Management Accounting Report: Techniques, Tools, and Applications

VerifiedAdded on 2020/06/06

|17

|4949

|255

Report

AI Summary

This report provides a comprehensive overview of management accounting, emphasizing its crucial role in organizations of all sizes. It explores various aspects, including the preparation of management accounting systems, different methods used in financial reporting, and the distinction between marginal and absorption costing. The report examines the advantages and disadvantages of different budgeting tools, illustrating their application in budgetary control. Furthermore, it delves into the impact of adopting management accounting systems on organizational financial performance, using Ryder Architecture as a case study. The report covers financial planning, analysis of financial statements, historical cost accounting, standard accounting, and budgetary control. It also details marginal costing, funds flow statements, and decision-making processes within the context of management accounting, providing a valuable resource for understanding and implementing effective financial strategies.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INRODUCTION..............................................................................................................................1

P-1 Management accounting and its different types...................................................................1

P-2 Different methods used for management accounting report................................................3

P-3 Marginal costs and absorption costs.....................................................................................4

P-4 Advantages and disadvantages of different budgeting tools................................................5

P-5 Adaptation of accounting system in organizations...............................................................7

M-1 The benefits of management accounting.............................................................................9

M-2 Management accounting technique and its benefits............................................................9

M-3 Different planning tools and their applications.................................................................10

M-4 How financial problems and management accounting leads to success...........................10

CONCLUSION:.............................................................................................................................11

INRODUCTION..............................................................................................................................1

P-1 Management accounting and its different types...................................................................1

P-2 Different methods used for management accounting report................................................3

P-3 Marginal costs and absorption costs.....................................................................................4

P-4 Advantages and disadvantages of different budgeting tools................................................5

P-5 Adaptation of accounting system in organizations...............................................................7

M-1 The benefits of management accounting.............................................................................9

M-2 Management accounting technique and its benefits............................................................9

M-3 Different planning tools and their applications.................................................................10

M-4 How financial problems and management accounting leads to success...........................10

CONCLUSION:.............................................................................................................................11

INRODUCTION

Management accounting plays a very crucial role in every big, medium and small

organization. It controls, manage and communicate goals and objectives to the overall

organization. It helps in maintaining the financial performance by preparing plans and budgets

for specific time period. This report will show the requirements in preparing different types of

management accounting systems. It will also show different methods used in management

accounting and difference between marginal and absorption cost. How these cost affects the

profits in business. Also the pros and cons of different planning tools for preparing budgetary

control. It shows the effect of organization in adopting the management accounting system to

survive and respond to their financial problems.

For undertaking this report the organisation selected is Ryder Architecture. The cited firm

belongs to construction sector and operates in very small area. Thus, this report will help in dev

eloping a relevant management accounting system for the cited establishment.

P-1 Management accounting and its different types

A process of preparing accounting reports that provide timely and accurate financial

information required by managers to take daily decisions. These reports identify, measure,

analyse, intercept and communicate the organization goals. The key difference between

managerial and finance accounting is that managerial accounting helps managers to take

decisions within the organization while financial accounting helps in providing information to

outside parties. Managerial accounting can be done by various techniques like margin analysis,

constraint analysis, capital budgeting, trend analysis, product costing and lean financial

modelling.

Essential requirements of management accounting system are:

Financial planning- It is a process in which planning is done to achieve primary objectives and

goals. It includes both long term and short term financial objectives by formulating policies and

developing procedures. These policies may relate to determination of capital amount, sources of

funds and distribution of income as well as use of debt along with equity capital. To do financial

Management accounting plays a very crucial role in every big, medium and small

organization. It controls, manage and communicate goals and objectives to the overall

organization. It helps in maintaining the financial performance by preparing plans and budgets

for specific time period. This report will show the requirements in preparing different types of

management accounting systems. It will also show different methods used in management

accounting and difference between marginal and absorption cost. How these cost affects the

profits in business. Also the pros and cons of different planning tools for preparing budgetary

control. It shows the effect of organization in adopting the management accounting system to

survive and respond to their financial problems.

For undertaking this report the organisation selected is Ryder Architecture. The cited firm

belongs to construction sector and operates in very small area. Thus, this report will help in dev

eloping a relevant management accounting system for the cited establishment.

P-1 Management accounting and its different types

A process of preparing accounting reports that provide timely and accurate financial

information required by managers to take daily decisions. These reports identify, measure,

analyse, intercept and communicate the organization goals. The key difference between

managerial and finance accounting is that managerial accounting helps managers to take

decisions within the organization while financial accounting helps in providing information to

outside parties. Managerial accounting can be done by various techniques like margin analysis,

constraint analysis, capital budgeting, trend analysis, product costing and lean financial

modelling.

Essential requirements of management accounting system are:

Financial planning- It is a process in which planning is done to achieve primary objectives and

goals. It includes both long term and short term financial objectives by formulating policies and

developing procedures. These policies may relate to determination of capital amount, sources of

funds and distribution of income as well as use of debt along with equity capital. To do financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

planning the past data and figures are needed of previous one or two years. Also what are the

goals and objectives that has to be achieved. Experienced managers are required to do a brief

financial planning of the organization.

Analysis of financial statements- It is used so that forecast can be done by using the data of

financial statements. It uses the techniques of trend analysis, cash funds, ratio analysis and cash

flow statements. It helps in giving information which will help the investors and creditors. Its

requirement is that the cash statements, fund statements and profit and loss statements is needed

to analyse the

Historical cost accounting- It provides data of cost relating to each job, process and department

so that comparison can be made with standard cost. It guides the management in cost controlling

and future planning. For this the past data of each employee, its hiring process and the

performance of that employee in that department is needed.

Standard accounting- It is the comparison and analysis of standard cost with actual cost to find

the variance between them. It is done so that remedial actions can be taken to control the cost.

The requirement for standard accounting is the cost sheet of the entire department is needed.

These costs include all the cost that have been incurred on producing a product.

Budgetary control- It is the process of planning and controlling various activities of business

for directing the business in right direction. It is generally done to find the return on investment.

For this the budgets of previous year is needed.

Marginal costing- It uses the technique of different costing and break even analysis for cost

control, decision making and profit maximisation. Break even analysis means a situation where

there is no profit no loss.

Funds flow statements- It helps in analysing the changes in financial position of business

between two dates by comparing the inflow and outflow of funds. It helps a lot in financial

analysis and control and future guidance. It is useful in long term financial planning as it is

based on increase or decrease in the working capital. The requirement to prepare fund flow

goals and objectives that has to be achieved. Experienced managers are required to do a brief

financial planning of the organization.

Analysis of financial statements- It is used so that forecast can be done by using the data of

financial statements. It uses the techniques of trend analysis, cash funds, ratio analysis and cash

flow statements. It helps in giving information which will help the investors and creditors. Its

requirement is that the cash statements, fund statements and profit and loss statements is needed

to analyse the

Historical cost accounting- It provides data of cost relating to each job, process and department

so that comparison can be made with standard cost. It guides the management in cost controlling

and future planning. For this the past data of each employee, its hiring process and the

performance of that employee in that department is needed.

Standard accounting- It is the comparison and analysis of standard cost with actual cost to find

the variance between them. It is done so that remedial actions can be taken to control the cost.

The requirement for standard accounting is the cost sheet of the entire department is needed.

These costs include all the cost that have been incurred on producing a product.

Budgetary control- It is the process of planning and controlling various activities of business

for directing the business in right direction. It is generally done to find the return on investment.

For this the budgets of previous year is needed.

Marginal costing- It uses the technique of different costing and break even analysis for cost

control, decision making and profit maximisation. Break even analysis means a situation where

there is no profit no loss.

Funds flow statements- It helps in analysing the changes in financial position of business

between two dates by comparing the inflow and outflow of funds. It helps a lot in financial

analysis and control and future guidance. It is useful in long term financial planning as it is

based on increase or decrease in the working capital. The requirement to prepare fund flow

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statements is all the information regarding the inflow and outflow of funds. Funds given by

shareholders, employees, etc.

Cash flow statements- It gives the detailed information of inflow and outflow of funds. It is

very useful for liquidity of analysis of business. It summarises the cash inflow and outflow of

business during a particular period, a month or a year. It required the cash inflow and outflow

information of debtors, creditors, current assets, etc.

Decision making- It gives management an option to select the best alternative from different

alternatives through techniques of capital budgeting, marginal costing, etc. the Management

select the best one which will help in maximising the profit. It requires the various reports of the

decision that has bee n taken or feedback of the decision taken.

Revaluation accounting- this technique helps in maintenance of capital of enterprise. It shows

the impact of changes in prices on preparing the financial statements. The information about the

capital of company like its debtors, creditors, fixed assets, current assets, etc.

Statistical and graphical method- It shows the information in various graphical and statistical

technique which helps the management in decision taking. These techniques can be investment ,

master, sales ,etc. the proper facts and figures of previous decision .

Ratio analysis- Its basic functions include forecasting, planning, coordination and control. It

gives the way to control business operations by undertaking both physical and monetary targets.

It requires a proper ratio analysis of different ratios like debt equity ratio, cash equity ratio,

working capital ratio, liquidity ratio, solvency ratio, profitability ratio, quick ratio,dividend ratio,

etc.

P-2 Different methods used for management accounting report.

Management accounting reports helps small business managers and owners to monitor

companies financial performance and are prepared frequently. An owner r manager may

represent these reports weekly, monthly or quarterly (Ax, and Greve, . 2017). there are various

types of reports.

shareholders, employees, etc.

Cash flow statements- It gives the detailed information of inflow and outflow of funds. It is

very useful for liquidity of analysis of business. It summarises the cash inflow and outflow of

business during a particular period, a month or a year. It required the cash inflow and outflow

information of debtors, creditors, current assets, etc.

Decision making- It gives management an option to select the best alternative from different

alternatives through techniques of capital budgeting, marginal costing, etc. the Management

select the best one which will help in maximising the profit. It requires the various reports of the

decision that has bee n taken or feedback of the decision taken.

Revaluation accounting- this technique helps in maintenance of capital of enterprise. It shows

the impact of changes in prices on preparing the financial statements. The information about the

capital of company like its debtors, creditors, fixed assets, current assets, etc.

Statistical and graphical method- It shows the information in various graphical and statistical

technique which helps the management in decision taking. These techniques can be investment ,

master, sales ,etc. the proper facts and figures of previous decision .

Ratio analysis- Its basic functions include forecasting, planning, coordination and control. It

gives the way to control business operations by undertaking both physical and monetary targets.

It requires a proper ratio analysis of different ratios like debt equity ratio, cash equity ratio,

working capital ratio, liquidity ratio, solvency ratio, profitability ratio, quick ratio,dividend ratio,

etc.

P-2 Different methods used for management accounting report.

Management accounting reports helps small business managers and owners to monitor

companies financial performance and are prepared frequently. An owner r manager may

represent these reports weekly, monthly or quarterly (Ax, and Greve, . 2017). there are various

types of reports.

Budget report- it helps to analyse business its performance. If the business is large enough these

reports analyse the performance of each department or division. It is generally prepared for

actual year by taking the data from previous year. These reports also provide information on

incentives of employees. Some funds may be given out to employees for their performance and

are not included in it. It helps in creating report in detailed manner and each end every revenue

and expenses are mentioned in it.

Accounts receivable - it helps the managers in managing cash flow which allows business to

extent their credit to customers. It include the information about how long have the customer is

engaged with business and form how much time he is the creditor of business. It includes the

invoices that are 30,60 or 90 days or more which helps in finding out the problem of the business

collection process (Fullerton, and et.al, 2013). If nay particular customer is unable to pay their

balance the company must need to make strong credit policies regarding this. It also helps in

collection department to view their old debts amount and restricting them to give further debt to

customer.

Job cost reports- it shows expenses for a specific project. They are matched with the revenue to

evaluate jobs probability helps in identifying the areas where there are growth opportunities .

The focus is entirely on those area. Instead of wasting time and money low profit margin areas,

business focus on other area. It is also used in analysing the expenses during the progress of

project so that managers can correct the waste areas where cost is being incurred.

Inventory and manufacturing- these reports are generally used in companies which uses

physical inventory to make their manufacturing process more efficient. They include working

hours, labour cost, per unit overhead cost,etc. Then comparison is made by manager between

different assembly line within the company and decision are taken to improve low performing

departments by providing them more funds (Fullerton, and et.al, 2014)

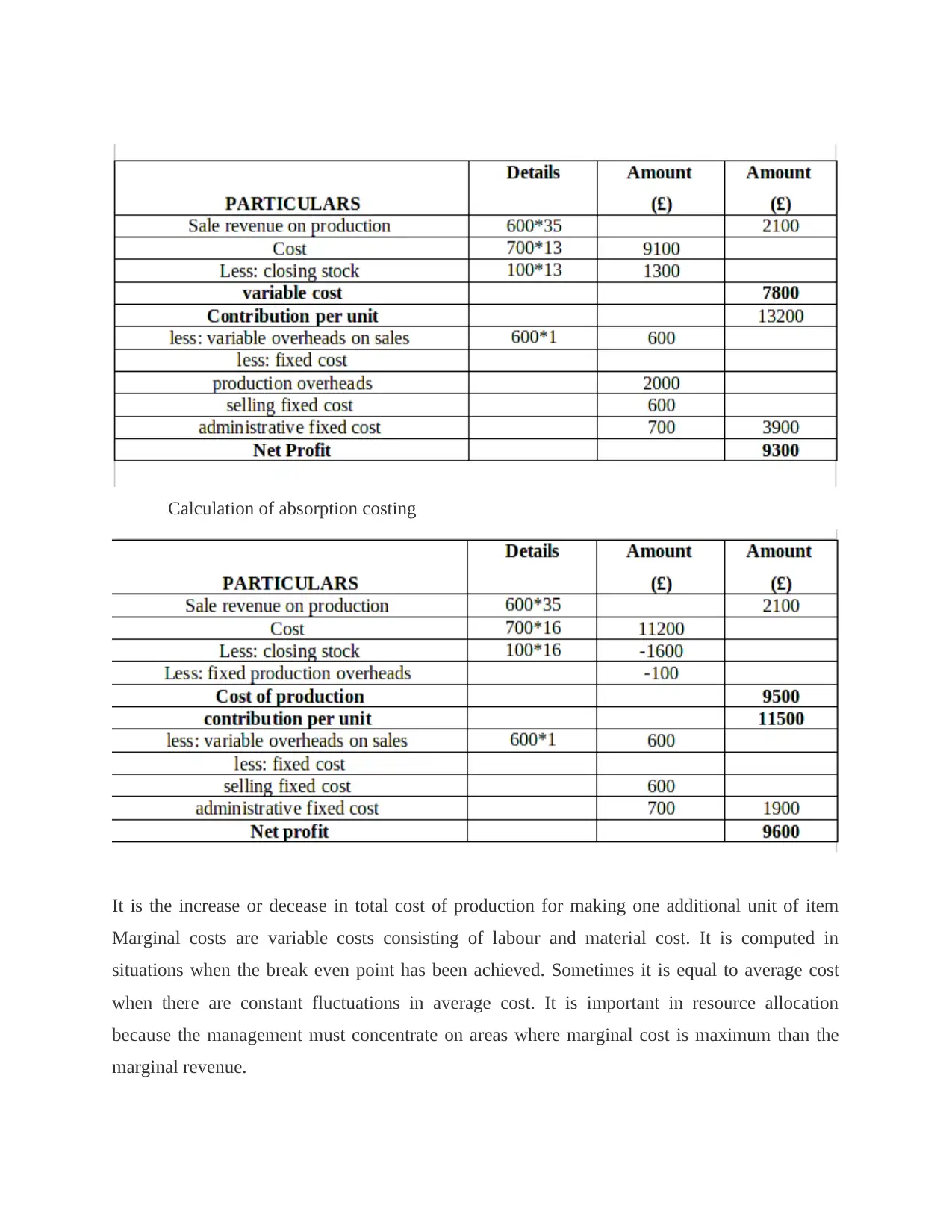

P-3 Marginal costs and absorption costs.

Calculation of marginal costing

reports analyse the performance of each department or division. It is generally prepared for

actual year by taking the data from previous year. These reports also provide information on

incentives of employees. Some funds may be given out to employees for their performance and

are not included in it. It helps in creating report in detailed manner and each end every revenue

and expenses are mentioned in it.

Accounts receivable - it helps the managers in managing cash flow which allows business to

extent their credit to customers. It include the information about how long have the customer is

engaged with business and form how much time he is the creditor of business. It includes the

invoices that are 30,60 or 90 days or more which helps in finding out the problem of the business

collection process (Fullerton, and et.al, 2013). If nay particular customer is unable to pay their

balance the company must need to make strong credit policies regarding this. It also helps in

collection department to view their old debts amount and restricting them to give further debt to

customer.

Job cost reports- it shows expenses for a specific project. They are matched with the revenue to

evaluate jobs probability helps in identifying the areas where there are growth opportunities .

The focus is entirely on those area. Instead of wasting time and money low profit margin areas,

business focus on other area. It is also used in analysing the expenses during the progress of

project so that managers can correct the waste areas where cost is being incurred.

Inventory and manufacturing- these reports are generally used in companies which uses

physical inventory to make their manufacturing process more efficient. They include working

hours, labour cost, per unit overhead cost,etc. Then comparison is made by manager between

different assembly line within the company and decision are taken to improve low performing

departments by providing them more funds (Fullerton, and et.al, 2014)

P-3 Marginal costs and absorption costs.

Calculation of marginal costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation of absorption costing

It is the increase or decease in total cost of production for making one additional unit of item

Marginal costs are variable costs consisting of labour and material cost. It is computed in

situations when the break even point has been achieved. Sometimes it is equal to average cost

when there are constant fluctuations in average cost. It is important in resource allocation

because the management must concentrate on areas where marginal cost is maximum than the

marginal revenue.

It is the increase or decease in total cost of production for making one additional unit of item

Marginal costs are variable costs consisting of labour and material cost. It is computed in

situations when the break even point has been achieved. Sometimes it is equal to average cost

when there are constant fluctuations in average cost. It is important in resource allocation

because the management must concentrate on areas where marginal cost is maximum than the

marginal revenue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption cost- A method in which all fixed and variable cost are considered as product cost. It

ensures that the incurred cost can be recovered by selling the product. Some fixed costs include

wages of labour, raw materials cost, etc. and variable cost include cost used in producing

product.

Difference between marginal and absorption costs:

Basis Marginal cost Absorption cost

Meaning A decision making technique

for getting the total cost of

production

A method in which total cost

of production is ascertained by

fixed and variable cost

Classification Fixed and variable Production, selling and

distribution

Cost recognition Variable cost is considered as

product cost and fixed cost is

considered as period cost

Both fixed and variable cost is

considered as product cost

Highlights Contribution per unit Profit per unit

Cost per unit Opening and closing stock

does not influence the cost per

unit

Opening and closing stock

influences the cost per unit.

Profitability It does not get affected It gets affected.

Cost data Presented to total contribution

of each product

Presented in conventional way.

Decision making It is used in decision making

process

It is used for external reporting

Inventory valuation It is not used for inventory

valuation

It can be used for inventory

valuation

ensures that the incurred cost can be recovered by selling the product. Some fixed costs include

wages of labour, raw materials cost, etc. and variable cost include cost used in producing

product.

Difference between marginal and absorption costs:

Basis Marginal cost Absorption cost

Meaning A decision making technique

for getting the total cost of

production

A method in which total cost

of production is ascertained by

fixed and variable cost

Classification Fixed and variable Production, selling and

distribution

Cost recognition Variable cost is considered as

product cost and fixed cost is

considered as period cost

Both fixed and variable cost is

considered as product cost

Highlights Contribution per unit Profit per unit

Cost per unit Opening and closing stock

does not influence the cost per

unit

Opening and closing stock

influences the cost per unit.

Profitability It does not get affected It gets affected.

Cost data Presented to total contribution

of each product

Presented in conventional way.

Decision making It is used in decision making

process

It is used for external reporting

Inventory valuation It is not used for inventory

valuation

It can be used for inventory

valuation

Fixed production overhead It does not consider fixed

production overhead

Fixed production overhead s

considered.

P-4 Advantages and disadvantages of different budgeting tools.

Budgeting is the formulation of plans in numerical terms for future period. Business

make budgets for departments, divisions or for the whole organization. It is generally made for

one year. There are different kinds of budgets made by organization.

Different tools of budgeting-

Standards- it helps the project manager to set standards to monitor progress. These standards

helps in controlling budget by maintaining a specific cost and amount required for project. Its

advantage is it help the manager to focus on other issues if the costs remain same within the

budget. These provide benchmarks for employees to judge their performance. It also helps in

recording of actual costs thereby setting standard cost for each job, labour, material and

overhead. It also provides integrity in the business as it establish what costs should be, who is

responsible for them and what actual costs are under control. The disadvantage are its prepared

on monthly basis and are often released on end of each month. If managers are incentives and

prepare reports on the basis of variance then it becomes difficult for them to take favourable

decisions.

Analogous- It uses the actual cost as a base for estimating the cost of new project. It is

beneficial only when the two projects are similar in nature. It is generally used by less

experienced managers. Its advantage is that the estimation is based on history of project so it

becomes easy to define the cost of new project. The time required to make the estimate is also

less. Its disadvantage is that the estimation made may not be always accurate.

Parametric- It uses the historical data and other variables to estimate the cost of new project. In

this the cost, time duration and scope of the new project. The advantages of this tool is that it

gives more accurate estimate than the analogous but its disadvantage is that all the variables

taken must be scalable to give accurate estimate of project. Each variable have to be briefly

discussed and only after that the estimation is made so it becomes time consuming process.

production overhead

Fixed production overhead s

considered.

P-4 Advantages and disadvantages of different budgeting tools.

Budgeting is the formulation of plans in numerical terms for future period. Business

make budgets for departments, divisions or for the whole organization. It is generally made for

one year. There are different kinds of budgets made by organization.

Different tools of budgeting-

Standards- it helps the project manager to set standards to monitor progress. These standards

helps in controlling budget by maintaining a specific cost and amount required for project. Its

advantage is it help the manager to focus on other issues if the costs remain same within the

budget. These provide benchmarks for employees to judge their performance. It also helps in

recording of actual costs thereby setting standard cost for each job, labour, material and

overhead. It also provides integrity in the business as it establish what costs should be, who is

responsible for them and what actual costs are under control. The disadvantage are its prepared

on monthly basis and are often released on end of each month. If managers are incentives and

prepare reports on the basis of variance then it becomes difficult for them to take favourable

decisions.

Analogous- It uses the actual cost as a base for estimating the cost of new project. It is

beneficial only when the two projects are similar in nature. It is generally used by less

experienced managers. Its advantage is that the estimation is based on history of project so it

becomes easy to define the cost of new project. The time required to make the estimate is also

less. Its disadvantage is that the estimation made may not be always accurate.

Parametric- It uses the historical data and other variables to estimate the cost of new project. In

this the cost, time duration and scope of the new project. The advantages of this tool is that it

gives more accurate estimate than the analogous but its disadvantage is that all the variables

taken must be scalable to give accurate estimate of project. Each variable have to be briefly

discussed and only after that the estimation is made so it becomes time consuming process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Top down method- It prepares the budget by estimating the cost of each process involved in

project. By doing this the manager decides in which process to provide more funds. The entire

decision making is in the hand of project manager. Its main advantage is that the cost of each

process is determined which helps in overall estimation of project at once. The operation and

maintenance resources do not impact the entire project. In this the employees know their roles

that what its expected from them. It is the managers in controlling the quality. Each person is

ranked at the same level. Its disadvantage there is an impact on morale of employees. The

employees who wish to have an emotional stake in their job, it demoralizes them. Managers are

not able to see what level of talent is there in the employees. The most creative employees starts

looking for a new opportunities that recognises their ability. It also becomes difficult to retain

employees.

Bottom up method- In this the project manager uses the quality of inputs to determine the

overall cost of project. The quality of result is entirely dependent on quality of inputs used.

Various software are used such as smart sheet, ace project,etc. to analyse the cost or project. Its

advantages is that the motivation of employees is increased due to ownership of budget. It is

decentralised budgeting system which helps in participation of employees as well. It leads to

more motivated and involvement of employees. It suits large organisation where there are many

department. They are more accurate as they are prepared by employees and managers who are

closet to sources of revenues and have expertise and knowledge. The employees become more

familiar with department to set the budget. It helps in better communication and coordination

between managers and departments. The disadvantage is that sometimes the decision taken may

be ineffective due to inexperienced mangers. Also, the budget preparation is slow and may arise

disputes between various departments. It includes budgetary slack problem which means the

mangers set targets which are easy to achieve. A lot of time is required in preparing this budget.

Also the lower level employees lacks expertise in resources allocation. Managers also may not

be able to find cost saving or a particular area and this may lead to increase in expenses.

Managers may have the knowledge of other department but they don't know the strategic goals

and financial objectives of the overall organisation.

The types of planning tool are as follows-

project. By doing this the manager decides in which process to provide more funds. The entire

decision making is in the hand of project manager. Its main advantage is that the cost of each

process is determined which helps in overall estimation of project at once. The operation and

maintenance resources do not impact the entire project. In this the employees know their roles

that what its expected from them. It is the managers in controlling the quality. Each person is

ranked at the same level. Its disadvantage there is an impact on morale of employees. The

employees who wish to have an emotional stake in their job, it demoralizes them. Managers are

not able to see what level of talent is there in the employees. The most creative employees starts

looking for a new opportunities that recognises their ability. It also becomes difficult to retain

employees.

Bottom up method- In this the project manager uses the quality of inputs to determine the

overall cost of project. The quality of result is entirely dependent on quality of inputs used.

Various software are used such as smart sheet, ace project,etc. to analyse the cost or project. Its

advantages is that the motivation of employees is increased due to ownership of budget. It is

decentralised budgeting system which helps in participation of employees as well. It leads to

more motivated and involvement of employees. It suits large organisation where there are many

department. They are more accurate as they are prepared by employees and managers who are

closet to sources of revenues and have expertise and knowledge. The employees become more

familiar with department to set the budget. It helps in better communication and coordination

between managers and departments. The disadvantage is that sometimes the decision taken may

be ineffective due to inexperienced mangers. Also, the budget preparation is slow and may arise

disputes between various departments. It includes budgetary slack problem which means the

mangers set targets which are easy to achieve. A lot of time is required in preparing this budget.

Also the lower level employees lacks expertise in resources allocation. Managers also may not

be able to find cost saving or a particular area and this may lead to increase in expenses.

Managers may have the knowledge of other department but they don't know the strategic goals

and financial objectives of the overall organisation.

The types of planning tool are as follows-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero based budgeting

The budget is prepared from the scratch base without indulging any previous year

historical figures in current year preparation.

Advantages

It is simple to prepare as no past year figures are taken.

No budget inflation prevails as entire budget is prepared from zero base.

Disadvantages

It is time-consuming as no reference is taken from past budget

It is disadvantageous because manpower is required which affects their routine work.

NPV

NPV is an effective planning tool which help to judge profitability aspect of new

investment and provides clarity whether investment should be made or not.

Advantages

It is suitable to use as cash flows are taken into account for assessing profitability of

project.

This method is helpful as it considers time value of money.

Disadvantages

The technique only judges profitability aspect but do not measures size of the project.

Discounting rate is based on estimation and generates unreliable results.

IRR

This technique is used to judge potential returns of the project. It is based on the formula

of NPV.

Advantages

The budget is prepared from the scratch base without indulging any previous year

historical figures in current year preparation.

Advantages

It is simple to prepare as no past year figures are taken.

No budget inflation prevails as entire budget is prepared from zero base.

Disadvantages

It is time-consuming as no reference is taken from past budget

It is disadvantageous because manpower is required which affects their routine work.

NPV

NPV is an effective planning tool which help to judge profitability aspect of new

investment and provides clarity whether investment should be made or not.

Advantages

It is suitable to use as cash flows are taken into account for assessing profitability of

project.

This method is helpful as it considers time value of money.

Disadvantages

The technique only judges profitability aspect but do not measures size of the project.

Discounting rate is based on estimation and generates unreliable results.

IRR

This technique is used to judge potential returns of the project. It is based on the formula

of NPV.

Advantages

Concept of time value of money is taken into account.

It is quite easy to calculate and interpret results

Disadvantages

Future costs are not considers which affects results drawn.

It is unsuitable when two projects to be assess have unequal size.

P-5 Adaptation of accounting system in organizations.

In today's constantly changing business environment it is important that the management

accounting officer must include all the factors that are required while making a budget. The

manager should be able to take good decisions that must help in achieving the objectives and

goals of business. It is important to have a flexible budget to survive n the market. The budget

must be made by focusing on the requirements of all the departments of organization. Time.

Cost, ,labour, etc and many other factors must be considered. Various accounting systems are:

Managerial accounting- it helps managers to provide information for planning, controlling and

managing the operations of business. On the basis of this important decisions are made by

managers for business. One type of managerial accounting is cost accounting in which the

managers compare the actual costs incurred in delivering a product with the planned costs. The

difference between them is been investigated by the managers. Another type of managerial

accounting is lean accounting in which the managers evaluate the process to decrease the cost of

products by eliminating the waste of resources.(.Maas, and et.al, 2016). Many big organization

follow this accounting system by hiring experienced managers. It helps in solving the financial

issues within the firm. If any business is investing too much on a particular department this

accounting helps in analysing that making equal distribution of resources to each department.

Thy focus on future actions to be taken by in order to improve the financial performance of the

organization. Due to the changing business environment if there comes any change in business

process the mangers can control that with the plan that they have made.

It is quite easy to calculate and interpret results

Disadvantages

Future costs are not considers which affects results drawn.

It is unsuitable when two projects to be assess have unequal size.

P-5 Adaptation of accounting system in organizations.

In today's constantly changing business environment it is important that the management

accounting officer must include all the factors that are required while making a budget. The

manager should be able to take good decisions that must help in achieving the objectives and

goals of business. It is important to have a flexible budget to survive n the market. The budget

must be made by focusing on the requirements of all the departments of organization. Time.

Cost, ,labour, etc and many other factors must be considered. Various accounting systems are:

Managerial accounting- it helps managers to provide information for planning, controlling and

managing the operations of business. On the basis of this important decisions are made by

managers for business. One type of managerial accounting is cost accounting in which the

managers compare the actual costs incurred in delivering a product with the planned costs. The

difference between them is been investigated by the managers. Another type of managerial

accounting is lean accounting in which the managers evaluate the process to decrease the cost of

products by eliminating the waste of resources.(.Maas, and et.al, 2016). Many big organization

follow this accounting system by hiring experienced managers. It helps in solving the financial

issues within the firm. If any business is investing too much on a particular department this

accounting helps in analysing that making equal distribution of resources to each department.

Thy focus on future actions to be taken by in order to improve the financial performance of the

organization. Due to the changing business environment if there comes any change in business

process the mangers can control that with the plan that they have made.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.