Management Accounting Report: Systems, Techniques and Analysis

VerifiedAdded on 2022/12/26

|28

|6033

|1

Report

AI Summary

This report provides a comprehensive overview of management accounting, detailing its principles, systems, and techniques. Part 1 focuses on various management accounting systems, including inventory management, price optimization, and cost accounting systems, and their respective roles. It emphasizes the importance of these systems in developing financial plans, improving management procedures, and maintaining profitability. The report then compares management accounting to financial accounting, highlighting their distinct purposes and users. Part 2 delves into cost techniques such as absorption costing and marginal costing, illustrating their implications for producing income statements. The report includes detailed financial statements under both costing methods, providing a clear comparison of their effects on profitability and financial reporting. Furthermore, it explores the integration of management accounting systems and reports within business processes, emphasizing how companies like UCK furniture utilize these systems to monitor output, maximize productivity, and make informed decisions. The report concludes by underscoring the importance of accurate, reliable, and updated information in management accounting for effective decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION (Part one)..........................................................................................................3

PART 1............................................................................................................................................3

CONCLUSION (Part 1)................................................................................................................18

REFERENCES (Part 1).................................................................................................................19

INTRODUCTION (Part two)........................................................................................................20

PART 2..........................................................................................................................................20

CONCLUSION (Part 2)................................................................................................................30

REFERENCES (Part 2).................................................................................................................32

INTRODUCTION (Part one)..........................................................................................................3

PART 1............................................................................................................................................3

CONCLUSION (Part 1)................................................................................................................18

REFERENCES (Part 1).................................................................................................................19

INTRODUCTION (Part two)........................................................................................................20

PART 2..........................................................................................................................................20

CONCLUSION (Part 2)................................................................................................................30

REFERENCES (Part 2).................................................................................................................32

INTRODUCTION (Part one)

Management accounting is the process of calculating company expenses and operations in order

to compile internal financial reports, accounts, journals, and journals and assist administrators in

achieving management goals (Drury, 2018). In other terms, it is the process of converting

monetary and expense information into valuable facts for effective business administration. This

reporting is used by the administrator to even provide accounting transactions to internal

customers so that they can make informed decisions and control productivity effectively. In such

part of report detailed information about different kinds of management accounting systems and

their role has been described. As well as in further part of report application of accounting

techniques is applied to produce financial statements as per the requirement.

PART 1

Section 1

1.1 Analysis of MA and requirements of each.

Management accounting with the use of technical expertise and experience to support internal

operations in the processing of business and audit reports. Different rules, strategy, and

supervision of the firm's activities are all based on these policies (Abdusalomova, 2019). The

only stipulation in management accounting is that evidence must be presented for the purpose of

promoting the effective decision making.

Importance of MA-

• Develop financial plans: The key responsibility of the management accountant is to develop

and implement successful financial strategies in order to forecast earnings and plan budgets that

contain both revenues and expenses. To keep track of all financial reports in various accounts as

required.

• Improve management procedures: This is a critical role in which management analyzes its

results and makes appropriate decisions. It would improve the major effectiveness of the key

operations by establishing a transparent and seamless internal and external process.

• Maintain profitability: There are analysing different styles of method that use by financial

manager to stay profitable of company. With the aid of research, the accountant calculate sales

toward fixed and also variable expense to know breakeven.

Management accounting is the process of calculating company expenses and operations in order

to compile internal financial reports, accounts, journals, and journals and assist administrators in

achieving management goals (Drury, 2018). In other terms, it is the process of converting

monetary and expense information into valuable facts for effective business administration. This

reporting is used by the administrator to even provide accounting transactions to internal

customers so that they can make informed decisions and control productivity effectively. In such

part of report detailed information about different kinds of management accounting systems and

their role has been described. As well as in further part of report application of accounting

techniques is applied to produce financial statements as per the requirement.

PART 1

Section 1

1.1 Analysis of MA and requirements of each.

Management accounting with the use of technical expertise and experience to support internal

operations in the processing of business and audit reports. Different rules, strategy, and

supervision of the firm's activities are all based on these policies (Abdusalomova, 2019). The

only stipulation in management accounting is that evidence must be presented for the purpose of

promoting the effective decision making.

Importance of MA-

• Develop financial plans: The key responsibility of the management accountant is to develop

and implement successful financial strategies in order to forecast earnings and plan budgets that

contain both revenues and expenses. To keep track of all financial reports in various accounts as

required.

• Improve management procedures: This is a critical role in which management analyzes its

results and makes appropriate decisions. It would improve the major effectiveness of the key

operations by establishing a transparent and seamless internal and external process.

• Maintain profitability: There are analysing different styles of method that use by financial

manager to stay profitable of company. With the aid of research, the accountant calculate sales

toward fixed and also variable expense to know breakeven.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principle of MA

• Designing and compiling: To analyse a particular business concern, all accounting records,

surveys, and other events focused on historical, current, and future results should be analysed

and collected (Abdusalomova, 2019). It refers to a framework that is structured to display all

relevant data in order to solve a particular problem.

• Administration by exception: The management uses this concept to present all necessary facts

and have control of the financial structure. Using this idea, compare real to budgeted costs and

make adjustments as needed.

Comparison of MA and FA

Basis Management Accounting Financial Accounting

Meaning Management accounting is a

mechanism that provides related

statistics to administrators in order

for them to formulate policies and

gather all financial data.

Financial accounting is a form of

accounting that focuses on the

preparing of financial statements in

order to provide financial data to

relevant consumers.

Purpose To make financial data available to

third parties.

To engage management in careful

preparations and decision-making

procedures by including accurate

reports on various activities.

Uses The corporation uses financial

accounting to present monetary data

to external customers.

MA is once used to display financial

data to internal customers.

Different types of MA system

Inventory management system- Stock control is a mechanism that uses a never-ending

inventory scheme to keep track of manufacturing operations. In basic terms, it means that as a

product moves from one phase to another at each point, from raw material to finished product, it

• Designing and compiling: To analyse a particular business concern, all accounting records,

surveys, and other events focused on historical, current, and future results should be analysed

and collected (Abdusalomova, 2019). It refers to a framework that is structured to display all

relevant data in order to solve a particular problem.

• Administration by exception: The management uses this concept to present all necessary facts

and have control of the financial structure. Using this idea, compare real to budgeted costs and

make adjustments as needed.

Comparison of MA and FA

Basis Management Accounting Financial Accounting

Meaning Management accounting is a

mechanism that provides related

statistics to administrators in order

for them to formulate policies and

gather all financial data.

Financial accounting is a form of

accounting that focuses on the

preparing of financial statements in

order to provide financial data to

relevant consumers.

Purpose To make financial data available to

third parties.

To engage management in careful

preparations and decision-making

procedures by including accurate

reports on various activities.

Uses The corporation uses financial

accounting to present monetary data

to external customers.

MA is once used to display financial

data to internal customers.

Different types of MA system

Inventory management system- Stock control is a mechanism that uses a never-ending

inventory scheme to keep track of manufacturing operations. In basic terms, it means that as a

product moves from one phase to another at each point, from raw material to finished product, it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

must be tracked and saved in a computerized system. All of this aids the boss in keeping track of

operations and making final decisions. This method is used in the form of UCK furniture to keep

track of people who purchase products for further processing. The most critical thing of this

method is to determine when raw materials are required and when purchasing orders are needed.

Price optimization system- Price optimization method is a statistical method in which a

business checks the price of a commodity at various levels to see what amount a buyer is willing

to pay and also making a profit (Jansen, 2018). The method aids companies in determining the

price at which they may market their goods in the most quantity given the degree of competition

and product production costs. In the context of above mentioned company, such accounting

system is used with an aim to set the price of products and service at a level on which they can

satisfy need of customers in an effective manner.

Cost accounting system- Cost accounting system is method where business analyse the cost of

production by using direct and indirect costs. If businesses wish to succeed or want to gain

decent profit organizations should know the information and which one is lucrative and which

one would be not. Companies can use a cost accounting scheme to determine the cost of a

commodity at each stage: original, work-in-progress, and final. Since UCK Furniture is the

largest supermarket chain in the United Kingdom, it is critical for them to determine the correct

product cost. This system's primary function is to analyse the cost of products manufactured by

the organization.

1.2 Various kinds of methods of MA reporting.

Management accounting reports- It is a report that the organization prepares to assess the success

of each department. In these papers, all of the data from each unit is collected, and then the

appropriate decisions are made. To generate this report, all company organisations use a variety

of systems, which help them sustain consistent results. For example, UCK furniture prepares

these reports in great detail and then makes the appropriate decisions.

Inventory-management report- The organization prepares this study to learn about their stock,

which includes unnecessary expenses and labour cost per hour (Bedford and Speklé, 2018). This

research assists businesses in saving a significant amount of money by efficiently using capital.

Since inventory is the most valuable thing for a company, this report shows how businesses are

using their inventory and where they are losing it. When UCK Furniture utilizes this report to

operations and making final decisions. This method is used in the form of UCK furniture to keep

track of people who purchase products for further processing. The most critical thing of this

method is to determine when raw materials are required and when purchasing orders are needed.

Price optimization system- Price optimization method is a statistical method in which a

business checks the price of a commodity at various levels to see what amount a buyer is willing

to pay and also making a profit (Jansen, 2018). The method aids companies in determining the

price at which they may market their goods in the most quantity given the degree of competition

and product production costs. In the context of above mentioned company, such accounting

system is used with an aim to set the price of products and service at a level on which they can

satisfy need of customers in an effective manner.

Cost accounting system- Cost accounting system is method where business analyse the cost of

production by using direct and indirect costs. If businesses wish to succeed or want to gain

decent profit organizations should know the information and which one is lucrative and which

one would be not. Companies can use a cost accounting scheme to determine the cost of a

commodity at each stage: original, work-in-progress, and final. Since UCK Furniture is the

largest supermarket chain in the United Kingdom, it is critical for them to determine the correct

product cost. This system's primary function is to analyse the cost of products manufactured by

the organization.

1.2 Various kinds of methods of MA reporting.

Management accounting reports- It is a report that the organization prepares to assess the success

of each department. In these papers, all of the data from each unit is collected, and then the

appropriate decisions are made. To generate this report, all company organisations use a variety

of systems, which help them sustain consistent results. For example, UCK furniture prepares

these reports in great detail and then makes the appropriate decisions.

Inventory-management report- The organization prepares this study to learn about their stock,

which includes unnecessary expenses and labour cost per hour (Bedford and Speklé, 2018). This

research assists businesses in saving a significant amount of money by efficiently using capital.

Since inventory is the most valuable thing for a company, this report shows how businesses are

using their inventory and where they are losing it. When UCK Furniture utilizes this report to

manage their resources, they review to see if the raw material for each product is being used

correctly. It enables the business to save a significant amount of product by preventing it from

being wasted.

Cost accounting report- This document is produced by the firms to recognise the cost of product.

It contains the material cost, labour cost or any other cost. It aids the corporation in determining

the cost of production and the cost of sale of a commodity. This study will help an organization

determine their profitability. This report is used by companies like UCK furniture to determine

the appropriate price for their products. It assists the organization in providing a low-cost

commodity to the consumer, resulting in a strong target market.

Account receivable report- The organization prepares this report to learn about the credit options

available in the industry which includes the company's credit refund policy for customers. It aids

the organization in identifying defaulters and other selection issues. This study is used by

companies like UCK Furniture to keep track of their bad debt and manage it. It allows the

business to save a substantial amount of money.

1.3 Importance of each MAS.

Relevance: The data gathered by the firm must be applicable to the corporation's market

operations and required for regular data review (Rikhardsson and Yigitbasioglu, 2018). The

accountant's job is to keep records of all transactions that have a direct or indirect effect on

company operations. As a result, it is essential to recognize trustworthy data and report it in

accounting books.

Update information: All the financial records should be revised as per the updates. As

organization apply improvements in sales plan so it effects on the performance in straightforward

manner. As a result, it is essential to apply improvements in information to give current

information to the manager.

Reliability-Information should have a consistent and agreeable effect on the collection method at

all collection points. This protocol for progress events and data bases should be specifically

defined and accessible for systems from manual, automatic, and other documents.

Understandable- Financial reporting should be accessible so that people can generate effective

ideas and read it quickly. On the basis of this material, schedule planned plans and prepare for

good decision.

correctly. It enables the business to save a significant amount of product by preventing it from

being wasted.

Cost accounting report- This document is produced by the firms to recognise the cost of product.

It contains the material cost, labour cost or any other cost. It aids the corporation in determining

the cost of production and the cost of sale of a commodity. This study will help an organization

determine their profitability. This report is used by companies like UCK furniture to determine

the appropriate price for their products. It assists the organization in providing a low-cost

commodity to the consumer, resulting in a strong target market.

Account receivable report- The organization prepares this report to learn about the credit options

available in the industry which includes the company's credit refund policy for customers. It aids

the organization in identifying defaulters and other selection issues. This study is used by

companies like UCK Furniture to keep track of their bad debt and manage it. It allows the

business to save a substantial amount of money.

1.3 Importance of each MAS.

Relevance: The data gathered by the firm must be applicable to the corporation's market

operations and required for regular data review (Rikhardsson and Yigitbasioglu, 2018). The

accountant's job is to keep records of all transactions that have a direct or indirect effect on

company operations. As a result, it is essential to recognize trustworthy data and report it in

accounting books.

Update information: All the financial records should be revised as per the updates. As

organization apply improvements in sales plan so it effects on the performance in straightforward

manner. As a result, it is essential to apply improvements in information to give current

information to the manager.

Reliability-Information should have a consistent and agreeable effect on the collection method at

all collection points. This protocol for progress events and data bases should be specifically

defined and accessible for systems from manual, automatic, and other documents.

Understandable- Financial reporting should be accessible so that people can generate effective

ideas and read it quickly. On the basis of this material, schedule planned plans and prepare for

good decision.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accuracy-The accountant's data entry in the financial records must be correct because it aids the

auditor in making decisions. If an accountant fails to correctly log their payments, data can be

captured and used, even if it has many applications.

Management accounting

System

Uses Application

Cost accounting system It is used by businesses to

forecast the cost of products

and services in an efficient

manner (Hiebl, 2018).

Afterwards, determine the

price of various products.

It is used in the UCK

manufacturing industries to

analyse the cost of each

product produced by the

company.

Inventory-management system The use of this structure to

properly manage inventory and

evaluate how many amounts

are required at various stages

at various levels.

This system is used by a

company to keep track of stock

at various levels and place

orders for more UCK

manufacturing industry.

Price optimisation system It is the most critical system

that a company uses to

perform market analysis and

analyse the effects of various

consumers' perceptions of their

goods.

This method is used to set an

optimal pricing structure for

UCK furniture in order to

maximize profit in a large

sense and make the best

decisions.

1.4 Integration of MAS and MA reports with business process.

Different forms of MA programs and reports play an important role in organizational procedures.

UCK furniture uses a variety of systems to monitor output and maximize productivity in the

auditor in making decisions. If an accountant fails to correctly log their payments, data can be

captured and used, even if it has many applications.

Management accounting

System

Uses Application

Cost accounting system It is used by businesses to

forecast the cost of products

and services in an efficient

manner (Hiebl, 2018).

Afterwards, determine the

price of various products.

It is used in the UCK

manufacturing industries to

analyse the cost of each

product produced by the

company.

Inventory-management system The use of this structure to

properly manage inventory and

evaluate how many amounts

are required at various stages

at various levels.

This system is used by a

company to keep track of stock

at various levels and place

orders for more UCK

manufacturing industry.

Price optimisation system It is the most critical system

that a company uses to

perform market analysis and

analyse the effects of various

consumers' perceptions of their

goods.

This method is used to set an

optimal pricing structure for

UCK furniture in order to

maximize profit in a large

sense and make the best

decisions.

1.4 Integration of MAS and MA reports with business process.

Different forms of MA programs and reports play an important role in organizational procedures.

UCK furniture uses a variety of systems to monitor output and maximize productivity in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

most efficient way possible (Hiebl and Richter, 2018). To successfully control all commercial

operations, UCK furniture employs a variety of systems such as price optimization, cost

accounting, and inventory management. Cost accounting can be used to forecast inventory costs,

and the reports can assist with cost management. Reports are used to analyse each division and

deal with various issues in order to aid in making the best decisions possible.

Section 2

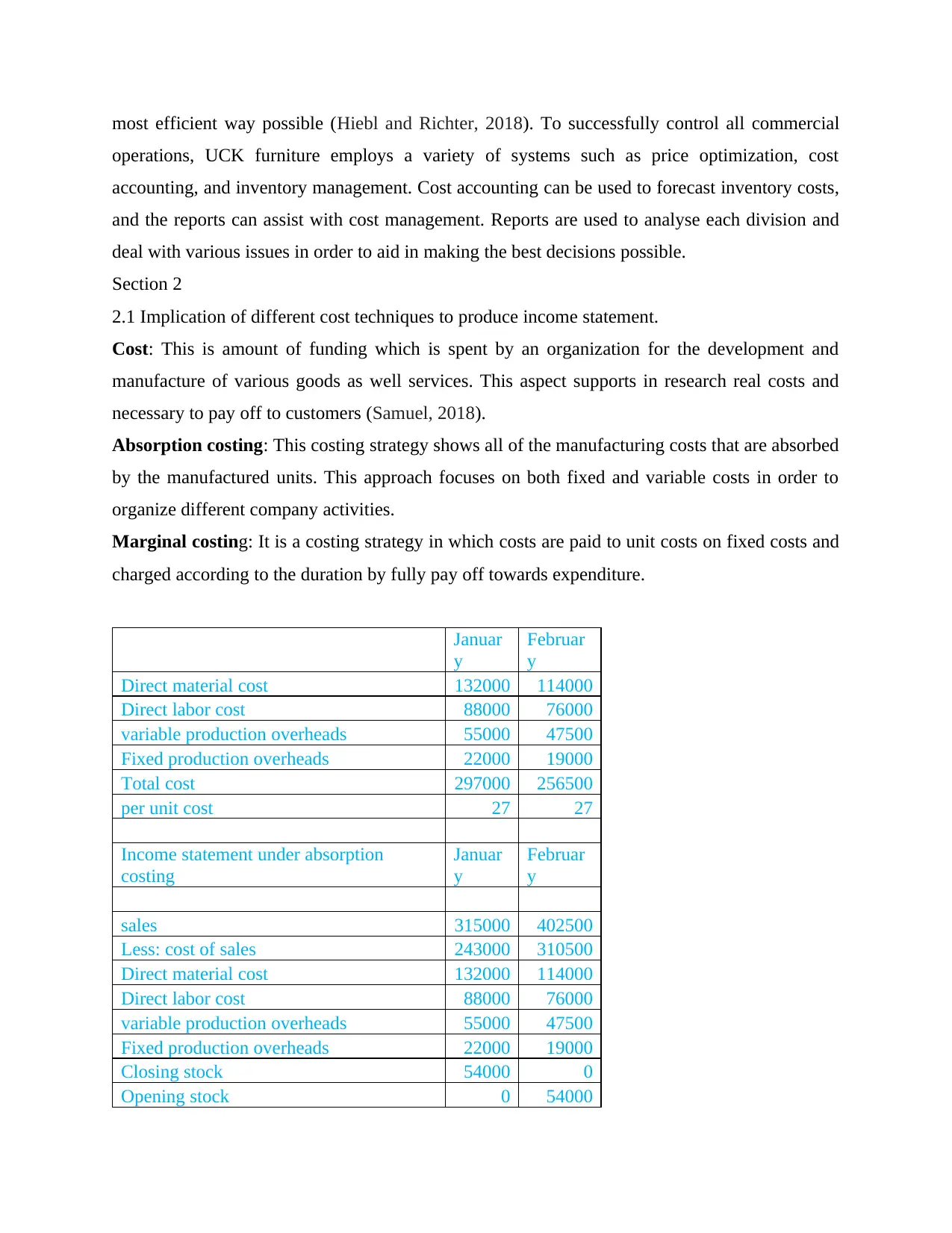

2.1 Implication of different cost techniques to produce income statement.

Cost: This is amount of funding which is spent by an organization for the development and

manufacture of various goods as well services. This aspect supports in research real costs and

necessary to pay off to customers (Samuel, 2018).

Absorption costing: This costing strategy shows all of the manufacturing costs that are absorbed

by the manufactured units. This approach focuses on both fixed and variable costs in order to

organize different company activities.

Marginal costing: It is a costing strategy in which costs are paid to unit costs on fixed costs and

charged according to the duration by fully pay off towards expenditure.

Januar

y

Februar

y

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Fixed production overheads 22000 19000

Total cost 297000 256500

per unit cost 27 27

Income statement under absorption

costing

Januar

y

Februar

y

sales 315000 402500

Less: cost of sales 243000 310500

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Fixed production overheads 22000 19000

Closing stock 54000 0

Opening stock 0 54000

operations, UCK furniture employs a variety of systems such as price optimization, cost

accounting, and inventory management. Cost accounting can be used to forecast inventory costs,

and the reports can assist with cost management. Reports are used to analyse each division and

deal with various issues in order to aid in making the best decisions possible.

Section 2

2.1 Implication of different cost techniques to produce income statement.

Cost: This is amount of funding which is spent by an organization for the development and

manufacture of various goods as well services. This aspect supports in research real costs and

necessary to pay off to customers (Samuel, 2018).

Absorption costing: This costing strategy shows all of the manufacturing costs that are absorbed

by the manufactured units. This approach focuses on both fixed and variable costs in order to

organize different company activities.

Marginal costing: It is a costing strategy in which costs are paid to unit costs on fixed costs and

charged according to the duration by fully pay off towards expenditure.

Januar

y

Februar

y

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Fixed production overheads 22000 19000

Total cost 297000 256500

per unit cost 27 27

Income statement under absorption

costing

Januar

y

Februar

y

sales 315000 402500

Less: cost of sales 243000 310500

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Fixed production overheads 22000 19000

Closing stock 54000 0

Opening stock 0 54000

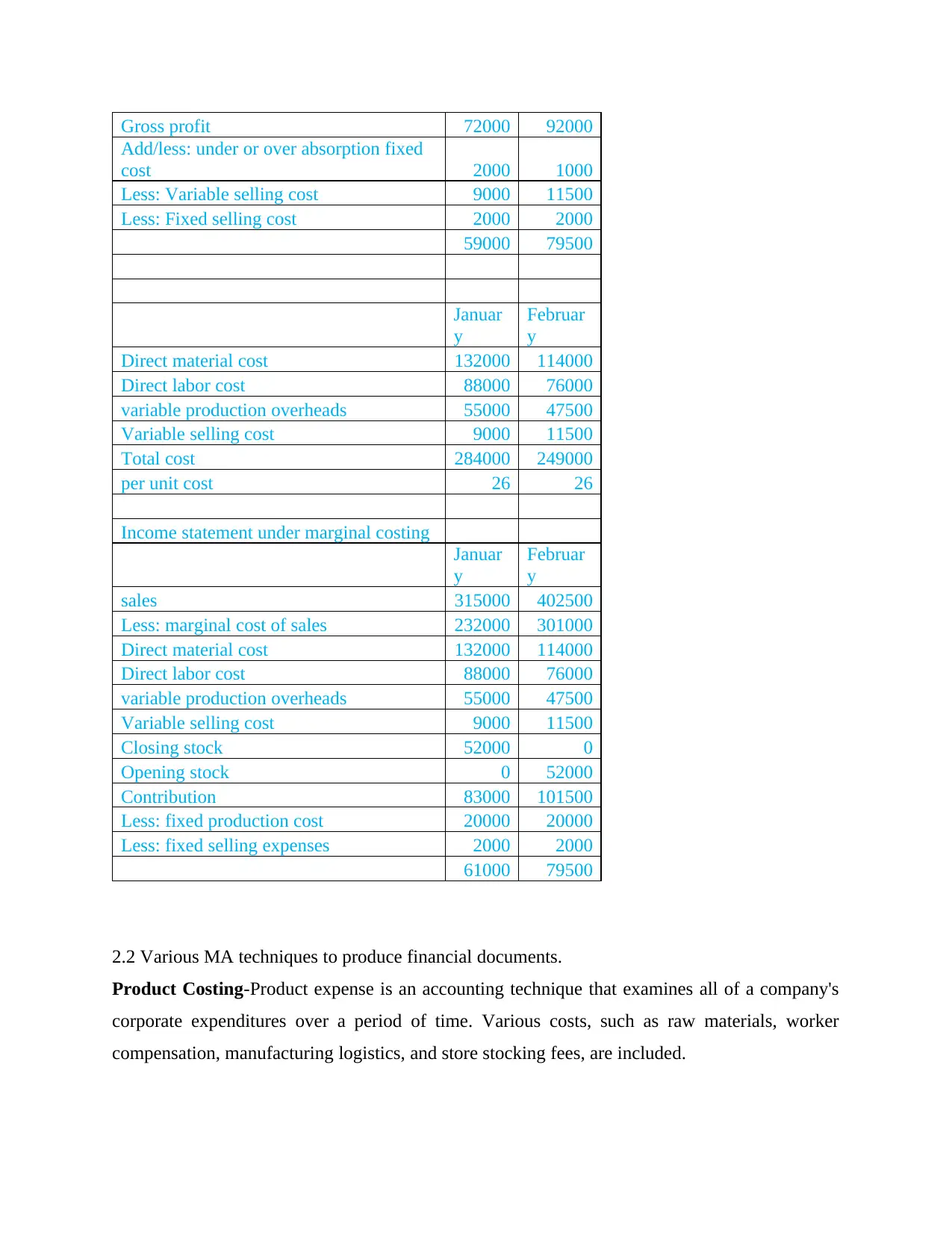

Gross profit 72000 92000

Add/less: under or over absorption fixed

cost 2000 1000

Less: Variable selling cost 9000 11500

Less: Fixed selling cost 2000 2000

59000 79500

Januar

y

Februar

y

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Variable selling cost 9000 11500

Total cost 284000 249000

per unit cost 26 26

Income statement under marginal costing

Januar

y

Februar

y

sales 315000 402500

Less: marginal cost of sales 232000 301000

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Variable selling cost 9000 11500

Closing stock 52000 0

Opening stock 0 52000

Contribution 83000 101500

Less: fixed production cost 20000 20000

Less: fixed selling expenses 2000 2000

61000 79500

2.2 Various MA techniques to produce financial documents.

Product Costing-Product expense is an accounting technique that examines all of a company's

corporate expenditures over a period of time. Various costs, such as raw materials, worker

compensation, manufacturing logistics, and store stocking fees, are included.

Add/less: under or over absorption fixed

cost 2000 1000

Less: Variable selling cost 9000 11500

Less: Fixed selling cost 2000 2000

59000 79500

Januar

y

Februar

y

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Variable selling cost 9000 11500

Total cost 284000 249000

per unit cost 26 26

Income statement under marginal costing

Januar

y

Februar

y

sales 315000 402500

Less: marginal cost of sales 232000 301000

Direct material cost 132000 114000

Direct labor cost 88000 76000

variable production overheads 55000 47500

Variable selling cost 9000 11500

Closing stock 52000 0

Opening stock 0 52000

Contribution 83000 101500

Less: fixed production cost 20000 20000

Less: fixed selling expenses 2000 2000

61000 79500

2.2 Various MA techniques to produce financial documents.

Product Costing-Product expense is an accounting technique that examines all of a company's

corporate expenditures over a period of time. Various costs, such as raw materials, worker

compensation, manufacturing logistics, and store stocking fees, are included.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed cost: It is mostly dependent on a specific time frame that does not alter as a result of

manufacturing activities.

Variable costs- This includes direct labour, taxation, and operational expenditures, which vary

directly and proportionally in response to changes in market activity level or volume.

Inventory costs: This expense is analysed by the management to determine how much stock can

be held, and the results differ depending on the customers. Various forms of stock levels are

listed, including:

• Ordering expense: In this cost comprise of salaries and associated corporation tax and also

incentives to guarantee about the labour cost in which company will assign inventory as per the

requirement.

• Holding expense: This costs related that involve to sufficient room to store that inventory

which again is included risk and also losses. The cost of room, money, and unsustainability is

calculated using this cost analysis.

• Administration expense: This cost refers to the salaries paid by the company to its workers, as

well as the price of products sold. It is advantageous to control such stock costs and deduct to red

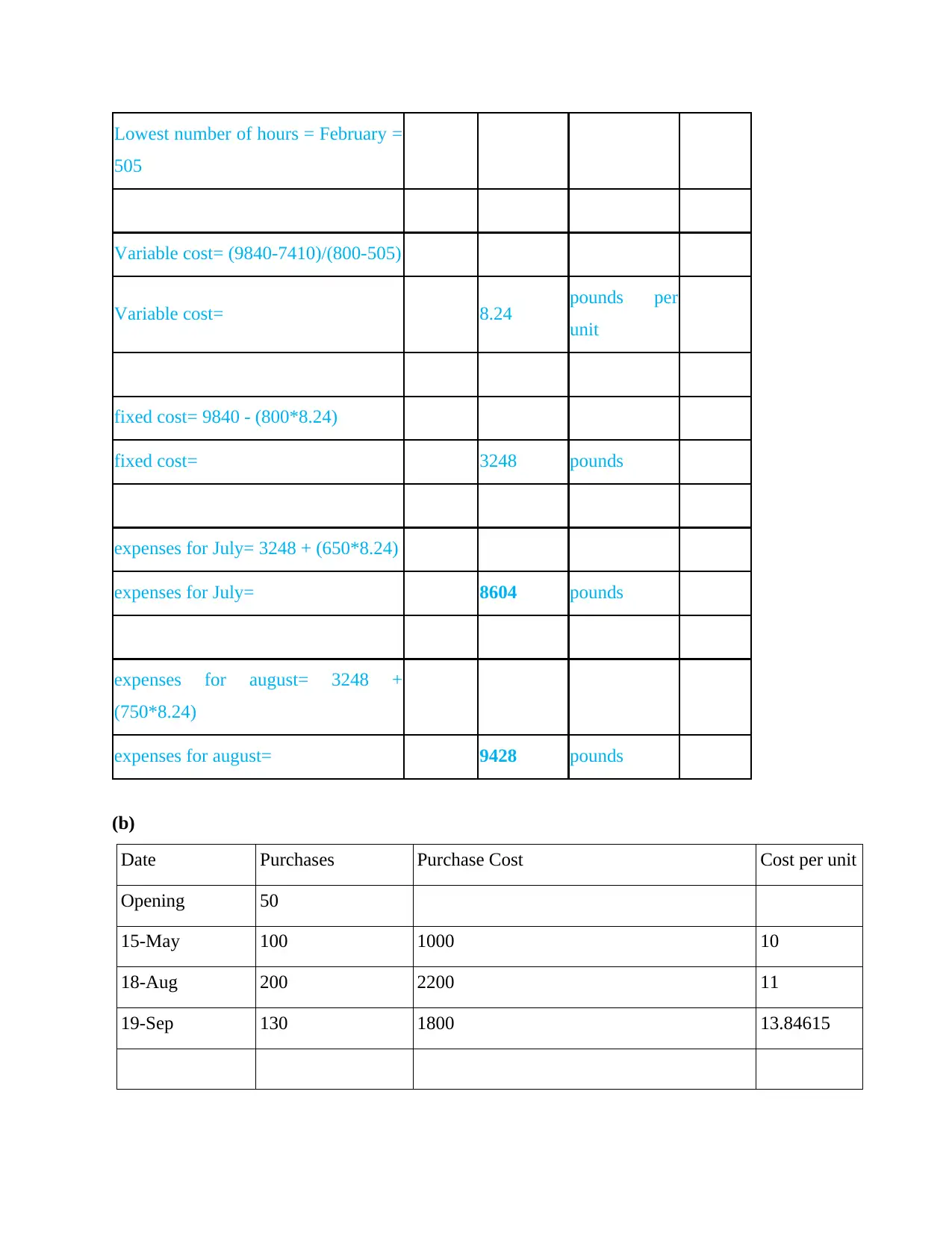

2.3 Preparation of financial reports and their interpretation:

(a)

Month Hours

Spent Expenses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours = June = 800

manufacturing activities.

Variable costs- This includes direct labour, taxation, and operational expenditures, which vary

directly and proportionally in response to changes in market activity level or volume.

Inventory costs: This expense is analysed by the management to determine how much stock can

be held, and the results differ depending on the customers. Various forms of stock levels are

listed, including:

• Ordering expense: In this cost comprise of salaries and associated corporation tax and also

incentives to guarantee about the labour cost in which company will assign inventory as per the

requirement.

• Holding expense: This costs related that involve to sufficient room to store that inventory

which again is included risk and also losses. The cost of room, money, and unsustainability is

calculated using this cost analysis.

• Administration expense: This cost refers to the salaries paid by the company to its workers, as

well as the price of products sold. It is advantageous to control such stock costs and deduct to red

2.3 Preparation of financial reports and their interpretation:

(a)

Month Hours

Spent Expenses

January 630 7960

February 505 7410

Mar 705 8285

April 555 7535

May 780 9110

June 795 9820

Highest number of hours = June = 800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Lowest number of hours = February =

505

Variable cost= (9840-7410)/(800-505)

Variable cost= 8.24 pounds per

unit

fixed cost= 9840 - (800*8.24)

fixed cost= 3248 pounds

expenses for July= 3248 + (650*8.24)

expenses for July= 8604 pounds

expenses for august= 3248 +

(750*8.24)

expenses for august= 9428 pounds

(b)

Date Purchases Purchase Cost Cost per unit

Opening 50

15-May 100 1000 10

18-Aug 200 2200 11

19-Sep 130 1800 13.84615

505

Variable cost= (9840-7410)/(800-505)

Variable cost= 8.24 pounds per

unit

fixed cost= 9840 - (800*8.24)

fixed cost= 3248 pounds

expenses for July= 3248 + (650*8.24)

expenses for July= 8604 pounds

expenses for august= 3248 +

(750*8.24)

expenses for august= 9428 pounds

(b)

Date Purchases Purchase Cost Cost per unit

Opening 50

15-May 100 1000 10

18-Aug 200 2200 11

19-Sep 130 1800 13.84615

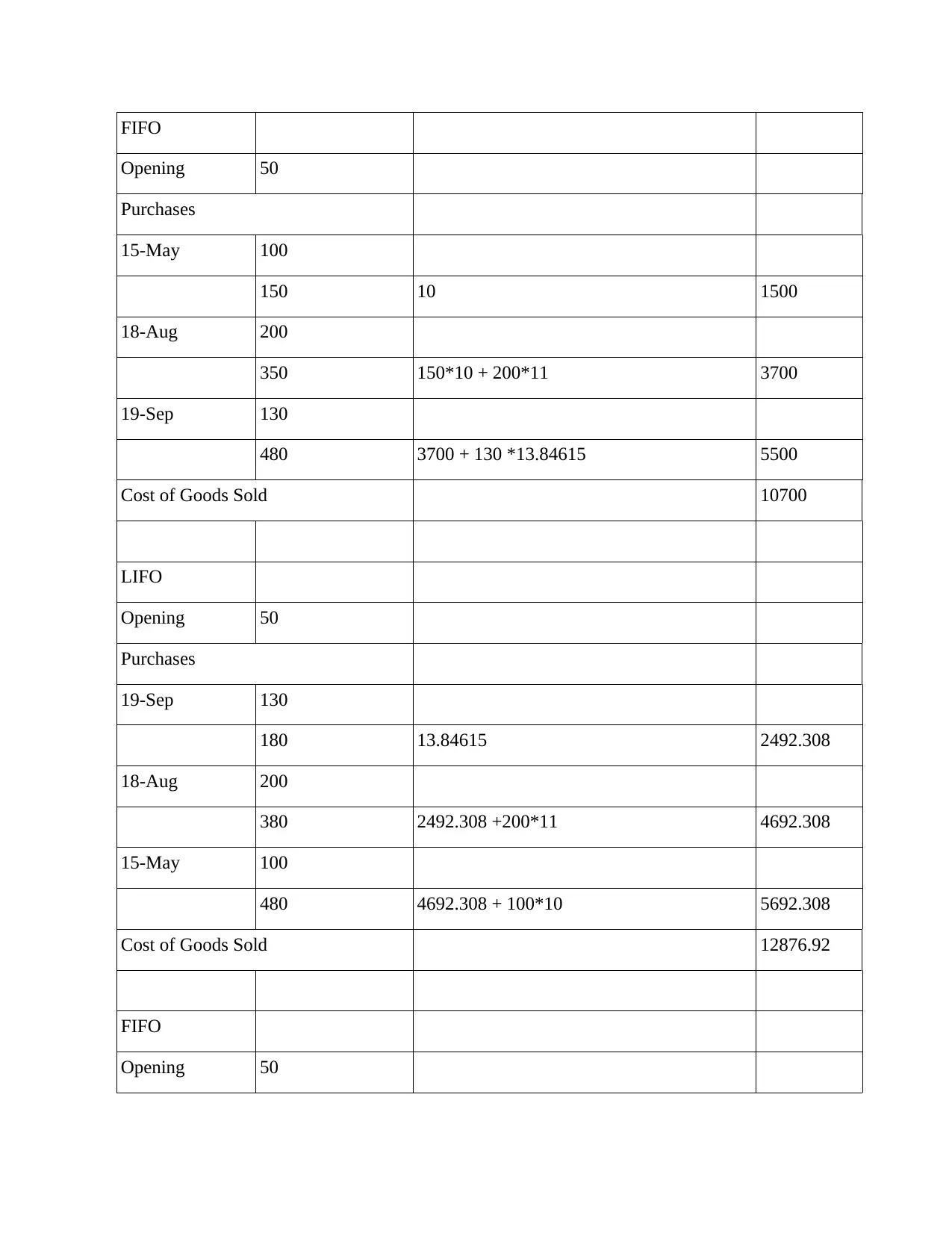

FIFO

Opening 50

Purchases

15-May 100

150 10 1500

18-Aug 200

350 150*10 + 200*11 3700

19-Sep 130

480 3700 + 130 *13.84615 5500

Cost of Goods Sold 10700

LIFO

Opening 50

Purchases

19-Sep 130

180 13.84615 2492.308

18-Aug 200

380 2492.308 +200*11 4692.308

15-May 100

480 4692.308 + 100*10 5692.308

Cost of Goods Sold 12876.92

FIFO

Opening 50

Opening 50

Purchases

15-May 100

150 10 1500

18-Aug 200

350 150*10 + 200*11 3700

19-Sep 130

480 3700 + 130 *13.84615 5500

Cost of Goods Sold 10700

LIFO

Opening 50

Purchases

19-Sep 130

180 13.84615 2492.308

18-Aug 200

380 2492.308 +200*11 4692.308

15-May 100

480 4692.308 + 100*10 5692.308

Cost of Goods Sold 12876.92

FIFO

Opening 50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.