Detailed Analysis of Management Accounting Systems and Techniques

VerifiedAdded on 2021/02/20

|21

|5729

|29

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques, focusing on Bright Star, a financial organization in the UK. The report covers various aspects of management accounting, including different types of systems such as inventory management, price optimization, and cost accounting. It delves into the roles and principles of management accounting, comparing it with financial accounting. Furthermore, the report elaborates on diverse reporting methods like inventory management reports, accounts receivable ageing reports, performance reports, and budget reports. The report also explores cost analysis techniques, including cost volume profit analysis, flexible budgeting, and cost variance, with a detailed explanation of absorption and marginal costing. Finally, the report discusses the advantages and disadvantages of budgetary control tools and compares how organizations adapt management accounting systems to address financial problems.

Management

Accounting Systems and

Techniques

Accounting Systems and

Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1 Explanation of management accounting along with assorted types of systems....................1

P2 Elaborate diverse methods of management accounting reporting.........................................4

Task 2...............................................................................................................................................5

P3 Figure out cost by the usage of cost analysis techniques by making useof absorption as

well as marginal costs.................................................................................................................5

TASK 3............................................................................................................................................1

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control........................................................................................................................1

TASK 4............................................................................................................................................4

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems. .....................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

.........................................................................................................................................................7

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1 Explanation of management accounting along with assorted types of systems....................1

P2 Elaborate diverse methods of management accounting reporting.........................................4

Task 2...............................................................................................................................................5

P3 Figure out cost by the usage of cost analysis techniques by making useof absorption as

well as marginal costs.................................................................................................................5

TASK 3............................................................................................................................................1

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control........................................................................................................................1

TASK 4............................................................................................................................................4

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems. .....................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................7

.........................................................................................................................................................7

INTRODUCTION

Management accounting is also referred to cost or managerial accounting. It is a process

of analysation of business cost along with operations for preparing internal financial records,

report as well as aids management within decision-making activities that assist in attainment of

business goals (Aldehayyat and Maan, 2013). It is the presentation of accounting information for

formulation of policies that must be opted by management for carrying out their everyday

activities. This report is based on Bright Star which is a financial organisation and is in United

Kingdom. They serve diverse organisations which deals in retail, manufacturing, food & safety

and various others. Stitchland Ltd is one of them who deals with manufacturing of clothes and

takes assistance from Bright star for carrying out their finances. This report deals with

management accounting along different types of its systems. In addition to this, diverse methods

are used and cost analysis is carried out for preparation of income statements. Furthermore, their

advantages as well as disadvantages have been illustrated with respect to budgetary control.

Apart from this, management accounting systems will be compared.

Task 1

P1 Explanation of management accounting along with assorted types of systems.

Management accounting: It is known as managerial accounting and it refers to a

process that furnish financial information and resources to managers of organisation within

decision-making process (Anandarajan, Anandarajan and Srinivasan, 2012). This is utilised

within internal teams of organisation as this is the only method which makes organisation

different from financial accounting. For an example, Stitchland Ltd organisation can make use of

this kind of accounting system for carrying out their operations within process associated with

manufacturing.

Management accounting system: This refers to system that comprises of internal

system and is used by organisation for measurement as well as evaluation of their performance.

The major objective of suck kind of systems is to render appropriate information to managers by

which they can carry out effectual decisions. So, Stitchland Ltd needs to make use of accounting

systems so that they can have specific data for development of effectual decisions (Christ and

Burritt, 2013). It is crucial tool as it comprises financial and non-financial information that aids

within business management.

1

Management accounting is also referred to cost or managerial accounting. It is a process

of analysation of business cost along with operations for preparing internal financial records,

report as well as aids management within decision-making activities that assist in attainment of

business goals (Aldehayyat and Maan, 2013). It is the presentation of accounting information for

formulation of policies that must be opted by management for carrying out their everyday

activities. This report is based on Bright Star which is a financial organisation and is in United

Kingdom. They serve diverse organisations which deals in retail, manufacturing, food & safety

and various others. Stitchland Ltd is one of them who deals with manufacturing of clothes and

takes assistance from Bright star for carrying out their finances. This report deals with

management accounting along different types of its systems. In addition to this, diverse methods

are used and cost analysis is carried out for preparation of income statements. Furthermore, their

advantages as well as disadvantages have been illustrated with respect to budgetary control.

Apart from this, management accounting systems will be compared.

Task 1

P1 Explanation of management accounting along with assorted types of systems.

Management accounting: It is known as managerial accounting and it refers to a

process that furnish financial information and resources to managers of organisation within

decision-making process (Anandarajan, Anandarajan and Srinivasan, 2012). This is utilised

within internal teams of organisation as this is the only method which makes organisation

different from financial accounting. For an example, Stitchland Ltd organisation can make use of

this kind of accounting system for carrying out their operations within process associated with

manufacturing.

Management accounting system: This refers to system that comprises of internal

system and is used by organisation for measurement as well as evaluation of their performance.

The major objective of suck kind of systems is to render appropriate information to managers by

which they can carry out effectual decisions. So, Stitchland Ltd needs to make use of accounting

systems so that they can have specific data for development of effectual decisions (Christ and

Burritt, 2013). It is crucial tool as it comprises financial and non-financial information that aids

within business management.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Importance to integrate different accounting systems within the organisations: Diverse

kinds of accounting systems exists which will aid Stitchland Ltd organisation. For an instance,

cost accounting system will assist within computation of cost along with inventory management

system that can be utilised within effectual management of stocks. Along with this, price

optimisation systems furnish a framework for determination of prices (Cohen and Karatzimas,

2013). This denotes that these accounting systems for their own significance.

Origin, role as well as principles of management accounting:

As per the history, they are being developed in England before as well as during

industrial revolution. It comprises of implementation o0f diverse tasks within series for

enhancing financial problems associated with organisation. Principles of management accounting

deals with relevance, influence as well as formulation of trust with respect to organisational

orientation.

Difference Between Management Accounting and Financial Accounting:

Management Accounting Financial Accounting

The aim is to render qualitative as well as

quantitative information to managers for

assisting them to formulate decisions.

In this case, goal is to provide accurate and just

financial position of the organisation to diverse

parties.

This is being used within internal reporting

such as report to CEO, managers.

It is utilised for external reporting and basically

for stakeholders.

They are not regulated by any kind of law as

well as confined to audit.

It has to be conferred according to specified

standards as well as their financial reports

needs to be audited.

There do not exist any kind of defined

frequency for generating reports and they can

be furnished wither quarterly, monthly or

weekly.

Financial reports are created at the end of

financial year (Cooper, 2017).

Diverse kinds of management accounting systems have been elaborated below:

Inventory management system: Such kind of systems are taken into consideration for

tracking movements of services as well as products into an entire procedures. It assists in

2

kinds of accounting systems exists which will aid Stitchland Ltd organisation. For an instance,

cost accounting system will assist within computation of cost along with inventory management

system that can be utilised within effectual management of stocks. Along with this, price

optimisation systems furnish a framework for determination of prices (Cohen and Karatzimas,

2013). This denotes that these accounting systems for their own significance.

Origin, role as well as principles of management accounting:

As per the history, they are being developed in England before as well as during

industrial revolution. It comprises of implementation o0f diverse tasks within series for

enhancing financial problems associated with organisation. Principles of management accounting

deals with relevance, influence as well as formulation of trust with respect to organisational

orientation.

Difference Between Management Accounting and Financial Accounting:

Management Accounting Financial Accounting

The aim is to render qualitative as well as

quantitative information to managers for

assisting them to formulate decisions.

In this case, goal is to provide accurate and just

financial position of the organisation to diverse

parties.

This is being used within internal reporting

such as report to CEO, managers.

It is utilised for external reporting and basically

for stakeholders.

They are not regulated by any kind of law as

well as confined to audit.

It has to be conferred according to specified

standards as well as their financial reports

needs to be audited.

There do not exist any kind of defined

frequency for generating reports and they can

be furnished wither quarterly, monthly or

weekly.

Financial reports are created at the end of

financial year (Cooper, 2017).

Diverse kinds of management accounting systems have been elaborated below:

Inventory management system: Such kind of systems are taken into consideration for

tracking movements of services as well as products into an entire procedures. It assists in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

evaluation of raw materials as well as finished goods which will assist organisation to

carry out production accordingly. Along with this, it will alleviate a way through which

demand as well as supply of services or products can be met. Its key function is to

maintain records of entire products that have been transferred into the warehouse (Daoud

and Triki, 2013). Stitchland Ltd is making use of this accounting system in diverse

services so that they enhance their productivity within specified time duration.

Price optimisation system: It is a type of accounting system which renders a basis for

determination of prices at an effectual level. It is responsible for allotment of prices by

taking into consideration cost as well as needed profit by taking into consideration

satisfaction of their customers. When prices offered by Stitchland Ltd will be fixed then it

will enable them to grab attention of ample number of customers.

Cost accounting system: It denotes accounting system that is also referred to costing

system. It is liable for rendering a framework for figuring out cost of products as well as

services. Along with this, due to accounting systems organisation compute overall cost

associated with production as well as services. Finally, it is serviceable for organisation

that carry out their operations within manufacturing sector. For an instance, Stitchland

Ltd organisation have executed these systems for management as well as controlling

entire cost related with production of clothes (Dillard and Yuthas, 2013). It is crucial for

organisation to predict entire cost as well as evaluate profitability which has been attained

by rendering services.

Job costing system: It is a system that is obligated for assigning and computing of cost

related with assorted activities separately. Finally, this accounting system will be helpful

in entities where there are lot of activities and jobs that have to be carried out. With

respect to Stitchland Ltd, accounting system are effectual as organisation can have

information related with cost of job within manufacturing activities.

Assets of management accounting systems:

Management accounting system comprises of different types of systems and each possess

their own importance. Stichland Ltd makes use of diverse management accounting systems, their

significance has been illustrated below:

Cost accounting system: Through this entire cost of system can be calculated with

respect to activities and operations that have been carried out (DRURY, 2013). It is necessary for

3

carry out production accordingly. Along with this, it will alleviate a way through which

demand as well as supply of services or products can be met. Its key function is to

maintain records of entire products that have been transferred into the warehouse (Daoud

and Triki, 2013). Stitchland Ltd is making use of this accounting system in diverse

services so that they enhance their productivity within specified time duration.

Price optimisation system: It is a type of accounting system which renders a basis for

determination of prices at an effectual level. It is responsible for allotment of prices by

taking into consideration cost as well as needed profit by taking into consideration

satisfaction of their customers. When prices offered by Stitchland Ltd will be fixed then it

will enable them to grab attention of ample number of customers.

Cost accounting system: It denotes accounting system that is also referred to costing

system. It is liable for rendering a framework for figuring out cost of products as well as

services. Along with this, due to accounting systems organisation compute overall cost

associated with production as well as services. Finally, it is serviceable for organisation

that carry out their operations within manufacturing sector. For an instance, Stitchland

Ltd organisation have executed these systems for management as well as controlling

entire cost related with production of clothes (Dillard and Yuthas, 2013). It is crucial for

organisation to predict entire cost as well as evaluate profitability which has been attained

by rendering services.

Job costing system: It is a system that is obligated for assigning and computing of cost

related with assorted activities separately. Finally, this accounting system will be helpful

in entities where there are lot of activities and jobs that have to be carried out. With

respect to Stitchland Ltd, accounting system are effectual as organisation can have

information related with cost of job within manufacturing activities.

Assets of management accounting systems:

Management accounting system comprises of different types of systems and each possess

their own importance. Stichland Ltd makes use of diverse management accounting systems, their

significance has been illustrated below:

Cost accounting system: Through this entire cost of system can be calculated with

respect to activities and operations that have been carried out (DRURY, 2013). It is necessary for

3

Stitchland Ltd organisation to measure accurate profit that has been earned by them by carrying

out comparison of incurred cost with amount that has been attained.

Inventory management system: This system is responsible for tracing movements of

services or products that are responsible for carrying out inventory management with respect to

stock that is available within warehouse. In context of Stitchland Ltd, this will assist them to

check that raw material is available and can be used for furnishing final product.

Price optimisation system: It assists in determination of prices of goods and services.

Within Stitchland Ltd, it will alleviate them to have a structure for assigning products with their

prices. Along with this, it will aid them to examine the influence on customers with respect to

amount for specified services (Hall, 2012).

Job costing system: This system can be used for furnishing information related with cost

of each job respectively. Along with this, it will aid them to have data related with amount

required for carrying out various activities within production process of Stitchland Ltd

organisation.

P2 Elaborate diverse methods of management accounting reporting.

Management accounting reporting is liable for management accountant which renders

direction to higher level management through which effectual decisions with respect to business

can be carried out. These reports can be utilised by management for evaluation of performance of

employees. Some of these are illustrated below:

Inventory management report: This is a crucial activity of management accountant for

preparation of report as it gives entire information related with inventory of Stitchland Ltd like

cost of storage, closing stock, etc. Inventory management report also renders information related

with methods that are valuable for closing the stock (Harrison and Lock, 2017). The major

objective of such kind of reports is to furnish balance in between customer services along with

inventory investment.

Accounts receivable ageing report: This report furnish details related with invoices that

are provided to customers with respect to credits that will aid Stitchland Ltd to find unpaid

customers amount as well as unpaid credit memos. This is a original tool that can be used for

determination of effectualness of credit, overdue for payment as well as gathering of functions.

Performance report: It is developed for carrying out performance measurement of their

employees and has been carried out by management accountant with respect to detailed

4

out comparison of incurred cost with amount that has been attained.

Inventory management system: This system is responsible for tracing movements of

services or products that are responsible for carrying out inventory management with respect to

stock that is available within warehouse. In context of Stitchland Ltd, this will assist them to

check that raw material is available and can be used for furnishing final product.

Price optimisation system: It assists in determination of prices of goods and services.

Within Stitchland Ltd, it will alleviate them to have a structure for assigning products with their

prices. Along with this, it will aid them to examine the influence on customers with respect to

amount for specified services (Hall, 2012).

Job costing system: This system can be used for furnishing information related with cost

of each job respectively. Along with this, it will aid them to have data related with amount

required for carrying out various activities within production process of Stitchland Ltd

organisation.

P2 Elaborate diverse methods of management accounting reporting.

Management accounting reporting is liable for management accountant which renders

direction to higher level management through which effectual decisions with respect to business

can be carried out. These reports can be utilised by management for evaluation of performance of

employees. Some of these are illustrated below:

Inventory management report: This is a crucial activity of management accountant for

preparation of report as it gives entire information related with inventory of Stitchland Ltd like

cost of storage, closing stock, etc. Inventory management report also renders information related

with methods that are valuable for closing the stock (Harrison and Lock, 2017). The major

objective of such kind of reports is to furnish balance in between customer services along with

inventory investment.

Accounts receivable ageing report: This report furnish details related with invoices that

are provided to customers with respect to credits that will aid Stitchland Ltd to find unpaid

customers amount as well as unpaid credit memos. This is a original tool that can be used for

determination of effectualness of credit, overdue for payment as well as gathering of functions.

Performance report: It is developed for carrying out performance measurement of their

employees and has been carried out by management accountant with respect to detailed

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statements that comprises of incentives that are being given employees with respect to

performance appraisals. This will lead to motivate employees of Stitchland Ltd and work in an

effectual manner along with this bonus and training is given to their working employees.

Budget Report: It is given by management of Stitchland Ltd with respect to their future

business operations as it will aid them to identify their exact business operations and according

to that they can take corrective actions for rendering benefits to overall operations of

organisation (Hitomi, 2017). It will give details about incentives that are being given employees,

if they carry out their operations in an affirmative way with respect to standards. This report will

aid organisation to ensure that resources of organisation are utilised in an appropriate manner for

improvisation of organisation.

Task 2

P3 Figure out cost by the usage of cost analysis techniques by making useof absorption as well

as marginal costs.

Cost: It denotes addition of overall expenditures which have occurred in diverse kinds of

operations as well as activities of organisation. It can be further divided into diverse categories

variable, fixed, direct and indirect, etc. Different types of costs occurs within Stitchland Ltd

organisation for an instance labour, material, cost associated with suppliers, etc. It denotes entire

process that is associated with computation of entire cost of diverse activities by which cost of

each activity is identified.

Cost volume profit analysis: It is an analysis technique that is linked with analysing

deviation within profits and cost. The primary objective of such kind of analysis is to identify

financial situations of organisation according to variance within volume as well as cost. In case

of Stitchland Ltd the difference in between these two factors can be evaluated by carrying out

analysis.

Flexible budgeting: It denotes a budgeting technique in which values of budget can be

altered with respect to volume and sales (Ismail and King, 2014). In context of Stitchland Ltd

organisation, they can make use of this budgeting method for changing the relationship in

between sales of clothes that have been taken place.

5

performance appraisals. This will lead to motivate employees of Stitchland Ltd and work in an

effectual manner along with this bonus and training is given to their working employees.

Budget Report: It is given by management of Stitchland Ltd with respect to their future

business operations as it will aid them to identify their exact business operations and according

to that they can take corrective actions for rendering benefits to overall operations of

organisation (Hitomi, 2017). It will give details about incentives that are being given employees,

if they carry out their operations in an affirmative way with respect to standards. This report will

aid organisation to ensure that resources of organisation are utilised in an appropriate manner for

improvisation of organisation.

Task 2

P3 Figure out cost by the usage of cost analysis techniques by making useof absorption as well

as marginal costs.

Cost: It denotes addition of overall expenditures which have occurred in diverse kinds of

operations as well as activities of organisation. It can be further divided into diverse categories

variable, fixed, direct and indirect, etc. Different types of costs occurs within Stitchland Ltd

organisation for an instance labour, material, cost associated with suppliers, etc. It denotes entire

process that is associated with computation of entire cost of diverse activities by which cost of

each activity is identified.

Cost volume profit analysis: It is an analysis technique that is linked with analysing

deviation within profits and cost. The primary objective of such kind of analysis is to identify

financial situations of organisation according to variance within volume as well as cost. In case

of Stitchland Ltd the difference in between these two factors can be evaluated by carrying out

analysis.

Flexible budgeting: It denotes a budgeting technique in which values of budget can be

altered with respect to volume and sales (Ismail and King, 2014). In context of Stitchland Ltd

organisation, they can make use of this budgeting method for changing the relationship in

between sales of clothes that have been taken place.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost variance: It refers to alteration within figured cost along with existent cost that has

been occurred. With respect to Stitchland Ltd, they need to examine the deviation in between

existent as well as computed cost of manufacturing (Lavia López and Hiebl, 2014).

Absorption & marginal costing:

Absorption costing: It is a kind of a costing technique in which both fixed as well as

variable costing are taken into account as a cost of product.

Marginal costing: This technique of costing is not similar to absorption costing instead

in this, variable cost is considered as unit case and in other hand fixed cost is given as period

cost.

Cost allocation: It refers to a process of allocation of overheads according to the

activities. Like in this case, Stitchland Ltd allot their expenditure according to various activities

associated with production (Namakonzi and Inanga, 2014).

Fixed cost: This is not based on level of output rather it is a kind of a which do not alter

with variation within quantity of production as well as sales. Fixed costs are rent, payment on

loans, insurance, etc.

Variable cost: It denotes a kind of cost that is associated with variance within production

along with sales that been incurred within Stitchland Ltd. This denotes that entire cost has

assorted nature with respect to fixed cost. They comprises of material cost, variable overhead.

Normal costing: It comprises of cost of products that also includes material cost, labour

cost along with other cost which took place within an organisation.

Standard costing: This is a standard cost that can be expected in terms of future aspects

for diverse activities. It takes place with respect to comparison in between actual performances.

Like in case Stitchland Ltd, they are making use of costing for measurement of exact cost.

Activity based costing: This activity is dependent on kinds of costing system that have

been assigned to diverse activities respectively.

Inventory cost: It is a type of cost that comprises of cost of storing, carrying as well as

ordering and various others (Ross, 2017). With respect to Stitchland Ltd, they figure out cost

associated with inventory by which they are able to manage entire cost.

Valuation methods:

6

been occurred. With respect to Stitchland Ltd, they need to examine the deviation in between

existent as well as computed cost of manufacturing (Lavia López and Hiebl, 2014).

Absorption & marginal costing:

Absorption costing: It is a kind of a costing technique in which both fixed as well as

variable costing are taken into account as a cost of product.

Marginal costing: This technique of costing is not similar to absorption costing instead

in this, variable cost is considered as unit case and in other hand fixed cost is given as period

cost.

Cost allocation: It refers to a process of allocation of overheads according to the

activities. Like in this case, Stitchland Ltd allot their expenditure according to various activities

associated with production (Namakonzi and Inanga, 2014).

Fixed cost: This is not based on level of output rather it is a kind of a which do not alter

with variation within quantity of production as well as sales. Fixed costs are rent, payment on

loans, insurance, etc.

Variable cost: It denotes a kind of cost that is associated with variance within production

along with sales that been incurred within Stitchland Ltd. This denotes that entire cost has

assorted nature with respect to fixed cost. They comprises of material cost, variable overhead.

Normal costing: It comprises of cost of products that also includes material cost, labour

cost along with other cost which took place within an organisation.

Standard costing: This is a standard cost that can be expected in terms of future aspects

for diverse activities. It takes place with respect to comparison in between actual performances.

Like in case Stitchland Ltd, they are making use of costing for measurement of exact cost.

Activity based costing: This activity is dependent on kinds of costing system that have

been assigned to diverse activities respectively.

Inventory cost: It is a type of cost that comprises of cost of storing, carrying as well as

ordering and various others (Ross, 2017). With respect to Stitchland Ltd, they figure out cost

associated with inventory by which they are able to manage entire cost.

Valuation methods:

6

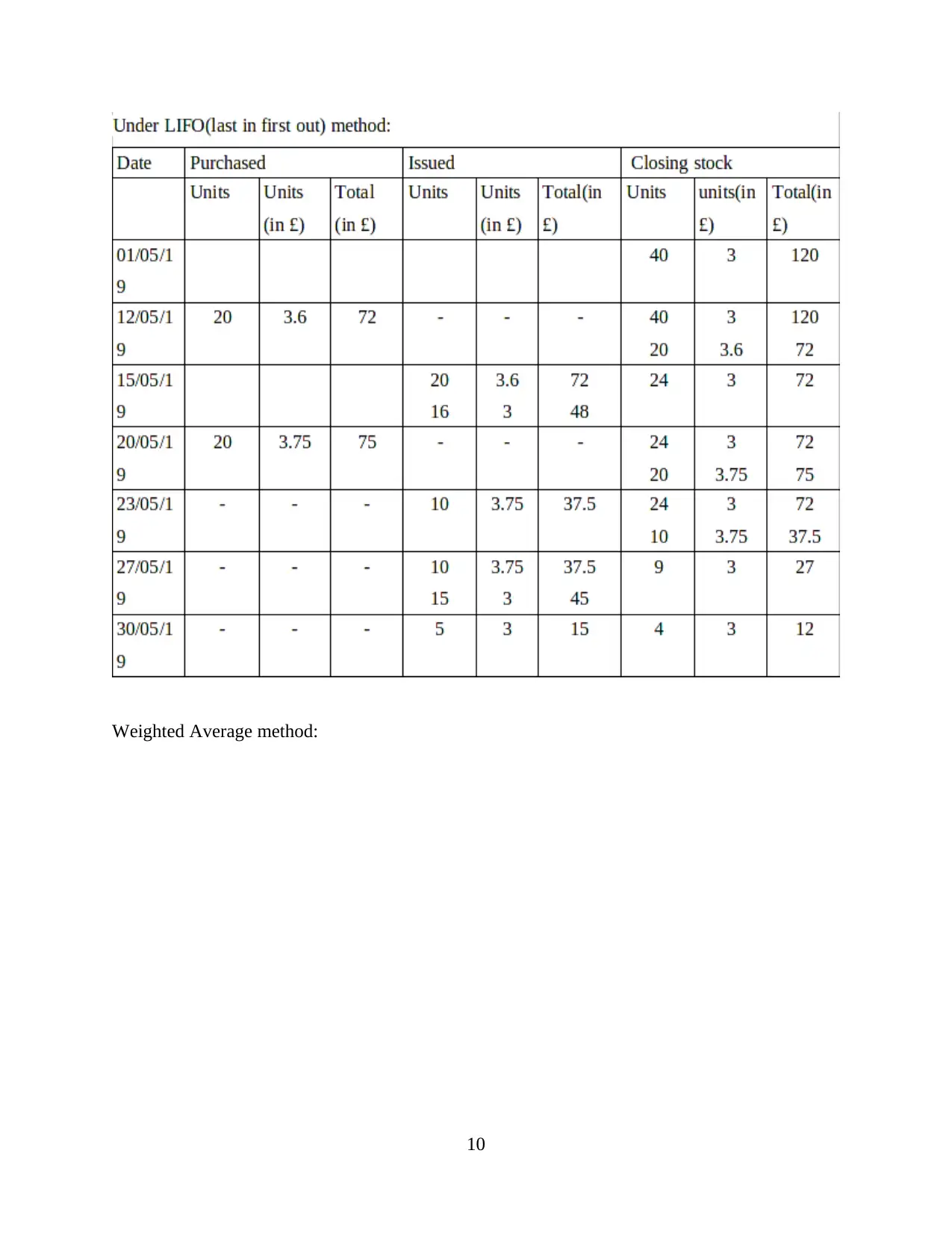

LIFO: This is a kind of method that has been used with respect to raw materials which

came at last were utilised at first. For an instance Stitchland Ltd organisation make use of raw

materials that were bought at last.

FIFO: This method is exactly opposite to LIFO. As in this case the stock that has been

bought at first is used initially. Like Stitchland Ltd make use of raw material bought at initial

stage so that it do not get hampered with passage of time.

Overhead: They denotes kind of expenses that are connected directly with labour as well

as material. For an instance, salary, rent are some examples (Soudani, 2012).

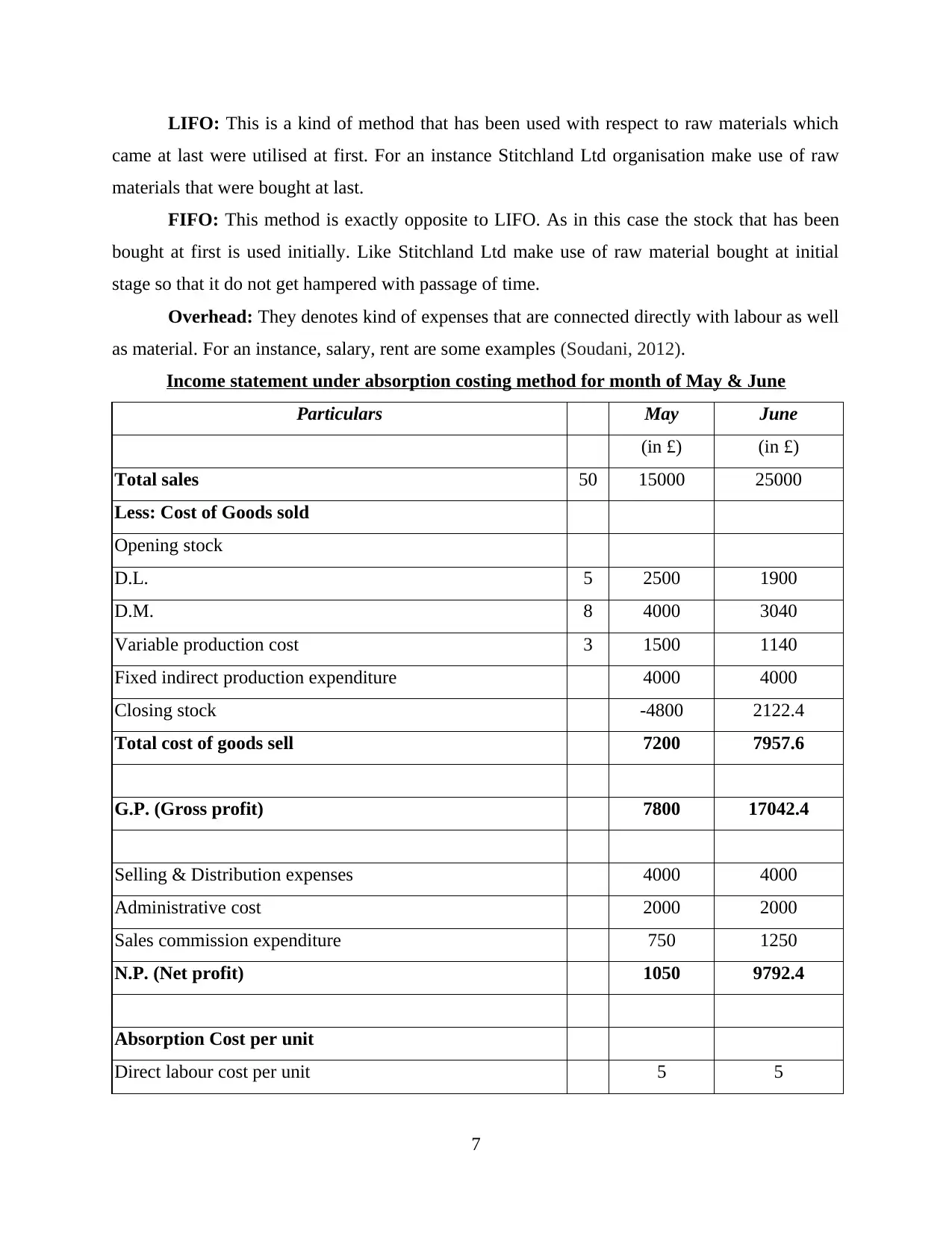

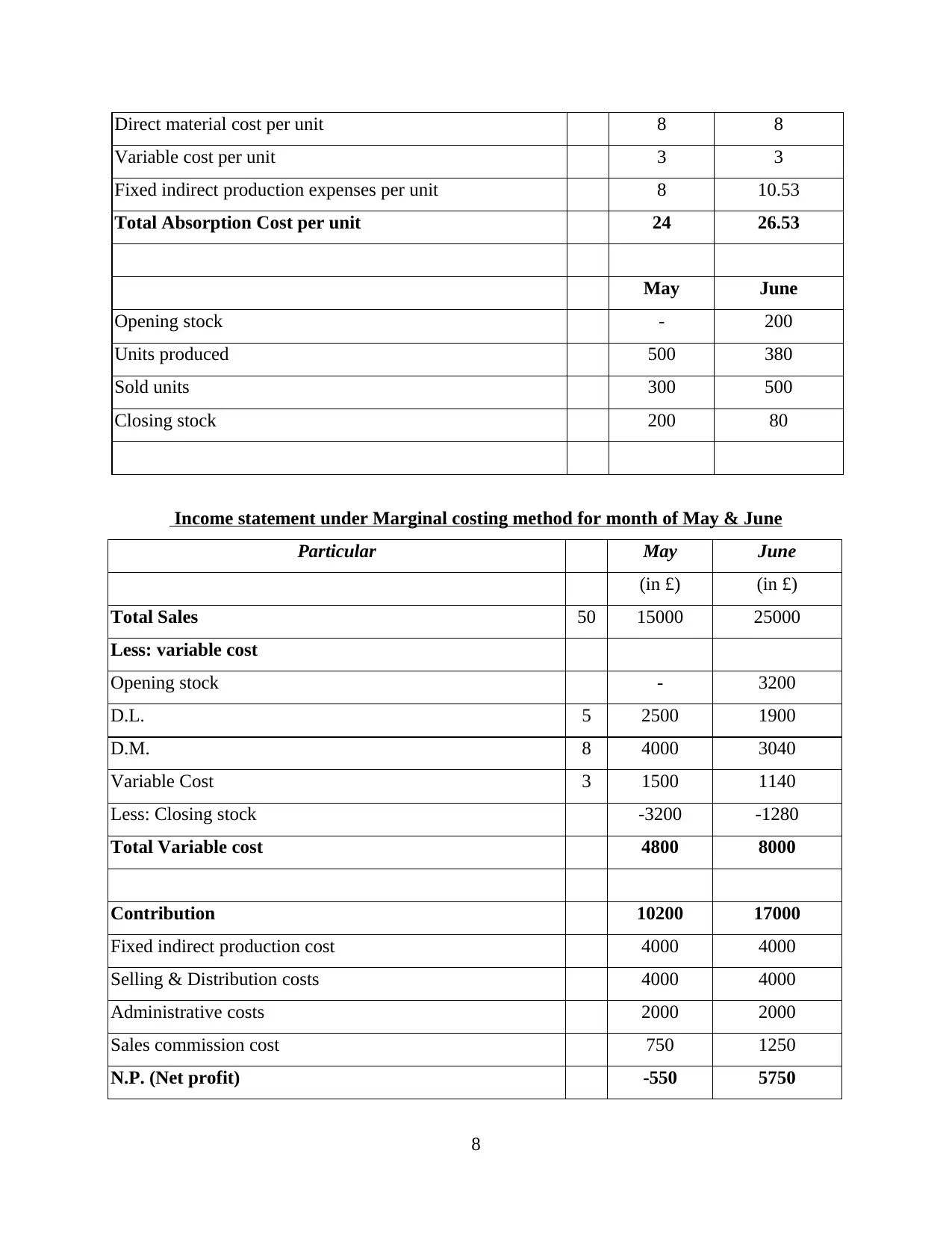

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

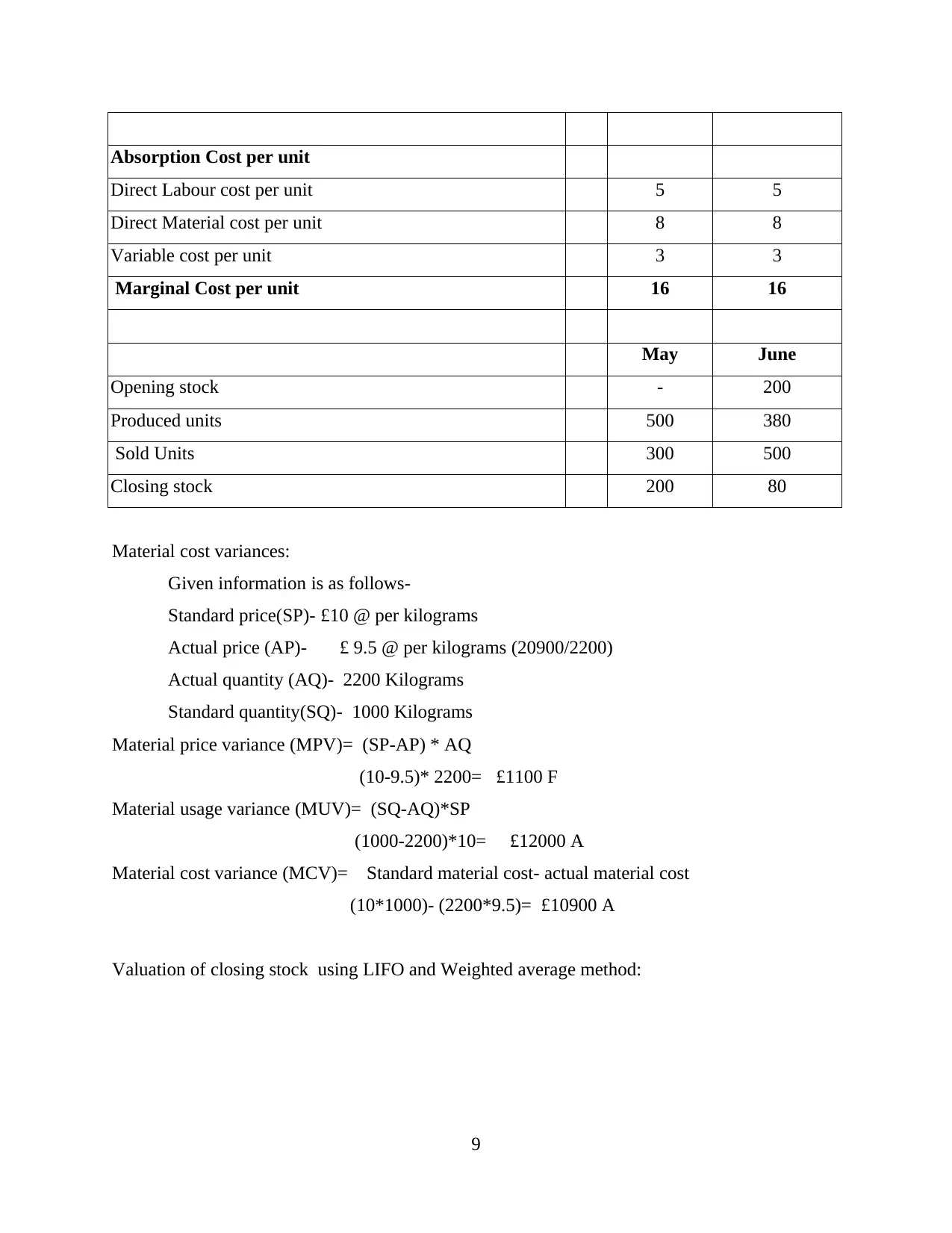

Absorption Cost per unit

Direct labour cost per unit 5 5

7

came at last were utilised at first. For an instance Stitchland Ltd organisation make use of raw

materials that were bought at last.

FIFO: This method is exactly opposite to LIFO. As in this case the stock that has been

bought at first is used initially. Like Stitchland Ltd make use of raw material bought at initial

stage so that it do not get hampered with passage of time.

Overhead: They denotes kind of expenses that are connected directly with labour as well

as material. For an instance, salary, rent are some examples (Soudani, 2012).

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

(10*1000)- (2200*9.5)= £10900 A

Valuation of closing stock using LIFO and Weighted average method:

9

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

(10*1000)- (2200*9.5)= £10900 A

Valuation of closing stock using LIFO and Weighted average method:

9

Weighted Average method:

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.