Comprehensive Management Accounting Report: Tech (UK) Limited

VerifiedAdded on 2020/07/22

|16

|4920

|52

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within Tech (UK) Limited, a mobile phone charger producer. It begins with an explanation of management accounting, emphasizing its importance in decision-making, cost control, and financial reporting. The report details various systems such as cost accounting, inventory management, and job costing. It then explores different types of managerial accounting reports, including budget reports, job costing reports, and inventory reports. The report also presents and compares income statements using absorption and marginal costing techniques, along with a reconciliation of profitability. Finally, it discusses the benefits of management accounting for Tech (UK) Limited and assesses the differences between management accounting systems and management reporting systems. The report includes tables and appendices to support its analysis and conclusions.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting Explanation and the essential of management accounting system 1

P2 Presenting financial information.......................................................................................3

M1 Evaluation of benefits......................................................................................................5

D1 Management accounting system assessment of and management reporting...................5

TASK 2............................................................................................................................................5

P3 Management accounting techniques:-...............................................................................5

M2 Techniques and reconcile the profitability.......................................................................6

D2 Interpret data for the business activities...........................................................................7

TASK 3............................................................................................................................................7

P4 Various budget system......................................................................................................7

M3 Analysis of different planning.......................................................................................10

D3 Evaluation of planning tools...........................................................................................10

TASK 4..........................................................................................................................................10

P5 Comparison the way of company are adapting management accounting system to respond

financial system....................................................................................................................10

CONCLUSION ............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting Explanation and the essential of management accounting system 1

P2 Presenting financial information.......................................................................................3

M1 Evaluation of benefits......................................................................................................5

D1 Management accounting system assessment of and management reporting...................5

TASK 2............................................................................................................................................5

P3 Management accounting techniques:-...............................................................................5

M2 Techniques and reconcile the profitability.......................................................................6

D2 Interpret data for the business activities...........................................................................7

TASK 3............................................................................................................................................7

P4 Various budget system......................................................................................................7

M3 Analysis of different planning.......................................................................................10

D3 Evaluation of planning tools...........................................................................................10

TASK 4..........................................................................................................................................10

P5 Comparison the way of company are adapting management accounting system to respond

financial system....................................................................................................................10

CONCLUSION ............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The process of ready to management reports and accounts that give appropriate and well

timed fiscal and statistical content needed by managers to make daily basis decisions is termed as

management accounting. In this, director usage the provisions of accounting content in order to

improved inform themselves. This present report is based on Tech (UK) Limited which is

producing particular charger for mobile telephone in the UK. In this report, explanation of

management accounting, their importance along with absorption and marginal costing are

covered. Other than that, benefits of different types of budgets, their process and importance are

discussed.

TASK 1

P1 Management accounting Explanation and the essential of management accounting system

Management accounting system is a profession which include partnering in the

management decision making that help managers in their working and decision. Through it,

managers can take their decision on daily basis. This is a process of handling the entire situation

in the company. Each and every company need management accounting system to make good

environment in their organisation (Fullerton and Widener, 2014). They want to secure their

entire information and data of the company, so they use the management accounting for their

business.

Management accounting manage the entire operational work in the company. Through it,

they can make some report of the company, it can be budget report, sales report, inventory report

and employees productivity report. In the financial accounting, they calculate the entire figure

which was invested in the organisation and which will be expense in the future. Other than that,

they can evaluate their profit and loss statements from the financial accounting. Management

accounting and financial accounting system play the important role in Tech (UK) Limited

company.

Importance of management accounting information: -

Management accounting play vital role in the organisation. There are lots of benefits

from the management accounting in the company. Through it, they can determine their aim and

set the goals of the company, it helps in the preparation of plan. Through it, their employee can

provide better services to their customers. Along with this, it increases efficiency of the business

1

The process of ready to management reports and accounts that give appropriate and well

timed fiscal and statistical content needed by managers to make daily basis decisions is termed as

management accounting. In this, director usage the provisions of accounting content in order to

improved inform themselves. This present report is based on Tech (UK) Limited which is

producing particular charger for mobile telephone in the UK. In this report, explanation of

management accounting, their importance along with absorption and marginal costing are

covered. Other than that, benefits of different types of budgets, their process and importance are

discussed.

TASK 1

P1 Management accounting Explanation and the essential of management accounting system

Management accounting system is a profession which include partnering in the

management decision making that help managers in their working and decision. Through it,

managers can take their decision on daily basis. This is a process of handling the entire situation

in the company. Each and every company need management accounting system to make good

environment in their organisation (Fullerton and Widener, 2014). They want to secure their

entire information and data of the company, so they use the management accounting for their

business.

Management accounting manage the entire operational work in the company. Through it,

they can make some report of the company, it can be budget report, sales report, inventory report

and employees productivity report. In the financial accounting, they calculate the entire figure

which was invested in the organisation and which will be expense in the future. Other than that,

they can evaluate their profit and loss statements from the financial accounting. Management

accounting and financial accounting system play the important role in Tech (UK) Limited

company.

Importance of management accounting information: -

Management accounting play vital role in the organisation. There are lots of benefits

from the management accounting in the company. Through it, they can determine their aim and

set the goals of the company, it helps in the preparation of plan. Through it, their employee can

provide better services to their customers. Along with this, it increases efficiency of the business

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and profitability. When company uses this management, it provides them effective management

control, so managers can take their better decision for any situation. When they will be able to

measure performance, then they can take decision of incentives which is given to the employees.

Management accounting gives this entire benefit to their managers, so it is very useful

accounting system in the organisation. Through it, they can beat any of the competitor in the

market and will be able to earn more profit and reward from the business (Renz, 2016).

Cost accounting system: -

It is the important system in the management accounting system for analysis the entire

cost of the company. Through it, they can examine about the cost or organisation. Other than

that, they can have analysis about the department and employees, who is giving their best or not

at their work place. Through cost accounting system, managers can control the entire expenses of

the organisation. In the cost accounting system, they can include the inventory rating activity,

cost accumulation activity, cost flow assumption, input measurement basis and ability of

recording inventory (Chenhall and Moers, 2015). These elements are very useful in the

organisation and it gives lot of information and knowledge to the managers. It is a model utilized

by the company to figuring the value of their good for profit investigation, inventory valuation

and cost control. In this system, company analyses about products or their profitability in the

business; other than that, they evaluate about their employees that their productivity is effective

or not for the company. In the Tech (UK) Limited, there are different types of departments are

working and they can use cost accounting system to improve their work at their work place.

Every department can evaluate the productivity of their team members, so that they can improve

their productivity.

Inventory management system: -

In the Tech (UK) Limited, they need to manage their inventory and it can be managed by

the inventory management system. Through it, they can manage their entire orders of parts of the

mobile telephone. It is the current process of automotive pasts and good into and out of a

organization's position. When Tech (UK) Limited import or export their products, they should

manage their sale and purchase data in the system and all data can be saved in the inventory

management system. Organisations handle their stock list on a daily basis as they place new

orders for goods and ship orders out to clients. Through it, managers can track end to end record

of their products and services. They can manage their warehouse from inventory system.

2

control, so managers can take their better decision for any situation. When they will be able to

measure performance, then they can take decision of incentives which is given to the employees.

Management accounting gives this entire benefit to their managers, so it is very useful

accounting system in the organisation. Through it, they can beat any of the competitor in the

market and will be able to earn more profit and reward from the business (Renz, 2016).

Cost accounting system: -

It is the important system in the management accounting system for analysis the entire

cost of the company. Through it, they can examine about the cost or organisation. Other than

that, they can have analysis about the department and employees, who is giving their best or not

at their work place. Through cost accounting system, managers can control the entire expenses of

the organisation. In the cost accounting system, they can include the inventory rating activity,

cost accumulation activity, cost flow assumption, input measurement basis and ability of

recording inventory (Chenhall and Moers, 2015). These elements are very useful in the

organisation and it gives lot of information and knowledge to the managers. It is a model utilized

by the company to figuring the value of their good for profit investigation, inventory valuation

and cost control. In this system, company analyses about products or their profitability in the

business; other than that, they evaluate about their employees that their productivity is effective

or not for the company. In the Tech (UK) Limited, there are different types of departments are

working and they can use cost accounting system to improve their work at their work place.

Every department can evaluate the productivity of their team members, so that they can improve

their productivity.

Inventory management system: -

In the Tech (UK) Limited, they need to manage their inventory and it can be managed by

the inventory management system. Through it, they can manage their entire orders of parts of the

mobile telephone. It is the current process of automotive pasts and good into and out of a

organization's position. When Tech (UK) Limited import or export their products, they should

manage their sale and purchase data in the system and all data can be saved in the inventory

management system. Organisations handle their stock list on a daily basis as they place new

orders for goods and ship orders out to clients. Through it, managers can track end to end record

of their products and services. They can manage their warehouse from inventory system.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Company can save their entire data of sales, purchase, return, delivery, and pending. They can

track any of the record in very easy process thorough inventory management system.

Job costing systems: -

This system relate to the procedure of roll up about the costs related with a particular

manufacture or service job. It need to accumulate direct materials, direct labour and overhead.

There are lots of department in the production, but they need to analysis about labour, direct

materials, and overhead. When they use of job costing system, they can track the cost of

materials that are utilized in the productions. Other than that, the this method can track the cost

of the labour utilized on a task. In the organisation, there are different types of equipment, so

they can get the depreciation on it. It also can be identified by the overhead of job costing

system. However, department of production can use this system, and track the entire job costing

in the business (Suomala and Lukka, 2014). It is the very useful system in the company for

controlling the cost. They can reduce their costing and increasing profitability from this

management accounting system.

P2 Presenting financial information

Types of managerial accounting reports: -

3

Illustration 1: Job costing report

(Sources : Job costing report, 2017)

track any of the record in very easy process thorough inventory management system.

Job costing systems: -

This system relate to the procedure of roll up about the costs related with a particular

manufacture or service job. It need to accumulate direct materials, direct labour and overhead.

There are lots of department in the production, but they need to analysis about labour, direct

materials, and overhead. When they use of job costing system, they can track the cost of

materials that are utilized in the productions. Other than that, the this method can track the cost

of the labour utilized on a task. In the organisation, there are different types of equipment, so

they can get the depreciation on it. It also can be identified by the overhead of job costing

system. However, department of production can use this system, and track the entire job costing

in the business (Suomala and Lukka, 2014). It is the very useful system in the company for

controlling the cost. They can reduce their costing and increasing profitability from this

management accounting system.

P2 Presenting financial information

Types of managerial accounting reports: -

3

Illustration 1: Job costing report

(Sources : Job costing report, 2017)

Management accounting report help owner of Tech (UK) Limited and their managers to

monitor the performance of the organisation. It is the portion for making sure that organisation

has complete the presentation of business performance and their finance condition. There are

following managerial accounting report which is managed in the company:

Budget report: - It report is an interior study utilised by administration to analyse the

estimation, fund prediction with effective execution figure gained during a time period. In

the organisation, there are different types of department and employees are working. The

managers allot different types of work to their department and members. Main thing is,

they should analyse that department or employee's productivity is effective or not in the

business (Quinn, 2014). If they are not giving according to their target, then company

will reduce their budget on that department.

Job costing report: - This report shows all expenses for a specific project or department.

They analyse that a particular department is earning revenue or not. If they found that

they’re not getting revenue according to company's target,

then they can reduce budget on that department. In the Tech (UK) Limited, lots of

employees are working and managers allotted different types of task to them according to

their knowledge and profile. However, job costing report shows that the employee's

productivity is good or not (Messner, 2016). Other than that, their work is worth or not

for the organisation. If they will not able to give their effective service to the company

then, they cannot get the incentives and bonus from the organisation.

Account receivable aging: - This report mange the cash flow of Tech (UK) Limited. In

this report they are mention all data of credit. They are providing their credit services to

the customers. Sometime some costumers are not able to pay their outstanding amount on

time, so company can track record and know about the customers who are not able to pay

their pending amount. When they are not paying their amount them company can take

action against that customers. Other than that, there are the customers who can able to

pay their amount on time. This report is very useful in the Tech (UK) Limited, because

they are providing credit service to their dealer and customers.

Inventory and manufacturing report: - It is the very effective report in Tech (UK) Limited

organisation. In this report, mangers can manage their entire information data of the

business. When they import or export their goods, then they need to keep their entire data

4

monitor the performance of the organisation. It is the portion for making sure that organisation

has complete the presentation of business performance and their finance condition. There are

following managerial accounting report which is managed in the company:

Budget report: - It report is an interior study utilised by administration to analyse the

estimation, fund prediction with effective execution figure gained during a time period. In

the organisation, there are different types of department and employees are working. The

managers allot different types of work to their department and members. Main thing is,

they should analyse that department or employee's productivity is effective or not in the

business (Quinn, 2014). If they are not giving according to their target, then company

will reduce their budget on that department.

Job costing report: - This report shows all expenses for a specific project or department.

They analyse that a particular department is earning revenue or not. If they found that

they’re not getting revenue according to company's target,

then they can reduce budget on that department. In the Tech (UK) Limited, lots of

employees are working and managers allotted different types of task to them according to

their knowledge and profile. However, job costing report shows that the employee's

productivity is good or not (Messner, 2016). Other than that, their work is worth or not

for the organisation. If they will not able to give their effective service to the company

then, they cannot get the incentives and bonus from the organisation.

Account receivable aging: - This report mange the cash flow of Tech (UK) Limited. In

this report they are mention all data of credit. They are providing their credit services to

the customers. Sometime some costumers are not able to pay their outstanding amount on

time, so company can track record and know about the customers who are not able to pay

their pending amount. When they are not paying their amount them company can take

action against that customers. Other than that, there are the customers who can able to

pay their amount on time. This report is very useful in the Tech (UK) Limited, because

they are providing credit service to their dealer and customers.

Inventory and manufacturing report: - It is the very effective report in Tech (UK) Limited

organisation. In this report, mangers can manage their entire information data of the

business. When they import or export their goods, then they need to keep their entire data

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in very safe place (Lavia López and Hiebl, 2014). However, they are managing their

entire data of sales, purchase, return, and delivery are in inventory report. Along with

this, managers can compare entire data for one another, so they can get the report of

costing. This is very useful report for Tech (UK) Limited, and their managers are using

this report for tracking. They can evaluate the data from inventory report in the business.

It is very important in the organisation, and its helping in make decision,

forecasting cash flow, helping understand performance variances and analysing the rate of return.

Other than that, it helps managers in making a budget report for their business. Through this

entire managerial accounting report, company can keep their information in the secure place.

They can track information on records when they require.

M1 Evaluation of benefits

Tech (UK) Limited get lots of benefits from management accounting system and

reporting system. This is very useful and important for them. Through it, they can earn the more

profit in the organisation.

D1 Management accounting system assessment of and management reporting

This both process are different to one another Through management accounting system

they can improve their entire accounting system and through management reporting system, they

can make the all report of the organisation.

TASK 2

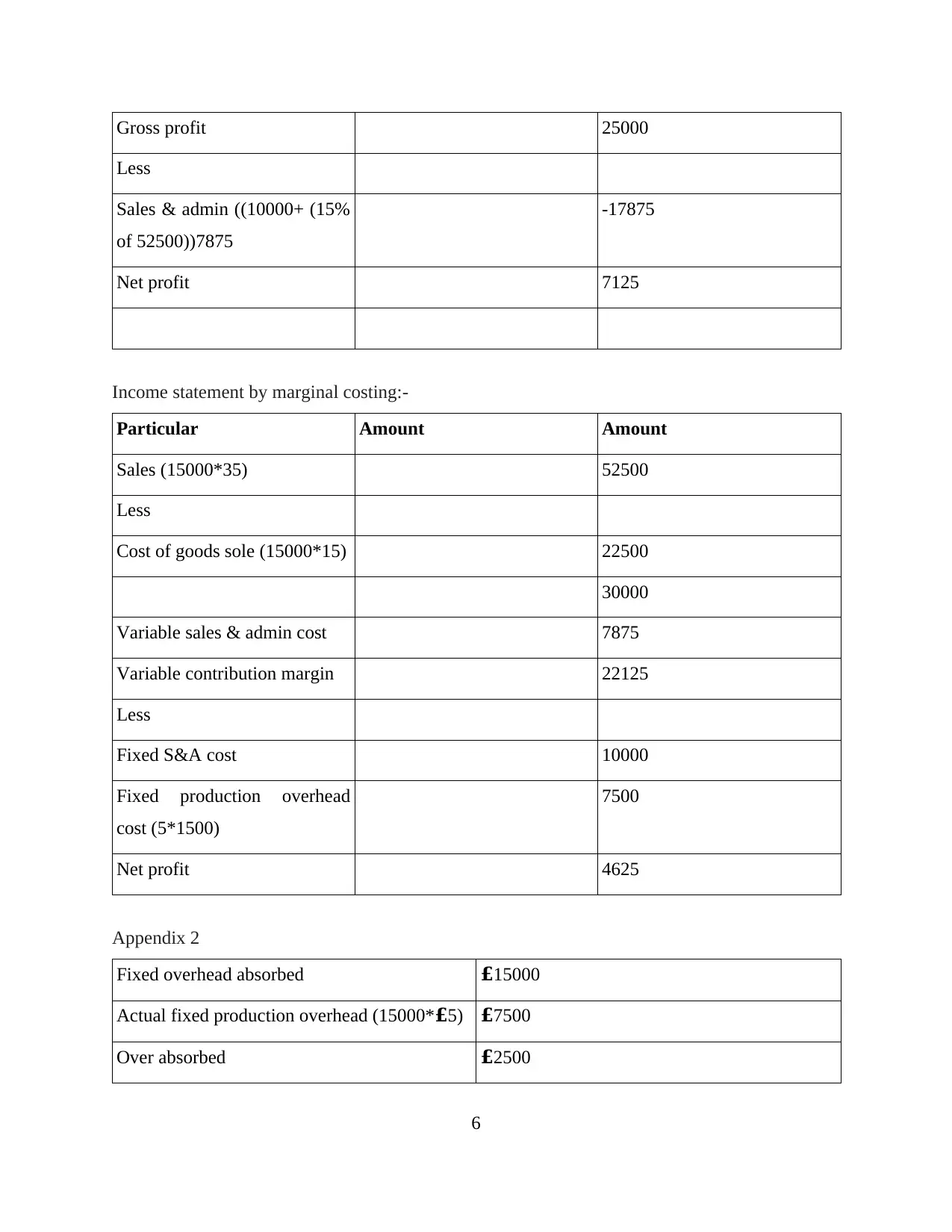

P3 Management accounting techniques:-

Income statement by absorption costing:-

Particular Amount Amount

Sales (1500*35) 52500

Less

Cost of goods sold

(1500*£20)

-30000

Adjustment for over

absorption

2500

5

entire data of sales, purchase, return, and delivery are in inventory report. Along with

this, managers can compare entire data for one another, so they can get the report of

costing. This is very useful report for Tech (UK) Limited, and their managers are using

this report for tracking. They can evaluate the data from inventory report in the business.

It is very important in the organisation, and its helping in make decision,

forecasting cash flow, helping understand performance variances and analysing the rate of return.

Other than that, it helps managers in making a budget report for their business. Through this

entire managerial accounting report, company can keep their information in the secure place.

They can track information on records when they require.

M1 Evaluation of benefits

Tech (UK) Limited get lots of benefits from management accounting system and

reporting system. This is very useful and important for them. Through it, they can earn the more

profit in the organisation.

D1 Management accounting system assessment of and management reporting

This both process are different to one another Through management accounting system

they can improve their entire accounting system and through management reporting system, they

can make the all report of the organisation.

TASK 2

P3 Management accounting techniques:-

Income statement by absorption costing:-

Particular Amount Amount

Sales (1500*35) 52500

Less

Cost of goods sold

(1500*£20)

-30000

Adjustment for over

absorption

2500

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross profit 25000

Less

Sales & admin ((10000+ (15%

of 52500))7875

-17875

Net profit 7125

Income statement by marginal costing:-

Particular Amount Amount

Sales (15000*35) 52500

Less

Cost of goods sole (15000*15) 22500

30000

Variable sales & admin cost 7875

Variable contribution margin 22125

Less

Fixed S&A cost 10000

Fixed production overhead

cost (5*1500)

7500

Net profit 4625

Appendix 2

Fixed overhead absorbed £15000

Actual fixed production overhead (15000*£5) £7500

Over absorbed £2500

6

Less

Sales & admin ((10000+ (15%

of 52500))7875

-17875

Net profit 7125

Income statement by marginal costing:-

Particular Amount Amount

Sales (15000*35) 52500

Less

Cost of goods sole (15000*15) 22500

30000

Variable sales & admin cost 7875

Variable contribution margin 22125

Less

Fixed S&A cost 10000

Fixed production overhead

cost (5*1500)

7500

Net profit 4625

Appendix 2

Fixed overhead absorbed £15000

Actual fixed production overhead (15000*£5) £7500

Over absorbed £2500

6

Appendix 3

Profit under absorption 7125

Difference in units: closing inventory (500units

*£5)

2500

Profit under marginal costing 4625

M2 Techniques and reconcile the profitability

There are two types of costing system, and thorough both system company can make a

report of income and statements. This both report shows proper figure of the P&L.

D2 Interpret data for the business activities

This entire figure of P&L statements can make by the marginal and absorption costing

system. It help company in showing the accurate data and reduce the cost of the organization.

TASK 3

P4 Various budget system

AS estimate costs, revenues, and resources over a specific time, reflective a reading of

upcoming fiscal conditions and goals. Budget is most important tool in the business, because

through it, company can able to make cash flow budget, capital and master budget, operating and

expenditure budget (Cullen and Gorst, 2013).

Cash flow budget:- This budget is a helpful management instrument because it forces

company to think their agriculture idea for the time period, and trial their agricultural

idea, such as if they will produces enough financial gain to meet all their cash demand.

This budget report maintain the entire cash of the organisation. Maintaining a cash flow

budget will help you forecast your company's entire financial health. Through it company

can make their another budget5, and provide them fund from this budget (Morales and

Lambert, 2013). It is very useful in the organisation. Cash flow budget based on

company's financial condition. If their condition of financial is good then they can

provide budget to the another depart.

Advantages and disadvantage:-

It is much direct as profit is extremely dependent on accounting conversations and concept. It is

able to satisfy the entire requirement of all customers better since cash flow is more direct its

7

Profit under absorption 7125

Difference in units: closing inventory (500units

*£5)

2500

Profit under marginal costing 4625

M2 Techniques and reconcile the profitability

There are two types of costing system, and thorough both system company can make a

report of income and statements. This both report shows proper figure of the P&L.

D2 Interpret data for the business activities

This entire figure of P&L statements can make by the marginal and absorption costing

system. It help company in showing the accurate data and reduce the cost of the organization.

TASK 3

P4 Various budget system

AS estimate costs, revenues, and resources over a specific time, reflective a reading of

upcoming fiscal conditions and goals. Budget is most important tool in the business, because

through it, company can able to make cash flow budget, capital and master budget, operating and

expenditure budget (Cullen and Gorst, 2013).

Cash flow budget:- This budget is a helpful management instrument because it forces

company to think their agriculture idea for the time period, and trial their agricultural

idea, such as if they will produces enough financial gain to meet all their cash demand.

This budget report maintain the entire cash of the organisation. Maintaining a cash flow

budget will help you forecast your company's entire financial health. Through it company

can make their another budget5, and provide them fund from this budget (Morales and

Lambert, 2013). It is very useful in the organisation. Cash flow budget based on

company's financial condition. If their condition of financial is good then they can

provide budget to the another depart.

Advantages and disadvantage:-

It is much direct as profit is extremely dependent on accounting conversations and concept. It is

able to satisfy the entire requirement of all customers better since cash flow is more direct its

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

messages. Cash flow budget provide effective satisfaction to the shareholders and management.

Disadvantage of this budget is that it avoid the accoutrement or matched conception.

Operating budget:- This budget is the combination of known expenses, expected future

costs, and fore castes income over the course of a year (Christ, 2014). It is very useful

budget for the company, because they require more fund for operating their all

departments. Operating budget is based on entire operational work and their department.

When managers will not get the appropriate productivity of the employees of different

department, then they can reduce their budget from operating system. So, they can able to

reduce their budget on the employees or department are not giving their effective

performance to the company. Their profit and revenues is depend on the employees and

department's productivity. If they will not give their effective performance then the

company will not be able to achieve their target and goals.

Advantages and disadvantage:-

Company can make their accountability great through operating budget system,. But their

information and time for managing can be very costly. Other than that, they can handle the all

expenses in good way, but they need more fund and more employees for the operating budget

and it can be expensive for the company. Through it, managers can projecting the expense3s of

future, and it will help organization in deceasing their expenses, but disadvantage of this is, that

company can not be sure that which types of expenses will be reduce in the future (Horton and

de Araujo Wanderley, C. 201).

Capital budget:- Capital budget is based on the capital receipts and payments. This

budget is also incorporates transaction in the public account. It is the process used by the

organisation for determine and ranking potential expenditure or investment that are

significant in amount. When they start their business, they require equipment, purchasing

vehicles, and buildings, so it all capital are expenditure capita. They can make a report for

this entire expenditure capital and analysis that it is worth or not for the company.

Advantages and disadvantage:-

This budgeting system helps an organisation to identify the different types of risk involved in an

investment opportunities. Other than that, they can know the risks affect the return of the

organisation (Fourie and Kumar, 2015). It assist to sort an advised decision about all investment

taking into circumstance all possible alternative. Disadvantage of capital budget is that capital

8

Disadvantage of this budget is that it avoid the accoutrement or matched conception.

Operating budget:- This budget is the combination of known expenses, expected future

costs, and fore castes income over the course of a year (Christ, 2014). It is very useful

budget for the company, because they require more fund for operating their all

departments. Operating budget is based on entire operational work and their department.

When managers will not get the appropriate productivity of the employees of different

department, then they can reduce their budget from operating system. So, they can able to

reduce their budget on the employees or department are not giving their effective

performance to the company. Their profit and revenues is depend on the employees and

department's productivity. If they will not give their effective performance then the

company will not be able to achieve their target and goals.

Advantages and disadvantage:-

Company can make their accountability great through operating budget system,. But their

information and time for managing can be very costly. Other than that, they can handle the all

expenses in good way, but they need more fund and more employees for the operating budget

and it can be expensive for the company. Through it, managers can projecting the expense3s of

future, and it will help organization in deceasing their expenses, but disadvantage of this is, that

company can not be sure that which types of expenses will be reduce in the future (Horton and

de Araujo Wanderley, C. 201).

Capital budget:- Capital budget is based on the capital receipts and payments. This

budget is also incorporates transaction in the public account. It is the process used by the

organisation for determine and ranking potential expenditure or investment that are

significant in amount. When they start their business, they require equipment, purchasing

vehicles, and buildings, so it all capital are expenditure capita. They can make a report for

this entire expenditure capital and analysis that it is worth or not for the company.

Advantages and disadvantage:-

This budgeting system helps an organisation to identify the different types of risk involved in an

investment opportunities. Other than that, they can know the risks affect the return of the

organisation (Fourie and Kumar, 2015). It assist to sort an advised decision about all investment

taking into circumstance all possible alternative. Disadvantage of capital budget is that capital

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budgeting decisions are for long term and mainly irreversible in nature. Other than that, this

method is based on the estimations, so it will not be able to provide accurate information to the

managers. A big disadvantage of capital budget is that a incorrect capital budgeting decision take

can impact the long term permanence of the organisation and therefore it requires to be dome

judiciously by the occupational group who understand the project well.

The budget formulation process:-

Understanding or budget strategies and preparation is , not just to deduct expenditure

protections. In this process, they need to know about framework of budget decisions, responsible

person for designing and ready the budget, know the primary steps . Other than that they should

need to know about critical imperfection in process and its overcome, and ways to changes in

budget plans (Klychova and Valieva, 2015).

When company need budget prepare process, then they should to follow the rules and

regulations of the budget preparation process. First step of this process is to understand, “What is

the model in which budget decisions are made”? However, they should to know about

framework and budget decision which they are made in the organisation. In this step, they should

know about the rules and regulations of the government in budget preparation process, and

through that rules they can identify the responsibilities for the elements of budget preparation

process. The second step of this process is recognise the useful of budget principles. They should

know about the separated economical and structural categorize that meet worldwide

standardized. After that, they can identify the responsibilities within the budget system. They can

distribute their budgeting system between executive and legislative branches. They can provide

some information to them like legislature quality to suggest spending, power of rectification and

executive power to limit spending appropriations. They can distribute their powers to the

executive and it is number of agencies involved in this system, structure of negotiations, and

agenda for setting budget negotiations. Along with this, they should know the ways of activities

funded (Schaltegger and Zvezdov, 2013). In this process they can use some activities for fund

and it is revenue accounts, borrowed resources, multiple, funds, special funds, contingency fund

etc. This all are the sources of fund, so company can easily borrow the fund from this activities.

If they will follow the entire activities of this process, then organisation can get their goals and

target of their business. Further, they should know about the person who takes the responsibility

for the designing and formulation of the budget. The responsibilities of formulating fund usually

9

method is based on the estimations, so it will not be able to provide accurate information to the

managers. A big disadvantage of capital budget is that a incorrect capital budgeting decision take

can impact the long term permanence of the organisation and therefore it requires to be dome

judiciously by the occupational group who understand the project well.

The budget formulation process:-

Understanding or budget strategies and preparation is , not just to deduct expenditure

protections. In this process, they need to know about framework of budget decisions, responsible

person for designing and ready the budget, know the primary steps . Other than that they should

need to know about critical imperfection in process and its overcome, and ways to changes in

budget plans (Klychova and Valieva, 2015).

When company need budget prepare process, then they should to follow the rules and

regulations of the budget preparation process. First step of this process is to understand, “What is

the model in which budget decisions are made”? However, they should to know about

framework and budget decision which they are made in the organisation. In this step, they should

know about the rules and regulations of the government in budget preparation process, and

through that rules they can identify the responsibilities for the elements of budget preparation

process. The second step of this process is recognise the useful of budget principles. They should

know about the separated economical and structural categorize that meet worldwide

standardized. After that, they can identify the responsibilities within the budget system. They can

distribute their budgeting system between executive and legislative branches. They can provide

some information to them like legislature quality to suggest spending, power of rectification and

executive power to limit spending appropriations. They can distribute their powers to the

executive and it is number of agencies involved in this system, structure of negotiations, and

agenda for setting budget negotiations. Along with this, they should know the ways of activities

funded (Schaltegger and Zvezdov, 2013). In this process they can use some activities for fund

and it is revenue accounts, borrowed resources, multiple, funds, special funds, contingency fund

etc. This all are the sources of fund, so company can easily borrow the fund from this activities.

If they will follow the entire activities of this process, then organisation can get their goals and

target of their business. Further, they should know about the person who takes the responsibility

for the designing and formulation of the budget. The responsibilities of formulating fund usually

9

lies with the government department of finance with input from the line government department

and few little disbursement agencies. They should know about the primary steps in fund

preparation method. The basic step in fund planning should be the examination of a

macroeconomic model for the budget year. The second step should be the allotment of this

worldwide among form government department, departure area of reserves to be managed by the

government department of finance. The 3rd step should be for the give direction about fund

section to set up a budget circular to line government department. The next step should be

comprises the negotiation, usually at official and then bilateral or collective ministerial level,

leading eventually to statement and the last step six is cabinet endorsement of the substance for

inclusion in the budget that will go to parliament.

M3 Analysis of different planning

There are different types of system for budget and they can use any of the budget system

for their organisation. They can make their own budget system from their managers so it will be

help company in comparison of both budget report.

D3 Evaluation of planning tools

This all budget report can resolve the problems of the company. If they will follow the

rules and regulations of budget report then they will be able to get accurate solutions of their

issues.

TASK 4

P5 Comparison the way of company are adapting management accounting system to respond

financial system

In the Tech (UK) Limited, they face different types of problems at their work place. They

have lots of competitor in the market, so they are facing some biggest problems in the market.

Their competitors are using management accounting report, budget report, and follow the budget

preparation process (McLaren and Mitchell, 2016). The thing is that, they are not able to know

about their processes, and they are facing the problem that they are not able to know the

situations of the business. Company can reduce this entire problems with effective solution. They

can adapts the management accounting system to react to financial problems.

Financial governance:- The consequences of failure can be devastating for a council is

the most effective for better governance. No substance how great the part of a council's

governance may be fiscal failure can bring in undone. In this system, government set the

10

and few little disbursement agencies. They should know about the primary steps in fund

preparation method. The basic step in fund planning should be the examination of a

macroeconomic model for the budget year. The second step should be the allotment of this

worldwide among form government department, departure area of reserves to be managed by the

government department of finance. The 3rd step should be for the give direction about fund

section to set up a budget circular to line government department. The next step should be

comprises the negotiation, usually at official and then bilateral or collective ministerial level,

leading eventually to statement and the last step six is cabinet endorsement of the substance for

inclusion in the budget that will go to parliament.

M3 Analysis of different planning

There are different types of system for budget and they can use any of the budget system

for their organisation. They can make their own budget system from their managers so it will be

help company in comparison of both budget report.

D3 Evaluation of planning tools

This all budget report can resolve the problems of the company. If they will follow the

rules and regulations of budget report then they will be able to get accurate solutions of their

issues.

TASK 4

P5 Comparison the way of company are adapting management accounting system to respond

financial system

In the Tech (UK) Limited, they face different types of problems at their work place. They

have lots of competitor in the market, so they are facing some biggest problems in the market.

Their competitors are using management accounting report, budget report, and follow the budget

preparation process (McLaren and Mitchell, 2016). The thing is that, they are not able to know

about their processes, and they are facing the problem that they are not able to know the

situations of the business. Company can reduce this entire problems with effective solution. They

can adapts the management accounting system to react to financial problems.

Financial governance:- The consequences of failure can be devastating for a council is

the most effective for better governance. No substance how great the part of a council's

governance may be fiscal failure can bring in undone. In this system, government set the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.