Management Accounting Report: Analysis of Tech UK Operations

VerifiedAdded on 2020/06/03

|18

|4588

|44

Report

AI Summary

This report offers a comprehensive analysis of management accounting practices within Tech UK, an electronic gadgets manufacturing enterprise. It begins by defining management accounting and distinguishing it from financial accounting, emphasizing its role in internal decision-making. The report then delves into various cost accounting systems, including actual, normal, and standard costing, alongside inventory and job costing systems. It further explores different types of management accounting reports, such as budget, accounts receivable, job costing, and inventory reports, highlighting the importance of effective information presentation. The report includes the preparation of income statements using both absorption and marginal costing methods. Additionally, it examines budgeting, covering different budget types, the budgeting process, and the importance of budgeting for planning and control. Finally, the report discusses the application of the balance scorecard approach to address financial problems, concluding with a summary of key findings and references.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 (a) Explanation of management accounting......................................................................3

Difference between management and financial accounting...................................................3

Importance of management accounting information as decision making tool.......................4

Cost accounting systems ........................................................................................................4

Inventory management systems.............................................................................................5

Job costing systems ...............................................................................................................5

P2 (b) Difference types of management accounting reports..................................................6

P2 (b) Importance of presentation of information in effective manner.................................7

TASK 2............................................................................................................................................7

P3 Preparation of income statements.....................................................................................7

TASK 3..........................................................................................................................................10

P4 (a) Different kinds of budget and their merits and demerits ..........................................10

P4 (b) Process of preparing budget involving determination of pricing and different costing

systems.................................................................................................................................11

P4 (c) Importance of budget as a tool for planning control purpose....................................12

TASK 4..........................................................................................................................................13

P5 Way to use balance scorecard approach for responding to financial problems..............13

CONCLUSION..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 (a) Explanation of management accounting......................................................................3

Difference between management and financial accounting...................................................3

Importance of management accounting information as decision making tool.......................4

Cost accounting systems ........................................................................................................4

Inventory management systems.............................................................................................5

Job costing systems ...............................................................................................................5

P2 (b) Difference types of management accounting reports..................................................6

P2 (b) Importance of presentation of information in effective manner.................................7

TASK 2............................................................................................................................................7

P3 Preparation of income statements.....................................................................................7

TASK 3..........................................................................................................................................10

P4 (a) Different kinds of budget and their merits and demerits ..........................................10

P4 (b) Process of preparing budget involving determination of pricing and different costing

systems.................................................................................................................................11

P4 (c) Importance of budget as a tool for planning control purpose....................................12

TASK 4..........................................................................................................................................13

P5 Way to use balance scorecard approach for responding to financial problems..............13

CONCLUSION..............................................................................................................................15

REFERENCES...............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a well-defined and established process used for formulation of

reports of management, accounting statements that provide relevant, time financial along with

the statistical information which is needed by the managers in order to make day to day as well

as short term decisions (Hilton, and Platt, 2013). It is used to generate monthly and weekly

reports for people inside the organization. Present report is based on the analysis of Tech UK

which is electronic gadgets manufacturing enterprise in UK which used different types of

management accounting system in order to regulate their smooth business operations along with

achievement of growth in profitability. In this report, distinction between management

accounting and financial accounting has been determined along with its importance as tool for

decision making. Further, Income statement has been prepared by using the two important

methods of cost accounting such as marginal and absorption costing.

TASK 1

P1 (a) Explanation of management accounting

Management accounting have been considered as effective process as well as techniques

which concentrates in the effective and efficient use of resource of organization in order to assist

the managers in their activities of increasing both customers and shareholders values (Ward,

2012). Management system of accounting is also considered as information system that has been

used to develop the information needed by the managers in order to control the resources and

creating values. In present report, management accounting systems used by the Tech (UK)

limited have been analyzed as a trainee management accountant.

Difference between management and financial accounting.

There is major difference between management and financial accounting because the

financial data along with information which is collected by the management accountants of Tech

(UK) limited is only for internal utilization whereas financial accounting information has been

collected and used by the external parties such as shareholders and investors etc. Financial

accounting system follows the generally accepted accounting principles whereas management

Management accounting is a well-defined and established process used for formulation of

reports of management, accounting statements that provide relevant, time financial along with

the statistical information which is needed by the managers in order to make day to day as well

as short term decisions (Hilton, and Platt, 2013). It is used to generate monthly and weekly

reports for people inside the organization. Present report is based on the analysis of Tech UK

which is electronic gadgets manufacturing enterprise in UK which used different types of

management accounting system in order to regulate their smooth business operations along with

achievement of growth in profitability. In this report, distinction between management

accounting and financial accounting has been determined along with its importance as tool for

decision making. Further, Income statement has been prepared by using the two important

methods of cost accounting such as marginal and absorption costing.

TASK 1

P1 (a) Explanation of management accounting

Management accounting have been considered as effective process as well as techniques

which concentrates in the effective and efficient use of resource of organization in order to assist

the managers in their activities of increasing both customers and shareholders values (Ward,

2012). Management system of accounting is also considered as information system that has been

used to develop the information needed by the managers in order to control the resources and

creating values. In present report, management accounting systems used by the Tech (UK)

limited have been analyzed as a trainee management accountant.

Difference between management and financial accounting.

There is major difference between management and financial accounting because the

financial data along with information which is collected by the management accountants of Tech

(UK) limited is only for internal utilization whereas financial accounting information has been

collected and used by the external parties such as shareholders and investors etc. Financial

accounting system follows the generally accepted accounting principles whereas management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accountants do not implement these principles. Further, the financial reports and statements that

are formulated by accountants involve the performance, budgets as well as costs reports which

are usually concentrated towards a specific segment with in the business enterprise such as

production line or functional units whereas the financial accountants of the enterprise collects the

information in order to develop financial statements for showing the financial position of the

overall company (Parker, 2012). Moreover, reports of financial accounting depends upon the

previous information which emphasis on the independence as well as verifiability whereas MA

information as well as reports are not controlled by the standards or regulations of accounting

and its content has been designed by the needs of managers.

Importance of management accounting information as decision making tool.

Employers and manager of Tech (UK) limited also have to take countless decision while

producing their new products in every business day. Information of management accounting

provides them input from the data to take those important decisions that will improve the

decision making of company for long term (Fullerton, Kennedy and Widener, 2014). Through

this information, managers of Tech UK limited will be able examine the costs that differ along

the alternatives of advertising for their special charger for mobile telephone and other carry on

gadgets , not considering the common costs. Further, through utilization techniques of activity

based costing, manager of Tech (UK) can also determine the important task and activities needed

to develop and service a products line. It allows the organization to concentrate on advertising its

special charger to its target customers. Primary use of information related to management

accounting is to delegate the information that will be used for manufacturing the product.

Budgeting, projection of financial statements and balance scorecard are major illustration of the

way through which the management accounting information have been used to delegate

information to support the management control the future financial position of Tech (UK).

Cost accounting systems

Actual costing: A system of cost accounting that always utilize the actual costs, rates of

direct costs as well as relevant qualities which are used for production to demonstrate the

costs of specific product. For example: ADC= ACR* actual qualities, actual indirect

are formulated by accountants involve the performance, budgets as well as costs reports which

are usually concentrated towards a specific segment with in the business enterprise such as

production line or functional units whereas the financial accountants of the enterprise collects the

information in order to develop financial statements for showing the financial position of the

overall company (Parker, 2012). Moreover, reports of financial accounting depends upon the

previous information which emphasis on the independence as well as verifiability whereas MA

information as well as reports are not controlled by the standards or regulations of accounting

and its content has been designed by the needs of managers.

Importance of management accounting information as decision making tool.

Employers and manager of Tech (UK) limited also have to take countless decision while

producing their new products in every business day. Information of management accounting

provides them input from the data to take those important decisions that will improve the

decision making of company for long term (Fullerton, Kennedy and Widener, 2014). Through

this information, managers of Tech UK limited will be able examine the costs that differ along

the alternatives of advertising for their special charger for mobile telephone and other carry on

gadgets , not considering the common costs. Further, through utilization techniques of activity

based costing, manager of Tech (UK) can also determine the important task and activities needed

to develop and service a products line. It allows the organization to concentrate on advertising its

special charger to its target customers. Primary use of information related to management

accounting is to delegate the information that will be used for manufacturing the product.

Budgeting, projection of financial statements and balance scorecard are major illustration of the

way through which the management accounting information have been used to delegate

information to support the management control the future financial position of Tech (UK).

Cost accounting systems

Actual costing: A system of cost accounting that always utilize the actual costs, rates of

direct costs as well as relevant qualities which are used for production to demonstrate the

costs of specific product. For example: ADC= ACR* actual qualities, actual indirect

expenses= allocated indirect cost rates * actual qualities. In tech (UK), this formula has been

used to calculate and analyze the overall production expenses.

Normal costing: Method of costing accounting that is evolved to provide values to the

products manufactured by the enterprise along with the actual material expenses directs cost

of labor as well as manufacturing overheads which are based on the predetermined rate of

production overheads (Lambert and Sponem, 2012).

Standard costing: It is also considered as practice that used for substitution of an expected

cost for actual expenses in the records of management accounting and further recording of

alterations periodically by determining the distinction between the actual and expected costs

(Standard costing, 2018).

Inventory management systems

Systems of managing inventories are used for tracking of products of Tech UK through

their overall supply chain or portion of business in which the company operates. In

manufacturing organization like Tech (UK), inventory management systems are used for

tracking of materials, the inventory levels for parts and finish products (Lavia López and Hiebl,

2014 ). It also involves the process reordering and making integration with the ERP software’s.

Further, there are two main types of inventory management system that needs to be used by

company such as perpetual and periodic inventory systems. In Periodic inventory systems the

data have been updated within specific time duration usually within a year whereas perpetual

inventory system is used by Tech (UK) to update inventory data continuously in order to analyze

the quantity and availability of inventories in appropriate manner. Barcode technology has been

used in perpetual system of inventory management.

Job costing systems

Job costing is mainly considered as a method that has been used for assigning the cost of

manufacturing to an individual product or the batches of the product. This method of cost accounting has

been used in the situation when the products and services have been produced are sufficiently distinct

from each other (The job costing system, 2018). It is also involves the accumulation of cost of raw

materials, overheads and labor for the accomplishment of specific job. Usually there are three different

types of things that have to be included in the method of job costing such as direct materials, labor and

used to calculate and analyze the overall production expenses.

Normal costing: Method of costing accounting that is evolved to provide values to the

products manufactured by the enterprise along with the actual material expenses directs cost

of labor as well as manufacturing overheads which are based on the predetermined rate of

production overheads (Lambert and Sponem, 2012).

Standard costing: It is also considered as practice that used for substitution of an expected

cost for actual expenses in the records of management accounting and further recording of

alterations periodically by determining the distinction between the actual and expected costs

(Standard costing, 2018).

Inventory management systems

Systems of managing inventories are used for tracking of products of Tech UK through

their overall supply chain or portion of business in which the company operates. In

manufacturing organization like Tech (UK), inventory management systems are used for

tracking of materials, the inventory levels for parts and finish products (Lavia López and Hiebl,

2014 ). It also involves the process reordering and making integration with the ERP software’s.

Further, there are two main types of inventory management system that needs to be used by

company such as perpetual and periodic inventory systems. In Periodic inventory systems the

data have been updated within specific time duration usually within a year whereas perpetual

inventory system is used by Tech (UK) to update inventory data continuously in order to analyze

the quantity and availability of inventories in appropriate manner. Barcode technology has been

used in perpetual system of inventory management.

Job costing systems

Job costing is mainly considered as a method that has been used for assigning the cost of

manufacturing to an individual product or the batches of the product. This method of cost accounting has

been used in the situation when the products and services have been produced are sufficiently distinct

from each other (The job costing system, 2018). It is also involves the accumulation of cost of raw

materials, overheads and labor for the accomplishment of specific job. Usually there are three different

types of things that have to be included in the method of job costing such as direct materials, labor and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overhead. In present context, manager of Tech (UK) limited will also needs to use this in order to track

the cost of materials that is used them at the time of manufacturing their special charger for mobile

telephone and other gadgets. Through these systems, company can also track the cost of labor they have

used for manufacturing of their product. Further, the job costing systems also assigns the costs of

overheads to one or more costs pools.

P2 (b) Difference types of management accounting reports.

There are some different management accounting reports have been developed by the

management accountants in Tech (UK) limited that help the employers as well as managers to

monitor the performance of organization and these are prepared frequently within the

accounting period as per requirement. Some important management accounting reports have

been mentioned below:

Budget report: These are considered as important reports that assist the owners of Tech

(UK) limited in analyzing performance of their organization along with department

performance and control the costs (Contrafatto and Burns, 2013). This report has been

used by the management in order to compare the budgeted, estimated along with the

actual performance number attained during the time duration.

Account receivable report: It is also important management accounting report that usually

highlights those customers of Tech (UK) limited who have unpaid invoices and also the

unpaid credit memos. It is considered as primary tool that has been used by the managers

of company to demonstrate the invoice which is overdue for the payment along with the

effectiveness of the credit as well as collection functions.

Job costing report: It is an important report of managerial accounting that is used to

determine the expenses for a specific project of organization. These expenses have been

compared with the revenue received in order to evaluate the profitability. In present

context, managers of Tech (UK) limited also use this reports to analyze the cost of labor

which they have incurred to manufacture their special mobile charger and other gadgets

for a project. It also helps in identifying the highest areas of income of the business so

that organization will focus their efforts there rather than wasting time and funds on the

low profits margins.

the cost of materials that is used them at the time of manufacturing their special charger for mobile

telephone and other gadgets. Through these systems, company can also track the cost of labor they have

used for manufacturing of their product. Further, the job costing systems also assigns the costs of

overheads to one or more costs pools.

P2 (b) Difference types of management accounting reports.

There are some different management accounting reports have been developed by the

management accountants in Tech (UK) limited that help the employers as well as managers to

monitor the performance of organization and these are prepared frequently within the

accounting period as per requirement. Some important management accounting reports have

been mentioned below:

Budget report: These are considered as important reports that assist the owners of Tech

(UK) limited in analyzing performance of their organization along with department

performance and control the costs (Contrafatto and Burns, 2013). This report has been

used by the management in order to compare the budgeted, estimated along with the

actual performance number attained during the time duration.

Account receivable report: It is also important management accounting report that usually

highlights those customers of Tech (UK) limited who have unpaid invoices and also the

unpaid credit memos. It is considered as primary tool that has been used by the managers

of company to demonstrate the invoice which is overdue for the payment along with the

effectiveness of the credit as well as collection functions.

Job costing report: It is an important report of managerial accounting that is used to

determine the expenses for a specific project of organization. These expenses have been

compared with the revenue received in order to evaluate the profitability. In present

context, managers of Tech (UK) limited also use this reports to analyze the cost of labor

which they have incurred to manufacture their special mobile charger and other gadgets

for a project. It also helps in identifying the highest areas of income of the business so

that organization will focus their efforts there rather than wasting time and funds on the

low profits margins.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory and production report: manufacturing enterprises like Tech UK, with the

physical inventory will also use the managerial accounting reports in order to make their

process of manufacturing products more effective and efficient. It involves the inventory

waste and per unit overhead costs.

P2 (b) Importance of presentation of information in effective manner.

Accounting data as well as information have been presented by the managers in the forms

of tables of numbers and charts that along with the clear determine of the cost of labor,

overheads and material costs in order to make comparison with the revenue which is received

after sale of goods after making for the effective evaluation of profitability and performance of

organization in market (Herbert and Seal, 2012). Appropriate presentation of data will be useful

analysis tool for Tech (UK) limited and if the data are being effectively interpreted then this will

facilitate the manager in process of decision making. There are various software packages which

have allowed the managers of Tech (UK) in creation of charts that will look very professional

and provide effective analysis of information so that cost of producing the given product can be

estimated and reduced in future. Further, it supports the organization in formulation and

implementation of strategy. It also contributes to improve the company’s competitive advantage

in terms of quality of products, time of delivery, cost, flexibility and the innovation through

distinctive process improvements and techniques of managing the cost.

TASK 2

P3 Preparation of income statements

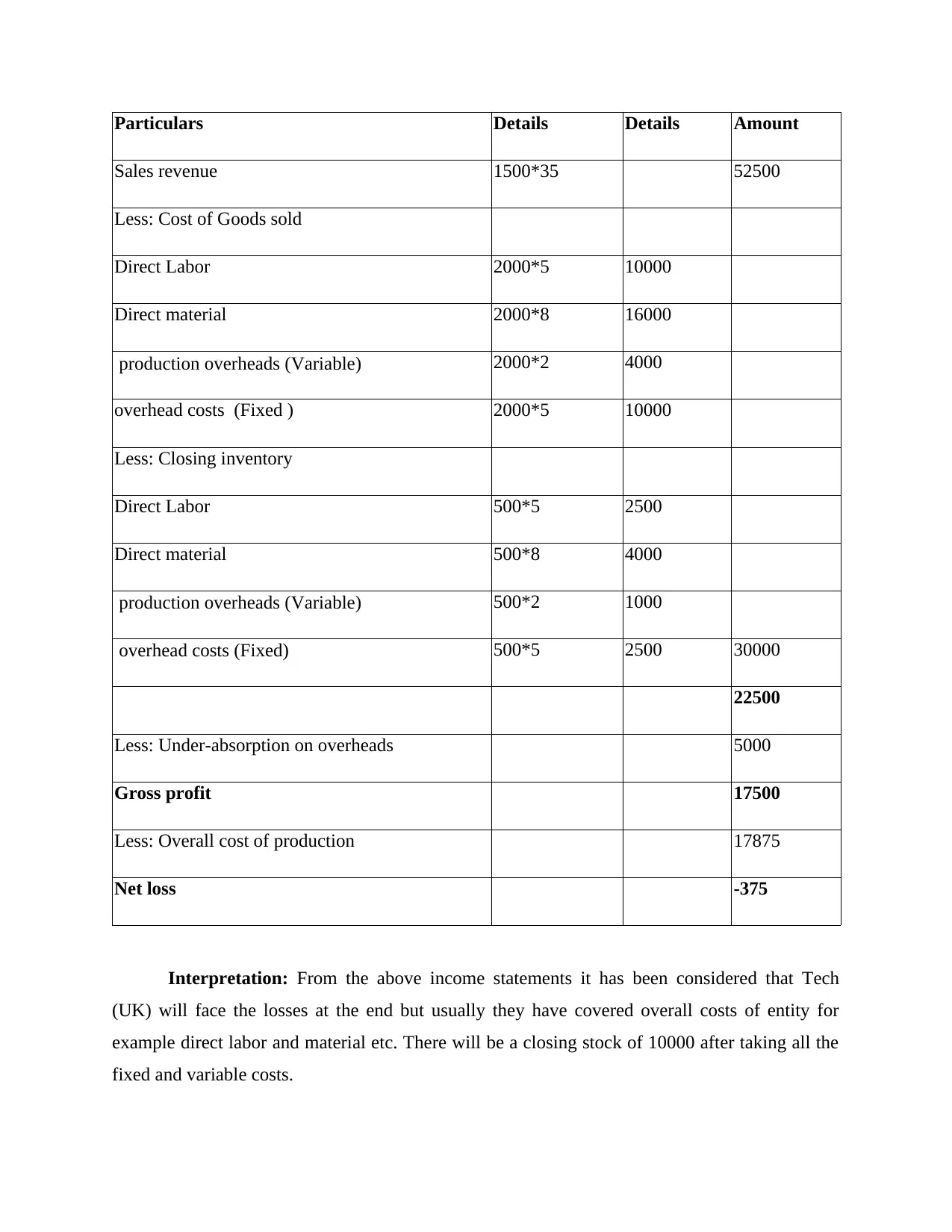

Absorption costing: It is considered as methods of cost accounting in which no

difference is made between the fixed and variable costs in the calculation of profits.

Statement of absorption costing estimated that fixed costs is associated to products so that

all the production costs whether it is fixed or variable will become a part of cost

manufacturing product.

Absorption costing:

Income statement for TECH (UK) on absorption costing

physical inventory will also use the managerial accounting reports in order to make their

process of manufacturing products more effective and efficient. It involves the inventory

waste and per unit overhead costs.

P2 (b) Importance of presentation of information in effective manner.

Accounting data as well as information have been presented by the managers in the forms

of tables of numbers and charts that along with the clear determine of the cost of labor,

overheads and material costs in order to make comparison with the revenue which is received

after sale of goods after making for the effective evaluation of profitability and performance of

organization in market (Herbert and Seal, 2012). Appropriate presentation of data will be useful

analysis tool for Tech (UK) limited and if the data are being effectively interpreted then this will

facilitate the manager in process of decision making. There are various software packages which

have allowed the managers of Tech (UK) in creation of charts that will look very professional

and provide effective analysis of information so that cost of producing the given product can be

estimated and reduced in future. Further, it supports the organization in formulation and

implementation of strategy. It also contributes to improve the company’s competitive advantage

in terms of quality of products, time of delivery, cost, flexibility and the innovation through

distinctive process improvements and techniques of managing the cost.

TASK 2

P3 Preparation of income statements

Absorption costing: It is considered as methods of cost accounting in which no

difference is made between the fixed and variable costs in the calculation of profits.

Statement of absorption costing estimated that fixed costs is associated to products so that

all the production costs whether it is fixed or variable will become a part of cost

manufacturing product.

Absorption costing:

Income statement for TECH (UK) on absorption costing

Particulars Details Details Amount

Sales revenue 1500*35 52500

Less: Cost of Goods sold

Direct Labor 2000*5 10000

Direct material 2000*8 16000

production overheads (Variable) 2000*2 4000

overhead costs (Fixed ) 2000*5 10000

Less: Closing inventory

Direct Labor 500*5 2500

Direct material 500*8 4000

production overheads (Variable) 500*2 1000

overhead costs (Fixed) 500*5 2500 30000

22500

Less: Under-absorption on overheads 5000

Gross profit 17500

Less: Overall cost of production 17875

Net loss -375

Interpretation: From the above income statements it has been considered that Tech

(UK) will face the losses at the end but usually they have covered overall costs of entity for

example direct labor and material etc. There will be a closing stock of 10000 after taking all the

fixed and variable costs.

Sales revenue 1500*35 52500

Less: Cost of Goods sold

Direct Labor 2000*5 10000

Direct material 2000*8 16000

production overheads (Variable) 2000*2 4000

overhead costs (Fixed ) 2000*5 10000

Less: Closing inventory

Direct Labor 500*5 2500

Direct material 500*8 4000

production overheads (Variable) 500*2 1000

overhead costs (Fixed) 500*5 2500 30000

22500

Less: Under-absorption on overheads 5000

Gross profit 17500

Less: Overall cost of production 17875

Net loss -375

Interpretation: From the above income statements it has been considered that Tech

(UK) will face the losses at the end but usually they have covered overall costs of entity for

example direct labor and material etc. There will be a closing stock of 10000 after taking all the

fixed and variable costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

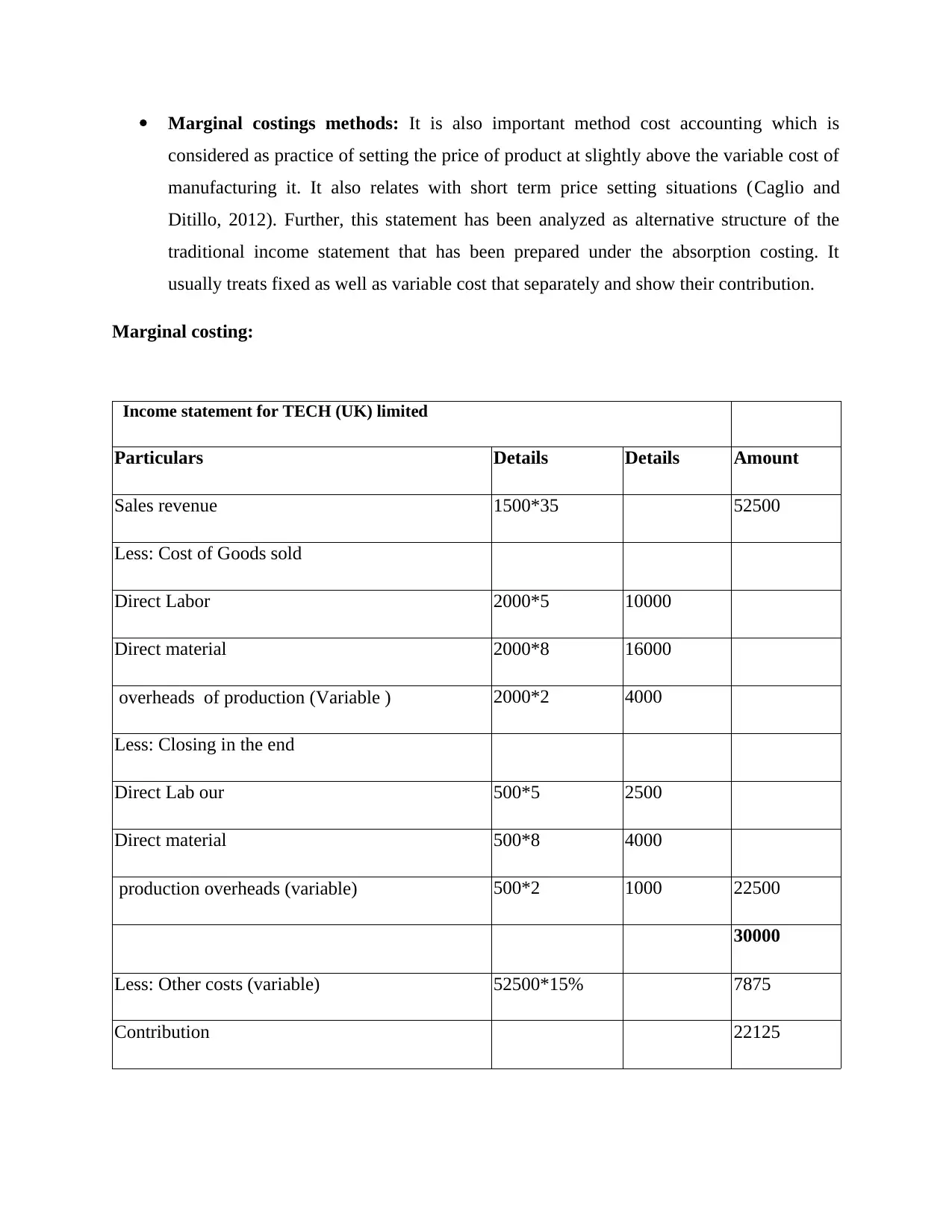

Marginal costings methods: It is also important method cost accounting which is

considered as practice of setting the price of product at slightly above the variable cost of

manufacturing it. It also relates with short term price setting situations (Caglio and

Ditillo, 2012). Further, this statement has been analyzed as alternative structure of the

traditional income statement that has been prepared under the absorption costing. It

usually treats fixed as well as variable cost that separately and show their contribution.

Marginal costing:

Income statement for TECH (UK) limited

Particulars Details Details Amount

Sales revenue 1500*35 52500

Less: Cost of Goods sold

Direct Labor 2000*5 10000

Direct material 2000*8 16000

overheads of production (Variable ) 2000*2 4000

Less: Closing in the end

Direct Lab our 500*5 2500

Direct material 500*8 4000

production overheads (variable) 500*2 1000 22500

30000

Less: Other costs (variable) 52500*15% 7875

Contribution 22125

considered as practice of setting the price of product at slightly above the variable cost of

manufacturing it. It also relates with short term price setting situations (Caglio and

Ditillo, 2012). Further, this statement has been analyzed as alternative structure of the

traditional income statement that has been prepared under the absorption costing. It

usually treats fixed as well as variable cost that separately and show their contribution.

Marginal costing:

Income statement for TECH (UK) limited

Particulars Details Details Amount

Sales revenue 1500*35 52500

Less: Cost of Goods sold

Direct Labor 2000*5 10000

Direct material 2000*8 16000

overheads of production (Variable ) 2000*2 4000

Less: Closing in the end

Direct Lab our 500*5 2500

Direct material 500*8 4000

production overheads (variable) 500*2 1000 22500

30000

Less: Other costs (variable) 52500*15% 7875

Contribution 22125

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

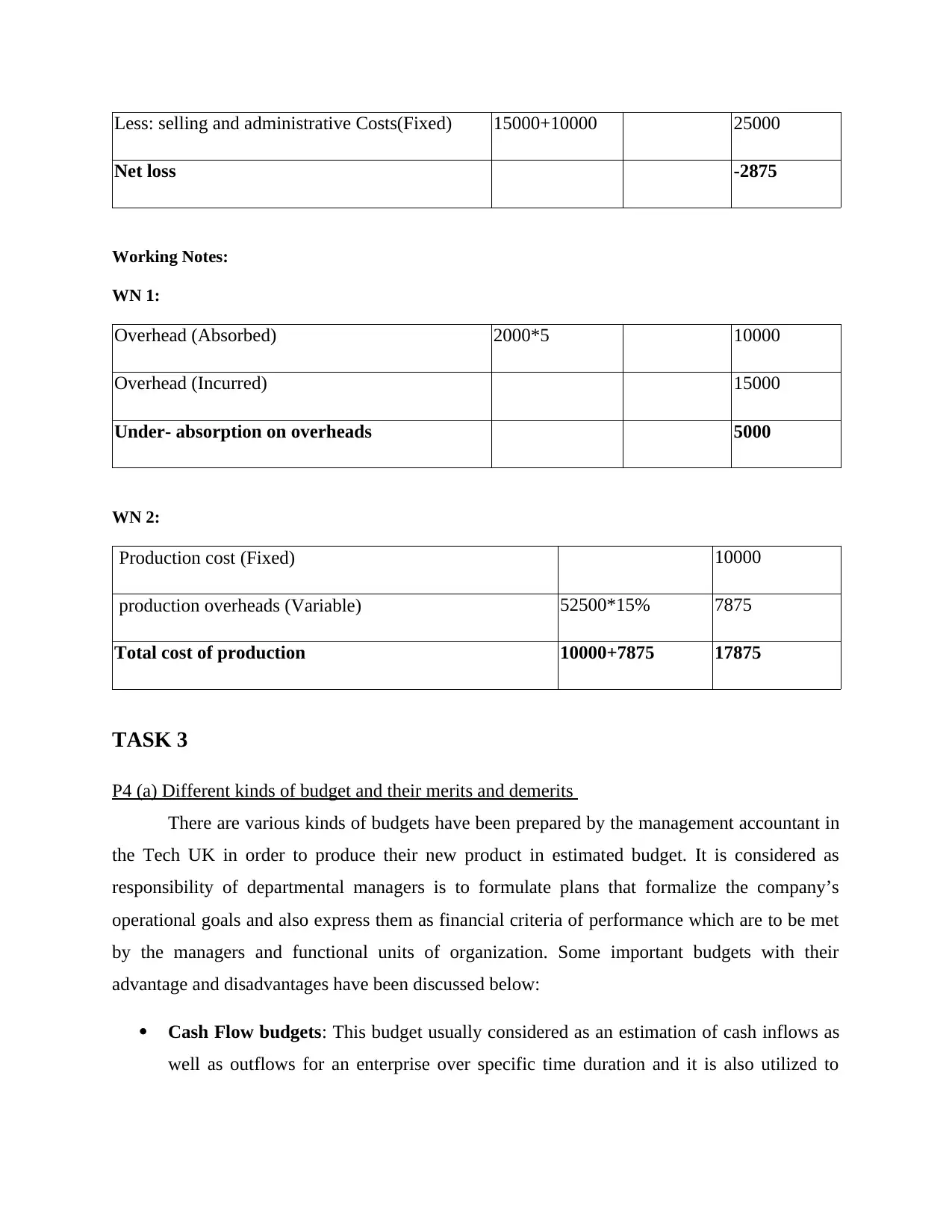

Less: selling and administrative Costs(Fixed) 15000+10000 25000

Net loss -2875

Working Notes:

WN 1:

Overhead (Absorbed) 2000*5 10000

Overhead (Incurred) 15000

Under- absorption on overheads 5000

WN 2:

Production cost (Fixed) 10000

production overheads (Variable) 52500*15% 7875

Total cost of production 10000+7875 17875

TASK 3

P4 (a) Different kinds of budget and their merits and demerits

There are various kinds of budgets have been prepared by the management accountant in

the Tech UK in order to produce their new product in estimated budget. It is considered as

responsibility of departmental managers is to formulate plans that formalize the company’s

operational goals and also express them as financial criteria of performance which are to be met

by the managers and functional units of organization. Some important budgets with their

advantage and disadvantages have been discussed below:

Cash Flow budgets: This budget usually considered as an estimation of cash inflows as

well as outflows for an enterprise over specific time duration and it is also utilized to

Net loss -2875

Working Notes:

WN 1:

Overhead (Absorbed) 2000*5 10000

Overhead (Incurred) 15000

Under- absorption on overheads 5000

WN 2:

Production cost (Fixed) 10000

production overheads (Variable) 52500*15% 7875

Total cost of production 10000+7875 17875

TASK 3

P4 (a) Different kinds of budget and their merits and demerits

There are various kinds of budgets have been prepared by the management accountant in

the Tech UK in order to produce their new product in estimated budget. It is considered as

responsibility of departmental managers is to formulate plans that formalize the company’s

operational goals and also express them as financial criteria of performance which are to be met

by the managers and functional units of organization. Some important budgets with their

advantage and disadvantages have been discussed below:

Cash Flow budgets: This budget usually considered as an estimation of cash inflows as

well as outflows for an enterprise over specific time duration and it is also utilized to

analyze that whether the organization has sufficient cash to operate. Organization needs

to utilize the sales and production forecasts in order to develop the budget of cash along

with the estimations about the expenditures which are required and accounts receivables

Advantages: Considered as beneficial as it provides actual forecast required to complete

production.

Disadvantages: Time consuming method and not always provide actual support in analyzing the

actual required completing the production in future financial period.

Purchase budget: It is also important budget that consist the cost of raw materials which

is purchased by Tech UK during each budget period (Bouten and Hoozée, 2013).

Moreover, the amount which is specified in the budget is considered as the amount that

is required to make sure that there will be a sufficient amount of inventory in

organization so that customers order for special mobile telephone charger can be met. In

simple words, Purchase budget will simply match along with the actual number of units

that is expected to be sold in the financial or budget time duration.

Advantages: Help in representation of actual amount which is incurred from the sale of products

and services. Disadvantages: Also considered as time consuming approach and less reliable.

Operating budgets: These are considered as the budgets that mainly involve the revenue

as well as operating expenses which surrounded with day to day business activities of

Tech UK. Operating revenues always signifies the sale of products and services.

Operating expenses will determine the costs of products sold along with the overhead and

administrative costs which are directly related to the manufacturing of goods and

services.

Advantages: Through this, Managers compare ongoing results to budget throughout the year,

planning and adjusting for variations in revenue.

Disadvantages: Effective management accounting techniques but it will not provide support in

reduction of costs and expenses.

to utilize the sales and production forecasts in order to develop the budget of cash along

with the estimations about the expenditures which are required and accounts receivables

Advantages: Considered as beneficial as it provides actual forecast required to complete

production.

Disadvantages: Time consuming method and not always provide actual support in analyzing the

actual required completing the production in future financial period.

Purchase budget: It is also important budget that consist the cost of raw materials which

is purchased by Tech UK during each budget period (Bouten and Hoozée, 2013).

Moreover, the amount which is specified in the budget is considered as the amount that

is required to make sure that there will be a sufficient amount of inventory in

organization so that customers order for special mobile telephone charger can be met. In

simple words, Purchase budget will simply match along with the actual number of units

that is expected to be sold in the financial or budget time duration.

Advantages: Help in representation of actual amount which is incurred from the sale of products

and services. Disadvantages: Also considered as time consuming approach and less reliable.

Operating budgets: These are considered as the budgets that mainly involve the revenue

as well as operating expenses which surrounded with day to day business activities of

Tech UK. Operating revenues always signifies the sale of products and services.

Operating expenses will determine the costs of products sold along with the overhead and

administrative costs which are directly related to the manufacturing of goods and

services.

Advantages: Through this, Managers compare ongoing results to budget throughout the year,

planning and adjusting for variations in revenue.

Disadvantages: Effective management accounting techniques but it will not provide support in

reduction of costs and expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.