Management Accounting: Decision Making Concepts and Techniques Report

VerifiedAdded on 2022/12/28

|19

|4817

|30

Report

AI Summary

This report delves into management accounting principles and their practical applications, focusing on Connect Catering Services in the UK. It covers essential requirements of different management accounting systems, including cost and inventory management. The report explains various reporting methods such as budgeting, aging reports, and cost accounting. It then explores cost analysis techniques, preparing income statements using marginal and absorption costing. Furthermore, it discusses planning tools for budgetary control, comparing the advantages and disadvantages of each. Finally, the report analyzes how organizations adapt management accounting systems to address financial challenges, providing a comprehensive overview of the subject matter.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction .....................................................................................................................................3

Task1................................................................................................................................................3

P1 Management accounting it's essential requirements of different types of management

accounting systems.....................................................................................................................3

P2 Explain different methods used for management accounting reporting................................5

Task2................................................................................................................................................7

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs. .........................................................................7

......................................................................10

Task3..............................................................................................................................................11

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................11

Task 4.............................................................................................................................................13

P5 Compare how organizations are adapting management accounting systems to respond to

financial problems. ........................................................................................................................13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

Introduction .....................................................................................................................................3

Task1................................................................................................................................................3

P1 Management accounting it's essential requirements of different types of management

accounting systems.....................................................................................................................3

P2 Explain different methods used for management accounting reporting................................5

Task2................................................................................................................................................7

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs. .........................................................................7

......................................................................10

Task3..............................................................................................................................................11

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control......................................................................................................................11

Task 4.............................................................................................................................................13

P5 Compare how organizations are adapting management accounting systems to respond to

financial problems. ........................................................................................................................13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................15

Introduction

Management accounting can be simply be defined as an accounting tools that is fruitful

to ensure that the organisation are using the best possible use of their limited and valuable

resource. It is applied for solving a number of tasks that includes measuring, analysing and

mainly presenting their financial information to the managers to make quicker and well-

informed decisions (Jansen, 2018). Talking in context of small and medium- sized companies,

management accounting solves a number of issues that includes limited credit facilities, lack of

demand of their product or service offerings and weaker or inappropriate recording system.

Connect Catering Services, is one of the well-known caterers for fresh foods and

are family oriented in U.K. They have been successful in operating their business for the last

thirty years through their excellent quality products and services. This projects aids their

management and includes important of management accounting it's practical application by

different techniques. Adding to this, it also covers different planning tools that will support them

in solving the financial issues.

Task1

P1 Management accounting it's essential requirements of different types of management

accounting systems.

Management accounting is relevant tools and selects the most useful financial information

that are annually recorded in important financial statements that include profit and loss

account,Balance sheet and cash flow statements (Maas and et. al., 2016). It's main aim is to

improve the decision making process of the company with the ultimate aim to make their process

sustainable in order to reach their desired objectives.

Management accounting has been successful to make immense contribution and have

resulted in effective decision making. Some of it's main principle has aided diverse organization

around the world to enhance the manager's decision making capabilities and in turn contributed

significantly in increase their productivity. This principles can be elaborated in detailed for it's

better understanding.

Management accounting can be simply be defined as an accounting tools that is fruitful

to ensure that the organisation are using the best possible use of their limited and valuable

resource. It is applied for solving a number of tasks that includes measuring, analysing and

mainly presenting their financial information to the managers to make quicker and well-

informed decisions (Jansen, 2018). Talking in context of small and medium- sized companies,

management accounting solves a number of issues that includes limited credit facilities, lack of

demand of their product or service offerings and weaker or inappropriate recording system.

Connect Catering Services, is one of the well-known caterers for fresh foods and

are family oriented in U.K. They have been successful in operating their business for the last

thirty years through their excellent quality products and services. This projects aids their

management and includes important of management accounting it's practical application by

different techniques. Adding to this, it also covers different planning tools that will support them

in solving the financial issues.

Task1

P1 Management accounting it's essential requirements of different types of management

accounting systems.

Management accounting is relevant tools and selects the most useful financial information

that are annually recorded in important financial statements that include profit and loss

account,Balance sheet and cash flow statements (Maas and et. al., 2016). It's main aim is to

improve the decision making process of the company with the ultimate aim to make their process

sustainable in order to reach their desired objectives.

Management accounting has been successful to make immense contribution and have

resulted in effective decision making. Some of it's main principle has aided diverse organization

around the world to enhance the manager's decision making capabilities and in turn contributed

significantly in increase their productivity. This principles can be elaborated in detailed for it's

better understanding.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Influence: This is one of the critical principle. It states the influence of communication

and it's power to strengthen decision making capabilities . It states the accurate and fair

information that is useful in analysing in order to evaluate and select the best alternative

that is most appropriate to solve the specific issue that have arisen in the company. This

is done, as it integrates diverse thought process as impact of actions in one department

effects all the other department and accordingly establishes proper co-ordination and

enhances productivity of the entire organisation (Boučková, 2015). This further aids to

become authoritative due to the result of getting access to the most required information

that is useful to them.

Relevance: Information is important for one and all. It is just that every individual and

different organization want to access the most useful information that is relevant for them

along with the individual making the decisions from all the available resources. It is

important for the decision maker to carefully understand requirement of all of their

shareholder as they are operating their business with the ultimate aim to maximize their

welfare. Adding to this point, it is important to ensure that they is a proper balance of all

the information including external and internal and financial and non financial.

Value: It is important to predict it's value. Management accounting is capable to link it's

processes to company's model and it is important to know the demand of it's macro

economic environment. This mainly deals with carefully evaluating all the available

opportunity and grabbing the best opportunity that minimizing the risks involved and aids

to follow a pathway that leads to maximization the value of it's crucial investments . It is

important for them to undergo situational analysis in order to make best decisions by

being well informed about the market conditions specifically in their industry and

economy and adopt the same as it is vital for their survival.

Creditability: It is very much important for improve and make the decision making

process more creditable. It is carefully evaluate the alternatives and select the most

reliable decisions. This further support the Company to fulfil the desires of the company.

It is important for management accounting experts to look towards the interest of all its

stakeholder and on a timely basis by taking regular feedbacks and addressing their

overall issues at the earliest (Gibassier and Schaltegger, 2015). It is crucial for experts of

management accounting to consider the feedbacks of all it's stakeholders in order to take

and it's power to strengthen decision making capabilities . It states the accurate and fair

information that is useful in analysing in order to evaluate and select the best alternative

that is most appropriate to solve the specific issue that have arisen in the company. This

is done, as it integrates diverse thought process as impact of actions in one department

effects all the other department and accordingly establishes proper co-ordination and

enhances productivity of the entire organisation (Boučková, 2015). This further aids to

become authoritative due to the result of getting access to the most required information

that is useful to them.

Relevance: Information is important for one and all. It is just that every individual and

different organization want to access the most useful information that is relevant for them

along with the individual making the decisions from all the available resources. It is

important for the decision maker to carefully understand requirement of all of their

shareholder as they are operating their business with the ultimate aim to maximize their

welfare. Adding to this point, it is important to ensure that they is a proper balance of all

the information including external and internal and financial and non financial.

Value: It is important to predict it's value. Management accounting is capable to link it's

processes to company's model and it is important to know the demand of it's macro

economic environment. This mainly deals with carefully evaluating all the available

opportunity and grabbing the best opportunity that minimizing the risks involved and aids

to follow a pathway that leads to maximization the value of it's crucial investments . It is

important for them to undergo situational analysis in order to make best decisions by

being well informed about the market conditions specifically in their industry and

economy and adopt the same as it is vital for their survival.

Creditability: It is very much important for improve and make the decision making

process more creditable. It is carefully evaluate the alternatives and select the most

reliable decisions. This further support the Company to fulfil the desires of the company.

It is important for management accounting experts to look towards the interest of all its

stakeholder and on a timely basis by taking regular feedbacks and addressing their

overall issues at the earliest (Gibassier and Schaltegger, 2015). It is crucial for experts of

management accounting to consider the feedbacks of all it's stakeholders in order to take

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the most appropriate decision that is in the best interest and maximizes That will be

fruitful for them in enhancing their productivity and become more creditable. This will

ultimately be beneficial for them to become leader in their industry.

It is important to understand the different management accounting system in to generate

significant information to become profitable. The some of the various types of management

accounting can be explained in detail below:

Cost accounting system: This is important system as it aids to make an accurate estimates for

making crucial decisions including ways to minimizing cost by eliminating unproductive

expenses and maximizing their profitability (Phan, Baird and Su, 2017). Adding to this, it is also

fruitful for doing accurate estimates to determine the closing stock with respect to raw material,

work in progress and final goods.

Inventory management system: This is basically defined as the computer based system to

record, update and monitor the company's stocks that includes closing inventory amounts, sales,

orders and deliveries. Many Organization has implemented this system in order to balance their

inventory by recording the information in a organized and systematic manner.

P2 Explain different methods used for management accounting reporting

Management accounting is also called by another name as cost accounting. It focuses on

engaging attention to account for financial information of the previous year. It is important for

the firm to generate relevant information that helps them to analyze their performance and take

corrective actions that is essential for their growth. It is vital to include factors such as it's

usefulness,timeless and completeness. The report is mainly used to plan, engage in regulating all

their activities at each steps by crucial decision-making by measuring performance and doing the

improvement needed to enhance their processes. There are number of methods used for reporting

the same. Some of them can be explained below;

Budgeting reports: The main aim of these reports is to compare the company's actual

performance with that of budgeted or standard performance for a particular period. Budget is

made by taking last year's data and taking the average of three to five years. But, an impressive

budget is one that also include unforeseen situations that may arise in the future (Novas, Alves

and Sousa, A., 2017). It comprises of all the revenues as well as expenditures that will aids them

to reach closer to their standard performance. This report is helpful for the manager's to measure

fruitful for them in enhancing their productivity and become more creditable. This will

ultimately be beneficial for them to become leader in their industry.

It is important to understand the different management accounting system in to generate

significant information to become profitable. The some of the various types of management

accounting can be explained in detail below:

Cost accounting system: This is important system as it aids to make an accurate estimates for

making crucial decisions including ways to minimizing cost by eliminating unproductive

expenses and maximizing their profitability (Phan, Baird and Su, 2017). Adding to this, it is also

fruitful for doing accurate estimates to determine the closing stock with respect to raw material,

work in progress and final goods.

Inventory management system: This is basically defined as the computer based system to

record, update and monitor the company's stocks that includes closing inventory amounts, sales,

orders and deliveries. Many Organization has implemented this system in order to balance their

inventory by recording the information in a organized and systematic manner.

P2 Explain different methods used for management accounting reporting

Management accounting is also called by another name as cost accounting. It focuses on

engaging attention to account for financial information of the previous year. It is important for

the firm to generate relevant information that helps them to analyze their performance and take

corrective actions that is essential for their growth. It is vital to include factors such as it's

usefulness,timeless and completeness. The report is mainly used to plan, engage in regulating all

their activities at each steps by crucial decision-making by measuring performance and doing the

improvement needed to enhance their processes. There are number of methods used for reporting

the same. Some of them can be explained below;

Budgeting reports: The main aim of these reports is to compare the company's actual

performance with that of budgeted or standard performance for a particular period. Budget is

made by taking last year's data and taking the average of three to five years. But, an impressive

budget is one that also include unforeseen situations that may arise in the future (Novas, Alves

and Sousa, A., 2017). It comprises of all the revenues as well as expenditures that will aids them

to reach closer to their standard performance. This report is helpful for the manager's to measure

the performance of each of their talented force and accordingly provide them incentives in order

to sustain as well as further improve their performance.

Account receivable aging report: This report's purpose can be implied by it's name itself. It

keeps a record of each of the outstanding balances in turn keeping record of their receivable and

it's level of important on the type of activities company is engaged in. It is very crucial for their

catering business. It states the issues faced by them in their collection process. This report will

aid the company to identify their defaulters and generate information with respect of their credit

worthiness. This further helps them to know their liquidity position and accordingly make

changes in their credit policy.

Cost managerial accounting reports: This report consists of all the cost the goods that are

manufactured by them. These cost mainly includes raw material, direct material, direct labour

and overhead expenses (Joshi and Li, 2016). The total costs arrived is divided by total amount

of productions. This measures helps to determine profit and to estimate profit margins.

Performance reports: This reports is created to monitor the performance of each of it's

department. It helps the managers to plan and implement powerful strategies that are essential

for the growth of their organisation. Individual, who perform well are rewarded that is vital for

ensuring that they are able to sustain their performance. While, under performers are either laid

off or one who have a higher potential are motivated to become efficient to be able to arrive at

their standard performance.

Other Managerial accounting reports: This report includes all the other that are not mentioned

under specific heads but are vital for their smooth and easier operations. These mainly includes

Order information report, competitor analysis reports and other related reports. They are either

generated within the organization or outsourced, by selecting the most appropriate method that

minimizes their cost (Amara and Benelifa, 2017). It is crucial to access are highly reliable in

generating the most creditable as well as authentic reports.

to sustain as well as further improve their performance.

Account receivable aging report: This report's purpose can be implied by it's name itself. It

keeps a record of each of the outstanding balances in turn keeping record of their receivable and

it's level of important on the type of activities company is engaged in. It is very crucial for their

catering business. It states the issues faced by them in their collection process. This report will

aid the company to identify their defaulters and generate information with respect of their credit

worthiness. This further helps them to know their liquidity position and accordingly make

changes in their credit policy.

Cost managerial accounting reports: This report consists of all the cost the goods that are

manufactured by them. These cost mainly includes raw material, direct material, direct labour

and overhead expenses (Joshi and Li, 2016). The total costs arrived is divided by total amount

of productions. This measures helps to determine profit and to estimate profit margins.

Performance reports: This reports is created to monitor the performance of each of it's

department. It helps the managers to plan and implement powerful strategies that are essential

for the growth of their organisation. Individual, who perform well are rewarded that is vital for

ensuring that they are able to sustain their performance. While, under performers are either laid

off or one who have a higher potential are motivated to become efficient to be able to arrive at

their standard performance.

Other Managerial accounting reports: This report includes all the other that are not mentioned

under specific heads but are vital for their smooth and easier operations. These mainly includes

Order information report, competitor analysis reports and other related reports. They are either

generated within the organization or outsourced, by selecting the most appropriate method that

minimizes their cost (Amara and Benelifa, 2017). It is crucial to access are highly reliable in

generating the most creditable as well as authentic reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

It is must for “Connecting Catering Services U.K' to have a thorough understanding of

the technique that is most appropriate for them. There are very techniques and their usefulness is

highly dependent on the nature and size of different company (Alsharari and Al-Shboul, 2019).

As this project, emphasizes more absorption and marginal costing so, it's explanation is detailed

below for it's better understanding.

Marginal Costing: This costing comprises of all those cost that includes at the start when the

company is established. There have variety of benefits that they include bifurcating the cost into

fixed and variable. This help in appropriate computation of cost and helps in determine

profitability. Thereby, identifying their profit margin and taking the necessary steps for it's

improvement.

Absorption Costing: This basically includes all the cost that are associated with expenses that

are incurred in connection with direct material, direct labour and overhead expenses. It is must

for them to follow all the requirement of generality accepted accounting principles(G.A.A.P).

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

It is must for “Connecting Catering Services U.K' to have a thorough understanding of

the technique that is most appropriate for them. There are very techniques and their usefulness is

highly dependent on the nature and size of different company (Alsharari and Al-Shboul, 2019).

As this project, emphasizes more absorption and marginal costing so, it's explanation is detailed

below for it's better understanding.

Marginal Costing: This costing comprises of all those cost that includes at the start when the

company is established. There have variety of benefits that they include bifurcating the cost into

fixed and variable. This help in appropriate computation of cost and helps in determine

profitability. Thereby, identifying their profit margin and taking the necessary steps for it's

improvement.

Absorption Costing: This basically includes all the cost that are associated with expenses that

are incurred in connection with direct material, direct labour and overhead expenses. It is must

for them to follow all the requirement of generality accepted accounting principles(G.A.A.P).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

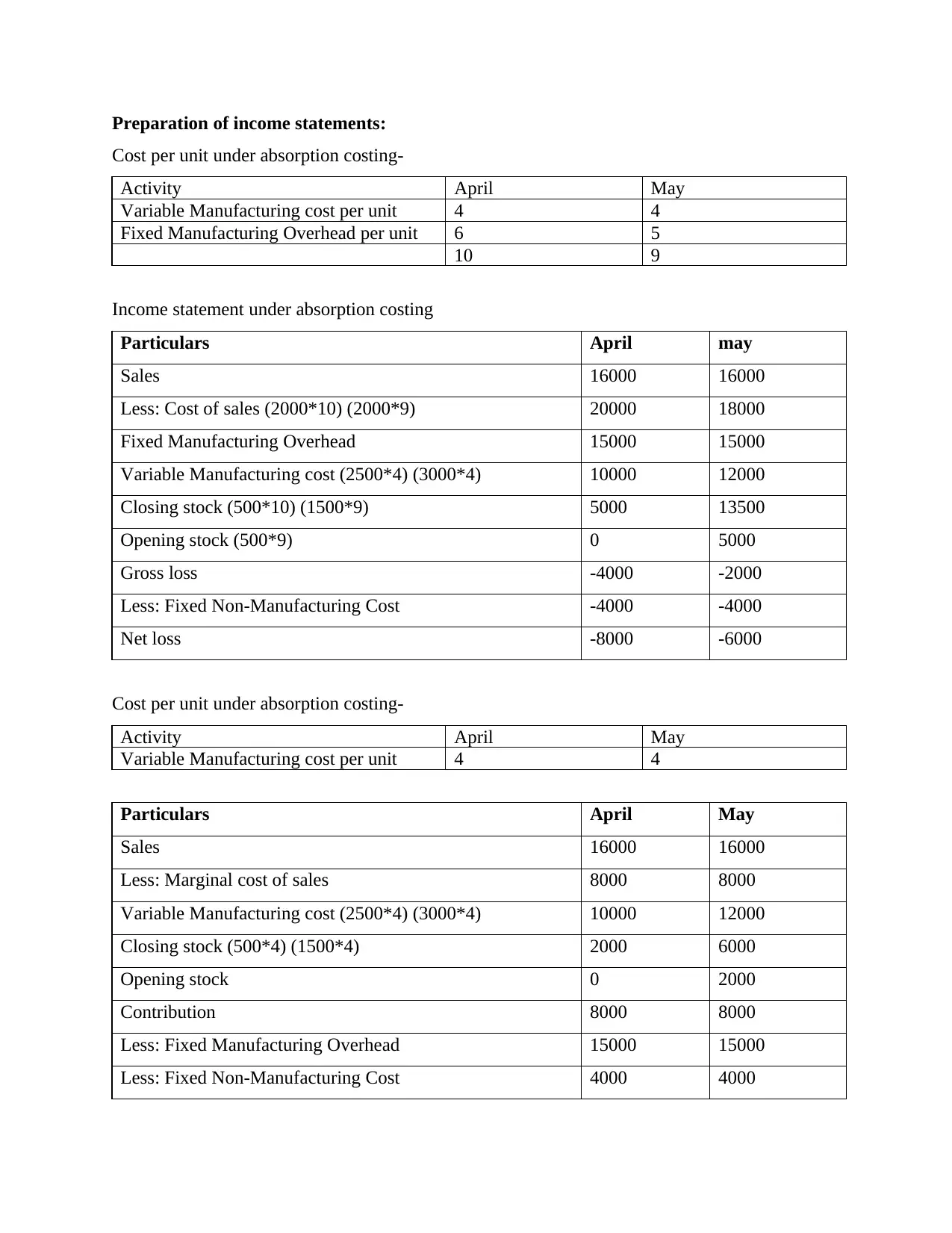

Preparation of income statements:

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

10 9

Income statement under absorption costing

Particulars April may

Sales 16000 16000

Less: Cost of sales (2000*10) (2000*9) 20000 18000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*10) (1500*9) 5000 13500

Opening stock (500*9) 0 5000

Gross loss -4000 -2000

Less: Fixed Non-Manufacturing Cost -4000 -4000

Net loss -8000 -6000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April May

Sales 16000 16000

Less: Marginal cost of sales 8000 8000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*4) (1500*4) 2000 6000

Opening stock 0 2000

Contribution 8000 8000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non-Manufacturing Cost 4000 4000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Fixed Manufacturing Overhead per unit 6 5

10 9

Income statement under absorption costing

Particulars April may

Sales 16000 16000

Less: Cost of sales (2000*10) (2000*9) 20000 18000

Fixed Manufacturing Overhead 15000 15000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*10) (1500*9) 5000 13500

Opening stock (500*9) 0 5000

Gross loss -4000 -2000

Less: Fixed Non-Manufacturing Cost -4000 -4000

Net loss -8000 -6000

Cost per unit under absorption costing-

Activity April May

Variable Manufacturing cost per unit 4 4

Particulars April May

Sales 16000 16000

Less: Marginal cost of sales 8000 8000

Variable Manufacturing cost (2500*4) (3000*4) 10000 12000

Closing stock (500*4) (1500*4) 2000 6000

Opening stock 0 2000

Contribution 8000 8000

Less: Fixed Manufacturing Overhead 15000 15000

Less: Fixed Non-Manufacturing Cost 4000 4000

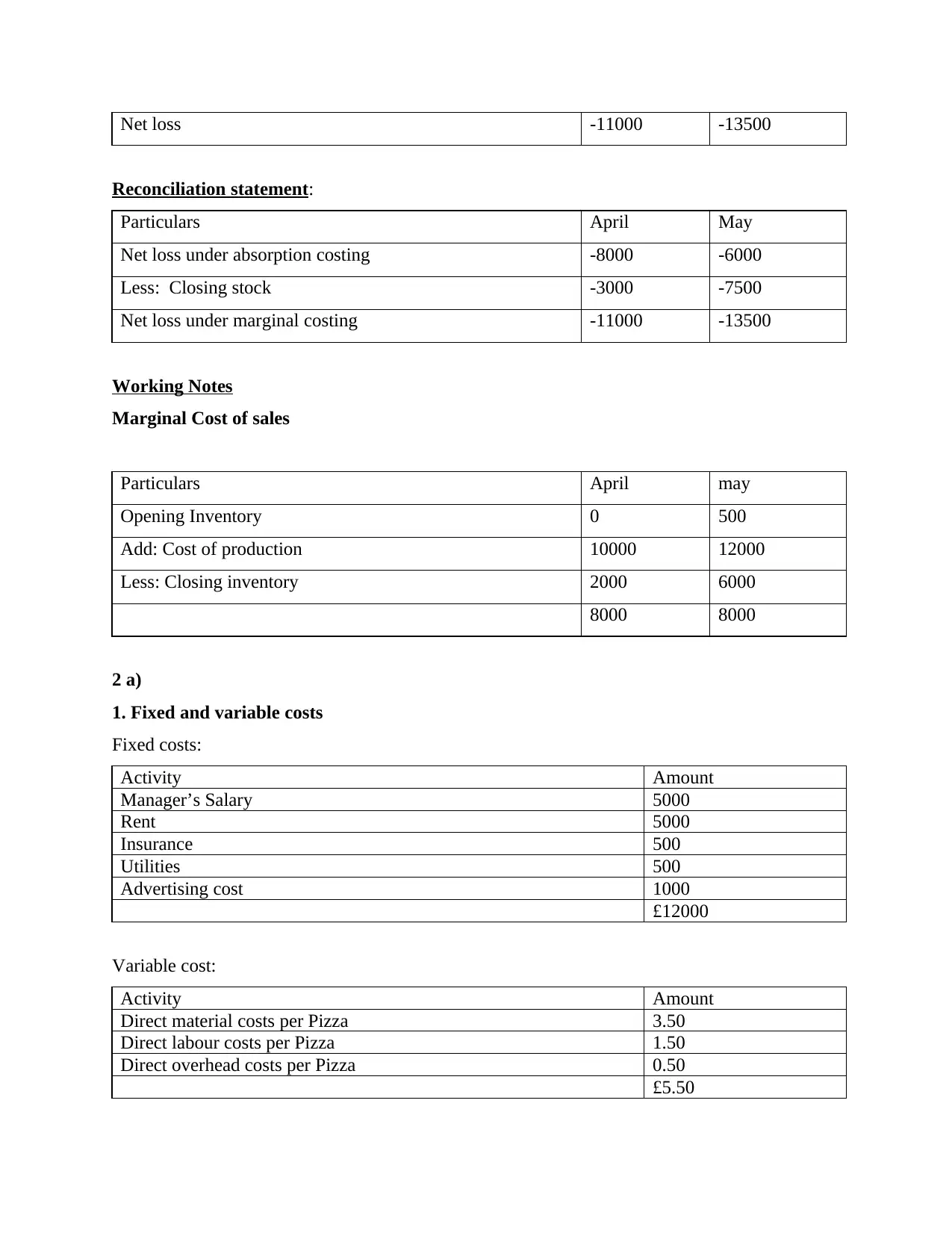

Net loss -11000 -13500

Reconciliation statement:

Particulars April May

Net loss under absorption costing -8000 -6000

Less: Closing stock -3000 -7500

Net loss under marginal costing -11000 -13500

Working Notes

Marginal Cost of sales

Particulars April may

Opening Inventory 0 500

Add: Cost of production 10000 12000

Less: Closing inventory 2000 6000

8000 8000

2 a)

1. Fixed and variable costs

Fixed costs:

Activity Amount

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£12000

Variable cost:

Activity Amount

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£5.50

Reconciliation statement:

Particulars April May

Net loss under absorption costing -8000 -6000

Less: Closing stock -3000 -7500

Net loss under marginal costing -11000 -13500

Working Notes

Marginal Cost of sales

Particulars April may

Opening Inventory 0 500

Add: Cost of production 10000 12000

Less: Closing inventory 2000 6000

8000 8000

2 a)

1. Fixed and variable costs

Fixed costs:

Activity Amount

Manager’s Salary 5000

Rent 5000

Insurance 500

Utilities 500

Advertising cost 1000

£12000

Variable cost:

Activity Amount

Direct material costs per Pizza 3.50

Direct labour costs per Pizza 1.50

Direct overhead costs per Pizza 0.50

£5.50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

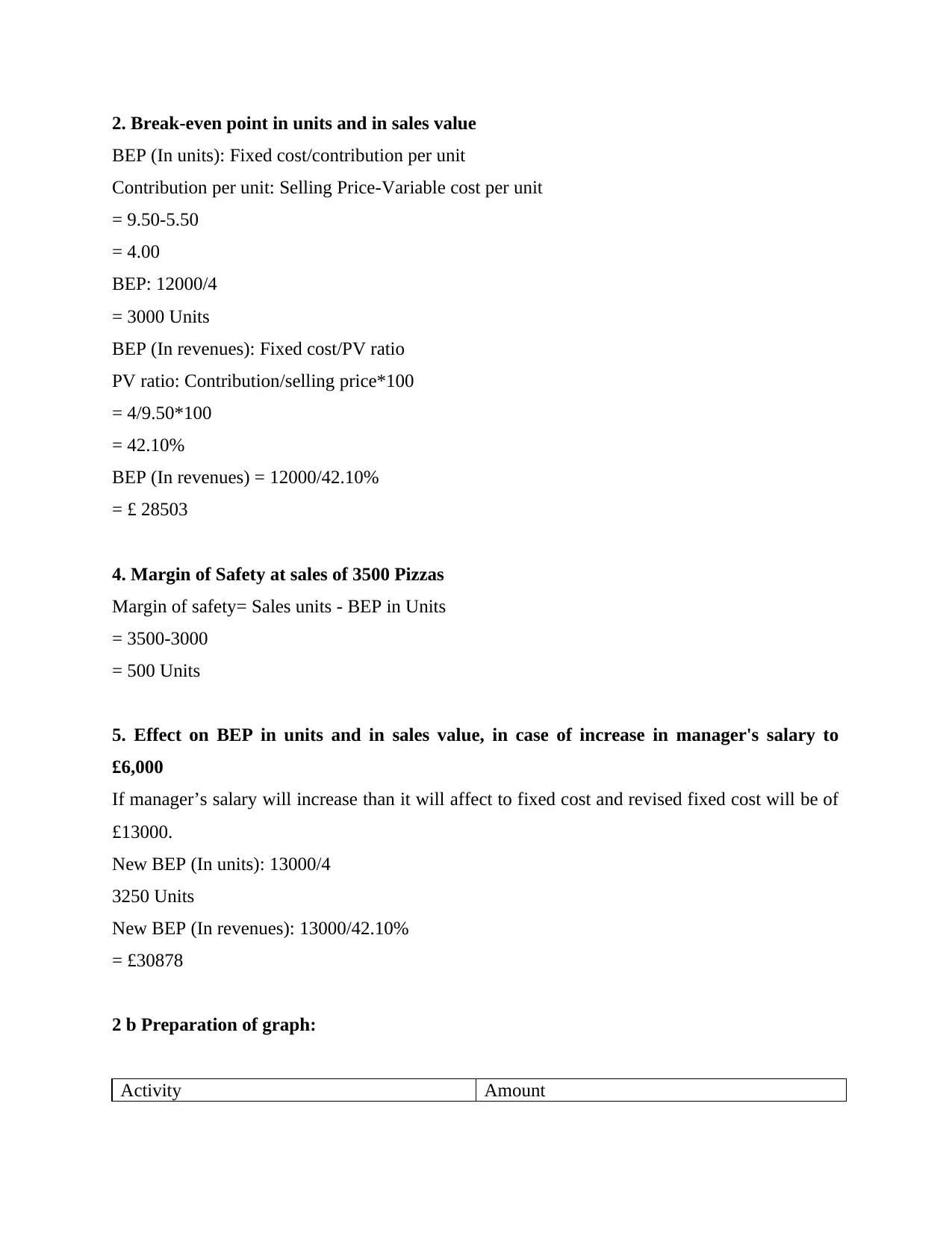

2. Break-even point in units and in sales value

BEP (In units): Fixed cost/contribution per unit

Contribution per unit: Selling Price-Variable cost per unit

= 9.50-5.50

= 4.00

BEP: 12000/4

= 3000 Units

BEP (In revenues): Fixed cost/PV ratio

PV ratio: Contribution/selling price*100

= 4/9.50*100

= 42.10%

BEP (In revenues) = 12000/42.10%

= £ 28503

4. Margin of Safety at sales of 3500 Pizzas

Margin of safety= Sales units - BEP in Units

= 3500-3000

= 500 Units

5. Effect on BEP in units and in sales value, in case of increase in manager's salary to

£6,000

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000/4

3250 Units

New BEP (In revenues): 13000/42.10%

= £30878

2 b Preparation of graph:

Activity Amount

BEP (In units): Fixed cost/contribution per unit

Contribution per unit: Selling Price-Variable cost per unit

= 9.50-5.50

= 4.00

BEP: 12000/4

= 3000 Units

BEP (In revenues): Fixed cost/PV ratio

PV ratio: Contribution/selling price*100

= 4/9.50*100

= 42.10%

BEP (In revenues) = 12000/42.10%

= £ 28503

4. Margin of Safety at sales of 3500 Pizzas

Margin of safety= Sales units - BEP in Units

= 3500-3000

= 500 Units

5. Effect on BEP in units and in sales value, in case of increase in manager's salary to

£6,000

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New BEP (In units): 13000/4

3250 Units

New BEP (In revenues): 13000/42.10%

= £30878

2 b Preparation of graph:

Activity Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed CostCompanies prepare cost

budget which is used to find variance in

actual cost incurred and budgeted target. Cost

budgets shall be flexible enough to

incorporate changes in targets as and when

they arise.

12000

BEP point 28503

Flexible budget

Items Actual Budgeted Variance

Sales price 10 9.50 .50 Favourable

Sales units 12000 10000 2000 Favourable

Revenues 120000 95000 25000 Favourable

Fixed cost 15000 12000 3000 Adverse

Variable cost 5 5.50 .50 Favourable

From this financial information, it can be interpret is company is quite closer to it's standard

performance. It needs to just concentrate on doing a gap analysis on their fixed cost in order to

be able to realize it's objectives.

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed CostCompanies prepare cost

budget which is used to find variance in

actual cost incurred and budgeted target. Cost

budgets shall be flexible enough to

incorporate changes in targets as and when

they arise.

12000

BEP point 28503

Flexible budget

Items Actual Budgeted Variance

Sales price 10 9.50 .50 Favourable

Sales units 12000 10000 2000 Favourable

Revenues 120000 95000 25000 Favourable

Fixed cost 15000 12000 3000 Adverse

Variable cost 5 5.50 .50 Favourable

From this financial information, it can be interpret is company is quite closer to it's standard

performance. It needs to just concentrate on doing a gap analysis on their fixed cost in order to

be able to realize it's objectives.

Task3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control

Planing tools is defined as tools that track the performance of each of their department at

every stage. It is must for identifying the gap analysis and taking immediate corrective actions

by implementing by way of initiating program that helps to address the issues and take

sustainable measures to realize their aims . It is must for them to a very effective budget have

increases the efficiency as well as effectiveness of organization as a whole (Collis and Hussey,

2017). They comprises of diverse tools that includes pricing strategies, budget, implementing

powerful and effective strategies that enhances customer satisfaction. Some of the main planning

tools can be explained below in detail:

Cash Budget: It is the budget that comprises of all expected or standard revenues and expenses.

It is mainly report for estimating the cash that will be available in the near future.

Advantages:

It helps them in carefully monitoring their actual cash inflow and utilize their cash

effectively. It is even helpful as it acts as an provision meet any cash deficiencies that may arise

in the future and identify it's cash position in the future.

Disadvantages:

It's one of the major demerit is that , cash budget it is highly dependent on the accuracy of

it's estimates. Adding to it, it is highly inflexible and faces difficulty in changing as per dynamic

situations arising in the market.pestle analysis of marks and spencer

Variance analysis: It helps to provide a detailed summary of actual performance in comparison to

that of it's planned or standard performance.

Advantages:

This technique helps in breaking down the cost and in turn is simpler to understanding

wherein budgetary control can be possible (Malina, 2017). It is easier for mangers to take

efficient as well as taking sustainable measures for their future growth.

Disadvantages:

The main disadvantage of variance analysis is that it is very much time consuming as it

takes a longer time and monitoring this tool delays in making appropriate changes.

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control

Planing tools is defined as tools that track the performance of each of their department at

every stage. It is must for identifying the gap analysis and taking immediate corrective actions

by implementing by way of initiating program that helps to address the issues and take

sustainable measures to realize their aims . It is must for them to a very effective budget have

increases the efficiency as well as effectiveness of organization as a whole (Collis and Hussey,

2017). They comprises of diverse tools that includes pricing strategies, budget, implementing

powerful and effective strategies that enhances customer satisfaction. Some of the main planning

tools can be explained below in detail:

Cash Budget: It is the budget that comprises of all expected or standard revenues and expenses.

It is mainly report for estimating the cash that will be available in the near future.

Advantages:

It helps them in carefully monitoring their actual cash inflow and utilize their cash

effectively. It is even helpful as it acts as an provision meet any cash deficiencies that may arise

in the future and identify it's cash position in the future.

Disadvantages:

It's one of the major demerit is that , cash budget it is highly dependent on the accuracy of

it's estimates. Adding to it, it is highly inflexible and faces difficulty in changing as per dynamic

situations arising in the market.pestle analysis of marks and spencer

Variance analysis: It helps to provide a detailed summary of actual performance in comparison to

that of it's planned or standard performance.

Advantages:

This technique helps in breaking down the cost and in turn is simpler to understanding

wherein budgetary control can be possible (Malina, 2017). It is easier for mangers to take

efficient as well as taking sustainable measures for their future growth.

Disadvantages:

The main disadvantage of variance analysis is that it is very much time consuming as it

takes a longer time and monitoring this tool delays in making appropriate changes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.