Management Accounting: Evaluating Systems, Reporting & Techniques

VerifiedAdded on 2024/05/16

|24

|4944

|498

Report

AI Summary

This report provides a comprehensive overview of management accounting, emphasizing the importance of management accounting systems within organizations. It explores various management accounting reporting methods and their benefits, alongside an analysis of different costing techniques such as marginal and absorption costing, and their impact on financial reporting. The assignment evaluates the integration of management accounting systems and reporting within organizational processes, highlighting the role of planning tools and budgetary control in achieving sustainable success. Furthermore, it discusses the effectiveness of these tools in budget preparation and the significance of corporate governance in preventing financial problems, demonstrating how a robust management accounting system contributes to overall organizational success. The document includes practical examples and financial statement preparations using different costing methods.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction....................................................................................................................................3

Task 1..............................................................................................................................................4

P1.................................................................................................................................................4

P2.................................................................................................................................................6

M1................................................................................................................................................7

D1................................................................................................................................................8

P3.................................................................................................................................................9

M2..............................................................................................................................................12

D2..............................................................................................................................................13

P4...............................................................................................................................................14

M3..............................................................................................................................................15

P5...............................................................................................................................................17

M4..............................................................................................................................................17

D3..............................................................................................................................................19

Conclusion....................................................................................................................................20

References.....................................................................................................................................21

2

Introduction....................................................................................................................................3

Task 1..............................................................................................................................................4

P1.................................................................................................................................................4

P2.................................................................................................................................................6

M1................................................................................................................................................7

D1................................................................................................................................................8

P3.................................................................................................................................................9

M2..............................................................................................................................................12

D2..............................................................................................................................................13

P4...............................................................................................................................................14

M3..............................................................................................................................................15

P5...............................................................................................................................................17

M4..............................................................................................................................................17

D3..............................................................................................................................................19

Conclusion....................................................................................................................................20

References.....................................................................................................................................21

2

Introduction

The assignment includes the concept related to management accounting and importance of

management accounting system in the organization. There are various methods of management

accounting reporting are stated along with various reports formed in an organization. The

benefits of the management accounting system along with its integration with the management

accounting reporting is also stated. There is an analysis of various costing techniques and

analysis of the results achieved. The assignment also includes different types of planning tools of

budgetary control along with other methods than budgeting is also stated. The ways through

which management accounting system leads to organizational success by solving the problems

related to finance are also included. The planning tools importance in leading the company

towards sustainable success is also stated in the assignment along with their effectiveness while

preparing the budget. The report also consists of a brief about the corporate governance along

with its usefulness to prevent the problems related to finance.

3

The assignment includes the concept related to management accounting and importance of

management accounting system in the organization. There are various methods of management

accounting reporting are stated along with various reports formed in an organization. The

benefits of the management accounting system along with its integration with the management

accounting reporting is also stated. There is an analysis of various costing techniques and

analysis of the results achieved. The assignment also includes different types of planning tools of

budgetary control along with other methods than budgeting is also stated. The ways through

which management accounting system leads to organizational success by solving the problems

related to finance are also included. The planning tools importance in leading the company

towards sustainable success is also stated in the assignment along with their effectiveness while

preparing the budget. The report also consists of a brief about the corporate governance along

with its usefulness to prevent the problems related to finance.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

P1. Explain management accounting and give the essential requirements of different types

of management accounting systems.

According to Bodnar, et. al., (2012), Management accounting systems are systems which

records, analyze and interpret financial information and interpret financial information into

meaningful analysis. Management managers need to plan, organize, interpret and analyze

financial and non-financial information for relevant decision making and for setting futuristic

goals.

Management accounting subjectivity:

The major functions of management accounting systems are that it records data and interpret data

into meaningful information, the information or reporting so interpreted is highly useful for

communicating with each other managers, it records and controls account as well, it also

analyses both quantitative and qualitative information, it considers all kinds of information as

non-metric information are also highly useful for making relevant decision making (Chen, et. al.,

2012).

Various accounting systems:

Financial accounting systems: Financial accounting is the accounting branch which records and

analyzes all the financial transactions. Financial accounting systems are the integrated systems

which not only keep access to transactions and generate meaningful information.

The major purpose of financial accounting systems is that it is an accounting system and internal

control. In an organization, every specific year, a number of accounting transactions takes place

which has to recognize and reconciling financial figures, therefore, this system is mainly an

accounting system and is used for internal control purpose. It is also useful for the purpose of

auditing. Auditing requires re-confirmation and re-checking of all financial transactions which is

easily done through cost accounting system (Chen, et. al., 2012).

Cost accounting systems: Cost accounting system provides detailed description making

products costing and describing the cost incurred for production of a single unit. There are

different types of costing systems such as process costing, job costing process, product costing

and activity-based costing. Activity-based costing is a system which makes costing in

accordance with the organization processes (Chen, et. al., 2012).

Management accounting systems: These systems are critically important for organizations for

the purpose of decision making, organizational support, and profitability management and for

investment management. An organization has to go through a large number of financial

transactions involving big project investments, products development and other decisions (Drury,

2013).

4

P1. Explain management accounting and give the essential requirements of different types

of management accounting systems.

According to Bodnar, et. al., (2012), Management accounting systems are systems which

records, analyze and interpret financial information and interpret financial information into

meaningful analysis. Management managers need to plan, organize, interpret and analyze

financial and non-financial information for relevant decision making and for setting futuristic

goals.

Management accounting subjectivity:

The major functions of management accounting systems are that it records data and interpret data

into meaningful information, the information or reporting so interpreted is highly useful for

communicating with each other managers, it records and controls account as well, it also

analyses both quantitative and qualitative information, it considers all kinds of information as

non-metric information are also highly useful for making relevant decision making (Chen, et. al.,

2012).

Various accounting systems:

Financial accounting systems: Financial accounting is the accounting branch which records and

analyzes all the financial transactions. Financial accounting systems are the integrated systems

which not only keep access to transactions and generate meaningful information.

The major purpose of financial accounting systems is that it is an accounting system and internal

control. In an organization, every specific year, a number of accounting transactions takes place

which has to recognize and reconciling financial figures, therefore, this system is mainly an

accounting system and is used for internal control purpose. It is also useful for the purpose of

auditing. Auditing requires re-confirmation and re-checking of all financial transactions which is

easily done through cost accounting system (Chen, et. al., 2012).

Cost accounting systems: Cost accounting system provides detailed description making

products costing and describing the cost incurred for production of a single unit. There are

different types of costing systems such as process costing, job costing process, product costing

and activity-based costing. Activity-based costing is a system which makes costing in

accordance with the organization processes (Chen, et. al., 2012).

Management accounting systems: These systems are critically important for organizations for

the purpose of decision making, organizational support, and profitability management and for

investment management. An organization has to go through a large number of financial

transactions involving big project investments, products development and other decisions (Drury,

2013).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax accounting: there are different types of an organisational structure such as sole proprietor,

partnership organization, companies etc. the different structures requires implementation of

different taxes such as GST, international taxation, double taxation etc. The major purpose is to

evaluate taxation figures for an organization (Drury, 2013).

5

partnership organization, companies etc. the different structures requires implementation of

different taxes such as GST, international taxation, double taxation etc. The major purpose is to

evaluate taxation figures for an organization (Drury, 2013).

5

P2. Explain different methods used for management accounting reporting?

Every organization prepares different accounting reporting such as trading and profit and loss

account, statement of financial position, cash flow, fund flow and cost of goods sold. The

different reporting is done to analyse financial expenditure and financial incomes (Drury, 2013).

Trading and profit and loss account: this account is prepared for measuring organization profits

by analysing the trading financial figures of sales and direct costing. The trading calculates the

gross profits by analysis direct expenses and the profit and loss account ascertains all the indirect

expenses and indirect incomes and calculates net profits (Drury, 2013).

Balance sheet: this statement presents the financial figures of assets and liabilities. This is

ascertained at a point of time which measures the value of assets like fixed assets, plant, and

machinery and also measures the value of liabilities like long-term debt, long-term liabilities etc.

(Drury, 2013).

Cash flow statement: This statement considers the inflows and outflows of cash during a

specific period. Since cash is a most important form of liquid asset and it is essential to evaluate

cash flows so as to reconcile with other accounting transactions (Parker, 2012).

Cost of goods sold: this statement describes the valuation of the cost of products by ascertaining

the direct cost incurred over the organization. The cost ascertained in this segment includes

opening inventory, direct material cost, direct labor cost, production overheads and the value of

closing inventory (Parker, 2012).

The various accounting systems are as follows:

Cost accounting system: A cost accounting system is one system which makes an analysis of

products costing. There are different types of costing system such as process costing, activity

based costing etc. For instance: segregation of product activities into series aids in making

costing.

Inventory management system: Inventory management system is one which keeps proper

planning and controlling of inventory and also analyse the costing of such products. There are a

number of inventory terms which have to be EOQ, inventory order level, inventory carrying cost

etc. For instance: the carrying cost per unit of a product A is an example of inventory

management system (Sánchez-Rodríguez, et. al., 2012).

Job costing system: This system makes costing for products in accordance with every batch.

The costing is done for every batch, though every batch might have identical products but the

costing values might differ and lead to different profitability and revenues and hence job costing

is useful for evaluating products value.

Price optimizing system: this system is useful for measuring pricing of products to be sold. All

the products which have to be sold require having a pricing. The pricing system requires a lot of

information and makes products pricing (Sánchez-Rodríguez, et. al., 2012).

6

Every organization prepares different accounting reporting such as trading and profit and loss

account, statement of financial position, cash flow, fund flow and cost of goods sold. The

different reporting is done to analyse financial expenditure and financial incomes (Drury, 2013).

Trading and profit and loss account: this account is prepared for measuring organization profits

by analysing the trading financial figures of sales and direct costing. The trading calculates the

gross profits by analysis direct expenses and the profit and loss account ascertains all the indirect

expenses and indirect incomes and calculates net profits (Drury, 2013).

Balance sheet: this statement presents the financial figures of assets and liabilities. This is

ascertained at a point of time which measures the value of assets like fixed assets, plant, and

machinery and also measures the value of liabilities like long-term debt, long-term liabilities etc.

(Drury, 2013).

Cash flow statement: This statement considers the inflows and outflows of cash during a

specific period. Since cash is a most important form of liquid asset and it is essential to evaluate

cash flows so as to reconcile with other accounting transactions (Parker, 2012).

Cost of goods sold: this statement describes the valuation of the cost of products by ascertaining

the direct cost incurred over the organization. The cost ascertained in this segment includes

opening inventory, direct material cost, direct labor cost, production overheads and the value of

closing inventory (Parker, 2012).

The various accounting systems are as follows:

Cost accounting system: A cost accounting system is one system which makes an analysis of

products costing. There are different types of costing system such as process costing, activity

based costing etc. For instance: segregation of product activities into series aids in making

costing.

Inventory management system: Inventory management system is one which keeps proper

planning and controlling of inventory and also analyse the costing of such products. There are a

number of inventory terms which have to be EOQ, inventory order level, inventory carrying cost

etc. For instance: the carrying cost per unit of a product A is an example of inventory

management system (Sánchez-Rodríguez, et. al., 2012).

Job costing system: This system makes costing for products in accordance with every batch.

The costing is done for every batch, though every batch might have identical products but the

costing values might differ and lead to different profitability and revenues and hence job costing

is useful for evaluating products value.

Price optimizing system: this system is useful for measuring pricing of products to be sold. All

the products which have to be sold require having a pricing. The pricing system requires a lot of

information and makes products pricing (Sánchez-Rodríguez, et. al., 2012).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M1. Evaluate the benefits of management accounting systems and their application within

an organisational context.

In an organizational context, MIS and DSS are two vital systems which require being assessing

and installing. Both the systems have their own pros and cons to be evaluated.

MIS i.e. management information system is an integrated software application which combines

the organizational processes. A manager has to input data into the MIS system and also need to

put into varied assumptions and futuristic goals for making analysing and interpreting result

(Teatime, 2013).

The major benefits of installing MIS are as follows:

• It is a major source for centralizing database and providing easy access to all. This is a

major source for easing facilities and more prompt communication among managers and

employees (Teittinen, 2013).

• It is also useful for other management accounting systems. Since it centralizes data at one

place, another department can easily use the data for making decisions.

• The most useful factor about it is that it helps in decision making. Organisations need to

formulate decisions regarding organization processes, inventory management,

manufacturing processes, project investment, capital projects etc. (Teittinen, 2013).

• DSS i.e. decision-making system is another application which mainly considered as

intelligence software as it is used by the higher authority for making relevant decisions

and comparing a different set of problems.

• It helps in solving complex managerial issues and problems which involves complex

decisions issues.

• DSS is a kind of artificial intelligence which is used for formulating decisions in complex

situations (Theriou, and Aggelidis, 2014).

• Though it is quite complex, proper installation of data must be done and thus, the proper

interpretation is made.

8

an organisational context.

In an organizational context, MIS and DSS are two vital systems which require being assessing

and installing. Both the systems have their own pros and cons to be evaluated.

MIS i.e. management information system is an integrated software application which combines

the organizational processes. A manager has to input data into the MIS system and also need to

put into varied assumptions and futuristic goals for making analysing and interpreting result

(Teatime, 2013).

The major benefits of installing MIS are as follows:

• It is a major source for centralizing database and providing easy access to all. This is a

major source for easing facilities and more prompt communication among managers and

employees (Teittinen, 2013).

• It is also useful for other management accounting systems. Since it centralizes data at one

place, another department can easily use the data for making decisions.

• The most useful factor about it is that it helps in decision making. Organisations need to

formulate decisions regarding organization processes, inventory management,

manufacturing processes, project investment, capital projects etc. (Teittinen, 2013).

• DSS i.e. decision-making system is another application which mainly considered as

intelligence software as it is used by the higher authority for making relevant decisions

and comparing a different set of problems.

• It helps in solving complex managerial issues and problems which involves complex

decisions issues.

• DSS is a kind of artificial intelligence which is used for formulating decisions in complex

situations (Theriou, and Aggelidis, 2014).

• Though it is quite complex, proper installation of data must be done and thus, the proper

interpretation is made.

8

D1. Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes.

DSS is a management system which contains integrated interface and aids highest authority in

decision making. This system is implemented at varying levels such as planning, management,

and operations. ESS system is highly used by executive managers for ascertaining solutions for

organizational issues faced by executives. It is mainly used for the operational level (Theriou,

and Aggelidis, 2014).

Thus, there is a high level of difference between both the systems and thus, organizations take up

benefits of both the systems. DSS helps in quite accurate and precise decision making and relax

the work of highest authority while ESS is a system which aids in operational data and making

organizational decisions.

There are different reporting’s which are generated through these systems which present

financial information such as incomes, expenses, valuation of assets and liabilities, gross profits,

cash flows, values of reserves etc. (Theriou, and Aggelidis, 2014).

This information must be accurate and relevant and must also adhere to the management

accounting characteristics such as relevancy, materiality, understand ability, timelines for

becoming useful information. The presentation also plays a key role in presenting financial

figures to all stakeholders such as shareholders, suppliers, creditors etc.

9

reporting is integrated within organisational processes.

DSS is a management system which contains integrated interface and aids highest authority in

decision making. This system is implemented at varying levels such as planning, management,

and operations. ESS system is highly used by executive managers for ascertaining solutions for

organizational issues faced by executives. It is mainly used for the operational level (Theriou,

and Aggelidis, 2014).

Thus, there is a high level of difference between both the systems and thus, organizations take up

benefits of both the systems. DSS helps in quite accurate and precise decision making and relax

the work of highest authority while ESS is a system which aids in operational data and making

organizational decisions.

There are different reporting’s which are generated through these systems which present

financial information such as incomes, expenses, valuation of assets and liabilities, gross profits,

cash flows, values of reserves etc. (Theriou, and Aggelidis, 2014).

This information must be accurate and relevant and must also adhere to the management

accounting characteristics such as relevancy, materiality, understand ability, timelines for

becoming useful information. The presentation also plays a key role in presenting financial

figures to all stakeholders such as shareholders, suppliers, creditors etc.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

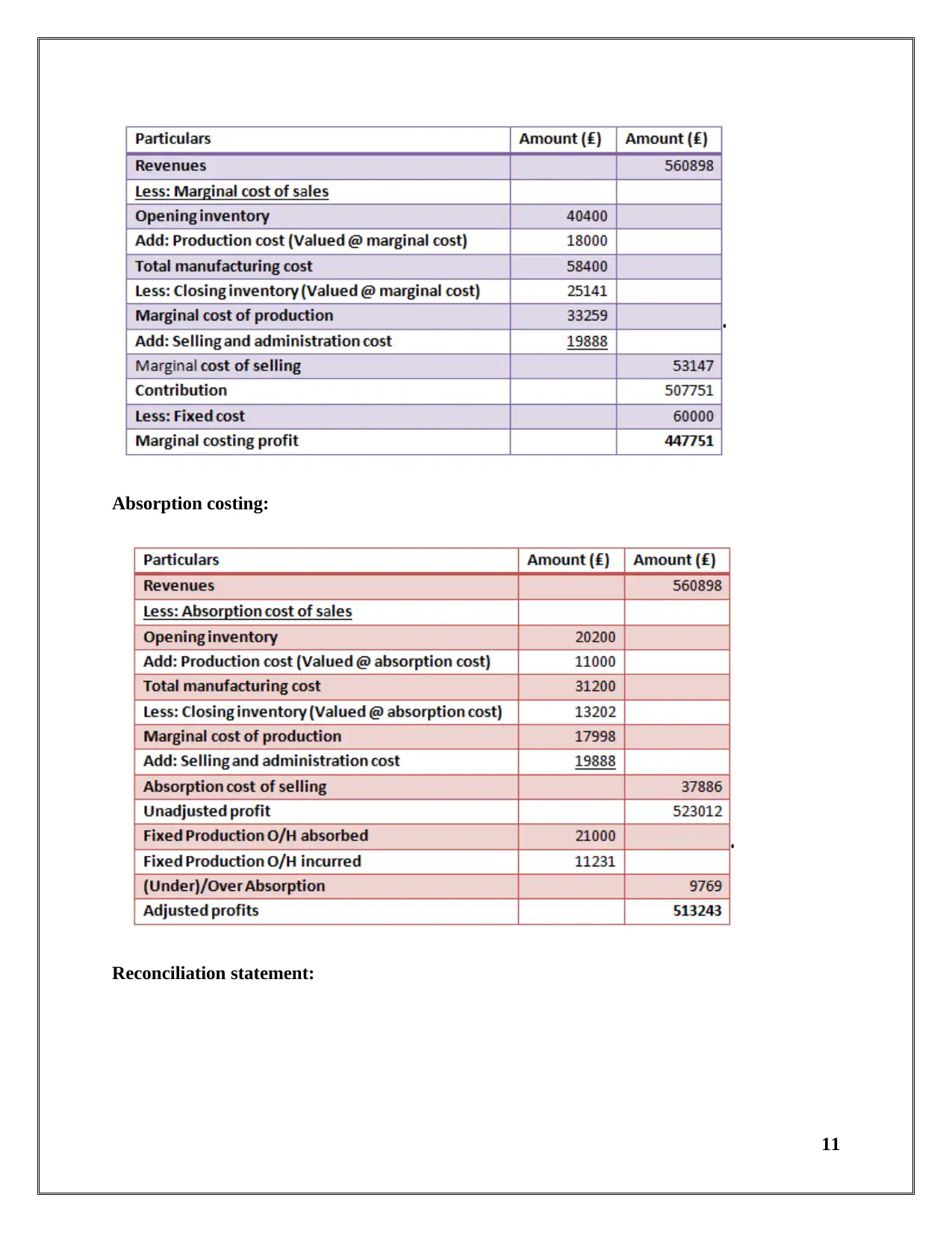

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing.

Cost refers to the expenditure made for manufacturing products and costs are classified into a

number of factors, direct cost, and indirect cost, product cost, process cost and flexible costing

etc.

Direct cost and indirect cost: Direct costs are the costs which are directly incurred over the

manufacturing products and indirect costs are the overall costs which do not have any direct

attribution to products. Direct costs are direct material, direct labor and indirect costs are

administrative cost, selling costing etc. (Warren, et. al., 2015).

Fixed and variable cost: Fixed costs are the costs which have to be incurred irrespective of

production capacity while variable costs are incurred in accordance with the production capacity.

Period cost: A period costs which are incurred and cannot be capitalized. The various examples

are pre-paid expenses, inventory expenses and fixed assets (Warren, et. al., 2015).

Product cost: Product costs are costs which directly attributes to the production of products.

Various product costs are direct labor cost, direct material costs, and factory overheads. Since

expenditures of these costs are essential for the production of products and hence, product costs

are maintained.

Marginal costing:

In this technique, per unit cost of products are analysed through considering variable cost and not

fixed costs and the valuation of the closing stock is valued at variable cost.

Absorption costing:

In this technique, products per unit costs are done by considering both variable and fixed cost. It

is based on absorbed cost concept (Warren, et. al., 2015).

Normal and standard costing: In normal costing, actual costs of products are ascertained and

these define the actual costs incurred for products. In standard costing, certain standards are set

for products which have to be met.

Activity-based costing: This is a costing technique in which activities involved in product

manufacturing are lined up and costing is done in accordance with the activities. The major

advantages of the technique are that it aids in improvising activities processing and improvising

distribution, selling and other activities. The disadvantage of the systems is data

misinterpretation, requires excessive time and efforts which further leads to delay (Warren, et.

al., 2015).

Marginal costing:

10

statement using marginal and absorption costing.

Cost refers to the expenditure made for manufacturing products and costs are classified into a

number of factors, direct cost, and indirect cost, product cost, process cost and flexible costing

etc.

Direct cost and indirect cost: Direct costs are the costs which are directly incurred over the

manufacturing products and indirect costs are the overall costs which do not have any direct

attribution to products. Direct costs are direct material, direct labor and indirect costs are

administrative cost, selling costing etc. (Warren, et. al., 2015).

Fixed and variable cost: Fixed costs are the costs which have to be incurred irrespective of

production capacity while variable costs are incurred in accordance with the production capacity.

Period cost: A period costs which are incurred and cannot be capitalized. The various examples

are pre-paid expenses, inventory expenses and fixed assets (Warren, et. al., 2015).

Product cost: Product costs are costs which directly attributes to the production of products.

Various product costs are direct labor cost, direct material costs, and factory overheads. Since

expenditures of these costs are essential for the production of products and hence, product costs

are maintained.

Marginal costing:

In this technique, per unit cost of products are analysed through considering variable cost and not

fixed costs and the valuation of the closing stock is valued at variable cost.

Absorption costing:

In this technique, products per unit costs are done by considering both variable and fixed cost. It

is based on absorbed cost concept (Warren, et. al., 2015).

Normal and standard costing: In normal costing, actual costs of products are ascertained and

these define the actual costs incurred for products. In standard costing, certain standards are set

for products which have to be met.

Activity-based costing: This is a costing technique in which activities involved in product

manufacturing are lined up and costing is done in accordance with the activities. The major

advantages of the technique are that it aids in improvising activities processing and improvising

distribution, selling and other activities. The disadvantage of the systems is data

misinterpretation, requires excessive time and efforts which further leads to delay (Warren, et.

al., 2015).

Marginal costing:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing:

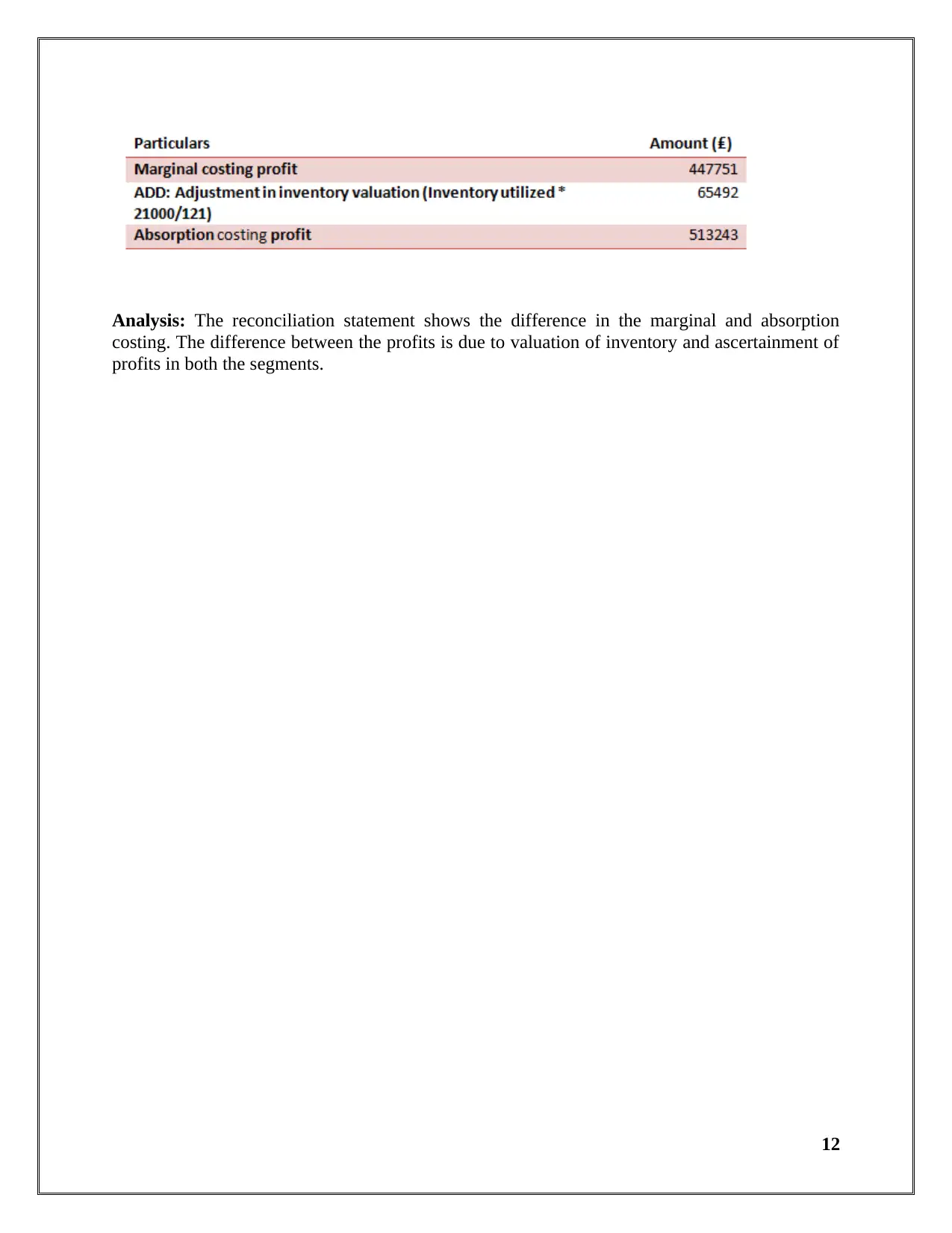

Reconciliation statement:

11

Reconciliation statement:

11

Analysis: The reconciliation statement shows the difference in the marginal and absorption

costing. The difference between the profits is due to valuation of inventory and ascertainment of

profits in both the segments.

12

costing. The difference between the profits is due to valuation of inventory and ascertainment of

profits in both the segments.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.