Detailed Analysis of Management Accounting Systems for Aston Chemicals

VerifiedAdded on 2020/12/30

|20

|5519

|52

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Aston Chemicals. It begins by defining management accounting and outlining its benefits, including various costing systems like cost accounting and job costing. The report then explains different types of management accounting reports, such as budget reports and performance reports, and their significance. It further evaluates the integration of management accounting and reporting systems. The report delves into absorption costing and marginal costing, illustrating their use with income statements and break-even analysis. Planning tools for budgetary control, along with their advantages and disadvantages, are discussed. The report analyzes how Aston Chemicals' management accounting techniques respond to financial problems and concludes with an evaluation of how planning tools can solve financial issues. The report also includes tables to help with the understanding of the concepts.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1 ...........................................................................................................................................4

Explaining management accounting and various benefits of management accounting. ............4

Explaining the different types of management accounting reports ............................................6

Benefits of management accounting systems and how they applied in the organization...........7

Evaluating the integration of management accounting systems and management reporting

systems in an organization. ........................................................................................................8

TASK 2 ...........................................................................................................................................8

Explaining the absorption costing and marginal costing............................................................8

Drawing a income statements with the help of marginal and absorption costing .....................9

B. Computing the following problem with the help of break-even analysis. ..........................11

Applying the range of techniques in producing the financial report. .......................................12

Producing the financial report that accurately apply and interpret data for business activity.. 13

TASK 3..........................................................................................................................................14

A. Advantages and disadvantages of planning tools for budgetary control..............................14

B. Application of the planning tools for preparing, forecasting and analysing budgets...........15

C. Comparing the management accounting systems of Aston Chemicals and how it deals with

the financial problems...............................................................................................................16

D. Analysing how Aston Chemical's management accounting techniques respond to financial

problems....................................................................................................................................16

E. Evaluating how planning tools can be used to solve financial problems.............................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................4

TASK 1 ...........................................................................................................................................4

Explaining management accounting and various benefits of management accounting. ............4

Explaining the different types of management accounting reports ............................................6

Benefits of management accounting systems and how they applied in the organization...........7

Evaluating the integration of management accounting systems and management reporting

systems in an organization. ........................................................................................................8

TASK 2 ...........................................................................................................................................8

Explaining the absorption costing and marginal costing............................................................8

Drawing a income statements with the help of marginal and absorption costing .....................9

B. Computing the following problem with the help of break-even analysis. ..........................11

Applying the range of techniques in producing the financial report. .......................................12

Producing the financial report that accurately apply and interpret data for business activity.. 13

TASK 3..........................................................................................................................................14

A. Advantages and disadvantages of planning tools for budgetary control..............................14

B. Application of the planning tools for preparing, forecasting and analysing budgets...........15

C. Comparing the management accounting systems of Aston Chemicals and how it deals with

the financial problems...............................................................................................................16

D. Analysing how Aston Chemical's management accounting techniques respond to financial

problems....................................................................................................................................16

E. Evaluating how planning tools can be used to solve financial problems.............................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

Index of Tables

Table 1: benefits of management accounting..................................................................................8

Table 2: income statement with Marginal costing.........................................................................10

Table 3: income statement with Absorption costing......................................................................11

Table 4: break even analysis .........................................................................................................12

Table 1: benefits of management accounting..................................................................................8

Table 2: income statement with Marginal costing.........................................................................10

Table 3: income statement with Absorption costing......................................................................11

Table 4: break even analysis .........................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting plays an important role in business organization. It is a type of

accounting which helps manager in decision making. Decision making is process which takes

place in every organization.

Aston chemicals was formed in 1990. It provides raw materials to European personal care

industries. The present assignment is based on management accounting. Present assignment will

explain meaning of management accounting and also provide essential requirements of different

types of management accounting systems and their benefits. Report will also present different

type of management accounting reports and their importance in Aston Chemicals. This

assignment will also provide deep insight of integration of management accounting system and

management reporting. Report will also depict information about marginal and absorption

costing techniques of accounting with their income statements. The advantages and

disadvantages of different planning tools for budgetary control will be covered in report. Later, it

will provide techniques of management accounting with respect to responding financial

problems.

TASK 1

Explaining management accounting and various benefits of management accounting.

Management accounting is a profession that consisted of combination of financial and

non-financial statements which gives useful information to management for managers to take an

effective decision making. It plays a very significant role in giving information to workers

working inside organization. It has very wide scope as it gathers and retrieve all information that

is related to particular organization.

It includes process of preparation of managerial reports accounts helping to render

accurate and well-timed financial and statistical data that is essential for managers to make

important judgments in business organization. Unlike financial accounting, MA gives

information in the format of report on weakly basis to managers of departments and CEO.

Different types of management accounting systems are discussed under.

Cost accounting systems

This system of accounting is also known as product costing and costing systems. This a

technique which management of Aston Chemicals used for estimating the cost of their products

for valuing their inventory, analyzing profit and to control cost. Sometimes it becomes difficult

Management accounting plays an important role in business organization. It is a type of

accounting which helps manager in decision making. Decision making is process which takes

place in every organization.

Aston chemicals was formed in 1990. It provides raw materials to European personal care

industries. The present assignment is based on management accounting. Present assignment will

explain meaning of management accounting and also provide essential requirements of different

types of management accounting systems and their benefits. Report will also present different

type of management accounting reports and their importance in Aston Chemicals. This

assignment will also provide deep insight of integration of management accounting system and

management reporting. Report will also depict information about marginal and absorption

costing techniques of accounting with their income statements. The advantages and

disadvantages of different planning tools for budgetary control will be covered in report. Later, it

will provide techniques of management accounting with respect to responding financial

problems.

TASK 1

Explaining management accounting and various benefits of management accounting.

Management accounting is a profession that consisted of combination of financial and

non-financial statements which gives useful information to management for managers to take an

effective decision making. It plays a very significant role in giving information to workers

working inside organization. It has very wide scope as it gathers and retrieve all information that

is related to particular organization.

It includes process of preparation of managerial reports accounts helping to render

accurate and well-timed financial and statistical data that is essential for managers to make

important judgments in business organization. Unlike financial accounting, MA gives

information in the format of report on weakly basis to managers of departments and CEO.

Different types of management accounting systems are discussed under.

Cost accounting systems

This system of accounting is also known as product costing and costing systems. This a

technique which management of Aston Chemicals used for estimating the cost of their products

for valuing their inventory, analyzing profit and to control cost. Sometimes it becomes difficult

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to estimate the correct cost for product and services so that profit can be earned. For an

organization it is very important to them to know about profitable or non-profitable services

products in organization should have and this could only be possible when organization have

estimated the correct cost of product (Ax and Greve, 2017). This systems help Aston chemicals

in identifying exact cost for products which are essential to them. Includes the three costing

examples which helps management is ascertaining the good cost accounting system that are

standard, normal and actual costing.

Requirements

It is required measuring the efficiency of organization. It is required in fixation of prices.

Job costing system

Allotment of manufacturing cost to individual products and batches of products known as

job costing system. When product manufactured are sufficiently different from each other job

costing systems are used. The management of Aston chemicals uses job costing when

management have to allocate manufacturing cost in organization.

Requirements

It is required to obtain the cost of each activity individually. It is required to allocate the cost of each activity.

Prize optimizing systems

The system aids to analyze the best practicable cost that should be quoted for production

of goods and services, is price optimizing system (Cooper, Ezzamel and Qu, 2017). It provides

opportunity to concentrate on different goals and objectives of Aston chemicals.

Requirements It helps in identifying the best possible price of product and services.

Inventory valuation systems

This system inside the organization helps in managing inventories. To manage inventory

in proper way, Aston chemicals uses inventory management systems. The system manages each

and everything for inventory starting from purchasing of raw material to the finished goods and

to closing stock. Examples of these systems are LIFO (Last in first out) and FIFO(First in first

out) these two are inventory management system which helps Aston chemicals in managing

inventories.

organization it is very important to them to know about profitable or non-profitable services

products in organization should have and this could only be possible when organization have

estimated the correct cost of product (Ax and Greve, 2017). This systems help Aston chemicals

in identifying exact cost for products which are essential to them. Includes the three costing

examples which helps management is ascertaining the good cost accounting system that are

standard, normal and actual costing.

Requirements

It is required measuring the efficiency of organization. It is required in fixation of prices.

Job costing system

Allotment of manufacturing cost to individual products and batches of products known as

job costing system. When product manufactured are sufficiently different from each other job

costing systems are used. The management of Aston chemicals uses job costing when

management have to allocate manufacturing cost in organization.

Requirements

It is required to obtain the cost of each activity individually. It is required to allocate the cost of each activity.

Prize optimizing systems

The system aids to analyze the best practicable cost that should be quoted for production

of goods and services, is price optimizing system (Cooper, Ezzamel and Qu, 2017). It provides

opportunity to concentrate on different goals and objectives of Aston chemicals.

Requirements It helps in identifying the best possible price of product and services.

Inventory valuation systems

This system inside the organization helps in managing inventories. To manage inventory

in proper way, Aston chemicals uses inventory management systems. The system manages each

and everything for inventory starting from purchasing of raw material to the finished goods and

to closing stock. Examples of these systems are LIFO (Last in first out) and FIFO(First in first

out) these two are inventory management system which helps Aston chemicals in managing

inventories.

Requirements

It is required in managing the inventory of an enterprise so that warehouse could be

effectively managed

Inventory management system required to enhance the accuracy of inventory.

Explaining the different types of management accounting reports

Management accounting put the emphasis on internal information of organization. The

reports of management accounting are used for regulating, decision making, planning and

measuring performance. These reports are prepared on continuous basis all through financial

years. They provide the internal information of the organization. Following are management

accounting reports which Aston chemical uses are listed under.

Budget reports: Budget reports are the fundamental reports of management accounting.

It is very useful for the manager and owner of the business in understanding and controlling cost

in an organization. It does not matter whether organization is unified or having several

departments (Management Accounting: Meaning, Functions and Characteristics, 2017). Aston

chemicals uses budget reports to understand the grand scheme for their business. With evaluation

of expenses in prior years it becomes easy for organization in estimating the budgets for the year

and finds place to cut costs.

Account receivable aging reports: In an Organization there are some customers's which

are provided with credit facilities. This type of reports is essential for those businesses that offers

credit to the customers. It gives the enactment of credit balances including different categories

for products that are 30, 60 and 90 days late (Eldenburg and et.al., 2016). These reports help the

organization in identifying defaulters as well as issues in administration in collecting that credits.

Aston chemicals prepares accounts receivable aging reports in order to identify the defaulters to

their company.

Job cost report: These report are the sight view of cost accumulated in a one project

while comparing expected revenue obtained by them. This report aids leaders to measure

fruitfulness of particular types of activity and modify their operations by direction on jobs that

provide more profit. This report offers summary of full information. Aston chemicals uses these

report for realization of cost incurred as comparison with their selling price.

It is required in managing the inventory of an enterprise so that warehouse could be

effectively managed

Inventory management system required to enhance the accuracy of inventory.

Explaining the different types of management accounting reports

Management accounting put the emphasis on internal information of organization. The

reports of management accounting are used for regulating, decision making, planning and

measuring performance. These reports are prepared on continuous basis all through financial

years. They provide the internal information of the organization. Following are management

accounting reports which Aston chemical uses are listed under.

Budget reports: Budget reports are the fundamental reports of management accounting.

It is very useful for the manager and owner of the business in understanding and controlling cost

in an organization. It does not matter whether organization is unified or having several

departments (Management Accounting: Meaning, Functions and Characteristics, 2017). Aston

chemicals uses budget reports to understand the grand scheme for their business. With evaluation

of expenses in prior years it becomes easy for organization in estimating the budgets for the year

and finds place to cut costs.

Account receivable aging reports: In an Organization there are some customers's which

are provided with credit facilities. This type of reports is essential for those businesses that offers

credit to the customers. It gives the enactment of credit balances including different categories

for products that are 30, 60 and 90 days late (Eldenburg and et.al., 2016). These reports help the

organization in identifying defaulters as well as issues in administration in collecting that credits.

Aston chemicals prepares accounts receivable aging reports in order to identify the defaulters to

their company.

Job cost report: These report are the sight view of cost accumulated in a one project

while comparing expected revenue obtained by them. This report aids leaders to measure

fruitfulness of particular types of activity and modify their operations by direction on jobs that

provide more profit. This report offers summary of full information. Aston chemicals uses these

report for realization of cost incurred as comparison with their selling price.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance reports: These are the reports which are made to review performance of

whole company as well as new employees. In large organization, departmental reports are

prepared to analyze performance of every departments of organization. Aston chemicals uses

these reports in order to determines performance of an employee as well as organization

(Fullerton, Kennedy and Widener, 2014).

Benefits of management accounting systems and how they applied in the organization.

Management accounting

systems

Benefits

Cost accounting systems It helps in budget compliance, as actual cost is compared

with standard cost to see if any department of business is

spending more than expected.

It helps organization in measuring efficiency, than maintain

and last in improving.

It helps in fixing of prices for the products and services.

It identifies profitable and unprofitable activities of

business.

Job costing system Profit of every activity in the organization is clearly

identified.

Detailed analysis of the cost of material, overhead and labor

of each activity are given by the job costing system.

In job costing management can estimate the cost of job on

the basis of past records.

Prize optimizing systems It helps in investigation of competent cost over product and

services (Kihn and Ihantola, 2015).

It finds out the appropriate cost of several products of goods

and services.

Inventory valuation

systems

The accuracy of inventory orders are improved by inventory

management systems.

It helps in organizing the warehouse properly.

whole company as well as new employees. In large organization, departmental reports are

prepared to analyze performance of every departments of organization. Aston chemicals uses

these reports in order to determines performance of an employee as well as organization

(Fullerton, Kennedy and Widener, 2014).

Benefits of management accounting systems and how they applied in the organization.

Management accounting

systems

Benefits

Cost accounting systems It helps in budget compliance, as actual cost is compared

with standard cost to see if any department of business is

spending more than expected.

It helps organization in measuring efficiency, than maintain

and last in improving.

It helps in fixing of prices for the products and services.

It identifies profitable and unprofitable activities of

business.

Job costing system Profit of every activity in the organization is clearly

identified.

Detailed analysis of the cost of material, overhead and labor

of each activity are given by the job costing system.

In job costing management can estimate the cost of job on

the basis of past records.

Prize optimizing systems It helps in investigation of competent cost over product and

services (Kihn and Ihantola, 2015).

It finds out the appropriate cost of several products of goods

and services.

Inventory valuation

systems

The accuracy of inventory orders are improved by inventory

management systems.

It helps in organizing the warehouse properly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If there are so many places, then this system become

important because necessity to co-ordinate supplies at all

position depends on variances in demand and other factors.

Table 1: benefits of management accounting

Evaluating the integration of management accounting systems and management reporting

systems in an organization.

Management reporting and management accounting systems are efficiently integrated

inside Aston chemicals. Working of both systems leads the organization at top. The qualitative

and quantitative data of functional and operational performances are obtained by integration of

management accounting and reporting systems. The combination of management accounting

systems and reporting is very much beneficial for Aston chemicals. The data obtained from these

managements accounting systems is stored in form of reports and helps in identifying the

performance of organization. The reporting systems are made supervise operations in Aston

chemicals timely. And if any problem arises, corrections are to be taken (Malmi, 2016). This

effective combination helps organization to identify objectives and goals within in time

periphery. Aston chemicals uses these systems in order to identify problems in the organization

in the formal so that appropriate steps are to be taken. This helps firm in developing better

understanding of effective decision-making and helps in establishing the planning in all levels of

organizations.

TASK 2

Explaining the absorption costing and marginal costing.

Absorption costing

Absorption costing is also known as total absorption costing. It is a technique of MA

which imply total cost of production or providing a service. This method not only includes the

cost of labor and material but also all the expenses of production whether fixed or variable. This

method of MA absorbs all the cost that are produced by the units. It is also referred as full

costing method. Absorption costing is frequently line with variable costing or direct costing. It

includes all the cost which are indulged in the production like direct labor, overhead cost and

direct material. Basically, its nature is different from other costing methods because it takes all

the cost into consideration. For Aston absorption costing has proved very beneficial. It

important because necessity to co-ordinate supplies at all

position depends on variances in demand and other factors.

Table 1: benefits of management accounting

Evaluating the integration of management accounting systems and management reporting

systems in an organization.

Management reporting and management accounting systems are efficiently integrated

inside Aston chemicals. Working of both systems leads the organization at top. The qualitative

and quantitative data of functional and operational performances are obtained by integration of

management accounting and reporting systems. The combination of management accounting

systems and reporting is very much beneficial for Aston chemicals. The data obtained from these

managements accounting systems is stored in form of reports and helps in identifying the

performance of organization. The reporting systems are made supervise operations in Aston

chemicals timely. And if any problem arises, corrections are to be taken (Malmi, 2016). This

effective combination helps organization to identify objectives and goals within in time

periphery. Aston chemicals uses these systems in order to identify problems in the organization

in the formal so that appropriate steps are to be taken. This helps firm in developing better

understanding of effective decision-making and helps in establishing the planning in all levels of

organizations.

TASK 2

Explaining the absorption costing and marginal costing.

Absorption costing

Absorption costing is also known as total absorption costing. It is a technique of MA

which imply total cost of production or providing a service. This method not only includes the

cost of labor and material but also all the expenses of production whether fixed or variable. This

method of MA absorbs all the cost that are produced by the units. It is also referred as full

costing method. Absorption costing is frequently line with variable costing or direct costing. It

includes all the cost which are indulged in the production like direct labor, overhead cost and

direct material. Basically, its nature is different from other costing methods because it takes all

the cost into consideration. For Aston absorption costing has proved very beneficial. It

influenced value of fixed costs involved in production (Nitzl, 2018). It displays less modification

in net profits in case of constant production but fluctuating sales.

Marginal costing

In this tool of accounting fixed cost for every period is totally written off against

contribution while variable cost is charged into units. This technique of management accounting

do not consider the fixed cost in estimating the expenses. An extra cost occurred in producing

one single additional is expresses as marginal cost. It is calculated by taking all the variable cost

like , direct material, labor, expenses and other variable overhead.

Direct Labour + Direct Expenses + Direct Material +Variable Overhead + variable

expenses = Marginal Cost

However, it aids managers to taking various decisions of business like discontinuing a

commodity or services, substitutions f machines etc. It also helps management in deciding the

appropriate level of job, through Break Even Point analysis or CVP analysis, that signals the

effect of increasing or decreasing production level, on the company’s overall profit.

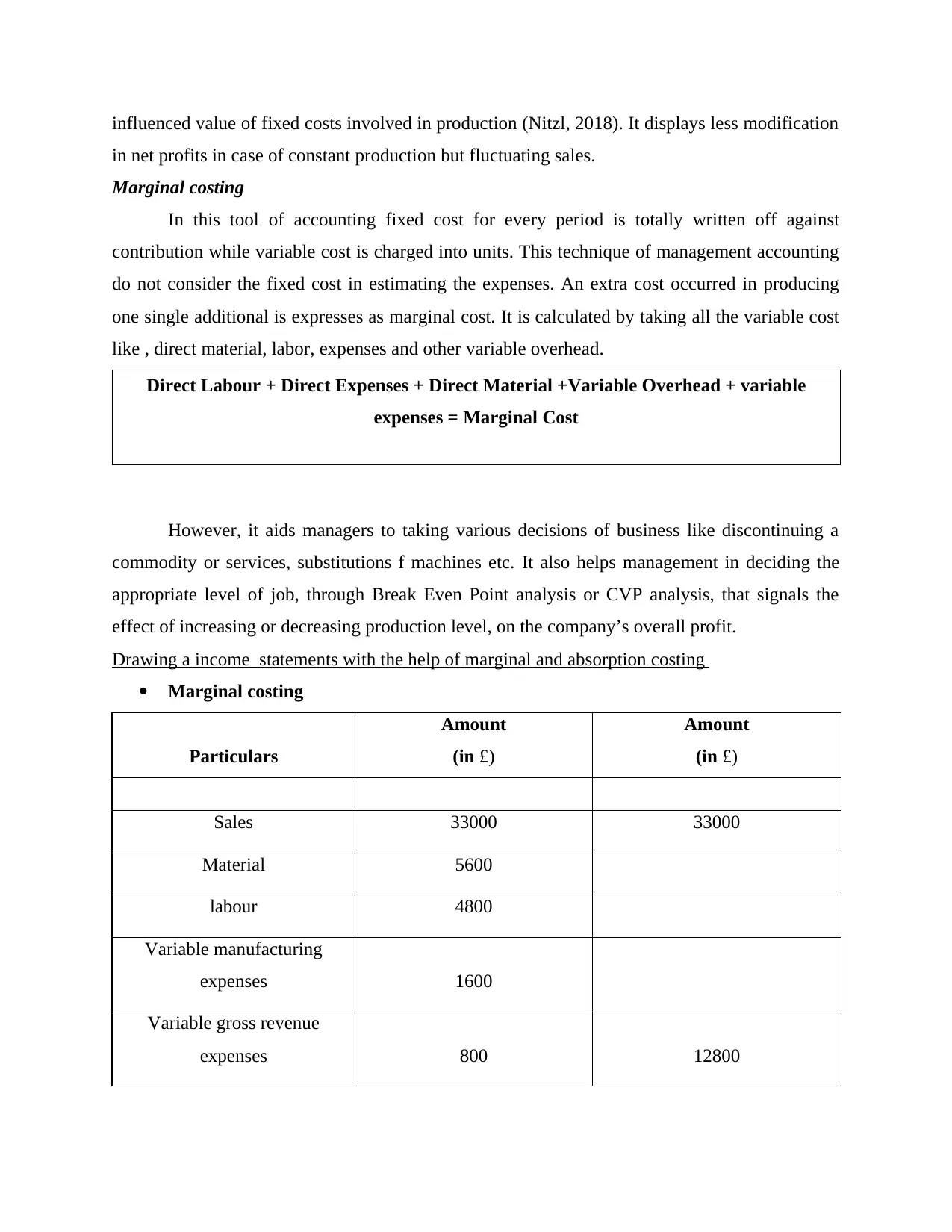

Drawing a income statements with the help of marginal and absorption costing

Marginal costing

Particulars

Amount

(in £)

Amount

(in £)

Sales 33000 33000

Material 5600

labour 4800

Variable manufacturing

expenses 1600

Variable gross revenue

expenses 800 12800

in net profits in case of constant production but fluctuating sales.

Marginal costing

In this tool of accounting fixed cost for every period is totally written off against

contribution while variable cost is charged into units. This technique of management accounting

do not consider the fixed cost in estimating the expenses. An extra cost occurred in producing

one single additional is expresses as marginal cost. It is calculated by taking all the variable cost

like , direct material, labor, expenses and other variable overhead.

Direct Labour + Direct Expenses + Direct Material +Variable Overhead + variable

expenses = Marginal Cost

However, it aids managers to taking various decisions of business like discontinuing a

commodity or services, substitutions f machines etc. It also helps management in deciding the

appropriate level of job, through Break Even Point analysis or CVP analysis, that signals the

effect of increasing or decreasing production level, on the company’s overall profit.

Drawing a income statements with the help of marginal and absorption costing

Marginal costing

Particulars

Amount

(in £)

Amount

(in £)

Sales 33000 33000

Material 5600

labour 4800

Variable manufacturing

expenses 1600

Variable gross revenue

expenses 800 12800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

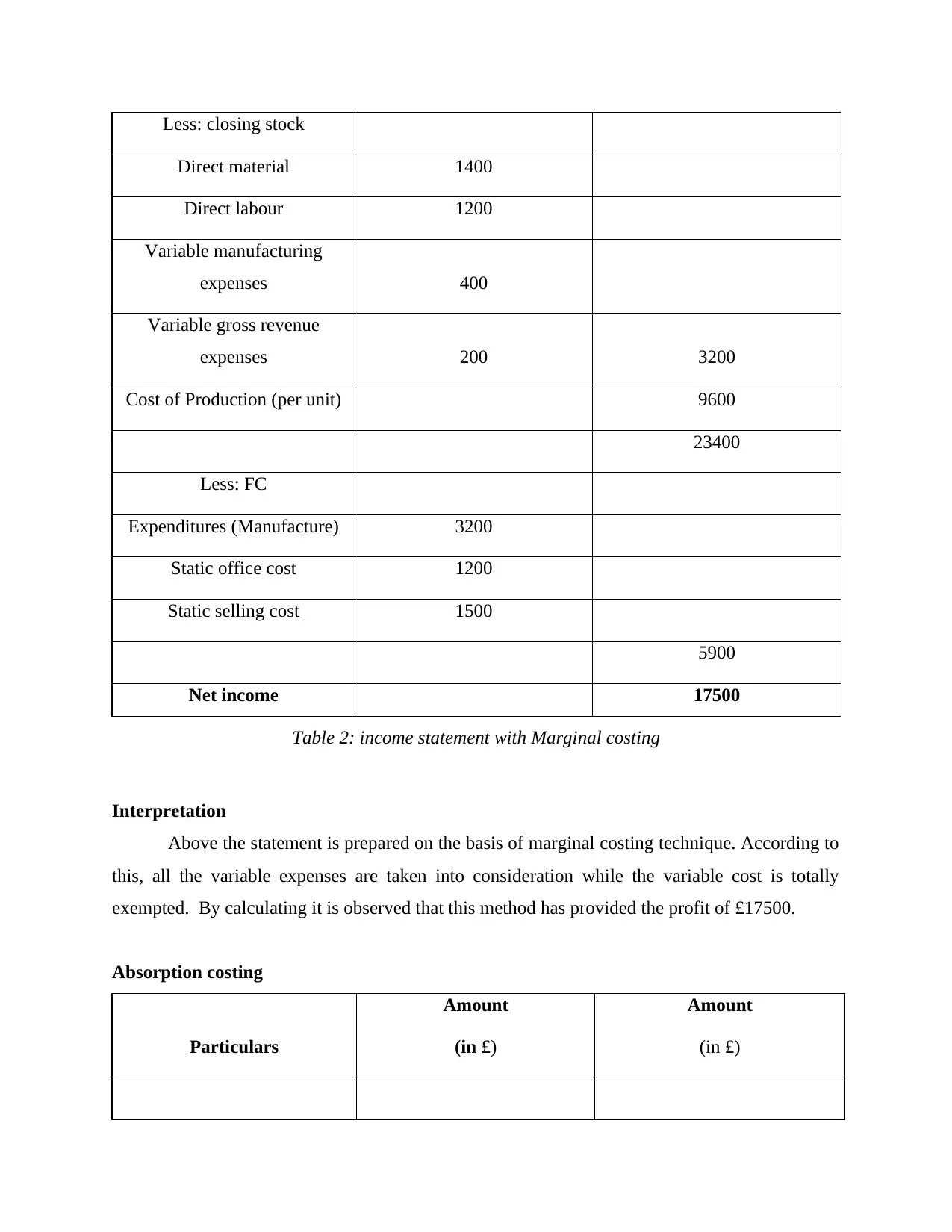

Less: closing stock

Direct material 1400

Direct labour 1200

Variable manufacturing

expenses 400

Variable gross revenue

expenses 200 3200

Cost of Production (per unit) 9600

23400

Less: FC

Expenditures (Manufacture) 3200

Static office cost 1200

Static selling cost 1500

5900

Net income 17500

Table 2: income statement with Marginal costing

Interpretation

Above the statement is prepared on the basis of marginal costing technique. According to

this, all the variable expenses are taken into consideration while the variable cost is totally

exempted. By calculating it is observed that this method has provided the profit of £17500.

Absorption costing

Particulars

Amount

(in £)

Amount

(in £)

Direct material 1400

Direct labour 1200

Variable manufacturing

expenses 400

Variable gross revenue

expenses 200 3200

Cost of Production (per unit) 9600

23400

Less: FC

Expenditures (Manufacture) 3200

Static office cost 1200

Static selling cost 1500

5900

Net income 17500

Table 2: income statement with Marginal costing

Interpretation

Above the statement is prepared on the basis of marginal costing technique. According to

this, all the variable expenses are taken into consideration while the variable cost is totally

exempted. By calculating it is observed that this method has provided the profit of £17500.

Absorption costing

Particulars

Amount

(in £)

Amount

(in £)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Sales 33000 33000

Direct material 5600

Direct labour 4800

Variable expenses 1600

Variable revenue expenses 800 12800

Deduct: stock at the end

DM(direct material) 1400

DL (direct labour) 1200

Variable sales expenses 200

Less: Variable sales overhead 600 3400

Less: Absorption of Overheads

(Fixed)

Cost of production 9400

Per unit contribution 23600

Less: FC

Expenses (production) 3200

Fixed office expense 1200

Fixed selling expense 1500 5900

Net Income 17700

Table 3: income statement with Absorption costing

Interpretation

The method has been adopted for the calculation of following information is absorption

costing for the all the expenses are taken into consideration whether fixed or variable. On

evaluating these figure it is obtained that organization has earned income of £17700, which is

Direct material 5600

Direct labour 4800

Variable expenses 1600

Variable revenue expenses 800 12800

Deduct: stock at the end

DM(direct material) 1400

DL (direct labour) 1200

Variable sales expenses 200

Less: Variable sales overhead 600 3400

Less: Absorption of Overheads

(Fixed)

Cost of production 9400

Per unit contribution 23600

Less: FC

Expenses (production) 3200

Fixed office expense 1200

Fixed selling expense 1500 5900

Net Income 17700

Table 3: income statement with Absorption costing

Interpretation

The method has been adopted for the calculation of following information is absorption

costing for the all the expenses are taken into consideration whether fixed or variable. On

evaluating these figure it is obtained that organization has earned income of £17700, which is

more than marginal costing. So this technique is more useful for the Aston Chemicals for further

use.

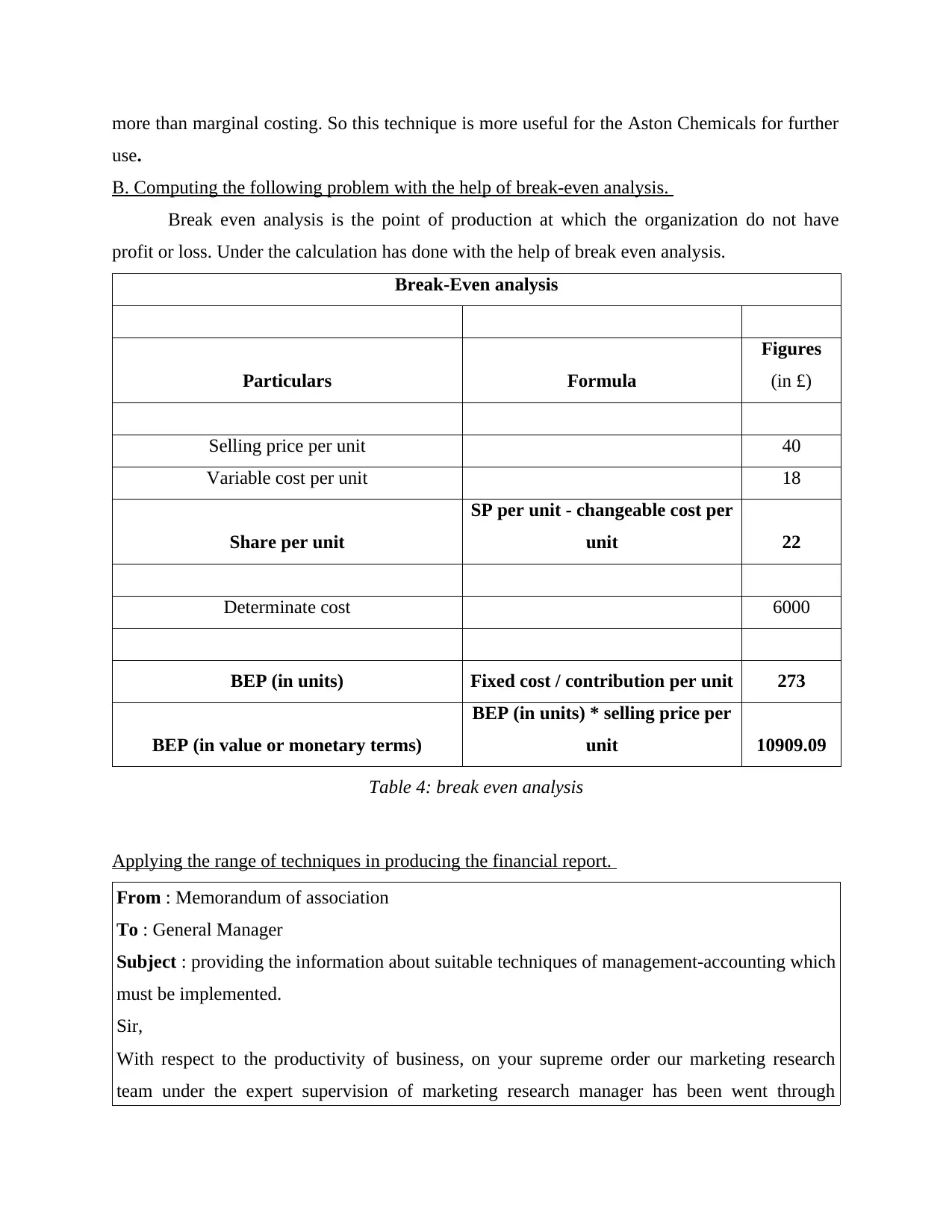

B. Computing the following problem with the help of break-even analysis.

Break even analysis is the point of production at which the organization do not have

profit or loss. Under the calculation has done with the help of break even analysis.

Break-Even analysis

Particulars Formula

Figures

(in £)

Selling price per unit 40

Variable cost per unit 18

Share per unit

SP per unit - changeable cost per

unit 22

Determinate cost 6000

BEP (in units) Fixed cost / contribution per unit 273

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit 10909.09

Table 4: break even analysis

Applying the range of techniques in producing the financial report.

From : Memorandum of association

To : General Manager

Subject : providing the information about suitable techniques of management-accounting which

must be implemented.

Sir,

With respect to the productivity of business, on your supreme order our marketing research

team under the expert supervision of marketing research manager has been went through

use.

B. Computing the following problem with the help of break-even analysis.

Break even analysis is the point of production at which the organization do not have

profit or loss. Under the calculation has done with the help of break even analysis.

Break-Even analysis

Particulars Formula

Figures

(in £)

Selling price per unit 40

Variable cost per unit 18

Share per unit

SP per unit - changeable cost per

unit 22

Determinate cost 6000

BEP (in units) Fixed cost / contribution per unit 273

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit 10909.09

Table 4: break even analysis

Applying the range of techniques in producing the financial report.

From : Memorandum of association

To : General Manager

Subject : providing the information about suitable techniques of management-accounting which

must be implemented.

Sir,

With respect to the productivity of business, on your supreme order our marketing research

team under the expert supervision of marketing research manager has been went through

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.