Management Accounting System and Techniques: Ryder Architecture

VerifiedAdded on 2023/06/18

|19

|5317

|458

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and techniques as applied to Ryder Architecture, a UK-based construction company, through the lens of Equilibrium Asset Management, a financial consultancy. It explores various types of managerial accounting systems, including inventory management, cost accounting, job costing, and price optimization, detailing their benefits and integration within business processes. The report also examines several methods for management accounting reporting, such as budget reports, accounts receivable aging reports, cost accounting reports, inventory management reports, and performance reports. Furthermore, it delves into different costing techniques like direct and indirect costs, cost analysis, cost-volume-profit analysis, flexible budgeting, cost variance analysis, marginal and absorption costing, and cost allocation. The study highlights the advantages and disadvantages of various planning tools and their application in budget preparation and forecasting, along with the role of management accounting systems in responding to financial problems and maintaining sustainable success. The report concludes by emphasizing the importance of integrating management accounting systems and managerial accounting reporting to improve business operations and efficiency.

Management accounting

system & techniques

system & techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

TASK 1............................................................................................................................................3

P1.Managerial accounting and various types of MAS: .........................................................3

P2. Several methods utilised for management accounting reporting: .................................5

M1.Several benefits of management accounting system along with their application within an

organisation:...........................................................................................................................6

D1.Integration of different MAS and managerial accounting reporting within an entity's

business processes:.................................................................................................................6

TASK 2............................................................................................................................................7

P3 Calculation of cost using different costing techniques......................................................7

PART 2..........................................................................................................................................12

TASK 3..........................................................................................................................................12

P4. Advantages and disadvantages of different types of planning tools:.............................12

M3. Use of planning tools and applications in preparing and forecasting budgets:.............13

TASK 4..........................................................................................................................................13

P5. Adoption of management accounting system to respond financial problems:...............13

M4. Role of MAS in responding several financial problems and maintain sustainable success:

..............................................................................................................................................15

D3. Planing tools used in solving financial issues:..............................................................15

CONCLUSION..............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

TASK 1............................................................................................................................................3

P1.Managerial accounting and various types of MAS: .........................................................3

P2. Several methods utilised for management accounting reporting: .................................5

M1.Several benefits of management accounting system along with their application within an

organisation:...........................................................................................................................6

D1.Integration of different MAS and managerial accounting reporting within an entity's

business processes:.................................................................................................................6

TASK 2............................................................................................................................................7

P3 Calculation of cost using different costing techniques......................................................7

PART 2..........................................................................................................................................12

TASK 3..........................................................................................................................................12

P4. Advantages and disadvantages of different types of planning tools:.............................12

M3. Use of planning tools and applications in preparing and forecasting budgets:.............13

TASK 4..........................................................................................................................................13

P5. Adoption of management accounting system to respond financial problems:...............13

M4. Role of MAS in responding several financial problems and maintain sustainable success:

..............................................................................................................................................15

D3. Planing tools used in solving financial issues:..............................................................15

CONCLUSION..............................................................................................................................15

REFERENCES................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is defined as the system which is associated with representation

of financial information so that day to day operations of organisation can be executed in most

effective manner. In this manner internal working of the business can be improved and various

internal obligations can be completed (Akpanabia and Ekwutosi, 2021) . Management

accounting system is associated with planning various operational activities for future business

aspects. Managerial accounting is recommended with gaining valuable data so that in broad

sense day to day activities can be executed in most effective manner. In order to get appropriate

knowledge regarding management accounting a medium-sized financial consultancy named

Equilibrium Asset Management is taken which is having various clients such as Ryder

Architecture. Ryder Architecture company is taken which is construction company situated in

UK. This report is providing various types of managerial accounting system and methods those

can be used by the organisation in order to understand purpose of reporting and other constraints.

There are various tools which are being used by an organisation in order to render significant

planning and to provide controlling measures as well. In this manner with the help of significant

tools of management accounting system financial issues can also be resolved by the organisation.

PART 1

TASK 1

P1.Managerial accounting and various types of MAS:

Management accounting: Management accounting system is associated with accounting

entries and the same are being used by business managers in order to execute the process of

decision making and to control various functions including business performance. The major

objective of management accounting is to maximise profits and minimise overall losses so that

various inconsistencies within financial records can be predicted and at the same time important

decisions can also be taken. Using various methods and concepts effective planning can be made

and consistent decisions can be taken.

Management accounting system: This is defined as an integral system which is

implemented within business processes so that to understand business operations and to shape

future as well (Alabdullah and Ahmed, 2020). Within management accounting system various

Management accounting is defined as the system which is associated with representation

of financial information so that day to day operations of organisation can be executed in most

effective manner. In this manner internal working of the business can be improved and various

internal obligations can be completed (Akpanabia and Ekwutosi, 2021) . Management

accounting system is associated with planning various operational activities for future business

aspects. Managerial accounting is recommended with gaining valuable data so that in broad

sense day to day activities can be executed in most effective manner. In order to get appropriate

knowledge regarding management accounting a medium-sized financial consultancy named

Equilibrium Asset Management is taken which is having various clients such as Ryder

Architecture. Ryder Architecture company is taken which is construction company situated in

UK. This report is providing various types of managerial accounting system and methods those

can be used by the organisation in order to understand purpose of reporting and other constraints.

There are various tools which are being used by an organisation in order to render significant

planning and to provide controlling measures as well. In this manner with the help of significant

tools of management accounting system financial issues can also be resolved by the organisation.

PART 1

TASK 1

P1.Managerial accounting and various types of MAS:

Management accounting: Management accounting system is associated with accounting

entries and the same are being used by business managers in order to execute the process of

decision making and to control various functions including business performance. The major

objective of management accounting is to maximise profits and minimise overall losses so that

various inconsistencies within financial records can be predicted and at the same time important

decisions can also be taken. Using various methods and concepts effective planning can be made

and consistent decisions can be taken.

Management accounting system: This is defined as an integral system which is

implemented within business processes so that to understand business operations and to shape

future as well (Alabdullah and Ahmed, 2020). Within management accounting system various

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

tools and options are used so that to align with such functions and business objectives as well.

Some of these managerial accounting system as under:

Inventory management system: Inventory management is majorly used by manufacturing

businesses so that to manage their inventory in most effective manner. This system is

used by Equilibrium Asset Management for their clients such as Ryder Architecture so

that to keep record of various goods and inventory so that purpose of goods preparation.

There are three types of inventory management system such as LIFO, FIFO and AVCO.

For Ryder Architecture FIFO is used by the organisation within building manufacturing

process (Alzoubi, 2018). This system is associated with keeping detailed information

regarding stock and its availability. With the help of appropriate inventory management

system information related to stock can be added so that in smooth manner business

operations can be executed. This may also be helpful for managers to maintain level of

inventory as accordance with requirement and needs.

Cost accounting system: This system of accounting could be helpful for managers so that

to analyse differential activities within manufacturing. This is utilised by Equilibrium

Asset Management for their client Ryder Architecture so that to gain various detailed

information related to expenses which are directly in linkage with building construction

and other aspects. For business this is significant to have track record of direct and

indirect expenses within functions so that value can be added to the enterprise and at the

same time differential information can be gathered.

Job costing system: This is the system which is used in order to assign and accumulate

cost for each unit of manufactured goods. With the help of this system Equilibrium Asset

Management provide assistance to their client in relation to examine cost of each

manufactured building. This is significant for the business to analyse cost for every

different item which is used by them in their final products so that to add value for the

organisation and to determine cost for every building constructed by them.

Price optimisation system: This is defined as the system which is used in order to set

prices for the products used within organisation (Ameen and et. al., 2018). This tool is

used by Equilibrium Asset Management for their client Ryder Architecture so that to

provide assistance to manager for setting of prices. This is essential for the company to

set out prices and to meet expectation of their customers as well.

Some of these managerial accounting system as under:

Inventory management system: Inventory management is majorly used by manufacturing

businesses so that to manage their inventory in most effective manner. This system is

used by Equilibrium Asset Management for their clients such as Ryder Architecture so

that to keep record of various goods and inventory so that purpose of goods preparation.

There are three types of inventory management system such as LIFO, FIFO and AVCO.

For Ryder Architecture FIFO is used by the organisation within building manufacturing

process (Alzoubi, 2018). This system is associated with keeping detailed information

regarding stock and its availability. With the help of appropriate inventory management

system information related to stock can be added so that in smooth manner business

operations can be executed. This may also be helpful for managers to maintain level of

inventory as accordance with requirement and needs.

Cost accounting system: This system of accounting could be helpful for managers so that

to analyse differential activities within manufacturing. This is utilised by Equilibrium

Asset Management for their client Ryder Architecture so that to gain various detailed

information related to expenses which are directly in linkage with building construction

and other aspects. For business this is significant to have track record of direct and

indirect expenses within functions so that value can be added to the enterprise and at the

same time differential information can be gathered.

Job costing system: This is the system which is used in order to assign and accumulate

cost for each unit of manufactured goods. With the help of this system Equilibrium Asset

Management provide assistance to their client in relation to examine cost of each

manufactured building. This is significant for the business to analyse cost for every

different item which is used by them in their final products so that to add value for the

organisation and to determine cost for every building constructed by them.

Price optimisation system: This is defined as the system which is used in order to set

prices for the products used within organisation (Ameen and et. al., 2018). This tool is

used by Equilibrium Asset Management for their client Ryder Architecture so that to

provide assistance to manager for setting of prices. This is essential for the company to

set out prices and to meet expectation of their customers as well.

P2. Several methods utilised for management accounting reporting:

For an organisation in order to perform their daily activities management accounting

plays significant role and resultantly various information to staff. In this manner differential

system of accounting is being used which are defined as under:

Budget report: This is defined as the integral part of report which is being used by

the management in render to assess accurate information to their staff (Caperchione

and et. al., 2019). In other words with the help of this report actual and budgeted

results or information can be compared so that actual results can be ascertained using

estimated figures.

Account receivable ageing report: This type of report is associated with creation of

list of owned amount from various clients. In the context of Equilibrium Asset

Management this report is used by the organisation in order to track outstanding

amount due from clients of Ryder Architecture. This is beneficial for organisation so

that to examine overall amount of due amount by their customers so that various

credit policies can be made so that situation of late payment can be avoided.

Cost accounting report: This report is associated with manufacturing organisation so

that to assess differentiated costs and to execute business activities in appropriate

manner as well. This report is providing activities related to controlling of cost so

that activities related to cost reduction can be executed. In the context of Ryder

Architecture the organisation is preparing this report in order to find cost of their

each raw material.

Inventory management report: An organisation is associated with providing such

reports which are related with inventory. This report is providing the information

which is helpful in managing inventory in systematic manner. In the context of

Equilibrium Asset Management they are providing inventory management report for

their client such as Ryder Architecture so that to examine requirement of raw

material and their prices as well.

Performance report: Performance report is related to the provision of performance

within organisation (Crowther, 2018). Management staff of Ryder Architecture

prepares this report so that to examine overall efficiency and to gain their

For an organisation in order to perform their daily activities management accounting

plays significant role and resultantly various information to staff. In this manner differential

system of accounting is being used which are defined as under:

Budget report: This is defined as the integral part of report which is being used by

the management in render to assess accurate information to their staff (Caperchione

and et. al., 2019). In other words with the help of this report actual and budgeted

results or information can be compared so that actual results can be ascertained using

estimated figures.

Account receivable ageing report: This type of report is associated with creation of

list of owned amount from various clients. In the context of Equilibrium Asset

Management this report is used by the organisation in order to track outstanding

amount due from clients of Ryder Architecture. This is beneficial for organisation so

that to examine overall amount of due amount by their customers so that various

credit policies can be made so that situation of late payment can be avoided.

Cost accounting report: This report is associated with manufacturing organisation so

that to assess differentiated costs and to execute business activities in appropriate

manner as well. This report is providing activities related to controlling of cost so

that activities related to cost reduction can be executed. In the context of Ryder

Architecture the organisation is preparing this report in order to find cost of their

each raw material.

Inventory management report: An organisation is associated with providing such

reports which are related with inventory. This report is providing the information

which is helpful in managing inventory in systematic manner. In the context of

Equilibrium Asset Management they are providing inventory management report for

their client such as Ryder Architecture so that to examine requirement of raw

material and their prices as well.

Performance report: Performance report is related to the provision of performance

within organisation (Crowther, 2018). Management staff of Ryder Architecture

prepares this report so that to examine overall efficiency and to gain their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

contribution. With the help of this report major contribution is received by

supervisors as in context of gaining controlling measures within business activities.

M1.Several benefits of management accounting system along with their application within an

organisation:

Management accounting system Benefit

Cost accounting system This system is used within Ryder Architecture so that to

get assistance as in terms of executing business

operations in effective manner.

Inventory management system This is used within Ryder Architecture so that to keep

track record of inventory within business.

Price optimisation system For Ryder Architecture this system can be used in order

to set prices and to meet expectations of their clients.

Job costing system This system helps management of Ryder Architecture in

order to analyse cost for different activities and to

perform various activities as accordance with client

specifications.

D1.Integration of different MAS and managerial accounting reporting within an entity's business

processes:

The entire management accounting systems are associated with improvising business

operations along with gaining greater efficiency as well. This is clear that integration of various

management accounting systems and managerial accounting may lead into gaining efficiency in

business processes (Ferdous, Adams and Boyce, 2019). In the context of Ryder Architecture

inventory management system is being used so that to obtain information related with inventory

and other related operations. Another example for Ryder Architecture is that the company is

using integrated cost accounting system in their production processes which could be helpful in

examining accurate cost of production. Using of integrated managerial accounting system of

reporting can be helpful in executing business functions. With the help of integration of

inventory management system with business operations this will lead to gain effective utilisation

supervisors as in context of gaining controlling measures within business activities.

M1.Several benefits of management accounting system along with their application within an

organisation:

Management accounting system Benefit

Cost accounting system This system is used within Ryder Architecture so that to

get assistance as in terms of executing business

operations in effective manner.

Inventory management system This is used within Ryder Architecture so that to keep

track record of inventory within business.

Price optimisation system For Ryder Architecture this system can be used in order

to set prices and to meet expectations of their clients.

Job costing system This system helps management of Ryder Architecture in

order to analyse cost for different activities and to

perform various activities as accordance with client

specifications.

D1.Integration of different MAS and managerial accounting reporting within an entity's business

processes:

The entire management accounting systems are associated with improvising business

operations along with gaining greater efficiency as well. This is clear that integration of various

management accounting systems and managerial accounting may lead into gaining efficiency in

business processes (Ferdous, Adams and Boyce, 2019). In the context of Ryder Architecture

inventory management system is being used so that to obtain information related with inventory

and other related operations. Another example for Ryder Architecture is that the company is

using integrated cost accounting system in their production processes which could be helpful in

examining accurate cost of production. Using of integrated managerial accounting system of

reporting can be helpful in executing business functions. With the help of integration of

inventory management system with business operations this will lead to gain effective utilisation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of resources. Thus it can be said that management accounting system and managerial accounting

reporting are helpful in appropriate integration of organisational processes.

TASK 2

P3 Calculation of cost using different costing techniques

Cost: This is defined as the total sum which is paid by buyer to seller in lieu of their

product. For the purpose of attracting number of customers Ryder Architecture is required to set

such an appropriate structure of cost so that to construct their building. There are different types

of costs which are being used within business activities which are elaborated as under:

Direct cost: This type of cost is directly implicated to main product which is building in

the context of Ryder Architecture. Example for this expanse is depreciation, salaries etc.

Indirect cost: These types of expenses are not directly implicated on the final products

or on construction unit in context of Ryder Architecture. For example rent, utilities,

telephone expenses etc.

Cost analysis:This is defined as the process which is used in order to examine benefits

for differential activities and to execute various functions. This analysis is used within business

functions for the purpose of decision making and to attain long term business objectives.

Cost volume profit: This is defined as the method which is utilised by managers of

Ryder Architecture so that to analyse change in profit by change in volume of sales.

Flexible budgeting: This is defined as the method in which budget is formulated as

accordance with change of activity level (Fuzi and et. al., 2019). This budgeting method is used

within Ryder Architecture this is helping the company to analysing profit for every increasing

cost.

Cost variance: This is defined as the tool which can be used by Ryder Architecture in

order to examine difference between actual and budgeted cost. This is used by the organisation in

order to frame strategic decision.

Marginal costing: In costing method per unit cost remains the same and fixed and

variable cost are regarded as the two major types. The issue of over and under absorption can be

sorted so that the same can be used in fixation of prices, profit and other aspects such as BEP.

Absorption costing: This method is used in order to prepare financial records and with

the help of this method Ryder Architecture may get clear view of gross profit and net profit.

reporting are helpful in appropriate integration of organisational processes.

TASK 2

P3 Calculation of cost using different costing techniques

Cost: This is defined as the total sum which is paid by buyer to seller in lieu of their

product. For the purpose of attracting number of customers Ryder Architecture is required to set

such an appropriate structure of cost so that to construct their building. There are different types

of costs which are being used within business activities which are elaborated as under:

Direct cost: This type of cost is directly implicated to main product which is building in

the context of Ryder Architecture. Example for this expanse is depreciation, salaries etc.

Indirect cost: These types of expenses are not directly implicated on the final products

or on construction unit in context of Ryder Architecture. For example rent, utilities,

telephone expenses etc.

Cost analysis:This is defined as the process which is used in order to examine benefits

for differential activities and to execute various functions. This analysis is used within business

functions for the purpose of decision making and to attain long term business objectives.

Cost volume profit: This is defined as the method which is utilised by managers of

Ryder Architecture so that to analyse change in profit by change in volume of sales.

Flexible budgeting: This is defined as the method in which budget is formulated as

accordance with change of activity level (Fuzi and et. al., 2019). This budgeting method is used

within Ryder Architecture this is helping the company to analysing profit for every increasing

cost.

Cost variance: This is defined as the tool which can be used by Ryder Architecture in

order to examine difference between actual and budgeted cost. This is used by the organisation in

order to frame strategic decision.

Marginal costing: In costing method per unit cost remains the same and fixed and

variable cost are regarded as the two major types. The issue of over and under absorption can be

sorted so that the same can be used in fixation of prices, profit and other aspects such as BEP.

Absorption costing: This method is used in order to prepare financial records and with

the help of this method Ryder Architecture may get clear view of gross profit and net profit.

Fixed cost: This type of costs are constant irrespective of level of production or other

constraints. Example of such costs are tax, interest and rent.

Variable cost: This cost is having characteristics of increasing and decreasing as

accordance with level of production or number of constructed building in terms of Ryder

Architecture. Example for this type of cost is wages, material etc.

Cost allocation: This is defined as the procedure which is associated with identification,

aggregation and other activities (Hariyati, Tjahjadi and Soewarno, 2019). In the context of Ryder

Architecture this method is used so that to allocate cost within different functional areas.

Standard costing: In this type of costing method variance is calculated within actual and

standard cost. In giant organisation this is difficult to gather funds for differential activities so for

this purpose standard cost is used in order to save time.

Normal costing: This method is assisting in order to analyse variance between standard

and actual overhead. This is also assisting the management to understand and maintain

performance for completion of project.

Activity based costing: This is defined as the method of costing that is used by Ryder

Architecture so that to assign cost for varied activities.

Role of costing in setting price: Costing is helpful in setting of prices so in the context

of Ryder Architecture using method of costing the organisation may get assistance in analysing

cost so that prices of constructed building can be set.

Inventory cost: The cost related with procurement, management and storage is

collectively called as inventory cost. There are differential types of cost which are seen within

Ryder Architecture such as:

Ordering cost: This cost is taking place at the time of placing order to suppliers by

Ryder Architecture.

Carrying cost: This is also known as holding cost which is incurred by Ryder

Architecture for holding overall material.

Shortage cost: In the context of Ryder Architecture they do not have any such stock

inventory cost to take place.

Benefits of reducing inventory cost:

With the help of reducing inventory profit can be maximised and in this manner

amount can be saved.

constraints. Example of such costs are tax, interest and rent.

Variable cost: This cost is having characteristics of increasing and decreasing as

accordance with level of production or number of constructed building in terms of Ryder

Architecture. Example for this type of cost is wages, material etc.

Cost allocation: This is defined as the procedure which is associated with identification,

aggregation and other activities (Hariyati, Tjahjadi and Soewarno, 2019). In the context of Ryder

Architecture this method is used so that to allocate cost within different functional areas.

Standard costing: In this type of costing method variance is calculated within actual and

standard cost. In giant organisation this is difficult to gather funds for differential activities so for

this purpose standard cost is used in order to save time.

Normal costing: This method is assisting in order to analyse variance between standard

and actual overhead. This is also assisting the management to understand and maintain

performance for completion of project.

Activity based costing: This is defined as the method of costing that is used by Ryder

Architecture so that to assign cost for varied activities.

Role of costing in setting price: Costing is helpful in setting of prices so in the context

of Ryder Architecture using method of costing the organisation may get assistance in analysing

cost so that prices of constructed building can be set.

Inventory cost: The cost related with procurement, management and storage is

collectively called as inventory cost. There are differential types of cost which are seen within

Ryder Architecture such as:

Ordering cost: This cost is taking place at the time of placing order to suppliers by

Ryder Architecture.

Carrying cost: This is also known as holding cost which is incurred by Ryder

Architecture for holding overall material.

Shortage cost: In the context of Ryder Architecture they do not have any such stock

inventory cost to take place.

Benefits of reducing inventory cost:

With the help of reducing inventory profit can be maximised and in this manner

amount can be saved.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

With the help of minimised inventory cost competitive advantage can be attained

and in this manner large customers can be attracted.

Cost variances: In the process of determining budget cost of inventory different types of

variances are used. These are named as cost, price, usage and many more (Johnsson, Normann

and Svensson, 2020). With the help of this Ryder Architecture can analyse difference between

actual and standard price.

Overhead costs: All the type of expenses which are being faced by Ryder Architecture

during construction of their building are known as overheads.

and in this manner large customers can be attracted.

Cost variances: In the process of determining budget cost of inventory different types of

variances are used. These are named as cost, price, usage and many more (Johnsson, Normann

and Svensson, 2020). With the help of this Ryder Architecture can analyse difference between

actual and standard price.

Overhead costs: All the type of expenses which are being faced by Ryder Architecture

during construction of their building are known as overheads.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

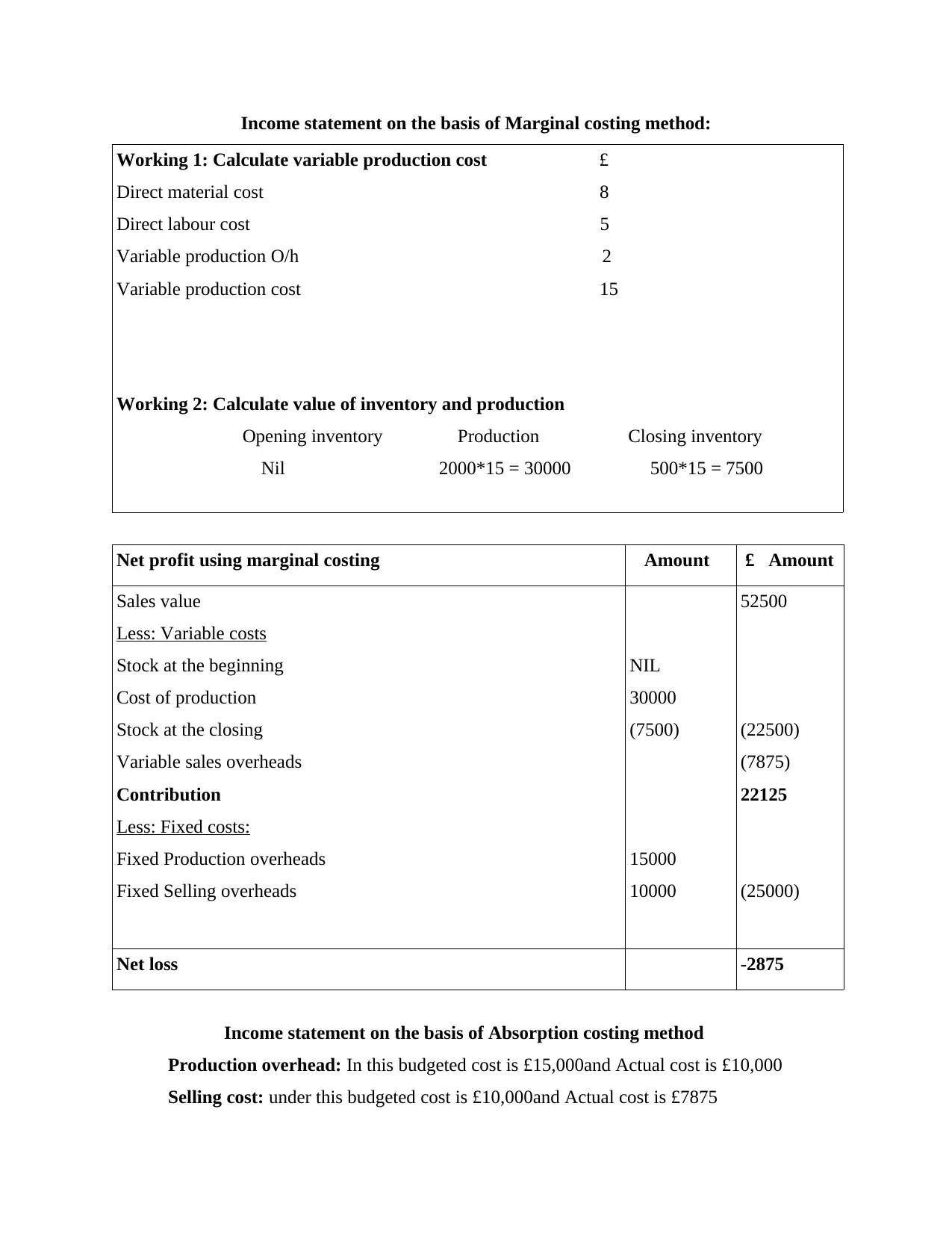

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the beginning

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the beginning

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.