Management Accounting Report: Techniques and Financial Reporting

VerifiedAdded on 2020/12/10

|18

|4484

|236

Report

AI Summary

This report delves into the core principles and applications of management accounting within the context of ABC Ltd. It explores essential requirements of different management accounting systems, including cost accounting, inventory management, job costing, and price optimization. The report details various management accounting reporting methods such as performance reports, cost managerial accounting reports, budget reports, and account receivable aging reports. It evaluates the benefits of a management accounting system, highlighting its application in organizations like ABC Ltd. The report also covers the calculation of costs using marginal and absorption costing techniques, along with the application of a range of management accounting techniques and producing appropriate financial reporting documents. Furthermore, it examines different types of planning tools used for budgetary control, their advantages, and disadvantages, and how organizations adapt management accounting systems to respond to financial problems. The analysis provides a comprehensive understanding of how management accounting aids in financial decision-making, cost control, and strategic planning within a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................5

LO 1 ................................................................................................................................................5

P1. Explaining management accounting and essential requirements of different types of ........5

management accounting systems................................................................................................5

P2. Explaining methods used for different management accounting reporting..........................6

M1. Evaluate benefits of management accounting system and their application in organisation

.....................................................................................................................................................7

D1. Evaluate management accounting system and management accounting reporting

integrated in organization ...........................................................................................................8

LO2..................................................................................................................................................8

P3. Calculating cost by using appropriate techniques of cost analysis for preparing an Income

.....................................................................................................................................................8

Statement using Marginal and absorption costs..........................................................................8

M2. Applying a range of management accounting techniques and producing appropriate

financial reporting documents.....................................................................................................9

D2. Producing financial reports that accurately apply and interpret data for a range of business

activities....................................................................................................................................10

LO3 ..............................................................................................................................................10

P4. Advantages and disadvantages of different types of planning tools used for budgetary ...10

control.......................................................................................................................................10

M3. Use of different planning tools and their application in preparing budget........................12

D3. Evaluation of planning tools to solve organizational problems.........................................12

LO4................................................................................................................................................13

P5. Compare how organisations are adapting management accounting systems to respond to

...................................................................................................................................................13

financial problems.....................................................................................................................13

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................5

LO 1 ................................................................................................................................................5

P1. Explaining management accounting and essential requirements of different types of ........5

management accounting systems................................................................................................5

P2. Explaining methods used for different management accounting reporting..........................6

M1. Evaluate benefits of management accounting system and their application in organisation

.....................................................................................................................................................7

D1. Evaluate management accounting system and management accounting reporting

integrated in organization ...........................................................................................................8

LO2..................................................................................................................................................8

P3. Calculating cost by using appropriate techniques of cost analysis for preparing an Income

.....................................................................................................................................................8

Statement using Marginal and absorption costs..........................................................................8

M2. Applying a range of management accounting techniques and producing appropriate

financial reporting documents.....................................................................................................9

D2. Producing financial reports that accurately apply and interpret data for a range of business

activities....................................................................................................................................10

LO3 ..............................................................................................................................................10

P4. Advantages and disadvantages of different types of planning tools used for budgetary ...10

control.......................................................................................................................................10

M3. Use of different planning tools and their application in preparing budget........................12

D3. Evaluation of planning tools to solve organizational problems.........................................12

LO4................................................................................................................................................13

P5. Compare how organisations are adapting management accounting systems to respond to

...................................................................................................................................................13

financial problems.....................................................................................................................13

M4 Analyzing financial problems with help of management accounting ............................14

CONCLUSION .............................................................................................................................15

REFERENCES .............................................................................................................................16

CONCLUSION .............................................................................................................................15

REFERENCES .............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting is a process of evaluating, identifying and preparing management

accounts, reports and business strategy so as to provide accurate, fair and timely information

related to both financial, managerial and other non-financial information necessary for decision-

making (Berry, A.J., and et.al., 2016). It sometimes also helps in interpreting & communicating

information to the stakeholders of company for making important investment related decision.

Further more, different management accounting techniques has been used by the company

named as ABC Ltd. for controlling cost, making budgets. It has also explained that how a

company uses different management accounting tools in solving its financial problem and

thereby achieve its organisational goal. Management Accounting reporting has also been

explained which contains material information about the company's financial position, cost

incurred, non monetary information which helps the company in planning & formulating

business strategies, preparing budgets, measuring performance, decision-making and estimating

future profits and cost to be incurred (Berry, A.J., and et.al., 2016).

Management Accounting is a process of evaluating, identifying and preparing management

accounts, reports and business strategy so as to provide accurate, fair and timely information

related to both financial, managerial and other non-financial information necessary for decision-

making (Berry, A.J., and et.al., 2016). It sometimes also helps in interpreting & communicating

information to the stakeholders of company for making important investment related decision.

Further more, different management accounting techniques has been used by the company

named as ABC Ltd. for controlling cost, making budgets. It has also explained that how a

company uses different management accounting tools in solving its financial problem and

thereby achieve its organisational goal. Management Accounting reporting has also been

explained which contains material information about the company's financial position, cost

incurred, non monetary information which helps the company in planning & formulating

business strategies, preparing budgets, measuring performance, decision-making and estimating

future profits and cost to be incurred (Berry, A.J., and et.al., 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MAIN BODY

LO 1

P1. Explaining management accounting and essential requirements of different types of

management accounting systems.

Management accounting is an internal business process which helps the organisation in

determining and controlling the cost, making effective plans and budgets, making of

management accounts and reports which aids the management of organisation in taking

managerial decision (Herschung, F., and et.al., 2017). It helps the company in making better

business related decisions and make plans related to the department policies so as to maximize

profits & minimizing costs. Management accounting deals with monetary and non - monetary

data whereas financial accounting only emphasizes on monetary information of the company.

The essential requirements of different types of management accounting systems are as follows:

1. Cost Accounting System - A process used by company in estimating, evaluating and

analysing the cost incurred by company in carrying on business activities i.e. for manufacturing a

product. It helps in valuation of inventory, preparing budgets and controlling cost. It has

following two types:

1. Process Costing Method - It emphasizes on determining costs incurred for carrying on large

production functions. It considers similar products for such costing method and distributed by

total output for ascertaining cost per unit.

2. Job order Costing Method - It is a process which involves collection of cost of production

related to some specific unit or a group. This method is used for costing unique products and

helps customers in ascertaining exact cost incurred.

2. Inventory Management System - It helps company in monitoring and tracking goods,

products within supply chain and area where business operates. It helps in ensuring and

improving the continuity of workflow, evaluating exact inventory figure and its reorder before

stock out situation arises. This system has two sub types:

1. LIFO - LIFO stands for "Last in, first out". A method of inventory valuation in which last

inventory item purchased is sold first (Herschung, F., and et.al., 2017).

2. FIFO - FIFO stands for "First in, first out". It is a method in which goods purchased first are

the goods sold first.

LO 1

P1. Explaining management accounting and essential requirements of different types of

management accounting systems.

Management accounting is an internal business process which helps the organisation in

determining and controlling the cost, making effective plans and budgets, making of

management accounts and reports which aids the management of organisation in taking

managerial decision (Herschung, F., and et.al., 2017). It helps the company in making better

business related decisions and make plans related to the department policies so as to maximize

profits & minimizing costs. Management accounting deals with monetary and non - monetary

data whereas financial accounting only emphasizes on monetary information of the company.

The essential requirements of different types of management accounting systems are as follows:

1. Cost Accounting System - A process used by company in estimating, evaluating and

analysing the cost incurred by company in carrying on business activities i.e. for manufacturing a

product. It helps in valuation of inventory, preparing budgets and controlling cost. It has

following two types:

1. Process Costing Method - It emphasizes on determining costs incurred for carrying on large

production functions. It considers similar products for such costing method and distributed by

total output for ascertaining cost per unit.

2. Job order Costing Method - It is a process which involves collection of cost of production

related to some specific unit or a group. This method is used for costing unique products and

helps customers in ascertaining exact cost incurred.

2. Inventory Management System - It helps company in monitoring and tracking goods,

products within supply chain and area where business operates. It helps in ensuring and

improving the continuity of workflow, evaluating exact inventory figure and its reorder before

stock out situation arises. This system has two sub types:

1. LIFO - LIFO stands for "Last in, first out". A method of inventory valuation in which last

inventory item purchased is sold first (Herschung, F., and et.al., 2017).

2. FIFO - FIFO stands for "First in, first out". It is a method in which goods purchased first are

the goods sold first.

3. Job Costing System - A process in which cost and its related information associated with

specific product or any business activity or any specific job process is determined for the

knowledge of customer. It takes into consideration Direct material, labour and overhead costs. It

helps customer in getting cost reimbursed under terms and conditions as defined in contract. By

using job costing system, the company can ascertained cost at any stage of job completed and

comparing it with estimated costs prepared thereby helping in controlling cost and maximizing

profits (Herschung, F., and et.al., 2017).

4. Price Optimisation System - It is a mathematical analysis done by company for determining

that how at different level of prices, demand will vary accordingly. It helps in analysing future

profit levels by studying and understanding the demand fluctuation with reference to price

changes. It considers three factors as price elements:

1. Strategy of pricing a product;

2. Product value for both buyer as well as seller, and

3. Procedures used for increasing profits level.

P2. Explaining methods used for different management accounting reporting.

The management accounting emphasizes on internal processes of the business

organisation. Management accounting reporting is generally a process of planning, evaluating,

monitoring, and decision making on the basis of material information provided about the

company's financial position, cost incurred, non monetary information which helps the company

in planning & formulating business strategies, preparing budgets, measuring performance,

decision-making and estimating future profits and cost to be incurred (Herschung, F., and et.al.,

2017).

Different methods used for management accounting reporting are as follows:

1. Performance Reports - Performance report is a report which provides the success journey of

a business project or employee. It helps the company in monitoring and reviewing the

performance thereby assisting in decision making. Such reports provide deeper view of the

working of business organisation. It is important for every company to monitor and keep a track

of strategy & policy developed for attainment of mission.

specific product or any business activity or any specific job process is determined for the

knowledge of customer. It takes into consideration Direct material, labour and overhead costs. It

helps customer in getting cost reimbursed under terms and conditions as defined in contract. By

using job costing system, the company can ascertained cost at any stage of job completed and

comparing it with estimated costs prepared thereby helping in controlling cost and maximizing

profits (Herschung, F., and et.al., 2017).

4. Price Optimisation System - It is a mathematical analysis done by company for determining

that how at different level of prices, demand will vary accordingly. It helps in analysing future

profit levels by studying and understanding the demand fluctuation with reference to price

changes. It considers three factors as price elements:

1. Strategy of pricing a product;

2. Product value for both buyer as well as seller, and

3. Procedures used for increasing profits level.

P2. Explaining methods used for different management accounting reporting.

The management accounting emphasizes on internal processes of the business

organisation. Management accounting reporting is generally a process of planning, evaluating,

monitoring, and decision making on the basis of material information provided about the

company's financial position, cost incurred, non monetary information which helps the company

in planning & formulating business strategies, preparing budgets, measuring performance,

decision-making and estimating future profits and cost to be incurred (Herschung, F., and et.al.,

2017).

Different methods used for management accounting reporting are as follows:

1. Performance Reports - Performance report is a report which provides the success journey of

a business project or employee. It helps the company in monitoring and reviewing the

performance thereby assisting in decision making. Such reports provide deeper view of the

working of business organisation. It is important for every company to monitor and keep a track

of strategy & policy developed for attainment of mission.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Cost Managerial Accounting Report - Management accounting evaluates the costs of

involved in producing a specific unit or group of units. This report considers direct raw material

costs, direct labour cost and overhead cost, and other costs. The total cost figure is then divided

by the total number of output for ascertaining the cost per unit. It helps in realizing the product

cost prices and selling prices and comparing for determining the profit margins (Herschung, F.,

and et.al., 2017).

3. Budget Report - It helps in controlling business cost and expenses by preparing estimated

budgets and comparing actual results with the estimated budget prepared to ascertain variances,

if any. It helps in achieving maximum profitability with minimum cost of production and limited

budget amount.

4. Account Receivable Aging Report - This report considers accounts receivables for making

crucial management decisions. It emphasises on credit side of business. Apart from credit

amount, balance remains helps in identifying defaulting person and problem in cash collection

process of company.

M1. Evaluate benefits of management accounting system and their application in organisation

Management accounting system is an effective system used by companies to

manage financial information and to manage accounting reports of different departments. In

ABC firm the management accounting system used in its operations and sales department ,

finance department etc. Benefits of management accounting system -

Analysis of cost- It helps in calculating actual cost of different projects with the

expected cost. In firm ABC it projects the cost and compare them which helps the company to

find out the areas of company which are under performed and help the company to take measures

to correct them (Herschung, F., and et.al., 2017).

Analysis of trend – It uses reports that help the Company ABC to make future

decisions by using trend analysis which helps the company to forecast future sales and

preparation of budgets. This helps the company to find out its expenditure and expected return on

the project.

Analysis of constraints – It helps ABC company to find obstacles or limitations

in the process of production or sales. It helps company to figure out the reason why company's

operations are not efficient. In short, it evaluates the workflow of the company.

involved in producing a specific unit or group of units. This report considers direct raw material

costs, direct labour cost and overhead cost, and other costs. The total cost figure is then divided

by the total number of output for ascertaining the cost per unit. It helps in realizing the product

cost prices and selling prices and comparing for determining the profit margins (Herschung, F.,

and et.al., 2017).

3. Budget Report - It helps in controlling business cost and expenses by preparing estimated

budgets and comparing actual results with the estimated budget prepared to ascertain variances,

if any. It helps in achieving maximum profitability with minimum cost of production and limited

budget amount.

4. Account Receivable Aging Report - This report considers accounts receivables for making

crucial management decisions. It emphasises on credit side of business. Apart from credit

amount, balance remains helps in identifying defaulting person and problem in cash collection

process of company.

M1. Evaluate benefits of management accounting system and their application in organisation

Management accounting system is an effective system used by companies to

manage financial information and to manage accounting reports of different departments. In

ABC firm the management accounting system used in its operations and sales department ,

finance department etc. Benefits of management accounting system -

Analysis of cost- It helps in calculating actual cost of different projects with the

expected cost. In firm ABC it projects the cost and compare them which helps the company to

find out the areas of company which are under performed and help the company to take measures

to correct them (Herschung, F., and et.al., 2017).

Analysis of trend – It uses reports that help the Company ABC to make future

decisions by using trend analysis which helps the company to forecast future sales and

preparation of budgets. This helps the company to find out its expenditure and expected return on

the project.

Analysis of constraints – It helps ABC company to find obstacles or limitations

in the process of production or sales. It helps company to figure out the reason why company's

operations are not efficient. In short, it evaluates the workflow of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1. Evaluate management accounting system and management accounting reporting integrated

in organization

Management accounting system and management reporting system are system that helps

a company in controlling its finance, analyzing its cost, managing its project and forecasting

trend and deciding budget.

The ABC company uses this system to provide direction to the business and to increase the

profitability and productivity of firm. It helps the company to fix the target to see if the

employees of firm can manage the standards or not. It helps the company to formulate its budget

according to the performances of various departments. They both facilitate decision making in

the company with ease and efficiency. Both this system helps the company to achieve its goals

and to manage it finances and resources effectively. The key benefits of both the system are-

They tell the company about both financial as well as non- financial indicators of different

departments of the company (Herschung, F., and et.al., 2017).

They use huge data for calculations and to estimate future trend and projections. It provides

information to ABC company in actual and estimated cost analysis of the company. It prepares

report on training of company's employees and ensures regulation of employee's responsibilities.

LO2

P3. Calculating cost by using appropriate techniques of cost analysis for preparing an Income

Statement using Marginal and absorption costs.

in organization

Management accounting system and management reporting system are system that helps

a company in controlling its finance, analyzing its cost, managing its project and forecasting

trend and deciding budget.

The ABC company uses this system to provide direction to the business and to increase the

profitability and productivity of firm. It helps the company to fix the target to see if the

employees of firm can manage the standards or not. It helps the company to formulate its budget

according to the performances of various departments. They both facilitate decision making in

the company with ease and efficiency. Both this system helps the company to achieve its goals

and to manage it finances and resources effectively. The key benefits of both the system are-

They tell the company about both financial as well as non- financial indicators of different

departments of the company (Herschung, F., and et.al., 2017).

They use huge data for calculations and to estimate future trend and projections. It provides

information to ABC company in actual and estimated cost analysis of the company. It prepares

report on training of company's employees and ensures regulation of employee's responsibilities.

LO2

P3. Calculating cost by using appropriate techniques of cost analysis for preparing an Income

Statement using Marginal and absorption costs.

M2. Applying a range of management accounting techniques and producing appropriate financial

reporting documents.

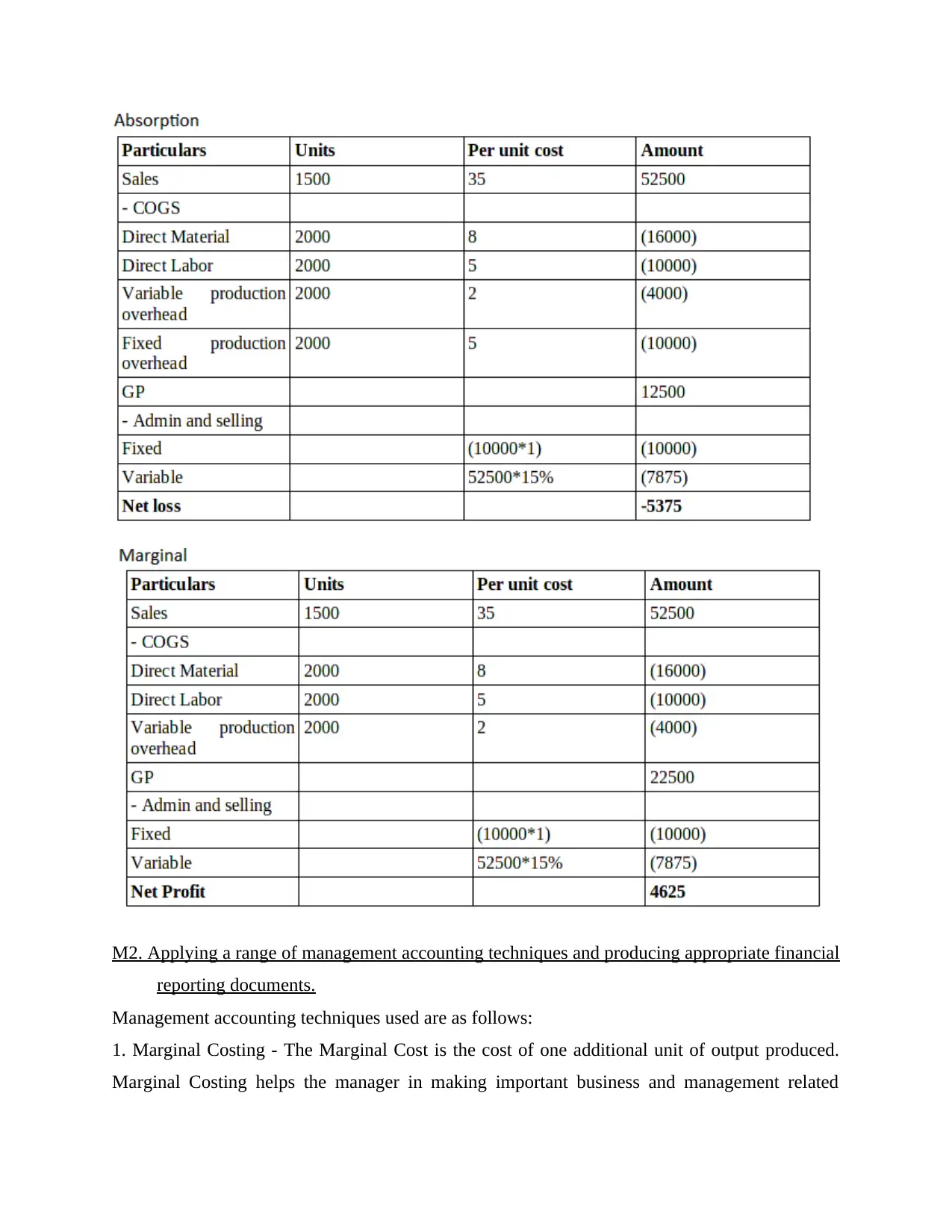

Management accounting techniques used are as follows:

1. Marginal Costing - The Marginal Cost is the cost of one additional unit of output produced.

Marginal Costing helps the manager in making important business and management related

reporting documents.

Management accounting techniques used are as follows:

1. Marginal Costing - The Marginal Cost is the cost of one additional unit of output produced.

Marginal Costing helps the manager in making important business and management related

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decisions such as purchasing of a new machinery or replacement of any plant and manufacturing

units. It helps in making profit plans for future with the help of break even analysis.

2. Absorption Costing - It is a costing technique basically used for valuing inventory and stock. It

ensures that all the cost related to production and manufacturing process are properly absorbed

by the number of units produced. It considers both the variable and fixed cost as a product cost.

It ensures that product cost calculated is accurate and fair.

D2. Producing financial reports that accurately apply and interpret data for a range of business

activities.

From the above calculation it can be interpreted that ABC Ltd. is using Marginal Costing

method and Absorption Costing method as management accounting techniques for evaluating the

net profit earn by the company. By using Marginal Costing method, the company is earning

more profit which is improving the financial performance of the company, which is considered

as a good factor from the point of view of investors and other stakeholders as it will lead to

wealth creation for them (Herschung, F., and et.al., 2017).

LO3

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.

Different types of planning tools used for budgetary control are as follows:

1. Financial Budget – It deals with financial planning, accounting and decision making related

to cash inflows & outflows, revenue - expenditure for a certain period and its impacts on

business. It helps in ascertainment of true financial position of the company. It has following 2

types:

Cash Budget – It forecast future cash position of company, actual cash inflows and outflows,

availability of surplus cash with business, expenses incurred and profit earned (Sheth, K.N. and

Sheth, K.N., 2017).

Capital Expenditure Budget – The heavy investment made for acquiring or purchasing new

assets, plant & machinery, land etc. by company by borrowing from outside the company.

ADVANTAGE – It helps in making financial plans for business operations, investment related

decision etc. It ensures timely availability of all resources by managing cash flows. The purpose

units. It helps in making profit plans for future with the help of break even analysis.

2. Absorption Costing - It is a costing technique basically used for valuing inventory and stock. It

ensures that all the cost related to production and manufacturing process are properly absorbed

by the number of units produced. It considers both the variable and fixed cost as a product cost.

It ensures that product cost calculated is accurate and fair.

D2. Producing financial reports that accurately apply and interpret data for a range of business

activities.

From the above calculation it can be interpreted that ABC Ltd. is using Marginal Costing

method and Absorption Costing method as management accounting techniques for evaluating the

net profit earn by the company. By using Marginal Costing method, the company is earning

more profit which is improving the financial performance of the company, which is considered

as a good factor from the point of view of investors and other stakeholders as it will lead to

wealth creation for them (Herschung, F., and et.al., 2017).

LO3

P4. Advantages and disadvantages of different types of planning tools used for budgetary

control.

Different types of planning tools used for budgetary control are as follows:

1. Financial Budget – It deals with financial planning, accounting and decision making related

to cash inflows & outflows, revenue - expenditure for a certain period and its impacts on

business. It helps in ascertainment of true financial position of the company. It has following 2

types:

Cash Budget – It forecast future cash position of company, actual cash inflows and outflows,

availability of surplus cash with business, expenses incurred and profit earned (Sheth, K.N. and

Sheth, K.N., 2017).

Capital Expenditure Budget – The heavy investment made for acquiring or purchasing new

assets, plant & machinery, land etc. by company by borrowing from outside the company.

ADVANTAGE – It helps in making financial plans for business operations, investment related

decision etc. It ensures timely availability of all resources by managing cash flows. The purpose

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

behind preparing estimated budgets is to ensure that organisation is working & yielding results

thereby leading to growth and profitability.

DISADVANTAGE – In financial budget, cash budget is prepared for meeting the day to day

expenses, therefore not possible to determine accurate cash requirements of business. As the

budget is prepared for meeting future expenses, it is very difficult to prepare budget when market

condition is not favourable or under inflation.

2. Operating Budget – It analyses & estimates the projected revenues and expenditure, income

or expenses during specified period. It is of 3 types:

Sales or Revenue Budget - It forecast future revenue and income of organisation from future

business operations (Sheth, K.N. and Sheth, K.N., 2017).

Expense Budget - It predicts upcoming expenses of organisation for specified time period.

Project Budget - It forecast about business estimated profit, it will earn from difference between

sales and expenses figure of a specified period.

ADVANTAGE - It helps in forecasting revenue to be generated by achieving set defined goals,

thereby reducing expenses such as cost of production, operating expenses. It ensures effective

allocation of resources to project required in achieving business goals.

DISADVANTAGE - Budget prepared may brings resistance to development, innovative and

creative ideas, changes required in plan. Decision-making process becomes inflexible when

inadequate assumptions are made making budget unrealistic.

3. Non monetary Budget - Budget prepared for meeting non - monetary business operations

depending upon the economic conditions (Sheth, K.N. and Sheth, K.N., 2017). It includes:

Fixed and Variable Cost - Those expense which organisation has to incur even not working or

carrying own its business operations like rent, salary etc. are Fixed cost. Variable cost means the

cost which vary with the business operations.

ADVANTAGE - By providing cost friendly budget control techniques helps in effective

accomplishment of business operation.

DISADVANTAGE - Budget is prepared keeping in mind the current organisational structure

which may not fit in current business condition leading to non accomplishment of organisational

goals.

thereby leading to growth and profitability.

DISADVANTAGE – In financial budget, cash budget is prepared for meeting the day to day

expenses, therefore not possible to determine accurate cash requirements of business. As the

budget is prepared for meeting future expenses, it is very difficult to prepare budget when market

condition is not favourable or under inflation.

2. Operating Budget – It analyses & estimates the projected revenues and expenditure, income

or expenses during specified period. It is of 3 types:

Sales or Revenue Budget - It forecast future revenue and income of organisation from future

business operations (Sheth, K.N. and Sheth, K.N., 2017).

Expense Budget - It predicts upcoming expenses of organisation for specified time period.

Project Budget - It forecast about business estimated profit, it will earn from difference between

sales and expenses figure of a specified period.

ADVANTAGE - It helps in forecasting revenue to be generated by achieving set defined goals,

thereby reducing expenses such as cost of production, operating expenses. It ensures effective

allocation of resources to project required in achieving business goals.

DISADVANTAGE - Budget prepared may brings resistance to development, innovative and

creative ideas, changes required in plan. Decision-making process becomes inflexible when

inadequate assumptions are made making budget unrealistic.

3. Non monetary Budget - Budget prepared for meeting non - monetary business operations

depending upon the economic conditions (Sheth, K.N. and Sheth, K.N., 2017). It includes:

Fixed and Variable Cost - Those expense which organisation has to incur even not working or

carrying own its business operations like rent, salary etc. are Fixed cost. Variable cost means the

cost which vary with the business operations.

ADVANTAGE - By providing cost friendly budget control techniques helps in effective

accomplishment of business operation.

DISADVANTAGE - Budget is prepared keeping in mind the current organisational structure

which may not fit in current business condition leading to non accomplishment of organisational

goals.

4. Static Budget - The budget prepared remains fixed irrespective of changes in factors such as

operational activities, plans, strategy, sales, production level.

ADVANTAGE - Static budget helps company in controlling the cost of prod, operating expenses

thereby achieving business goals in cost effective manner. It also provides a insight view about

company & helps in decision making (Sheth, K.N. and Sheth, K.N., 2017).

DISADVANTAGE - Lack of flexibility is one of disadvantage of static budget. Because of its

fixed nature, any changes in factors such as sales, revenue etc. will not allow any further

allocation of resources required for completing business operations.

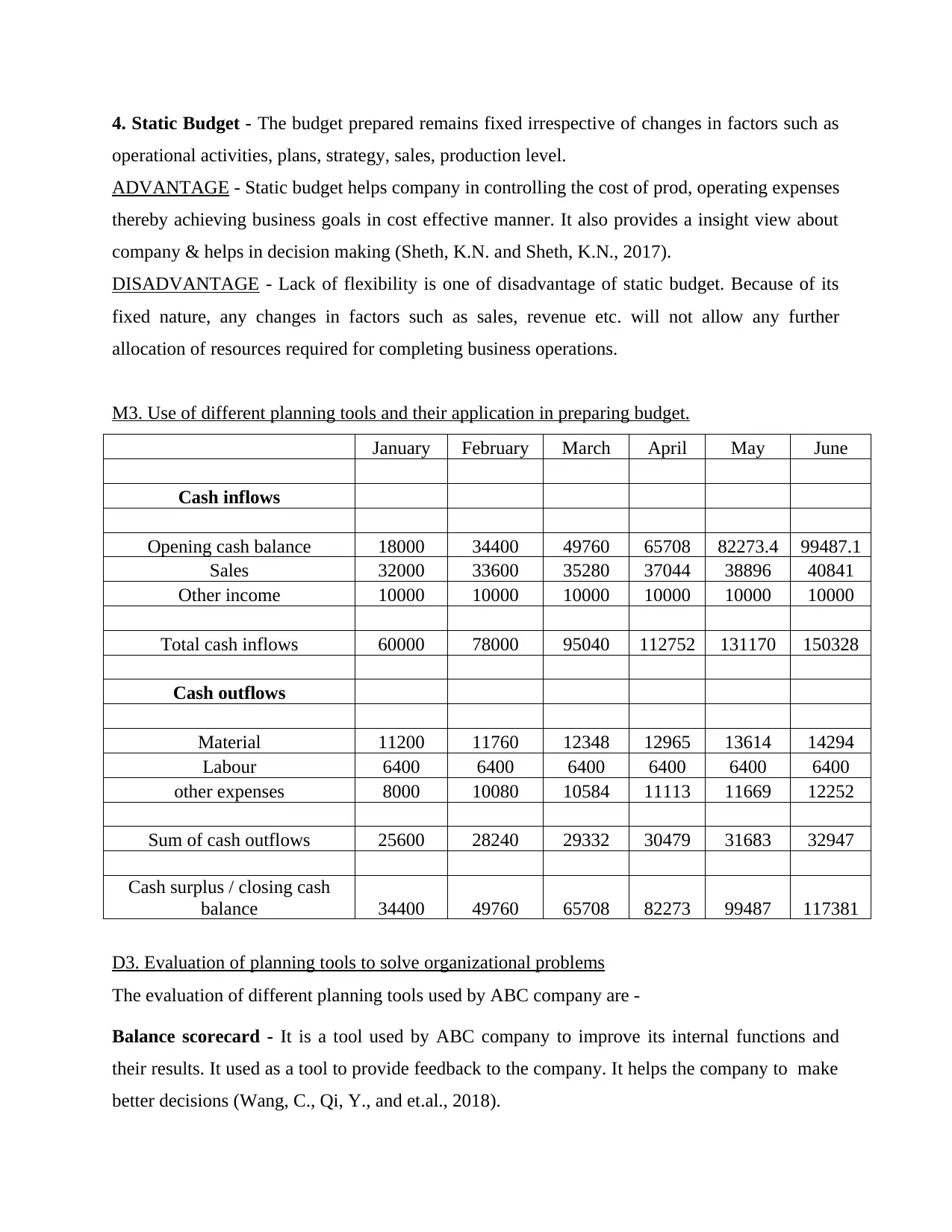

M3. Use of different planning tools and their application in preparing budget.

January February March April May June

Cash inflows

Opening cash balance 18000 34400 49760 65708 82273.4 99487.1

Sales 32000 33600 35280 37044 38896 40841

Other income 10000 10000 10000 10000 10000 10000

Total cash inflows 60000 78000 95040 112752 131170 150328

Cash outflows

Material 11200 11760 12348 12965 13614 14294

Labour 6400 6400 6400 6400 6400 6400

other expenses 8000 10080 10584 11113 11669 12252

Sum of cash outflows 25600 28240 29332 30479 31683 32947

Cash surplus / closing cash

balance 34400 49760 65708 82273 99487 117381

D3. Evaluation of planning tools to solve organizational problems

The evaluation of different planning tools used by ABC company are -

Balance scorecard - It is a tool used by ABC company to improve its internal functions and

their results. It used as a tool to provide feedback to the company. It helps the company to make

better decisions (Wang, C., Qi, Y., and et.al., 2018).

operational activities, plans, strategy, sales, production level.

ADVANTAGE - Static budget helps company in controlling the cost of prod, operating expenses

thereby achieving business goals in cost effective manner. It also provides a insight view about

company & helps in decision making (Sheth, K.N. and Sheth, K.N., 2017).

DISADVANTAGE - Lack of flexibility is one of disadvantage of static budget. Because of its

fixed nature, any changes in factors such as sales, revenue etc. will not allow any further

allocation of resources required for completing business operations.

M3. Use of different planning tools and their application in preparing budget.

January February March April May June

Cash inflows

Opening cash balance 18000 34400 49760 65708 82273.4 99487.1

Sales 32000 33600 35280 37044 38896 40841

Other income 10000 10000 10000 10000 10000 10000

Total cash inflows 60000 78000 95040 112752 131170 150328

Cash outflows

Material 11200 11760 12348 12965 13614 14294

Labour 6400 6400 6400 6400 6400 6400

other expenses 8000 10080 10584 11113 11669 12252

Sum of cash outflows 25600 28240 29332 30479 31683 32947

Cash surplus / closing cash

balance 34400 49760 65708 82273 99487 117381

D3. Evaluation of planning tools to solve organizational problems

The evaluation of different planning tools used by ABC company are -

Balance scorecard - It is a tool used by ABC company to improve its internal functions and

their results. It used as a tool to provide feedback to the company. It helps the company to make

better decisions (Wang, C., Qi, Y., and et.al., 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.