Financial Analysis: Management Accounting Report for Toyota Ltd

VerifiedAdded on 2020/06/04

|13

|3000

|235

Report

AI Summary

This report delves into the management accounting practices of Toyota Ltd, a prominent UK-based car manufacturer. It begins by outlining the crucial role of a management accountant in planning and controlling Toyota's business activities, emphasizing financial stewardship, decision-making processes, and the importance of a management information system. The report then provides a detailed explanation of cost classification, including direct and indirect costs, and cost behavior (fixed, variable, and semi-variable costs), along with cost cards for direct materials, labor, and variable overheads. Furthermore, it explores the preparation and significance of various budgets, such as sales, production, direct material, direct labor, and variable overhead budgets, and highlights the importance of variance analysis as a key management accounting tool for identifying and addressing discrepancies between planned and actual financial performance. The report concludes by emphasizing the significance of these tools for effective cost control and profitability enhancement within Toyota.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1) ROLE OF MANAGEMENT ACCOUNTANT FOR PLANNING AND CONTROLLING

BUSINESS ACTIVITIES OF TOYOTA (300)..............................................................................1

2) COST CLASSIFICATION AND BEHAVIOUR (650)..............................................................2

Reasons behind cost classification on the basis of their.............................................................2

3) SEVERAL BUDGETS FOR TOYOTA ....................................................................................5

Sales budget................................................................................................................................5

Production budget.......................................................................................................................5

Direct material budget.................................................................................................................5

Direct labour budget....................................................................................................................5

Variable overhead budget...........................................................................................................6

Importance of preparing and identified budgets.........................................................................6

4) SIGNIFICANCE OF VARIANCE ANALYSIS.........................................................................6

CONCLUSION................................................................................................................................6

REFERENCE...................................................................................................................................8

APPENDIX......................................................................................................................................9

INTRODUCTION...........................................................................................................................1

1) ROLE OF MANAGEMENT ACCOUNTANT FOR PLANNING AND CONTROLLING

BUSINESS ACTIVITIES OF TOYOTA (300)..............................................................................1

2) COST CLASSIFICATION AND BEHAVIOUR (650)..............................................................2

Reasons behind cost classification on the basis of their.............................................................2

3) SEVERAL BUDGETS FOR TOYOTA ....................................................................................5

Sales budget................................................................................................................................5

Production budget.......................................................................................................................5

Direct material budget.................................................................................................................5

Direct labour budget....................................................................................................................5

Variable overhead budget...........................................................................................................6

Importance of preparing and identified budgets.........................................................................6

4) SIGNIFICANCE OF VARIANCE ANALYSIS.........................................................................6

CONCLUSION................................................................................................................................6

REFERENCE...................................................................................................................................8

APPENDIX......................................................................................................................................9

INDEX OF TABLES

Table 1: Direct material cost card....................................................................................................4

Table 2: Labour cost card................................................................................................................4

Table 3: Variable overhead cost card...............................................................................................4

Table 4: Sales budget for Toyota Ltd..............................................................................................9

Table 5: Production budget for Toyota Ltd.....................................................................................9

Table 6: Direct material budget for Toyota Ltd...............................................................................9

Table 7: Direct labour budget for Toyota Ltd................................................................................10

Table 8: Direct variable overhead budget for Toyota Ltd.............................................................10

Table 1: Direct material cost card....................................................................................................4

Table 2: Labour cost card................................................................................................................4

Table 3: Variable overhead cost card...............................................................................................4

Table 4: Sales budget for Toyota Ltd..............................................................................................9

Table 5: Production budget for Toyota Ltd.....................................................................................9

Table 6: Direct material budget for Toyota Ltd...............................................................................9

Table 7: Direct labour budget for Toyota Ltd................................................................................10

Table 8: Direct variable overhead budget for Toyota Ltd.............................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is multidisciplinary approach which is helpful for decision

making and preparing strategies for creating further innovations in business operations. It

includes costing and budgeting for decision making and forecasting for implementations. The

present report is based on understanding ways to cost control for production of goods and

services as well increasing profitability for Toyota Ltd working in manufacturing industry. It is

one of the well kn own entity of UK which provides varieties of cars and vehicle equipment to

million customers globally. In this regard, role of management accountant for decision making

regarding business operations for entity is to be described (Management Accounting, 2016).

However, cost classifications and characteristics can express through this assignment. Moreover,

different budget as estimation for incurring expenses including sales, purchase, material and

overhead is to introduced. In order to this, importance of variance analysis for effectiveness of

Toyota can identify. Thus, students are able to understand several tools and aspects of

management accounting through this report for decision making related to business operations

for entity deeply.

1) ROLE OF MANAGEMENT ACCOUNTANT FOR PLANNING AND

CONTROLLING BUSINESS ACTIVITIES OF TOYOTA (300)

To

CEO

TOYOTA Ltd

As per the case scenario, it is recognised that Toyota is planning to cost effectiveness

and increasing its profitability. For this purpose, management accountant of the entity plays

crucial role in relation to planning and controlling over business activities (Akyol, Tuncel and

Bayhan, 2015). However, contribution of management accountant for organisation's

effectiveness can describe below:

Stewardship accounting: Management accountant of Toyota prepares and maintains

financial transactions of the entity. In this regard, actual economic position of

organisation is presented in a systematic manner. However, different business

operations including sales, purchases, overhead and other transactions are maintained

1

Management accounting is multidisciplinary approach which is helpful for decision

making and preparing strategies for creating further innovations in business operations. It

includes costing and budgeting for decision making and forecasting for implementations. The

present report is based on understanding ways to cost control for production of goods and

services as well increasing profitability for Toyota Ltd working in manufacturing industry. It is

one of the well kn own entity of UK which provides varieties of cars and vehicle equipment to

million customers globally. In this regard, role of management accountant for decision making

regarding business operations for entity is to be described (Management Accounting, 2016).

However, cost classifications and characteristics can express through this assignment. Moreover,

different budget as estimation for incurring expenses including sales, purchase, material and

overhead is to introduced. In order to this, importance of variance analysis for effectiveness of

Toyota can identify. Thus, students are able to understand several tools and aspects of

management accounting through this report for decision making related to business operations

for entity deeply.

1) ROLE OF MANAGEMENT ACCOUNTANT FOR PLANNING AND

CONTROLLING BUSINESS ACTIVITIES OF TOYOTA (300)

To

CEO

TOYOTA Ltd

As per the case scenario, it is recognised that Toyota is planning to cost effectiveness

and increasing its profitability. For this purpose, management accountant of the entity plays

crucial role in relation to planning and controlling over business activities (Akyol, Tuncel and

Bayhan, 2015). However, contribution of management accountant for organisation's

effectiveness can describe below:

Stewardship accounting: Management accountant of Toyota prepares and maintains

financial transactions of the entity. In this regard, actual economic position of

organisation is presented in a systematic manner. However, different business

operations including sales, purchases, overhead and other transactions are maintained

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Chouhan, Soral and Chandra, 2017). In addition to this, he ensures monetary security

of the company to present all transactions. Thus, expenses incurred and gained revenue

for business operations are recognised through this accounting system. Moreover,

different financial statements and notes are prepared by management accountant that

shows economic position of entity. Therefore, stewarding accounting is one of the great

function of management accountant to maintain financial security of the entity.

Decision making process: Management accountant of the entity plays crucial role in

decision making for long-term and short-term period. Including this, he forecasts and

makes decision regarding business operations in future time period to achieve its

effectiveness. Thus, corporate strategy, formulating, market strategy are evolved

through this accounting system (El and Lindefors, 2016).

Management Information System: Several information related to business operations

including financial and non-economic are exchanged as well presented by management

accountant. In this regard, discussion about business operations generates different ideas

for optimum utilization of resources and fund (Johnson, 2014). It influences

productivity and profitability of entity. Therefore, appropriate decisions can be made

through this process which remains useful for providing better services.

Thus, from above mentioned performances of management accountant, it is recognised

that he plays vital role in decision making process for Toyota Ltd. However, effective planning

and controlling over business operations and improving its efficiency. It is useful for adequate

allocation of resources and fund that impacts on production system of goods (Laviana and et.al.,

2016). Hence, cost effectiveness for producing cars and vehicle equipment as well profitability

of entity can be improved by effective contribute in planning and decision making for entity's

effectiveness systematically.

2) COST CLASSIFICATION AND BEHAVIOUR (650)

Reasons behind cost classification on the basis of their

a)Types: Types of cost is classified in Direct and indirect costs, Cost which are

accurately traced by Toyota are its direct cost and it is, in contrast to variable cost (Akyol,

2

of the company to present all transactions. Thus, expenses incurred and gained revenue

for business operations are recognised through this accounting system. Moreover,

different financial statements and notes are prepared by management accountant that

shows economic position of entity. Therefore, stewarding accounting is one of the great

function of management accountant to maintain financial security of the entity.

Decision making process: Management accountant of the entity plays crucial role in

decision making for long-term and short-term period. Including this, he forecasts and

makes decision regarding business operations in future time period to achieve its

effectiveness. Thus, corporate strategy, formulating, market strategy are evolved

through this accounting system (El and Lindefors, 2016).

Management Information System: Several information related to business operations

including financial and non-economic are exchanged as well presented by management

accountant. In this regard, discussion about business operations generates different ideas

for optimum utilization of resources and fund (Johnson, 2014). It influences

productivity and profitability of entity. Therefore, appropriate decisions can be made

through this process which remains useful for providing better services.

Thus, from above mentioned performances of management accountant, it is recognised

that he plays vital role in decision making process for Toyota Ltd. However, effective planning

and controlling over business operations and improving its efficiency. It is useful for adequate

allocation of resources and fund that impacts on production system of goods (Laviana and et.al.,

2016). Hence, cost effectiveness for producing cars and vehicle equipment as well profitability

of entity can be improved by effective contribute in planning and decision making for entity's

effectiveness systematically.

2) COST CLASSIFICATION AND BEHAVIOUR (650)

Reasons behind cost classification on the basis of their

a)Types: Types of cost is classified in Direct and indirect costs, Cost which are

accurately traced by Toyota are its direct cost and it is, in contrast to variable cost (Akyol,

2

Tuncel and Bayhan, 2015). Further, not just the salary and wages of employees but the regular

expenses, cost incurred on production of spare parts etc.

Indirect cost which can not be determined exactly, activities which are not regularly

practised in the company and whose cost cannot be traced like for example, cost of depreciation,

salaries and wages, power, occurred in the manufacturing plant.

b) Behaviour: Behaviour: On the basis of behaviour cost is divided into some categories

like, fixed cost, variable cost and semi variable cost.

Fixed Cost: The fixed cost remains unaffected in given period, it does not change with

changes in output and input in the company (El and Lindefors, 2016). For instance, Toyota's

every year depreciation, rent, insurance, property tax, utility remain unchanged and helps in

controlling cost and maximizing profits.

Variable Cost: Increase input and output lead to increase in variable cost and decrease in

input and out lead to decrease in variable cost. Toyota need to control its variable cost like labour

cost, salary and wages, delivery charges, shipping charges to increase its net turnover.

Semi-variable cost: This is the mixture of both cost that is variable and fixed cost, it

keeps on changing a per the volume but not in direct proportion (Johnson, 2014). Like for

example, If Toyota increase the level of production line operations it will lead to change in cost.

c) Functions: Cost of the company is divide into several functions such as production,

administration, selling, finance, distribution, research and development, quality check etc.

Toyota controls its production cost by controlling salaries, labour related expenses, store

expenses etc (Najjar, Strickland and Kaplan, 2016).

The company can monitor its administration cost by keeping a check over charges levied

by bank, office related depreciation, audit and legal fees.

Distribution cost of Toyota includes transportation costs, warehouse rents, commission to

distribution channel etc.

d) Relevance: Companies cost can be relevant and irrelevant, this classification of cost is

helpful for managers in decision making (Sandborn, 2017). In Toyota, when different aspects of

activities are considered, like manager need to select the best alternative which would be

3

expenses, cost incurred on production of spare parts etc.

Indirect cost which can not be determined exactly, activities which are not regularly

practised in the company and whose cost cannot be traced like for example, cost of depreciation,

salaries and wages, power, occurred in the manufacturing plant.

b) Behaviour: Behaviour: On the basis of behaviour cost is divided into some categories

like, fixed cost, variable cost and semi variable cost.

Fixed Cost: The fixed cost remains unaffected in given period, it does not change with

changes in output and input in the company (El and Lindefors, 2016). For instance, Toyota's

every year depreciation, rent, insurance, property tax, utility remain unchanged and helps in

controlling cost and maximizing profits.

Variable Cost: Increase input and output lead to increase in variable cost and decrease in

input and out lead to decrease in variable cost. Toyota need to control its variable cost like labour

cost, salary and wages, delivery charges, shipping charges to increase its net turnover.

Semi-variable cost: This is the mixture of both cost that is variable and fixed cost, it

keeps on changing a per the volume but not in direct proportion (Johnson, 2014). Like for

example, If Toyota increase the level of production line operations it will lead to change in cost.

c) Functions: Cost of the company is divide into several functions such as production,

administration, selling, finance, distribution, research and development, quality check etc.

Toyota controls its production cost by controlling salaries, labour related expenses, store

expenses etc (Najjar, Strickland and Kaplan, 2016).

The company can monitor its administration cost by keeping a check over charges levied

by bank, office related depreciation, audit and legal fees.

Distribution cost of Toyota includes transportation costs, warehouse rents, commission to

distribution channel etc.

d) Relevance: Companies cost can be relevant and irrelevant, this classification of cost is

helpful for managers in decision making (Sandborn, 2017). In Toyota, when different aspects of

activities are considered, like manager need to select the best alternative which would be

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

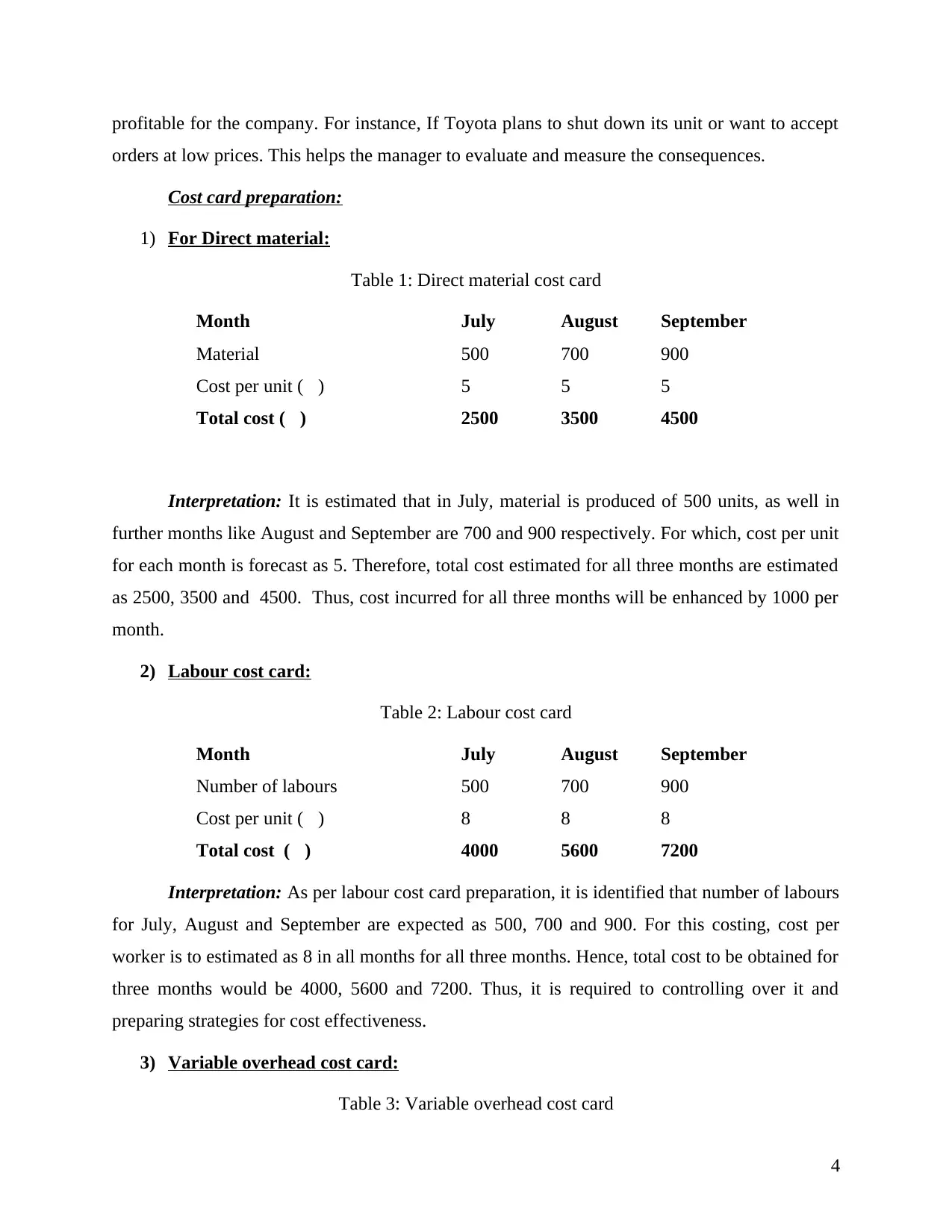

profitable for the company. For instance, If Toyota plans to shut down its unit or want to accept

orders at low prices. This helps the manager to evaluate and measure the consequences.

Cost card preparation:

1) For Direct material:

Table 1: Direct material cost card

Month July August September

Material 500 700 900

Cost per unit (£) 5 5 5

Total cost (£) 2500 3500 4500

Interpretation: It is estimated that in July, material is produced of 500 units, as well in

further months like August and September are 700 and 900 respectively. For which, cost per unit

for each month is forecast as 5. Therefore, total cost estimated for all three months are estimated

as 2500, 3500 and 4500. Thus, cost incurred for all three months will be enhanced by 1000 per

month.

2) Labour cost card:

Table 2: Labour cost card

Month July August September

Number of labours 500 700 900

Cost per unit (£) 8 8 8

Total cost (£) 4000 5600 7200

Interpretation: As per labour cost card preparation, it is identified that number of labours

for July, August and September are expected as 500, 700 and 900. For this costing, cost per

worker is to estimated as 8 in all months for all three months. Hence, total cost to be obtained for

three months would be 4000, 5600 and 7200. Thus, it is required to controlling over it and

preparing strategies for cost effectiveness.

3) Variable overhead cost card:

Table 3: Variable overhead cost card

4

orders at low prices. This helps the manager to evaluate and measure the consequences.

Cost card preparation:

1) For Direct material:

Table 1: Direct material cost card

Month July August September

Material 500 700 900

Cost per unit (£) 5 5 5

Total cost (£) 2500 3500 4500

Interpretation: It is estimated that in July, material is produced of 500 units, as well in

further months like August and September are 700 and 900 respectively. For which, cost per unit

for each month is forecast as 5. Therefore, total cost estimated for all three months are estimated

as 2500, 3500 and 4500. Thus, cost incurred for all three months will be enhanced by 1000 per

month.

2) Labour cost card:

Table 2: Labour cost card

Month July August September

Number of labours 500 700 900

Cost per unit (£) 8 8 8

Total cost (£) 4000 5600 7200

Interpretation: As per labour cost card preparation, it is identified that number of labours

for July, August and September are expected as 500, 700 and 900. For this costing, cost per

worker is to estimated as 8 in all months for all three months. Hence, total cost to be obtained for

three months would be 4000, 5600 and 7200. Thus, it is required to controlling over it and

preparing strategies for cost effectiveness.

3) Variable overhead cost card:

Table 3: Variable overhead cost card

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

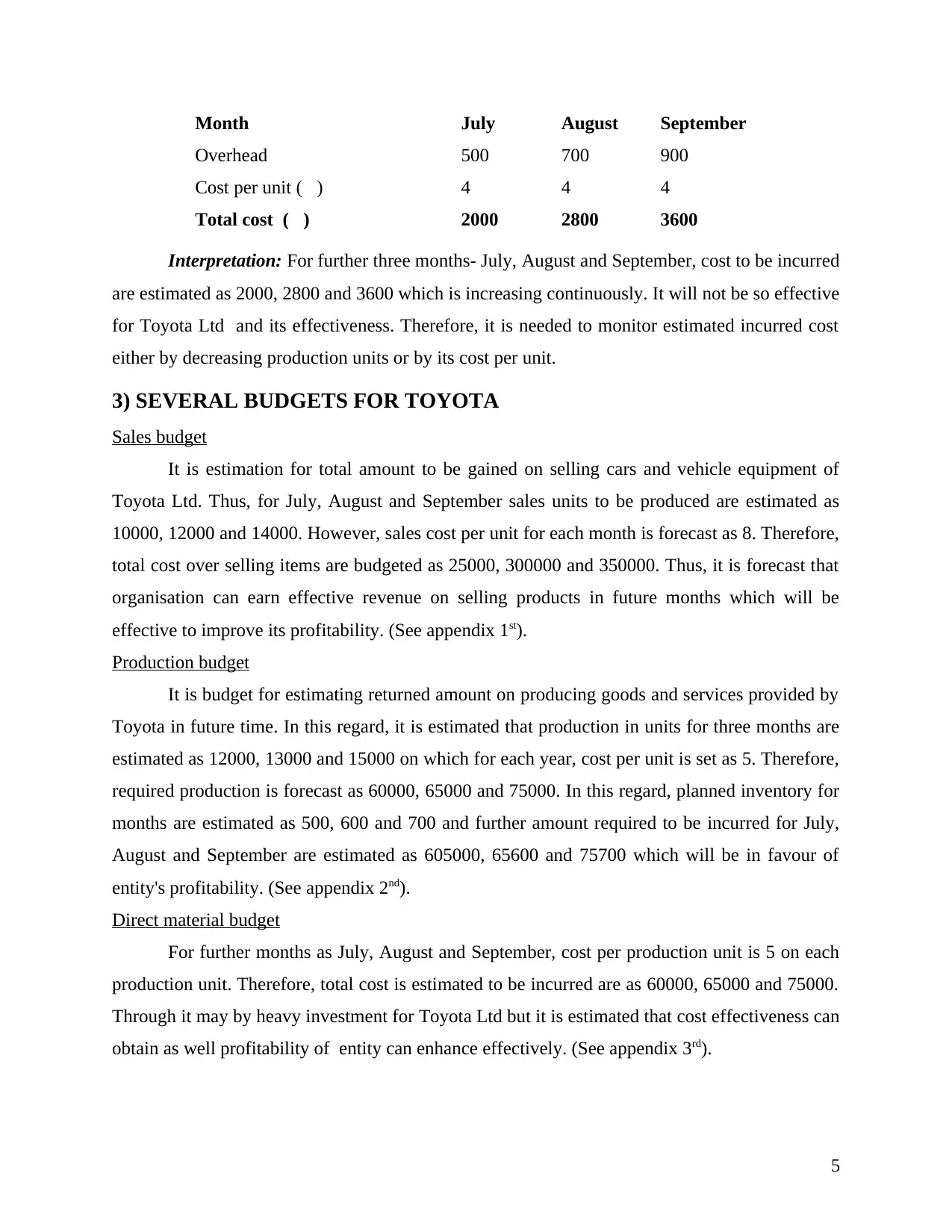

Month July August September

Overhead 500 700 900

Cost per unit (£) 4 4 4

Total cost (£) 2000 2800 3600

Interpretation: For further three months- July, August and September, cost to be incurred

are estimated as 2000, 2800 and 3600 which is increasing continuously. It will not be so effective

for Toyota Ltd and its effectiveness. Therefore, it is needed to monitor estimated incurred cost

either by decreasing production units or by its cost per unit.

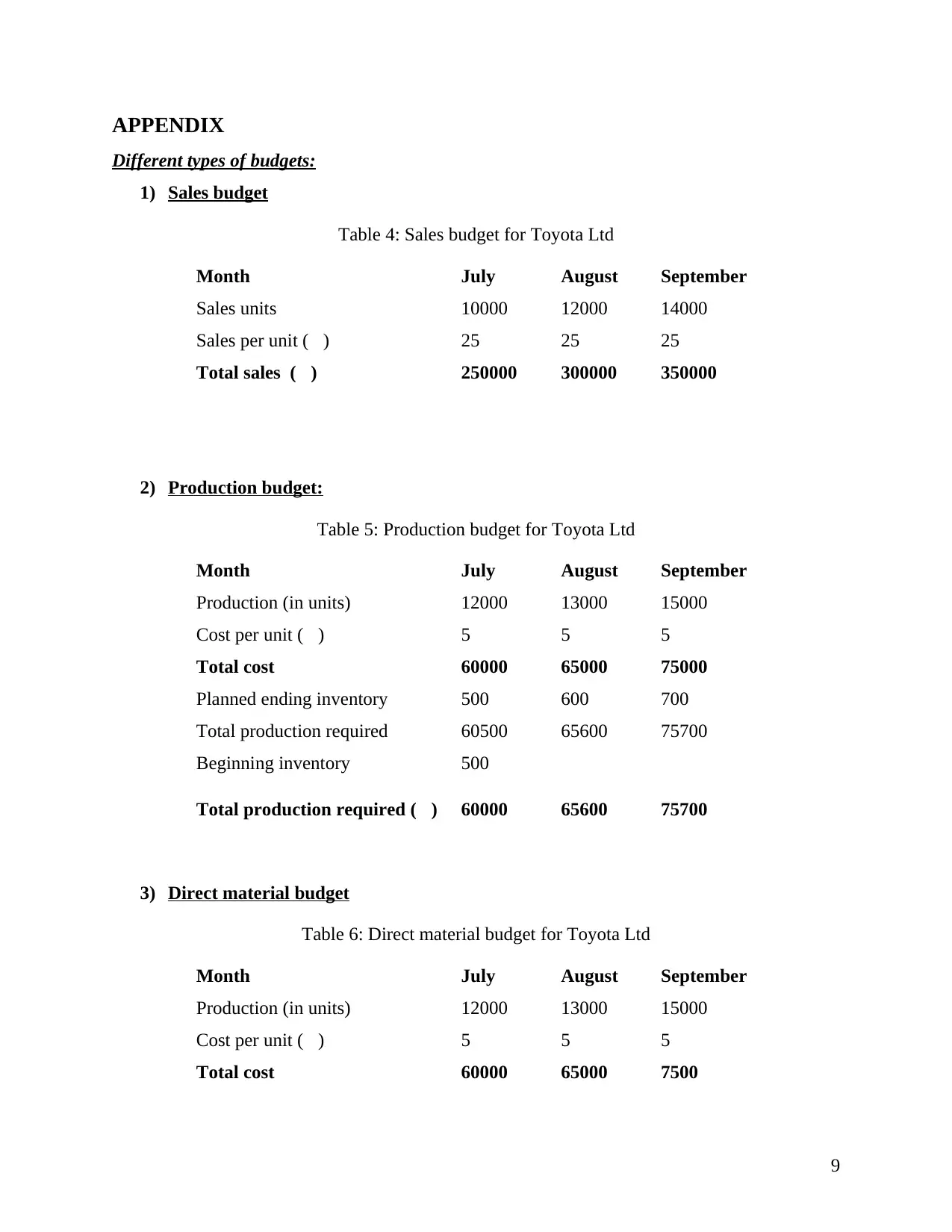

3) SEVERAL BUDGETS FOR TOYOTA

Sales budget

It is estimation for total amount to be gained on selling cars and vehicle equipment of

Toyota Ltd. Thus, for July, August and September sales units to be produced are estimated as

10000, 12000 and 14000. However, sales cost per unit for each month is forecast as 8. Therefore,

total cost over selling items are budgeted as 25000, 300000 and 350000. Thus, it is forecast that

organisation can earn effective revenue on selling products in future months which will be

effective to improve its profitability. (See appendix 1st).

Production budget

It is budget for estimating returned amount on producing goods and services provided by

Toyota in future time. In this regard, it is estimated that production in units for three months are

estimated as 12000, 13000 and 15000 on which for each year, cost per unit is set as 5. Therefore,

required production is forecast as 60000, 65000 and 75000. In this regard, planned inventory for

months are estimated as 500, 600 and 700 and further amount required to be incurred for July,

August and September are estimated as 605000, 65600 and 75700 which will be in favour of

entity's profitability. (See appendix 2nd).

Direct material budget

For further months as July, August and September, cost per production unit is 5 on each

production unit. Therefore, total cost is estimated to be incurred are as 60000, 65000 and 75000.

Through it may by heavy investment for Toyota Ltd but it is estimated that cost effectiveness can

obtain as well profitability of entity can enhance effectively. (See appendix 3rd).

5

Overhead 500 700 900

Cost per unit (£) 4 4 4

Total cost (£) 2000 2800 3600

Interpretation: For further three months- July, August and September, cost to be incurred

are estimated as 2000, 2800 and 3600 which is increasing continuously. It will not be so effective

for Toyota Ltd and its effectiveness. Therefore, it is needed to monitor estimated incurred cost

either by decreasing production units or by its cost per unit.

3) SEVERAL BUDGETS FOR TOYOTA

Sales budget

It is estimation for total amount to be gained on selling cars and vehicle equipment of

Toyota Ltd. Thus, for July, August and September sales units to be produced are estimated as

10000, 12000 and 14000. However, sales cost per unit for each month is forecast as 8. Therefore,

total cost over selling items are budgeted as 25000, 300000 and 350000. Thus, it is forecast that

organisation can earn effective revenue on selling products in future months which will be

effective to improve its profitability. (See appendix 1st).

Production budget

It is budget for estimating returned amount on producing goods and services provided by

Toyota in future time. In this regard, it is estimated that production in units for three months are

estimated as 12000, 13000 and 15000 on which for each year, cost per unit is set as 5. Therefore,

required production is forecast as 60000, 65000 and 75000. In this regard, planned inventory for

months are estimated as 500, 600 and 700 and further amount required to be incurred for July,

August and September are estimated as 605000, 65600 and 75700 which will be in favour of

entity's profitability. (See appendix 2nd).

Direct material budget

For further months as July, August and September, cost per production unit is 5 on each

production unit. Therefore, total cost is estimated to be incurred are as 60000, 65000 and 75000.

Through it may by heavy investment for Toyota Ltd but it is estimated that cost effectiveness can

obtain as well profitability of entity can enhance effectively. (See appendix 3rd).

5

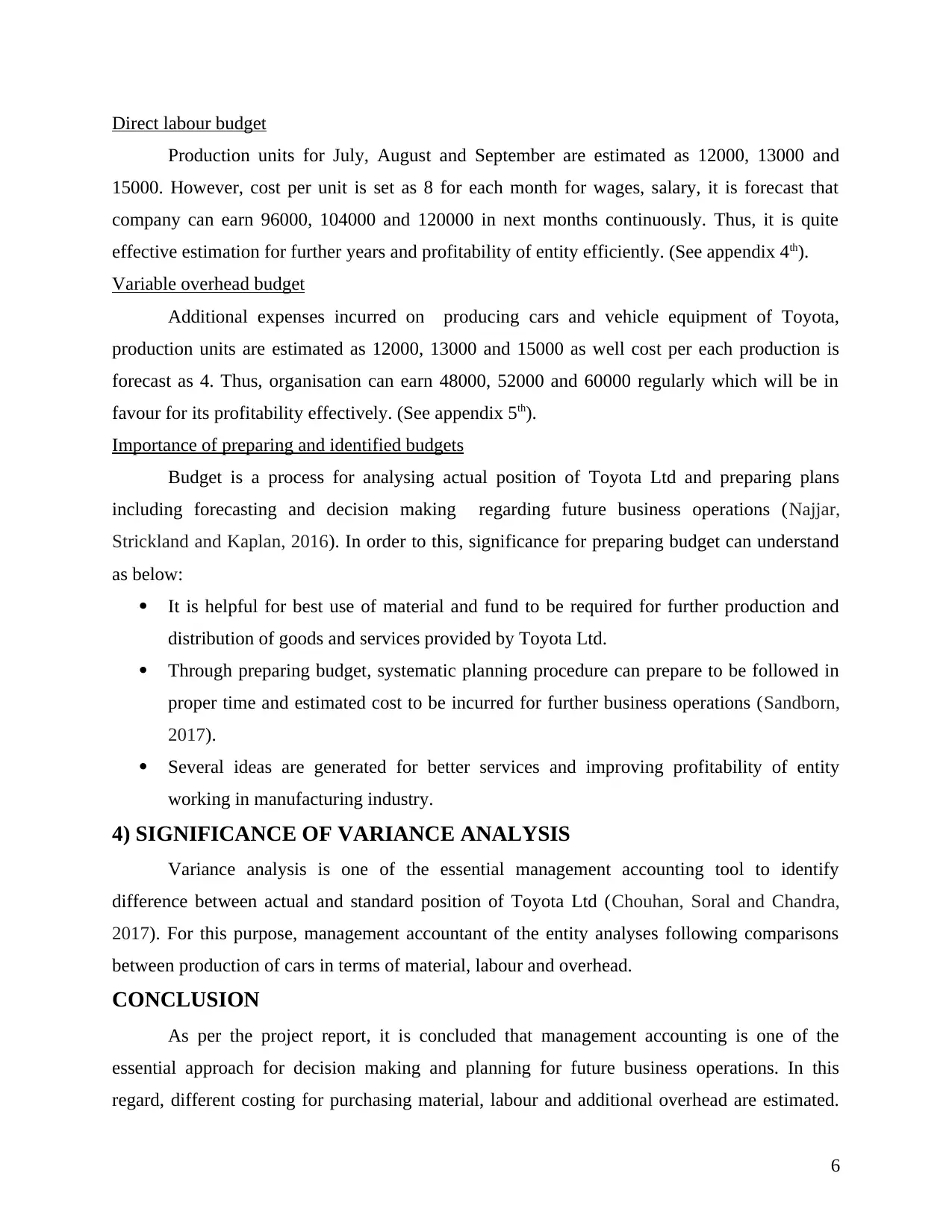

Direct labour budget

Production units for July, August and September are estimated as 12000, 13000 and

15000. However, cost per unit is set as 8 for each month for wages, salary, it is forecast that

company can earn 96000, 104000 and 120000 in next months continuously. Thus, it is quite

effective estimation for further years and profitability of entity efficiently. (See appendix 4th).

Variable overhead budget

Additional expenses incurred on producing cars and vehicle equipment of Toyota,

production units are estimated as 12000, 13000 and 15000 as well cost per each production is

forecast as 4. Thus, organisation can earn 48000, 52000 and 60000 regularly which will be in

favour for its profitability effectively. (See appendix 5th).

Importance of preparing and identified budgets

Budget is a process for analysing actual position of Toyota Ltd and preparing plans

including forecasting and decision making regarding future business operations (Najjar,

Strickland and Kaplan, 2016). In order to this, significance for preparing budget can understand

as below:

It is helpful for best use of material and fund to be required for further production and

distribution of goods and services provided by Toyota Ltd.

Through preparing budget, systematic planning procedure can prepare to be followed in

proper time and estimated cost to be incurred for further business operations (Sandborn,

2017).

Several ideas are generated for better services and improving profitability of entity

working in manufacturing industry.

4) SIGNIFICANCE OF VARIANCE ANALYSIS

Variance analysis is one of the essential management accounting tool to identify

difference between actual and standard position of Toyota Ltd (Chouhan, Soral and Chandra,

2017). For this purpose, management accountant of the entity analyses following comparisons

between production of cars in terms of material, labour and overhead.

CONCLUSION

As per the project report, it is concluded that management accounting is one of the

essential approach for decision making and planning for future business operations. In this

regard, different costing for purchasing material, labour and additional overhead are estimated.

6

Production units for July, August and September are estimated as 12000, 13000 and

15000. However, cost per unit is set as 8 for each month for wages, salary, it is forecast that

company can earn 96000, 104000 and 120000 in next months continuously. Thus, it is quite

effective estimation for further years and profitability of entity efficiently. (See appendix 4th).

Variable overhead budget

Additional expenses incurred on producing cars and vehicle equipment of Toyota,

production units are estimated as 12000, 13000 and 15000 as well cost per each production is

forecast as 4. Thus, organisation can earn 48000, 52000 and 60000 regularly which will be in

favour for its profitability effectively. (See appendix 5th).

Importance of preparing and identified budgets

Budget is a process for analysing actual position of Toyota Ltd and preparing plans

including forecasting and decision making regarding future business operations (Najjar,

Strickland and Kaplan, 2016). In order to this, significance for preparing budget can understand

as below:

It is helpful for best use of material and fund to be required for further production and

distribution of goods and services provided by Toyota Ltd.

Through preparing budget, systematic planning procedure can prepare to be followed in

proper time and estimated cost to be incurred for further business operations (Sandborn,

2017).

Several ideas are generated for better services and improving profitability of entity

working in manufacturing industry.

4) SIGNIFICANCE OF VARIANCE ANALYSIS

Variance analysis is one of the essential management accounting tool to identify

difference between actual and standard position of Toyota Ltd (Chouhan, Soral and Chandra,

2017). For this purpose, management accountant of the entity analyses following comparisons

between production of cars in terms of material, labour and overhead.

CONCLUSION

As per the project report, it is concluded that management accounting is one of the

essential approach for decision making and planning for future business operations. In this

regard, different costing for purchasing material, labour and additional overhead are estimated.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

However, cost classifications in different contexts of types, behaviour, relevance are understood.

In addition to this, different budgets for decision making and further business operations are

forecast for further months' operations evolving July, August and September. However, variance

analysis for production and distribution of cars and vehicle equipment are presented that requires

to create bridge the gap for entity's effectiveness. Thus, management accounting and its different

aspects are understood through this report for further decision making and business operations

effectively.

7

In addition to this, different budgets for decision making and further business operations are

forecast for further months' operations evolving July, August and September. However, variance

analysis for production and distribution of cars and vehicle equipment are presented that requires

to create bridge the gap for entity's effectiveness. Thus, management accounting and its different

aspects are understood through this report for further decision making and business operations

effectively.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCE

Books and Journal

Akyol, D.E., Tuncel, G. and Bayhan, G.M., 2015. A comparative analysis of activity-based

costing and traditional costing. World Academy of Science, Engineering and

Technology. 3(2). pp.44-47.

Chouhan, V., Soral, G. and Chandra, B., 2017. Activity based costing model for inventory

valuation. Management Science Letters. 7(3). pp.135-144.

El Alaoui, S. and Lindefors, N., 2016. Combining Time-Driven Activity-Based Costing with

Clinical Outcome in Cost-Effectiveness Analysis to Measure Value in Treatment of

Depression. PloS one. 11(10). p.e0165389.

Johnson, P.F., 2014. Purchasing and supply management. McGraw-Hill Higher Education.

Laviana, A.A. and et.al., 2016. Utilizing time‐driven activity‐based costing to understand the

short‐and long‐term costs of treating localized, low‐risk prostate cancer.Cancer. 122(3)

pp.447-455.

Najjar, P.A., Strickland, M. and Kaplan, R.S., 2016. Time-Driven Activity-Based Costing for

Surgical Episodes. JAMA surgery.

Sandborn, P., 2017. Activity-Based Costing (ABC). In Cost Analysis of Electronic Systems.

14(2). pp. 77-92.

Online

Management Accounting. 2016. [online]. Available through:

<http://www.ddegjust.ac.in/studymaterial/mcom/mc-105.pdf>. [Accessed on 14th July

2017].

8

Books and Journal

Akyol, D.E., Tuncel, G. and Bayhan, G.M., 2015. A comparative analysis of activity-based

costing and traditional costing. World Academy of Science, Engineering and

Technology. 3(2). pp.44-47.

Chouhan, V., Soral, G. and Chandra, B., 2017. Activity based costing model for inventory

valuation. Management Science Letters. 7(3). pp.135-144.

El Alaoui, S. and Lindefors, N., 2016. Combining Time-Driven Activity-Based Costing with

Clinical Outcome in Cost-Effectiveness Analysis to Measure Value in Treatment of

Depression. PloS one. 11(10). p.e0165389.

Johnson, P.F., 2014. Purchasing and supply management. McGraw-Hill Higher Education.

Laviana, A.A. and et.al., 2016. Utilizing time‐driven activity‐based costing to understand the

short‐and long‐term costs of treating localized, low‐risk prostate cancer.Cancer. 122(3)

pp.447-455.

Najjar, P.A., Strickland, M. and Kaplan, R.S., 2016. Time-Driven Activity-Based Costing for

Surgical Episodes. JAMA surgery.

Sandborn, P., 2017. Activity-Based Costing (ABC). In Cost Analysis of Electronic Systems.

14(2). pp. 77-92.

Online

Management Accounting. 2016. [online]. Available through:

<http://www.ddegjust.ac.in/studymaterial/mcom/mc-105.pdf>. [Accessed on 14th July

2017].

8

APPENDIX

Different types of budgets:

1) Sales budget

Table 4: Sales budget for Toyota Ltd

Month July August September

Sales units 10000 12000 14000

Sales per unit (£) 25 25 25

Total sales (£) 250000 300000 350000

2) Production budget:

Table 5: Production budget for Toyota Ltd

Month July August September

Production (in units) 12000 13000 15000

Cost per unit (£) 5 5 5

Total cost 60000 65000 75000

Planned ending inventory 500 600 700

Total production required 60500 65600 75700

Beginning inventory 500

Total production required (£) 60000 65600 75700

3) Direct material budget

Table 6: Direct material budget for Toyota Ltd

Month July August September

Production (in units) 12000 13000 15000

Cost per unit (£) 5 5 5

Total cost 60000 65000 7500

9

Different types of budgets:

1) Sales budget

Table 4: Sales budget for Toyota Ltd

Month July August September

Sales units 10000 12000 14000

Sales per unit (£) 25 25 25

Total sales (£) 250000 300000 350000

2) Production budget:

Table 5: Production budget for Toyota Ltd

Month July August September

Production (in units) 12000 13000 15000

Cost per unit (£) 5 5 5

Total cost 60000 65000 75000

Planned ending inventory 500 600 700

Total production required 60500 65600 75700

Beginning inventory 500

Total production required (£) 60000 65600 75700

3) Direct material budget

Table 6: Direct material budget for Toyota Ltd

Month July August September

Production (in units) 12000 13000 15000

Cost per unit (£) 5 5 5

Total cost 60000 65000 7500

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.