Management Accounting Report for Thirdway Group: Unit 5, CCL-019-023

VerifiedAdded on 2021/02/19

|17

|5943

|49

Report

AI Summary

This report provides a detailed analysis of management accounting, focusing on the Thirdway Group Plc. It begins by defining management accounting, its systems (inventory management, cost accounting, price optimization, and job costing), and the differences between management and financial accounting. The report then explores methods of management accounting reporting, including budget reports, performance reports, accounts receivable reports, and inventory management reports. It highlights the benefits of a management accounting system, such as improved efficiency and decision-making, while also acknowledging potential disadvantages like cost and time investment. The report further examines cost analysis techniques, including absorption and marginal costing, and different planning tools for budgetary control. Finally, it addresses adapting management accounting systems to respond to financial problems, offering insights into integrating these systems with accounting reports and their overall role in organizational management.

UNIT 5: MANAGEMENT ACCOUNTING

STUDENT ID CCL-019-023

STUDENT ID CCL-019-023

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

P1.Management accounting systems and its various types:...................................................1

P2.Methods used for management accounting reporting:......................................................4

M1.Benefits of management accounting system: ..................................................................5

D1.Integration of Management accounting system with accounting reports:........................5

TASK 2............................................................................................................................................6

M2.Different techniques of management accounting system:...............................................9

TASK 3..........................................................................................................................................10

P4.Different types of planning tools for budgetary control:.................................................10

TASK 4..........................................................................................................................................12

P5.Adapting management accounting systems to respond to financial problems:..............12

M3.Use of different planning tools:.....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

P1.Management accounting systems and its various types:...................................................1

P2.Methods used for management accounting reporting:......................................................4

M1.Benefits of management accounting system: ..................................................................5

D1.Integration of Management accounting system with accounting reports:........................5

TASK 2............................................................................................................................................6

M2.Different techniques of management accounting system:...............................................9

TASK 3..........................................................................................................................................10

P4.Different types of planning tools for budgetary control:.................................................10

TASK 4..........................................................................................................................................12

P5.Adapting management accounting systems to respond to financial problems:..............12

M3.Use of different planning tools:.....................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a process of application of professional knowledge and skill

in the preparation of accounting information to assist the managerial personnel in planning,

implementation, control and monitor the operations of an undertakings. In this, Management

accountants use various information relating to cost of a particular product and provides

assistance to reduce the cost. To understanding the management accounting, a company named

Thirdway Group Plc is chosen, which is engaged in furniture, architecture work and other

company is given in this report named as Nero Ltd. This report is divided into four task, the

first task talks about the management accounting system, its various types and methods used for

management accounting reporting. Second task explains the different cost techniques for

analysis of cost and for preparation of income statements using marginal and absorption costing.

Third task provides the details about various planning tools used for budgetary control and their

advantages and disadvantages whereas forth task describes the ways for adopting management

accounting systems to respond the financial problems.

TASK 1

P1.Management accounting systems and its various types:

Management accounting is the process to prepare different types reports regarding to

internal activities then present in front of top management. In present time every organisation

want to maintain and control their internal system in effective manner so they can apply

management accounting system.

Management accounting system is the collection of activities relating to the monetary

aspects of an company which are necessary for recording of these transactions for future

perspective. It gives a systematic view of transactions and helps in smooth functioning of the

business operations. By the help of this, a summarised financial statements is prepared at year

end which includes balance sheet, profit and loss account, cash flow statements and so on. The

Thirdway Group Plc uses the various types of management accounting systems which are as

follows:

Inventory management system: This system is very important in any organisation

because it tracks record of all the inventory chain in an organisation. It covers everything

from production to retail, warehousing to shipping and all movements of stocks since the

Management accounting is a process of application of professional knowledge and skill

in the preparation of accounting information to assist the managerial personnel in planning,

implementation, control and monitor the operations of an undertakings. In this, Management

accountants use various information relating to cost of a particular product and provides

assistance to reduce the cost. To understanding the management accounting, a company named

Thirdway Group Plc is chosen, which is engaged in furniture, architecture work and other

company is given in this report named as Nero Ltd. This report is divided into four task, the

first task talks about the management accounting system, its various types and methods used for

management accounting reporting. Second task explains the different cost techniques for

analysis of cost and for preparation of income statements using marginal and absorption costing.

Third task provides the details about various planning tools used for budgetary control and their

advantages and disadvantages whereas forth task describes the ways for adopting management

accounting systems to respond the financial problems.

TASK 1

P1.Management accounting systems and its various types:

Management accounting is the process to prepare different types reports regarding to

internal activities then present in front of top management. In present time every organisation

want to maintain and control their internal system in effective manner so they can apply

management accounting system.

Management accounting system is the collection of activities relating to the monetary

aspects of an company which are necessary for recording of these transactions for future

perspective. It gives a systematic view of transactions and helps in smooth functioning of the

business operations. By the help of this, a summarised financial statements is prepared at year

end which includes balance sheet, profit and loss account, cash flow statements and so on. The

Thirdway Group Plc uses the various types of management accounting systems which are as

follows:

Inventory management system: This system is very important in any organisation

because it tracks record of all the inventory chain in an organisation. It covers everything

from production to retail, warehousing to shipping and all movements of stocks since the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

stage it purchased (Bennett and James, 2017). In an inventory management system,

various sub system exist which is essential part of this system such as warehousing

inventory management, retail inventory management etc. For this, various valuation

method are used like FIFO, LIFO and weighted average method for valuation of

inventories.

Cost accounting system: It is also called product costing system and costing system also.

This system is a framework used by Thirdway Group Plc to estimate the cost of their

products and services for calculating the actual profits of the company. It is essential to

have this system in an organisation because by the help of this it can value its raw

materials, work in progress and finished goods and as a result, may easily find out that

which product is profitable and which one is not. Cost accounting system has mainly two

types, which are job order costing and process costing.

Price optimisation system: This system is very useful in an organisation because it is

helpful in determining a preferred set of prices so that an organisation like Thirdway

Group Plc can increase its profitability for the interest of its stakeholders. It is

mathematical function that helps the organisation to determine in what way customer

react in different pricing situations for its products and services (Burritt and Tingey-

Holyoak, 2012).

Job costing: In job costing system, cost is determined for a particular job or assignment

which is given to perform to a particular person. This helps the Thirdway Group in

establishing the workers performance relating to particular job and cost incurred related

to same job.

Distinction between management and financial accounting:

There are number of differences between financial accounting and management

accounting, some of these are as follows:

Aggregation: Financial accounting is helpful in reporting the entire business activities

relating to finance which focuses only on the monetary items but management

accounting also focuses on the non monetary items and it provides more detailed report

related to product line, geographical region and so on.

Efficiency: Financial accounting focuses more on achieving efficiency in profitability of

business whereas other is more engaged in proving efficiency in employees working.

various sub system exist which is essential part of this system such as warehousing

inventory management, retail inventory management etc. For this, various valuation

method are used like FIFO, LIFO and weighted average method for valuation of

inventories.

Cost accounting system: It is also called product costing system and costing system also.

This system is a framework used by Thirdway Group Plc to estimate the cost of their

products and services for calculating the actual profits of the company. It is essential to

have this system in an organisation because by the help of this it can value its raw

materials, work in progress and finished goods and as a result, may easily find out that

which product is profitable and which one is not. Cost accounting system has mainly two

types, which are job order costing and process costing.

Price optimisation system: This system is very useful in an organisation because it is

helpful in determining a preferred set of prices so that an organisation like Thirdway

Group Plc can increase its profitability for the interest of its stakeholders. It is

mathematical function that helps the organisation to determine in what way customer

react in different pricing situations for its products and services (Burritt and Tingey-

Holyoak, 2012).

Job costing: In job costing system, cost is determined for a particular job or assignment

which is given to perform to a particular person. This helps the Thirdway Group in

establishing the workers performance relating to particular job and cost incurred related

to same job.

Distinction between management and financial accounting:

There are number of differences between financial accounting and management

accounting, some of these are as follows:

Aggregation: Financial accounting is helpful in reporting the entire business activities

relating to finance which focuses only on the monetary items but management

accounting also focuses on the non monetary items and it provides more detailed report

related to product line, geographical region and so on.

Efficiency: Financial accounting focuses more on achieving efficiency in profitability of

business whereas other is more engaged in proving efficiency in employees working.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standards: Financial accounting system is required to comply with various accounting

standards whereas there is no requirement of compliance in case of management

accounting.

Timing: In financial accounting, financial statements are required to be issued at year

end but in management accounting, reports is prepared much more frequently for

shorter period.

Valuation: Financial accounting involves valuation of asset and liabilities including

revaluation, impairment adjustments and so on. But in management accounting, there is

no requirement of such valuation.

Systems: Financial accounting pays no attention to the overall business systems that are

responsible for generation of profits. But management accounting is interested in the

location of bottleneck operations that are ultimately responsible for enhancement of

profits of the company.

Origin of management accounting:

Management accounting is first emerged during early industrial revolution in leading

industries. It is arise after financial accounting hence it trace its origins and double entry book

keeping had been used for more than 300 years as provided by some researches.

Role of management accounting:

Forecasting: Management accounting helps the company in forecasting its future business

operations and required arrangements which helps the company to plan its work accordingly.

Decision making: Management accounting also helps the managers of company in taking

important business related decisions.

Cash flow: A cash flow problem may be solve by implementing the management accounting

which provides details in what portion funds is required in various operations.

Performance variances: it assist the mangers in evaluating and monitor the performances of

various employees in the company.

Rate of return: Management accounting provides the details about the required rate of return to

shareholders. Therefore, mangers may act according to this to achieve such point.

The role of the management accountant is to perform a series of tasks to ensure their

company's financial security, handling essentially all financial matters and thus helping to drive

the business's overall management and strategy.

standards whereas there is no requirement of compliance in case of management

accounting.

Timing: In financial accounting, financial statements are required to be issued at year

end but in management accounting, reports is prepared much more frequently for

shorter period.

Valuation: Financial accounting involves valuation of asset and liabilities including

revaluation, impairment adjustments and so on. But in management accounting, there is

no requirement of such valuation.

Systems: Financial accounting pays no attention to the overall business systems that are

responsible for generation of profits. But management accounting is interested in the

location of bottleneck operations that are ultimately responsible for enhancement of

profits of the company.

Origin of management accounting:

Management accounting is first emerged during early industrial revolution in leading

industries. It is arise after financial accounting hence it trace its origins and double entry book

keeping had been used for more than 300 years as provided by some researches.

Role of management accounting:

Forecasting: Management accounting helps the company in forecasting its future business

operations and required arrangements which helps the company to plan its work accordingly.

Decision making: Management accounting also helps the managers of company in taking

important business related decisions.

Cash flow: A cash flow problem may be solve by implementing the management accounting

which provides details in what portion funds is required in various operations.

Performance variances: it assist the mangers in evaluating and monitor the performances of

various employees in the company.

Rate of return: Management accounting provides the details about the required rate of return to

shareholders. Therefore, mangers may act according to this to achieve such point.

The role of the management accountant is to perform a series of tasks to ensure their

company's financial security, handling essentially all financial matters and thus helping to drive

the business's overall management and strategy.

Principles of management accounting:

Four globally accepted principles includes influence, relevance and value trust which

provides guidelines to the companies.

P2.Methods used for management accounting reporting:

In an organisation, management accounting reports is made for providing overall

overview of the management practices, policies and procedures to the top level management. In

order to carry out the reporting, similar formats are required to be used in all types of reports to

maintain integrity and avoidance of any mistakes in reporting. These reports can also be helpful

to understand of nature, size, complexity of various key matters for various stakeholders.

Thirdway Group Plc shall include the following reports that prepared in in different methods

which are as follows:

Budget Report: This report is prepared by the management accountant and in this

reports, company forecast its business operations for some future period and instruct the

working staff company to work to achieve the figures as given in the budget report. If

there is any variances from budget report, then company shall require to find the reasons

for this and take corrective actions and measures to achieve desired results.

Performance report: This report is prepared by an organisation for evaluating

performance of the business operations which is done by company's personnel. This is

prepared by the managers of the company to evaluate the efficiency and effectiveness of

the employees and taking appropriate action in case of performance is not up-to the

target standard and in case, performance of employees is greater that target performance

then providing incentives to the employees is good practice motivation of employees.

Accounts receivable report: It is report which provides information about customer of

the companies who purchase the company's product on credit in chronological date

format. This is prepared by the manager to know how much money is receivable from

the customers and assist in taking appropriate action in case of non payment of money

by the debtors in pre-determined period. This report is also useful for maintaining a

requite amount of funds in cash for working capital requirements.

Inventory management report: These types of report help in tracking inventory record

from the stage of buying the raw materials and to the stage of manufacturing of the

Four globally accepted principles includes influence, relevance and value trust which

provides guidelines to the companies.

P2.Methods used for management accounting reporting:

In an organisation, management accounting reports is made for providing overall

overview of the management practices, policies and procedures to the top level management. In

order to carry out the reporting, similar formats are required to be used in all types of reports to

maintain integrity and avoidance of any mistakes in reporting. These reports can also be helpful

to understand of nature, size, complexity of various key matters for various stakeholders.

Thirdway Group Plc shall include the following reports that prepared in in different methods

which are as follows:

Budget Report: This report is prepared by the management accountant and in this

reports, company forecast its business operations for some future period and instruct the

working staff company to work to achieve the figures as given in the budget report. If

there is any variances from budget report, then company shall require to find the reasons

for this and take corrective actions and measures to achieve desired results.

Performance report: This report is prepared by an organisation for evaluating

performance of the business operations which is done by company's personnel. This is

prepared by the managers of the company to evaluate the efficiency and effectiveness of

the employees and taking appropriate action in case of performance is not up-to the

target standard and in case, performance of employees is greater that target performance

then providing incentives to the employees is good practice motivation of employees.

Accounts receivable report: It is report which provides information about customer of

the companies who purchase the company's product on credit in chronological date

format. This is prepared by the manager to know how much money is receivable from

the customers and assist in taking appropriate action in case of non payment of money

by the debtors in pre-determined period. This report is also useful for maintaining a

requite amount of funds in cash for working capital requirements.

Inventory management report: These types of report help in tracking inventory record

from the stage of buying the raw materials and to the stage of manufacturing of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

finished goods. It is advantageous for the company to prepare this report because it helps

the company in reducing the chances of stock out condition.

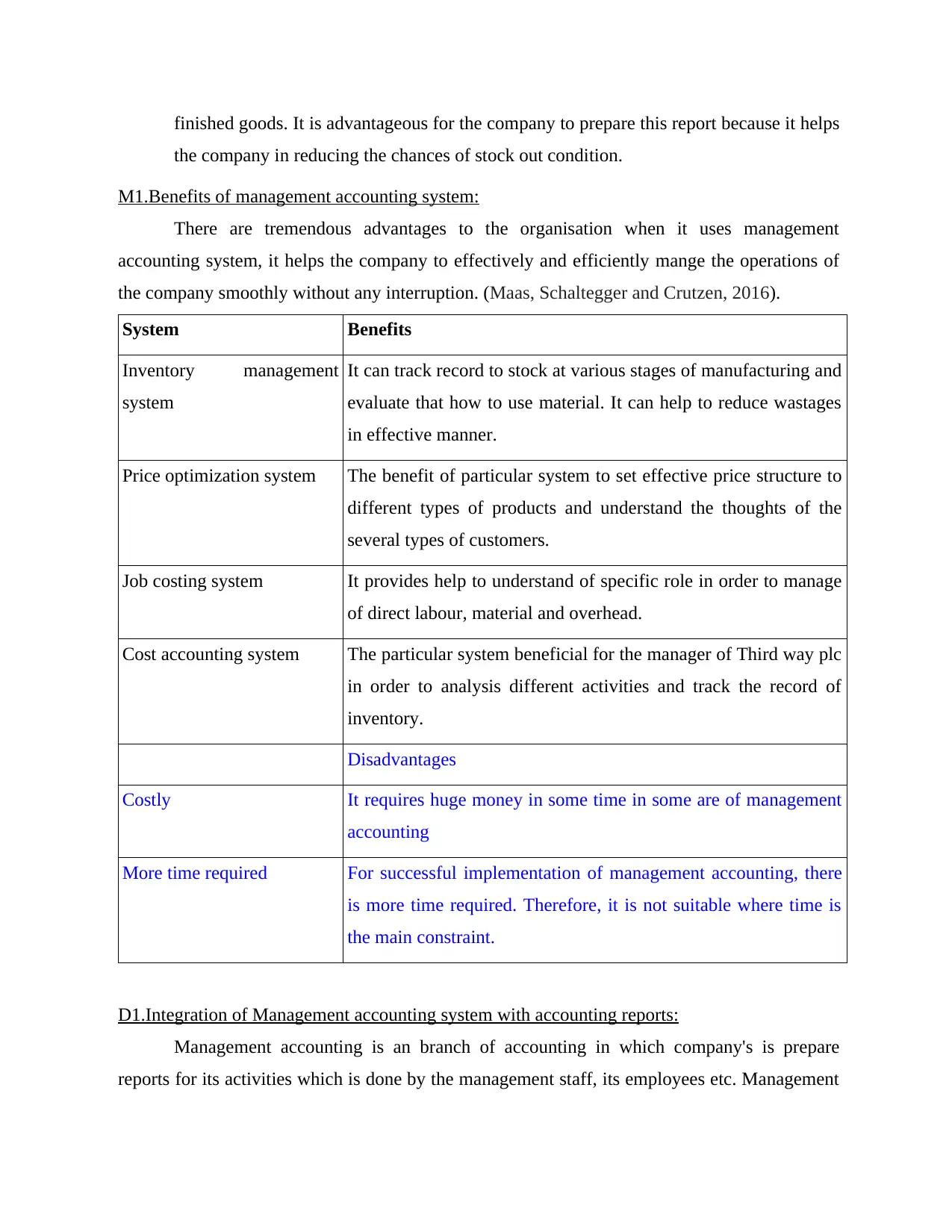

M1.Benefits of management accounting system:

There are tremendous advantages to the organisation when it uses management

accounting system, it helps the company to effectively and efficiently mange the operations of

the company smoothly without any interruption. (Maas, Schaltegger and Crutzen, 2016).

System Benefits

Inventory management

system

It can track record to stock at various stages of manufacturing and

evaluate that how to use material. It can help to reduce wastages

in effective manner.

Price optimization system The benefit of particular system to set effective price structure to

different types of products and understand the thoughts of the

several types of customers.

Job costing system It provides help to understand of specific role in order to manage

of direct labour, material and overhead.

Cost accounting system The particular system beneficial for the manager of Third way plc

in order to analysis different activities and track the record of

inventory.

Disadvantages

Costly It requires huge money in some time in some are of management

accounting

More time required For successful implementation of management accounting, there

is more time required. Therefore, it is not suitable where time is

the main constraint.

D1.Integration of Management accounting system with accounting reports:

Management accounting is an branch of accounting in which company's is prepare

reports for its activities which is done by the management staff, its employees etc. Management

the company in reducing the chances of stock out condition.

M1.Benefits of management accounting system:

There are tremendous advantages to the organisation when it uses management

accounting system, it helps the company to effectively and efficiently mange the operations of

the company smoothly without any interruption. (Maas, Schaltegger and Crutzen, 2016).

System Benefits

Inventory management

system

It can track record to stock at various stages of manufacturing and

evaluate that how to use material. It can help to reduce wastages

in effective manner.

Price optimization system The benefit of particular system to set effective price structure to

different types of products and understand the thoughts of the

several types of customers.

Job costing system It provides help to understand of specific role in order to manage

of direct labour, material and overhead.

Cost accounting system The particular system beneficial for the manager of Third way plc

in order to analysis different activities and track the record of

inventory.

Disadvantages

Costly It requires huge money in some time in some are of management

accounting

More time required For successful implementation of management accounting, there

is more time required. Therefore, it is not suitable where time is

the main constraint.

D1.Integration of Management accounting system with accounting reports:

Management accounting is an branch of accounting in which company's is prepare

reports for its activities which is done by the management staff, its employees etc. Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting system and reporting are essential aspect of integrated within other managerial

activities and processes. For intense accounting process provides basic information for

preparation of different reports in management accounting system.. Accounting system assist in

facing different issues and problems that may arise in business organisation. Beside this,

managers frames account receivable reports using price optimisation system which assist in

maintaining information effectively (Cazier, Rego and Wilson, 2015).

TASK 2

Cost: It is an monetary amount which is given by the company for performing its manufacturing

related tasks and other business operations effectively and efficiently.

Fixed cost: it may be defines as cost which is either already incurred in past or which is to be

incurred in future but determination of occurrence is already decided in past. Fixed cost is

considered irrelevant in all type of decisions.

Variable cost: It is cost which is increased as per the volume of operations but per unit cost shall

be remain constant in different volume of operations.

Indirect cost: it may be defined as cost which is incurred in production process and can not be

identified in particular product.

Absorption costing:

It is a managerial accounting cost method for calculating all costs related with In

absorption costing, an organisation consider all types of cost whether it is historical or future

cost (i.e. relevant cost, irrelevant cost or sunk cost). This costing method is used by the

enterprises when they want to find out the total cost of its regular product which it is producing

and for which, there is a demand in the market. In this costing method, company consider the

fixed cost (either avoidable fixed cost or unavoidable fixed cost) (Lavia López and Hiebl, 2014).

Marginal Costing:

In marginal costing, an organisation consider only that cost which is relevant for producing an

product (i.e. relevant cost only). This costing method is used by the enterprises when they want to find

out the minimum cost which will be incurred if company will produce that product. The product which

has no demand in existing market but it comes as an offer from new market or an offer from new

customer. In this costing method, company shall not consider fixed cost at all (Jacobs, 2012).

activities and processes. For intense accounting process provides basic information for

preparation of different reports in management accounting system.. Accounting system assist in

facing different issues and problems that may arise in business organisation. Beside this,

managers frames account receivable reports using price optimisation system which assist in

maintaining information effectively (Cazier, Rego and Wilson, 2015).

TASK 2

Cost: It is an monetary amount which is given by the company for performing its manufacturing

related tasks and other business operations effectively and efficiently.

Fixed cost: it may be defines as cost which is either already incurred in past or which is to be

incurred in future but determination of occurrence is already decided in past. Fixed cost is

considered irrelevant in all type of decisions.

Variable cost: It is cost which is increased as per the volume of operations but per unit cost shall

be remain constant in different volume of operations.

Indirect cost: it may be defined as cost which is incurred in production process and can not be

identified in particular product.

Absorption costing:

It is a managerial accounting cost method for calculating all costs related with In

absorption costing, an organisation consider all types of cost whether it is historical or future

cost (i.e. relevant cost, irrelevant cost or sunk cost). This costing method is used by the

enterprises when they want to find out the total cost of its regular product which it is producing

and for which, there is a demand in the market. In this costing method, company consider the

fixed cost (either avoidable fixed cost or unavoidable fixed cost) (Lavia López and Hiebl, 2014).

Marginal Costing:

In marginal costing, an organisation consider only that cost which is relevant for producing an

product (i.e. relevant cost only). This costing method is used by the enterprises when they want to find

out the minimum cost which will be incurred if company will produce that product. The product which

has no demand in existing market but it comes as an offer from new market or an offer from new

customer. In this costing method, company shall not consider fixed cost at all (Jacobs, 2012).

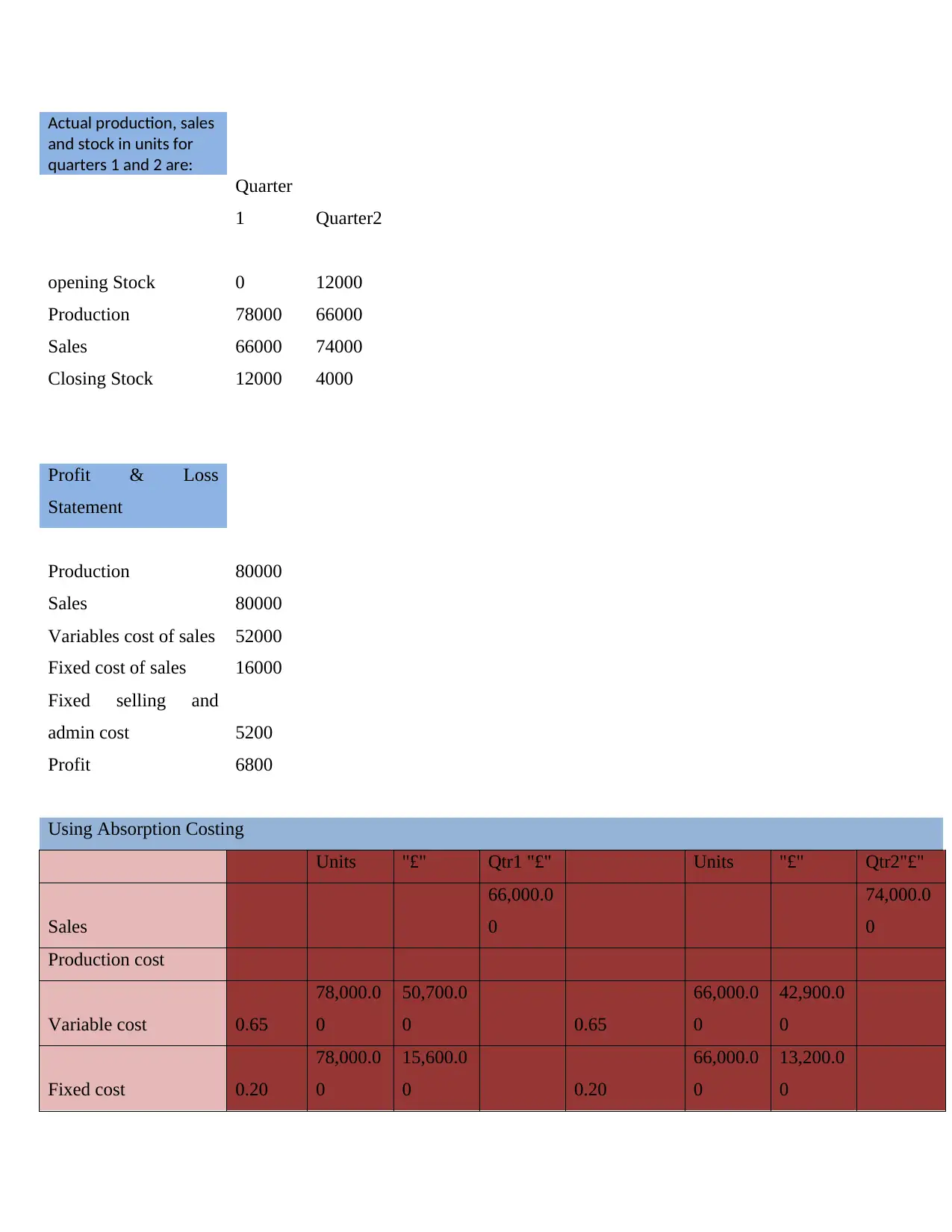

Actual production, sales

and stock in units for

quarters 1 and 2 are:

Quarter

1 Quarter2

opening Stock 0 12000

Production 78000 66000

Sales 66000 74000

Closing Stock 12000 4000

Profit & Loss

Statement

Production 80000

Sales 80000

Variables cost of sales 52000

Fixed cost of sales 16000

Fixed selling and

admin cost 5200

Profit 6800

Using Absorption Costing

Units "£" Qtr1 "£" Units "£" Qtr2"£"

Sales

66,000.0

0

74,000.0

0

Production cost

Variable cost 0.65

78,000.0

0

50,700.0

0 0.65

66,000.0

0

42,900.0

0

Fixed cost 0.20

78,000.0

0

15,600.0

0 0.20

66,000.0

0

13,200.0

0

and stock in units for

quarters 1 and 2 are:

Quarter

1 Quarter2

opening Stock 0 12000

Production 78000 66000

Sales 66000 74000

Closing Stock 12000 4000

Profit & Loss

Statement

Production 80000

Sales 80000

Variables cost of sales 52000

Fixed cost of sales 16000

Fixed selling and

admin cost 5200

Profit 6800

Using Absorption Costing

Units "£" Qtr1 "£" Units "£" Qtr2"£"

Sales

66,000.0

0

74,000.0

0

Production cost

Variable cost 0.65

78,000.0

0

50,700.0

0 0.65

66,000.0

0

42,900.0

0

Fixed cost 0.20

78,000.0

0

15,600.0

0 0.20

66,000.0

0

13,200.0

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

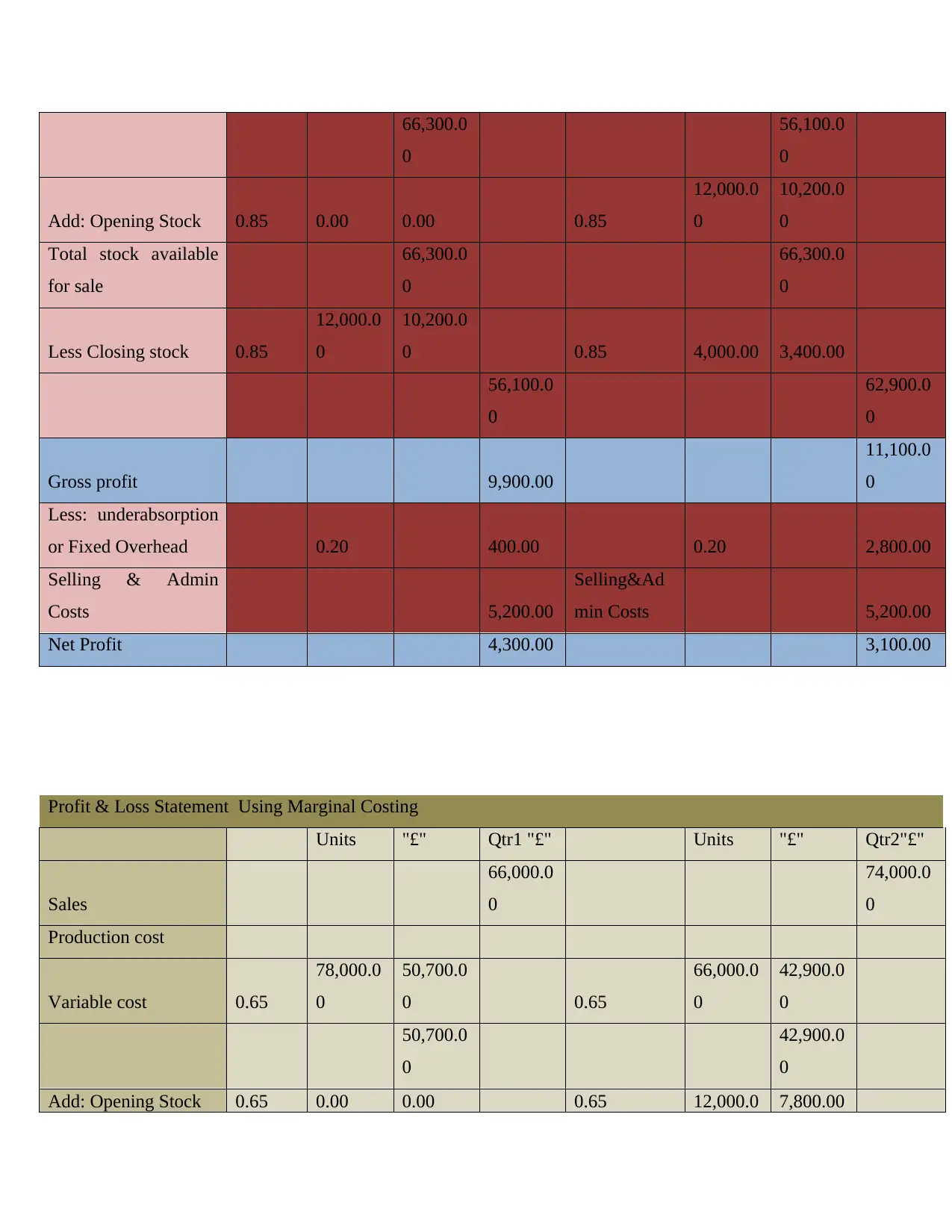

66,300.0

0

56,100.0

0

Add: Opening Stock 0.85 0.00 0.00 0.85

12,000.0

0

10,200.0

0

Total stock available

for sale

66,300.0

0

66,300.0

0

Less Closing stock 0.85

12,000.0

0

10,200.0

0 0.85 4,000.00 3,400.00

56,100.0

0

62,900.0

0

Gross profit 9,900.00

11,100.0

0

Less: underabsorption

or Fixed Overhead 0.20 400.00 0.20 2,800.00

Selling & Admin

Costs 5,200.00

Selling&Ad

min Costs 5,200.00

Net Profit 4,300.00 3,100.00

Profit & Loss Statement Using Marginal Costing

Units "£" Qtr1 "£" Units "£" Qtr2"£"

Sales

66,000.0

0

74,000.0

0

Production cost

Variable cost 0.65

78,000.0

0

50,700.0

0 0.65

66,000.0

0

42,900.0

0

50,700.0

0

42,900.0

0

Add: Opening Stock 0.65 0.00 0.00 0.65 12,000.0 7,800.00

0

56,100.0

0

Add: Opening Stock 0.85 0.00 0.00 0.85

12,000.0

0

10,200.0

0

Total stock available

for sale

66,300.0

0

66,300.0

0

Less Closing stock 0.85

12,000.0

0

10,200.0

0 0.85 4,000.00 3,400.00

56,100.0

0

62,900.0

0

Gross profit 9,900.00

11,100.0

0

Less: underabsorption

or Fixed Overhead 0.20 400.00 0.20 2,800.00

Selling & Admin

Costs 5,200.00

Selling&Ad

min Costs 5,200.00

Net Profit 4,300.00 3,100.00

Profit & Loss Statement Using Marginal Costing

Units "£" Qtr1 "£" Units "£" Qtr2"£"

Sales

66,000.0

0

74,000.0

0

Production cost

Variable cost 0.65

78,000.0

0

50,700.0

0 0.65

66,000.0

0

42,900.0

0

50,700.0

0

42,900.0

0

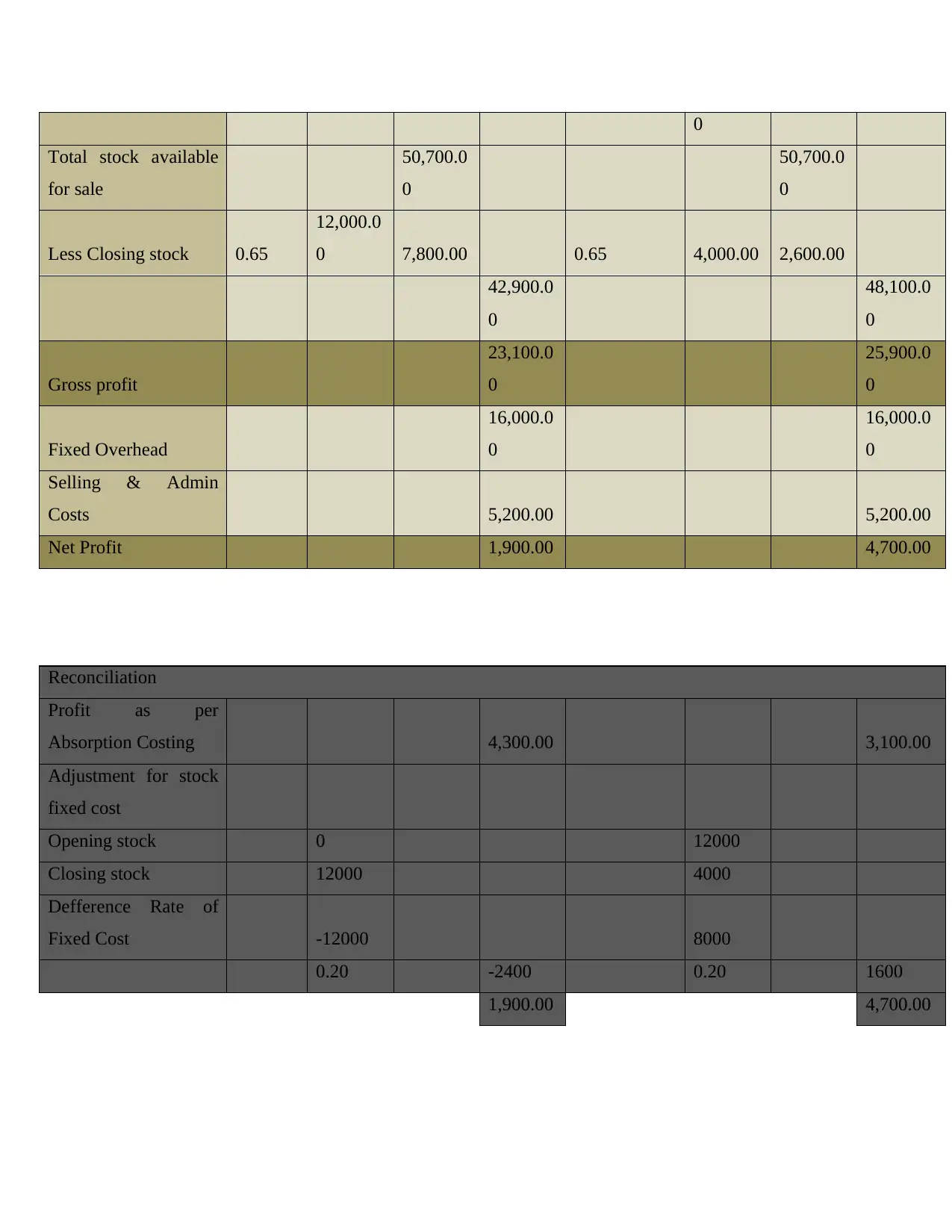

Add: Opening Stock 0.65 0.00 0.00 0.65 12,000.0 7,800.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0

Total stock available

for sale

50,700.0

0

50,700.0

0

Less Closing stock 0.65

12,000.0

0 7,800.00 0.65 4,000.00 2,600.00

42,900.0

0

48,100.0

0

Gross profit

23,100.0

0

25,900.0

0

Fixed Overhead

16,000.0

0

16,000.0

0

Selling & Admin

Costs 5,200.00 5,200.00

Net Profit 1,900.00 4,700.00

Reconciliation

Profit as per

Absorption Costing 4,300.00 3,100.00

Adjustment for stock

fixed cost

Opening stock 0 12000

Closing stock 12000 4000

Defference Rate of

Fixed Cost -12000 8000

0.20 -2400 0.20 1600

1,900.00 4,700.00

Total stock available

for sale

50,700.0

0

50,700.0

0

Less Closing stock 0.65

12,000.0

0 7,800.00 0.65 4,000.00 2,600.00

42,900.0

0

48,100.0

0

Gross profit

23,100.0

0

25,900.0

0

Fixed Overhead

16,000.0

0

16,000.0

0

Selling & Admin

Costs 5,200.00 5,200.00

Net Profit 1,900.00 4,700.00

Reconciliation

Profit as per

Absorption Costing 4,300.00 3,100.00

Adjustment for stock

fixed cost

Opening stock 0 12000

Closing stock 12000 4000

Defference Rate of

Fixed Cost -12000 8000

0.20 -2400 0.20 1600

1,900.00 4,700.00

Interpretation- On the basis of above mentioned numerical it can be analysed that there are two

techniques are used which are absorption and marginal costing method. In the absorption

costing net profit is of 4300 & 3100 in both quarters. While in the marginal costing net profit is

of 1900 & 4700 in both quarters. So it can be interpreted that net profit is different in both

methods.

Reasons for change in profits in absorption costing and marginal costing:

There is difference in gross profit in both marginal costing and absorption costing, this is

Normal and standard costing, activity-based costing and the role of costing in setting price.

happen due to change in procedures of calculating gross profit in the these two costing system.

In absorption costing, fixed production cost is also included while calculating the profits but in

marginal costing, only relevant costs are considered which is incurred due to production of a

product.

M2.Different techniques of management accounting system:

Different management accounting techniques are useful for business entities as they

provide assistance in classifying, analysing, controlling and defining business aspects. There are

various kind of management accounting techniques such as activity based costing system,

standard costing system etc. All these play an important role in the presentation of financial

reports. Accounting techniques help to understand the business. The managerial personnels of

Third way Ltd is applying different kind of techniques in order to formulate financial reports

which provides a fair view about company's business. It also assist in controlling various

function of business to enhance productivity.

TASK 3

P4.Different types of planning tools for budgetary control:

Budget is defined as the estimation of all the income and expenses in an organisation. It

requires planning of earnings for the future period. Thirdway Group prepares budget for

tracking of it's gains and losses over a specified period of time. For understanding the various

planning tools , some term is need to be understandable, which are as follows:

techniques are used which are absorption and marginal costing method. In the absorption

costing net profit is of 4300 & 3100 in both quarters. While in the marginal costing net profit is

of 1900 & 4700 in both quarters. So it can be interpreted that net profit is different in both

methods.

Reasons for change in profits in absorption costing and marginal costing:

There is difference in gross profit in both marginal costing and absorption costing, this is

Normal and standard costing, activity-based costing and the role of costing in setting price.

happen due to change in procedures of calculating gross profit in the these two costing system.

In absorption costing, fixed production cost is also included while calculating the profits but in

marginal costing, only relevant costs are considered which is incurred due to production of a

product.

M2.Different techniques of management accounting system:

Different management accounting techniques are useful for business entities as they

provide assistance in classifying, analysing, controlling and defining business aspects. There are

various kind of management accounting techniques such as activity based costing system,

standard costing system etc. All these play an important role in the presentation of financial

reports. Accounting techniques help to understand the business. The managerial personnels of

Third way Ltd is applying different kind of techniques in order to formulate financial reports

which provides a fair view about company's business. It also assist in controlling various

function of business to enhance productivity.

TASK 3

P4.Different types of planning tools for budgetary control:

Budget is defined as the estimation of all the income and expenses in an organisation. It

requires planning of earnings for the future period. Thirdway Group prepares budget for

tracking of it's gains and losses over a specified period of time. For understanding the various

planning tools , some term is need to be understandable, which are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.