Management Accounting Report: Financial Problem Solving Techniques

VerifiedAdded on 2021/02/19

|17

|3857

|35

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its role in financial analysis and problem-solving within a business context, specifically referencing A&R Cambridge Ltd. It begins by defining management accounting, its systems, and requirements, contrasting it with financial accounting. The report then details various methods used in management accounting reports, including income statements, cash flow statements, and balance sheets. Furthermore, it delves into costing techniques, such as absorption and marginal costing, illustrating their application in preparing income statements. The report also covers different management accounting systems for resolving financial problems, supported by practical examples and calculations, demonstrating the practical application of these techniques. The report concludes by providing a detailed analysis of financial data and the importance of management accounting in making informed business decisions.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P 1 Explaining management accounting, management accounting systems and their

requirements in the company ......................................................................................................1

P2 Methods used for management accounting report..................................................................3

P 3 Preparing income statements using marginal and absorption costing techniques of

management accounting...............................................................................................................4

P 4................................................................................................................................................8

Case 4.........................................................................................................................................10

P 5. Comparing different management accounting system used for resolving financial

problems.....................................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P 1 Explaining management accounting, management accounting systems and their

requirements in the company ......................................................................................................1

P2 Methods used for management accounting report..................................................................3

P 3 Preparing income statements using marginal and absorption costing techniques of

management accounting...............................................................................................................4

P 4................................................................................................................................................8

Case 4.........................................................................................................................................10

P 5. Comparing different management accounting system used for resolving financial

problems.....................................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

A provision made of the set of numerous financial information of the company for the

purpose of using it in the business organisation and helping its managers for the development

purpose is nothing but a management accounting. It can also be defined as a process of analysing

internal performance of the company and summarise them in an effective manner so that

managers could easily analyse the actual performance and formulate their plans and strategies for

the business in more effective manner. A&R Cambridge Ltd. is a medium szized manufacturing

company of England. it was established in 2017. The present study shows a report explaning

detailed information about overall management accounting system, its requirement in the

company along with major difference of management accounting system with financial

accounting.

In addition, the study also shows an explanation regarding different types of planning

tools of budgetary control system and their critical analysis. It provides details regarding

numerous types of management accounting system that can be used by the various business

organisations in order to develop strength of the company in responding to various financial

problems arise in the company. In addition, a part of the present assignment also shows some

practical financial problems solved with the help of appropriate techniques of management

accounting system.

LO 1

P 1 Explaining management accounting, management accounting systems and their

requirements in the company

Management accounting

The term management accounting can be described as a range of methods used in the

management of numerous monitory and non monitory activities relating to financial performance

of the company (Fernando, 2016). It is analysing, summarising and presenting each financial

transaction of the company in more presentable way so that even a non commercial manager

could understand the actual financial position of the company. In this regard, the management

accounting can also be defined as a branch of accounting that performs its operations by assisting

the managers in their decision making process in context to financial performance of company.

Key functions of management accounting

1

A provision made of the set of numerous financial information of the company for the

purpose of using it in the business organisation and helping its managers for the development

purpose is nothing but a management accounting. It can also be defined as a process of analysing

internal performance of the company and summarise them in an effective manner so that

managers could easily analyse the actual performance and formulate their plans and strategies for

the business in more effective manner. A&R Cambridge Ltd. is a medium szized manufacturing

company of England. it was established in 2017. The present study shows a report explaning

detailed information about overall management accounting system, its requirement in the

company along with major difference of management accounting system with financial

accounting.

In addition, the study also shows an explanation regarding different types of planning

tools of budgetary control system and their critical analysis. It provides details regarding

numerous types of management accounting system that can be used by the various business

organisations in order to develop strength of the company in responding to various financial

problems arise in the company. In addition, a part of the present assignment also shows some

practical financial problems solved with the help of appropriate techniques of management

accounting system.

LO 1

P 1 Explaining management accounting, management accounting systems and their

requirements in the company

Management accounting

The term management accounting can be described as a range of methods used in the

management of numerous monitory and non monitory activities relating to financial performance

of the company (Fernando, 2016). It is analysing, summarising and presenting each financial

transaction of the company in more presentable way so that even a non commercial manager

could understand the actual financial position of the company. In this regard, the management

accounting can also be defined as a branch of accounting that performs its operations by assisting

the managers in their decision making process in context to financial performance of company.

Key functions of management accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Following are the major key functions of managerial accounting in the business

organisation:

To provide sufficient data to the managers.

Modifying each information recieved by them in such a way so that it could be used by

the managers for their decision making process.

To assist managerial accountants in improving their quality of performing their

managerial functions

Management accounting system also performs a key function of being a mean of

communication in the company regarding financial information.

Types of management accounting:

Following are different types of management accounting system that can be adopted by

an organisation in order to improve quality of management and control:

Financial accounting system

The financial accounting system can be defined as a branch of overall accounting system

that concerns with analysis of various financial transactions performed by the company and

summarising them in a professional manner for the purpose of preparing various financial reports

such as statement of financial position, income statements, cash flow statements, etc.

For this purpose the managerial accountant needs to follow several rules and procedures

provided by GAAP, Financial accounting standard board (FASB) etc. These bodies provides

several guidelines, rules and procedures that laws that is needed to be comply by each business

organisation in order to prepare their financial reports.

In addition, the AIS (Accounting information system) helps the financial accountant in

improving the quality of collecting summarising and presenting the financial data in more

presentable manner (Accounting Systems & Rules. 2017). It AIS is a computer based system that

also helps in maintaining the financial information and tracking each financial and accounting

transaction of the business in an effective way.

Furthermore, the adoption of financial accounting system is required by the company in

order to improve the internal control system of the company and providing each information to

financial accountant more accurately.

Cost accounting system

2

organisation:

To provide sufficient data to the managers.

Modifying each information recieved by them in such a way so that it could be used by

the managers for their decision making process.

To assist managerial accountants in improving their quality of performing their

managerial functions

Management accounting system also performs a key function of being a mean of

communication in the company regarding financial information.

Types of management accounting:

Following are different types of management accounting system that can be adopted by

an organisation in order to improve quality of management and control:

Financial accounting system

The financial accounting system can be defined as a branch of overall accounting system

that concerns with analysis of various financial transactions performed by the company and

summarising them in a professional manner for the purpose of preparing various financial reports

such as statement of financial position, income statements, cash flow statements, etc.

For this purpose the managerial accountant needs to follow several rules and procedures

provided by GAAP, Financial accounting standard board (FASB) etc. These bodies provides

several guidelines, rules and procedures that laws that is needed to be comply by each business

organisation in order to prepare their financial reports.

In addition, the AIS (Accounting information system) helps the financial accountant in

improving the quality of collecting summarising and presenting the financial data in more

presentable manner (Accounting Systems & Rules. 2017). It AIS is a computer based system that

also helps in maintaining the financial information and tracking each financial and accounting

transaction of the business in an effective way.

Furthermore, the adoption of financial accounting system is required by the company in

order to improve the internal control system of the company and providing each information to

financial accountant more accurately.

Cost accounting system

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting system is also one major type of management accounting system that

enables the managers in improving their management and control over the cost incurred by the

company. With the help of this system, managers also becomes able to detect the areas in which

A&R Cambridge Ltd. can cut down the cost without sacrificing with any quality of working or

profit generation capacity of the business.

Product costing, activity based costing, etc. are some methods used in the cost accounting

system. With the help of these methods, managers of the firm can determine different costs

incurred by the business in each activity. In this order, managerial accountant can become able to

improve their efficiency of monitoring each activity relating to cost and develop more effective

controlling measures for the firm in context to cost control of the company.

Management accounting system

Management accounting system is set of management accounting system is a set of rules

and guidelines that helps in presenting each information of the A&R Cambridge Ltd. regarding

its financial activities performed by the company during a specific time period. Adoption of this

system leads in helping the managers in their decision making process in context to the

improving the financial position of the company in the competitive market. This system also

provides various methods for the purpose of controlling and managing various activities such as

profit generation, investment decision, cost control, price optimisation, etc.

Tax accounting system

This system is required to be adopted by all those business organisations that needs to

pay tax to the Government (Ibrahim, 2019. International taxation, corporate tax, individual tax,

tax on partnership businesses, etc. are some core branches of the tax accounting system. These

branches can be adopted by any person of the country including individuals, corporations,

business organisation, etc. as per their needs.

P2 Methods used for management accounting report

Management accounting report is used to present the data in systematic manner to get evaluate

the information and take the useful decisions in the organization. Different methods are used by

the organization for management accounting report such as :

Income statement : The purpose of income statement is to provide the financial earnings of the

organization in specific period which can be monthly, quarterly or annually. It also known as

profit and loss account or earning statement. It was used by the A & R Cambridge limited to

3

enables the managers in improving their management and control over the cost incurred by the

company. With the help of this system, managers also becomes able to detect the areas in which

A&R Cambridge Ltd. can cut down the cost without sacrificing with any quality of working or

profit generation capacity of the business.

Product costing, activity based costing, etc. are some methods used in the cost accounting

system. With the help of these methods, managers of the firm can determine different costs

incurred by the business in each activity. In this order, managerial accountant can become able to

improve their efficiency of monitoring each activity relating to cost and develop more effective

controlling measures for the firm in context to cost control of the company.

Management accounting system

Management accounting system is set of management accounting system is a set of rules

and guidelines that helps in presenting each information of the A&R Cambridge Ltd. regarding

its financial activities performed by the company during a specific time period. Adoption of this

system leads in helping the managers in their decision making process in context to the

improving the financial position of the company in the competitive market. This system also

provides various methods for the purpose of controlling and managing various activities such as

profit generation, investment decision, cost control, price optimisation, etc.

Tax accounting system

This system is required to be adopted by all those business organisations that needs to

pay tax to the Government (Ibrahim, 2019. International taxation, corporate tax, individual tax,

tax on partnership businesses, etc. are some core branches of the tax accounting system. These

branches can be adopted by any person of the country including individuals, corporations,

business organisation, etc. as per their needs.

P2 Methods used for management accounting report

Management accounting report is used to present the data in systematic manner to get evaluate

the information and take the useful decisions in the organization. Different methods are used by

the organization for management accounting report such as :

Income statement : The purpose of income statement is to provide the financial earnings of the

organization in specific period which can be monthly, quarterly or annually. It also known as

profit and loss account or earning statement. It was used by the A & R Cambridge limited to

3

demonstrate the profitability and expenses of the organization to the different stakeholder and

customer to attract toward the business unit. The difference between the income and expenses

represent the net income or loss of the organization which was used for distributing the dividends

to the shareholders.

Cash flow statement : Cash flow statement is used to present the activities which generate the

cash or uses the cash in the organization. A & R Cambridge limited company present the total

cash inflow and outflow in a particular accounting period via the cash flow statement. The

purpose of the cash flow statement is to provide the information related to the cash payments,

cash receipts and net changes in the company because of the financial, operating and investing

activity.

Balance sheet : Balance sheet present financial status of the business in a particular accounting

year. It presents the total number of asset and liability in the organization to manage the debtor

and creditor of the business. A & R Cambridge limited analysis the financial position of the

business to control the activity and analysis the various factor which affect the growth of the

business.

Cost accounting system : Cost accounting system is also known as product costing system. It is

used by the company to estimate the cost of the product and services of the business to evaluate

the profitability, valuation of inventory and control the cost. For example evaluating the relation

between the cost and profit help the A & R Cambridge limited company to take the effective

decision and set the perfect price for their product.

Job costing system : Job costing system is mostly used in the customized product or when

customer orders the product. In job costing system they estimate each job cost and charge

according to the job. For example a house builder estimate the cost according to the different job

like building the structure, painting, furnishing etc.

Price optimizing system : It is used to analyse the reaction or behaviour of the customer

according to the price of the product. It also helps the company to analyse the price determine by

them is efficient or not ) (Gencia and et.al., 2016). For example by optimizing the price A & R

Cambridge limited company is able to analyse the buying behaviour of the customer.

4

customer to attract toward the business unit. The difference between the income and expenses

represent the net income or loss of the organization which was used for distributing the dividends

to the shareholders.

Cash flow statement : Cash flow statement is used to present the activities which generate the

cash or uses the cash in the organization. A & R Cambridge limited company present the total

cash inflow and outflow in a particular accounting period via the cash flow statement. The

purpose of the cash flow statement is to provide the information related to the cash payments,

cash receipts and net changes in the company because of the financial, operating and investing

activity.

Balance sheet : Balance sheet present financial status of the business in a particular accounting

year. It presents the total number of asset and liability in the organization to manage the debtor

and creditor of the business. A & R Cambridge limited analysis the financial position of the

business to control the activity and analysis the various factor which affect the growth of the

business.

Cost accounting system : Cost accounting system is also known as product costing system. It is

used by the company to estimate the cost of the product and services of the business to evaluate

the profitability, valuation of inventory and control the cost. For example evaluating the relation

between the cost and profit help the A & R Cambridge limited company to take the effective

decision and set the perfect price for their product.

Job costing system : Job costing system is mostly used in the customized product or when

customer orders the product. In job costing system they estimate each job cost and charge

according to the job. For example a house builder estimate the cost according to the different job

like building the structure, painting, furnishing etc.

Price optimizing system : It is used to analyse the reaction or behaviour of the customer

according to the price of the product. It also helps the company to analyse the price determine by

them is efficient or not ) (Gencia and et.al., 2016). For example by optimizing the price A & R

Cambridge limited company is able to analyse the buying behaviour of the customer.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

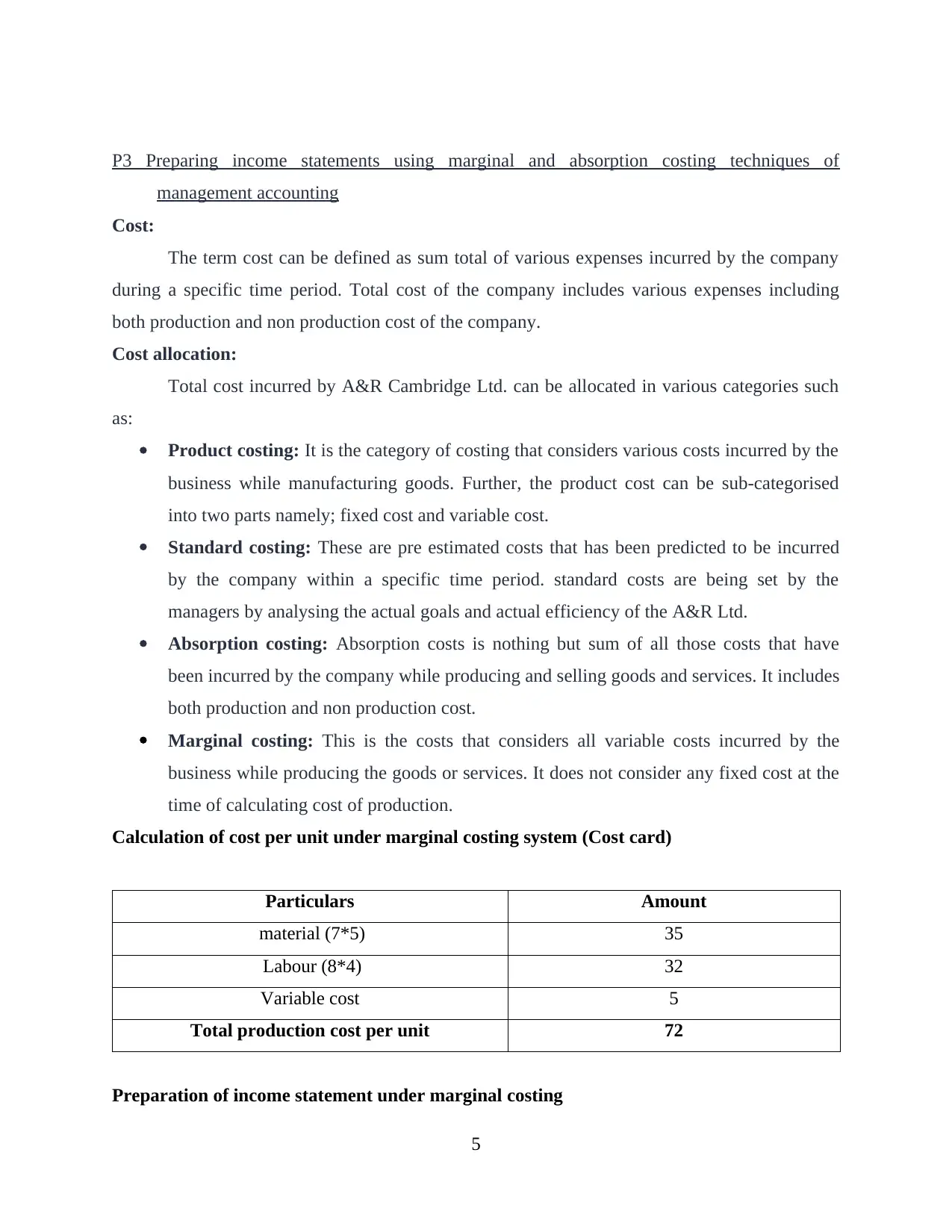

P3 Preparing income statements using marginal and absorption costing techniques of

management accounting

Cost:

The term cost can be defined as sum total of various expenses incurred by the company

during a specific time period. Total cost of the company includes various expenses including

both production and non production cost of the company.

Cost allocation:

Total cost incurred by A&R Cambridge Ltd. can be allocated in various categories such

as:

Product costing: It is the category of costing that considers various costs incurred by the

business while manufacturing goods. Further, the product cost can be sub-categorised

into two parts namely; fixed cost and variable cost.

Standard costing: These are pre estimated costs that has been predicted to be incurred

by the company within a specific time period. standard costs are being set by the

managers by analysing the actual goals and actual efficiency of the A&R Ltd.

Absorption costing: Absorption costs is nothing but sum of all those costs that have

been incurred by the company while producing and selling goods and services. It includes

both production and non production cost.

Marginal costing: This is the costs that considers all variable costs incurred by the

business while producing the goods or services. It does not consider any fixed cost at the

time of calculating cost of production.

Calculation of cost per unit under marginal costing system (Cost card)

Particulars Amount

material (7*5) 35

Labour (8*4) 32

Variable cost 5

Total production cost per unit 72

Preparation of income statement under marginal costing

5

management accounting

Cost:

The term cost can be defined as sum total of various expenses incurred by the company

during a specific time period. Total cost of the company includes various expenses including

both production and non production cost of the company.

Cost allocation:

Total cost incurred by A&R Cambridge Ltd. can be allocated in various categories such

as:

Product costing: It is the category of costing that considers various costs incurred by the

business while manufacturing goods. Further, the product cost can be sub-categorised

into two parts namely; fixed cost and variable cost.

Standard costing: These are pre estimated costs that has been predicted to be incurred

by the company within a specific time period. standard costs are being set by the

managers by analysing the actual goals and actual efficiency of the A&R Ltd.

Absorption costing: Absorption costs is nothing but sum of all those costs that have

been incurred by the company while producing and selling goods and services. It includes

both production and non production cost.

Marginal costing: This is the costs that considers all variable costs incurred by the

business while producing the goods or services. It does not consider any fixed cost at the

time of calculating cost of production.

Calculation of cost per unit under marginal costing system (Cost card)

Particulars Amount

material (7*5) 35

Labour (8*4) 32

Variable cost 5

Total production cost per unit 72

Preparation of income statement under marginal costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

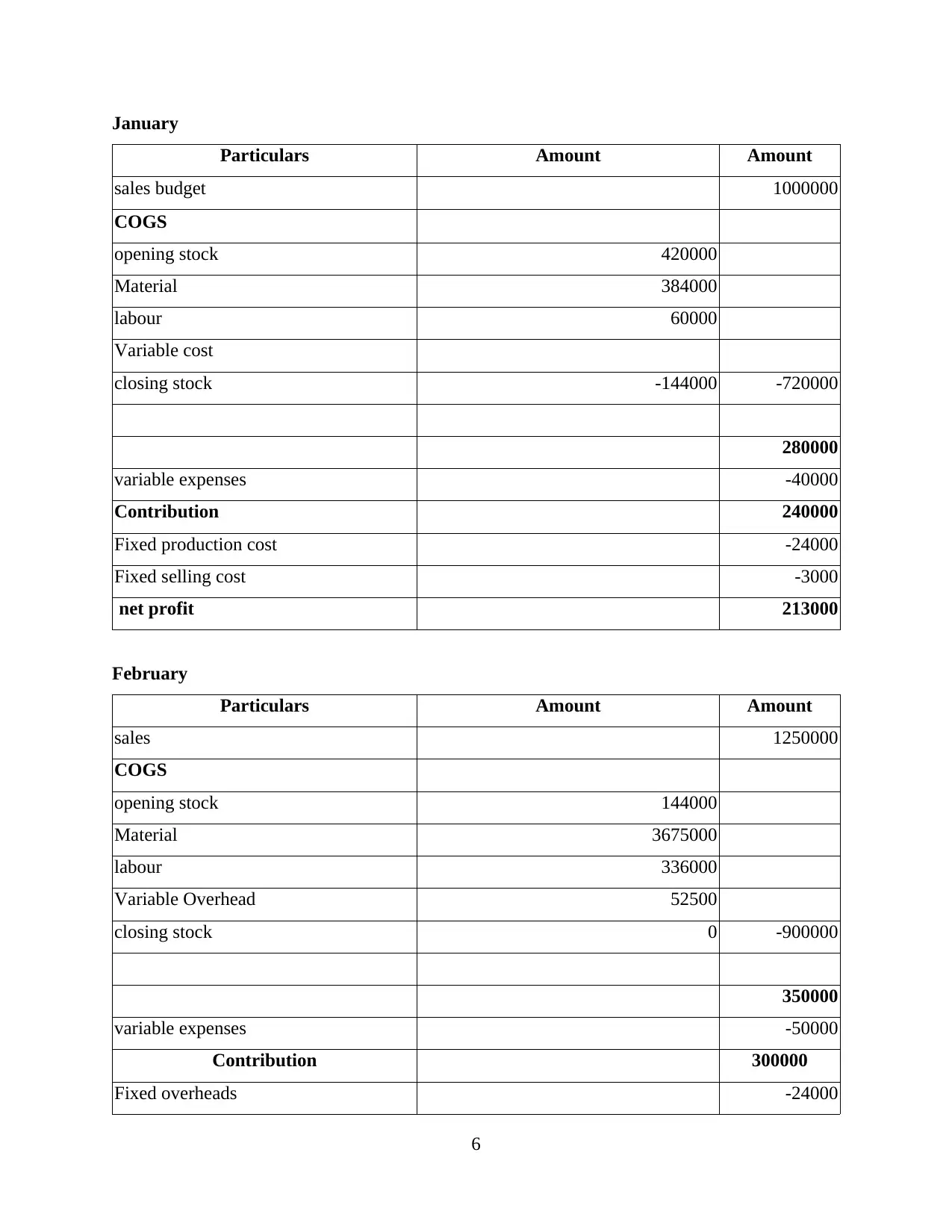

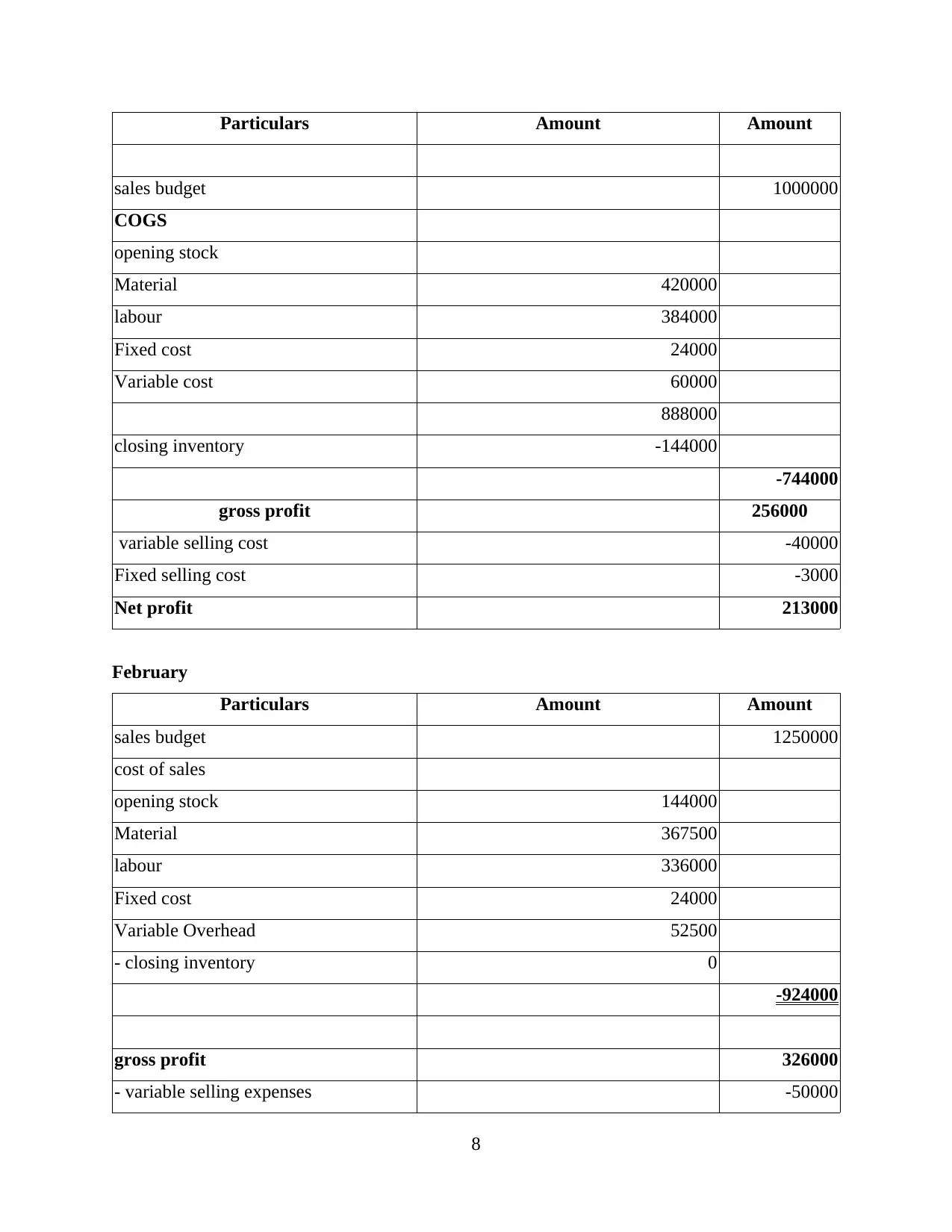

January

Particulars Amount Amount

sales budget 1000000

COGS

opening stock 420000

Material 384000

labour 60000

Variable cost

closing stock -144000 -720000

280000

variable expenses -40000

Contribution 240000

Fixed production cost -24000

Fixed selling cost -3000

net profit 213000

February

Particulars Amount Amount

sales 1250000

COGS

opening stock 144000

Material 3675000

labour 336000

Variable Overhead 52500

closing stock 0 -900000

350000

variable expenses -50000

Contribution 300000

Fixed overheads -24000

6

Particulars Amount Amount

sales budget 1000000

COGS

opening stock 420000

Material 384000

labour 60000

Variable cost

closing stock -144000 -720000

280000

variable expenses -40000

Contribution 240000

Fixed production cost -24000

Fixed selling cost -3000

net profit 213000

February

Particulars Amount Amount

sales 1250000

COGS

opening stock 144000

Material 3675000

labour 336000

Variable Overhead 52500

closing stock 0 -900000

350000

variable expenses -50000

Contribution 300000

Fixed overheads -24000

6

Fixed selling expenses -3000

Net profit 273000

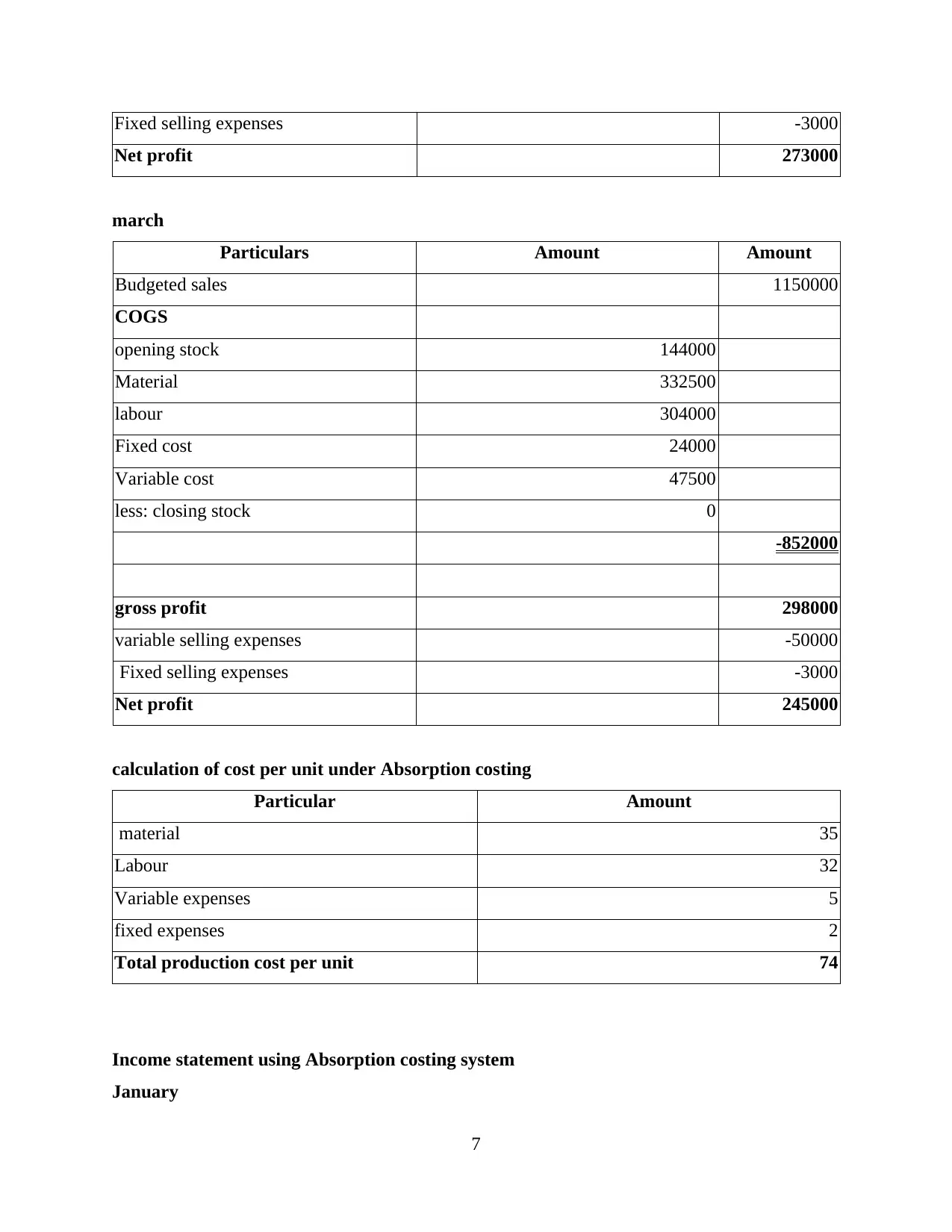

march

Particulars Amount Amount

Budgeted sales 1150000

COGS

opening stock 144000

Material 332500

labour 304000

Fixed cost 24000

Variable cost 47500

less: closing stock 0

-852000

gross profit 298000

variable selling expenses -50000

Fixed selling expenses -3000

Net profit 245000

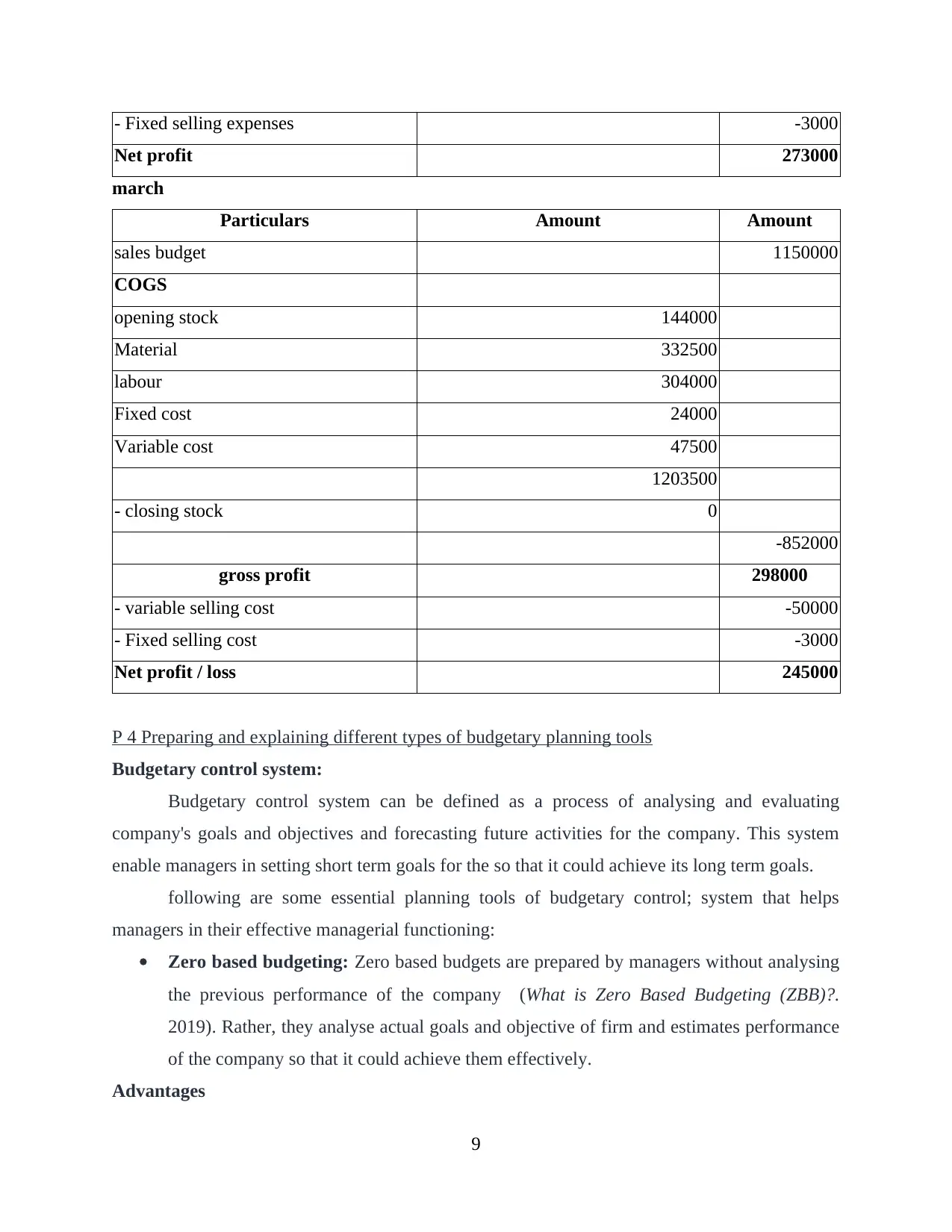

calculation of cost per unit under Absorption costing

Particular Amount

material 35

Labour 32

Variable expenses 5

fixed expenses 2

Total production cost per unit 74

Income statement using Absorption costing system

January

7

Net profit 273000

march

Particulars Amount Amount

Budgeted sales 1150000

COGS

opening stock 144000

Material 332500

labour 304000

Fixed cost 24000

Variable cost 47500

less: closing stock 0

-852000

gross profit 298000

variable selling expenses -50000

Fixed selling expenses -3000

Net profit 245000

calculation of cost per unit under Absorption costing

Particular Amount

material 35

Labour 32

Variable expenses 5

fixed expenses 2

Total production cost per unit 74

Income statement using Absorption costing system

January

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount Amount

sales budget 1000000

COGS

opening stock

Material 420000

labour 384000

Fixed cost 24000

Variable cost 60000

888000

closing inventory -144000

-744000

gross profit 256000

variable selling cost -40000

Fixed selling cost -3000

Net profit 213000

February

Particulars Amount Amount

sales budget 1250000

cost of sales

opening stock 144000

Material 367500

labour 336000

Fixed cost 24000

Variable Overhead 52500

- closing inventory 0

-924000

gross profit 326000

- variable selling expenses -50000

8

sales budget 1000000

COGS

opening stock

Material 420000

labour 384000

Fixed cost 24000

Variable cost 60000

888000

closing inventory -144000

-744000

gross profit 256000

variable selling cost -40000

Fixed selling cost -3000

Net profit 213000

February

Particulars Amount Amount

sales budget 1250000

cost of sales

opening stock 144000

Material 367500

labour 336000

Fixed cost 24000

Variable Overhead 52500

- closing inventory 0

-924000

gross profit 326000

- variable selling expenses -50000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

- Fixed selling expenses -3000

Net profit 273000

march

Particulars Amount Amount

sales budget 1150000

COGS

opening stock 144000

Material 332500

labour 304000

Fixed cost 24000

Variable cost 47500

1203500

- closing stock 0

-852000

gross profit 298000

- variable selling cost -50000

- Fixed selling cost -3000

Net profit / loss 245000

P 4 Preparing and explaining different types of budgetary planning tools

Budgetary control system:

Budgetary control system can be defined as a process of analysing and evaluating

company's goals and objectives and forecasting future activities for the company. This system

enable managers in setting short term goals for the so that it could achieve its long term goals.

following are some essential planning tools of budgetary control; system that helps

managers in their effective managerial functioning:

Zero based budgeting: Zero based budgets are prepared by managers without analysing

the previous performance of the company (What is Zero Based Budgeting (ZBB)?.

2019). Rather, they analyse actual goals and objective of firm and estimates performance

of the company so that it could achieve them effectively.

Advantages

9

Net profit 273000

march

Particulars Amount Amount

sales budget 1150000

COGS

opening stock 144000

Material 332500

labour 304000

Fixed cost 24000

Variable cost 47500

1203500

- closing stock 0

-852000

gross profit 298000

- variable selling cost -50000

- Fixed selling cost -3000

Net profit / loss 245000

P 4 Preparing and explaining different types of budgetary planning tools

Budgetary control system:

Budgetary control system can be defined as a process of analysing and evaluating

company's goals and objectives and forecasting future activities for the company. This system

enable managers in setting short term goals for the so that it could achieve its long term goals.

following are some essential planning tools of budgetary control; system that helps

managers in their effective managerial functioning:

Zero based budgeting: Zero based budgets are prepared by managers without analysing

the previous performance of the company (What is Zero Based Budgeting (ZBB)?.

2019). Rather, they analyse actual goals and objective of firm and estimates performance

of the company so that it could achieve them effectively.

Advantages

9

▪ It improves efficiency of company in achiveing the goals.

▪ It reduces the working of analysing previous performance of business.

Disadvantage

▪ It requires professional skills of managers.

▪ Company needs to invest huge money in preparation of this budget.

Cash budgets: Cash budgets refers to a statement showing estimation of movement of

cash and cash equivalents within the business. This budget helps in detecting areas of

usage as well as areas of generation of cash and cash equivalent for the A&R cambridge

Ltd.

Advantages

▪ It helps in maintaining sufficient liquidity within the firm.

▪ It provides information regarding several areas through which business can

generate cash and cash equivalents to be used in the business.

Disadvantage

▪ Estimation of value of cash is not possible.

▪ This budget fails at the time of change in value of money.

Operational budgets: Operational budgets are set of those budgets that describes

estimated performance of the business in its various operations. sales budgets, production

budgets, purchase budgets, etc. are some main types of operational budgets.

Advantages

▪ It helps in predicting each core operation of A&R Cambridge Ltd.

▪ It provides information regarding numerous resources that would be required by

firm within specific time.

Disadvantage

▪ It results in generation of rigidity within various business operations.

▪ It fails if company takes another project other than pre decided projects.

Case 3

Sales budget

Particulars Product EC1 Product EC2 Product EC3

Budgeted sales 2000 4000 3000

per unit prince 100 130 150

10

▪ It reduces the working of analysing previous performance of business.

Disadvantage

▪ It requires professional skills of managers.

▪ Company needs to invest huge money in preparation of this budget.

Cash budgets: Cash budgets refers to a statement showing estimation of movement of

cash and cash equivalents within the business. This budget helps in detecting areas of

usage as well as areas of generation of cash and cash equivalent for the A&R cambridge

Ltd.

Advantages

▪ It helps in maintaining sufficient liquidity within the firm.

▪ It provides information regarding several areas through which business can

generate cash and cash equivalents to be used in the business.

Disadvantage

▪ Estimation of value of cash is not possible.

▪ This budget fails at the time of change in value of money.

Operational budgets: Operational budgets are set of those budgets that describes

estimated performance of the business in its various operations. sales budgets, production

budgets, purchase budgets, etc. are some main types of operational budgets.

Advantages

▪ It helps in predicting each core operation of A&R Cambridge Ltd.

▪ It provides information regarding numerous resources that would be required by

firm within specific time.

Disadvantage

▪ It results in generation of rigidity within various business operations.

▪ It fails if company takes another project other than pre decided projects.

Case 3

Sales budget

Particulars Product EC1 Product EC2 Product EC3

Budgeted sales 2000 4000 3000

per unit prince 100 130 150

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.