Management Accounting and Financial Analysis of Tech (UK) Ltd

VerifiedAdded on 2024/06/28

|25

|4396

|65

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Tech (UK) Limited. It defines management accounting and differentiates it from financial accounting, emphasizing its role in internal decision-making. The report explores various management accounting tools, including cost accounting systems (actual, normal, and standard), inventory management systems (FIFO, LIFO, AVCO), and job costing systems (batch, process, and service costing). It also discusses the types of managerial accounting reports, such as scheduled, exception, and demand reports, highlighting the importance of understandable information presentation. The benefits of management accounting for Tech (UK) Limited are outlined, including improved decision-making, performance analysis, and resource allocation. The report further examines the integration of management accounting systems with organizational processes and includes an income statement preparation using marginal and absorption costing techniques. Finally, it touches upon planning tools for budgeting and forecasting, as well as strategies for responding to financial problems and achieving sustainable success. Desklib offers a variety of resources, including solved assignments and past papers, to support students in their studies.

Unit 5 - Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:............................................................................................................................... 3

P1: Explanation of management accounting and the essential requirements of management

accounting system...................................................................................................................... 4

P2. Presenting financial information:.........................................................................................8

M1: Benefits of management accounting in Tech (UK) Limited:.........................................9

D1: Integration of management accounting systems and management accounting reporting

with organisational processes...............................................................................................10

P3. You are required to prepare income statements for the month of September...................11

M2. Reconciliation of profits:.............................................................................................. 15

D2. Accurately apply and interpret the data for the business activities...............................16

P4..............................................................................................................................................17

M3. Analyse the use of different planning tools in preparing and forecasting budgets.......19

P5. Explain ways by which the Balanced Scorecard approach suggested by the auditors can

be used to respond its financial problem and compare this approach to another management

accounting approach used in another organisation of your choice..........................................20

M4. How in responding to financial problems, management accounting can lead

organisations to sustainable success (D3)............................................................................21

Conclusion:.............................................................................................................................. 22

References:............................................................................................................................... 23

2

Introduction:............................................................................................................................... 3

P1: Explanation of management accounting and the essential requirements of management

accounting system...................................................................................................................... 4

P2. Presenting financial information:.........................................................................................8

M1: Benefits of management accounting in Tech (UK) Limited:.........................................9

D1: Integration of management accounting systems and management accounting reporting

with organisational processes...............................................................................................10

P3. You are required to prepare income statements for the month of September...................11

M2. Reconciliation of profits:.............................................................................................. 15

D2. Accurately apply and interpret the data for the business activities...............................16

P4..............................................................................................................................................17

M3. Analyse the use of different planning tools in preparing and forecasting budgets.......19

P5. Explain ways by which the Balanced Scorecard approach suggested by the auditors can

be used to respond its financial problem and compare this approach to another management

accounting approach used in another organisation of your choice..........................................20

M4. How in responding to financial problems, management accounting can lead

organisations to sustainable success (D3)............................................................................21

Conclusion:.............................................................................................................................. 22

References:............................................................................................................................... 23

2

Introduction:

The following report related with concepts and fundamentals of management accounting

helps the users in applying the methods and techniques in improving the business activity.

The various systems of management accounting will be identified and explained in order to

use them in performing the operations of business effectively and efficiently. The costing

techniques of management accounting consisting of absorption and marginal costing will be

applied to obtain per unit cost of production for company Tech (UK) Ltd. The technique of

costing will help the business managers in making costing decision of company. The report

will also include the explanation regarding various planning tools that can be utilized for the

purpose of budgeting and forecasting the business activities. The various techniques and tools

will also be identified for responding to financial problems in an organisation and this will

help in bating the long term sustainability in the business environment.

3

The following report related with concepts and fundamentals of management accounting

helps the users in applying the methods and techniques in improving the business activity.

The various systems of management accounting will be identified and explained in order to

use them in performing the operations of business effectively and efficiently. The costing

techniques of management accounting consisting of absorption and marginal costing will be

applied to obtain per unit cost of production for company Tech (UK) Ltd. The technique of

costing will help the business managers in making costing decision of company. The report

will also include the explanation regarding various planning tools that can be utilized for the

purpose of budgeting and forecasting the business activities. The various techniques and tools

will also be identified for responding to financial problems in an organisation and this will

help in bating the long term sustainability in the business environment.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P1: Explanation of management accounting and the essential requirements of

management accounting system

Definition of management accounting:

The management accounting can be defined as the branch of accounting in which various

tools and techniques are used in order to identify ad record the business transactions of the

company and presenting these information in a data format to the managers of company for

making economic decision. Thus it can be referred to as the tool of decision making for the

business managers of company. The reports will be presented in relation to different

departments and business activities of the business and the systems of management

accounting will help the managers in analysing and evaluating the business situation for

taking an efficient decision (Drury, 2015).

Financial accounting:

This will refer to the branch of accounting in which financial transactions are recorded and

ten financial reports are presented in a manner that the users will be able to evaluate and

analyse the financial position and performance of company for making their investment

decision.

Differences between management accounting and financial accounting:

Management accounting Financial accounting

The users of management accounting reports

are concerned with the internal activities of

the company and managing internal control

within the business.

The users of financial reporting are

associated with making investment decision

in the company (Edmonds & Olds, 2013).

The primary objective of management

accounting is to help busies s managers in

taking economic decision of company.

The objective here is to analyse financial

situation and making investment in the

company.

The frequency of reporting depends on the The frequency of reporting is either annually,

4

management accounting system

Definition of management accounting:

The management accounting can be defined as the branch of accounting in which various

tools and techniques are used in order to identify ad record the business transactions of the

company and presenting these information in a data format to the managers of company for

making economic decision. Thus it can be referred to as the tool of decision making for the

business managers of company. The reports will be presented in relation to different

departments and business activities of the business and the systems of management

accounting will help the managers in analysing and evaluating the business situation for

taking an efficient decision (Drury, 2015).

Financial accounting:

This will refer to the branch of accounting in which financial transactions are recorded and

ten financial reports are presented in a manner that the users will be able to evaluate and

analyse the financial position and performance of company for making their investment

decision.

Differences between management accounting and financial accounting:

Management accounting Financial accounting

The users of management accounting reports

are concerned with the internal activities of

the company and managing internal control

within the business.

The users of financial reporting are

associated with making investment decision

in the company (Edmonds & Olds, 2013).

The primary objective of management

accounting is to help busies s managers in

taking economic decision of company.

The objective here is to analyse financial

situation and making investment in the

company.

The frequency of reporting depends on the The frequency of reporting is either annually,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

perception of management and they will

prepare reports on their needs.

half yearly a quarterly reporting.

The data are prepared after taking into

consideration the future goals and forecasts

of the company (Edmonds & Olds, 2013).

The past information is the base of preparing

financial reports of company.

Importance of management accounting information as a decision-making tool for

department managers:

Information can be defined as the data which can be used for making decisions and

evaluating the assessing the current situation. The information utilized form various sources

are converted into data with the use of various management accounting systems.

Management accounting tools can be defined as those techniques and systems which help in

extracting useful information form the company and presenting them in an appropriate

manner to the business managers so that they can make efficient decisions. The importance of

these tools in decision making function can be explained as under:

In review of performance – In Tech (UK) Limited the management accounting tools

can be utilized to evaluate the existing performance and reviewing the efficient and

effectiveness with which the operations are being carried out (Drury, 2015).

Make or buy decision – The use of costing techniques like marginal costing will help

in assessing and identifying the relevant cost of manufacturing and accordingly make

or buy decisions can be taken for the company.

Pricing decision – The pricing decision regarding the selling prices of the products

and services offered by Tech (UK) Limited will be determined based on the

assessment performed and reports received in management accounting.

Cost accounting systems:

The cost accounting system in management accounting can be in the form of actual costing

system, normal costing system and standard costing system. The cost system will help in

identifying and classifying the cost based on nature and this will help in taking revenue

decision for the company.

5

prepare reports on their needs.

half yearly a quarterly reporting.

The data are prepared after taking into

consideration the future goals and forecasts

of the company (Edmonds & Olds, 2013).

The past information is the base of preparing

financial reports of company.

Importance of management accounting information as a decision-making tool for

department managers:

Information can be defined as the data which can be used for making decisions and

evaluating the assessing the current situation. The information utilized form various sources

are converted into data with the use of various management accounting systems.

Management accounting tools can be defined as those techniques and systems which help in

extracting useful information form the company and presenting them in an appropriate

manner to the business managers so that they can make efficient decisions. The importance of

these tools in decision making function can be explained as under:

In review of performance – In Tech (UK) Limited the management accounting tools

can be utilized to evaluate the existing performance and reviewing the efficient and

effectiveness with which the operations are being carried out (Drury, 2015).

Make or buy decision – The use of costing techniques like marginal costing will help

in assessing and identifying the relevant cost of manufacturing and accordingly make

or buy decisions can be taken for the company.

Pricing decision – The pricing decision regarding the selling prices of the products

and services offered by Tech (UK) Limited will be determined based on the

assessment performed and reports received in management accounting.

Cost accounting systems:

The cost accounting system in management accounting can be in the form of actual costing

system, normal costing system and standard costing system. The cost system will help in

identifying and classifying the cost based on nature and this will help in taking revenue

decision for the company.

5

Actual costing system – The actual costing system considers the actual cost incurred

for producing or manufacturing the products. The fixed overheads are allocated according to

the labour hours worked for each particular product.

Normal costing system – The normal costing system can be defined as the system of

costing in which only variable cost of producing or manufacturing the product will be

utilized for calculation of unit cost.

Standard costing system – This is the system of defining standard costs for

manufacturing the products or services and these costs will be taken to determine the

pricing policies of company.

Inventory management systems – The inventory management system of the company can

be referred to as the management accounting system in which the inventory items concerned

with work in progress and finished goods will be tracked and recorded for obtaining an

optimum level of inventory to be maintained in company. The system will help in achieving

economies of scale and low cost of production.

FIFO – The first in first out method of inventory costing system will consider the

oldest inventory cost for calculating the cost of production first.

LIFO – In this method latest cost of acquiring the inventory will be considered for

calculating cost of production for the company.

AVCO – Average cost of inventory will take the average cost of purchasing the

inventory in order to calculate cost of production (Horngren, et. al., 2013).

Job costing system – The job costing system of the company will refer to the system in

which various jobs will be identified in a decentralised organisation based on the customer

orders and costing statement will be prepared accordingly.

Batch costing – The system will be associated with cost system in which separate

batch will be established for each of the job to be performed in company and cost

classification will be made accordingly.

Process costing – The process costing system will be associated with the technique in

which various processes will be critically identified and observed to record the cost

activities and cost transactions.

Service costing – The costing system in which services are identified and costs are

determined based on those services.

6

for producing or manufacturing the products. The fixed overheads are allocated according to

the labour hours worked for each particular product.

Normal costing system – The normal costing system can be defined as the system of

costing in which only variable cost of producing or manufacturing the product will be

utilized for calculation of unit cost.

Standard costing system – This is the system of defining standard costs for

manufacturing the products or services and these costs will be taken to determine the

pricing policies of company.

Inventory management systems – The inventory management system of the company can

be referred to as the management accounting system in which the inventory items concerned

with work in progress and finished goods will be tracked and recorded for obtaining an

optimum level of inventory to be maintained in company. The system will help in achieving

economies of scale and low cost of production.

FIFO – The first in first out method of inventory costing system will consider the

oldest inventory cost for calculating the cost of production first.

LIFO – In this method latest cost of acquiring the inventory will be considered for

calculating cost of production for the company.

AVCO – Average cost of inventory will take the average cost of purchasing the

inventory in order to calculate cost of production (Horngren, et. al., 2013).

Job costing system – The job costing system of the company will refer to the system in

which various jobs will be identified in a decentralised organisation based on the customer

orders and costing statement will be prepared accordingly.

Batch costing – The system will be associated with cost system in which separate

batch will be established for each of the job to be performed in company and cost

classification will be made accordingly.

Process costing – The process costing system will be associated with the technique in

which various processes will be critically identified and observed to record the cost

activities and cost transactions.

Service costing – The costing system in which services are identified and costs are

determined based on those services.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2. Presenting financial information:

Different types of managerial accounting reports:

The various types of management reports are the sources which help in providing adequate

and accurate amount of data to the business managers in order to make efficient decision

making. The types of reports are presented below:

Scheduled reports – The scheduled reports are the form of management reports which helps

in extracting the data form multiple dashboards on a one time basis or on a recurring basis.

The scheduled reports will help the business managers in scheduling the operations in an

organised and systematic manner (Drury, 2015).

Exception reports – The exception reports in management accounting will refer to those

reports which highlight or reflect the abnormal items or those items which falls outside the

range specified in an efficient manner. The exception reports as prepared for the business

managers will help in providing knowledge about the controls required in operational

performance of the enterprise. Thus it can be an effective tool in controlling business

performance.

Demand reports – The demand reports can be represented as the type of reporting which is

prepared and presented on the demand of managers of company. The demand reports will be

required and prepared to solve a complex or specified problem.

Importance for the information to be presented in manner that must be

understandable:

The information presented in the management reports will be crucial in determining the

condition associated with financial performance and position of the company based on which

comparison can be made. The information thus should be presented in an appropriate and

understandable manner so that managers can easily understand the situation and take

decisions accordingly. The complexity in presentation of reports will make the decision

difficult for the investors and managers and this will lead to inaccurate decision making.

8

Different types of managerial accounting reports:

The various types of management reports are the sources which help in providing adequate

and accurate amount of data to the business managers in order to make efficient decision

making. The types of reports are presented below:

Scheduled reports – The scheduled reports are the form of management reports which helps

in extracting the data form multiple dashboards on a one time basis or on a recurring basis.

The scheduled reports will help the business managers in scheduling the operations in an

organised and systematic manner (Drury, 2015).

Exception reports – The exception reports in management accounting will refer to those

reports which highlight or reflect the abnormal items or those items which falls outside the

range specified in an efficient manner. The exception reports as prepared for the business

managers will help in providing knowledge about the controls required in operational

performance of the enterprise. Thus it can be an effective tool in controlling business

performance.

Demand reports – The demand reports can be represented as the type of reporting which is

prepared and presented on the demand of managers of company. The demand reports will be

required and prepared to solve a complex or specified problem.

Importance for the information to be presented in manner that must be

understandable:

The information presented in the management reports will be crucial in determining the

condition associated with financial performance and position of the company based on which

comparison can be made. The information thus should be presented in an appropriate and

understandable manner so that managers can easily understand the situation and take

decisions accordingly. The complexity in presentation of reports will make the decision

difficult for the investors and managers and this will lead to inaccurate decision making.

8

M1: Benefits of management accounting in Tech (UK) Limited:

Better decision making – It can be observed that the company Tech (UK) Limited has

been looking forward to expand its business operations and therefore the management needs

to plan the strategic direction of the company in order to achieve better results. The tools of

management accounting will help the enterprise in achieving efficient decisions for the

company.

Analysing and evaluating current situation of the company – The various reports

prepared in management accounting will help the enterprise and managers to evaluate the

current situation and compare these with the current trends. This will help in identifying the

loopholes in efficient operational system and thus better results can be obtained (Horngren,

et. al., 2013).

Allocation of adequate resources and better funding options – The use of management

accounting will help the business in utilizing adequate sources of finances for the company

and this will assist in achieving maximum utilization of resources and low cost of capital.

9

Better decision making – It can be observed that the company Tech (UK) Limited has

been looking forward to expand its business operations and therefore the management needs

to plan the strategic direction of the company in order to achieve better results. The tools of

management accounting will help the enterprise in achieving efficient decisions for the

company.

Analysing and evaluating current situation of the company – The various reports

prepared in management accounting will help the enterprise and managers to evaluate the

current situation and compare these with the current trends. This will help in identifying the

loopholes in efficient operational system and thus better results can be obtained (Horngren,

et. al., 2013).

Allocation of adequate resources and better funding options – The use of management

accounting will help the business in utilizing adequate sources of finances for the company

and this will assist in achieving maximum utilization of resources and low cost of capital.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D1: Integration of management accounting systems and management accounting

reporting with organisational processes.

The integration of management accounting systems and reporting can be achieved in the

following manner:

The systems of management accounting should be linked and integrated with

financial reporting system of the enterprise Tech (UK) Limited so that accurate financial

reports can be prepared and presented adequate for the business managers.

The communication between the reporting managers and the system managers should

be efficient enough in order to create a sound reporting system in the company.

The integration will help the business managers in selecting an appropriate option of

financing for the company Tech (UK) Limited and decision regarding allocation of financial

resources can be optimum for the company (Horngren, et. al., 2013).

10

reporting with organisational processes.

The integration of management accounting systems and reporting can be achieved in the

following manner:

The systems of management accounting should be linked and integrated with

financial reporting system of the enterprise Tech (UK) Limited so that accurate financial

reports can be prepared and presented adequate for the business managers.

The communication between the reporting managers and the system managers should

be efficient enough in order to create a sound reporting system in the company.

The integration will help the business managers in selecting an appropriate option of

financing for the company Tech (UK) Limited and decision regarding allocation of financial

resources can be optimum for the company (Horngren, et. al., 2013).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

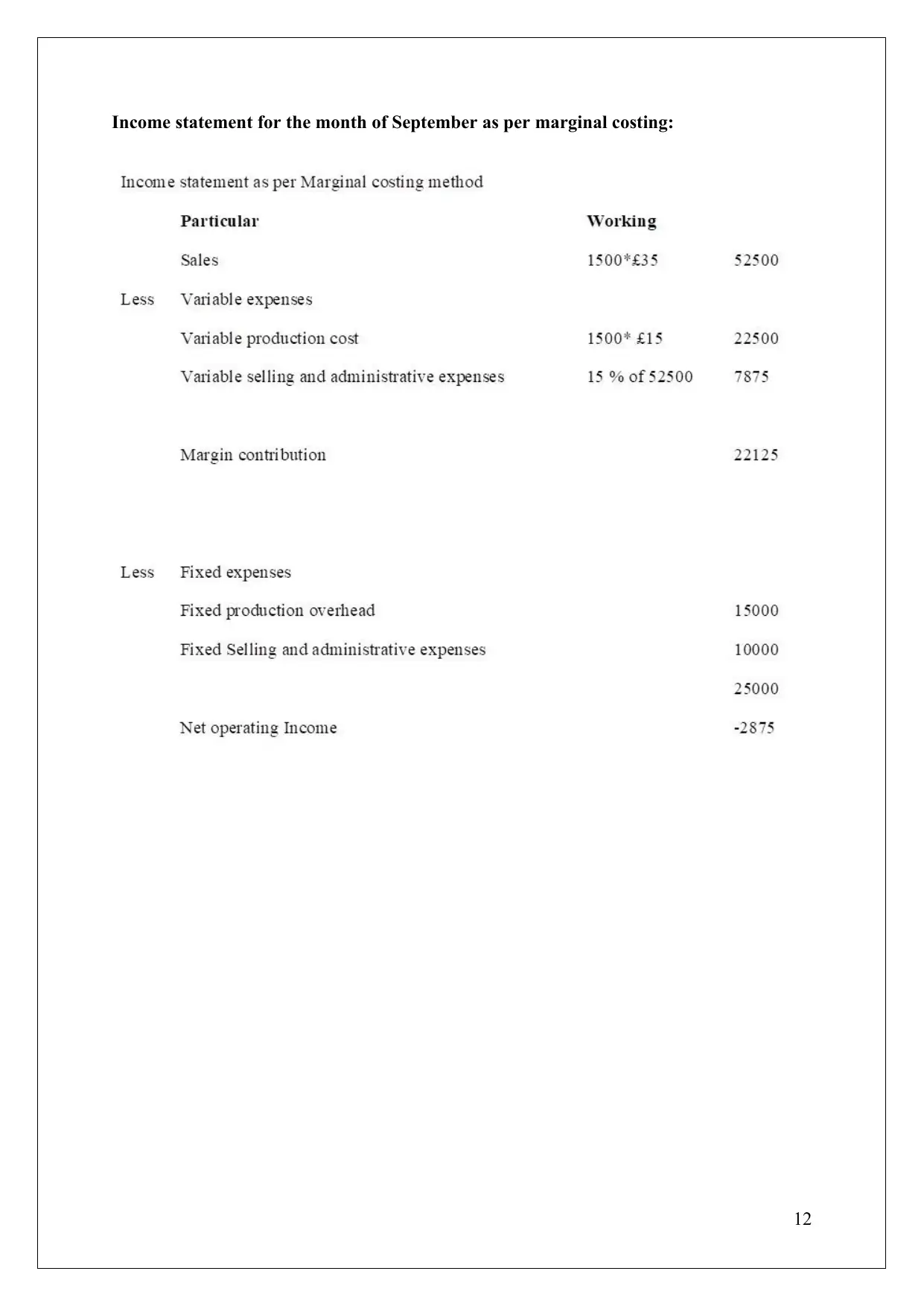

P3. You are required to prepare income statements for the month of September.

Marginal costing:

The marginal costing technique of management accounting is concerned with the costing

system in which all the variable cost of manufacturing the products and services will be

considered for calculation of per unit cost of production for the company. This will help the

business managers in obtaining the knowledge about the relevant cost of manufacturing the

product and the costing decision can be taken accordingly. The preparation of marginal

costing statement will require calculating contribution achieved form the product and this will

help in determining the fixed cost component in the company and the profit desired to be

achieved.

Absorption costing:

The absorption costing technique of management accounting can be referred to as the system

of costing in which all the cost associated with production of goods and services consisting of

fixed and variable cost of production will be considered for calculating the unit cost of

production for the company. The gross profit will be determined after deducting expenses

form the associated revenues of company and the net profit will be determined after

deducting the operating expenses from the gross profit acquired by company. The absorption

costing method allocated the overheads on the basis of predetermined absorption rate

determined by the company. The type of costing method will allow the business managers in

obtaining knowledge about the cost of production of company (Horngren, et. al., 2013).

11

Marginal costing:

The marginal costing technique of management accounting is concerned with the costing

system in which all the variable cost of manufacturing the products and services will be

considered for calculation of per unit cost of production for the company. This will help the

business managers in obtaining the knowledge about the relevant cost of manufacturing the

product and the costing decision can be taken accordingly. The preparation of marginal

costing statement will require calculating contribution achieved form the product and this will

help in determining the fixed cost component in the company and the profit desired to be

achieved.

Absorption costing:

The absorption costing technique of management accounting can be referred to as the system

of costing in which all the cost associated with production of goods and services consisting of

fixed and variable cost of production will be considered for calculating the unit cost of

production for the company. The gross profit will be determined after deducting expenses

form the associated revenues of company and the net profit will be determined after

deducting the operating expenses from the gross profit acquired by company. The absorption

costing method allocated the overheads on the basis of predetermined absorption rate

determined by the company. The type of costing method will allow the business managers in

obtaining knowledge about the cost of production of company (Horngren, et. al., 2013).

11

Income statement for the month of September as per marginal costing:

12

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.