HNBS 305: Management Accounting Report - UCK Furniture Analysis

VerifiedAdded on 2022/12/23

|25

|3575

|1

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within the context of UCK furniture. It begins by defining management accounting and exploring various systems such as cost accounting, job costing, and inventory management. The report then presents detailed calculations using absorption and marginal costing methods, including cost cards and financial reporting documents. Further, the report analyzes financial data and techniques for a range of business activities, including budgetary reports, inventory management reports, and performance management reports. The report also covers variance analysis, planning tools, and financial problem-solving, providing insights into their importance for business decision-making and financial strategy. The report concludes with an overview of the key findings and their implications for effective management accounting practices.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Management accounting systems:...............................................................................................3

Methods for management accounting reporting:.........................................................................1

Benefits of management accounting system & their applications for businesses:......................2

How management accounting system & management accounting integrated for businesses:....2

TASK 2............................................................................................................................................2

2.1.................................................................................................................................................2

2.2. Apply range of MA techniques and form financial reporting document:.............................4

2.3. Financial reports that accurately apply and interpret data for a range of business activities:

......................................................................................................................................................6

2.4.................................................................................................................................................9

3.1...............................................................................................................................................10

3.2...............................................................................................................................................12

4.1...............................................................................................................................................13

Apply range for management accounting techniques & produce appropriate financial

reporting:....................................................................................................................................14

Importance of variance analysis for businesses:........................................................................15

TASK 3..........................................................................................................................................15

Various planning tools, their advantages & disadvantages:......................................................15

TASK 4..........................................................................................................................................15

Various financial problems:.......................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

Management accounting systems:...............................................................................................3

Methods for management accounting reporting:.........................................................................1

Benefits of management accounting system & their applications for businesses:......................2

How management accounting system & management accounting integrated for businesses:....2

TASK 2............................................................................................................................................2

2.1.................................................................................................................................................2

2.2. Apply range of MA techniques and form financial reporting document:.............................4

2.3. Financial reports that accurately apply and interpret data for a range of business activities:

......................................................................................................................................................6

2.4.................................................................................................................................................9

3.1...............................................................................................................................................10

3.2...............................................................................................................................................12

4.1...............................................................................................................................................13

Apply range for management accounting techniques & produce appropriate financial

reporting:....................................................................................................................................14

Importance of variance analysis for businesses:........................................................................15

TASK 3..........................................................................................................................................15

Various planning tools, their advantages & disadvantages:......................................................15

TASK 4..........................................................................................................................................15

Various financial problems:.......................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

The term management accounting can be defined as an accounting approach which

emphasis on financial and non-financial aspect of company during a specified period of time.

Such accounting is used to present data in form of reports which are used by management team

to take significant actions. The objective of report is to understand role of management

accounting in the context of companies’ day to day operations. The entire part of report is based

on a scenario of UCK furniture which produces different kinds of wooden items. The report

contains detailed information about various accounting techniques systems, reports etc. In

addition to this, planning tools of budgeting are also explained with rational to their importance

to deal with financial issues.

Management accounting systems:

Management accounting is about managing accounting reports which helps management

for generating their activities & helps for strategic decision making. Management includes

planning, organising, analysing, managing, budgeting data for managers for their decision

making.

Management accounting system is about which businesses use for knowing & evaluating

its activities for management for businesses. In context to UCK furniture this company using

management accounting system which helps it for knowing costs for its produce goods,

inventory management, customers demand. It gives views for business decisions for taking

corrective actions. It shows business has various departments because it shows basis for

production & functions for knowing business performance (Abdusalomova, 2019).

Cost accounting system: It is management accounting system which company use for

estimate its value for goods for knowing how much profitability business achieves. In context to

UCK furniture, this company uses this for setting its pricing strategy which helps it for analysing

profitability for business. It is about which helps for knowing where it spend its expenses &

where it which resource helps it for earning. It is about which helps to analyse & report for

improvement for its production costs control & efficiency.

Essential requirements: For this management accounting system, it needs for various

costs which are occur for different manufacture for producing goods. The information which

needs for managers which it gives for their strategic decisions.

The term management accounting can be defined as an accounting approach which

emphasis on financial and non-financial aspect of company during a specified period of time.

Such accounting is used to present data in form of reports which are used by management team

to take significant actions. The objective of report is to understand role of management

accounting in the context of companies’ day to day operations. The entire part of report is based

on a scenario of UCK furniture which produces different kinds of wooden items. The report

contains detailed information about various accounting techniques systems, reports etc. In

addition to this, planning tools of budgeting are also explained with rational to their importance

to deal with financial issues.

Management accounting systems:

Management accounting is about managing accounting reports which helps management

for generating their activities & helps for strategic decision making. Management includes

planning, organising, analysing, managing, budgeting data for managers for their decision

making.

Management accounting system is about which businesses use for knowing & evaluating

its activities for management for businesses. In context to UCK furniture this company using

management accounting system which helps it for knowing costs for its produce goods,

inventory management, customers demand. It gives views for business decisions for taking

corrective actions. It shows business has various departments because it shows basis for

production & functions for knowing business performance (Abdusalomova, 2019).

Cost accounting system: It is management accounting system which company use for

estimate its value for goods for knowing how much profitability business achieves. In context to

UCK furniture, this company uses this for setting its pricing strategy which helps it for analysing

profitability for business. It is about which helps for knowing where it spend its expenses &

where it which resource helps it for earning. It is about which helps to analyse & report for

improvement for its production costs control & efficiency.

Essential requirements: For this management accounting system, it needs for various

costs which are occur for different manufacture for producing goods. The information which

needs for managers which it gives for their strategic decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing system: Job costing is about analysing procedure for business where job is

different & performs according to customers demand. How changes for price has change in

demand for goods which is produce by business. In context to UCK furniture, company uses this

system for analysing company's activities which needs by customers which it controls. The

company use it for analysing its procedure according to customers wants.

Essential requirements: This management accounting system is for how customers

demand affects by change in demand. It is require by senior authority for managing company's

operations. It helps business for setting prices in that manner so that it satisfies customers for

fulfilling their needs & helps business for maintaining profitability (Järvinen, 2016).

Inventory management system: It is about for which business tracks its inventory level,

sales & its orders which it receives by client. Managers using various inventory management

methods which includes average inventory method, FIFO, LIFO etc. the company use it for

create work order & analysis for raw material needed by businesses. In context to UCK furniture,

this business use this management accounting system for knowing inventory performance which

helps its procedures for know about orders.

Essential requirements: This requires for company for knowing its inventory

management, its sales orders, storage costs etc. The managers are needs for this for maintaining

costs of production for setting prices. It helps for maintaining goods costs which gives higher

profitability.

Price optimisation system: This management accounting system which business using

for its mathematical process for knowing various prices for business goods which sales by

various sources. In context to UCK furniture, this company using this system for knowing costs

of each goods produce by it. It helps this business for setting optimum prices for its goods so that

it helps for achieve objectives & gives higher profitability.

Essential requirements: This needs for businesses for knowing information related for

costs which includes for its goods. Managers of business are needs for their strategic decision

making. It helps it for managing expenses & earns higher profitability which shows better

performance.

Methods for management accounting reporting:

Management accounting reporting is a tool which is used by financial managers to do

financial accounting for making decisions, controlling and planning all the operational activities.

different & performs according to customers demand. How changes for price has change in

demand for goods which is produce by business. In context to UCK furniture, company uses this

system for analysing company's activities which needs by customers which it controls. The

company use it for analysing its procedure according to customers wants.

Essential requirements: This management accounting system is for how customers

demand affects by change in demand. It is require by senior authority for managing company's

operations. It helps business for setting prices in that manner so that it satisfies customers for

fulfilling their needs & helps business for maintaining profitability (Järvinen, 2016).

Inventory management system: It is about for which business tracks its inventory level,

sales & its orders which it receives by client. Managers using various inventory management

methods which includes average inventory method, FIFO, LIFO etc. the company use it for

create work order & analysis for raw material needed by businesses. In context to UCK furniture,

this business use this management accounting system for knowing inventory performance which

helps its procedures for know about orders.

Essential requirements: This requires for company for knowing its inventory

management, its sales orders, storage costs etc. The managers are needs for this for maintaining

costs of production for setting prices. It helps for maintaining goods costs which gives higher

profitability.

Price optimisation system: This management accounting system which business using

for its mathematical process for knowing various prices for business goods which sales by

various sources. In context to UCK furniture, this company using this system for knowing costs

of each goods produce by it. It helps this business for setting optimum prices for its goods so that

it helps for achieve objectives & gives higher profitability.

Essential requirements: This needs for businesses for knowing information related for

costs which includes for its goods. Managers of business are needs for their strategic decision

making. It helps it for managing expenses & earns higher profitability which shows better

performance.

Methods for management accounting reporting:

Management accounting reporting is a tool which is used by financial managers to do

financial accounting for making decisions, controlling and planning all the operational activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

UCK furniture uses this mechanism which is useful for making any financial decision regarding

production of product to delivering the final produce to consumers. Following are different

management accounting reports.

Budgetary report

Budgetary report is prepared by accountants and other operational or production

managers of UCK. This report is processed to know about the available funds company have to

spend on the operational and production activities. Cost of producing a new or existing product

needs funds and budgetary report shows available funds.

Inventory management report

Inventory means industrial goods which are used to manufacture goods to be sold or the

goods which are to be sale to the customers. Inventory management report shows how much

industrial goods we have in stock to manufacture consumer goods. Also how many consumers

goods are available for the sales. All and all this report calculates the available inventory of the

company which is used by sales managers of UCK furniture.

Performance management report

UCK furniture uses performance management report to measure the performance of

whole organization or individual employees. This tool is useful to evaluate the progress or

performance of a employee and whole organisation. On the basis of report company decides

what are the major changes should be done to improve the performance (Pedroso and Gomes,

2020).

Accounting receivable report

UCK Furniture have a wide customer range so accounting managers prepare accounting

receivable report to keep a check on financial receivables of the firm. This report is very useful

to evaluate the financial position of the country. A periodic report is prepared to record all the

financial receivable of the firm.

Benefits of management accounting system & their applications for businesses:

It is process which gives financial data for managers for their strategic decision making.

It basically use by internal employees, for statical better decisions. In context to UCK furniture,

this system helps for increase business performance by managing its resources which gives it

competitive advantage, cash flow management, profitability management. Management

production of product to delivering the final produce to consumers. Following are different

management accounting reports.

Budgetary report

Budgetary report is prepared by accountants and other operational or production

managers of UCK. This report is processed to know about the available funds company have to

spend on the operational and production activities. Cost of producing a new or existing product

needs funds and budgetary report shows available funds.

Inventory management report

Inventory means industrial goods which are used to manufacture goods to be sold or the

goods which are to be sale to the customers. Inventory management report shows how much

industrial goods we have in stock to manufacture consumer goods. Also how many consumers

goods are available for the sales. All and all this report calculates the available inventory of the

company which is used by sales managers of UCK furniture.

Performance management report

UCK furniture uses performance management report to measure the performance of

whole organization or individual employees. This tool is useful to evaluate the progress or

performance of a employee and whole organisation. On the basis of report company decides

what are the major changes should be done to improve the performance (Pedroso and Gomes,

2020).

Accounting receivable report

UCK Furniture have a wide customer range so accounting managers prepare accounting

receivable report to keep a check on financial receivables of the firm. This report is very useful

to evaluate the financial position of the country. A periodic report is prepared to record all the

financial receivable of the firm.

Benefits of management accounting system & their applications for businesses:

It is process which gives financial data for managers for their strategic decision making.

It basically use by internal employees, for statical better decisions. In context to UCK furniture,

this system helps for increase business performance by managing its resources which gives it

competitive advantage, cash flow management, profitability management. Management

accounting system helps business for maintaining better performance for businesses (Pervan and

Dropulić, 2019).

How management accounting system & management accounting integrated for businesses:

Management accounting system & methods are integrated as both are suing for keep

tracking financial performance for business. In context to UCK furniture, it gives insight for

managers which increases their decision making & better performance for business activities.

TASK 2

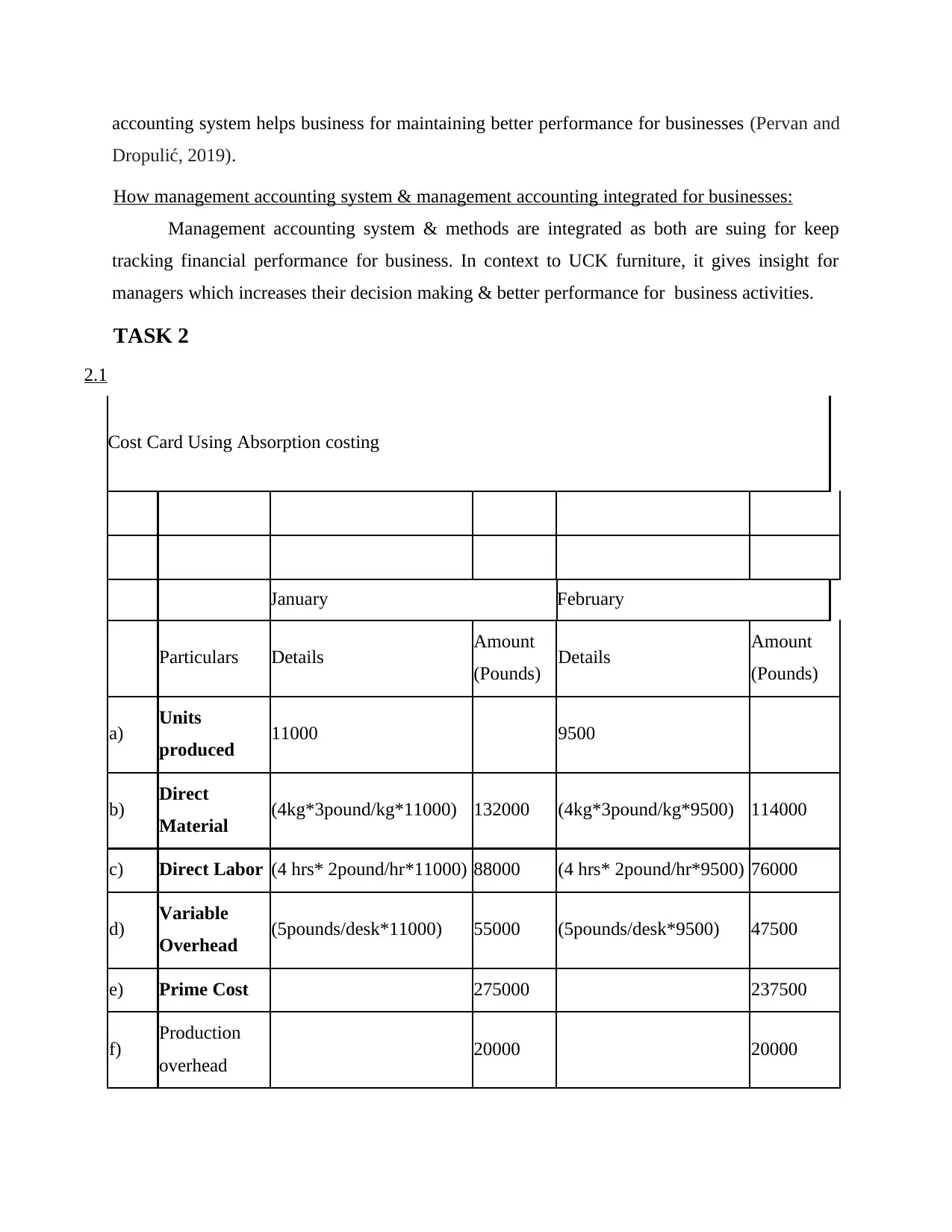

2.1

Cost Card Using Absorption costing

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) Units

produced 11000 9500

b) Direct

Material (4kg*3pound/kg*11000) 132000 (4kg*3pound/kg*9500) 114000

c) Direct Labor (4 hrs* 2pound/hr*11000) 88000 (4 hrs* 2pound/hr*9500) 76000

d) Variable

Overhead (5pounds/desk*11000) 55000 (5pounds/desk*9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

Dropulić, 2019).

How management accounting system & management accounting integrated for businesses:

Management accounting system & methods are integrated as both are suing for keep

tracking financial performance for business. In context to UCK furniture, it gives insight for

managers which increases their decision making & better performance for business activities.

TASK 2

2.1

Cost Card Using Absorption costing

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) Units

produced 11000 9500

b) Direct

Material (4kg*3pound/kg*11000) 132000 (4kg*3pound/kg*9500) 114000

c) Direct Labor (4 hrs* 2pound/hr*11000) 88000 (4 hrs* 2pound/hr*9500) 76000

d) Variable

Overhead (5pounds/desk*11000) 55000 (5pounds/desk*9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

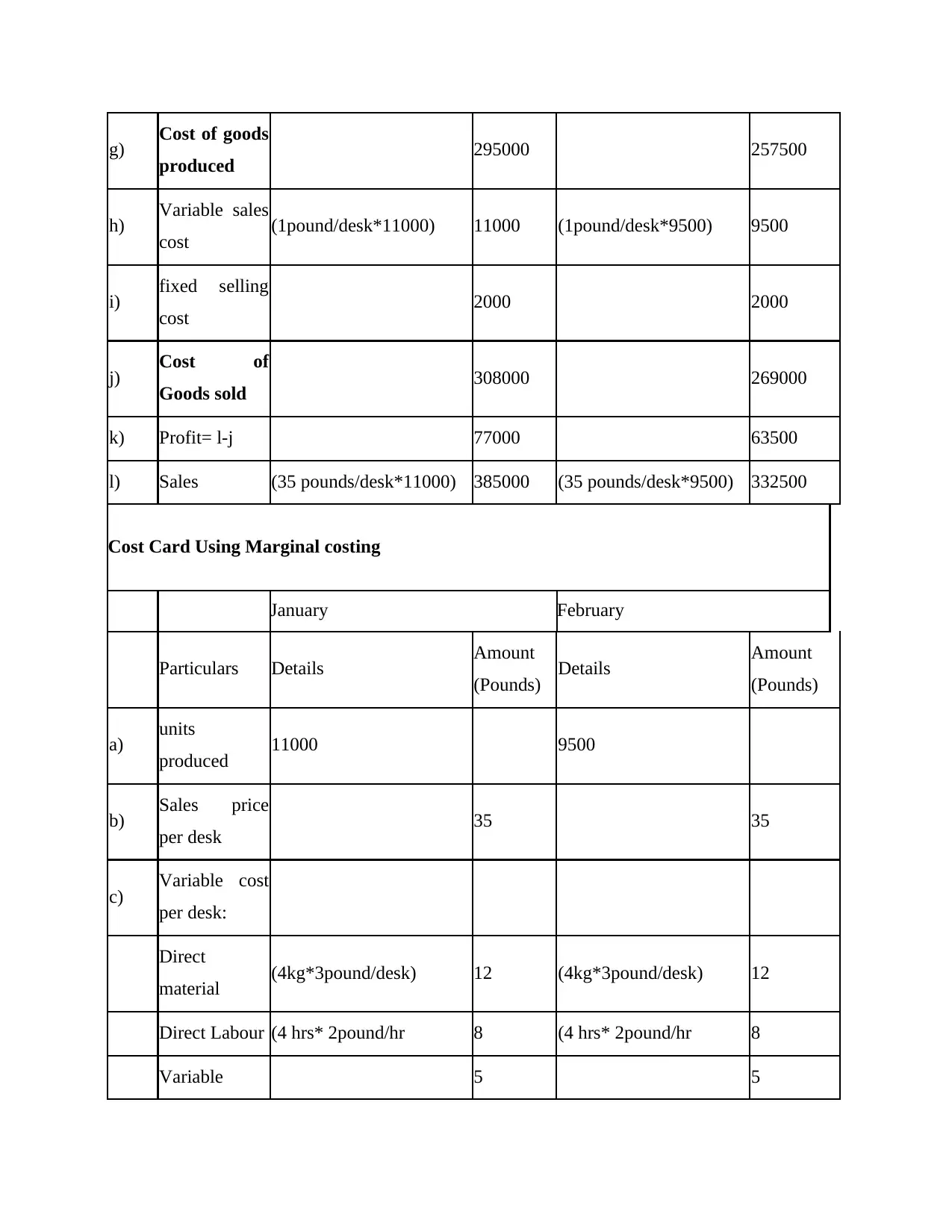

g) Cost of goods

produced 295000 257500

h) Variable sales

cost (1pound/desk*11000) 11000 (1pound/desk*9500) 9500

i) fixed selling

cost 2000 2000

j) Cost of

Goods sold 308000 269000

k) Profit= l-j 77000 63500

l) Sales (35 pounds/desk*11000) 385000 (35 pounds/desk*9500) 332500

Cost Card Using Marginal costing

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) units

produced 11000 9500

b) Sales price

per desk 35 35

c) Variable cost

per desk:

Direct

material (4kg*3pound/desk) 12 (4kg*3pound/desk) 12

Direct Labour (4 hrs* 2pound/hr 8 (4 hrs* 2pound/hr 8

Variable 5 5

produced 295000 257500

h) Variable sales

cost (1pound/desk*11000) 11000 (1pound/desk*9500) 9500

i) fixed selling

cost 2000 2000

j) Cost of

Goods sold 308000 269000

k) Profit= l-j 77000 63500

l) Sales (35 pounds/desk*11000) 385000 (35 pounds/desk*9500) 332500

Cost Card Using Marginal costing

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) units

produced 11000 9500

b) Sales price

per desk 35 35

c) Variable cost

per desk:

Direct

material (4kg*3pound/desk) 12 (4kg*3pound/desk) 12

Direct Labour (4 hrs* 2pound/hr 8 (4 hrs* 2pound/hr 8

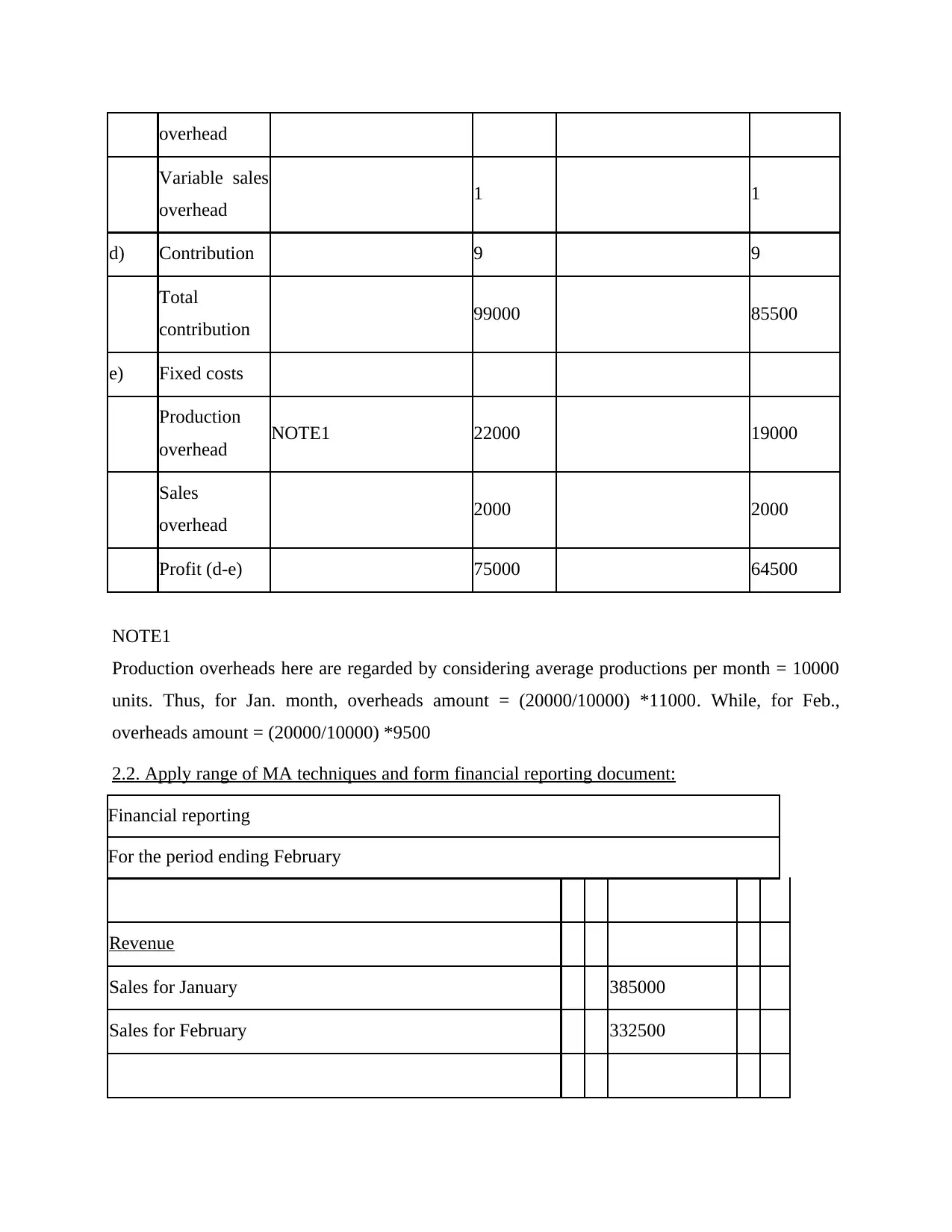

Variable 5 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

overhead

Variable sales

overhead 1 1

d) Contribution 9 9

Total

contribution 99000 85500

e) Fixed costs

Production

overhead NOTE1 22000 19000

Sales

overhead 2000 2000

Profit (d-e) 75000 64500

NOTE1

Production overheads here are regarded by considering average productions per month = 10000

units. Thus, for Jan. month, overheads amount = (20000/10000) *11000. While, for Feb.,

overheads amount = (20000/10000) *9500

2.2. Apply range of MA techniques and form financial reporting document:

Financial reporting

For the period ending February

Revenue

Sales for January 385000

Sales for February 332500

Variable sales

overhead 1 1

d) Contribution 9 9

Total

contribution 99000 85500

e) Fixed costs

Production

overhead NOTE1 22000 19000

Sales

overhead 2000 2000

Profit (d-e) 75000 64500

NOTE1

Production overheads here are regarded by considering average productions per month = 10000

units. Thus, for Jan. month, overheads amount = (20000/10000) *11000. While, for Feb.,

overheads amount = (20000/10000) *9500

2.2. Apply range of MA techniques and form financial reporting document:

Financial reporting

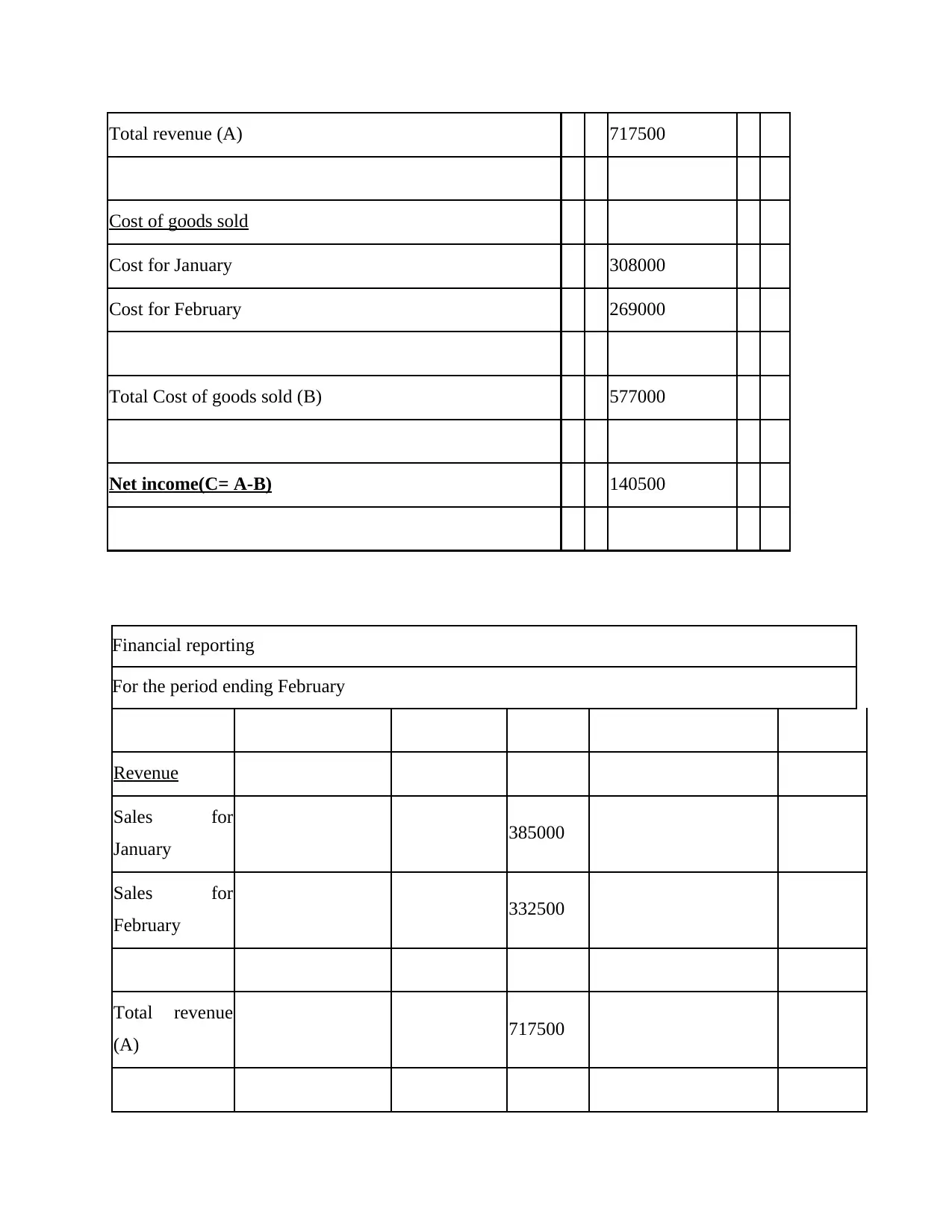

For the period ending February

Revenue

Sales for January 385000

Sales for February 332500

Total revenue (A) 717500

Cost of goods sold

Cost for January 308000

Cost for February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

Financial reporting

For the period ending February

Revenue

Sales for

January 385000

Sales for

February 332500

Total revenue

(A) 717500

Cost of goods sold

Cost for January 308000

Cost for February 269000

Total Cost of goods sold (B) 577000

Net income(C= A-B) 140500

Financial reporting

For the period ending February

Revenue

Sales for

January 385000

Sales for

February 332500

Total revenue

(A) 717500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of goods

sold

Cost for

January 308000

Cost for

February 269000

Total Cost of

goods sold (B) 577000

Net

income(C= A-

B)

140500

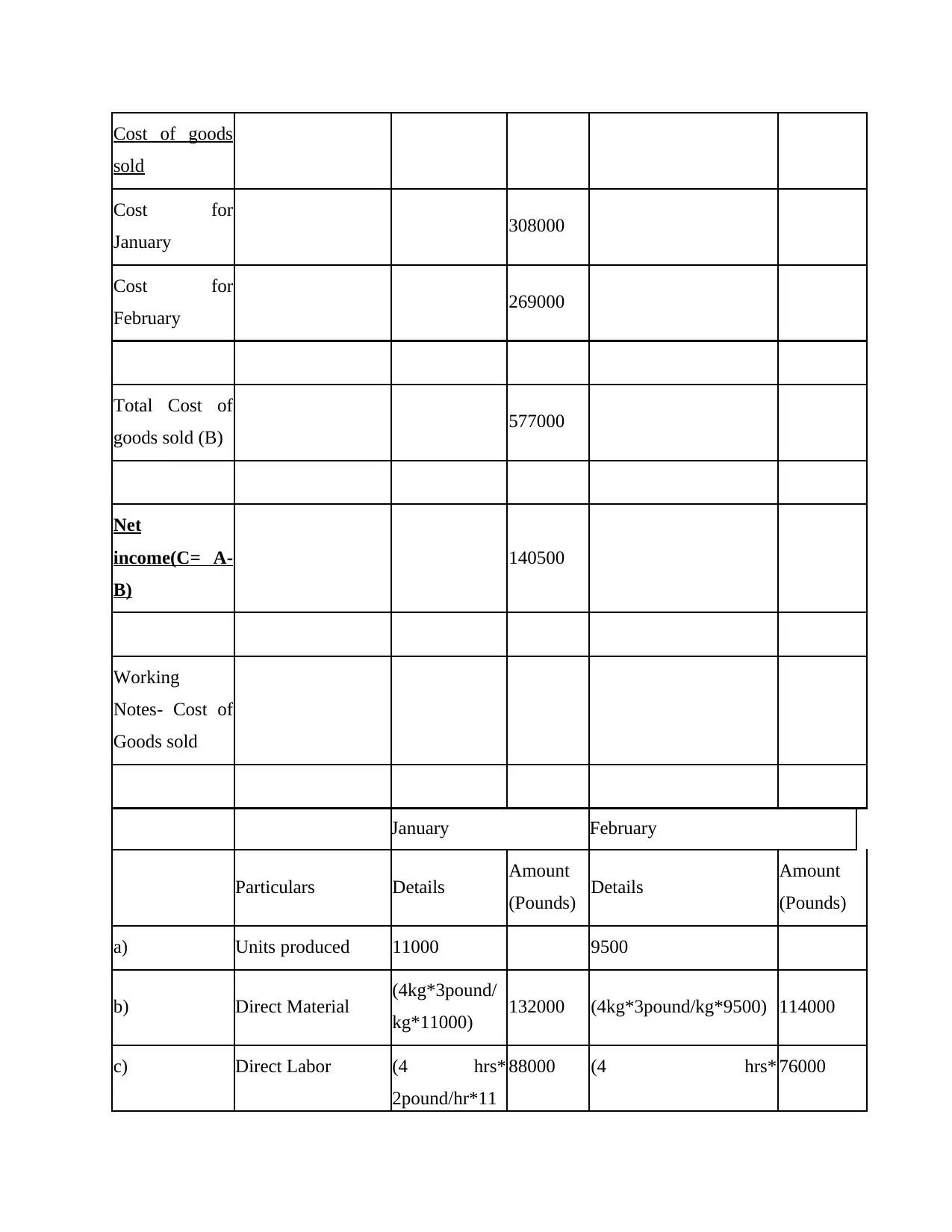

Working

Notes- Cost of

Goods sold

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) Units produced 11000 9500

b) Direct Material (4kg*3pound/

kg*11000) 132000 (4kg*3pound/kg*9500) 114000

c) Direct Labor (4 hrs*

2pound/hr*11

88000 (4 hrs* 76000

sold

Cost for

January 308000

Cost for

February 269000

Total Cost of

goods sold (B) 577000

Net

income(C= A-

B)

140500

Working

Notes- Cost of

Goods sold

January February

Particulars Details Amount

(Pounds) Details Amount

(Pounds)

a) Units produced 11000 9500

b) Direct Material (4kg*3pound/

kg*11000) 132000 (4kg*3pound/kg*9500) 114000

c) Direct Labor (4 hrs*

2pound/hr*11

88000 (4 hrs* 76000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

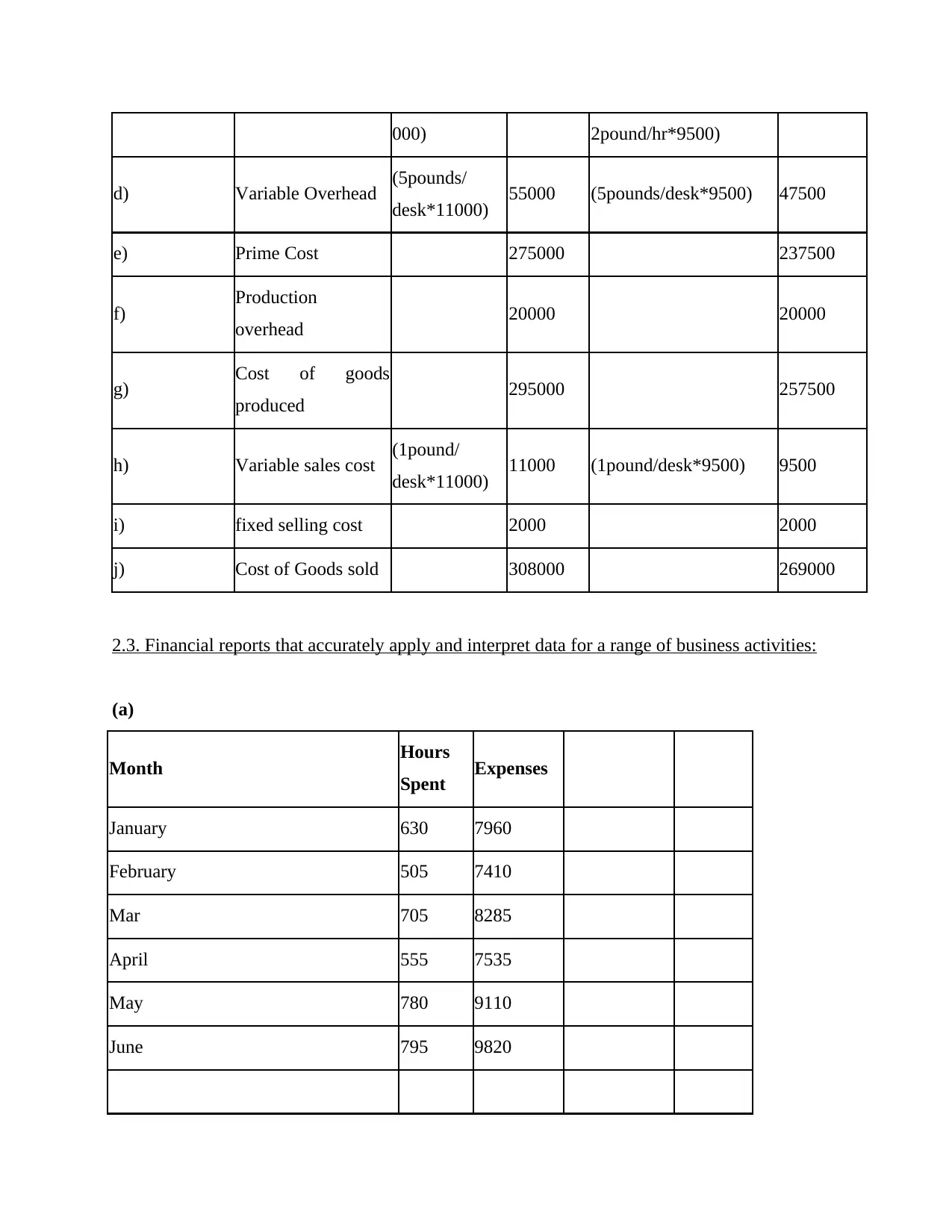

000) 2pound/hr*9500)

d) Variable Overhead (5pounds/

desk*11000) 55000 (5pounds/desk*9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

g) Cost of goods

produced 295000 257500

h) Variable sales cost (1pound/

desk*11000) 11000 (1pound/desk*9500) 9500

i) fixed selling cost 2000 2000

j) Cost of Goods sold 308000 269000

2.3. Financial reports that accurately apply and interpret data for a range of business activities:

(a)

Month Hours

Spent Expenses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

d) Variable Overhead (5pounds/

desk*11000) 55000 (5pounds/desk*9500) 47500

e) Prime Cost 275000 237500

f) Production

overhead 20000 20000

g) Cost of goods

produced 295000 257500

h) Variable sales cost (1pound/

desk*11000) 11000 (1pound/desk*9500) 9500

i) fixed selling cost 2000 2000

j) Cost of Goods sold 308000 269000

2.3. Financial reports that accurately apply and interpret data for a range of business activities:

(a)

Month Hours

Spent Expenses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

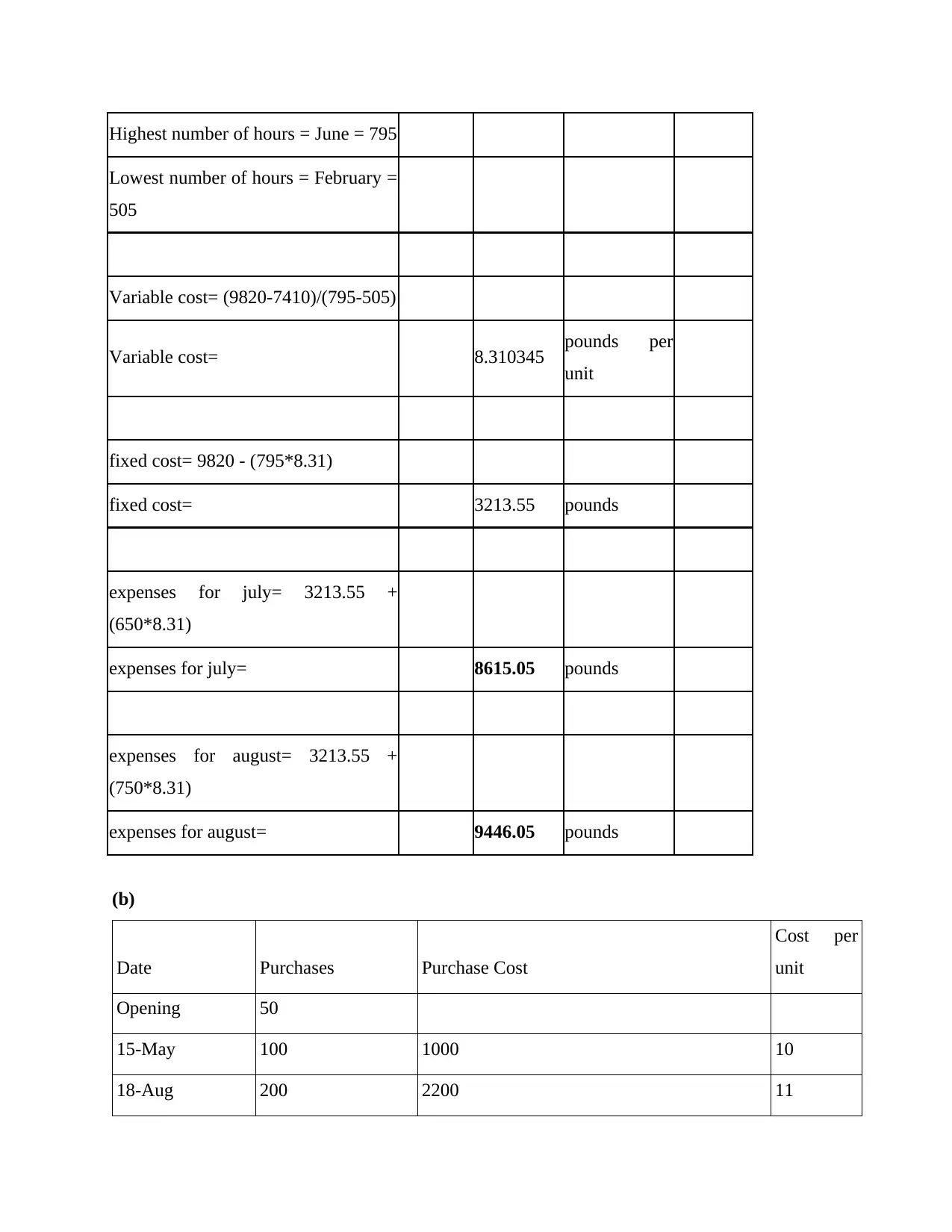

Highest number of hours = June = 795

Lowest number of hours = February =

505

Variable cost= (9820-7410)/(795-505)

Variable cost= 8.310345 pounds per

unit

fixed cost= 9820 - (795*8.31)

fixed cost= 3213.55 pounds

expenses for july= 3213.55 +

(650*8.31)

expenses for july= 8615.05 pounds

expenses for august= 3213.55 +

(750*8.31)

expenses for august= 9446.05 pounds

(b)

Date Purchases Purchase Cost

Cost per

unit

Opening 50

15-May 100 1000 10

18-Aug 200 2200 11

Lowest number of hours = February =

505

Variable cost= (9820-7410)/(795-505)

Variable cost= 8.310345 pounds per

unit

fixed cost= 9820 - (795*8.31)

fixed cost= 3213.55 pounds

expenses for july= 3213.55 +

(650*8.31)

expenses for july= 8615.05 pounds

expenses for august= 3213.55 +

(750*8.31)

expenses for august= 9446.05 pounds

(b)

Date Purchases Purchase Cost

Cost per

unit

Opening 50

15-May 100 1000 10

18-Aug 200 2200 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.