Higher National Diploma: Unit 5 Management Accounting Report

VerifiedAdded on 2022/12/27

|18

|4079

|1

Report

AI Summary

This report delves into the core concepts and techniques of management accounting, focusing on their application in decision-making. It begins by explaining different types of management accounting systems, including job costing, inventory management, cost accounting, and price optimization, highlighting their advantages and disadvantages. The report then explores various management accounting reports, such as budget reports, accounts receivable aging reports, cost managerial accounting reports, and performance reports, detailing their significance. Further, the report provides an income statement using both absorption and marginal costing methods, along with a reconciliation statement. It also includes an analysis of fixed and variable costs, margin of safety, and break-even point calculations. Finally, the report describes different types of planning tools for budgetary control and analyzes the use of management accounting systems in solving financial problems, providing a comprehensive overview of the subject matter.

UNIT 5 – MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explaining different types of management accounting system.............................................3

P2 Explaining different methods used for management accounting reports...............................5

Task 2...............................................................................................................................................7

P3. ...............................................................................................................................................7

TASK 3..........................................................................................................................................11

P4 Describing advantages and disadvantages of different types of planning tools for budgetary

control ......................................................................................................................................11

P5. Analysing use of management accounting system for solving financial problems............13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explaining different types of management accounting system.............................................3

P2 Explaining different methods used for management accounting reports...............................5

Task 2...............................................................................................................................................7

P3. ...............................................................................................................................................7

TASK 3..........................................................................................................................................11

P4 Describing advantages and disadvantages of different types of planning tools for budgetary

control ......................................................................................................................................11

P5. Analysing use of management accounting system for solving financial problems............13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting (MA) refers to the stipulation of financial data and proposal to

the company for achieving higher profitability and development. It is significant in the current

scenarios as it helps management accountant to take strategic decisions for efficient functioning

of the organization. The present report focuses on MA concepts and techniques for decision-

making. Additionally, the report will elaborate different types of management accounting

systems along with its advantages and disadvantages. The current report also gives detail of

different types of reports of MA. Additionally, it represents income statement using absorption

and marginal costing. The report also show segregation between fixed and variable cost along

with computation of margin of safety & break even point. The particular report also describes

different types of planning tool for budgetary control. Further, this study represents how

management accounting is utilized for solving financial problems.

MAIN BODY

TASK 1

P1 Explaining different types of management accounting system

Management accounting system use several methods to gather financial information for

the preparation reports for company (Management accounting and its importance. 2019). In

addition to this, these reports aid management to take strategic decision for smooth functioning

of the business. With respect to this, there are basically four types of management accounting

system which area as follows:

Job costing system

It is the system that collects the information regarding the cost associated with particular

production and service. Additionally, management accountant can aid Connect Catering Services

(CCS) to identify its organization's profits and loss (Agustina, 2020). With respect to this, the

system may be beneficial for CCS to evaluate costing related to particular job in present and also

for the future. In addition to this, it provides assistance in determining variance between the

actual and estimated cost of particular job. There are various merits and demerits that CCS will

get through this are as follows

Advantages Disadvantages

Management accounting (MA) refers to the stipulation of financial data and proposal to

the company for achieving higher profitability and development. It is significant in the current

scenarios as it helps management accountant to take strategic decisions for efficient functioning

of the organization. The present report focuses on MA concepts and techniques for decision-

making. Additionally, the report will elaborate different types of management accounting

systems along with its advantages and disadvantages. The current report also gives detail of

different types of reports of MA. Additionally, it represents income statement using absorption

and marginal costing. The report also show segregation between fixed and variable cost along

with computation of margin of safety & break even point. The particular report also describes

different types of planning tool for budgetary control. Further, this study represents how

management accounting is utilized for solving financial problems.

MAIN BODY

TASK 1

P1 Explaining different types of management accounting system

Management accounting system use several methods to gather financial information for

the preparation reports for company (Management accounting and its importance. 2019). In

addition to this, these reports aid management to take strategic decision for smooth functioning

of the business. With respect to this, there are basically four types of management accounting

system which area as follows:

Job costing system

It is the system that collects the information regarding the cost associated with particular

production and service. Additionally, management accountant can aid Connect Catering Services

(CCS) to identify its organization's profits and loss (Agustina, 2020). With respect to this, the

system may be beneficial for CCS to evaluate costing related to particular job in present and also

for the future. In addition to this, it provides assistance in determining variance between the

actual and estimated cost of particular job. There are various merits and demerits that CCS will

get through this are as follows

Advantages Disadvantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability for each job can

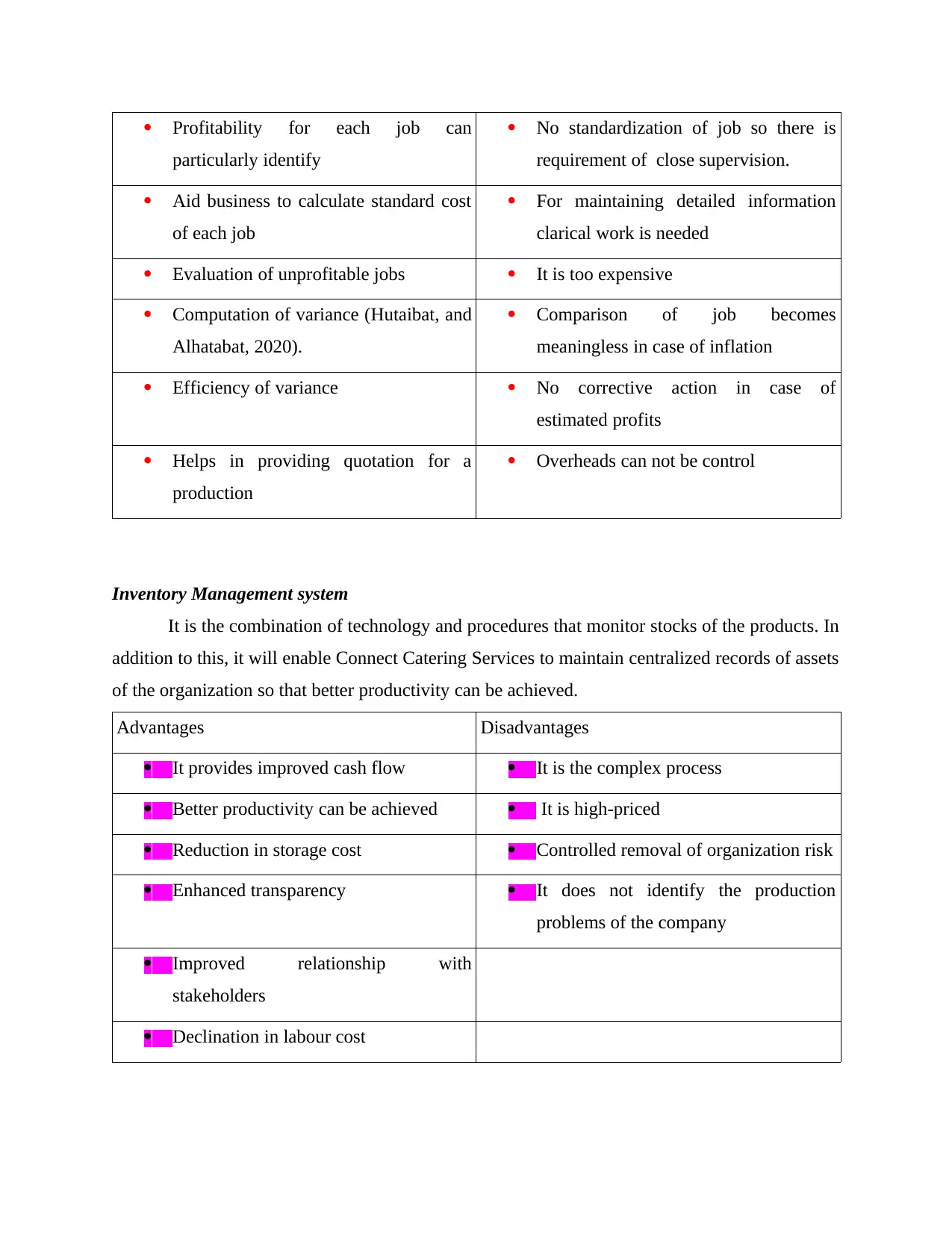

particularly identify

No standardization of job so there is

requirement of close supervision.

Aid business to calculate standard cost

of each job

For maintaining detailed information

clarical work is needed

Evaluation of unprofitable jobs It is too expensive

Computation of variance (Hutaibat, and

Alhatabat, 2020).

Comparison of job becomes

meaningless in case of inflation

Efficiency of variance No corrective action in case of

estimated profits

Helps in providing quotation for a

production

Overheads can not be control

Inventory Management system

It is the combination of technology and procedures that monitor stocks of the products. In

addition to this, it will enable Connect Catering Services to maintain centralized records of assets

of the organization so that better productivity can be achieved.

Advantages Disadvantages

It provides improved cash flow It is the complex process

Better productivity can be achieved It is high-priced

Reduction in storage cost Controlled removal of organization risk

Enhanced transparency It does not identify the production

problems of the company

Improved relationship with

stakeholders

Declination in labour cost

particularly identify

No standardization of job so there is

requirement of close supervision.

Aid business to calculate standard cost

of each job

For maintaining detailed information

clarical work is needed

Evaluation of unprofitable jobs It is too expensive

Computation of variance (Hutaibat, and

Alhatabat, 2020).

Comparison of job becomes

meaningless in case of inflation

Efficiency of variance No corrective action in case of

estimated profits

Helps in providing quotation for a

production

Overheads can not be control

Inventory Management system

It is the combination of technology and procedures that monitor stocks of the products. In

addition to this, it will enable Connect Catering Services to maintain centralized records of assets

of the organization so that better productivity can be achieved.

Advantages Disadvantages

It provides improved cash flow It is the complex process

Better productivity can be achieved It is high-priced

Reduction in storage cost Controlled removal of organization risk

Enhanced transparency It does not identify the production

problems of the company

Improved relationship with

stakeholders

Declination in labour cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

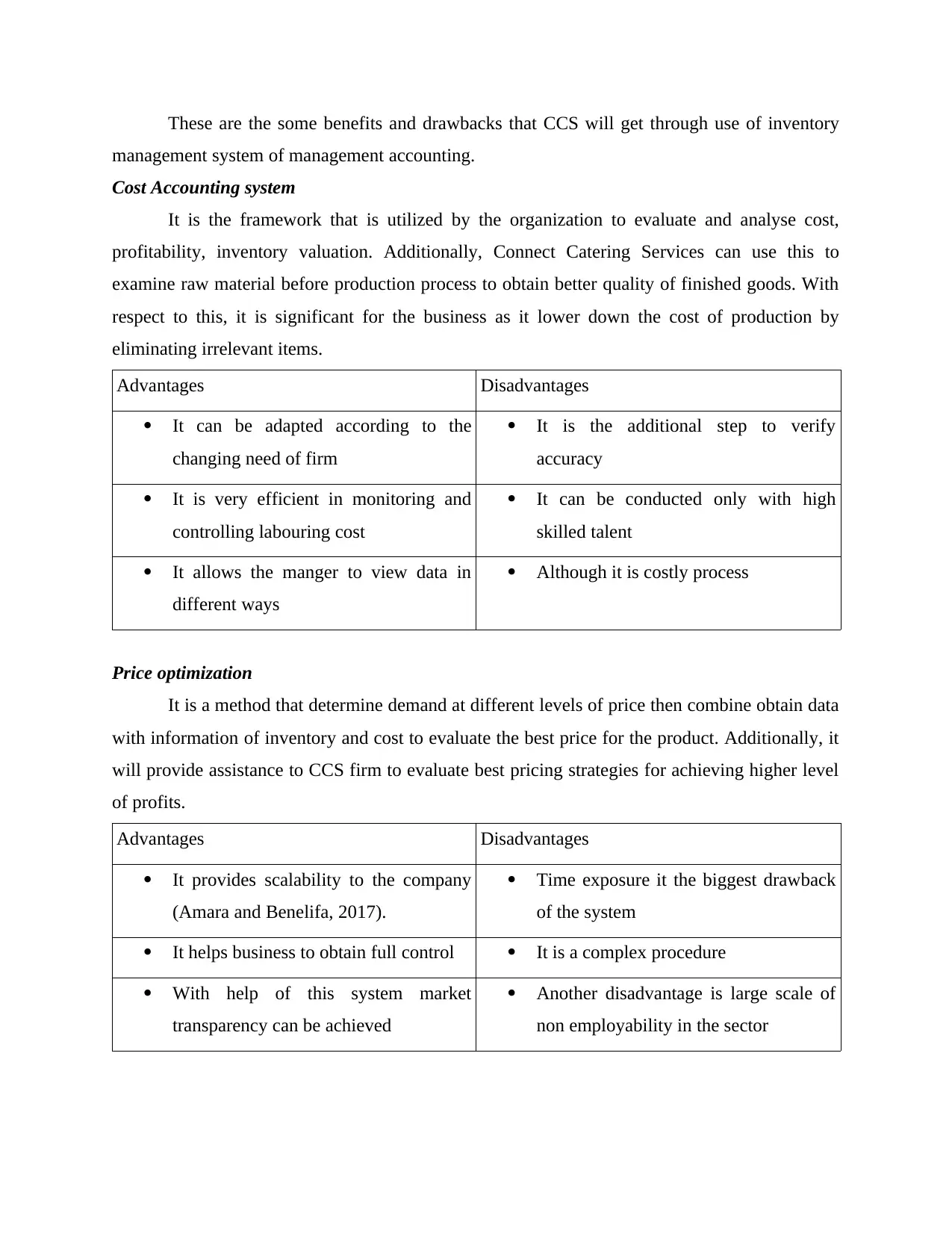

These are the some benefits and drawbacks that CCS will get through use of inventory

management system of management accounting.

Cost Accounting system

It is the framework that is utilized by the organization to evaluate and analyse cost,

profitability, inventory valuation. Additionally, Connect Catering Services can use this to

examine raw material before production process to obtain better quality of finished goods. With

respect to this, it is significant for the business as it lower down the cost of production by

eliminating irrelevant items.

Advantages Disadvantages

It can be adapted according to the

changing need of firm

It is the additional step to verify

accuracy

It is very efficient in monitoring and

controlling labouring cost

It can be conducted only with high

skilled talent

It allows the manger to view data in

different ways

Although it is costly process

Price optimization

It is a method that determine demand at different levels of price then combine obtain data

with information of inventory and cost to evaluate the best price for the product. Additionally, it

will provide assistance to CCS firm to evaluate best pricing strategies for achieving higher level

of profits.

Advantages Disadvantages

It provides scalability to the company

(Amara and Benelifa, 2017).

Time exposure it the biggest drawback

of the system

It helps business to obtain full control It is a complex procedure

With help of this system market

transparency can be achieved

Another disadvantage is large scale of

non employability in the sector

management system of management accounting.

Cost Accounting system

It is the framework that is utilized by the organization to evaluate and analyse cost,

profitability, inventory valuation. Additionally, Connect Catering Services can use this to

examine raw material before production process to obtain better quality of finished goods. With

respect to this, it is significant for the business as it lower down the cost of production by

eliminating irrelevant items.

Advantages Disadvantages

It can be adapted according to the

changing need of firm

It is the additional step to verify

accuracy

It is very efficient in monitoring and

controlling labouring cost

It can be conducted only with high

skilled talent

It allows the manger to view data in

different ways

Although it is costly process

Price optimization

It is a method that determine demand at different levels of price then combine obtain data

with information of inventory and cost to evaluate the best price for the product. Additionally, it

will provide assistance to CCS firm to evaluate best pricing strategies for achieving higher level

of profits.

Advantages Disadvantages

It provides scalability to the company

(Amara and Benelifa, 2017).

Time exposure it the biggest drawback

of the system

It helps business to obtain full control It is a complex procedure

With help of this system market

transparency can be achieved

Another disadvantage is large scale of

non employability in the sector

Full control is another benefit that firm

can get through this system.

P2 Explaining different methods used for management accounting reports

Management accounting reports are utilized for planning, organizing, regulating,

decision-making and measuring performance. In addition to this, following are the different

types of management accounting reports.

Budget Report

CSS use this reports to measure company's performance through evaluating each

department of the firm. In addition to this, every company prepare budget in the initial stage to

estimate its future expenditure so that it can effectively allocate financial resources. With respect

to this, these reports helps organization to compare its present position with previous so that

suitable major actions can be taken (Hlaciuc and et.al., 2017). Further, management account of

Connecting Catering Service can take decision regarding employees incentives, cost reduction of

suppliers and vendors.

Accounts Receivable Ageing Report

This is the crucial report that gives the company idea about organization should offer

credit to consumers or not (Types of managerial accounting reports, 2020). It provides an

overview of credit balances according to segregation of period such as 30, 60 and 90 days. With

respect to this, if there are many defaulters then company need to make completely new strict

procedure for credit transaction. Additionally, it is essentially to do the same for better cash flow

In add-on to this, it allows the organization to adjust its credit policies so that CCS can match its

norms & condition with customers capacity.

Cost Managerial Accounting Report

This report can help CCS to obtain cost of raw material, labour, overhead, etc. In addition

to this, it aids company to find overall summary of all the information of the firm. With respect

to this, manager can take decision regarding selling price of product with help of these cost

evaluation (Lasyoud and Alsharari, 2017). Additionally, profit margins can be estimated with

help of transparent view of cost of production of products. In aspect to this, these reports are very

beneficial for the CCS to evaluate profitability and cost of each procedure of the company.

Performance Reports

can get through this system.

P2 Explaining different methods used for management accounting reports

Management accounting reports are utilized for planning, organizing, regulating,

decision-making and measuring performance. In addition to this, following are the different

types of management accounting reports.

Budget Report

CSS use this reports to measure company's performance through evaluating each

department of the firm. In addition to this, every company prepare budget in the initial stage to

estimate its future expenditure so that it can effectively allocate financial resources. With respect

to this, these reports helps organization to compare its present position with previous so that

suitable major actions can be taken (Hlaciuc and et.al., 2017). Further, management account of

Connecting Catering Service can take decision regarding employees incentives, cost reduction of

suppliers and vendors.

Accounts Receivable Ageing Report

This is the crucial report that gives the company idea about organization should offer

credit to consumers or not (Types of managerial accounting reports, 2020). It provides an

overview of credit balances according to segregation of period such as 30, 60 and 90 days. With

respect to this, if there are many defaulters then company need to make completely new strict

procedure for credit transaction. Additionally, it is essentially to do the same for better cash flow

In add-on to this, it allows the organization to adjust its credit policies so that CCS can match its

norms & condition with customers capacity.

Cost Managerial Accounting Report

This report can help CCS to obtain cost of raw material, labour, overhead, etc. In addition

to this, it aids company to find overall summary of all the information of the firm. With respect

to this, manager can take decision regarding selling price of product with help of these cost

evaluation (Lasyoud and Alsharari, 2017). Additionally, profit margins can be estimated with

help of transparent view of cost of production of products. In aspect to this, these reports are very

beneficial for the CCS to evaluate profitability and cost of each procedure of the company.

Performance Reports

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is prepared to evaluate performance of the organizations and employees of each

team. With respect to this, it is also utilized to compare the current performance with the past to

check that company is going in upward or downward direction. Further, managers use this report

to take strategic decision regarding the employees increment, promotion, appreciation, etc.

Furthermore, it offers the deep insights into the working strategies of Connecting Catering

Service.

Other Managerial Accounting Report

Competitors, market and industry analysis report are very essential for the better

functioning of the CCS. In addition to this, it evaluates scope of the company in the industry by

identifying opportunities and weakness of the business. With respect to this, it is vital component

of management accountant as these reports gives overview of all transaction of the organization.

These are different reports of management accountant that help the organization to take

strategic and operational decision for the effective planning and controlling of CCS.

Task 2

P3.

Income statement using absorption costing

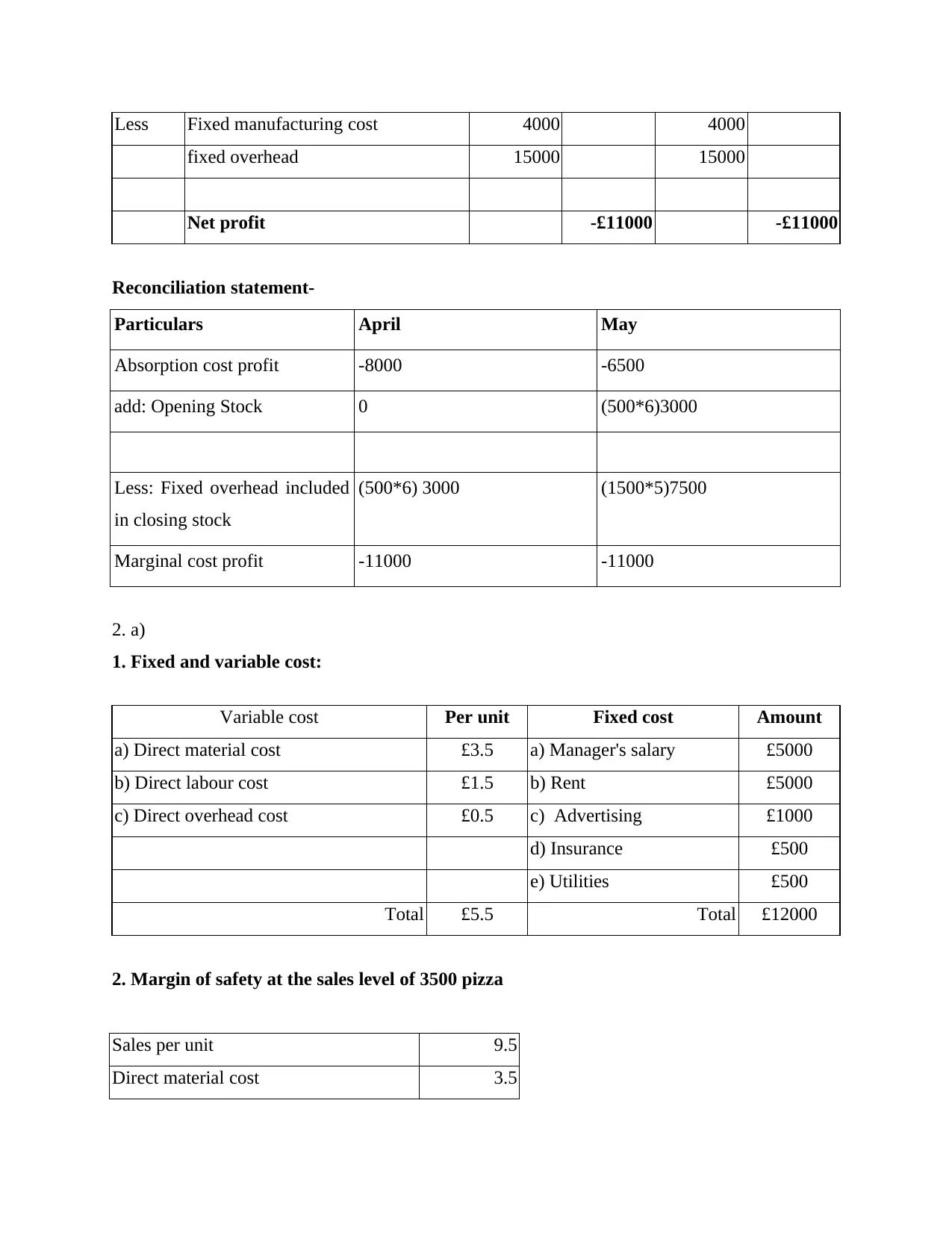

April May

sales 16000 16000

Add: Variable manufacturing cost 10000 12000

Fixed manufacturing cost 15000 15000

27000

Cost of goods available for sales 25000

Add: Opening stock 0 5000

Less Closing stock 5000 13500

team. With respect to this, it is also utilized to compare the current performance with the past to

check that company is going in upward or downward direction. Further, managers use this report

to take strategic decision regarding the employees increment, promotion, appreciation, etc.

Furthermore, it offers the deep insights into the working strategies of Connecting Catering

Service.

Other Managerial Accounting Report

Competitors, market and industry analysis report are very essential for the better

functioning of the CCS. In addition to this, it evaluates scope of the company in the industry by

identifying opportunities and weakness of the business. With respect to this, it is vital component

of management accountant as these reports gives overview of all transaction of the organization.

These are different reports of management accountant that help the organization to take

strategic and operational decision for the effective planning and controlling of CCS.

Task 2

P3.

Income statement using absorption costing

April May

sales 16000 16000

Add: Variable manufacturing cost 10000 12000

Fixed manufacturing cost 15000 15000

27000

Cost of goods available for sales 25000

Add: Opening stock 0 5000

Less Closing stock 5000 13500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

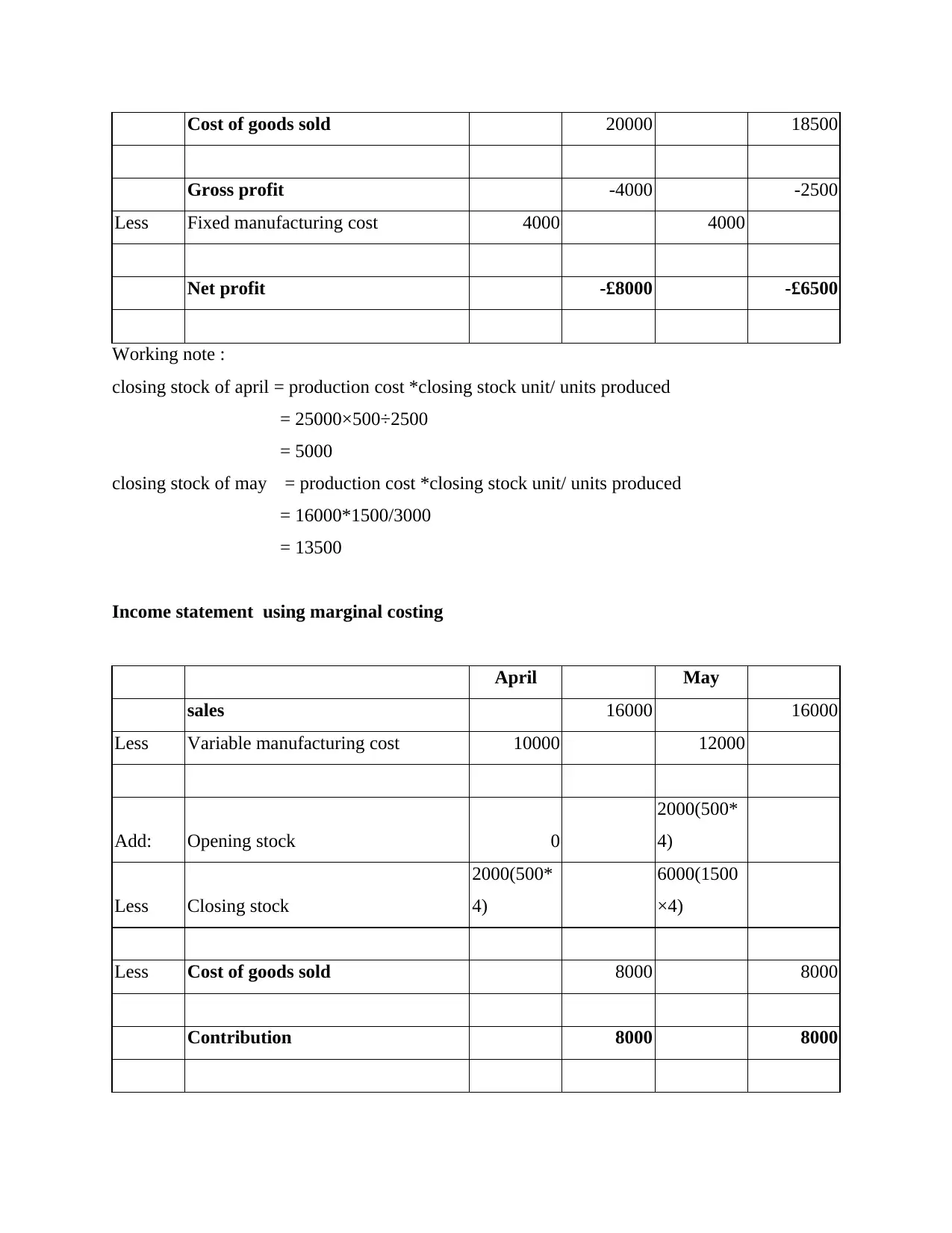

Cost of goods sold 20000 18500

Gross profit -4000 -2500

Less Fixed manufacturing cost 4000 4000

Net profit -£8000 -£6500

Working note :

closing stock of april = production cost *closing stock unit/ units produced

= 25000×500÷2500

= 5000

closing stock of may = production cost *closing stock unit/ units produced

= 16000*1500/3000

= 13500

Income statement using marginal costing

April May

sales 16000 16000

Less Variable manufacturing cost 10000 12000

Add: Opening stock 0

2000(500*

4)

Less Closing stock

2000(500*

4)

6000(1500

×4)

Less Cost of goods sold 8000 8000

Contribution 8000 8000

Gross profit -4000 -2500

Less Fixed manufacturing cost 4000 4000

Net profit -£8000 -£6500

Working note :

closing stock of april = production cost *closing stock unit/ units produced

= 25000×500÷2500

= 5000

closing stock of may = production cost *closing stock unit/ units produced

= 16000*1500/3000

= 13500

Income statement using marginal costing

April May

sales 16000 16000

Less Variable manufacturing cost 10000 12000

Add: Opening stock 0

2000(500*

4)

Less Closing stock

2000(500*

4)

6000(1500

×4)

Less Cost of goods sold 8000 8000

Contribution 8000 8000

Less Fixed manufacturing cost 4000 4000

fixed overhead 15000 15000

Net profit -£11000 -£11000

Reconciliation statement-

Particulars April May

Absorption cost profit -8000 -6500

add: Opening Stock 0 (500*6)3000

Less: Fixed overhead included

in closing stock

(500*6) 3000 (1500*5)7500

Marginal cost profit -11000 -11000

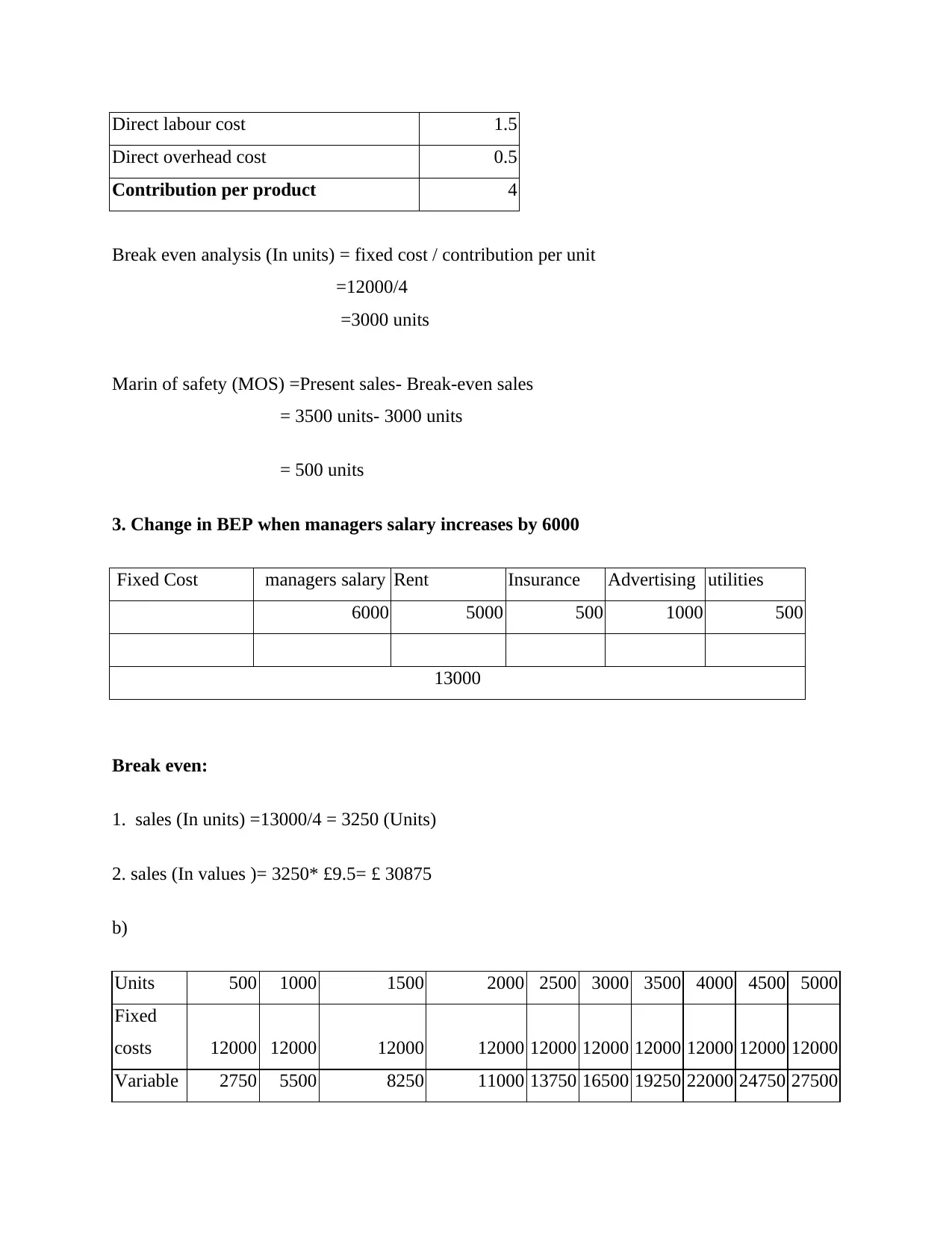

2. a)

1. Fixed and variable cost:

Variable cost Per unit Fixed cost Amount

a) Direct material cost £3.5 a) Manager's salary £5000

b) Direct labour cost £1.5 b) Rent £5000

c) Direct overhead cost £0.5 c) Advertising £1000

d) Insurance £500

e) Utilities £500

Total £5.5 Total £12000

2. Margin of safety at the sales level of 3500 pizza

Sales per unit 9.5

Direct material cost 3.5

fixed overhead 15000 15000

Net profit -£11000 -£11000

Reconciliation statement-

Particulars April May

Absorption cost profit -8000 -6500

add: Opening Stock 0 (500*6)3000

Less: Fixed overhead included

in closing stock

(500*6) 3000 (1500*5)7500

Marginal cost profit -11000 -11000

2. a)

1. Fixed and variable cost:

Variable cost Per unit Fixed cost Amount

a) Direct material cost £3.5 a) Manager's salary £5000

b) Direct labour cost £1.5 b) Rent £5000

c) Direct overhead cost £0.5 c) Advertising £1000

d) Insurance £500

e) Utilities £500

Total £5.5 Total £12000

2. Margin of safety at the sales level of 3500 pizza

Sales per unit 9.5

Direct material cost 3.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct labour cost 1.5

Direct overhead cost 0.5

Contribution per product 4

Break even analysis (In units) = fixed cost / contribution per unit

=12000/4

=3000 units

Marin of safety (MOS) =Present sales- Break-even sales

= 3500 units- 3000 units

= 500 units

3. Change in BEP when managers salary increases by 6000

Fixed Cost managers salary Rent Insurance Advertising utilities

6000 5000 500 1000 500

13000

Break even:

1. sales (In units) =13000/4 = 3250 (Units)

2. sales (In values )= 3250* £9.5= £ 30875

b)

Units 500 1000 1500 2000 2500 3000 3500 4000 4500 5000

Fixed

costs 12000 12000 12000 12000 12000 12000 12000 12000 12000 12000

Variable 2750 5500 8250 11000 13750 16500 19250 22000 24750 27500

Direct overhead cost 0.5

Contribution per product 4

Break even analysis (In units) = fixed cost / contribution per unit

=12000/4

=3000 units

Marin of safety (MOS) =Present sales- Break-even sales

= 3500 units- 3000 units

= 500 units

3. Change in BEP when managers salary increases by 6000

Fixed Cost managers salary Rent Insurance Advertising utilities

6000 5000 500 1000 500

13000

Break even:

1. sales (In units) =13000/4 = 3250 (Units)

2. sales (In values )= 3250* £9.5= £ 30875

b)

Units 500 1000 1500 2000 2500 3000 3500 4000 4500 5000

Fixed

costs 12000 12000 12000 12000 12000 12000 12000 12000 12000 12000

Variable 2750 5500 8250 11000 13750 16500 19250 22000 24750 27500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

costs

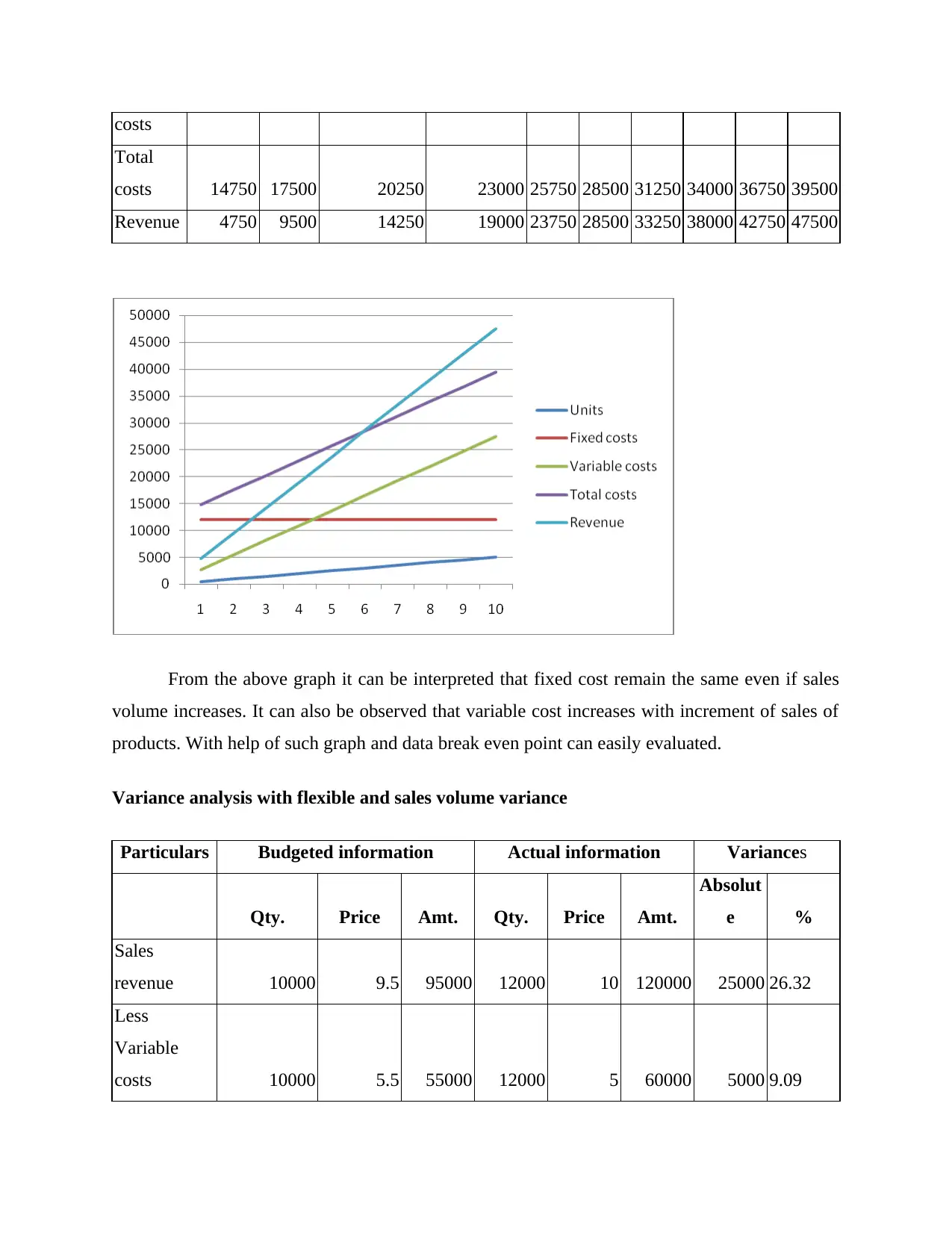

Total

costs 14750 17500 20250 23000 25750 28500 31250 34000 36750 39500

Revenue 4750 9500 14250 19000 23750 28500 33250 38000 42750 47500

From the above graph it can be interpreted that fixed cost remain the same even if sales

volume increases. It can also be observed that variable cost increases with increment of sales of

products. With help of such graph and data break even point can easily evaluated.

Variance analysis with flexible and sales volume variance

Particulars Budgeted information Actual information Variances

Qty. Price Amt. Qty. Price Amt.

Absolut

e %

Sales

revenue 10000 9.5 95000 12000 10 120000 25000 26.32

Less

Variable

costs 10000 5.5 55000 12000 5 60000 5000 9.09

Total

costs 14750 17500 20250 23000 25750 28500 31250 34000 36750 39500

Revenue 4750 9500 14250 19000 23750 28500 33250 38000 42750 47500

From the above graph it can be interpreted that fixed cost remain the same even if sales

volume increases. It can also be observed that variable cost increases with increment of sales of

products. With help of such graph and data break even point can easily evaluated.

Variance analysis with flexible and sales volume variance

Particulars Budgeted information Actual information Variances

Qty. Price Amt. Qty. Price Amt.

Absolut

e %

Sales

revenue 10000 9.5 95000 12000 10 120000 25000 26.32

Less

Variable

costs 10000 5.5 55000 12000 5 60000 5000 9.09

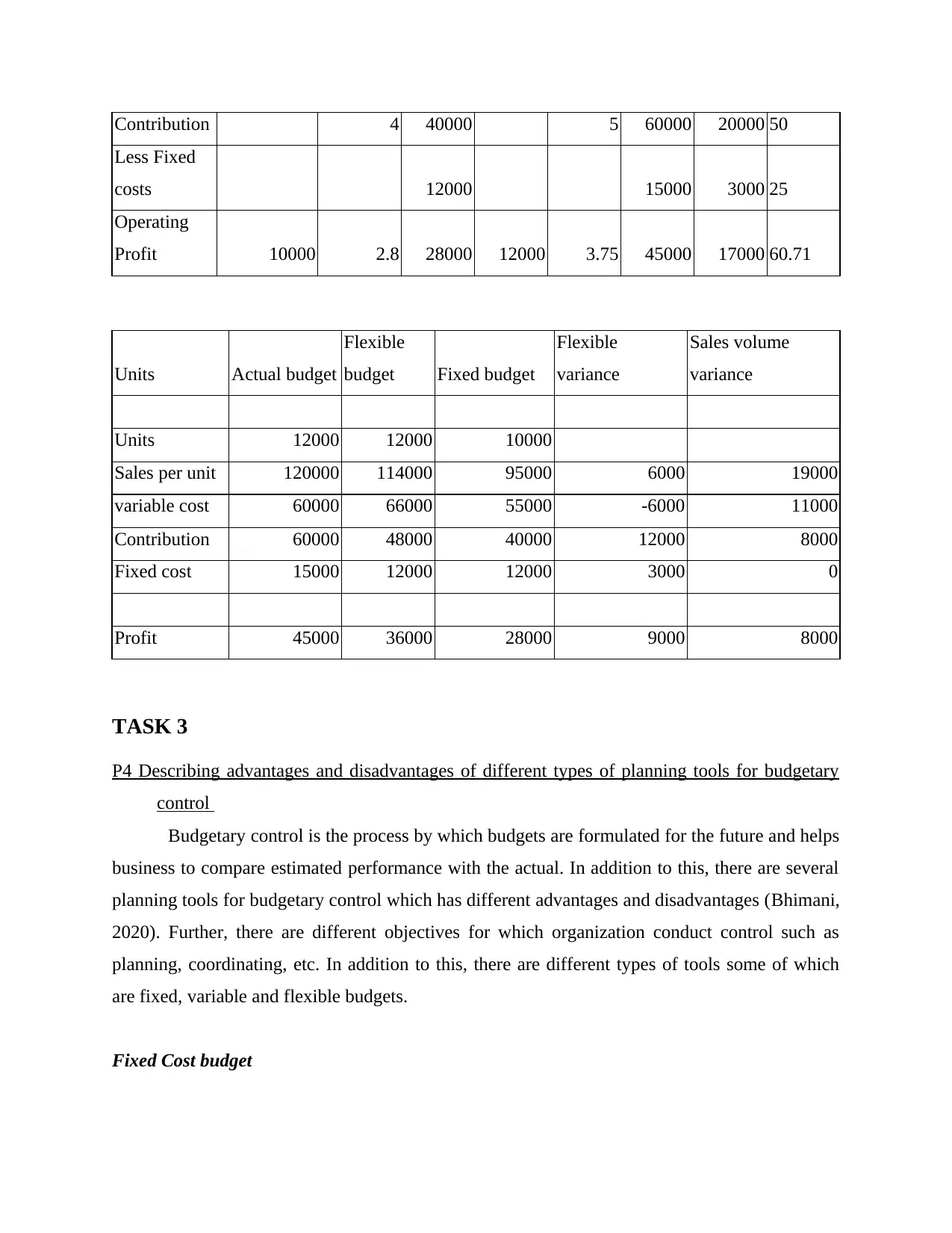

Contribution 4 40000 5 60000 20000 50

Less Fixed

costs 12000 15000 3000 25

Operating

Profit 10000 2.8 28000 12000 3.75 45000 17000 60.71

Units Actual budget

Flexible

budget Fixed budget

Flexible

variance

Sales volume

variance

Units 12000 12000 10000

Sales per unit 120000 114000 95000 6000 19000

variable cost 60000 66000 55000 -6000 11000

Contribution 60000 48000 40000 12000 8000

Fixed cost 15000 12000 12000 3000 0

Profit 45000 36000 28000 9000 8000

TASK 3

P4 Describing advantages and disadvantages of different types of planning tools for budgetary

control

Budgetary control is the process by which budgets are formulated for the future and helps

business to compare estimated performance with the actual. In addition to this, there are several

planning tools for budgetary control which has different advantages and disadvantages (Bhimani,

2020). Further, there are different objectives for which organization conduct control such as

planning, coordinating, etc. In addition to this, there are different types of tools some of which

are fixed, variable and flexible budgets.

Fixed Cost budget

Less Fixed

costs 12000 15000 3000 25

Operating

Profit 10000 2.8 28000 12000 3.75 45000 17000 60.71

Units Actual budget

Flexible

budget Fixed budget

Flexible

variance

Sales volume

variance

Units 12000 12000 10000

Sales per unit 120000 114000 95000 6000 19000

variable cost 60000 66000 55000 -6000 11000

Contribution 60000 48000 40000 12000 8000

Fixed cost 15000 12000 12000 3000 0

Profit 45000 36000 28000 9000 8000

TASK 3

P4 Describing advantages and disadvantages of different types of planning tools for budgetary

control

Budgetary control is the process by which budgets are formulated for the future and helps

business to compare estimated performance with the actual. In addition to this, there are several

planning tools for budgetary control which has different advantages and disadvantages (Bhimani,

2020). Further, there are different objectives for which organization conduct control such as

planning, coordinating, etc. In addition to this, there are different types of tools some of which

are fixed, variable and flexible budgets.

Fixed Cost budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.