Evaluation of Management Accounting Systems and Reporting at Tesco

VerifiedAdded on 2021/02/19

|15

|3910

|87

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within Tesco. It begins by defining management accounting and emphasizing the significance of its systems, including inventory management, job costing, and price optimization. The report then explores various reporting methods, such as performance reports, accounts receivable reports, and budget reports. It evaluates the benefits and applications of these management accounting systems, highlighting their impact on operational efficiency and profitability. Furthermore, the report analyzes planning tools like activity-based costing and breakeven analysis, assessing their effectiveness in organizational decision-making. Finally, the report provides a computation of net profit using both marginal and absorption costing methods, offering a comprehensive overview of management accounting practices within a real-world business context. The report is a valuable resource for students seeking insights into accounting principles and their practical applications.

Management & Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

PART 1............................................................................................................................................3

a. Explaining the concept of management accounting and the importance of management

accounting systems......................................................................................................................3

b. Explaining various methods that can be used for management accounting reporting............4

c. Evaluating the benefits and the application of the MA systems..............................................5

d. Evaluating the integration between management accounting systems and reporting.............6

PART 2............................................................................................................................................7

Analyzing different planning tools and its effectiveness in the organization..............................7

TASK 2............................................................................................................................................8

PART 1............................................................................................................................................8

Computation of net profit by applying both marginal and absorption costing method...............8

PART 2..........................................................................................................................................11

CONCLUSION..............................................................................................................................12

TASK 1............................................................................................................................................3

PART 1............................................................................................................................................3

a. Explaining the concept of management accounting and the importance of management

accounting systems......................................................................................................................3

b. Explaining various methods that can be used for management accounting reporting............4

c. Evaluating the benefits and the application of the MA systems..............................................5

d. Evaluating the integration between management accounting systems and reporting.............6

PART 2............................................................................................................................................7

Analyzing different planning tools and its effectiveness in the organization..............................7

TASK 2............................................................................................................................................8

PART 1............................................................................................................................................8

Computation of net profit by applying both marginal and absorption costing method...............8

PART 2..........................................................................................................................................11

CONCLUSION..............................................................................................................................12

INTRODUCTION

Management accounting refers to the process for analyzing the cost of the business and

the operations for preparing the financial reports for the internal management. This helps the

managers in the process of decision making for achieving the business goals. Management

accounting is an act of formulating the financial and the costing data then converting this data

into the useful information for the management staff and the executives within organization. The

present study is based on Tesco, the largest multinational groceries and also the general

merchandise company. Furthermore, the study provides the deep insights relating to the systems

and the methods under the management accounting. The study also facilitates focus on the

different planning tools and the computation of the net profit by using the marginal and the

absorption costing technique.

TASK 1

PART 1

a. Explaining the concept of management accounting and the importance of management

accounting systems.

Management accounting means the practice of identifying, recording, classifying,

analyzing and presenting the financial information which helps the internal management of

Tesco in making the suitable business decisions in context of the future needs (Alamri, 2019).

Unlike the financial accounting, management accounting does not require any kind of auditing

and in complying with the standards. This accounting is not compulsory or mandatory for the

managers to prepare and it reflects the budgeting and the information in relation to the

management aspects. Management accounting facilitatesfor the detailed report in respect of the

profits that are gained from the product, customer, product line, and the geographic region

whereas financial accounting provides for the reporting of results for the whole business of

Tesco.

Essential requirements of different management accounting systems-

Inventory management accounting system-This system traces the goods by using the supply

chain or by the part of it in which Tesco operates its business. It keeps the track of the movement

of goods from the warehouse to delivering it to the ultimate consumers. The essential

requirement of this system for Tesco is to manage its inventory and ensuring proper control over

it.

Job costing system- This system of the management accounting keeps an account for all the

direct and the indirect cost that is involved in each job. It is the system which facilitates the

Management accounting refers to the process for analyzing the cost of the business and

the operations for preparing the financial reports for the internal management. This helps the

managers in the process of decision making for achieving the business goals. Management

accounting is an act of formulating the financial and the costing data then converting this data

into the useful information for the management staff and the executives within organization. The

present study is based on Tesco, the largest multinational groceries and also the general

merchandise company. Furthermore, the study provides the deep insights relating to the systems

and the methods under the management accounting. The study also facilitates focus on the

different planning tools and the computation of the net profit by using the marginal and the

absorption costing technique.

TASK 1

PART 1

a. Explaining the concept of management accounting and the importance of management

accounting systems.

Management accounting means the practice of identifying, recording, classifying,

analyzing and presenting the financial information which helps the internal management of

Tesco in making the suitable business decisions in context of the future needs (Alamri, 2019).

Unlike the financial accounting, management accounting does not require any kind of auditing

and in complying with the standards. This accounting is not compulsory or mandatory for the

managers to prepare and it reflects the budgeting and the information in relation to the

management aspects. Management accounting facilitatesfor the detailed report in respect of the

profits that are gained from the product, customer, product line, and the geographic region

whereas financial accounting provides for the reporting of results for the whole business of

Tesco.

Essential requirements of different management accounting systems-

Inventory management accounting system-This system traces the goods by using the supply

chain or by the part of it in which Tesco operates its business. It keeps the track of the movement

of goods from the warehouse to delivering it to the ultimate consumers. The essential

requirement of this system for Tesco is to manage its inventory and ensuring proper control over

it.

Job costing system- This system of the management accounting keeps an account for all the

direct and the indirect cost that is involved in each job. It is the system which facilitates the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information regarding the revenues and the cost which in turn leads to reporting of the

standardized profitability of the business. This system is essential for Tesco in maintaining the

information relating to the cost of each job and accordingly developing control over the

unnecessary expenses.

Price optimization system-It is the mathematical tool that is used to determine the response

of the customers towards different price set up for the products and the services of the company.

It is the system that allows for setting the best price for meeting the goals like profit

maximization (Chenhalland Moers, 2015). The data that is used in this technique involves

operating cost, historic sales, inventories and survey data. The essential requirement of this

system is that it fix the price that is good for both potential buyers and the company.

Cost accounting system- It refers to the system that is used by Tesco in estimating the

appropriate cost for their product so that profit can be analyzed, inventory can be valued and

could keep control over the cost. It is important for the enterprise in terms of keeping the

operations profitable. It helps in ascertaining the accurate cost involved in producing the product.

This system is required by Tesco for ascertaining the cost involved in producing its product and

keeping control over the spending. The two major cost accounting systems are job costing and

process costing system.

Job order costing- It is the system of cost accounting that helps in assigning the

manufacturing cost for each job. This process is labor intensive as he cost is accumulated

for each of the job. Tesco can use this approach for its unique products like the consulting

projects or the custom designed machinery etc.

Process costing- It is an accounting system that accumulates or assigns the

manufacturing cost to each process. It is the most appropriate technique for the firm when

its production process involves several divisions and the flow of cost from one division to

the other.

b. Explaining various methods that can be used for management accounting reporting.

Management accounting reporting plays a crucial role in assessing the performance of the

business. Essential strategic insights can be developed by preparing the reports regarding the

cost, inventory, budget and other managerial aspects. Various reports that are framed by the

manager’s are-

Performance reports- This report of management accounting is created for reviewing the

performance of Tesco as well as the performance of its employees in performing the task as per

the standard set. Performance report is used by the managers in making the strategic decisions

relating to the future needs of the enterprise (Curry, 2019). This report plays a vital role in

keeping a relevant measure of the strategy towards the mission and the vision of Tesco.

standardized profitability of the business. This system is essential for Tesco in maintaining the

information relating to the cost of each job and accordingly developing control over the

unnecessary expenses.

Price optimization system-It is the mathematical tool that is used to determine the response

of the customers towards different price set up for the products and the services of the company.

It is the system that allows for setting the best price for meeting the goals like profit

maximization (Chenhalland Moers, 2015). The data that is used in this technique involves

operating cost, historic sales, inventories and survey data. The essential requirement of this

system is that it fix the price that is good for both potential buyers and the company.

Cost accounting system- It refers to the system that is used by Tesco in estimating the

appropriate cost for their product so that profit can be analyzed, inventory can be valued and

could keep control over the cost. It is important for the enterprise in terms of keeping the

operations profitable. It helps in ascertaining the accurate cost involved in producing the product.

This system is required by Tesco for ascertaining the cost involved in producing its product and

keeping control over the spending. The two major cost accounting systems are job costing and

process costing system.

Job order costing- It is the system of cost accounting that helps in assigning the

manufacturing cost for each job. This process is labor intensive as he cost is accumulated

for each of the job. Tesco can use this approach for its unique products like the consulting

projects or the custom designed machinery etc.

Process costing- It is an accounting system that accumulates or assigns the

manufacturing cost to each process. It is the most appropriate technique for the firm when

its production process involves several divisions and the flow of cost from one division to

the other.

b. Explaining various methods that can be used for management accounting reporting.

Management accounting reporting plays a crucial role in assessing the performance of the

business. Essential strategic insights can be developed by preparing the reports regarding the

cost, inventory, budget and other managerial aspects. Various reports that are framed by the

manager’s are-

Performance reports- This report of management accounting is created for reviewing the

performance of Tesco as well as the performance of its employees in performing the task as per

the standard set. Performance report is used by the managers in making the strategic decisions

relating to the future needs of the enterprise (Curry, 2019). This report plays a vital role in

keeping a relevant measure of the strategy towards the mission and the vision of Tesco.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts receivable reports- This report refers to the detailed information in context of

the credit that is provided by Tescoto its customers and other creditors. It helps the firm in

adjusting the credit policies in order to align them to the repayment capability of the customers.

Costing reports- This report provides for the accrual of the cost in a particular project in

comparison with the budgeted or the expected revenue generated by that particular project. It

helps the managers of Tesco in evaluating the profitability associated with the specific kind of

the job and to optimize the operations of their business by emphasizing on jobs that are tend to

be most profitable.

Inventory report- In this report the records relating to the inventory of the enterprise are

maintained and the combination of technology is used for managing the inventory. This report

helps in centralizing the data on the cost of the inventory, labor cost and other overhead cost that

is involved in production process, facilitates the raw data for optimizing the machining or the

assembly.

Budget report- This report includes the preparation of the budget in relation to all the

activities of Tesco and is considered as the most important report of the managerial accounting.

It enables the owners of the business in understanding and controlling the costs of the enterprise

by providing the budgeted figures for several departments within the organization (Hopper and

Bui, 2016). Through this report estimation regarding the future budget is possible and also helps

in finding the places for cutting down the cost.

Thus, it is important for Tesco to choose the right type of the report which helps in

achieving the goals more effectively and efficiently. Through these reports, deeper insights can

be attained in capturing the opportunities in the overall marketplace.

c. Evaluating the benefits and the application of the MA systems.

Various benefits and applications are attached with the application of the management

accounting systems for Tesco as follows-

Inventory management system-

Benefits- This system assists the organization in achieving the efficiency and the

productivity in the operations of the business. This system helps in carrying out the smooth

functioning of the operations. It minimizes the cost and strives for maximizing the sales and the

profits by managing the orders at the various sales channels.

Application- Inventory management system is used for integrating the entire business of

Tesco. It allows the company in meeting its sales target as it makes the way for fulfilling the

revenue of the business.

Job costing system-

the credit that is provided by Tescoto its customers and other creditors. It helps the firm in

adjusting the credit policies in order to align them to the repayment capability of the customers.

Costing reports- This report provides for the accrual of the cost in a particular project in

comparison with the budgeted or the expected revenue generated by that particular project. It

helps the managers of Tesco in evaluating the profitability associated with the specific kind of

the job and to optimize the operations of their business by emphasizing on jobs that are tend to

be most profitable.

Inventory report- In this report the records relating to the inventory of the enterprise are

maintained and the combination of technology is used for managing the inventory. This report

helps in centralizing the data on the cost of the inventory, labor cost and other overhead cost that

is involved in production process, facilitates the raw data for optimizing the machining or the

assembly.

Budget report- This report includes the preparation of the budget in relation to all the

activities of Tesco and is considered as the most important report of the managerial accounting.

It enables the owners of the business in understanding and controlling the costs of the enterprise

by providing the budgeted figures for several departments within the organization (Hopper and

Bui, 2016). Through this report estimation regarding the future budget is possible and also helps

in finding the places for cutting down the cost.

Thus, it is important for Tesco to choose the right type of the report which helps in

achieving the goals more effectively and efficiently. Through these reports, deeper insights can

be attained in capturing the opportunities in the overall marketplace.

c. Evaluating the benefits and the application of the MA systems.

Various benefits and applications are attached with the application of the management

accounting systems for Tesco as follows-

Inventory management system-

Benefits- This system assists the organization in achieving the efficiency and the

productivity in the operations of the business. This system helps in carrying out the smooth

functioning of the operations. It minimizes the cost and strives for maximizing the sales and the

profits by managing the orders at the various sales channels.

Application- Inventory management system is used for integrating the entire business of

Tesco. It allows the company in meeting its sales target as it makes the way for fulfilling the

revenue of the business.

Job costing system-

Benefits- It provides for the details regarding the type of the cost that is present in the

manufacturing process. This involves the labor cost, overhead charges and the direct cost. It

determines the profitability for each job that helps the probable customers for deciding the job

feasibility.

Application- It is used for evaluating the work quality by using several statistical

methods. This method helps Tesco in computing the cost overheads for meeting the particular

needs in the precise manner.

Price optimization system-

Benefits-It is the strategy that helps the company in knowing the business for retaining

the customers and in earning the profitability. It helps in assessing the demand for the product

and the services.

Application- This system is useful for measuring the suitable price level for delivering

the products to the ultimate consumers. By using this technique an entity can create large

customer base which in turn increases the sales and also the profitability within the business

(Horton and de Araujo Wanderley, 2018). It is the only management system which acts as the

mathematical tool for setting up the optimum price and in allocating the financial resources in

profitable ventures.

Cost accounting system-

Benefits- This system helps in measuring and continuous improvement in the efficiency

of Tesco. It throws the highlights on the activities that brings profits into the business and

identifies those activities that inculcate losses. Cost accounting system helps Tesco in fixing the

prices based on its production cost.

Application- Cost accounting system is used by Tesco in ascertaining the cost involved

and reducing the unnecessary cost so that optimum use of the resources can be possible.

d. Evaluating the integration between management accounting systems and reporting.

The integration between management system and reporting is that systems allows for the

effective reporting regarding the cost, performance, budget and receivable information to the

organization so that standards set can be compared with the actual and if any deviation present

could be resolved by taking the appropriate measures (Latan and et.al., 2018). Reporting forms

the set of the financial as well as the non-financial measures of the performance as it providing

the detailed level of information relating to the internal management activities within the Tesco.

Systems provide algorithm for computing the reporting indicators. Thus, both are interlinked and

play a vital role in managing the operations and the activities in efficient and effective manner.

manufacturing process. This involves the labor cost, overhead charges and the direct cost. It

determines the profitability for each job that helps the probable customers for deciding the job

feasibility.

Application- It is used for evaluating the work quality by using several statistical

methods. This method helps Tesco in computing the cost overheads for meeting the particular

needs in the precise manner.

Price optimization system-

Benefits-It is the strategy that helps the company in knowing the business for retaining

the customers and in earning the profitability. It helps in assessing the demand for the product

and the services.

Application- This system is useful for measuring the suitable price level for delivering

the products to the ultimate consumers. By using this technique an entity can create large

customer base which in turn increases the sales and also the profitability within the business

(Horton and de Araujo Wanderley, 2018). It is the only management system which acts as the

mathematical tool for setting up the optimum price and in allocating the financial resources in

profitable ventures.

Cost accounting system-

Benefits- This system helps in measuring and continuous improvement in the efficiency

of Tesco. It throws the highlights on the activities that brings profits into the business and

identifies those activities that inculcate losses. Cost accounting system helps Tesco in fixing the

prices based on its production cost.

Application- Cost accounting system is used by Tesco in ascertaining the cost involved

and reducing the unnecessary cost so that optimum use of the resources can be possible.

d. Evaluating the integration between management accounting systems and reporting.

The integration between management system and reporting is that systems allows for the

effective reporting regarding the cost, performance, budget and receivable information to the

organization so that standards set can be compared with the actual and if any deviation present

could be resolved by taking the appropriate measures (Latan and et.al., 2018). Reporting forms

the set of the financial as well as the non-financial measures of the performance as it providing

the detailed level of information relating to the internal management activities within the Tesco.

Systems provide algorithm for computing the reporting indicators. Thus, both are interlinked and

play a vital role in managing the operations and the activities in efficient and effective manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 2

Analyzing different planning tools and its effectiveness in the organization

Activity based costing- It is the methodology that is used precisely for allocating the

overhead cost to each of the activity involved in the business. After assigning the cost to

activities cost could be assigned to cost objects which uses the activities to which it is assigned.

This system helps is effective for reducing the cost relating to the overhead. This technique tends

to be more effective in the complex business environments faced by Tesco such as the staff has

to deal with different machines, products and the processes which requires skills (Maas,

Schalteggerand Crutzen, 2016). ABC is the planning tool that is designed for tracing the cost

incurred in the activities. It facilitates the better information regarding the profitability and cost

of distribution. It is an excellent tool in measuring the specific cost in relation to activity which

in turn helps in reaching the objective of cost reduction for the management of Tesco. It provides

for the unnecessary cost involved in the activity and suggests measures for elimination such cost.

It facilitates correct evaluation of the profits, margins ascertained for product and in overall

operations of Tesco.

Breakeven analysis-It is technique that refers to the examination and the evaluation of

safety margins for Tesco on the basis of the revenue collected and attached to the cost. Assessing

the different level of the price in relation to several levels of the demand that the business uses

this technique for determining required level of the sales for covering out the entire fixed cost

incurred by the enterprise. It tells the company about the level of the investment that it should

reach for recovering the initial outlay. Specifically break even analysis is used by an entity as the

metric and the computation of the margin of safety in context of achieving the target of the

desired sales. It is the most effective technique as it tells about the current performance of the

company and helps in forecasting the future estimations relating the cash requirements.

Benchmarking- This planning tool is counted as best for attaining the excellence in the

performance and reaching the competitive edge against the competitors that has been adopted by

Tesco. It helps in knowing the strategies, products and the processes that are considered best in

the overall market so that competencies can be created.It is the practice of measuring the

company’s performance in terms of its products, processes and services with that of another

business that is been considered as the best in the overall industry or the market (Messner, 2016).

It resolves the financial problems in identifying the internal opportunities so that better

improvement can be attained.It is said to be the effective tool as it helps in improving the quality

in the products and the services f the organization on a continuous basis. It assists the firm in

leading towards better performance with cost efficiency and allows for determining the areas that

needs improvement.

Analyzing different planning tools and its effectiveness in the organization

Activity based costing- It is the methodology that is used precisely for allocating the

overhead cost to each of the activity involved in the business. After assigning the cost to

activities cost could be assigned to cost objects which uses the activities to which it is assigned.

This system helps is effective for reducing the cost relating to the overhead. This technique tends

to be more effective in the complex business environments faced by Tesco such as the staff has

to deal with different machines, products and the processes which requires skills (Maas,

Schalteggerand Crutzen, 2016). ABC is the planning tool that is designed for tracing the cost

incurred in the activities. It facilitates the better information regarding the profitability and cost

of distribution. It is an excellent tool in measuring the specific cost in relation to activity which

in turn helps in reaching the objective of cost reduction for the management of Tesco. It provides

for the unnecessary cost involved in the activity and suggests measures for elimination such cost.

It facilitates correct evaluation of the profits, margins ascertained for product and in overall

operations of Tesco.

Breakeven analysis-It is technique that refers to the examination and the evaluation of

safety margins for Tesco on the basis of the revenue collected and attached to the cost. Assessing

the different level of the price in relation to several levels of the demand that the business uses

this technique for determining required level of the sales for covering out the entire fixed cost

incurred by the enterprise. It tells the company about the level of the investment that it should

reach for recovering the initial outlay. Specifically break even analysis is used by an entity as the

metric and the computation of the margin of safety in context of achieving the target of the

desired sales. It is the most effective technique as it tells about the current performance of the

company and helps in forecasting the future estimations relating the cash requirements.

Benchmarking- This planning tool is counted as best for attaining the excellence in the

performance and reaching the competitive edge against the competitors that has been adopted by

Tesco. It helps in knowing the strategies, products and the processes that are considered best in

the overall market so that competencies can be created.It is the practice of measuring the

company’s performance in terms of its products, processes and services with that of another

business that is been considered as the best in the overall industry or the market (Messner, 2016).

It resolves the financial problems in identifying the internal opportunities so that better

improvement can be attained.It is said to be the effective tool as it helps in improving the quality

in the products and the services f the organization on a continuous basis. It assists the firm in

leading towards better performance with cost efficiency and allows for determining the areas that

needs improvement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

PART 1

Marginal costing-It means ascertaining profits by differentiating the fixed and the

variable cost and also the effect of changes in the profit for reaching the output. It is the costing

technique where the variable cost is been charged to the cost units and fixed cost for a specific

period is wholly write off over the contribution (Nishimura, 2019). It refers to as the additional

cost that is involved in the production of an extra output unit. It is the method that is used in the

internal reporting where the marginal cost are been charged to the units of the cost and the fixed

cost. It helps in eliminating the fixed overhead that is associated with the production cost and

also helps in carry forward the portion of fixed overhead to subsequent period. Through this

technique the problem in relation the over and the under absorption is been avoided.

Absorption costing- It is the managerial accounting method that accounts for all the

expenses that are attached with the manufacturing of a specific product. It uses the overhead and

the sum of the direct cost associated in manufacturing the product as the cost basis.It is method

where the fixed costs are assigned directly in manufacturing the product. It includes both fixed

and the variable overhead cost so that correct evaluation of the profits can be ascertained. It

offers the recording of the expenses till the inventory is actually been sold in the market or to the

customers (Quattrone, 2016). This helps in improved assessment of the profits for the particular

accounting period.

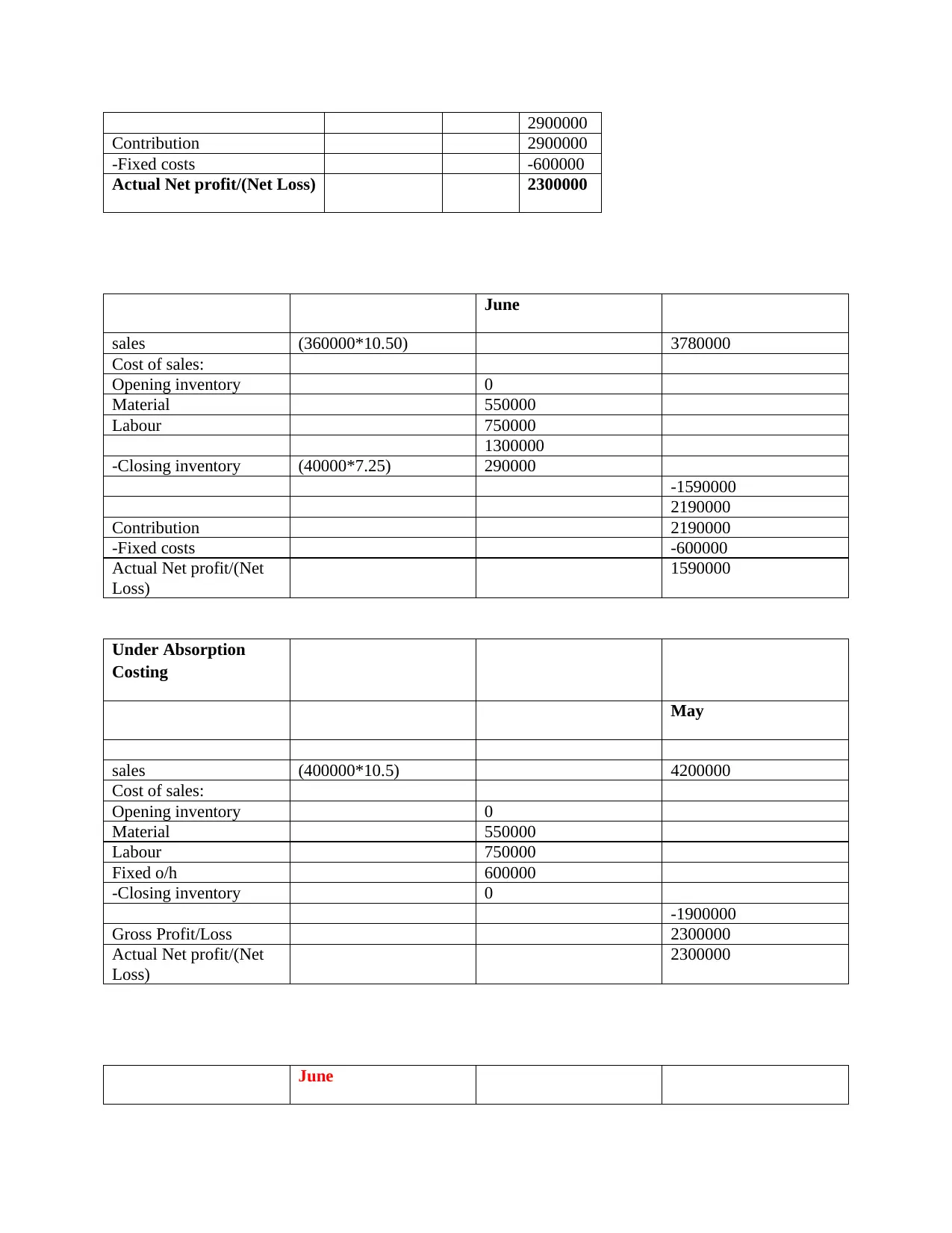

Computation of net profit by applying both marginal and absorption costing method

.

PART 1

Marginal costing-It means ascertaining profits by differentiating the fixed and the

variable cost and also the effect of changes in the profit for reaching the output. It is the costing

technique where the variable cost is been charged to the cost units and fixed cost for a specific

period is wholly write off over the contribution (Nishimura, 2019). It refers to as the additional

cost that is involved in the production of an extra output unit. It is the method that is used in the

internal reporting where the marginal cost are been charged to the units of the cost and the fixed

cost. It helps in eliminating the fixed overhead that is associated with the production cost and

also helps in carry forward the portion of fixed overhead to subsequent period. Through this

technique the problem in relation the over and the under absorption is been avoided.

Absorption costing- It is the managerial accounting method that accounts for all the

expenses that are attached with the manufacturing of a specific product. It uses the overhead and

the sum of the direct cost associated in manufacturing the product as the cost basis.It is method

where the fixed costs are assigned directly in manufacturing the product. It includes both fixed

and the variable overhead cost so that correct evaluation of the profits can be ascertained. It

offers the recording of the expenses till the inventory is actually been sold in the market or to the

customers (Quattrone, 2016). This helps in improved assessment of the profits for the particular

accounting period.

Computation of net profit by applying both marginal and absorption costing method

.

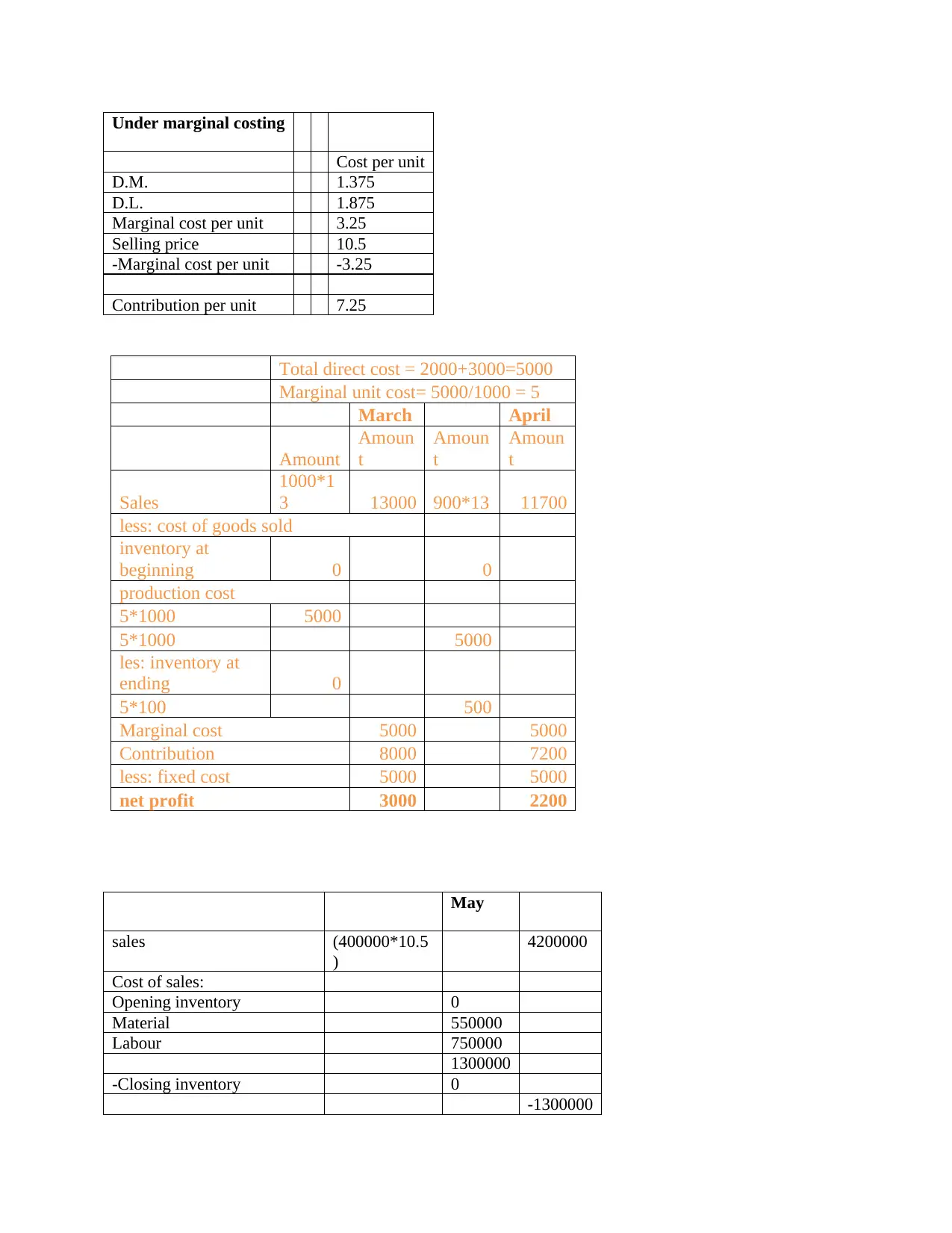

Under marginal costing

Cost per unit

D.M. 1.375

D.L. 1.875

Marginal cost per unit 3.25

Selling price 10.5

-Marginal cost per unit -3.25

Contribution per unit 7.25

Total direct cost = 2000+3000=5000

Marginal unit cost= 5000/1000 = 5

March April

Amount

Amoun

t

Amoun

t

Amoun

t

Sales

1000*1

3 13000 900*13 11700

less: cost of goods sold

inventory at

beginning 0 0

production cost

5*1000 5000

5*1000 5000

les: inventory at

ending 0

5*100 500

Marginal cost 5000 5000

Contribution 8000 7200

less: fixed cost 5000 5000

net profit 3000 2200

May

sales (400000*10.5

)

4200000

Cost of sales:

Opening inventory 0

Material 550000

Labour 750000

1300000

-Closing inventory 0

-1300000

Cost per unit

D.M. 1.375

D.L. 1.875

Marginal cost per unit 3.25

Selling price 10.5

-Marginal cost per unit -3.25

Contribution per unit 7.25

Total direct cost = 2000+3000=5000

Marginal unit cost= 5000/1000 = 5

March April

Amount

Amoun

t

Amoun

t

Amoun

t

Sales

1000*1

3 13000 900*13 11700

less: cost of goods sold

inventory at

beginning 0 0

production cost

5*1000 5000

5*1000 5000

les: inventory at

ending 0

5*100 500

Marginal cost 5000 5000

Contribution 8000 7200

less: fixed cost 5000 5000

net profit 3000 2200

May

sales (400000*10.5

)

4200000

Cost of sales:

Opening inventory 0

Material 550000

Labour 750000

1300000

-Closing inventory 0

-1300000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2900000

Contribution 2900000

-Fixed costs -600000

Actual Net profit/(Net Loss) 2300000

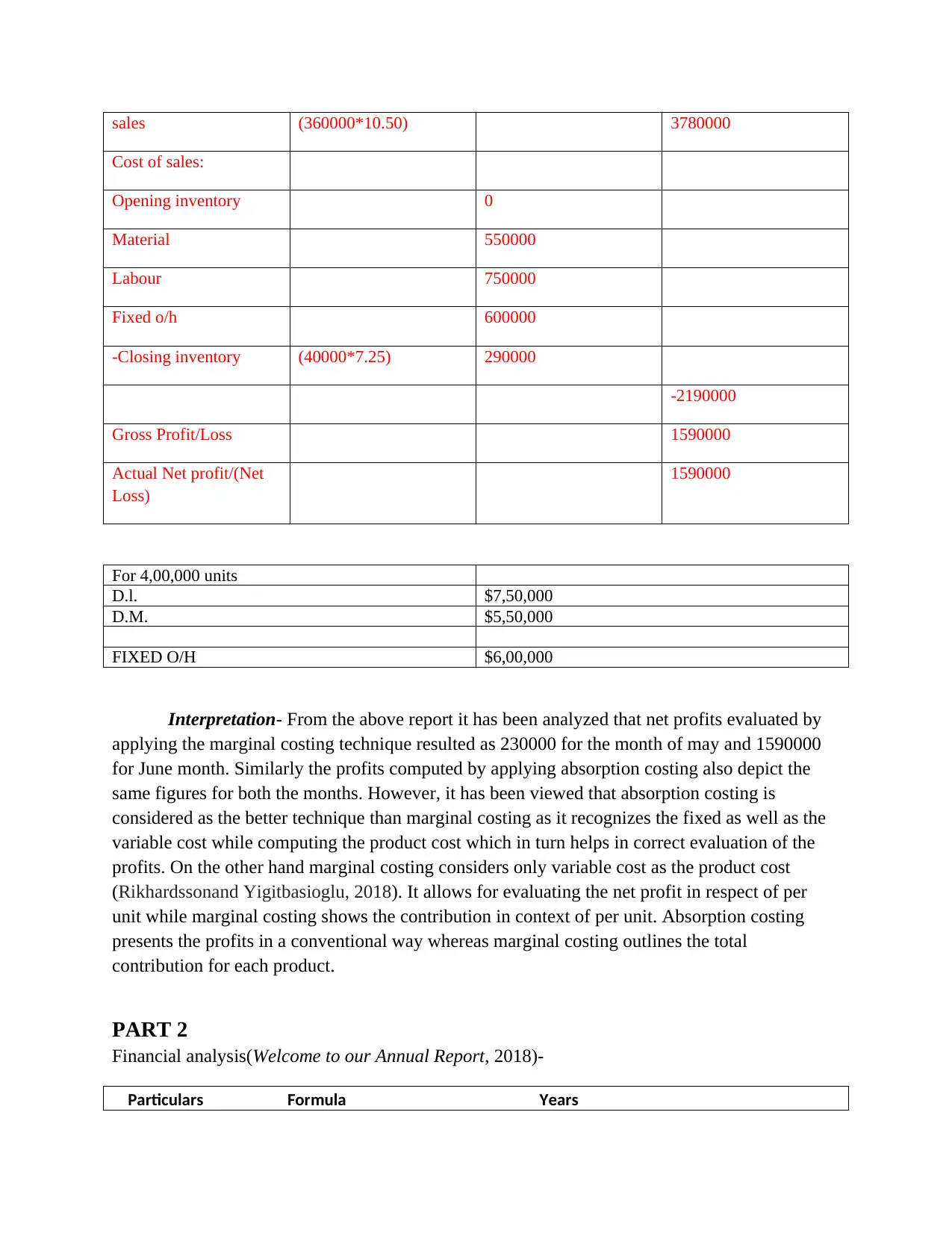

June

sales (360000*10.50) 3780000

Cost of sales:

Opening inventory 0

Material 550000

Labour 750000

1300000

-Closing inventory (40000*7.25) 290000

-1590000

2190000

Contribution 2190000

-Fixed costs -600000

Actual Net profit/(Net

Loss)

1590000

Under Absorption

Costing

May

sales (400000*10.5) 4200000

Cost of sales:

Opening inventory 0

Material 550000

Labour 750000

Fixed o/h 600000

-Closing inventory 0

-1900000

Gross Profit/Loss 2300000

Actual Net profit/(Net

Loss)

2300000

June

Contribution 2900000

-Fixed costs -600000

Actual Net profit/(Net Loss) 2300000

June

sales (360000*10.50) 3780000

Cost of sales:

Opening inventory 0

Material 550000

Labour 750000

1300000

-Closing inventory (40000*7.25) 290000

-1590000

2190000

Contribution 2190000

-Fixed costs -600000

Actual Net profit/(Net

Loss)

1590000

Under Absorption

Costing

May

sales (400000*10.5) 4200000

Cost of sales:

Opening inventory 0

Material 550000

Labour 750000

Fixed o/h 600000

-Closing inventory 0

-1900000

Gross Profit/Loss 2300000

Actual Net profit/(Net

Loss)

2300000

June

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales (360000*10.50) 3780000

Cost of sales:

Opening inventory 0

Material 550000

Labour 750000

Fixed o/h 600000

-Closing inventory (40000*7.25) 290000

-2190000

Gross Profit/Loss 1590000

Actual Net profit/(Net

Loss)

1590000

For 4,00,000 units

D.l. $7,50,000

D.M. $5,50,000

FIXED O/H $6,00,000

Interpretation- From the above report it has been analyzed that net profits evaluated by

applying the marginal costing technique resulted as 230000 for the month of may and 1590000

for June month. Similarly the profits computed by applying absorption costing also depict the

same figures for both the months. However, it has been viewed that absorption costing is

considered as the better technique than marginal costing as it recognizes the fixed as well as the

variable cost while computing the product cost which in turn helps in correct evaluation of the

profits. On the other hand marginal costing considers only variable cost as the product cost

(Rikhardssonand Yigitbasioglu, 2018). It allows for evaluating the net profit in respect of per

unit while marginal costing shows the contribution in context of per unit. Absorption costing

presents the profits in a conventional way whereas marginal costing outlines the total

contribution for each product.

PART 2

Financial analysis(Welcome to our Annual Report, 2018)-

Particulars Formula Years

Cost of sales:

Opening inventory 0

Material 550000

Labour 750000

Fixed o/h 600000

-Closing inventory (40000*7.25) 290000

-2190000

Gross Profit/Loss 1590000

Actual Net profit/(Net

Loss)

1590000

For 4,00,000 units

D.l. $7,50,000

D.M. $5,50,000

FIXED O/H $6,00,000

Interpretation- From the above report it has been analyzed that net profits evaluated by

applying the marginal costing technique resulted as 230000 for the month of may and 1590000

for June month. Similarly the profits computed by applying absorption costing also depict the

same figures for both the months. However, it has been viewed that absorption costing is

considered as the better technique than marginal costing as it recognizes the fixed as well as the

variable cost while computing the product cost which in turn helps in correct evaluation of the

profits. On the other hand marginal costing considers only variable cost as the product cost

(Rikhardssonand Yigitbasioglu, 2018). It allows for evaluating the net profit in respect of per

unit while marginal costing shows the contribution in context of per unit. Absorption costing

presents the profits in a conventional way whereas marginal costing outlines the total

contribution for each product.

PART 2

Financial analysis(Welcome to our Annual Report, 2018)-

Particulars Formula Years

2017 2018

gross profit 2902 3350

operating profit 1017 1837

sales 55917 57491

gross profit ratio gross profit/sales*100 5% 6%

operating profit

ratio operating profit/sales*100 2% 3%

gearing ratio

debt 9433 7142

equity 6414 10458

debt-equity ratio

long term debts/shareholders

funds

1.47068

9

0.68292

2

interest cover

Earning before interest and tax 1017 1837

interest expense 874 631

interest coverage

ratio EBIT/interest expense

1.16361

6

2.91125

2

liquidity ratio

current asset 15073 13577

inventory 2301 2263

quick assets 12772 11314

current liability 19234 19238

current ratio current asset/current liability

0.78366

4

0.70573

9

quick ratio quick asset/current liability

0.66403

2

0.58810

7

Business Memo

From the above analysis it has been interpreted that profitability of Tesco is showing an increasing trend

as in the 2017 gross and the operating profit ratio of the company resulted as 5% & 2%. However, during

2018 the ratio increased from1% that is 6% and 3% which means that the company has to adopt

appropriate measures for gaining higher profit margins after payment of all its expense and costs. The

gearing or the leverage ratio includes the debt-equity and interest coverage ratio where the debt equity

ratio is decreasing that is from 1.47 to 0.68 which means a positive outcome as the long term debt or

borrowing is been declined and equity increases. On the other side the interest coverage ratio is showing

an increased ratio equates to 1.16 in 2017 and 2.91 in 2018 which means that the capability of the Tesco

increases in meeting its interest expenses over its liability (Sinaga and et.al., 2019). The liquidity position

of the organization is not showing better result as the current and the quick ratio is decreasing which

gross profit 2902 3350

operating profit 1017 1837

sales 55917 57491

gross profit ratio gross profit/sales*100 5% 6%

operating profit

ratio operating profit/sales*100 2% 3%

gearing ratio

debt 9433 7142

equity 6414 10458

debt-equity ratio

long term debts/shareholders

funds

1.47068

9

0.68292

2

interest cover

Earning before interest and tax 1017 1837

interest expense 874 631

interest coverage

ratio EBIT/interest expense

1.16361

6

2.91125

2

liquidity ratio

current asset 15073 13577

inventory 2301 2263

quick assets 12772 11314

current liability 19234 19238

current ratio current asset/current liability

0.78366

4

0.70573

9

quick ratio quick asset/current liability

0.66403

2

0.58810

7

Business Memo

From the above analysis it has been interpreted that profitability of Tesco is showing an increasing trend

as in the 2017 gross and the operating profit ratio of the company resulted as 5% & 2%. However, during

2018 the ratio increased from1% that is 6% and 3% which means that the company has to adopt

appropriate measures for gaining higher profit margins after payment of all its expense and costs. The

gearing or the leverage ratio includes the debt-equity and interest coverage ratio where the debt equity

ratio is decreasing that is from 1.47 to 0.68 which means a positive outcome as the long term debt or

borrowing is been declined and equity increases. On the other side the interest coverage ratio is showing

an increased ratio equates to 1.16 in 2017 and 2.91 in 2018 which means that the capability of the Tesco

increases in meeting its interest expenses over its liability (Sinaga and et.al., 2019). The liquidity position

of the organization is not showing better result as the current and the quick ratio is decreasing which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.