Management Accounting Report: Toyota Automotive Company Analysis

VerifiedAdded on 2020/07/22

|16

|5143

|32

Report

AI Summary

This report delves into the application of management accounting principles within Toyota. It begins by defining management accounting and its importance, contrasting it with financial accounting, and highlighting the various tools and techniques used, such as budgeting, ratio analysis, and variance analysis. The report then explores different costing systems, including expenditure, job costing, and process costing, and their relevance to Toyota's operations. It further examines the activities covered by management accounting reporting, like budget reporting, job costing reporting, and income statements. The core of the report focuses on a comparative analysis of absorption and marginal costing methods using financial data from Toyota, demonstrating how each method impacts profit calculation. The report also discusses the advantages and disadvantages of using budget planning tools for financial control within Toyota. Finally, it concludes by suggesting how management accounting can address Toyota's financial challenges and improve its decision-making processes.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1. Explicate administration accounting and supply the necessary necessitate of various

forms of administration accounting system................................................................................1

P.2. Various activity utilised for administration accounting coverage.......................................3

TASK 2............................................................................................................................................5

P.3. Absorption and marginal cost accounting acting.................................................................5

TASK 3............................................................................................................................................8

P.4. Vantage and disfavour of exploitation preparation implement that can be utilised for fund

control in Toyota company.........................................................................................................8

TASK 4 .........................................................................................................................................10

P.5. Acceptance of administration accounting scheme to response to fiscal problem..............10

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1. Explicate administration accounting and supply the necessary necessitate of various

forms of administration accounting system................................................................................1

P.2. Various activity utilised for administration accounting coverage.......................................3

TASK 2............................................................................................................................................5

P.3. Absorption and marginal cost accounting acting.................................................................5

TASK 3............................................................................................................................................8

P.4. Vantage and disfavour of exploitation preparation implement that can be utilised for fund

control in Toyota company.........................................................................................................8

TASK 4 .........................................................................................................................................10

P.5. Acceptance of administration accounting scheme to response to fiscal problem..............10

REFERENCES..............................................................................................................................13

INTRODUCTION

In this assignment, it reviews about to the different kinds of administration explanation

implement that could be utilised by Toyota corporation in order to effective management of their

operational exercises within the business effectively. Toyota business can utilise different kinds

of budgeting preparation approaches like cash budgeting, capital budgeting etc. in order to set the

desired targets and also can efficiently achieve them. We utilised some financial data of Toyota

automotive business to cost analysis of the firm in effective manner by using marginal costing

approach and absorption costing method. Furthermore, this study shows about advantages and

disadvantages of several kinds of management accounting budget planning tools in order to

sufficient budgeting control in the business in effective manner. Management accounting provide

some tools and techniques which must be effectively utilised by Toyota business in the firm in

order to accomplishment of their financial goals. Ultimately, we will discuss about to some

management accounting tools that can be helpful for Toyota automotive business in order to

better response for their financial problems and barriers in within the organisation in efficient

manner.

TASK 1

P.1. Explicate administration accounting and supply the necessary necessitate of various forms of

administration accounting system

To,

The General Manager of Toyota automotive Company, Japan. Date: 27th February 2018

Sub: Management accounting system acceptance and their importance.

Administration accounting define about the method in which business information is plumbed,

recognised and understood and assessed and connect financial issues and problem and follow

the process to accomplish organisational goals and objectives effectively. It is also concerned

about the cost accounting process in the business (Budding, Grossi and Tagesson, 2014). The

major differences between administration accounting and business accounting is that

information assessed by the administration accounting subordinate the manager of the

institution in order to make effective decision towards accomplishment of financial goals and

objectives of the business. Moreover, cost accounting refers to the information which is

provided to external party in the firm. Management accounting provides guidelines to the

1

In this assignment, it reviews about to the different kinds of administration explanation

implement that could be utilised by Toyota corporation in order to effective management of their

operational exercises within the business effectively. Toyota business can utilise different kinds

of budgeting preparation approaches like cash budgeting, capital budgeting etc. in order to set the

desired targets and also can efficiently achieve them. We utilised some financial data of Toyota

automotive business to cost analysis of the firm in effective manner by using marginal costing

approach and absorption costing method. Furthermore, this study shows about advantages and

disadvantages of several kinds of management accounting budget planning tools in order to

sufficient budgeting control in the business in effective manner. Management accounting provide

some tools and techniques which must be effectively utilised by Toyota business in the firm in

order to accomplishment of their financial goals. Ultimately, we will discuss about to some

management accounting tools that can be helpful for Toyota automotive business in order to

better response for their financial problems and barriers in within the organisation in efficient

manner.

TASK 1

P.1. Explicate administration accounting and supply the necessary necessitate of various forms of

administration accounting system

To,

The General Manager of Toyota automotive Company, Japan. Date: 27th February 2018

Sub: Management accounting system acceptance and their importance.

Administration accounting define about the method in which business information is plumbed,

recognised and understood and assessed and connect financial issues and problem and follow

the process to accomplish organisational goals and objectives effectively. It is also concerned

about the cost accounting process in the business (Budding, Grossi and Tagesson, 2014). The

major differences between administration accounting and business accounting is that

information assessed by the administration accounting subordinate the manager of the

institution in order to make effective decision towards accomplishment of financial goals and

objectives of the business. Moreover, cost accounting refers to the information which is

provided to external party in the firm. Management accounting provides guidelines to the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manager of Toyota automotive from to prepare report of statical and financial data which

fluctuate in the business in day to day process and according to them manage make their

decision. It is the process of preparing report to reach to requirements of the management in

effective manner. Several types of strategy can be applied on Toyota automotive business to

prepare budget reporting, ration analysis, variance analysis, marginal costing etc. all these

approaches could assist Toyota automotive business in order to efficient manage discipline of

standard in which the organisation must follow in respect to manage all aspects of the business

in effective form. Expenditure accounting scheme: Expenditure accounting scheme is used by mostly

manufacturing industry in order to determine their actual costing rate of producing

product and according to this approach, manufacturing cost could be reduced

effectively. This approach describe about to the method in which production and

service provision cost and expenses are computed and assessed on the basis of fixed

expenses, variable expenses and semi variable expenses (McManus, 2011). Above three

expenses are unique in their nature and they have also particular approach to collection

of expenses information in the business. In this approach it could be said that all

expenses are computed in management accounting books with the assistance of specific

method of accounting. Multiple numbers of advantages are presented here, Toyota

automotive corporation manager can easily find out the all expenses which has been

done in the business while production process at the workplace. Toyota manager need

to formulate cost accounting project in which organisational manager could easily find

out all kinds of expenses in automotive company and project will reduce the cost of all

expenses in the firm and also formulate specific adjustment in the process of cost

reduction strategy can be implemented on the business in effective manner. Thus, it can

be stated that several kinds of advantages of Toyota automotive business presented here

in order to reduce all costing of manufacturing products with the help of tools and

techniques of cost reduction in the firm efficiently. Job costing system: Job costing is the process which can be used most of the

manufacturing companies like Toyota automotive corporation in order to computing

proper data about to costing associated with particular product and services in the job

costing approach (Leitner, S., 2013). The job costing information could be needed in

2

fluctuate in the business in day to day process and according to them manage make their

decision. It is the process of preparing report to reach to requirements of the management in

effective manner. Several types of strategy can be applied on Toyota automotive business to

prepare budget reporting, ration analysis, variance analysis, marginal costing etc. all these

approaches could assist Toyota automotive business in order to efficient manage discipline of

standard in which the organisation must follow in respect to manage all aspects of the business

in effective form. Expenditure accounting scheme: Expenditure accounting scheme is used by mostly

manufacturing industry in order to determine their actual costing rate of producing

product and according to this approach, manufacturing cost could be reduced

effectively. This approach describe about to the method in which production and

service provision cost and expenses are computed and assessed on the basis of fixed

expenses, variable expenses and semi variable expenses (McManus, 2011). Above three

expenses are unique in their nature and they have also particular approach to collection

of expenses information in the business. In this approach it could be said that all

expenses are computed in management accounting books with the assistance of specific

method of accounting. Multiple numbers of advantages are presented here, Toyota

automotive corporation manager can easily find out the all expenses which has been

done in the business while production process at the workplace. Toyota manager need

to formulate cost accounting project in which organisational manager could easily find

out all kinds of expenses in automotive company and project will reduce the cost of all

expenses in the firm and also formulate specific adjustment in the process of cost

reduction strategy can be implemented on the business in effective manner. Thus, it can

be stated that several kinds of advantages of Toyota automotive business presented here

in order to reduce all costing of manufacturing products with the help of tools and

techniques of cost reduction in the firm efficiently. Job costing system: Job costing is the process which can be used most of the

manufacturing companies like Toyota automotive corporation in order to computing

proper data about to costing associated with particular product and services in the job

costing approach (Leitner, S., 2013). The job costing information could be needed in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

respect to submit a cost data to their customers into a contract where costs are give back.

This data assessment also necessary for Toyota automotive business in order to

ascertaining the quality of firm's assuming system which should be in given criteria and

that give the business effective profitability in the industry effectively. There are several

kinds of customised products are being acquired by Toyota automotive business at the

workplace and they all need give a specific cost to each particular customised product

and services in the business in effective manner (Qu, Cooper and Ezzamel, 2010).

Manager of Toyota Company can maintain a job costing accounting book in which they

can gather each custom product line costing and other several expenses as well in order

to classification of costing of each product line and with the help of tools they can

reduce costing of each product at the workplace.

Process costing: This is the process which can be used majorly by manufacturing

companies in the country like Toyota Company. Process costing is being used where

there are large volumes of manufacturing process being done on a particular

homogeneous product and services. It is helpful where each product volume could not

make differentiate from each other in mass production. Cost of each product

manufacturing must be same assumed as other products are being produced in the

company. In this approach cost of each product can be amassed during a given time

period. This approach can be used by Toyota Automotive company in order to prepare a

proper process costing methodology in the business in order to give a proper costing to

each customised product line in the enterprise effectively.

P.2. Various activity utilised for administration accounting coverage

Administration accounting reporting can be useful in order to operate each financial

function in the business in effective manner (B Douglas Clinton CMA, 2012). Toyota

Automotive Company required to implementation of various kinds of management accounting

reporting system at management level at the workplace in order to appropriate reporting can be

prepared by management accounting offices of Toyota business. With the assistance of these

approaches Toyota Automotive corporation can improve the financial performances of the firm

and easily can meet to their desired goals and objective in the business efficiently.

3

This data assessment also necessary for Toyota automotive business in order to

ascertaining the quality of firm's assuming system which should be in given criteria and

that give the business effective profitability in the industry effectively. There are several

kinds of customised products are being acquired by Toyota automotive business at the

workplace and they all need give a specific cost to each particular customised product

and services in the business in effective manner (Qu, Cooper and Ezzamel, 2010).

Manager of Toyota Company can maintain a job costing accounting book in which they

can gather each custom product line costing and other several expenses as well in order

to classification of costing of each product line and with the help of tools they can

reduce costing of each product at the workplace.

Process costing: This is the process which can be used majorly by manufacturing

companies in the country like Toyota Company. Process costing is being used where

there are large volumes of manufacturing process being done on a particular

homogeneous product and services. It is helpful where each product volume could not

make differentiate from each other in mass production. Cost of each product

manufacturing must be same assumed as other products are being produced in the

company. In this approach cost of each product can be amassed during a given time

period. This approach can be used by Toyota Automotive company in order to prepare a

proper process costing methodology in the business in order to give a proper costing to

each customised product line in the enterprise effectively.

P.2. Various activity utilised for administration accounting coverage

Administration accounting reporting can be useful in order to operate each financial

function in the business in effective manner (B Douglas Clinton CMA, 2012). Toyota

Automotive Company required to implementation of various kinds of management accounting

reporting system at management level at the workplace in order to appropriate reporting can be

prepared by management accounting offices of Toyota business. With the assistance of these

approaches Toyota Automotive corporation can improve the financial performances of the firm

and easily can meet to their desired goals and objective in the business efficiently.

3

Budget reporting: This is the financial status in the company. There are several kinds of

incomes and expenses are being generated in the business on regular basis. Appropriate

financial information in collected and documented in the financial accounting book

effectively and then prepare a budget according to the gathered data. Budget reporting is

often referred to the financial report of the company as well. Toyota Automotive

business's budget reporting have various parts which grounded on the financial

requirements and also data availability in the corporation as well. In the budget reporting

generate section covers the general income involved which is being done in the firm

while manufacturing process. Moreover, fixed and variable expenses are necessary to be

involved in the budget reporting process in order to run Toyota Automotive firm in

properly with its full potential in the business as well. It also provides proper information

to company's owner about major financial changes in the firm which can furnish

appropriate benefits to the company (Harris and Mongiello, 2012). Apart from this

budget reporting provides the value of the future prediction about Toyota Automotive

corporation's profit gain as well. Usually, This is prepared by financial experts of the

company on yearly basis. But large manufacturing company like Toyota Automotive

firm need to prepare it on quarterly basis in order to make it easy to formulate for the

company in order to effective cost reduction can be made in the business with the help of

budget reporting tools and mechanism. Job costing reporting: Job cost reporting can furnish critical data about the recent

position of job and could assist to estimation how you would complete every job form in

order to effective profitability generation in the business. If you are operating several

activities in the business then it is difficult to effectively manage them in the business.

You can easily recognise omissions and job troubled before it is getting late and with the

assistance of its tools and techniques (Abdel-Kader, ed., 2011). The management

accounting officer of Toyota Automotive Company can easily address them efficiently in

the firm. There might be several jobs in progress so that there is still strong possibility to

cost assigned by accounting officer in the firm which is incorrect. Job costing reporting

furnish detailed information about every job in the firm so that accounting officer of

Toyota Automotive business can easily apportion each product line cost in the firm

directly to the job. Job cost reporting could assist Toyota Automotive firm to ascertain

4

incomes and expenses are being generated in the business on regular basis. Appropriate

financial information in collected and documented in the financial accounting book

effectively and then prepare a budget according to the gathered data. Budget reporting is

often referred to the financial report of the company as well. Toyota Automotive

business's budget reporting have various parts which grounded on the financial

requirements and also data availability in the corporation as well. In the budget reporting

generate section covers the general income involved which is being done in the firm

while manufacturing process. Moreover, fixed and variable expenses are necessary to be

involved in the budget reporting process in order to run Toyota Automotive firm in

properly with its full potential in the business as well. It also provides proper information

to company's owner about major financial changes in the firm which can furnish

appropriate benefits to the company (Harris and Mongiello, 2012). Apart from this

budget reporting provides the value of the future prediction about Toyota Automotive

corporation's profit gain as well. Usually, This is prepared by financial experts of the

company on yearly basis. But large manufacturing company like Toyota Automotive

firm need to prepare it on quarterly basis in order to make it easy to formulate for the

company in order to effective cost reduction can be made in the business with the help of

budget reporting tools and mechanism. Job costing reporting: Job cost reporting can furnish critical data about the recent

position of job and could assist to estimation how you would complete every job form in

order to effective profitability generation in the business. If you are operating several

activities in the business then it is difficult to effectively manage them in the business.

You can easily recognise omissions and job troubled before it is getting late and with the

assistance of its tools and techniques (Abdel-Kader, ed., 2011). The management

accounting officer of Toyota Automotive Company can easily address them efficiently in

the firm. There might be several jobs in progress so that there is still strong possibility to

cost assigned by accounting officer in the firm which is incorrect. Job costing reporting

furnish detailed information about every job in the firm so that accounting officer of

Toyota Automotive business can easily apportion each product line cost in the firm

directly to the job. Job cost reporting could assist Toyota Automotive firm to ascertain

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

every job costing product line in each manufacture product and efficiently control them

as well in order to control the over range of product line in the business effectively.

Income statement: This is a financial statement which furnish the information about to

financial performance of the company in a specific time period. With the help of

financial statements Toyota Automotive firm can properly assessed of their financial

performance in the given time period like they can assess revenue generation of the

business in effective manner also examined the information about to expenses on

operation and non-operational exercises in the firm effectively. Financial statements also

review about new profit and losses of Toyota Automotive company effectively in a

particular financial duration of the corporation (Zainun Tuanmat and Smith, 2011).

There is no necessity of standard templates for showing the financial information of the

company. Income statements involves some elements like revenue, tax expenses, profit

and loss account, total comprehensive income etc. Toyota Automotive Company can

prepare a proper income statement with the help of its tools in context of easily identify

the financial gain and losses and according to them effectively profitable decision could

be made.

TASK 2

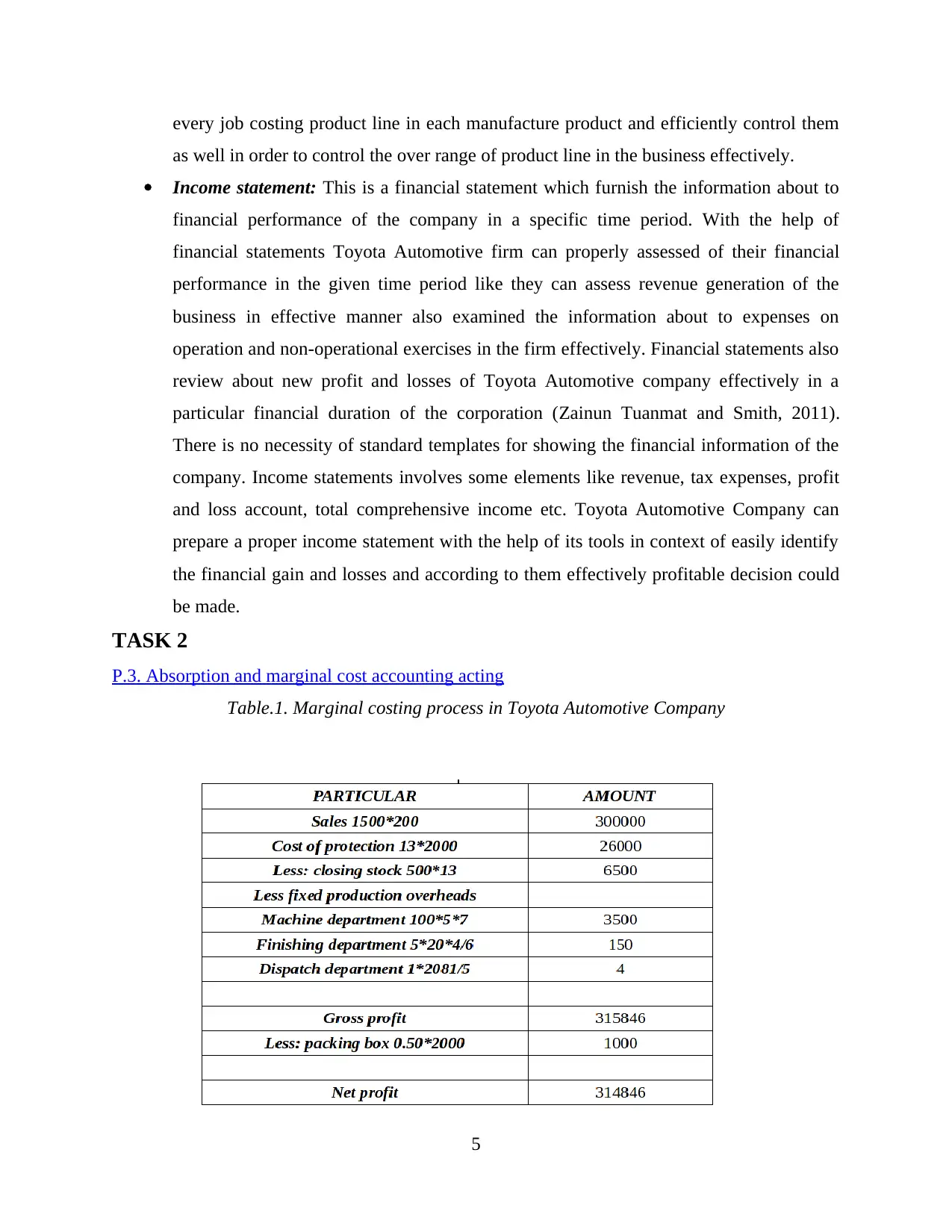

P.3. Absorption and marginal cost accounting acting

Table.1. Marginal costing process in Toyota Automotive Company

5

as well in order to control the over range of product line in the business effectively.

Income statement: This is a financial statement which furnish the information about to

financial performance of the company in a specific time period. With the help of

financial statements Toyota Automotive firm can properly assessed of their financial

performance in the given time period like they can assess revenue generation of the

business in effective manner also examined the information about to expenses on

operation and non-operational exercises in the firm effectively. Financial statements also

review about new profit and losses of Toyota Automotive company effectively in a

particular financial duration of the corporation (Zainun Tuanmat and Smith, 2011).

There is no necessity of standard templates for showing the financial information of the

company. Income statements involves some elements like revenue, tax expenses, profit

and loss account, total comprehensive income etc. Toyota Automotive Company can

prepare a proper income statement with the help of its tools in context of easily identify

the financial gain and losses and according to them effectively profitable decision could

be made.

TASK 2

P.3. Absorption and marginal cost accounting acting

Table.1. Marginal costing process in Toyota Automotive Company

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

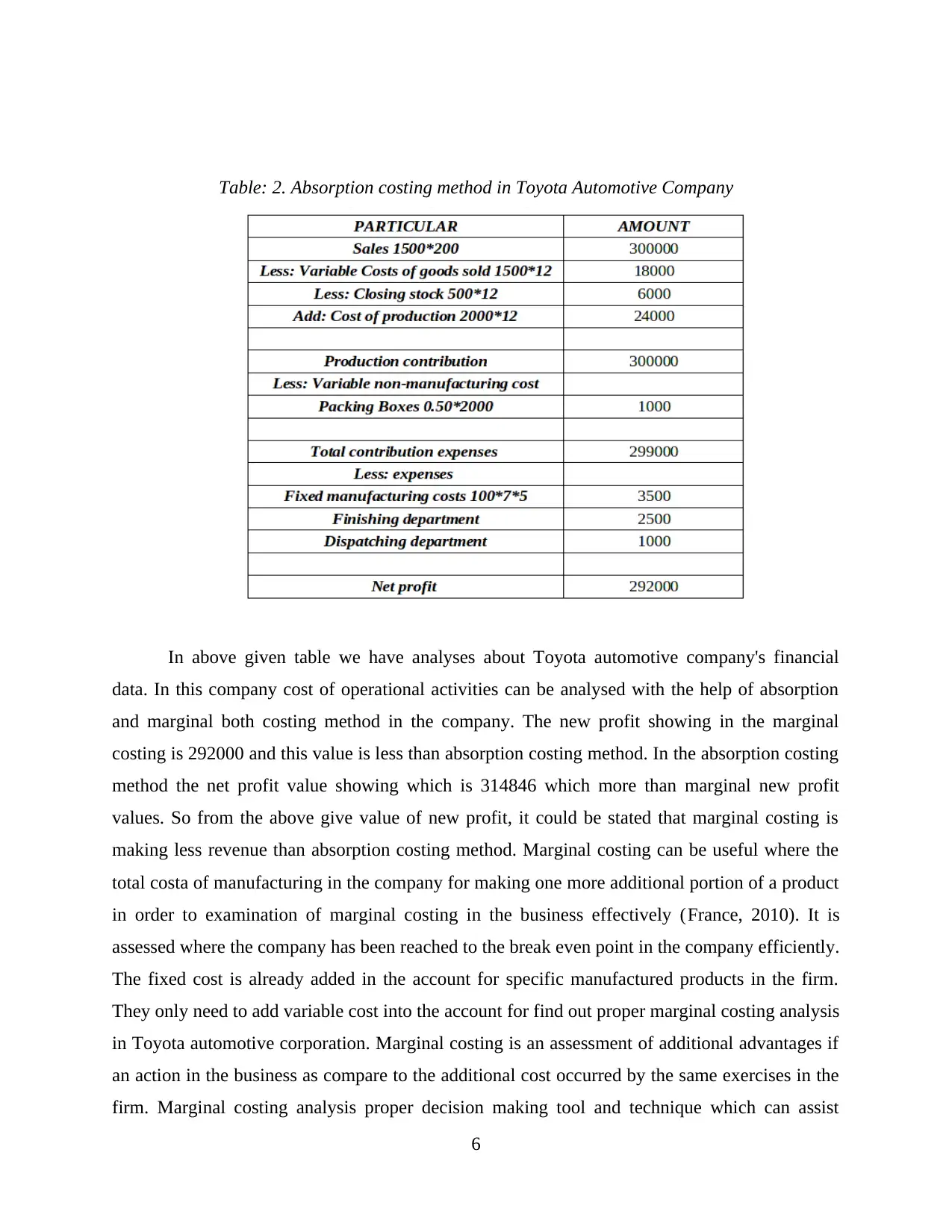

Table: 2. Absorption costing method in Toyota Automotive Company

In above given table we have analyses about Toyota automotive company's financial

data. In this company cost of operational activities can be analysed with the help of absorption

and marginal both costing method in the company. The new profit showing in the marginal

costing is 292000 and this value is less than absorption costing method. In the absorption costing

method the net profit value showing which is 314846 which more than marginal new profit

values. So from the above give value of new profit, it could be stated that marginal costing is

making less revenue than absorption costing method. Marginal costing can be useful where the

total costa of manufacturing in the company for making one more additional portion of a product

in order to examination of marginal costing in the business effectively (France, 2010). It is

assessed where the company has been reached to the break even point in the company efficiently.

The fixed cost is already added in the account for specific manufactured products in the firm.

They only need to add variable cost into the account for find out proper marginal costing analysis

in Toyota automotive corporation. Marginal costing is an assessment of additional advantages if

an action in the business as compare to the additional cost occurred by the same exercises in the

firm. Marginal costing analysis proper decision making tool and technique which can assist

6

In above given table we have analyses about Toyota automotive company's financial

data. In this company cost of operational activities can be analysed with the help of absorption

and marginal both costing method in the company. The new profit showing in the marginal

costing is 292000 and this value is less than absorption costing method. In the absorption costing

method the net profit value showing which is 314846 which more than marginal new profit

values. So from the above give value of new profit, it could be stated that marginal costing is

making less revenue than absorption costing method. Marginal costing can be useful where the

total costa of manufacturing in the company for making one more additional portion of a product

in order to examination of marginal costing in the business effectively (France, 2010). It is

assessed where the company has been reached to the break even point in the company efficiently.

The fixed cost is already added in the account for specific manufactured products in the firm.

They only need to add variable cost into the account for find out proper marginal costing analysis

in Toyota automotive corporation. Marginal costing is an assessment of additional advantages if

an action in the business as compare to the additional cost occurred by the same exercises in the

firm. Marginal costing analysis proper decision making tool and technique which can assist

6

Toyota automotive firm in terms of raise profitability of the business sufficiently. Marginal

costing is reviewing more net profitability than absorption costing method because of some of

fixed variable cost is added into the account of marginal costing method. Moreover, absorption

costing process is a managerial accounting costing approach which all expensing costs in

included which made in the business while producing a product in the business effectively.

Several direct costs are taken into account which is wages and salaries of employees, raw

material cost in manufacturing a product and some other overhead costing in the business like

utility cost utilising in producing a product. Absorption costing method includes all those cost

which is directly associated with manufacturing a good at the workplace. Toyota automotive

firm each product involves some fixed and variable costs into account and these costs are not

considered as expenses when company pays for them (Modell, 2014.).

They are considered as remain inventory in the business and they been taken into account

when inventory is sold in the market. Various positive and negative portions are associated with

both kind of costing analysis approach. With the assistance of both methods' administration

accounting official of Toyota automotive enterprise could easy figure out the growth of the

enterprise properly and then appropriate decision can be made by them in order to improvement

of financial performances of the firm efficiently. In the proceeding of marginal cost accounting,

one action could be recognised which is fixed disbursal is not taking into account immediately

while manufacturing process of Toyota firm. Fixed cost may occur in each production firm and

Toyota automotive Company need to cover these costing in the enterprise efficiently. It can be

stated that same costing system is appropriate for Toyota corporation in order to better financial

management in the enterprise. While expenses are added into account then that make wide level

contribution into the production process of the business. With the assistance of both techniques

business can easily find out the profitability and loss of Toyota automotive firm efficiently

(Macintosh and Quattrone 2010). It can be concluded that Toyota firm must implement these

strategies on their business in respect of determination of their disbursal and revenue within the

firm and terminated disbursal sections could be find out easy and with the assistance of

management accounting instrument and method, administration accounting official of Toyota

automotive enterprise could reduce the cost of production at the workplace. They can better

address the financial issues of this diem effectively with the assistance of these mechanisms

efficiently.

7

costing is reviewing more net profitability than absorption costing method because of some of

fixed variable cost is added into the account of marginal costing method. Moreover, absorption

costing process is a managerial accounting costing approach which all expensing costs in

included which made in the business while producing a product in the business effectively.

Several direct costs are taken into account which is wages and salaries of employees, raw

material cost in manufacturing a product and some other overhead costing in the business like

utility cost utilising in producing a product. Absorption costing method includes all those cost

which is directly associated with manufacturing a good at the workplace. Toyota automotive

firm each product involves some fixed and variable costs into account and these costs are not

considered as expenses when company pays for them (Modell, 2014.).

They are considered as remain inventory in the business and they been taken into account

when inventory is sold in the market. Various positive and negative portions are associated with

both kind of costing analysis approach. With the assistance of both methods' administration

accounting official of Toyota automotive enterprise could easy figure out the growth of the

enterprise properly and then appropriate decision can be made by them in order to improvement

of financial performances of the firm efficiently. In the proceeding of marginal cost accounting,

one action could be recognised which is fixed disbursal is not taking into account immediately

while manufacturing process of Toyota firm. Fixed cost may occur in each production firm and

Toyota automotive Company need to cover these costing in the enterprise efficiently. It can be

stated that same costing system is appropriate for Toyota corporation in order to better financial

management in the enterprise. While expenses are added into account then that make wide level

contribution into the production process of the business. With the assistance of both techniques

business can easily find out the profitability and loss of Toyota automotive firm efficiently

(Macintosh and Quattrone 2010). It can be concluded that Toyota firm must implement these

strategies on their business in respect of determination of their disbursal and revenue within the

firm and terminated disbursal sections could be find out easy and with the assistance of

management accounting instrument and method, administration accounting official of Toyota

automotive enterprise could reduce the cost of production at the workplace. They can better

address the financial issues of this diem effectively with the assistance of these mechanisms

efficiently.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P.4. Vantage and disfavour of exploitation preparation implement that can be utilised for fund

control in Toyota company

There are several kinds of management accounting tools and techniques available which

can be used in terms of effective management and control on budget at the workplace. Various

types of planning tools could be implemented on Toyota automotive business in order to

resolution of their financial issues in more effective manner (Bennett, Schaltegger and

Zvezdov,2013). These all planning tools have some advantage and disadvantages. Variety of

planning tools are available here in respect of formulation of efficient budgeting control at

Toyota automotive company's workplace.

Cash budgeting: Cash budgeting is a process in which approximation of cash inflow and

outflow is taken into the account in a business during a given financial time period. This

approach can be used by Toyota automotive firm to determination of how much volume of cash

available here for effective run the business in the industry. Toyota automotive companies can

utilisation of sales and forecasting strategy in order to formulate cash budgeting and apart from

this they can assume the expenses and account receivable in the business as well while preparing

cash budgeting in the firm. There are some vantage and disfavour of currency budgeting is as

below:

Advantages:

Cash budgeting planning helps the management of the firm to take their focus on

significant matters which must be taken in appropriate form to resolve financial issues

efficiently. It assists the manager of the firm to think forwards in order to effective management of

financial resources at the workplace effectively (.Hilton and Platt, 2013).

Disadvantages:

Major disfavour of currency program is that it is wholly based on the approximation of

cash flow in the business while preparing it so several times approximate value difficult

to meet in the business. Another main disadvantage is that it might take long time to accomplishment of their

desired target.

8

P.4. Vantage and disfavour of exploitation preparation implement that can be utilised for fund

control in Toyota company

There are several kinds of management accounting tools and techniques available which

can be used in terms of effective management and control on budget at the workplace. Various

types of planning tools could be implemented on Toyota automotive business in order to

resolution of their financial issues in more effective manner (Bennett, Schaltegger and

Zvezdov,2013). These all planning tools have some advantage and disadvantages. Variety of

planning tools are available here in respect of formulation of efficient budgeting control at

Toyota automotive company's workplace.

Cash budgeting: Cash budgeting is a process in which approximation of cash inflow and

outflow is taken into the account in a business during a given financial time period. This

approach can be used by Toyota automotive firm to determination of how much volume of cash

available here for effective run the business in the industry. Toyota automotive companies can

utilisation of sales and forecasting strategy in order to formulate cash budgeting and apart from

this they can assume the expenses and account receivable in the business as well while preparing

cash budgeting in the firm. There are some vantage and disfavour of currency budgeting is as

below:

Advantages:

Cash budgeting planning helps the management of the firm to take their focus on

significant matters which must be taken in appropriate form to resolve financial issues

efficiently. It assists the manager of the firm to think forwards in order to effective management of

financial resources at the workplace effectively (.Hilton and Platt, 2013).

Disadvantages:

Major disfavour of currency program is that it is wholly based on the approximation of

cash flow in the business while preparing it so several times approximate value difficult

to meet in the business. Another main disadvantage is that it might take long time to accomplishment of their

desired target.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed budget: Fixed budget is a management accounting planning tools which remains

unchanged whether sales and other exercises in the business raised and decreased. This is also

called a statical budgeting planning tool (Ramljak and Rogošić, 2012). As mentioned above in

never get changed so that disbursal in the business also never change while revenue of the

business fluctuate frequently. This is used when company in monopoly situation in which their

customer have no other option to chose other substitute of it.

Advantages:

The major advantages of fixed budgeting is that it is easy to implement on the business

because of static budget no need for frequent update in this budget planning tool. Fixed budgeting furnish strong value insight the company about cost and profitability

while variance analysis is being done in the business effectively.

Disadvantages:

The greatest disadvantage of fixed budgeting is that it's value always remain same and

never get changed (Burritt and Schaltegger, 2010.). This factor negative effect the

company profitability in the business. Fixed budgeting is depended on last few years values so that new business can

constituted in more challenging manner.

Zero based budgeting: In zero based budgeting process all disbursals should be justified

for every new financial period of the business. This is the budgeting process which start from

zero base in the firm and every utility in the corporation must be examined with the help of

requirements and costs needs in the firm. Toyota company can apply it on their business in order

to effective budgeting planning.

Advantages:

In zero based budgeting make each and every department in the business cost is

calculated on every operational activities of the firm. This budgeting process assist proper allotment of financial resources as departmental

wise so that it does not need historical data it is based in the actual data in the firm.

Disadvantages:

Zero base budgeting is a very lengthy process for each form so that it takes times to

formulation in the business so that it consumes quality of times of the company.

9

unchanged whether sales and other exercises in the business raised and decreased. This is also

called a statical budgeting planning tool (Ramljak and Rogošić, 2012). As mentioned above in

never get changed so that disbursal in the business also never change while revenue of the

business fluctuate frequently. This is used when company in monopoly situation in which their

customer have no other option to chose other substitute of it.

Advantages:

The major advantages of fixed budgeting is that it is easy to implement on the business

because of static budget no need for frequent update in this budget planning tool. Fixed budgeting furnish strong value insight the company about cost and profitability

while variance analysis is being done in the business effectively.

Disadvantages:

The greatest disadvantage of fixed budgeting is that it's value always remain same and

never get changed (Burritt and Schaltegger, 2010.). This factor negative effect the

company profitability in the business. Fixed budgeting is depended on last few years values so that new business can

constituted in more challenging manner.

Zero based budgeting: In zero based budgeting process all disbursals should be justified

for every new financial period of the business. This is the budgeting process which start from

zero base in the firm and every utility in the corporation must be examined with the help of

requirements and costs needs in the firm. Toyota company can apply it on their business in order

to effective budgeting planning.

Advantages:

In zero based budgeting make each and every department in the business cost is

calculated on every operational activities of the firm. This budgeting process assist proper allotment of financial resources as departmental

wise so that it does not need historical data it is based in the actual data in the firm.

Disadvantages:

Zero base budgeting is a very lengthy process for each form so that it takes times to

formulation in the business so that it consumes quality of times of the company.

9

It needs large numbers of highly efficient employees in order to preparation of zero based

budgeting and many companies does not have time to prepare it properly within the firm.

Capital budgeting method: Capital budgeting is the process in which a company

ascertain and examine potential disbursal or some investment which is large in the business.

These disbursals and investments included some projects of the business such as building a new

plant and investment in long terms business in several markets (DRURY, 2013). Toyota business

can apply capital budgeting process on their business to resolve financial problems effectively.

Advantages:

Capital budgeting assist the business to easily identify the investment alternative in which

the company can gain more effective yield from the market. It is also helpful tools for the business in order to formulate long terms investment

planning for the business in efficient form.

Disadvantages:

The major disadvantage of capital budgeting process is that it is long terms investment

process and it is totally irreversible investment in nature (Lukka and Modell, 2010).

This mechanism it totally based on the approximation and estimation so that its future

return always remain uncertain within the firm efficiently.

TASK 4

P.5. Acceptance of administration accounting scheme to response to fiscal problem

Most of the businesses faces several financial issues in the business cycle and

management accounting is the system which furnish several tools and techniques by which each

corporation can address their financial problems in effective form (Ward, 2012). Toyota

automotive company also can implement some management accounting tools in the business in

order to better response of each financial problem within the business efficiently. Key performance indicator: KPI is a tool which can be used for measuring financial

values and it is also demonstrated how effective business are running in the industry in

terms of accomplishment of their desired goals and key objectives (Bebbington and

Thomson, 2013). Toyota company utilise KPI tools at several stages in the firm in order

to evaluation of their achieving targets at top level. High level of KPI tools assist the

organisation to identify the overall executions of the organisation and low level of KPI

tool evaluate the departmental performances such as sales and marketing and call centre

10

budgeting and many companies does not have time to prepare it properly within the firm.

Capital budgeting method: Capital budgeting is the process in which a company

ascertain and examine potential disbursal or some investment which is large in the business.

These disbursals and investments included some projects of the business such as building a new

plant and investment in long terms business in several markets (DRURY, 2013). Toyota business

can apply capital budgeting process on their business to resolve financial problems effectively.

Advantages:

Capital budgeting assist the business to easily identify the investment alternative in which

the company can gain more effective yield from the market. It is also helpful tools for the business in order to formulate long terms investment

planning for the business in efficient form.

Disadvantages:

The major disadvantage of capital budgeting process is that it is long terms investment

process and it is totally irreversible investment in nature (Lukka and Modell, 2010).

This mechanism it totally based on the approximation and estimation so that its future

return always remain uncertain within the firm efficiently.

TASK 4

P.5. Acceptance of administration accounting scheme to response to fiscal problem

Most of the businesses faces several financial issues in the business cycle and

management accounting is the system which furnish several tools and techniques by which each

corporation can address their financial problems in effective form (Ward, 2012). Toyota

automotive company also can implement some management accounting tools in the business in

order to better response of each financial problem within the business efficiently. Key performance indicator: KPI is a tool which can be used for measuring financial

values and it is also demonstrated how effective business are running in the industry in

terms of accomplishment of their desired goals and key objectives (Bebbington and

Thomson, 2013). Toyota company utilise KPI tools at several stages in the firm in order

to evaluation of their achieving targets at top level. High level of KPI tools assist the

organisation to identify the overall executions of the organisation and low level of KPI

tool evaluate the departmental performances such as sales and marketing and call centre

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.