Comprehensive Analysis of Management Accounting Techniques and Systems

VerifiedAdded on 2022/12/22

|17

|2691

|27

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring various systems and methods. It begins by defining management accounting and its different types, including production cost, cash flow analysis, inventory turnover analysis, and constraint analysis. The report then delves into specific methods such as job costing, inventory management, and price optimization. Furthermore, it discusses the benefits of a management accounting system, such as improved decision-making, planning, and customer service. The report includes calculations related to cost cards, income statements under marginal costing, and the high-low method. It also covers LIFO, FIFO, and AVCO inventory methods, along with break-even analysis, cash collection schedules, and budgeting. Finally, the report touches upon financial ratio analysis, including return on capital employed (ROCE) and asset turnover, providing a complete picture of management accounting principles and their application.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

1.1 Management accounting system and different types............................................................3

1.2 Different methods of management accounting......................................................................4

1.3 Benefits of management accounting system..........................................................................5

2.1 cost card ................................................................................................................................6

2.2 Income statement under Marginal costing.............................................................................6

2.3 High-low method , LIFO FIFO and Avco.............................................................................2

2.4 Break even.............................................................................................................................4

Calculation of sales .....................................................................................................................4

Calculation of profit of 500000 units ..........................................................................................5

3.1 cash collection .......................................................................................................................5

3.2 Budget ...................................................................................................................................6

Part 2 ...............................................................................................................................................6

4.1 (i) Return on capital employed (ROCE)................................................................................6

4.2 (ii) Asset turnover ................................................................................................................6

Conclusion ......................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................3

1.1 Management accounting system and different types............................................................3

1.2 Different methods of management accounting......................................................................4

1.3 Benefits of management accounting system..........................................................................5

2.1 cost card ................................................................................................................................6

2.2 Income statement under Marginal costing.............................................................................6

2.3 High-low method , LIFO FIFO and Avco.............................................................................2

2.4 Break even.............................................................................................................................4

Calculation of sales .....................................................................................................................4

Calculation of profit of 500000 units ..........................................................................................5

3.1 cash collection .......................................................................................................................5

3.2 Budget ...................................................................................................................................6

Part 2 ...............................................................................................................................................6

4.1 (i) Return on capital employed (ROCE)................................................................................6

4.2 (ii) Asset turnover ................................................................................................................6

Conclusion ......................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Management accounting is used by the managers in the organisation to identify the

goals, objectives and also it describes financial performance of the organisation to managers

(Ameen and et.al, 2018). Through management accounting, managers can make plans and

policies for the company. This report speaks about the different types of management

accounting system along with this different type of management accounting system is explained

in this report. Different cost such as marginal and absorption is being mentioned in this report.

Various advantages and disadvantages of different types of planning tools used for budgetary

control is being mentioned in this report.

1.1 Management accounting system and different types

Management accounting system focuses on recognizing the cost which is related to

production of goods in the company. Management accounting system will help The London

college to track down its cost and financial statements so that college may attain the revenues.

So the management accounting system is basically used by the management of any company by

tacking the financial performance.

Types of managerial accounting system

Production cost

As the name suggest, production cost is used to determine the total cost which is

included in the production of cost, and cost can be divided in to different categories such as

variable, fixed , direct and indirect cost. Cost accounting is used to recognize the overhead as

well (Rikhardsson and et.al, 2018).

Cash flow analysis

Managers and managerial accountants manages the cash flow to know the impact of

business decisions. Most of the companies are indulge in recording the financial information on

accrual basis. With the help of cash flow company may know the inflows like how many

revenues have been generated by the company through sales and how many expenses they did in

the form of rent,, wages, production etc.

Inventory turnover analysis

Inventory turnover is being calculated in the company to know that how many times

they have changed and replaced the inventory apart from this, due to inventory turnover

Management accounting is used by the managers in the organisation to identify the

goals, objectives and also it describes financial performance of the organisation to managers

(Ameen and et.al, 2018). Through management accounting, managers can make plans and

policies for the company. This report speaks about the different types of management

accounting system along with this different type of management accounting system is explained

in this report. Different cost such as marginal and absorption is being mentioned in this report.

Various advantages and disadvantages of different types of planning tools used for budgetary

control is being mentioned in this report.

1.1 Management accounting system and different types

Management accounting system focuses on recognizing the cost which is related to

production of goods in the company. Management accounting system will help The London

college to track down its cost and financial statements so that college may attain the revenues.

So the management accounting system is basically used by the management of any company by

tacking the financial performance.

Types of managerial accounting system

Production cost

As the name suggest, production cost is used to determine the total cost which is

included in the production of cost, and cost can be divided in to different categories such as

variable, fixed , direct and indirect cost. Cost accounting is used to recognize the overhead as

well (Rikhardsson and et.al, 2018).

Cash flow analysis

Managers and managerial accountants manages the cash flow to know the impact of

business decisions. Most of the companies are indulge in recording the financial information on

accrual basis. With the help of cash flow company may know the inflows like how many

revenues have been generated by the company through sales and how many expenses they did in

the form of rent,, wages, production etc.

Inventory turnover analysis

Inventory turnover is being calculated in the company to know that how many times

they have changed and replaced the inventory apart from this, due to inventory turnover

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company may know how much inventory has been sold out. So the analysis of inventory

turnover assist the business to take better decisions for pricing, marketing, manufacturing and

also for purchasing new inventory (Allain and et.al, 2021). This assist the company to know

the cost incurred for the unsold items and inventories as well.

Constraint analysis

This states about the managerial accounting which involves review of constraints in the

production line. Along with this managerial accountants helps to determine the calculation of

constraints revenue and profit. It is valuable information for the managers to implement change

and also they can improvise the efficiencies of the production and sales procedure.

1.2 Different methods of management accounting

Job costing system

Job costing system talks about the procedure of accumulating the information which is

associated with the cost which is associated with the specific production and service job. This

information is necessary for the customer as well. It helps the company to know the estimation

cost of company as well. This job costing method needs three types of information

Direct material

Job costing system is being used by the company to track down the cost of material

which is being used by the company. This cost is being used by the company for the manual

tracking and also it assist the company to know the expenses of warehousing so the company

can save the extra cost.

Direct labour

The job costing system tracks the cost of labour which is being given by the company

and used in job as well (Abdusalomova, 2020). Direct labour generally assign to a job including

a time card and time-sheet, many companies using smart phones and internet to record the

work done by the labour.

Overhead

Job costing refers to overhead cost which states about the depreciation which is being

levied on the production, equipments and rent of the buildings. At the end of every accounting

period overhead is being decided.

Inventory management system

turnover assist the business to take better decisions for pricing, marketing, manufacturing and

also for purchasing new inventory (Allain and et.al, 2021). This assist the company to know

the cost incurred for the unsold items and inventories as well.

Constraint analysis

This states about the managerial accounting which involves review of constraints in the

production line. Along with this managerial accountants helps to determine the calculation of

constraints revenue and profit. It is valuable information for the managers to implement change

and also they can improvise the efficiencies of the production and sales procedure.

1.2 Different methods of management accounting

Job costing system

Job costing system talks about the procedure of accumulating the information which is

associated with the cost which is associated with the specific production and service job. This

information is necessary for the customer as well. It helps the company to know the estimation

cost of company as well. This job costing method needs three types of information

Direct material

Job costing system is being used by the company to track down the cost of material

which is being used by the company. This cost is being used by the company for the manual

tracking and also it assist the company to know the expenses of warehousing so the company

can save the extra cost.

Direct labour

The job costing system tracks the cost of labour which is being given by the company

and used in job as well (Abdusalomova, 2020). Direct labour generally assign to a job including

a time card and time-sheet, many companies using smart phones and internet to record the

work done by the labour.

Overhead

Job costing refers to overhead cost which states about the depreciation which is being

levied on the production, equipments and rent of the buildings. At the end of every accounting

period overhead is being decided.

Inventory management system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Many big companies uses inventory management system so that they can keep an eye on

the usage of inventory, this system is helpful for the company to track down the goods from

supply chain to the sale. This system is the collaboration of technology which oversee the

process of monitoring and maintaining the inventories , raw- material, and finished goods as

well which is ready for sell. By using inventory system in the company, they can find

minimise the unnecessary and extra cost apart from this company may know how much

inventory they have to purchase so that they do not have to face issues of surplus and deficit in

the inventory.

Price optimization

Prize optimisation is the procedure of collecting data from the customers and from the

market to analyse the exact price which is going on in the market and help the company to set

price of their product so that they do not have to face any kind of problem. If company charges

higher prices then its competitors no one customer will buy the good and products from the

particular company and if the company charges lower price as compared to the competitors then

it may have to face loss. So here prize optimisation helps the company to put the accurate cost.

For prize optimisation, company may gather data from customer survey, machine learning

outputs, and from the historical prices.

1.3 Benefits of management accounting system

Decision making

One of the biggest benefit of management accounting system that it provides different

charts, graph, tables which is beneficial for the company to forecast the revenues and sales of

the business apart from this, it is an accounting technique whi9ch is being used by the company

for costing, and statistics so that company make take the correct decision in the favour of the

company.

Planning

Management accounting helps the managers to analysis the data so that they can plan

the activities of the organisation and business. As per the given data management can make

p0lans and policies so that organisation do not have to face any kind of loss.

Controlling

The actual performance of any business is being compared and measured with the

standard plan so that the management can know how many efforts they have to put more so that

the usage of inventory, this system is helpful for the company to track down the goods from

supply chain to the sale. This system is the collaboration of technology which oversee the

process of monitoring and maintaining the inventories , raw- material, and finished goods as

well which is ready for sell. By using inventory system in the company, they can find

minimise the unnecessary and extra cost apart from this company may know how much

inventory they have to purchase so that they do not have to face issues of surplus and deficit in

the inventory.

Price optimization

Prize optimisation is the procedure of collecting data from the customers and from the

market to analyse the exact price which is going on in the market and help the company to set

price of their product so that they do not have to face any kind of problem. If company charges

higher prices then its competitors no one customer will buy the good and products from the

particular company and if the company charges lower price as compared to the competitors then

it may have to face loss. So here prize optimisation helps the company to put the accurate cost.

For prize optimisation, company may gather data from customer survey, machine learning

outputs, and from the historical prices.

1.3 Benefits of management accounting system

Decision making

One of the biggest benefit of management accounting system that it provides different

charts, graph, tables which is beneficial for the company to forecast the revenues and sales of

the business apart from this, it is an accounting technique whi9ch is being used by the company

for costing, and statistics so that company make take the correct decision in the favour of the

company.

Planning

Management accounting helps the managers to analysis the data so that they can plan

the activities of the organisation and business. As per the given data management can make

p0lans and policies so that organisation do not have to face any kind of loss.

Controlling

The actual performance of any business is being compared and measured with the

standard plan so that the management can know how many efforts they have to put more so that

they may attain their target profit and goal. This can only possible by management accounting.

Die to management accounting management of the company can make changes in the plans and

strategies and also the management can (makeBasova and et.al, 2020) budget for the standard

costing and budgetary as well.

Services to customer

With the help of management accounting, company may provide better and improves

services to the customers. And also make changes if the customer is not satisfied with the

product.

2.1 cost card

Particulars January February

Direct material 132000 114000

Direct labour 88000 76000

Variable production 55000 47500

Prime cost 275000 237500

Fixed production 20000 20000

Cost of goods 295000 257500

Variable selling cost 11000 9500

fixed selling cost 2000 2000

Cost of goods sold 308000 269000

Marginal costing

Particular Amount in £ (January) Amount in £ (February)

Sales 315000 332500

Direct labour 88000 76000

Direct material 132000 114000

Die to management accounting management of the company can make changes in the plans and

strategies and also the management can (makeBasova and et.al, 2020) budget for the standard

costing and budgetary as well.

Services to customer

With the help of management accounting, company may provide better and improves

services to the customers. And also make changes if the customer is not satisfied with the

product.

2.1 cost card

Particulars January February

Direct material 132000 114000

Direct labour 88000 76000

Variable production 55000 47500

Prime cost 275000 237500

Fixed production 20000 20000

Cost of goods 295000 257500

Variable selling cost 11000 9500

fixed selling cost 2000 2000

Cost of goods sold 308000 269000

Marginal costing

Particular Amount in £ (January) Amount in £ (February)

Sales 315000 332500

Direct labour 88000 76000

Direct material 132000 114000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

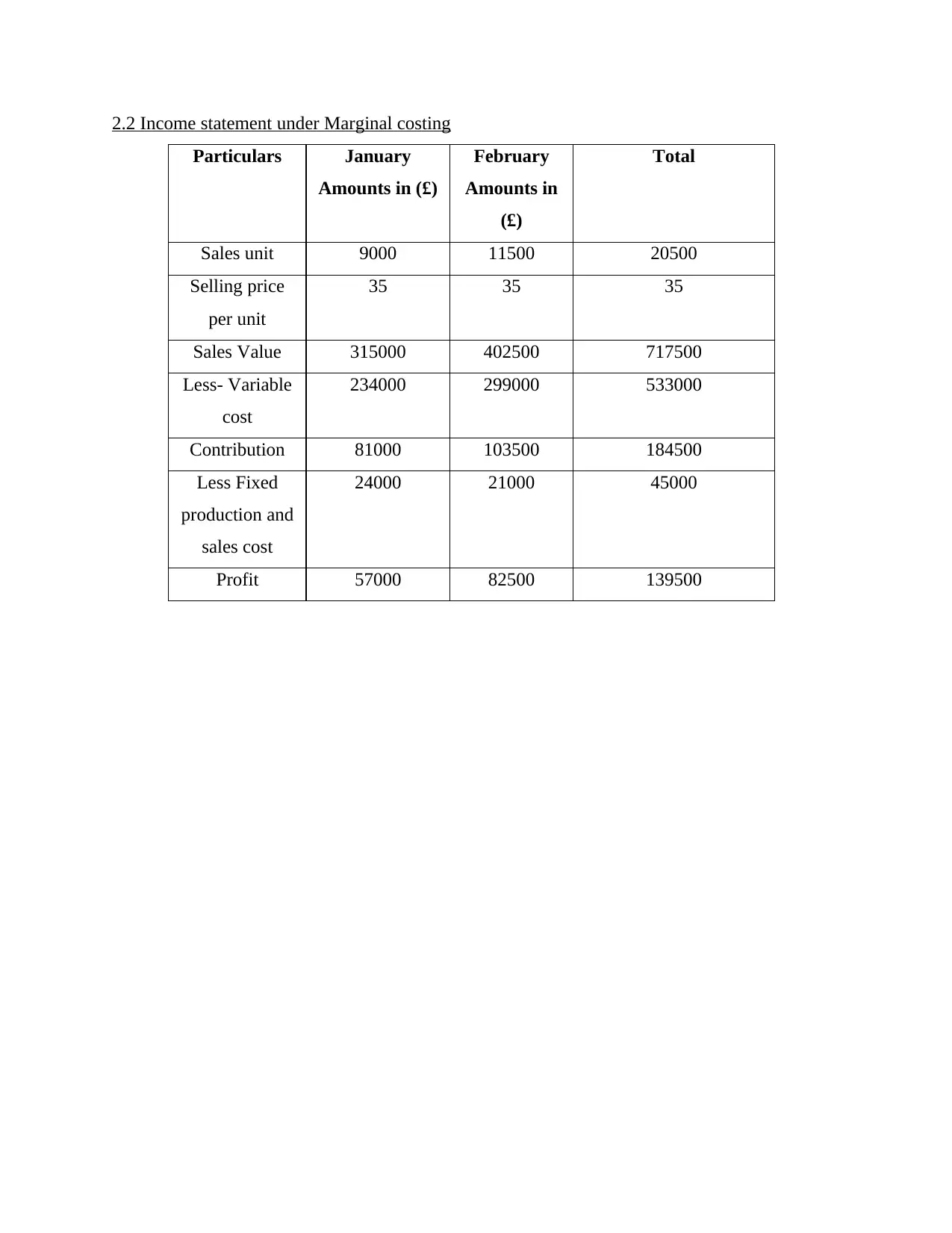

2.2 Income statement under Marginal costing

Particulars January

Amounts in (£)

February

Amounts in

(£)

Total

Sales unit 9000 11500 20500

Selling price

per unit

35 35 35

Sales Value 315000 402500 717500

Less- Variable

cost

234000 299000 533000

Contribution 81000 103500 184500

Less Fixed

production and

sales cost

24000 21000 45000

Profit 57000 82500 139500

Particulars January

Amounts in (£)

February

Amounts in

(£)

Total

Sales unit 9000 11500 20500

Selling price

per unit

35 35 35

Sales Value 315000 402500 717500

Less- Variable

cost

234000 299000 533000

Contribution 81000 103500 184500

Less Fixed

production and

sales cost

24000 21000 45000

Profit 57000 82500 139500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

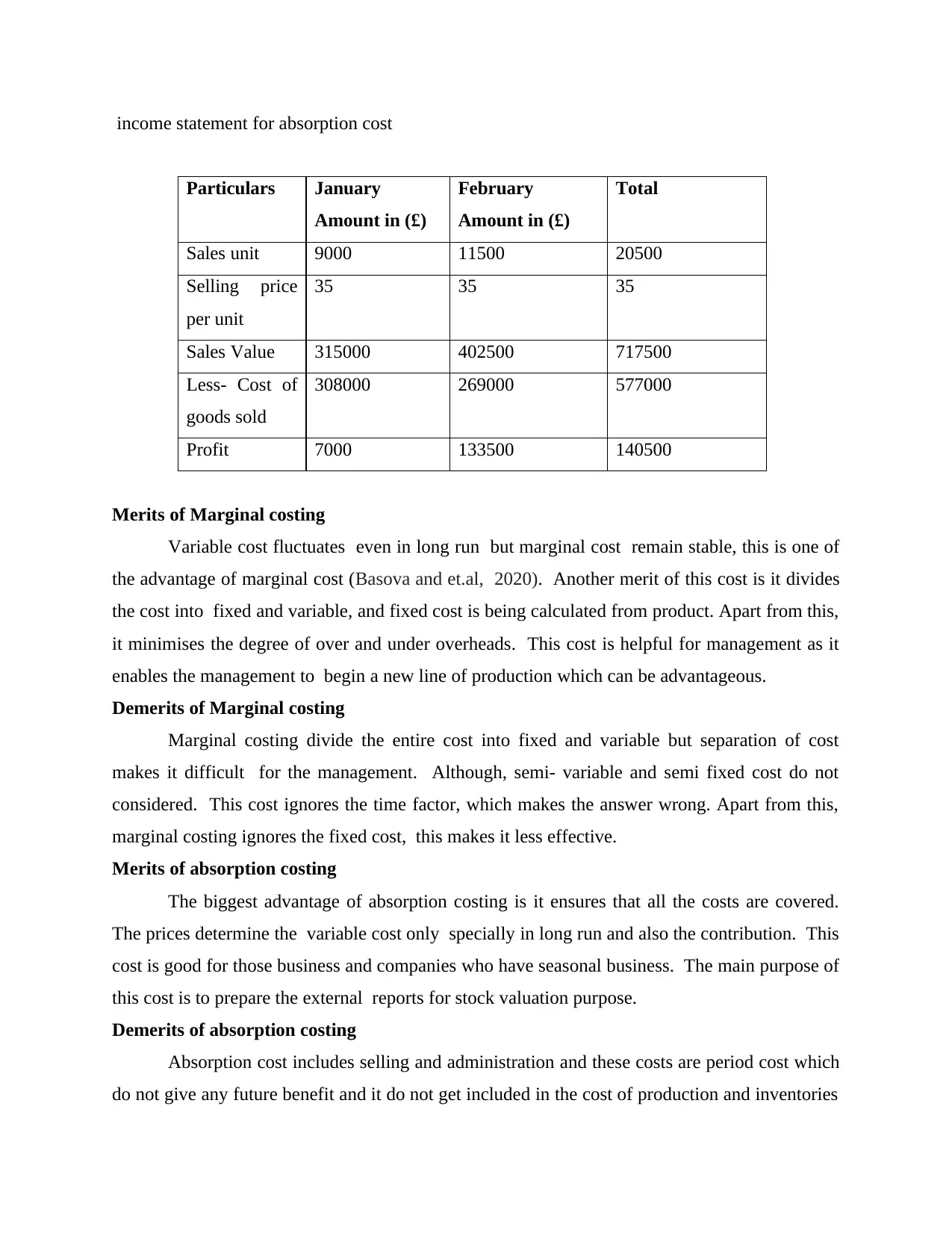

income statement for absorption cost

Particulars January

Amount in (£)

February

Amount in (£)

Total

Sales unit 9000 11500 20500

Selling price

per unit

35 35 35

Sales Value 315000 402500 717500

Less- Cost of

goods sold

308000 269000 577000

Profit 7000 133500 140500

Merits of Marginal costing

Variable cost fluctuates even in long run but marginal cost remain stable, this is one of

the advantage of marginal cost (Basova and et.al, 2020). Another merit of this cost is it divides

the cost into fixed and variable, and fixed cost is being calculated from product. Apart from this,

it minimises the degree of over and under overheads. This cost is helpful for management as it

enables the management to begin a new line of production which can be advantageous.

Demerits of Marginal costing

Marginal costing divide the entire cost into fixed and variable but separation of cost

makes it difficult for the management. Although, semi- variable and semi fixed cost do not

considered. This cost ignores the time factor, which makes the answer wrong. Apart from this,

marginal costing ignores the fixed cost, this makes it less effective.

Merits of absorption costing

The biggest advantage of absorption costing is it ensures that all the costs are covered.

The prices determine the variable cost only specially in long run and also the contribution. This

cost is good for those business and companies who have seasonal business. The main purpose of

this cost is to prepare the external reports for stock valuation purpose.

Demerits of absorption costing

Absorption cost includes selling and administration and these costs are period cost which

do not give any future benefit and it do not get included in the cost of production and inventories

Particulars January

Amount in (£)

February

Amount in (£)

Total

Sales unit 9000 11500 20500

Selling price

per unit

35 35 35

Sales Value 315000 402500 717500

Less- Cost of

goods sold

308000 269000 577000

Profit 7000 133500 140500

Merits of Marginal costing

Variable cost fluctuates even in long run but marginal cost remain stable, this is one of

the advantage of marginal cost (Basova and et.al, 2020). Another merit of this cost is it divides

the cost into fixed and variable, and fixed cost is being calculated from product. Apart from this,

it minimises the degree of over and under overheads. This cost is helpful for management as it

enables the management to begin a new line of production which can be advantageous.

Demerits of Marginal costing

Marginal costing divide the entire cost into fixed and variable but separation of cost

makes it difficult for the management. Although, semi- variable and semi fixed cost do not

considered. This cost ignores the time factor, which makes the answer wrong. Apart from this,

marginal costing ignores the fixed cost, this makes it less effective.

Merits of absorption costing

The biggest advantage of absorption costing is it ensures that all the costs are covered.

The prices determine the variable cost only specially in long run and also the contribution. This

cost is good for those business and companies who have seasonal business. The main purpose of

this cost is to prepare the external reports for stock valuation purpose.

Demerits of absorption costing

Absorption cost includes selling and administration and these costs are period cost which

do not give any future benefit and it do not get included in the cost of production and inventories

as well (Eory and et.al, 2018). This cost is not useful in the process of decision making, different

types of managerial problem like – selection of product mix, whether they should bough or not.

types of managerial problem like – selection of product mix, whether they should bough or not.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

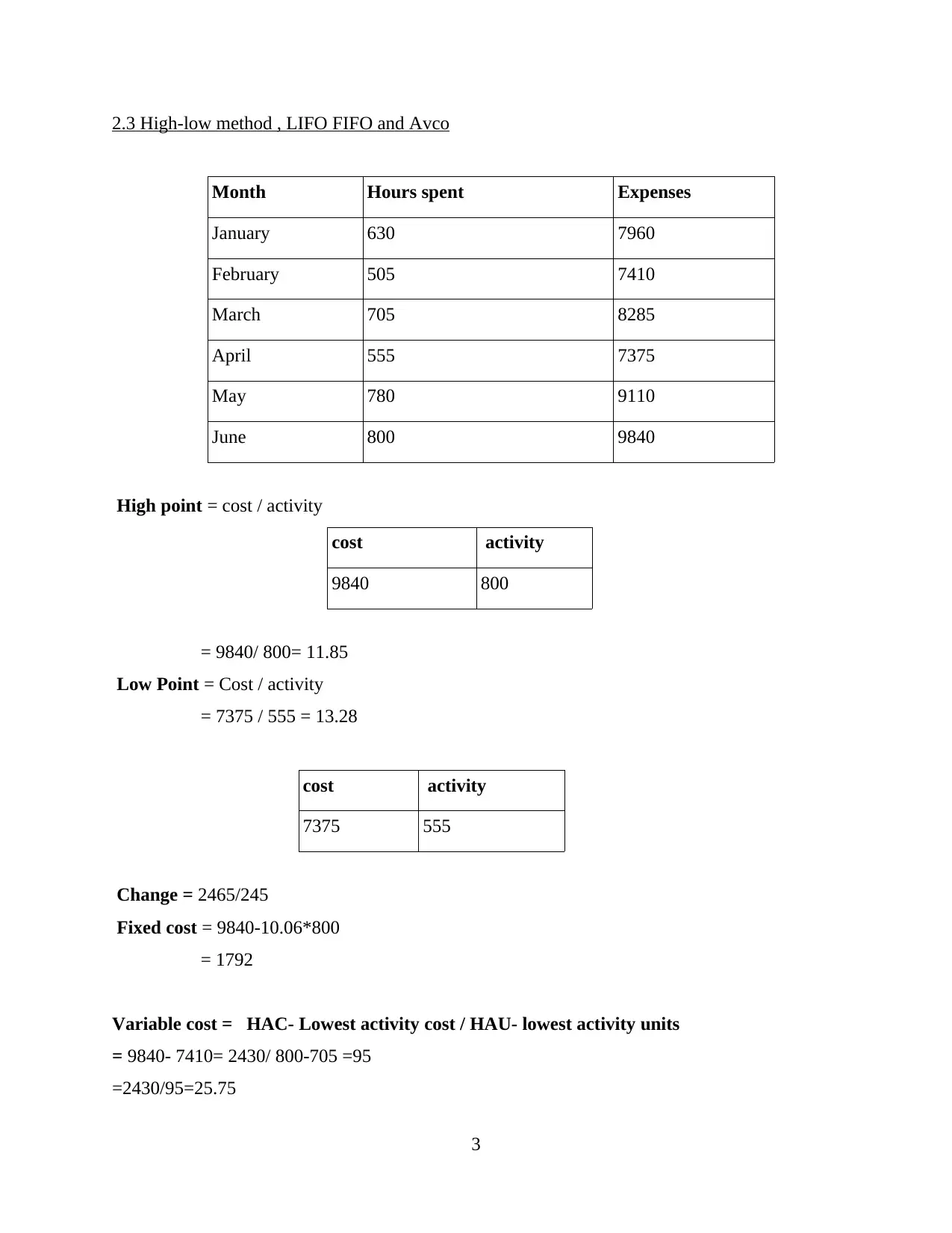

2.3 High-low method , LIFO FIFO and Avco

Month Hours spent Expenses

January 630 7960

February 505 7410

March 705 8285

April 555 7375

May 780 9110

June 800 9840

High point = cost / activity

cost activity

9840 800

= 9840/ 800= 11.85

Low Point = Cost / activity

= 7375 / 555 = 13.28

cost activity

7375 555

Change = 2465/245

Fixed cost = 9840-10.06*800

= 1792

Variable cost = HAC- Lowest activity cost / HAU- lowest activity units

= 9840- 7410= 2430/ 800-705 =95

=2430/95=25.75

3

Month Hours spent Expenses

January 630 7960

February 505 7410

March 705 8285

April 555 7375

May 780 9110

June 800 9840

High point = cost / activity

cost activity

9840 800

= 9840/ 800= 11.85

Low Point = Cost / activity

= 7375 / 555 = 13.28

cost activity

7375 555

Change = 2465/245

Fixed cost = 9840-10.06*800

= 1792

Variable cost = HAC- Lowest activity cost / HAU- lowest activity units

= 9840- 7410= 2430/ 800-705 =95

=2430/95=25.75

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

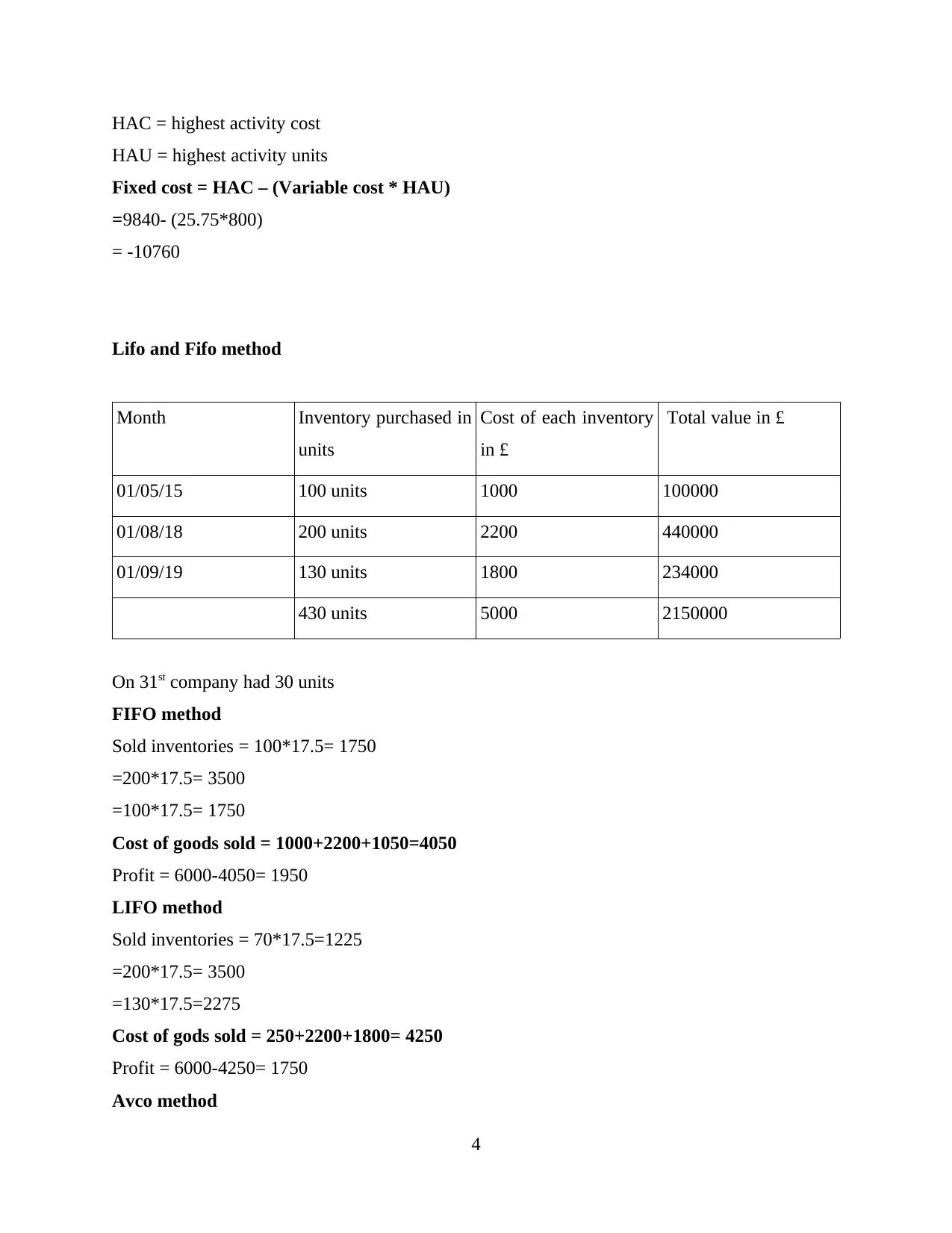

HAC = highest activity cost

HAU = highest activity units

Fixed cost = HAC – (Variable cost * HAU)

=9840- (25.75*800)

= -10760

Lifo and Fifo method

Month Inventory purchased in

units

Cost of each inventory

in £

Total value in £

01/05/15 100 units 1000 100000

01/08/18 200 units 2200 440000

01/09/19 130 units 1800 234000

430 units 5000 2150000

On 31st company had 30 units

FIFO method

Sold inventories = 100*17.5= 1750

=200*17.5= 3500

=100*17.5= 1750

Cost of goods sold = 1000+2200+1050=4050

Profit = 6000-4050= 1950

LIFO method

Sold inventories = 70*17.5=1225

=200*17.5= 3500

=130*17.5=2275

Cost of gods sold = 250+2200+1800= 4250

Profit = 6000-4250= 1750

Avco method

4

HAU = highest activity units

Fixed cost = HAC – (Variable cost * HAU)

=9840- (25.75*800)

= -10760

Lifo and Fifo method

Month Inventory purchased in

units

Cost of each inventory

in £

Total value in £

01/05/15 100 units 1000 100000

01/08/18 200 units 2200 440000

01/09/19 130 units 1800 234000

430 units 5000 2150000

On 31st company had 30 units

FIFO method

Sold inventories = 100*17.5= 1750

=200*17.5= 3500

=100*17.5= 1750

Cost of goods sold = 1000+2200+1050=4050

Profit = 6000-4050= 1950

LIFO method

Sold inventories = 70*17.5=1225

=200*17.5= 3500

=130*17.5=2275

Cost of gods sold = 250+2200+1800= 4250

Profit = 6000-4250= 1750

Avco method

4

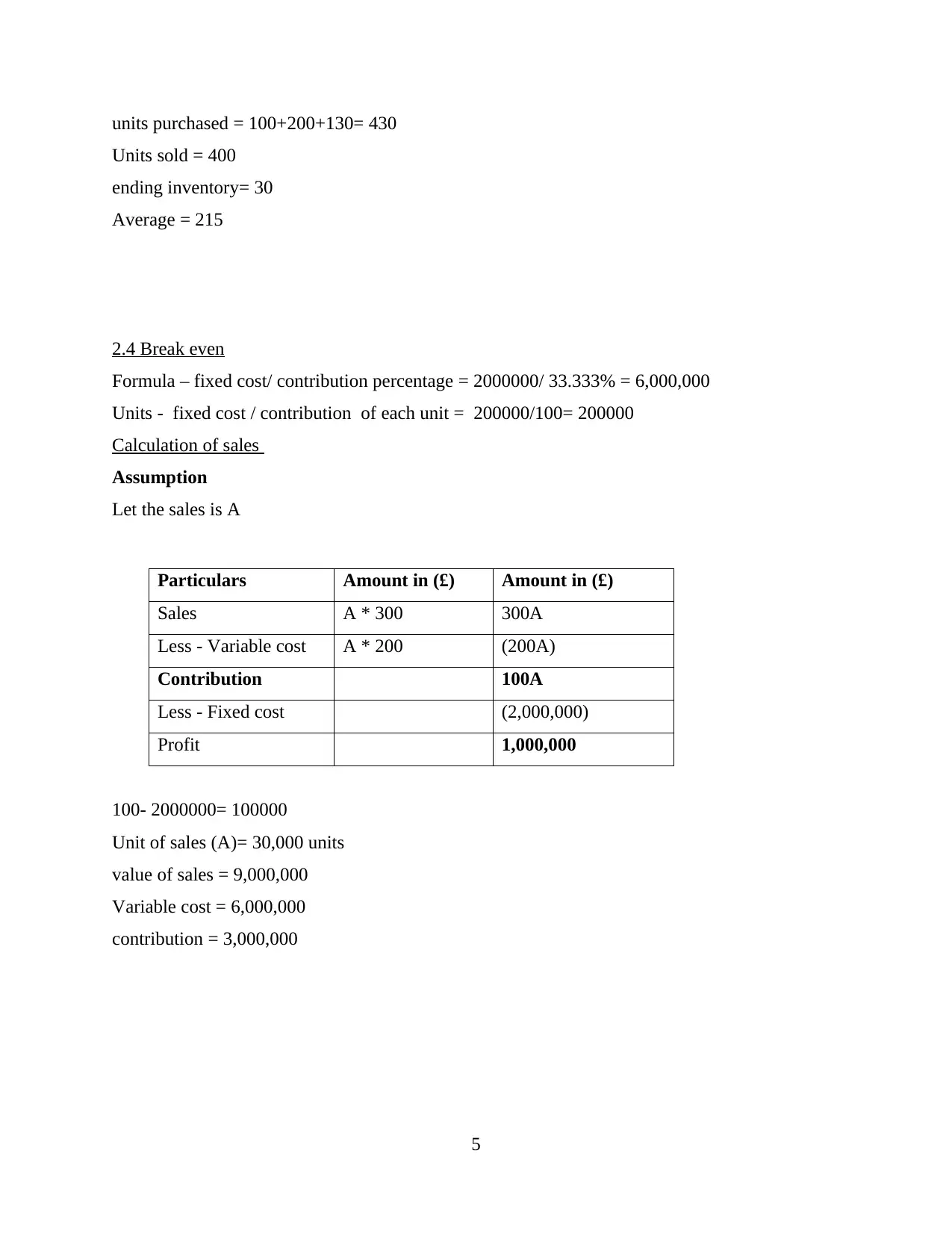

units purchased = 100+200+130= 430

Units sold = 400

ending inventory= 30

Average = 215

2.4 Break even

Formula – fixed cost/ contribution percentage = 2000000/ 33.333% = 6,000,000

Units - fixed cost / contribution of each unit = 200000/100= 200000

Calculation of sales

Assumption

Let the sales is A

Particulars Amount in (£) Amount in (£)

Sales A * 300 300A

Less - Variable cost A * 200 (200A)

Contribution 100A

Less - Fixed cost (2,000,000)

Profit 1,000,000

100- 2000000= 100000

Unit of sales (A)= 30,000 units

value of sales = 9,000,000

Variable cost = 6,000,000

contribution = 3,000,000

5

Units sold = 400

ending inventory= 30

Average = 215

2.4 Break even

Formula – fixed cost/ contribution percentage = 2000000/ 33.333% = 6,000,000

Units - fixed cost / contribution of each unit = 200000/100= 200000

Calculation of sales

Assumption

Let the sales is A

Particulars Amount in (£) Amount in (£)

Sales A * 300 300A

Less - Variable cost A * 200 (200A)

Contribution 100A

Less - Fixed cost (2,000,000)

Profit 1,000,000

100- 2000000= 100000

Unit of sales (A)= 30,000 units

value of sales = 9,000,000

Variable cost = 6,000,000

contribution = 3,000,000

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.