Management Accounting: Concepts, Techniques, and Decision Making

VerifiedAdded on 2023/01/12

|14

|3796

|44

Report

AI Summary

This report delves into the realm of management accounting, exploring its concepts, techniques, and their application in business decision-making. It begins with an introduction to management accounting, its systems, and the methods used for reporting, laying the groundwork for understanding its role in organizational development. The report then analyzes specific managerial accounting techniques like absorption and marginal costing through income statements, providing practical insights into cost analysis and profit determination. It further examines various planning tools, such as budgetary control techniques including zero-base, rolling, and activity-based budgets. The report also explores the impact of integrating managerial accounting systems and reports and how these tools can be used to overcome financial problems and lead organizations to sustainable success. Finally, the report concludes with an evaluation of how planning tools for accounting respond appropriately to solving financial problems, ultimately emphasizing the significance of management accounting in achieving organizational objectives. The report uses the case of Crèmes Limited to illustrate the practical application of these concepts and techniques.

Management Accounting Concepts and

Techniques in Decision Making

Techniques in Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................2

TASK1.............................................................................................................................................3

P1 Interpretation of Management accounting system................................................................3

P2 Methods used for management accounting reporting............................................................4

M1 Advantages of using management accounting system..........................................................1

D1 Impact of integration of managerial accounting system and reports..................................1

TASK 2............................................................................................................................................1

P3 Income statement using managerial accounting techniques...................................................1

D2 Interpretation of data by financial report...............................................................................4

TASK 3............................................................................................................................................4

P4 Interpretation of advantage and disadvantages of managerial planning tools...............4

M3 Uses of planning tools for budgeting and forecasting process..............................................6

TASK4.............................................................................................................................................6

P5 Explanation of how managerial accounting tool uses to overcome financial problem..........6

M4 Analyses how, in responding to financial problems, management accounting can lead

organisations to sustainable success............................................................................................8

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success................................................................8

CONCLUSION................................................................................................................................8

REFRENCES...................................................................................................................................9

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................2

TASK1.............................................................................................................................................3

P1 Interpretation of Management accounting system................................................................3

P2 Methods used for management accounting reporting............................................................4

M1 Advantages of using management accounting system..........................................................1

D1 Impact of integration of managerial accounting system and reports..................................1

TASK 2............................................................................................................................................1

P3 Income statement using managerial accounting techniques...................................................1

D2 Interpretation of data by financial report...............................................................................4

TASK 3............................................................................................................................................4

P4 Interpretation of advantage and disadvantages of managerial planning tools...............4

M3 Uses of planning tools for budgeting and forecasting process..............................................6

TASK4.............................................................................................................................................6

P5 Explanation of how managerial accounting tool uses to overcome financial problem..........6

M4 Analyses how, in responding to financial problems, management accounting can lead

organisations to sustainable success............................................................................................8

D3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success................................................................8

CONCLUSION................................................................................................................................8

REFRENCES...................................................................................................................................9

INTRODUCTION

Management accounting is provision of information collect from recording, analyzing,

evaluating transaction of daily business activites it is used for development of business. It also

known as managerial accounting. In other words management accounting is a systematic process

of decision making with the uses of accounting data. Business organization use policies,

techniques and various systems to formulate, planning and controlling managerial functional

activites. In order to understand the concept of management accounting Crèmes limited has been

taken. This organization provides ice creams, doughnuts, waffles food products and provides

service to their customers it is medium size organization, which is now suffers from financial

problem, to solve their problem this report has been prepared which contains all the essential

information regarding use of system, tools of management accounting to overcome issues of the

organization.

TASK1

P1 Interpretation of Management accounting system

Management accounting: It is a combination of two words management and accounting.

Management refers to the process of planning, organizing, coordinating, directing and

controlling business activites and accounting is a framework through which manager collect

information of daily transaction. Management accounting is systematic framework of presenting

accounting data in an efficient way which will assists manager for creation of policies. It is not a

special function of accounting it comprise as any form of accounting through which organization

conduct their activites more efficiently. Following are the system manager can use:

Job Costing System: This system is used in managerial accounting procedure in order to

determine cost of each activity of business. This method comprise of 6phases which start with

organization take inquiry related to the needs of customers and ending up with providing

products and services to customer. Job costing system is used for identifying enquiries, related to

the job activity (Resta, Gaiardelli, Pinto and Dotti, 2016).

Price Optimising System: It is implemented within the organization to understand the effect of

demand and supply factor of price discrimination Price optimization system will be used to

determine prices of product through which company can gain profits and established their

Management accounting is provision of information collect from recording, analyzing,

evaluating transaction of daily business activites it is used for development of business. It also

known as managerial accounting. In other words management accounting is a systematic process

of decision making with the uses of accounting data. Business organization use policies,

techniques and various systems to formulate, planning and controlling managerial functional

activites. In order to understand the concept of management accounting Crèmes limited has been

taken. This organization provides ice creams, doughnuts, waffles food products and provides

service to their customers it is medium size organization, which is now suffers from financial

problem, to solve their problem this report has been prepared which contains all the essential

information regarding use of system, tools of management accounting to overcome issues of the

organization.

TASK1

P1 Interpretation of Management accounting system

Management accounting: It is a combination of two words management and accounting.

Management refers to the process of planning, organizing, coordinating, directing and

controlling business activites and accounting is a framework through which manager collect

information of daily transaction. Management accounting is systematic framework of presenting

accounting data in an efficient way which will assists manager for creation of policies. It is not a

special function of accounting it comprise as any form of accounting through which organization

conduct their activites more efficiently. Following are the system manager can use:

Job Costing System: This system is used in managerial accounting procedure in order to

determine cost of each activity of business. This method comprise of 6phases which start with

organization take inquiry related to the needs of customers and ending up with providing

products and services to customer. Job costing system is used for identifying enquiries, related to

the job activity (Resta, Gaiardelli, Pinto and Dotti, 2016).

Price Optimising System: It is implemented within the organization to understand the effect of

demand and supply factor of price discrimination Price optimization system will be used to

determine prices of product through which company can gain profits and established their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

position in market. Manager will use price penetration, discounting pricing strategies, and cost

pricing in order to take decision regarding their price.

Cost Accounting system: It includes all the procedure through which organization can calculate

cost of processing, cost incurred during purchasing installing and uses of equipment for

manufacturing process it includes, marginal, job costing, process costing, standard costing

method which will help in identifying cost and risk for the organization.

Inventory Management System: It is one of the most useful system for business organizations.

Manager use this system to determine cost of inventor, it will help in maintain stock in an

efficient way . Managers use EOQ, ABC anaysis.JIT system it will help in determining numbers

and quality acquire at minimum, maximum level of stock

P2 Methods used for management accounting reporting.

Management accounting reports are formulated for providing facilities to manager to collect

information and decision related to future project. Following are the reports Creams Limited

can used for their organization

Budgeting report: This report is prepared on the basis of collection of information from

operating, financial, production purchases and master budget. Budget report is the summery

which explain to future inflow and outflow of business organization. Manager of Creams limited

will use this report for identifying their incomes and expenses and profitability rate of projects.

This report helps in analysing risk and also by formulating this report (Resta, Gaiardelli, Pinto

and Dotti, 2016).

Account receivable report: met is most essential managerial accounting report for

organizations. This report is formulated to determine the numbers of default debtors present in

organization. This report also help in identifying cause3s of slow growth rate of company and

debtors unable to pay their debt liabilities. By using summery data of account receivable report

manager of Creams limited will be make polices regarding their debtors so that they can able to

pay their liability amount to the company within short period of time and it will also help in

taking decision regarding attractive debtor policy so that debtors get attracted towards the offers

and it will help in increasing cash sales for to organization. This report is useful for enhancing

cash inflow of to organization

pricing in order to take decision regarding their price.

Cost Accounting system: It includes all the procedure through which organization can calculate

cost of processing, cost incurred during purchasing installing and uses of equipment for

manufacturing process it includes, marginal, job costing, process costing, standard costing

method which will help in identifying cost and risk for the organization.

Inventory Management System: It is one of the most useful system for business organizations.

Manager use this system to determine cost of inventor, it will help in maintain stock in an

efficient way . Managers use EOQ, ABC anaysis.JIT system it will help in determining numbers

and quality acquire at minimum, maximum level of stock

P2 Methods used for management accounting reporting.

Management accounting reports are formulated for providing facilities to manager to collect

information and decision related to future project. Following are the reports Creams Limited

can used for their organization

Budgeting report: This report is prepared on the basis of collection of information from

operating, financial, production purchases and master budget. Budget report is the summery

which explain to future inflow and outflow of business organization. Manager of Creams limited

will use this report for identifying their incomes and expenses and profitability rate of projects.

This report helps in analysing risk and also by formulating this report (Resta, Gaiardelli, Pinto

and Dotti, 2016).

Account receivable report: met is most essential managerial accounting report for

organizations. This report is formulated to determine the numbers of default debtors present in

organization. This report also help in identifying cause3s of slow growth rate of company and

debtors unable to pay their debt liabilities. By using summery data of account receivable report

manager of Creams limited will be make polices regarding their debtors so that they can able to

pay their liability amount to the company within short period of time and it will also help in

taking decision regarding attractive debtor policy so that debtors get attracted towards the offers

and it will help in increasing cash sales for to organization. This report is useful for enhancing

cash inflow of to organization

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory report: Business entities use managerial inventory report to collect information

regarding inventory. It will help in provide summery related to stock valuation, verification, cost

of maintaining inventory, level of maximum, minimum numbers of inventories etc. Bt using this

report managers can prepared polices to control their cost by managing wastage active an tools

of inventories.

Performance report: This report is brief summer of all the report, it will used for controlling

process. Managers formulated performance report for analysing performance of each employer,

sectors, department of organization. This report provides information through which manager

can recognize best employees and weak work force of the organization. Data collected from

performance report uses for take decision regarding incentive to their human resource according

to their performance (Trotman, Bauer and Humphreys, 2015).

M1 Advantages of using management accounting system

Management accounting item is vital tool for any business organization especially

Creams limited which comers under middle sixe organizations. By using various stems of

managerial accounting organization can reduce cost incurred in additional activites, theses

system also useful for determination of price of product on the basis of needs and requirement of

organization. Manager of Creams Limited will be used theses system as job costing, and prices

costing system help in determining cost and by using theses system their an achieve objectives.

D1 Impact of integration of managerial accounting system and reports

Integration of management accounting system and reports are essential both are essential

part and based on each other, manager of Creams limited made accounting reports on the basis of

data collected by management accounting system. It will help in achivement of organization goal

by effectively utilization of resource

TASK 2

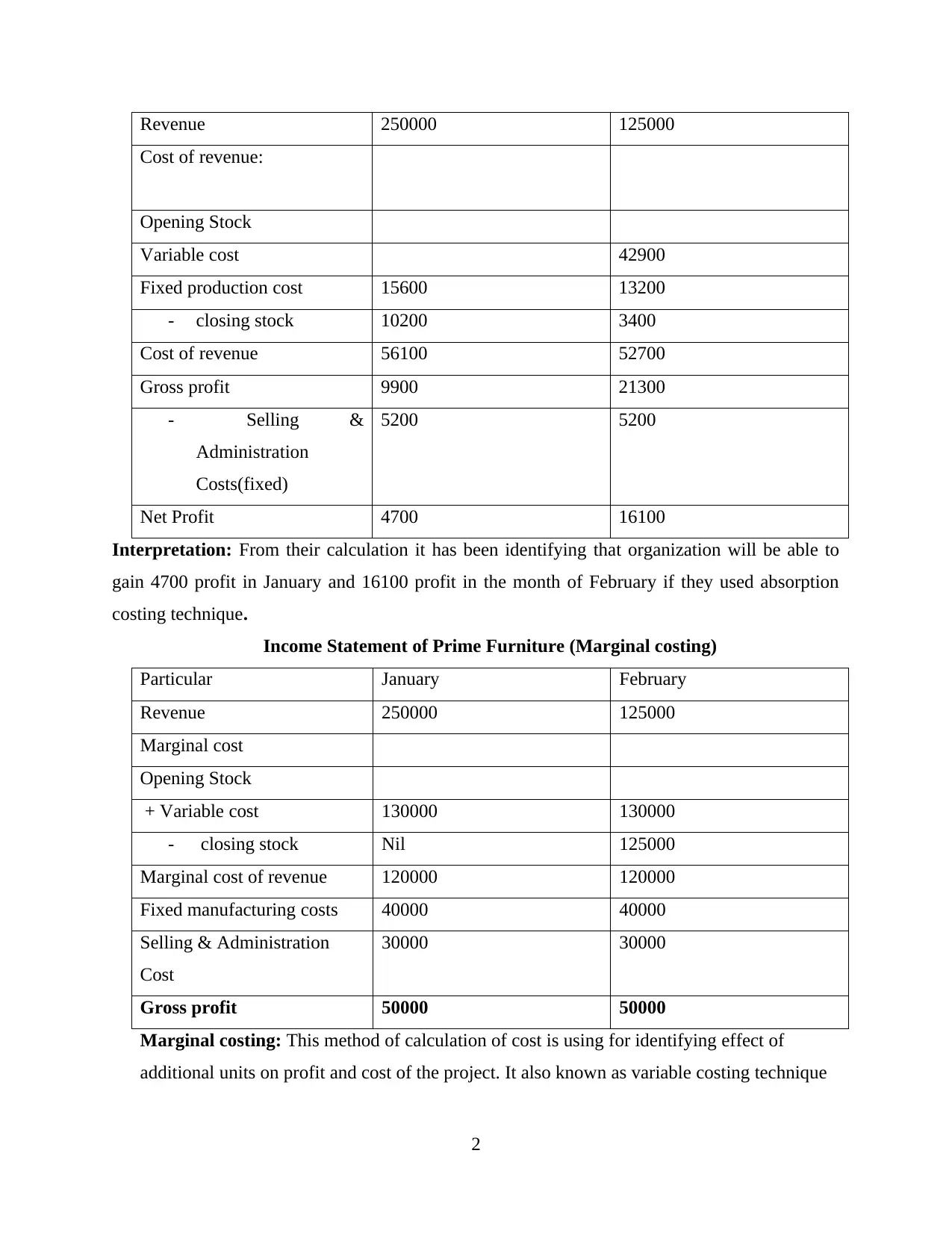

P3 Income statement using managerial accounting techniques

Absorption costing: It is a method through which organization can determine cost of

particular product by considering direct as well as indirect cost.

Income Statement of Prime Furniture (Absorption costing)

Particular January February

1

regarding inventory. It will help in provide summery related to stock valuation, verification, cost

of maintaining inventory, level of maximum, minimum numbers of inventories etc. Bt using this

report managers can prepared polices to control their cost by managing wastage active an tools

of inventories.

Performance report: This report is brief summer of all the report, it will used for controlling

process. Managers formulated performance report for analysing performance of each employer,

sectors, department of organization. This report provides information through which manager

can recognize best employees and weak work force of the organization. Data collected from

performance report uses for take decision regarding incentive to their human resource according

to their performance (Trotman, Bauer and Humphreys, 2015).

M1 Advantages of using management accounting system

Management accounting item is vital tool for any business organization especially

Creams limited which comers under middle sixe organizations. By using various stems of

managerial accounting organization can reduce cost incurred in additional activites, theses

system also useful for determination of price of product on the basis of needs and requirement of

organization. Manager of Creams Limited will be used theses system as job costing, and prices

costing system help in determining cost and by using theses system their an achieve objectives.

D1 Impact of integration of managerial accounting system and reports

Integration of management accounting system and reports are essential both are essential

part and based on each other, manager of Creams limited made accounting reports on the basis of

data collected by management accounting system. It will help in achivement of organization goal

by effectively utilization of resource

TASK 2

P3 Income statement using managerial accounting techniques

Absorption costing: It is a method through which organization can determine cost of

particular product by considering direct as well as indirect cost.

Income Statement of Prime Furniture (Absorption costing)

Particular January February

1

Revenue 250000 125000

Cost of revenue:

Opening Stock

Variable cost 42900

Fixed production cost 15600 13200

- closing stock 10200 3400

Cost of revenue 56100 52700

Gross profit 9900 21300

- Selling &

Administration

Costs(fixed)

5200 5200

Net Profit 4700 16100

Interpretation: From their calculation it has been identifying that organization will be able to

gain 4700 profit in January and 16100 profit in the month of February if they used absorption

costing technique.

Income Statement of Prime Furniture (Marginal costing)

Particular January February

Revenue 250000 125000

Marginal cost

Opening Stock

+ Variable cost 130000 130000

- closing stock Nil 125000

Marginal cost of revenue 120000 120000

Fixed manufacturing costs 40000 40000

Selling & Administration

Cost

30000 30000

Gross profit 50000 50000

Marginal costing: This method of calculation of cost is using for identifying effect of

additional units on profit and cost of the project. It also known as variable costing technique

2

Cost of revenue:

Opening Stock

Variable cost 42900

Fixed production cost 15600 13200

- closing stock 10200 3400

Cost of revenue 56100 52700

Gross profit 9900 21300

- Selling &

Administration

Costs(fixed)

5200 5200

Net Profit 4700 16100

Interpretation: From their calculation it has been identifying that organization will be able to

gain 4700 profit in January and 16100 profit in the month of February if they used absorption

costing technique.

Income Statement of Prime Furniture (Marginal costing)

Particular January February

Revenue 250000 125000

Marginal cost

Opening Stock

+ Variable cost 130000 130000

- closing stock Nil 125000

Marginal cost of revenue 120000 120000

Fixed manufacturing costs 40000 40000

Selling & Administration

Cost

30000 30000

Gross profit 50000 50000

Marginal costing: This method of calculation of cost is using for identifying effect of

additional units on profit and cost of the project. It also known as variable costing technique

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as in this method organization only consider variable cost. This will help indentifying

breakeven point of the projects (Chiarini and Vagnoni, 2015).

Absorption costing: It is a method through which organization can determine cost of

particular product by considering direct as well as indirect cost.

Interpretation: This calculation help in interpretation that if managers use marginal costing

technique then they can able to gain 5000 gross profit n the month of January as well as

February.

Standard cost: It is a modern technique of calculation of cost as this method help in utilization f

resource and minimization if cost in this method manager compare standard cost and actual cost

incurred during the project through which they can recognize amount of difference it will help in

reducing cost of the operations

Material Variance:

Material Cost Variance= Standard material cost – Actual material cost

Standard quantity * Standard Price – Actual quantity – Actual Price

Material Price Variance:

Particular Formula Amount

Material Price Variance Actual Quantity

(Standard Price –

Actual Price)

1100 (F)

Material Usage Variance

Particular Formula Amount

Material Usage Variance Standard Price (Standard

quantity – Actual quantity)

2000 (A)

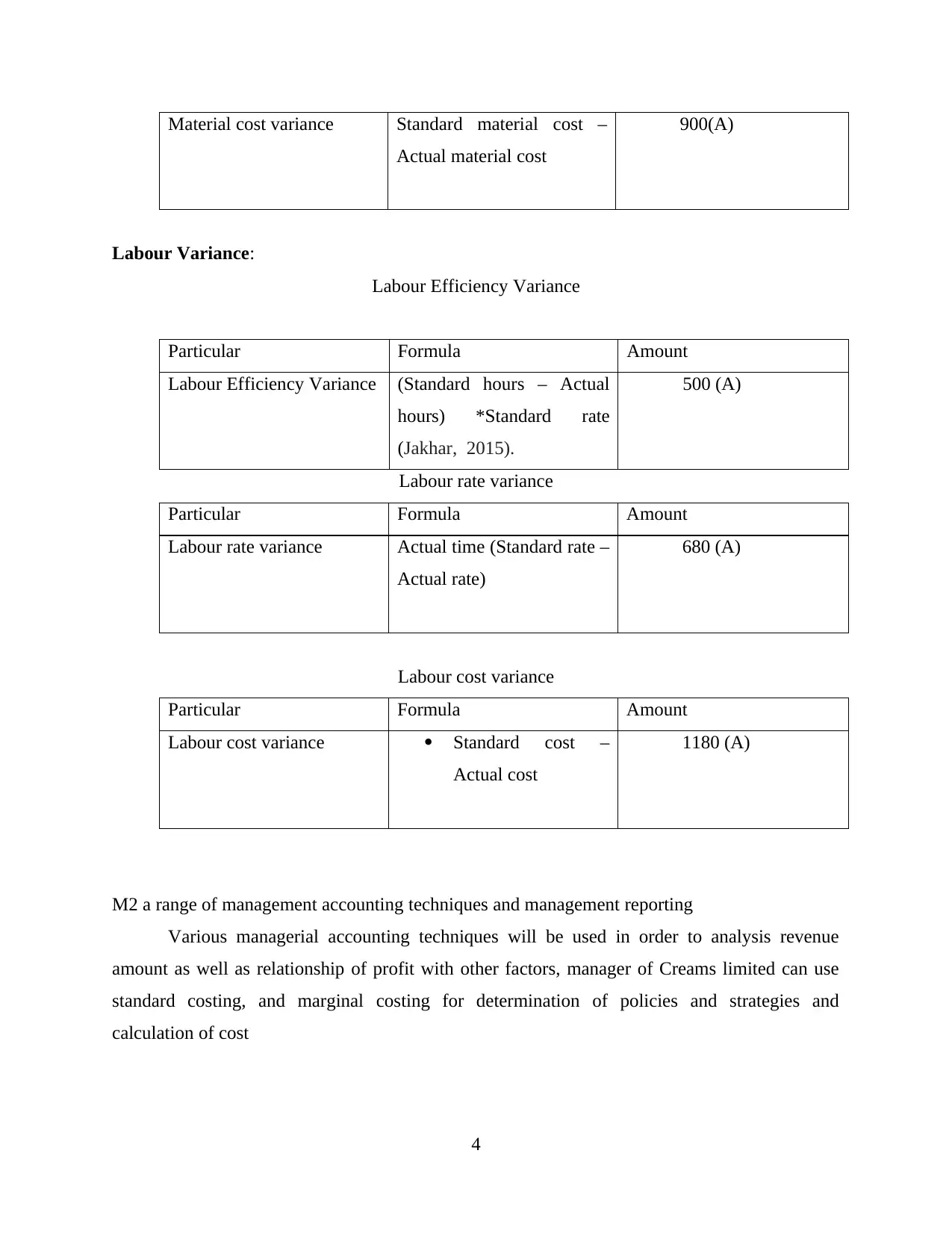

Material cost variance

Particular Formula Amount

3

breakeven point of the projects (Chiarini and Vagnoni, 2015).

Absorption costing: It is a method through which organization can determine cost of

particular product by considering direct as well as indirect cost.

Interpretation: This calculation help in interpretation that if managers use marginal costing

technique then they can able to gain 5000 gross profit n the month of January as well as

February.

Standard cost: It is a modern technique of calculation of cost as this method help in utilization f

resource and minimization if cost in this method manager compare standard cost and actual cost

incurred during the project through which they can recognize amount of difference it will help in

reducing cost of the operations

Material Variance:

Material Cost Variance= Standard material cost – Actual material cost

Standard quantity * Standard Price – Actual quantity – Actual Price

Material Price Variance:

Particular Formula Amount

Material Price Variance Actual Quantity

(Standard Price –

Actual Price)

1100 (F)

Material Usage Variance

Particular Formula Amount

Material Usage Variance Standard Price (Standard

quantity – Actual quantity)

2000 (A)

Material cost variance

Particular Formula Amount

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Material cost variance Standard material cost –

Actual material cost

900(A)

Labour Variance:

Labour Efficiency Variance

Particular Formula Amount

Labour Efficiency Variance (Standard hours – Actual

hours) *Standard rate

(Jakhar, 2015).

500 (A)

Labour rate variance

Particular Formula Amount

Labour rate variance Actual time (Standard rate –

Actual rate)

680 (A)

Labour cost variance

Particular Formula Amount

Labour cost variance Standard cost –

Actual cost

1180 (A)

M2 a range of management accounting techniques and management reporting

Various managerial accounting techniques will be used in order to analysis revenue

amount as well as relationship of profit with other factors, manager of Creams limited can use

standard costing, and marginal costing for determination of policies and strategies and

calculation of cost

4

Actual material cost

900(A)

Labour Variance:

Labour Efficiency Variance

Particular Formula Amount

Labour Efficiency Variance (Standard hours – Actual

hours) *Standard rate

(Jakhar, 2015).

500 (A)

Labour rate variance

Particular Formula Amount

Labour rate variance Actual time (Standard rate –

Actual rate)

680 (A)

Labour cost variance

Particular Formula Amount

Labour cost variance Standard cost –

Actual cost

1180 (A)

M2 a range of management accounting techniques and management reporting

Various managerial accounting techniques will be used in order to analysis revenue

amount as well as relationship of profit with other factors, manager of Creams limited can use

standard costing, and marginal costing for determination of policies and strategies and

calculation of cost

4

D2 Interpretation of data by financial report

Manager of Cream limited use data of marginal costing in order to for reports it will help

in providing best decision for the organization

TASK 3

P4 Interpretation of advantage and disadvantages of managerial planning tools

Planning tools: Theses tools of managerial accounting are used for controlling extra activites the

organization, they are help in formulating of strategies and work according to the ethical

principle of to organization. Following tools Manager of Creams Limited can be used for

controlling their business activites:

Budgetary control technique: Budget is a framework which formulated for providing

information related to future performance of organization. Following are the tools of budgetary

control (Lienert, Scholten, Egger and Maurer, 2015).

Zero Base Budgets: This budget is included in the methods of preparation of budgeting

organizations can use this method for formulate budget. In this method budget prepares from

initial level thus it also as Zero based budget.

Advantage:

This method is used for providing accurate information.

Chances of errors are comparatively low then other methods

Disadvantage

It require deep research for this type of budgets

Success of the budget depend in the skills of expertise who hire for researching and

formulation of budget.

Rolling Budget: This is one of the most useful method of budgeting in this technique budgets

are formulated for short time period probable for less then one year. When the duration of

budget complete managers compare their actual and standard target and ten format new budget

policies to remove all the errors. Many organization apply this method of budgeting

Advantage:

This method is help in enhancing efficiency.

It will help in controlling extra activites within the premises

5

Manager of Cream limited use data of marginal costing in order to for reports it will help

in providing best decision for the organization

TASK 3

P4 Interpretation of advantage and disadvantages of managerial planning tools

Planning tools: Theses tools of managerial accounting are used for controlling extra activites the

organization, they are help in formulating of strategies and work according to the ethical

principle of to organization. Following tools Manager of Creams Limited can be used for

controlling their business activites:

Budgetary control technique: Budget is a framework which formulated for providing

information related to future performance of organization. Following are the tools of budgetary

control (Lienert, Scholten, Egger and Maurer, 2015).

Zero Base Budgets: This budget is included in the methods of preparation of budgeting

organizations can use this method for formulate budget. In this method budget prepares from

initial level thus it also as Zero based budget.

Advantage:

This method is used for providing accurate information.

Chances of errors are comparatively low then other methods

Disadvantage

It require deep research for this type of budgets

Success of the budget depend in the skills of expertise who hire for researching and

formulation of budget.

Rolling Budget: This is one of the most useful method of budgeting in this technique budgets

are formulated for short time period probable for less then one year. When the duration of

budget complete managers compare their actual and standard target and ten format new budget

policies to remove all the errors. Many organization apply this method of budgeting

Advantage:

This method is help in enhancing efficiency.

It will help in controlling extra activites within the premises

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantage

It is a time consuming method.

Workforce get de motivated as the can not accept changing policies

Activity Base Budget: In this type of controlling technique budgets are prepared on the basis of

allocation of resource. Manager prepared budget by identifying cost allocation of their activites.

This type of budget is useful for manufacturing industries.

Advantage:

It will use for effectively utilization of resources

This method is helpful for controlling of cost.

Disadvantage

It is complex method of budgeting.

This method cannot adoptable for service industries.

Price strategy: Manager of Creams limited will use pricing strategies as tool of planning

control. Theses include all those strategies which will help in determination of prices of specific

product. Creams limited is provides ice cream products to their customers thus it is very

necessary for them to determine price after considering the entire factor. They can use price

penetration, price skimming strategies (Al Moussawi, Fardoun, and Louahlia-Gualous, 2016).

Advantage

This strategy will use for determination of price

It will help in identifying profitability ratio of the organization

Disadvantage

Rigid pricing policy cannot be applicable for organization as due to changes off time

customer’s demand for product change.

It requires great skills to determination of price of the product.

Cost system: This method of planning control used for control all the unwanted wastage cost for

the organization. It will help in identification of risk and formulation of policies to minimise

future risk.

Advantage:

This system is provide information related to cost

By using this system organization can get sustainability within the market

Disadvantage

6

It is a time consuming method.

Workforce get de motivated as the can not accept changing policies

Activity Base Budget: In this type of controlling technique budgets are prepared on the basis of

allocation of resource. Manager prepared budget by identifying cost allocation of their activites.

This type of budget is useful for manufacturing industries.

Advantage:

It will use for effectively utilization of resources

This method is helpful for controlling of cost.

Disadvantage

It is complex method of budgeting.

This method cannot adoptable for service industries.

Price strategy: Manager of Creams limited will use pricing strategies as tool of planning

control. Theses include all those strategies which will help in determination of prices of specific

product. Creams limited is provides ice cream products to their customers thus it is very

necessary for them to determine price after considering the entire factor. They can use price

penetration, price skimming strategies (Al Moussawi, Fardoun, and Louahlia-Gualous, 2016).

Advantage

This strategy will use for determination of price

It will help in identifying profitability ratio of the organization

Disadvantage

Rigid pricing policy cannot be applicable for organization as due to changes off time

customer’s demand for product change.

It requires great skills to determination of price of the product.

Cost system: This method of planning control used for control all the unwanted wastage cost for

the organization. It will help in identification of risk and formulation of policies to minimise

future risk.

Advantage:

This system is provide information related to cost

By using this system organization can get sustainability within the market

Disadvantage

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is complex method of calculation of cost

This method is very typical to apply in services industry.

M3 Uses of planning tools for budgeting and forecasting process

Planning tools help in forecasting and predication of future for business organization.

Manager of Creams limited use pricing strategies for determine price and they use activity

budgeting method in order to analysis their future cash inflows and also managing polices

for future objective.

TASK4

P5 Explanation of how managerial accounting tool uses to overcome financial problem.

Financial Problem: It is a type of situation which is arise due to lack of monetary resource

in the organization. Finance problem is a phase in which organizations are not able to pay or

sue their short term as well as long term liability by using their sources of funds. This type

of problem mainly arise n medium and small size industries (Kruis, Speklé, and Widener,

2016). These types of industries have potential workforce but due to their lack of capital

they suffers from problem of finance. At present time Creams Limited also suffers from

financial problem, manager of this organization cannot formulate strategies to overcome this

problem. Main reason of arise of finance problem within this organization is that they did

not have experienced or skills manager thus due to lack of managerial skills to organization

unable to formulate effective polices regarding debtor to take their payment back. From the

last 2 years sales volume of this organization also decrease this inflow of cash goes down as

compare to outflow and they suffers from financial problem. By using following tools of

managerial accounting organization will overcome from this problem:

Key Performance Indicator: This tool is used for performance evaluation method. KPI

help in measuring performance of department by using parameters. Manager of Creams

Limited will use this tool to increase their sales volume asset will help in comparing last

achieved target and current target versus gape between standard target of sales volume it

also motivated employees to increase their performance skills to get incentive as when the

sales raise their incentive amount or bonus amount t automatically raises and company

provides hem on the basis of their performance

7

This method is very typical to apply in services industry.

M3 Uses of planning tools for budgeting and forecasting process

Planning tools help in forecasting and predication of future for business organization.

Manager of Creams limited use pricing strategies for determine price and they use activity

budgeting method in order to analysis their future cash inflows and also managing polices

for future objective.

TASK4

P5 Explanation of how managerial accounting tool uses to overcome financial problem.

Financial Problem: It is a type of situation which is arise due to lack of monetary resource

in the organization. Finance problem is a phase in which organizations are not able to pay or

sue their short term as well as long term liability by using their sources of funds. This type

of problem mainly arise n medium and small size industries (Kruis, Speklé, and Widener,

2016). These types of industries have potential workforce but due to their lack of capital

they suffers from problem of finance. At present time Creams Limited also suffers from

financial problem, manager of this organization cannot formulate strategies to overcome this

problem. Main reason of arise of finance problem within this organization is that they did

not have experienced or skills manager thus due to lack of managerial skills to organization

unable to formulate effective polices regarding debtor to take their payment back. From the

last 2 years sales volume of this organization also decrease this inflow of cash goes down as

compare to outflow and they suffers from financial problem. By using following tools of

managerial accounting organization will overcome from this problem:

Key Performance Indicator: This tool is used for performance evaluation method. KPI

help in measuring performance of department by using parameters. Manager of Creams

Limited will use this tool to increase their sales volume asset will help in comparing last

achieved target and current target versus gape between standard target of sales volume it

also motivated employees to increase their performance skills to get incentive as when the

sales raise their incentive amount or bonus amount t automatically raises and company

provides hem on the basis of their performance

7

Benchmarking: It is the traditional method of managerial accounting used for resolve

problems of the organization. In benchmarking manager compare their actual outcomes with

set target or benchmark, it can be decided by organization on the basis of their rivalry

industries or target say by government or past performance of the company. By comprising

performance with ideal benchmarking manager of Creams limited can easily understood

mistakes and errors and they ill try to overcome all the errors it will help in increasing their

skills to provides term managerial service through which they are able to formulate standard

method policies for their debtor as well as creditors in order to control cash outflow and

improve cash inflow (Defoe, Dubas, Figner, and Van Aken 2015).

Financial Governance: This policy is used to track all the activites of business organization

in order to prevent them unethical activities. By using financial governance rule manager of

Creams limited able to formulate policies which work according to the ethical and law of

their constitution.

Statement of comparison

Particular Creams Ltd Bakers Restaurant Limited

Monetary issue It is mainly arise due to lack of skills

and slow growth rate of the

organization

In this organization monetary issue

arise due to lack of security of

financial resource.

Techniques to

solve issues

Creams limited uses benchmarking and

KPI technique of managerial

accounting in order to solve their

financial problem.

Manager of Bakers Restaurant

Limited used financial governance ,

balance scorecard techniques for cut

throat problems related to finance for

their organization

8

problems of the organization. In benchmarking manager compare their actual outcomes with

set target or benchmark, it can be decided by organization on the basis of their rivalry

industries or target say by government or past performance of the company. By comprising

performance with ideal benchmarking manager of Creams limited can easily understood

mistakes and errors and they ill try to overcome all the errors it will help in increasing their

skills to provides term managerial service through which they are able to formulate standard

method policies for their debtor as well as creditors in order to control cash outflow and

improve cash inflow (Defoe, Dubas, Figner, and Van Aken 2015).

Financial Governance: This policy is used to track all the activites of business organization

in order to prevent them unethical activities. By using financial governance rule manager of

Creams limited able to formulate policies which work according to the ethical and law of

their constitution.

Statement of comparison

Particular Creams Ltd Bakers Restaurant Limited

Monetary issue It is mainly arise due to lack of skills

and slow growth rate of the

organization

In this organization monetary issue

arise due to lack of security of

financial resource.

Techniques to

solve issues

Creams limited uses benchmarking and

KPI technique of managerial

accounting in order to solve their

financial problem.

Manager of Bakers Restaurant

Limited used financial governance ,

balance scorecard techniques for cut

throat problems related to finance for

their organization

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.