business.

Production report – Like sales report, production report is prepared including all details of

production of the firm. The production report includes detailed information related to the total

raw materials, labor and overhead costs that have been involved in the production process

(Warrenet al., 2015). The quantity of resources that are used in the production is also included in

the production report of the business.

Inventory report – This is another report that higher authority and the departments at Tech (UK)

Limited are needed to be prepared by considering detailed information regarding the inventory

6

reducing cost level of the firm by eliminating unnecessary costs (Aminbakhsh et al., 2015).

B. Presentation of financial information

I. Various types of management accounting reports

Management accounting controls overall activities of the firm by using different reports. Reports

are prepared for each activity or department. For example, if the case study of Tech (UK)

Limited is considered, it is noticeable that as a manufacturing firm, the business includes several

departments and under management accounting, every department needs to prepare separate

reports. Various types of reports under management accounting system are stated below:

Budgets – Budgets can be considered as the most important management accounting report that

shows plans for the business in the coming years. This report is not only important for systematic

operations of the business, but it is also important for proper allocation of resources

(Belleflamme and Peitz, 2015). Budgets are prepared by analyzing the past and present

performance of the business critically. Along with that analyzing the current resource base of the

business is very important.

Sales report – This report focuses on the value and volume of sales in an organization. It means

the report deals with the sales department of the company. In the sales report, the detailed

information regarding the revenue and direct and indirect costs of the business is available (Binti,

2016). Preparing sales report, the higher authority can easily understand changes in revenue level

of the business.

Production report – Like sales report, production report is prepared including all details of

production of the firm. The production report includes detailed information related to the total

raw materials, labor and overhead costs that have been involved in the production process

(Warrenet al., 2015). The quantity of resources that are used in the production is also included in

the production report of the business.

Inventory report – This is another report that higher authority and the departments at Tech (UK)

Limited are needed to be prepared by considering detailed information regarding the inventory

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

level of business (Weldonet al., 2016).Considering the inventory report, management at Tech

(UK) Limited can decide whether they should control inventory flow in the business or they

should continue with the current system.

Variance analysis report – This report is needed to be prepared so that the gaps in current

performance standard of the business can be identified. This report is prepared after comparing

the actual performance with the standard performance of the business (Weygandtet al., 2015).

Therefore, from the above discussion, it can be stated that the management accounting prepares

the report that are highly useful to the managers or higher authority of Tech (UK) Limited.

Hence, they must focus on proper presentation of the reports.

II. Why presenting management accounting information in an understandable manner is

important

From the previous discussion, it is very clear that management accounting activities generate

various or different information that is useful to the business.However, in this regard, it is

important to mention that the information must be presented in such a manner that is

understandable to every personnel in the higher organizational positions. It is because the

personnel in the top organizational positions makes final decision or strategies for the business,

which are developed based on management accounting information (Yilmaz and Ceran, 2017).

Now, if the information is present in critical manner and management cannot understand the

same, decisions will be imperfect, which will ultimately affect performance standard of the

business. At the same time, if the information is not present in an understandable manner, the

higher authority will also not get clear view of the current performance.

Task 2

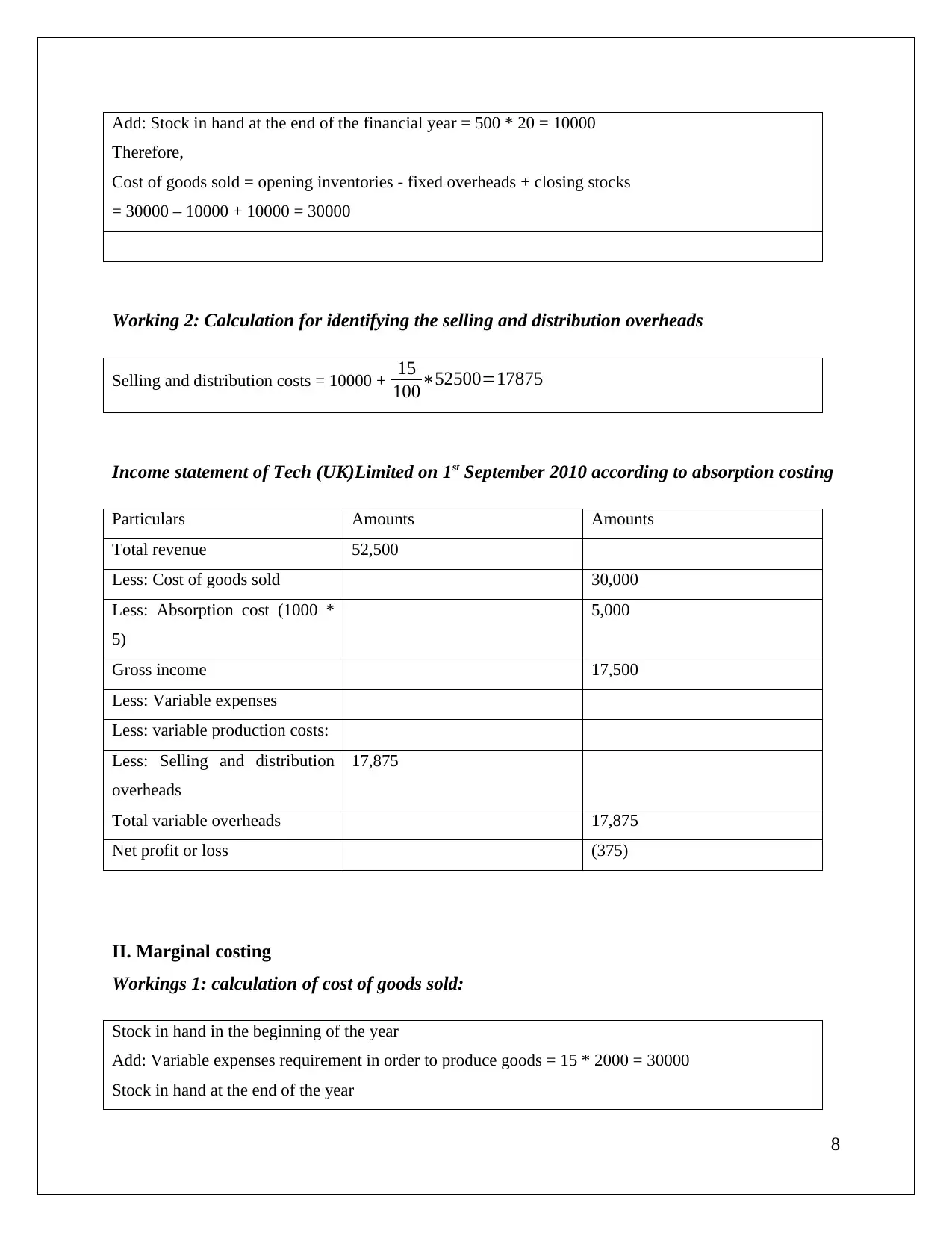

I. Absorption costing

Working 1: Calculation for identifying the cost of goods sold (COGS)

Stock in hand at the beginning of the financial year = 2000 * 15 = 30000

Less: Fixed or staticcosts = 2000 * 5 = 10000

7

(UK) Limited can decide whether they should control inventory flow in the business or they

should continue with the current system.

Variance analysis report – This report is needed to be prepared so that the gaps in current

performance standard of the business can be identified. This report is prepared after comparing

the actual performance with the standard performance of the business (Weygandtet al., 2015).

Therefore, from the above discussion, it can be stated that the management accounting prepares

the report that are highly useful to the managers or higher authority of Tech (UK) Limited.

Hence, they must focus on proper presentation of the reports.

II. Why presenting management accounting information in an understandable manner is

important

From the previous discussion, it is very clear that management accounting activities generate

various or different information that is useful to the business.However, in this regard, it is

important to mention that the information must be presented in such a manner that is

understandable to every personnel in the higher organizational positions. It is because the

personnel in the top organizational positions makes final decision or strategies for the business,

which are developed based on management accounting information (Yilmaz and Ceran, 2017).

Now, if the information is present in critical manner and management cannot understand the

same, decisions will be imperfect, which will ultimately affect performance standard of the

business. At the same time, if the information is not present in an understandable manner, the

higher authority will also not get clear view of the current performance.

Task 2

I. Absorption costing

Working 1: Calculation for identifying the cost of goods sold (COGS)

Stock in hand at the beginning of the financial year = 2000 * 15 = 30000

Less: Fixed or staticcosts = 2000 * 5 = 10000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Add: Stock in hand at the end of the financial year = 500 * 20 = 10000

Therefore,

Cost of goods sold = opening inventories - fixed overheads + closing stocks

= 30000 – 10000 + 10000 = 30000

Working 2: Calculation for identifying the selling and distribution overheads

Selling and distribution costs = 10000 + 15

100∗52500=17875

Income statement of Tech (UK)Limited on 1st September 2010 according to absorption costing

Particulars Amounts Amounts

Total revenue 52,500

Less: Cost of goods sold 30,000

Less: Absorption cost (1000 *

5)

5,000

Gross income 17,500

Less: Variable expenses

Less: variable production costs:

Less: Selling and distribution

overheads

17,875

Total variable overheads 17,875

Net profit or loss (375)

II. Marginal costing

Workings 1: calculation of cost of goods sold:

Stock in hand in the beginning of the year

Add: Variable expenses requirement in order to produce goods = 15 * 2000 = 30000

Stock in hand at the end of the year

8

Therefore,

Cost of goods sold = opening inventories - fixed overheads + closing stocks

= 30000 – 10000 + 10000 = 30000

Working 2: Calculation for identifying the selling and distribution overheads

Selling and distribution costs = 10000 + 15

100∗52500=17875

Income statement of Tech (UK)Limited on 1st September 2010 according to absorption costing

Particulars Amounts Amounts

Total revenue 52,500

Less: Cost of goods sold 30,000

Less: Absorption cost (1000 *

5)

5,000

Gross income 17,500

Less: Variable expenses

Less: variable production costs:

Less: Selling and distribution

overheads

17,875

Total variable overheads 17,875

Net profit or loss (375)

II. Marginal costing

Workings 1: calculation of cost of goods sold:

Stock in hand in the beginning of the year

Add: Variable expenses requirement in order to produce goods = 15 * 2000 = 30000

Stock in hand at the end of the year

8

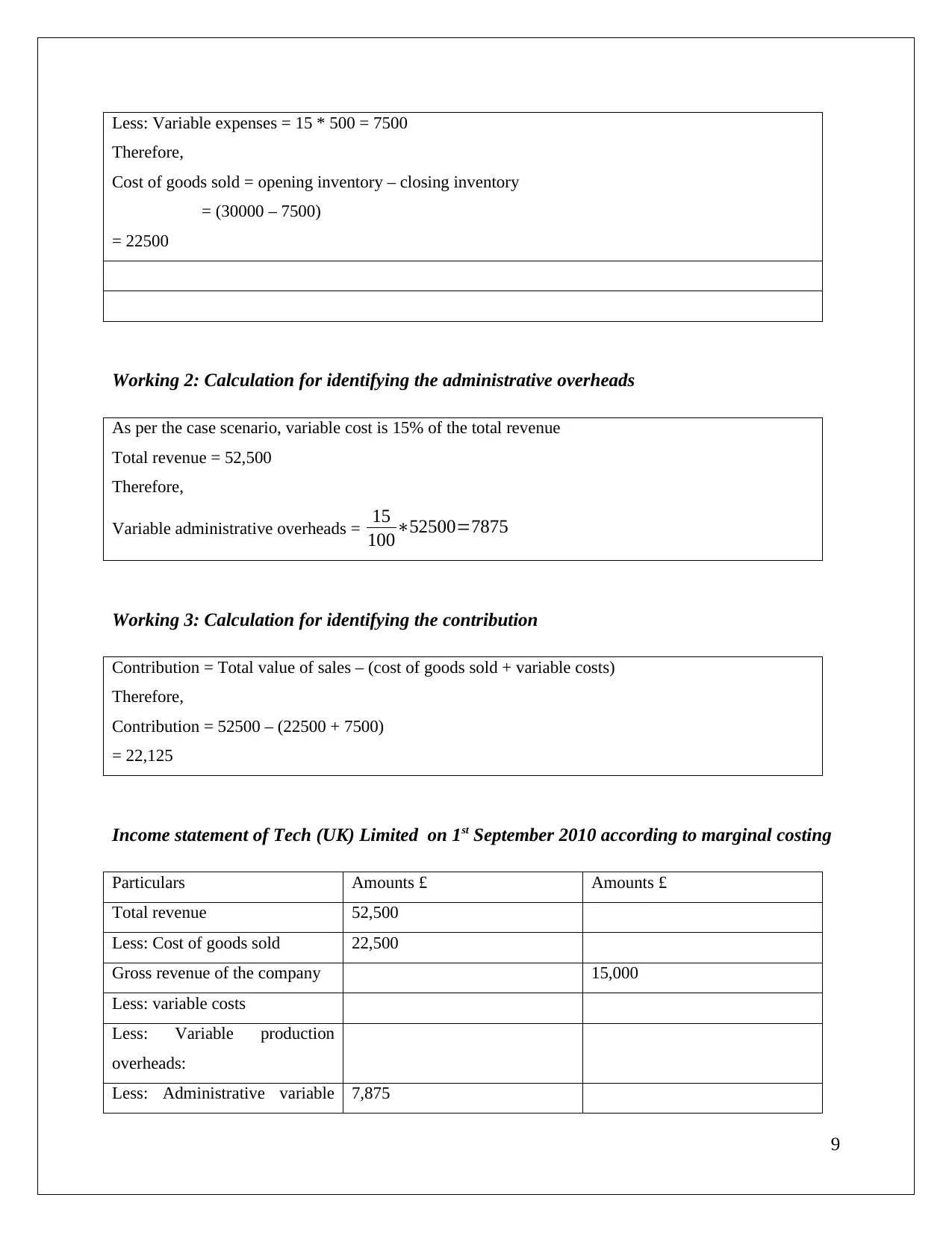

Less: Variable expenses = 15 * 500 = 7500

Therefore,

Cost of goods sold = opening inventory – closing inventory

= (30000 – 7500)

= 22500

Working 2: Calculation for identifying the administrative overheads

As per the case scenario, variable cost is 15% of the total revenue

Total revenue = 52,500

Therefore,

Variable administrative overheads = 15

100∗52500=7875

Working 3: Calculation for identifying the contribution

Contribution = Total value of sales – (cost of goods sold + variable costs)

Therefore,

Contribution = 52500 – (22500 + 7500)

= 22,125

Income statement of Tech (UK) Limited on 1st September 2010 according to marginal costing

Particulars Amounts £ Amounts £

Total revenue 52,500

Less: Cost of goods sold 22,500

Gross revenue of the company 15,000

Less: variable costs

Less: Variable production

overheads:

Less: Administrative variable 7,875

9

Therefore,

Cost of goods sold = opening inventory – closing inventory

= (30000 – 7500)

= 22500

Working 2: Calculation for identifying the administrative overheads

As per the case scenario, variable cost is 15% of the total revenue

Total revenue = 52,500

Therefore,

Variable administrative overheads = 15

100∗52500=7875

Working 3: Calculation for identifying the contribution

Contribution = Total value of sales – (cost of goods sold + variable costs)

Therefore,

Contribution = 52500 – (22500 + 7500)

= 22,125

Income statement of Tech (UK) Limited on 1st September 2010 according to marginal costing

Particulars Amounts £ Amounts £

Total revenue 52,500

Less: Cost of goods sold 22,500

Gross revenue of the company 15,000

Less: variable costs

Less: Variable production

overheads:

Less: Administrative variable 7,875

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overheads

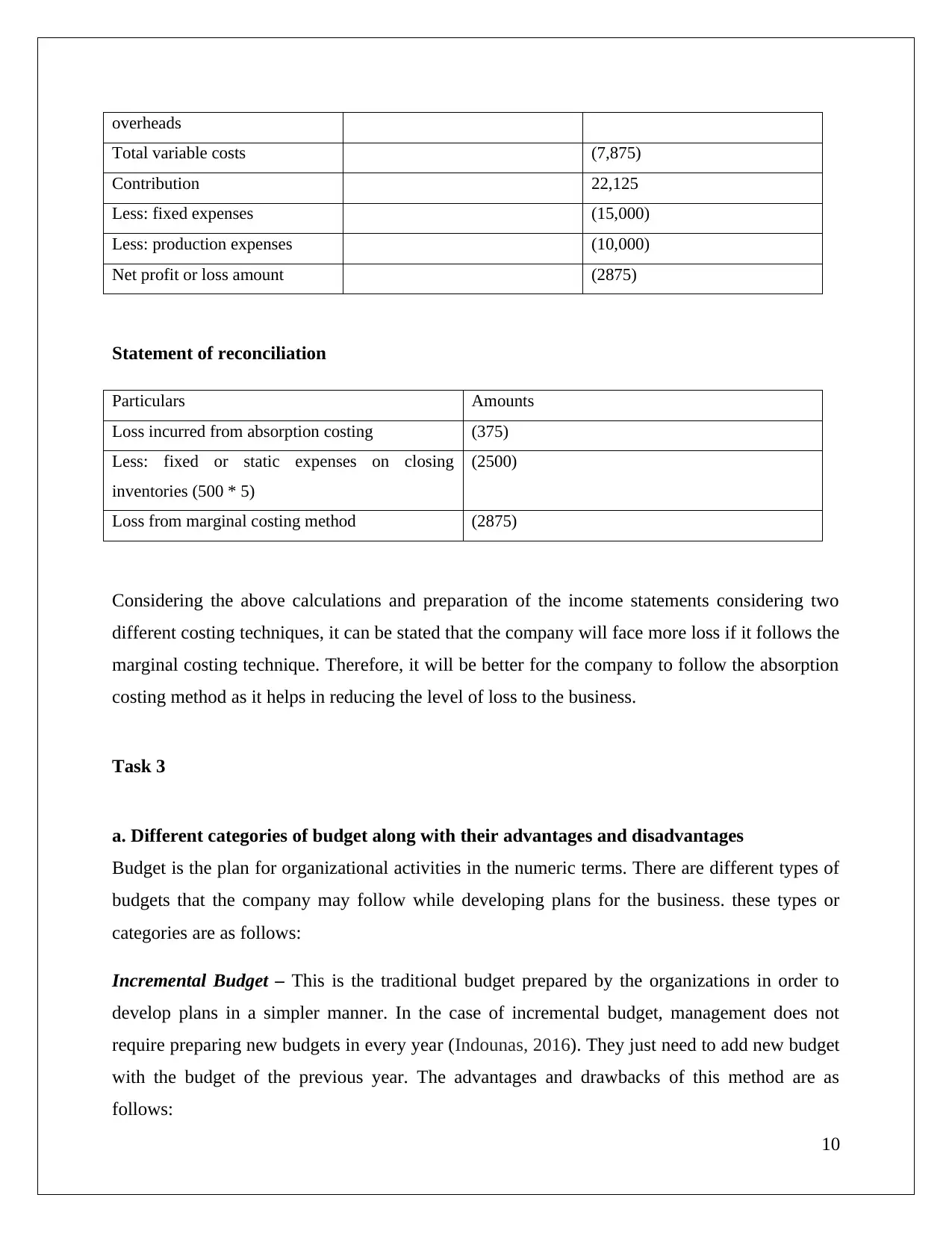

Total variable costs (7,875)

Contribution 22,125

Less: fixed expenses (15,000)

Less: production expenses (10,000)

Net profit or loss amount (2875)

Statement of reconciliation

Particulars Amounts

Loss incurred from absorption costing (375)

Less: fixed or static expenses on closing

inventories (500 * 5)

(2500)

Loss from marginal costing method (2875)

Considering the above calculations and preparation of the income statements considering two

different costing techniques, it can be stated that the company will face more loss if it follows the

marginal costing technique. Therefore, it will be better for the company to follow the absorption

costing method as it helps in reducing the level of loss to the business.

Task 3

a. Different categories of budget along with their advantages and disadvantages

Budget is the plan for organizational activities in the numeric terms. There are different types of

budgets that the company may follow while developing plans for the business. these types or

categories are as follows:

Incremental Budget – This is the traditional budget prepared by the organizations in order to

develop plans in a simpler manner. In the case of incremental budget, management does not

require preparing new budgets in every year (Indounas, 2016). They just need to add new budget

with the budget of the previous year. The advantages and drawbacks of this method are as

follows:

10

Total variable costs (7,875)

Contribution 22,125

Less: fixed expenses (15,000)

Less: production expenses (10,000)

Net profit or loss amount (2875)

Statement of reconciliation

Particulars Amounts

Loss incurred from absorption costing (375)

Less: fixed or static expenses on closing

inventories (500 * 5)

(2500)

Loss from marginal costing method (2875)

Considering the above calculations and preparation of the income statements considering two

different costing techniques, it can be stated that the company will face more loss if it follows the

marginal costing technique. Therefore, it will be better for the company to follow the absorption

costing method as it helps in reducing the level of loss to the business.

Task 3

a. Different categories of budget along with their advantages and disadvantages

Budget is the plan for organizational activities in the numeric terms. There are different types of

budgets that the company may follow while developing plans for the business. these types or

categories are as follows:

Incremental Budget – This is the traditional budget prepared by the organizations in order to

develop plans in a simpler manner. In the case of incremental budget, management does not

require preparing new budgets in every year (Indounas, 2016). They just need to add new budget

with the budget of the previous year. The advantages and drawbacks of this method are as

follows:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages:

This is the simplest method of budgeting that anyone can understand

Under this method of budgeting managers needs to involve less time to complete

budgeting process (Otley and Emmanuel, 2013)

Drawbacks:

This budgeting process does not influence managers reducing cost level

This budgeting system is less flexible and less logical(Weygandtet al., 2015)

Activity-based budgeting – This is the modern budgeting method, in which budget is prepared

after critical analysis of each activity of business. Critical analysis is made to identify actual

resource need of the activities(Belleflamme and Peitz, 2015). The advantages and disadvantages

are as follows:

Advantages:

This method of budgeting is very effective in reducing waste level of business

This method encourages managers for controlling cost level of business operations

Disadvantages:

The activity based budgeting technique is bit critical to understand(Otley and Emmanuel,

2013).

The activity based budgeting technique takes much time to analyze the activities

Zero-based budgeting – This technique of budgeting is also a modern budgeting process, in

which managers need to prepare the budget by considering zero as the base. It means in every

year new budget is needed to be prepared for the business(Binti, 2016). The merits and demerits

of the zero-based budgeting system are as follows:

Merits:

Zero-based budgeting system is very effective in controlling the cost and waste level of

the business.

11

This is the simplest method of budgeting that anyone can understand

Under this method of budgeting managers needs to involve less time to complete

budgeting process (Otley and Emmanuel, 2013)

Drawbacks:

This budgeting process does not influence managers reducing cost level

This budgeting system is less flexible and less logical(Weygandtet al., 2015)

Activity-based budgeting – This is the modern budgeting method, in which budget is prepared

after critical analysis of each activity of business. Critical analysis is made to identify actual

resource need of the activities(Belleflamme and Peitz, 2015). The advantages and disadvantages

are as follows:

Advantages:

This method of budgeting is very effective in reducing waste level of business

This method encourages managers for controlling cost level of business operations

Disadvantages:

The activity based budgeting technique is bit critical to understand(Otley and Emmanuel,

2013).

The activity based budgeting technique takes much time to analyze the activities

Zero-based budgeting – This technique of budgeting is also a modern budgeting process, in

which managers need to prepare the budget by considering zero as the base. It means in every

year new budget is needed to be prepared for the business(Binti, 2016). The merits and demerits

of the zero-based budgeting system are as follows:

Merits:

Zero-based budgeting system is very effective in controlling the cost and waste level of

the business.

11

This method is highly logical and scientific, which is applicable in modern business

context(Yilmaz and Ceran, 2017)

Demerits:

Zero-based budgeting system is time consuming

Zero-based budgeting system is not understandable to everyone because it requires

specific knowledge in the field.

Therefore, from the above discussion, it can be stated that there are several types of budgeting

method that are applicable to the business. however, before selecting any particular method,

proper analysis should be made to identify the actual need of the business.

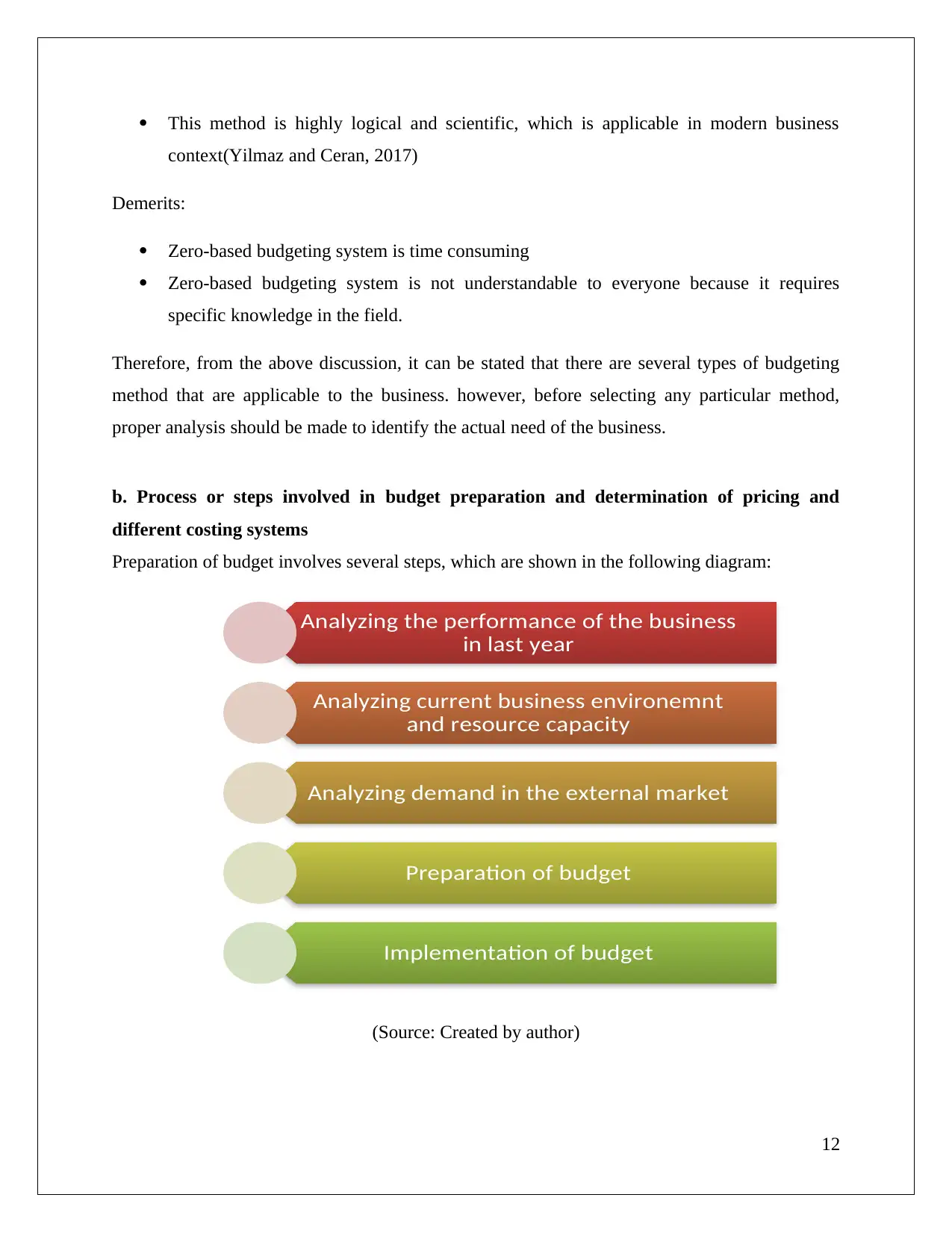

b. Process or steps involved in budget preparation and determination of pricing and

different costing systems

Preparation of budget involves several steps, which are shown in the following diagram:

(Source: Created by author)

12

Analyzing the performance of the business

in last year

Analyzing current business environemnt

and resource capacity

Analyzing demand in the external market

Preparation of budget

Implementation of budget

context(Yilmaz and Ceran, 2017)

Demerits:

Zero-based budgeting system is time consuming

Zero-based budgeting system is not understandable to everyone because it requires

specific knowledge in the field.

Therefore, from the above discussion, it can be stated that there are several types of budgeting

method that are applicable to the business. however, before selecting any particular method,

proper analysis should be made to identify the actual need of the business.

b. Process or steps involved in budget preparation and determination of pricing and

different costing systems

Preparation of budget involves several steps, which are shown in the following diagram:

(Source: Created by author)

12

Analyzing the performance of the business

in last year

Analyzing current business environemnt

and resource capacity

Analyzing demand in the external market

Preparation of budget

Implementation of budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.