Management Accounting in Zylla Company: Costing and Planning

VerifiedAdded on 2024/05/20

|27

|5296

|202

Report

AI Summary

This report delves into management accounting principles within the context of Zylla Company, focusing on the replacement of their current system. It highlights the importance of management accounting, detailing its role in improving quality, reducing costs, and facilitating effective decision-making through techniques like ABC and target costing. The report covers costing reports, operational and cash reports, departmental-wise reports, and appraisal reports, emphasizing their significance in analyzing costs and operational performance. It also explores price optimization, job costing, inventory management, and cost accounting as key elements for financial sustainability. Furthermore, the document discusses marginal and absorption costing techniques, budgetary control, and their impact on organizational success. Desklib offers a platform for students to access similar solved assignments and past papers.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction..................................................................................................................................4

LO1..................................................................................................................................................5

P1................................................................................................................................................5

P2................................................................................................................................................6

M1................................................................................................................................................8

D1..............................................................................................................................................10

LO2................................................................................................................................................11

P3..............................................................................................................................................11

M2..............................................................................................................................................13

D2..............................................................................................................................................15

LO3................................................................................................................................................16

P4..............................................................................................................................................16

M3..............................................................................................................................................19

LO4................................................................................................................................................21

P5..............................................................................................................................................21

M4..............................................................................................................................................22

D3..............................................................................................................................................24

Conclusion..................................................................................................................................25

2

Introduction..................................................................................................................................4

LO1..................................................................................................................................................5

P1................................................................................................................................................5

P2................................................................................................................................................6

M1................................................................................................................................................8

D1..............................................................................................................................................10

LO2................................................................................................................................................11

P3..............................................................................................................................................11

M2..............................................................................................................................................13

D2..............................................................................................................................................15

LO3................................................................................................................................................16

P4..............................................................................................................................................16

M3..............................................................................................................................................19

LO4................................................................................................................................................21

P5..............................................................................................................................................21

M4..............................................................................................................................................22

D3..............................................................................................................................................24

Conclusion..................................................................................................................................25

2

References..................................................................................................................................26

Introduction

The assignment is based on the management accounting in the Zylla company which

wants to replace their system with the new one as per the requirement. There is a

description of it and the essential requirement of the same in an organization. The

methods of reporting are also stated along with the benefits of the management

accounting systems. There is the inclusion of the relation between the management

accounting system and reporting with respect to the organizational context. The various

techniques of cost such as marginal and absorption costing are also included along with

its practical applicability. The various types of planning tools related to budgetary control

and management accounting are there on the assignment along with there advantages

and disadvantages. The importance of management accounting in determining the

problems and responding to it for the attainment of the success is also stated. The

planning tools are important for the success of solving the financial problems is included

to better understand the benefits of them.

3

Introduction

The assignment is based on the management accounting in the Zylla company which

wants to replace their system with the new one as per the requirement. There is a

description of it and the essential requirement of the same in an organization. The

methods of reporting are also stated along with the benefits of the management

accounting systems. There is the inclusion of the relation between the management

accounting system and reporting with respect to the organizational context. The various

techniques of cost such as marginal and absorption costing are also included along with

its practical applicability. The various types of planning tools related to budgetary control

and management accounting are there on the assignment along with there advantages

and disadvantages. The importance of management accounting in determining the

problems and responding to it for the attainment of the success is also stated. The

planning tools are important for the success of solving the financial problems is included

to better understand the benefits of them.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO1

P1.

The accounting can be divided into three categories financial accounting, management

accounting and cost accounting. Management accounting can be defined as the

analysis of the information that is being recorded in the financial accounting and cost

accounting techniques (Carrer Ride, 2016). The management accounting is the reason

for the shortcomings of the financial accounting as the financial accounting consists of

all the financial transaction only but in the diverse market, there are various other

factors that are surrounding the organization that needs to be analyzed for growth and

sustainable success.

The importance of the management accounting is as follows:-

Improve Quality and reduce cost – The market in this new era of technology and

modernization is very volatile and is very difficult to survive with proper earning. The

methods and techniques that are used in the management accounting are useful in

improving the quality of the company and reduce the cost providing an advantage over

the other competitors (Ghanbari, and Vaseli, 2015). The organizations are looking

forward to adopting these new methods to have effective management of the resources

that are available to have better efficiency and productivity.

Decision Making – The decision making is an important task which puts a lot of

pressure on the managers due to the diverse and complex condition that is prevailing.

The management accounting tools such as the ABC, ABM, Target costing, ERP, Six

Sigma etc. have facilitated the managers to forecast the various factors and also look at

the internal performance of the coming resulting in effective decision making (Ghanbari,

and Vaseli, 2015). The range of techniques helps in making continuous improvement in

the process and improvements in the financial positions of the company. The decision

making is made effective with the right decisions that are being taken by the

management with the help of analysis.

4

P1.

The accounting can be divided into three categories financial accounting, management

accounting and cost accounting. Management accounting can be defined as the

analysis of the information that is being recorded in the financial accounting and cost

accounting techniques (Carrer Ride, 2016). The management accounting is the reason

for the shortcomings of the financial accounting as the financial accounting consists of

all the financial transaction only but in the diverse market, there are various other

factors that are surrounding the organization that needs to be analyzed for growth and

sustainable success.

The importance of the management accounting is as follows:-

Improve Quality and reduce cost – The market in this new era of technology and

modernization is very volatile and is very difficult to survive with proper earning. The

methods and techniques that are used in the management accounting are useful in

improving the quality of the company and reduce the cost providing an advantage over

the other competitors (Ghanbari, and Vaseli, 2015). The organizations are looking

forward to adopting these new methods to have effective management of the resources

that are available to have better efficiency and productivity.

Decision Making – The decision making is an important task which puts a lot of

pressure on the managers due to the diverse and complex condition that is prevailing.

The management accounting tools such as the ABC, ABM, Target costing, ERP, Six

Sigma etc. have facilitated the managers to forecast the various factors and also look at

the internal performance of the coming resulting in effective decision making (Ghanbari,

and Vaseli, 2015). The range of techniques helps in making continuous improvement in

the process and improvements in the financial positions of the company. The decision

making is made effective with the right decisions that are being taken by the

management with the help of analysis.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2.

Costing Reports – The costing reports components are the price and quantity or the

volume. The reports that are included in the costing reports are Sales variance reports,

Material cost variances, labor cost variance and Overhead Variances. The Costing

reports have 4 steps for the preparation of the reports which are as follows:-

The costing reports is an effective tool to analyze the cost involved so that

improvements can be made in case of there is unfavorable results to increase the

profitability and efficiency.

Operational and cash reports – The operational reports are prepared for the day to

day activities such as the marketing, Production, selling as well as the cash budget. The

reports are prepared on the basis of the long-term goals and preparation of the plans.

The operation reports are useful to determine the reasons for the deviation in the results

that are being achieved by the organization. To achieve the long-term goals it is

important to break it down in short objectives and try to achieve them in an effective

way.

5

Setting of

standards

Comparison

with actual

Reporting

of Variance

Corrective

actions

Costing Reports – The costing reports components are the price and quantity or the

volume. The reports that are included in the costing reports are Sales variance reports,

Material cost variances, labor cost variance and Overhead Variances. The Costing

reports have 4 steps for the preparation of the reports which are as follows:-

The costing reports is an effective tool to analyze the cost involved so that

improvements can be made in case of there is unfavorable results to increase the

profitability and efficiency.

Operational and cash reports – The operational reports are prepared for the day to

day activities such as the marketing, Production, selling as well as the cash budget. The

reports are prepared on the basis of the long-term goals and preparation of the plans.

The operation reports are useful to determine the reasons for the deviation in the results

that are being achieved by the organization. To achieve the long-term goals it is

important to break it down in short objectives and try to achieve them in an effective

way.

5

Setting of

standards

Comparison

with actual

Reporting

of Variance

Corrective

actions

Departmental wise reports - The departmental wise reports are prepared by the

center managers of the organization on the basis of their respective departments such

as the Revenue earned, the cost incurred, as well as the investments that are being

made by the company. The methods include determining the returns that every

department has earned such as return on investment.

Appraisal Reports – It is important to check the feasibility of the investment project that

is being considered which can be understood with the help of the Investment appraisal

reports. There are various techniques that can be used for understanding the viability

such as the Payback, Net Present Value (NPV), Accounting rate of return (ARR),

Internal Rate of return (IRR) etc. making the decision making regarding the project

effective and beneficial for the organization.

(Figure - Project Appraisal Method)

(Source - Jinali, 2014)

6

center managers of the organization on the basis of their respective departments such

as the Revenue earned, the cost incurred, as well as the investments that are being

made by the company. The methods include determining the returns that every

department has earned such as return on investment.

Appraisal Reports – It is important to check the feasibility of the investment project that

is being considered which can be understood with the help of the Investment appraisal

reports. There are various techniques that can be used for understanding the viability

such as the Payback, Net Present Value (NPV), Accounting rate of return (ARR),

Internal Rate of return (IRR) etc. making the decision making regarding the project

effective and beneficial for the organization.

(Figure - Project Appraisal Method)

(Source - Jinali, 2014)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1.

Price Optimisation – The price has been a critical factor in the profitability of the

company due to various factors such as the volatility in the market condition with the

increase in the globalisation. The increase in the choice to the consumers has made the

organisation think about the pricing to be effective in various factors (Guy, 2012).

The price optimisation technique can be useful in the following way:-

The organisation can be beneficial in financially by helping to focus on the important

components of such as the margin, volume with respect to the revenue generated. It is

useful in providing the consistency among the sales and also alignment with the

strategies.

Job-Costing – The job costing is useful where there is a variety of products and it is

important to allocate the period cost to the respective jobs. To determine the profitability

of each division and products it is important that there are proper apportionment and

allocation of the cost to respected jobs which can be possible with the help of the Job

costing system (Ingram, 2018). It further results in determining the actual performance

and the key areas where the company must focus to increase the profitability of the

company. The Unit cost can be determined for the purpose of the managerial decision

making.

Inventory Management – There are a various benefit that is associated with the use of

inventory management system such as:-

7

Price

Optimisation

Direct

Financial

Benefits

Consistency

Allignment

with the

strategies

Price Optimisation – The price has been a critical factor in the profitability of the

company due to various factors such as the volatility in the market condition with the

increase in the globalisation. The increase in the choice to the consumers has made the

organisation think about the pricing to be effective in various factors (Guy, 2012).

The price optimisation technique can be useful in the following way:-

The organisation can be beneficial in financially by helping to focus on the important

components of such as the margin, volume with respect to the revenue generated. It is

useful in providing the consistency among the sales and also alignment with the

strategies.

Job-Costing – The job costing is useful where there is a variety of products and it is

important to allocate the period cost to the respective jobs. To determine the profitability

of each division and products it is important that there are proper apportionment and

allocation of the cost to respected jobs which can be possible with the help of the Job

costing system (Ingram, 2018). It further results in determining the actual performance

and the key areas where the company must focus to increase the profitability of the

company. The Unit cost can be determined for the purpose of the managerial decision

making.

Inventory Management – There are a various benefit that is associated with the use of

inventory management system such as:-

7

Price

Optimisation

Direct

Financial

Benefits

Consistency

Allignment

with the

strategies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The techniques and ideologies changed with the change in the market conditions and

time. The managers focus on increasing the production and decreasing the cost instead

of talking about an increase in the price of the product which made it important for the

organisation to look at the inventory management (Mwangi, and Nyambura, 2015). The

Effective management is important in having an effective level of the inventory which

reduces the cost of the company that is earlier invested in the stock. Inventory

management results in continuous supply and controlling of the cost by having the

optimum level of stock.

Cost- Accounting – The cost accounting is useful in attaining the financial

sustainability through effective management. The cost accounting is useful in setting up

of optimum pricing strategy by taking in account all the cost involved (Dražić, et. al.,

2016). It is useful for the organisation in determining and decision making about the

price. It is useful in increasing the profitability and productivity of the company by

reducing the cost involved in the production and making improvement in the efficiency.

8

Increased Production

Cost Control

Reduce Supply

Continous Supply

time. The managers focus on increasing the production and decreasing the cost instead

of talking about an increase in the price of the product which made it important for the

organisation to look at the inventory management (Mwangi, and Nyambura, 2015). The

Effective management is important in having an effective level of the inventory which

reduces the cost of the company that is earlier invested in the stock. Inventory

management results in continuous supply and controlling of the cost by having the

optimum level of stock.

Cost- Accounting – The cost accounting is useful in attaining the financial

sustainability through effective management. The cost accounting is useful in setting up

of optimum pricing strategy by taking in account all the cost involved (Dražić, et. al.,

2016). It is useful for the organisation in determining and decision making about the

price. It is useful in increasing the profitability and productivity of the company by

reducing the cost involved in the production and making improvement in the efficiency.

8

Increased Production

Cost Control

Reduce Supply

Continous Supply

D1.

The management accounting systems and reporting are important for the organisation.

The reporting is based on the information and data that are being recorded in the

system used by the organisation. The management accounting system is useful in

recording of the data but for an effective analysis it is important that there is proper

reporting of the data recorded which is being done by the management accounting

reporting. The system and reporting both are important for the decision making of the

organisation. The managers are able to take the decisions depending upon the reports

that are being generated. It is important to have a comparison and analysis of the

results that are being achieved by the organisation which can be possible with the

presentation of the data in a format which can be easily understood and comparable

(Smith, 2017). The management accounting system is an effective tool to keep a track

of all the transactions that are being recorded. The management accounting reporting

helps in reducing the cost of the company and management of the inventory levels. The

management accounting system and reporting are important for the effective

management increasing the productivity and profitability by providing a better

management of resources.

9

The management accounting systems and reporting are important for the organisation.

The reporting is based on the information and data that are being recorded in the

system used by the organisation. The management accounting system is useful in

recording of the data but for an effective analysis it is important that there is proper

reporting of the data recorded which is being done by the management accounting

reporting. The system and reporting both are important for the decision making of the

organisation. The managers are able to take the decisions depending upon the reports

that are being generated. It is important to have a comparison and analysis of the

results that are being achieved by the organisation which can be possible with the

presentation of the data in a format which can be easily understood and comparable

(Smith, 2017). The management accounting system is an effective tool to keep a track

of all the transactions that are being recorded. The management accounting reporting

helps in reducing the cost of the company and management of the inventory levels. The

management accounting system and reporting are important for the effective

management increasing the productivity and profitability by providing a better

management of resources.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO2

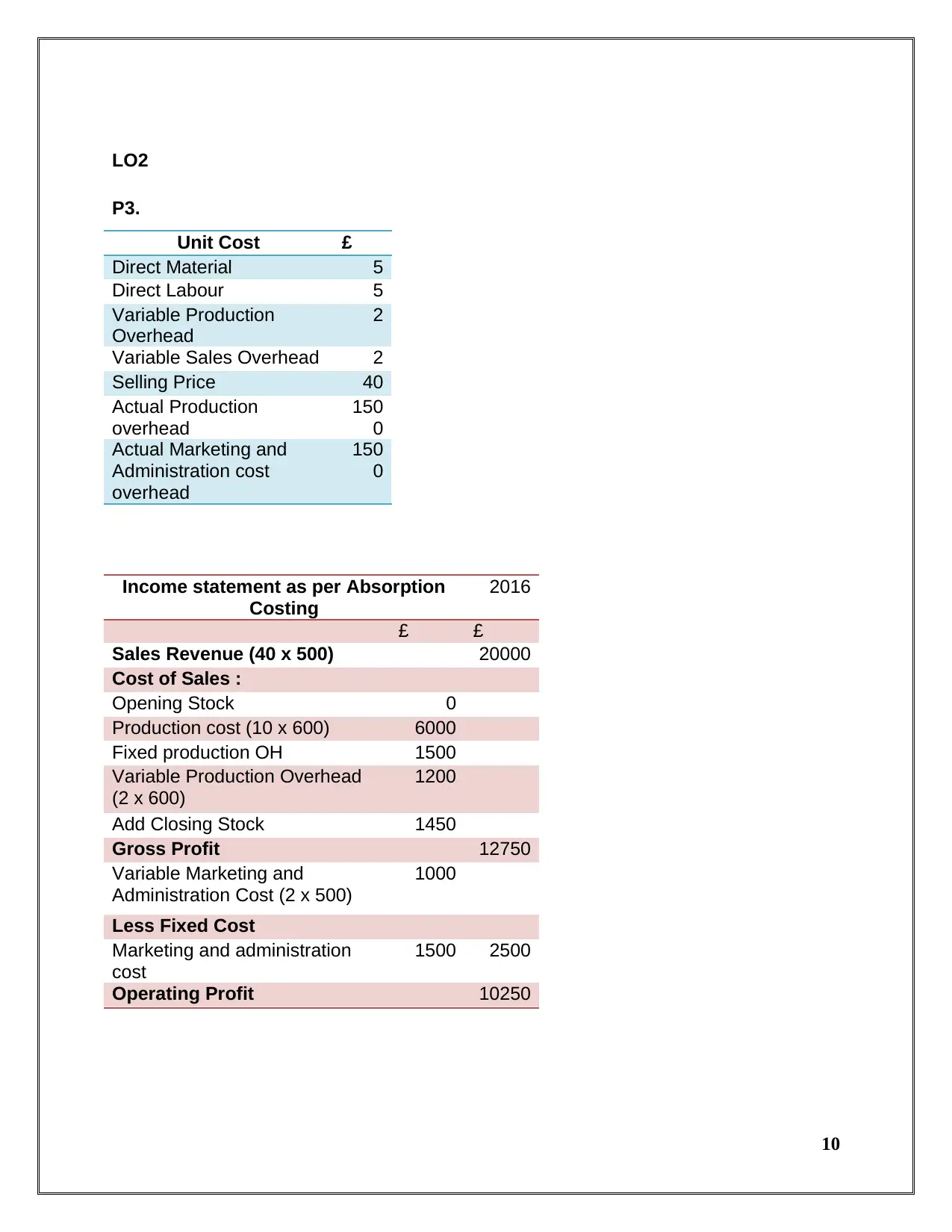

P3.

Unit Cost £

Direct Material 5

Direct Labour 5

Variable Production

Overhead

2

Variable Sales Overhead 2

Selling Price 40

Actual Production

overhead

150

0

Actual Marketing and

Administration cost

overhead

150

0

Income statement as per Absorption

Costing

2016

£ £

Sales Revenue (40 x 500) 20000

Cost of Sales :

Opening Stock 0

Production cost (10 x 600) 6000

Fixed production OH 1500

Variable Production Overhead

(2 x 600)

1200

Add Closing Stock 1450

Gross Profit 12750

Variable Marketing and

Administration Cost (2 x 500)

1000

Less Fixed Cost

Marketing and administration

cost

1500 2500

Operating Profit 10250

10

P3.

Unit Cost £

Direct Material 5

Direct Labour 5

Variable Production

Overhead

2

Variable Sales Overhead 2

Selling Price 40

Actual Production

overhead

150

0

Actual Marketing and

Administration cost

overhead

150

0

Income statement as per Absorption

Costing

2016

£ £

Sales Revenue (40 x 500) 20000

Cost of Sales :

Opening Stock 0

Production cost (10 x 600) 6000

Fixed production OH 1500

Variable Production Overhead

(2 x 600)

1200

Add Closing Stock 1450

Gross Profit 12750

Variable Marketing and

Administration Cost (2 x 500)

1000

Less Fixed Cost

Marketing and administration

cost

1500 2500

Operating Profit 10250

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

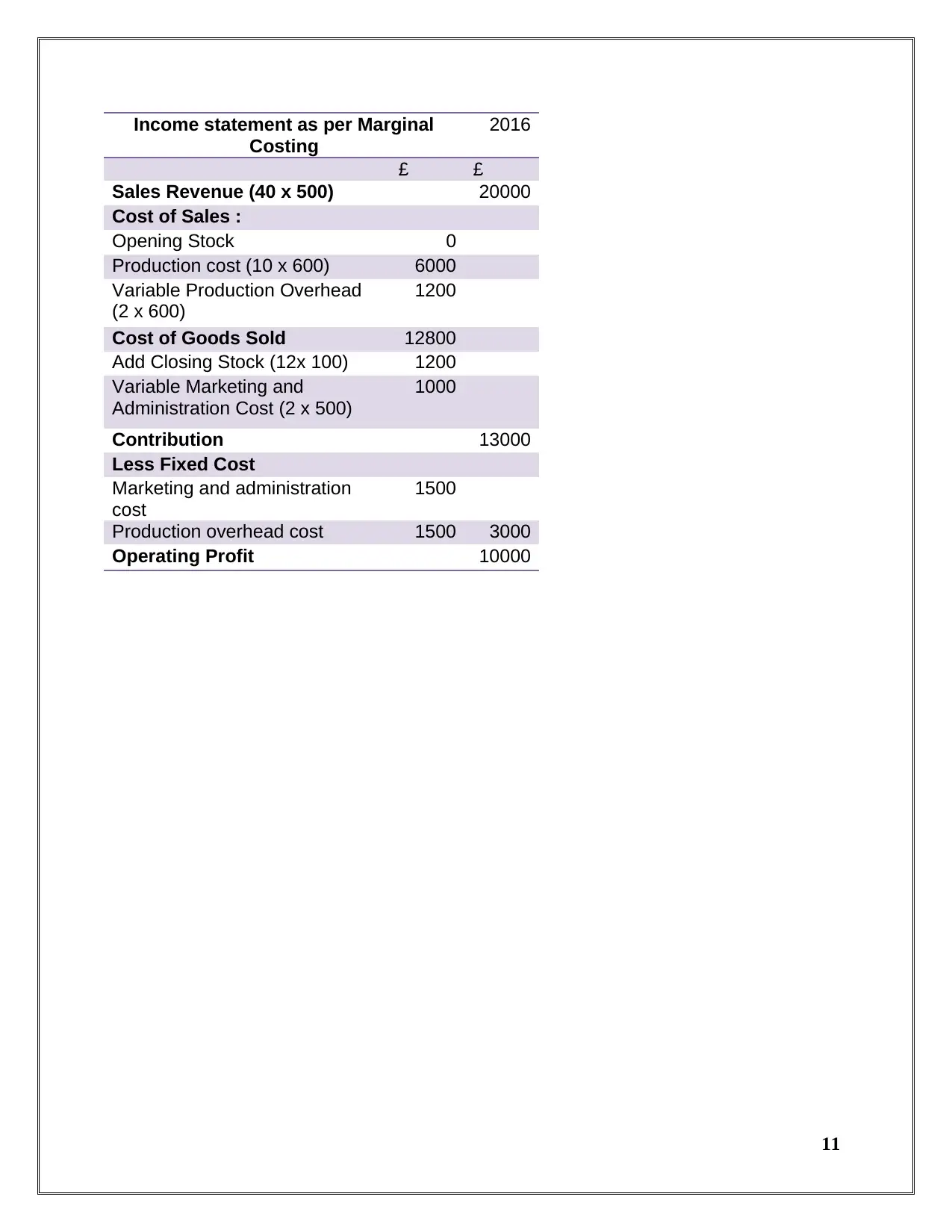

Income statement as per Marginal

Costing

2016

£ £

Sales Revenue (40 x 500) 20000

Cost of Sales :

Opening Stock 0

Production cost (10 x 600) 6000

Variable Production Overhead

(2 x 600)

1200

Cost of Goods Sold 12800

Add Closing Stock (12x 100) 1200

Variable Marketing and

Administration Cost (2 x 500)

1000

Contribution 13000

Less Fixed Cost

Marketing and administration

cost

1500

Production overhead cost 1500 3000

Operating Profit 10000

11

Costing

2016

£ £

Sales Revenue (40 x 500) 20000

Cost of Sales :

Opening Stock 0

Production cost (10 x 600) 6000

Variable Production Overhead

(2 x 600)

1200

Cost of Goods Sold 12800

Add Closing Stock (12x 100) 1200

Variable Marketing and

Administration Cost (2 x 500)

1000

Contribution 13000

Less Fixed Cost

Marketing and administration

cost

1500

Production overhead cost 1500 3000

Operating Profit 10000

11

M2.

The cost accounting techniques that are being used for the presentation of the data

includes the Marginal and Absorption costing. There are different types of cost such as

fixed cost, variable cost etc. The fixed cost remains same and does not change with the

change in production whereas the variable cost show changes with the level of

production. It is important to have a proper allocation and apportionment of the cost for

an effective costing of the product.

Marginal Costing – The marginal costing is the technique used by the managers for

the purpose of internal use. Marginal costing is the technique where only the variable

cost is being considered for the calculation of per unit of the product. It is useful in

calculating the contribution that is being provided by each and every unit (Garcia, 2017).

The marginal costing technique charges the fixed as the period cost and write it off in

the same period on the basis of the actual amount incurred. The marginal costing

technique is useful in facilitating the decision making and allocation of the resources by

the managers. The profit in the marginal costing is less in comparison to the absorption

costing.

Absorption Costing – The Absorption costing is the technique that is used for the

purpose of the stakeholders of the company. The absorption costing technique not only

considers the variable cost but also charge the fixed cost to the cost of the product as

under or over absorption of the cost. The gross profit is calculated through the

absorption costing and used to fulfill the statutory requirement. The absorption costing

technique absorbs the fixed cost of the production cost (Bragg, 2016). The absorption

costing technique is important to identify the profitability of the company. The profit in

comparison to marginal costing is more due to the absorption of the fixed cost incurred

instead of charging it at full in the same period. The fixed cost is carried forward in the

closing stock of the company.

The profit in both the techniques will be same in the long run. It will also be same if the

opening and closing inventory are same and there are no changes in the fixed cost of

12

The cost accounting techniques that are being used for the presentation of the data

includes the Marginal and Absorption costing. There are different types of cost such as

fixed cost, variable cost etc. The fixed cost remains same and does not change with the

change in production whereas the variable cost show changes with the level of

production. It is important to have a proper allocation and apportionment of the cost for

an effective costing of the product.

Marginal Costing – The marginal costing is the technique used by the managers for

the purpose of internal use. Marginal costing is the technique where only the variable

cost is being considered for the calculation of per unit of the product. It is useful in

calculating the contribution that is being provided by each and every unit (Garcia, 2017).

The marginal costing technique charges the fixed as the period cost and write it off in

the same period on the basis of the actual amount incurred. The marginal costing

technique is useful in facilitating the decision making and allocation of the resources by

the managers. The profit in the marginal costing is less in comparison to the absorption

costing.

Absorption Costing – The Absorption costing is the technique that is used for the

purpose of the stakeholders of the company. The absorption costing technique not only

considers the variable cost but also charge the fixed cost to the cost of the product as

under or over absorption of the cost. The gross profit is calculated through the

absorption costing and used to fulfill the statutory requirement. The absorption costing

technique absorbs the fixed cost of the production cost (Bragg, 2016). The absorption

costing technique is important to identify the profitability of the company. The profit in

comparison to marginal costing is more due to the absorption of the fixed cost incurred

instead of charging it at full in the same period. The fixed cost is carried forward in the

closing stock of the company.

The profit in both the techniques will be same in the long run. It will also be same if the

opening and closing inventory are same and there are no changes in the fixed cost of

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.