Management Accounting Analysis for Tesla Motors Performance Evaluation

VerifiedAdded on 2022/08/29

|18

|4169

|28

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Tesla Motors, an electric vehicle and clean energy company. The report begins by exploring the role of management accounting in providing crucial information for business organizations, especially in a rapidly changing technological and globalized environment. It examines the limitations of traditional budgeting approaches and highlights the advantages of Activity-Based Costing (ABC) and Activity-Based Management (ABM) in achieving strategic objectives. The report emphasizes how ABC and ABM can enhance decision-making, improve product costing, and support performance management within Tesla. Furthermore, it explores the application of these techniques in the context of Tesla's operations, including the potential benefits of ABM for strategic decisions related to product mix, sourcing, and overall business excellence. The report concludes by emphasizing the importance of adapting management accounting techniques to maintain a competitive edge and create value within the dynamic environment of the electric vehicle industry.

Running Head: MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

Name of the Student

Name of the University

Author Note

MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

Table of Contents

Task 1.........................................................................................................................................2

Management Accounting within the Tesla Motors....................................................................2

Task 2.........................................................................................................................................5

MEMO.......................................................................................................................................5

Task 3.......................................................................................................................................10

Introduction..............................................................................................................................10

Discussion................................................................................................................................10

Adoption of Balance Scorecard for measuring Organizational Performance......................10

Conclusion................................................................................................................................14

Reference..................................................................................................................................15

Table of Contents

Task 1.........................................................................................................................................2

Management Accounting within the Tesla Motors....................................................................2

Task 2.........................................................................................................................................5

MEMO.......................................................................................................................................5

Task 3.......................................................................................................................................10

Introduction..............................................................................................................................10

Discussion................................................................................................................................10

Adoption of Balance Scorecard for measuring Organizational Performance......................10

Conclusion................................................................................................................................14

Reference..................................................................................................................................15

2MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

Task 1

Management Accounting within the Tesla Motors

Tesla Inc is the American electric vehicle as well as clean energy company that is

based in California. The formation of Tesla Motors was to develop the electric sports cars. It

is automotive and car manufacturer company, which produces vehicles, which is fully

electric. It is specialized in manufacturing of electric vehicle, storage of battery energy from

home to the grid scale through its acquisition of the solar roof, SolarCity and solar panel tile

manufacturing. Tesla is accelerating transition of world to the sustained energy with the solar

panels, integrated renewable energy and electric cars (Tesla. 2020).

Management accounting plays vigorous role in provision and acquisition of the

information to business organizations. Globalization and change in technology lead towards

increased level of competition and with the advanced technology, the business organization

are required for getting the information more frequently for staying in competitive edge. Key

procedural and technological advancement can have deeper impact on the professional all

across the industries. The accounting future is heavily impacted by the array of multiple

factors, which include advancement of technology such as automation, artificial intelligence

and machine learning as well as shifting of industry and government standards (Sassen 2015).

If company is using traditional approach of accounting, then it will not be able to survive in

the competitive market. In this concern, management accountants respond effectively to the

changes in environment of business. Management accountants enhances competitiveness of

organization by increasing level of the productivity and efficiency and implementing the cost

leadership. In addition, management accounts should be able in delegating responsibilities as

well as improving and influencing decisions-making at the top levels (Theriou and Aggelidis

2014).

Task 1

Management Accounting within the Tesla Motors

Tesla Inc is the American electric vehicle as well as clean energy company that is

based in California. The formation of Tesla Motors was to develop the electric sports cars. It

is automotive and car manufacturer company, which produces vehicles, which is fully

electric. It is specialized in manufacturing of electric vehicle, storage of battery energy from

home to the grid scale through its acquisition of the solar roof, SolarCity and solar panel tile

manufacturing. Tesla is accelerating transition of world to the sustained energy with the solar

panels, integrated renewable energy and electric cars (Tesla. 2020).

Management accounting plays vigorous role in provision and acquisition of the

information to business organizations. Globalization and change in technology lead towards

increased level of competition and with the advanced technology, the business organization

are required for getting the information more frequently for staying in competitive edge. Key

procedural and technological advancement can have deeper impact on the professional all

across the industries. The accounting future is heavily impacted by the array of multiple

factors, which include advancement of technology such as automation, artificial intelligence

and machine learning as well as shifting of industry and government standards (Sassen 2015).

If company is using traditional approach of accounting, then it will not be able to survive in

the competitive market. In this concern, management accountants respond effectively to the

changes in environment of business. Management accountants enhances competitiveness of

organization by increasing level of the productivity and efficiency and implementing the cost

leadership. In addition, management accounts should be able in delegating responsibilities as

well as improving and influencing decisions-making at the top levels (Theriou and Aggelidis

2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

The uses of traditional budgeting approach will not help company in achieving its

strategic objective. The technological issues impact environment of business and ultimately

auditing and accounting research environment. Tesla is the marketing leader of its electric

vehicle. If its management accounting is not changed in accordance with the globalization,

change in technology and expectations of customer, then it will be having adverse impact on

performance of entity (van Helden and Uddin 2016). The company needs to be updated of

any changes taking place. In the modern business organization, operating in the globalized

economy, management accounting in its role of providing information, needs to break away

from the traditional approach2 of providing only the internal information to the external

market, rather in modern approach, it helps in informing team of decision-making and the

team of top management on the external constraints such as threats, changing market

conditions and competition that affects the business (Hopper, Lassou and Soobaroyen 2017).

In the company like Tesla, management accounting plays significant role in the

strategic business decision-making. One survey by “Ernst and Young” and “Institute of

Management Accountant” states that the management accounting helps in providing the

required input by the strategic decision-makers in business. In order to deal with the

challenges of changing market conditions, expectations of consumer and globalized world,

management accounting helps the managers for determining substitute products in market,

adequacy of fund for funding strategy, critical capabilities and determining key customers

(Ahmad 2014).

Hence, globalization has resulted into transforming management accounting and it is

quite evident that this transformation is still continued. The role of management accounting

has changed from the traditional approach of bean-accounting for becoming core partners in

almost all the task of management. Tesla needs to update their management accounting

techniques according to prevailing competitive conditions so that it can help business

The uses of traditional budgeting approach will not help company in achieving its

strategic objective. The technological issues impact environment of business and ultimately

auditing and accounting research environment. Tesla is the marketing leader of its electric

vehicle. If its management accounting is not changed in accordance with the globalization,

change in technology and expectations of customer, then it will be having adverse impact on

performance of entity (van Helden and Uddin 2016). The company needs to be updated of

any changes taking place. In the modern business organization, operating in the globalized

economy, management accounting in its role of providing information, needs to break away

from the traditional approach2 of providing only the internal information to the external

market, rather in modern approach, it helps in informing team of decision-making and the

team of top management on the external constraints such as threats, changing market

conditions and competition that affects the business (Hopper, Lassou and Soobaroyen 2017).

In the company like Tesla, management accounting plays significant role in the

strategic business decision-making. One survey by “Ernst and Young” and “Institute of

Management Accountant” states that the management accounting helps in providing the

required input by the strategic decision-makers in business. In order to deal with the

challenges of changing market conditions, expectations of consumer and globalized world,

management accounting helps the managers for determining substitute products in market,

adequacy of fund for funding strategy, critical capabilities and determining key customers

(Ahmad 2014).

Hence, globalization has resulted into transforming management accounting and it is

quite evident that this transformation is still continued. The role of management accounting

has changed from the traditional approach of bean-accounting for becoming core partners in

almost all the task of management. Tesla needs to update their management accounting

techniques according to prevailing competitive conditions so that it can help business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

operations for the better performance and establishment of competitive edge, better strategic

decision-making and creating and adding value to business operations. Further, it can also

help in tracking performance on the chosen key factors of success among the costing,

efficiency, quality, innovation and time, and referencing these to performance of the

competitors and implementation and development of the prevention of fraud and the internal

system of control within the business (Kloviene and Gimzauskiene 2014).

operations for the better performance and establishment of competitive edge, better strategic

decision-making and creating and adding value to business operations. Further, it can also

help in tracking performance on the chosen key factors of success among the costing,

efficiency, quality, innovation and time, and referencing these to performance of the

competitors and implementation and development of the prevention of fraud and the internal

system of control within the business (Kloviene and Gimzauskiene 2014).

5MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

.

Task 2

MEMO

To- Management

From:

Date: March 26, 2020

Subject- Limitation of traditional budgeting control system in the modern workplace and how

ABM and ABC will help the Tesla Motors in achieving their strategic objectives.

Dear Sir/Madam,

This memo is written in order to draw your kind attention regarding two concern. The first

concern is drawback associated with using traditional approach of budgetary control system

in the modern workplace and the second concern is the way ABM and ABC will result in

achieving its strategic objectives.

1)

The adoption of budgetary process has been for first time as key driver of performance at

beginning of twentieth-century. Since then, it has increasingly become vital as tool of

planning and controlling. However, in recent times, the process of traditional budgeting has

been criticized for not giving results in line with the needs of business. The evolving as well

as changing environment is requiring organizations for adopting more flexible tools.

Traditional budgeting is method of preparing budget, in which the budget of last year is taken

as base. The current year’s budget is prepared with the help of making changes to budgets of

last year by making adjustment in expenses based on rate of inflation, demand of consumer,

situation of market and other.

.

Task 2

MEMO

To- Management

From:

Date: March 26, 2020

Subject- Limitation of traditional budgeting control system in the modern workplace and how

ABM and ABC will help the Tesla Motors in achieving their strategic objectives.

Dear Sir/Madam,

This memo is written in order to draw your kind attention regarding two concern. The first

concern is drawback associated with using traditional approach of budgetary control system

in the modern workplace and the second concern is the way ABM and ABC will result in

achieving its strategic objectives.

1)

The adoption of budgetary process has been for first time as key driver of performance at

beginning of twentieth-century. Since then, it has increasingly become vital as tool of

planning and controlling. However, in recent times, the process of traditional budgeting has

been criticized for not giving results in line with the needs of business. The evolving as well

as changing environment is requiring organizations for adopting more flexible tools.

Traditional budgeting is method of preparing budget, in which the budget of last year is taken

as base. The current year’s budget is prepared with the help of making changes to budgets of

last year by making adjustment in expenses based on rate of inflation, demand of consumer,

situation of market and other.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

Traditional budgetary control system approach consumes enormous amounts of the resources

and time within individual business units and finance department that provides less value in

the return. Moreover, reason why the traditional budgeting takes more time is using of the

spreadsheets, which include inherent efficiencies are higher human error probabilities, issues

of duties segregation and not accurate formulations. Further, using spreadsheet could inclined

to the errors of data entry, issues of version control and there would be problem in devising

the formulations in accurate manner (Johansson and Siverbo 2014).

It produces unreliable and inaccurate results. It mainly results from the spreadsheets that is

not flexible enough in providing more dynamic assessment. It means that tools of the

traditional budgeting are not only vague, but it is also not able to provide the complete picture

of business needs.

The today’s complexities of market require collaborative approach for the process of

budgeting among different areas of budgeting. Instead, most of the entities empowers finance

department for performing task. The process of budget represents one of the few

opportunities for various functions of business for working together to reflect strategy and

position of corporate. The centralization of budgeting process in hands of finance function

will produce instead less accurate business reflection (Behery, Jabeen and Parakandi 2014).

As the managers are quite obsessed with hitting the numbers, however, they most often miss

out strategic intention of the budgeting. The process of traditional budgetary approach

focusses on reducing the cost in comparison to value creation of business that means

initiatives of strategy are having lower priorities. The traditional process might be perceived

as futile exercise, when there is no alignment of budgets with the drivers of business. Further,

most of the businesses are having annual cycle of budgeting and annual concentration, most

often makes the budget outdated shortly after it is created. There is no regular conducting of

Traditional budgetary control system approach consumes enormous amounts of the resources

and time within individual business units and finance department that provides less value in

the return. Moreover, reason why the traditional budgeting takes more time is using of the

spreadsheets, which include inherent efficiencies are higher human error probabilities, issues

of duties segregation and not accurate formulations. Further, using spreadsheet could inclined

to the errors of data entry, issues of version control and there would be problem in devising

the formulations in accurate manner (Johansson and Siverbo 2014).

It produces unreliable and inaccurate results. It mainly results from the spreadsheets that is

not flexible enough in providing more dynamic assessment. It means that tools of the

traditional budgeting are not only vague, but it is also not able to provide the complete picture

of business needs.

The today’s complexities of market require collaborative approach for the process of

budgeting among different areas of budgeting. Instead, most of the entities empowers finance

department for performing task. The process of budget represents one of the few

opportunities for various functions of business for working together to reflect strategy and

position of corporate. The centralization of budgeting process in hands of finance function

will produce instead less accurate business reflection (Behery, Jabeen and Parakandi 2014).

As the managers are quite obsessed with hitting the numbers, however, they most often miss

out strategic intention of the budgeting. The process of traditional budgetary approach

focusses on reducing the cost in comparison to value creation of business that means

initiatives of strategy are having lower priorities. The traditional process might be perceived

as futile exercise, when there is no alignment of budgets with the drivers of business. Further,

most of the businesses are having annual cycle of budgeting and annual concentration, most

often makes the budget outdated shortly after it is created. There is no regular conducting of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

reviews for taking changes into account. In real time, its not possible for the two-third of

entities for investigating details of their budget. It means reviews of budget often takes longer

than what is required. This defeats the purpose of the adaptation of change (Réka, Ştefan and

Daniel 2014).

Moreover, traditional approach of budgeting system also fails in motivating people for acting

in interest of entity, as it motivates un-professional attitudes in the cost centre of budget by

managers, supports bureaucracy and the vertical control by making the individual feel

undervalues and instead of allowing sharing of the knowledge, it supports the barriers of

department.

2)

ABC as well as ABM have brough radical changes in the system of cost management. It is no

longer that applicability of ABM is limited to the manufacturing entities. Further,

philosophies and principles of the activity-based thought applies equally to the entities in

different industries. ABC is considered as not only just costing method, rather technique for

managing the company in best way. As Tesla is forward-thinking company, it can apply this

technique in to manage company in the best possible way. ABC is the one-off exercise,

which measures the performance and cost of the activities, objects and resources that

consumes them for generating more meaningful and precise information for making the

decision.

ABC helps in providing more accurate technique of service or the product costing that leads

towards more accurate decisions regarding pricing. This helps in increasing knowledge of the

drivers of cost and overheads and makes the non-value adding and the costly activities much

more noticeable by letting the managers for eliminating or reducing them. Further, it enables

improvement of product as well as customer profitability analysis. Moreover, it supports

reviews for taking changes into account. In real time, its not possible for the two-third of

entities for investigating details of their budget. It means reviews of budget often takes longer

than what is required. This defeats the purpose of the adaptation of change (Réka, Ştefan and

Daniel 2014).

Moreover, traditional approach of budgeting system also fails in motivating people for acting

in interest of entity, as it motivates un-professional attitudes in the cost centre of budget by

managers, supports bureaucracy and the vertical control by making the individual feel

undervalues and instead of allowing sharing of the knowledge, it supports the barriers of

department.

2)

ABC as well as ABM have brough radical changes in the system of cost management. It is no

longer that applicability of ABM is limited to the manufacturing entities. Further,

philosophies and principles of the activity-based thought applies equally to the entities in

different industries. ABC is considered as not only just costing method, rather technique for

managing the company in best way. As Tesla is forward-thinking company, it can apply this

technique in to manage company in the best possible way. ABC is the one-off exercise,

which measures the performance and cost of the activities, objects and resources that

consumes them for generating more meaningful and precise information for making the

decision.

ABC helps in providing more accurate technique of service or the product costing that leads

towards more accurate decisions regarding pricing. This helps in increasing knowledge of the

drivers of cost and overheads and makes the non-value adding and the costly activities much

more noticeable by letting the managers for eliminating or reducing them. Further, it enables

improvement of product as well as customer profitability analysis. Moreover, it supports

8MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

technique of the performance management, for instance scorecards and constant

improvements.

Figure 1: ABC Process

In this concern, ABM draws on the ABC technique for providing decision-making and

management reporting. ABM is the fundamental shift in the emphasis from the traditional

coting and the measurement of performance. The activities are undertaken by people that

consumes resources and controlling activities allows for controlling cost at its sources. The

power and real value of the ABM comes from information and knowledge, which leads

towards better making of decisions and by leveraging, it gives measures for the improvement

(Cooper 2017).

If Tesla inculcates ABM in the company, then it will support excellence in business by

providing the information for enabling the strategic decisions of long-term relating to product

mix and sourcing. It allows the designers of product for having knowledge regarding impact

of multiple design on cost and the flexibility, afterwards modifying the designs according to

that. Further, ABM helps in supporting quest for the constant improvement with the help of

allowing management for gaining the new understanding of the activity performance by

giving focus on the demand sources for the activities as well as by allowing the management

technique of the performance management, for instance scorecards and constant

improvements.

Figure 1: ABC Process

In this concern, ABM draws on the ABC technique for providing decision-making and

management reporting. ABM is the fundamental shift in the emphasis from the traditional

coting and the measurement of performance. The activities are undertaken by people that

consumes resources and controlling activities allows for controlling cost at its sources. The

power and real value of the ABM comes from information and knowledge, which leads

towards better making of decisions and by leveraging, it gives measures for the improvement

(Cooper 2017).

If Tesla inculcates ABM in the company, then it will support excellence in business by

providing the information for enabling the strategic decisions of long-term relating to product

mix and sourcing. It allows the designers of product for having knowledge regarding impact

of multiple design on cost and the flexibility, afterwards modifying the designs according to

that. Further, ABM helps in supporting quest for the constant improvement with the help of

allowing management for gaining the new understanding of the activity performance by

giving focus on the demand sources for the activities as well as by allowing the management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

for creating incentives of behavior in order to improve more aspect of business. ABM helps

the management of Tesla un making informed decisions regarding business lines, product

process, product mix and designing of product, offering of services, pricing and capital

investment (Dong, Liu and Lin 2014).

If Tesla Motor is considering to implement ABM then it should understand that although

some markets or the product factors might make it beneficial potentially, while same factors

may not result into its implementation successfully. The system of ABM will give the better

chances to establish useful costing for the outputs. Further, ABC prompts the managers for

asking right set of questions and it becomes ABM, when it is used for designing services and

products, which exceeds or meets expectation of customer and can be produced as well as

delivered at the profit and signals that where discontinuous or continuous improvements in

the speed, efficiency and quality required. Further, it guides investment decisions and product

mix, enables to make choice among the alternative suppliers, negotiating about the features of

product, prices, quality service with the customers and delivery, employing effective and

efficient service and the distribution processes to target market and the segments of customer

and lastly, improves value of company’s services and products (Kaplan and Atkinson 2015).

If Tesla designs and implements ABM, then there include five basic information outputs,

which includes cost of the activities and processes of business, cost of the non-value-added

activities, activity-based measures of performance, accurate service or product cost and

drivers of cost. These outputs contribute to improvements in initiatives of the management

and improvement in the decision-making with the help of providing operating and cost

information regarding organizational activities.

Hence, this memo will be advantages in understanding traditional budgeting limitations and

the way ABC and ABM will be helpful in measuring organizational performance of Tesla.

for creating incentives of behavior in order to improve more aspect of business. ABM helps

the management of Tesla un making informed decisions regarding business lines, product

process, product mix and designing of product, offering of services, pricing and capital

investment (Dong, Liu and Lin 2014).

If Tesla Motor is considering to implement ABM then it should understand that although

some markets or the product factors might make it beneficial potentially, while same factors

may not result into its implementation successfully. The system of ABM will give the better

chances to establish useful costing for the outputs. Further, ABC prompts the managers for

asking right set of questions and it becomes ABM, when it is used for designing services and

products, which exceeds or meets expectation of customer and can be produced as well as

delivered at the profit and signals that where discontinuous or continuous improvements in

the speed, efficiency and quality required. Further, it guides investment decisions and product

mix, enables to make choice among the alternative suppliers, negotiating about the features of

product, prices, quality service with the customers and delivery, employing effective and

efficient service and the distribution processes to target market and the segments of customer

and lastly, improves value of company’s services and products (Kaplan and Atkinson 2015).

If Tesla designs and implements ABM, then there include five basic information outputs,

which includes cost of the activities and processes of business, cost of the non-value-added

activities, activity-based measures of performance, accurate service or product cost and

drivers of cost. These outputs contribute to improvements in initiatives of the management

and improvement in the decision-making with the help of providing operating and cost

information regarding organizational activities.

Hence, this memo will be advantages in understanding traditional budgeting limitations and

the way ABC and ABM will be helpful in measuring organizational performance of Tesla.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

Task 3

Introduction

Over last few decades, the complex environment of global business and the increasing

competitiveness of business have emphasized significance of the measurement of

performance. The methods of measuring performance have been adopted widely in the

various industries and it has received more attention. Further, measurement of company’s

success and implementation of effective strategies for the future success represents great

challenges for the consultants, researchers and managers. The business world has now

recognized balance scorecard as the promising tool for the performance measurement of

company at the firm level (Kalender and Vayvay 2016). Hence, this report aims to examine

BSC adoption approach that could be used for measuring organizational performance.

Discussion

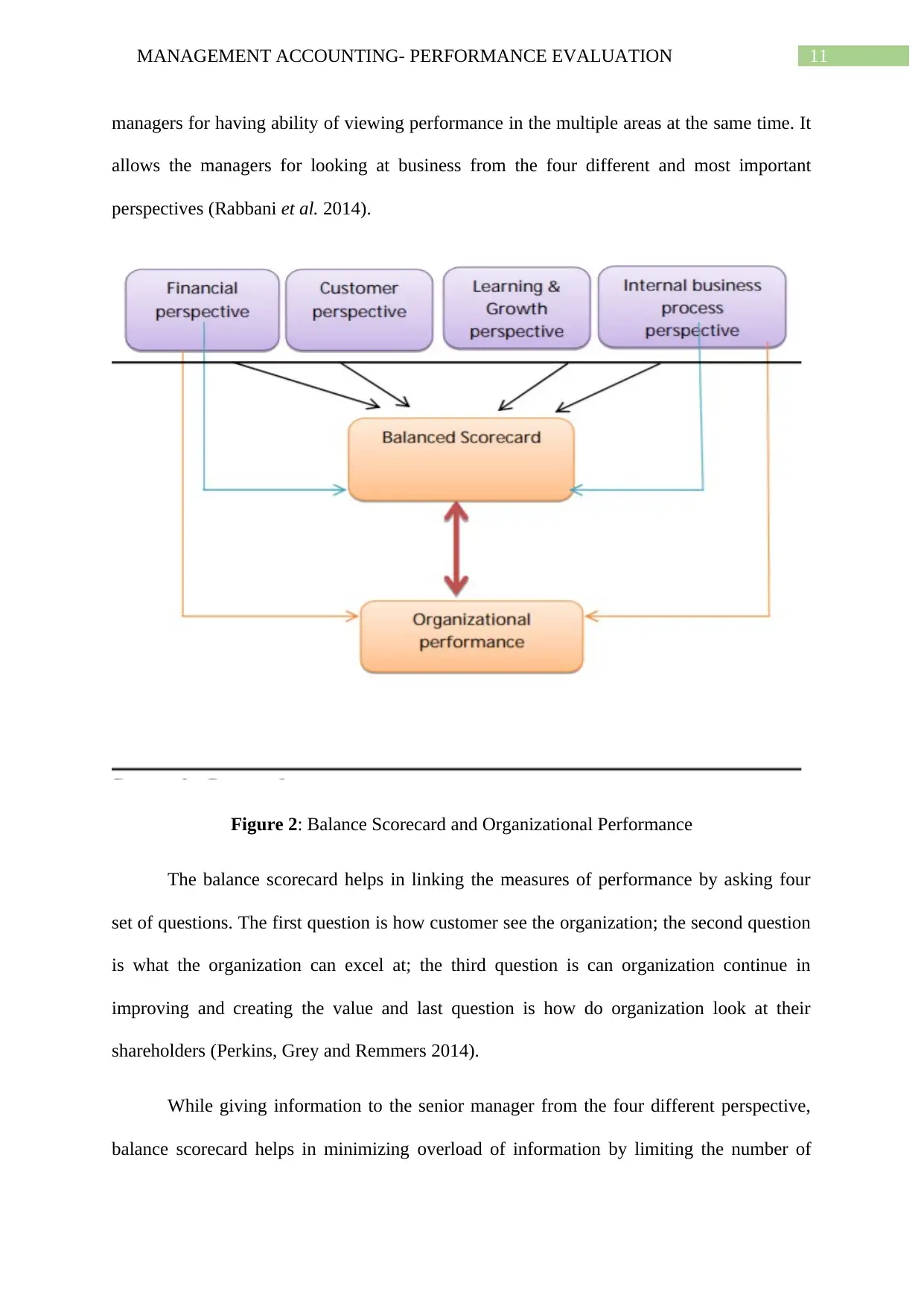

Adoption of Balance Scorecard for measuring Organizational Performance

BSC is set of the measures, which gives the top managers quick, but the

comprehensive view of the business organization. This includes the financial measures that

results of action that are taken previously. Further, it complements the financial measures

with the measures of operations, which are factors of the future financial performance on the

satisfaction of customer, internal processes and improvement and innovation activities of

organization. Further, if balance scorecard is thought as indicators as well as dials in the

flight cockpit, then for complex job of flying and navigating airplane, the pilots requires the

detailed information in relation to various aspects of flights (Busco and Quattrone 2015).

They require influence on the speed, bearing, destinations, altitude and the other indicators,

which summarizes predicted and current environment. If someone is relying on the one

instrument then it could be fatal. Likewise, complexity in managing the entity requires

Task 3

Introduction

Over last few decades, the complex environment of global business and the increasing

competitiveness of business have emphasized significance of the measurement of

performance. The methods of measuring performance have been adopted widely in the

various industries and it has received more attention. Further, measurement of company’s

success and implementation of effective strategies for the future success represents great

challenges for the consultants, researchers and managers. The business world has now

recognized balance scorecard as the promising tool for the performance measurement of

company at the firm level (Kalender and Vayvay 2016). Hence, this report aims to examine

BSC adoption approach that could be used for measuring organizational performance.

Discussion

Adoption of Balance Scorecard for measuring Organizational Performance

BSC is set of the measures, which gives the top managers quick, but the

comprehensive view of the business organization. This includes the financial measures that

results of action that are taken previously. Further, it complements the financial measures

with the measures of operations, which are factors of the future financial performance on the

satisfaction of customer, internal processes and improvement and innovation activities of

organization. Further, if balance scorecard is thought as indicators as well as dials in the

flight cockpit, then for complex job of flying and navigating airplane, the pilots requires the

detailed information in relation to various aspects of flights (Busco and Quattrone 2015).

They require influence on the speed, bearing, destinations, altitude and the other indicators,

which summarizes predicted and current environment. If someone is relying on the one

instrument then it could be fatal. Likewise, complexity in managing the entity requires

11MANAGEMENT ACCOUNTING- PERFORMANCE EVALUATION

managers for having ability of viewing performance in the multiple areas at the same time. It

allows the managers for looking at business from the four different and most important

perspectives (Rabbani et al. 2014).

Figure 2: Balance Scorecard and Organizational Performance

The balance scorecard helps in linking the measures of performance by asking four

set of questions. The first question is how customer see the organization; the second question

is what the organization can excel at; the third question is can organization continue in

improving and creating the value and last question is how do organization look at their

shareholders (Perkins, Grey and Remmers 2014).

While giving information to the senior manager from the four different perspective,

balance scorecard helps in minimizing overload of information by limiting the number of

managers for having ability of viewing performance in the multiple areas at the same time. It

allows the managers for looking at business from the four different and most important

perspectives (Rabbani et al. 2014).

Figure 2: Balance Scorecard and Organizational Performance

The balance scorecard helps in linking the measures of performance by asking four

set of questions. The first question is how customer see the organization; the second question

is what the organization can excel at; the third question is can organization continue in

improving and creating the value and last question is how do organization look at their

shareholders (Perkins, Grey and Remmers 2014).

While giving information to the senior manager from the four different perspective,

balance scorecard helps in minimizing overload of information by limiting the number of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.