Analysis of Transfer Pricing Approaches for Raven Industries

VerifiedAdded on 2022/11/26

|14

|3695

|443

Report

AI Summary

This report provides a comprehensive analysis of transfer pricing methods within the context of Raven Industries, a company with three divisions. The report begins by assessing the validity of a statement made by Cleveland regarding the profitability of the cushion division and the impact of transfer pricing. It then explores various transfer pricing approaches, including negotiated pricing and dual pricing, comparing their advantages and disadvantages. The report emphasizes the importance of aligning divisional goals with overall corporate objectives and the role of performance measurement in enhancing productivity. A revised profit statement based on the contribution margin approach is presented to evaluate divisional performance. Finally, the report concludes by recommending the best transfer pricing approach for the company. The analysis includes financial statements and calculations to support the recommendations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The present report contains the issues related to the determination of the transfer price. In large

organizations, activities may be divided into some division, and each of the managers is

responsible for the performance of their department. The present report is connected with the

determination of the transfer pricing approaches, by which the overall efficiency and

productivity can be achieved. In the given problem, the Raven Industries has three different

departments, in which cushion division transfer its product to the furniture division. Along with

this, the application of the contribution margin approach assists the increment in the profit of the

department. Further, Raven Industries should use the performance measurement approach for the

enhancement of the productivity and effectiveness of the company

The present report contains the issues related to the determination of the transfer price. In large

organizations, activities may be divided into some division, and each of the managers is

responsible for the performance of their department. The present report is connected with the

determination of the transfer pricing approaches, by which the overall efficiency and

productivity can be achieved. In the given problem, the Raven Industries has three different

departments, in which cushion division transfer its product to the furniture division. Along with

this, the application of the contribution margin approach assists the increment in the profit of the

department. Further, Raven Industries should use the performance measurement approach for the

enhancement of the productivity and effectiveness of the company

Table of Contents

Introduction......................................................................................................................................4

Assessment 3...................................................................................................................................4

Part 1............................................................................................................................................4

Part 2............................................................................................................................................9

Part 3..........................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Introduction......................................................................................................................................4

Assessment 3...................................................................................................................................4

Part 1............................................................................................................................................4

Part 2............................................................................................................................................9

Part 3..........................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The profitability of the buying and selling department of the company is affected by the transfer

price. Each department wants to increase its performance (Trost, and Heim, 2018). In the given

study, the problem related to the ascertainment of the transfer price is evaluated. There is some

technique, which can be implemented by the company for the determination of the transfer price;

the given report contains the same. Along with this, a recommendation to the manager also

provided with respect to the transfer price and the performance measurement is also presented in

the given study.

ASSESSMENT 3

Part 1

Ascertaining whether the Cleveland statement is correct or not

It can be stated that statement made by Cleveland is correct, it is because, the division of cushion

was not able to produce adequate profits, and was failing to bear a good position in the market

when its transfer to furniture division was made. Further, Cleveland decides to put the cushion

into sale into the furniture division, and the goods will be priced in ways that are more

productive and profitable. However, it has been believed by Cleveland that cushion division is

much more profitable as compared to the figures presented in the managerial authority’s reports.

These cushions for earning a certain profit, cushions would be sold on the outside market at the

common mark-up, which is a great idea. Since, Cleveland is an only a team player, and can

merely sell at cost for corporate benefit as a large, and states that the performance of the division

must be based on the division’s contribution if the cushions are sold at market prices, and it is

required that the same should be presented in a set of reformed and revised operating statements

means for internal reporting purposes.

An alternative approach that can be used by the company to set transfer prices, excluding market

price and manufacturing cost

The profitability of the buying and selling department of the company is affected by the transfer

price. Each department wants to increase its performance (Trost, and Heim, 2018). In the given

study, the problem related to the ascertainment of the transfer price is evaluated. There is some

technique, which can be implemented by the company for the determination of the transfer price;

the given report contains the same. Along with this, a recommendation to the manager also

provided with respect to the transfer price and the performance measurement is also presented in

the given study.

ASSESSMENT 3

Part 1

Ascertaining whether the Cleveland statement is correct or not

It can be stated that statement made by Cleveland is correct, it is because, the division of cushion

was not able to produce adequate profits, and was failing to bear a good position in the market

when its transfer to furniture division was made. Further, Cleveland decides to put the cushion

into sale into the furniture division, and the goods will be priced in ways that are more

productive and profitable. However, it has been believed by Cleveland that cushion division is

much more profitable as compared to the figures presented in the managerial authority’s reports.

These cushions for earning a certain profit, cushions would be sold on the outside market at the

common mark-up, which is a great idea. Since, Cleveland is an only a team player, and can

merely sell at cost for corporate benefit as a large, and states that the performance of the division

must be based on the division’s contribution if the cushions are sold at market prices, and it is

required that the same should be presented in a set of reformed and revised operating statements

means for internal reporting purposes.

An alternative approach that can be used by the company to set transfer prices, excluding market

price and manufacturing cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Transfer pricing means setting prices for goods and services sold among the controlled or

associated legal business entities. It seems that setting price meant for the internal transfer are

comparatively less crucial than the external sales, on the other hand, it has to be acknowledged

that the division in which large groups are divided and are expected to work as self-contained

units(Frost, Vogel, and Bagban, 2016). The decision on transfer pricing is highly critical, as the

top management is at a place to determine if or if not it is more viable for the good of service to

be purchased or sold on an internal or external basis, but simultaneously requires to be consider

the behavioral aspects like divisional managers motivation (KENTON, 2018).

For setting the transfer price, the given company aims to ensure that its goals coincide with the

controlled or related divisions, the transferred product price must also be determined that each

division’s profitability can be assured and the price must be set in a way that it incites corporate

profit-maximization.

It may be obvious that the credit to the supplying division is only balanced by an equal debit to

the receiving division, and thus, the entire company is considered, it bears a net zero impact. On

the other hand, there are significant behavioral as well as organizational elements related to the

transfer pricing and the decisions of adopting a method. The transfer pricing does impact each

division’s profit on a separate basis, and thus can impact the motivational level of all divisional

managers. The objective of management in the setting a transfer price is to stimulate goal

congruence between the divisional managers engaged in the transfers (Abdallah, 2016). Other

approaches which are available to the company in setting transfer prices, other than market price

and manufacturing cost are provided and enumerated as below:

Negotiated price

Negotiated prices are often prioritized as a mid-solution among the cost-based prices and market

prices. As per the negotiated process, the engaged managers act similarly like the managers of

independent companies. In addition, the negotiation strategies might be the same as those used

while trading with outer markets (Cooper and et al., 2017). In a situation where both of the

divisions are independent to address either with one another or in the out market, then the

negotiated price will be expected to be near to the external market price. In case, all of the output

of the selling division cannot be sold in the market, i.e. a portion should be put into sale to the

associated legal business entities. It seems that setting price meant for the internal transfer are

comparatively less crucial than the external sales, on the other hand, it has to be acknowledged

that the division in which large groups are divided and are expected to work as self-contained

units(Frost, Vogel, and Bagban, 2016). The decision on transfer pricing is highly critical, as the

top management is at a place to determine if or if not it is more viable for the good of service to

be purchased or sold on an internal or external basis, but simultaneously requires to be consider

the behavioral aspects like divisional managers motivation (KENTON, 2018).

For setting the transfer price, the given company aims to ensure that its goals coincide with the

controlled or related divisions, the transferred product price must also be determined that each

division’s profitability can be assured and the price must be set in a way that it incites corporate

profit-maximization.

It may be obvious that the credit to the supplying division is only balanced by an equal debit to

the receiving division, and thus, the entire company is considered, it bears a net zero impact. On

the other hand, there are significant behavioral as well as organizational elements related to the

transfer pricing and the decisions of adopting a method. The transfer pricing does impact each

division’s profit on a separate basis, and thus can impact the motivational level of all divisional

managers. The objective of management in the setting a transfer price is to stimulate goal

congruence between the divisional managers engaged in the transfers (Abdallah, 2016). Other

approaches which are available to the company in setting transfer prices, other than market price

and manufacturing cost are provided and enumerated as below:

Negotiated price

Negotiated prices are often prioritized as a mid-solution among the cost-based prices and market

prices. As per the negotiated process, the engaged managers act similarly like the managers of

independent companies. In addition, the negotiation strategies might be the same as those used

while trading with outer markets (Cooper and et al., 2017). In a situation where both of the

divisions are independent to address either with one another or in the out market, then the

negotiated price will be expected to be near to the external market price. In case, all of the output

of the selling division cannot be sold in the market, i.e. a portion should be put into sale to the

buying division, the negotiated prices will be expected to be lower as compared to the market

price, and sharing of the total margins will be done by divisions (Heimert and Michaelson,

2018). A negotiated transfer price to be success require certain conditions, which include, some

sort of external market for the intermediate product ( that is present in the cushion division),

sharing of all the market information between the negotiators, independence in buying or selling

on the outer basis, and optimal support from the upper management. Thus, the agreed prices can

also be employed for the measurement of performance. Hence, when there is the existence of

outside market for the intermediate product, however is not perfectly competitive and wherein a

minor number of distinct products are transferred, them a negotiated-transfer- price approach

results best, as in the case of cushion division, as the outside market price can deliver as an

estimation of the opportunity cost(de Matta and Miller, 2015).

The approach of setting transfer of negotiated price, in this, the organization does not mention

riles for the identification of transfer prices. In this way, the divisional managers are motivated to

do the negotiation for a collectively agreeable transfer price (Löffler, 2018). This is typically

integrated with free sourcing. Business segments are enabled to negotiate the transfer prices,

generally among the lower and upper limit set out. There is the presence of implication that the

buying segment is entitled to but from the outer sources, in case it does not agree on a price.

Thus, this independence is engaged with risks, as the division manager compete to earn a higher

share for the available profit. Due to this aspect, the company might mention performance

management objectives that might analyze managers based on the total profit generated by both

divisions, despite the division they work in (Horst, 2018). This approach meets all four criteria

of transfer pricing; it conceals full costs and considers a profit for the profit centre.

Simultaneously, it is lower as compared to the external price, managers are motivated for the

internal transfer, and the autonomy, performance evaluation and goal congruence criteria are not

into risks, Negotiated transfer pricing benefits the firm, with imitating a free market wherein

divisional managers purchase and sell from one another in a way that fosters arms-length

transactions.

Dual-pricing

The dual prices of transfer pricing, states that selling divisions puts the transferred goods into

sale at a market or negotiated market price or at a cost with a certain profit margin. However, the

price, and sharing of the total margins will be done by divisions (Heimert and Michaelson,

2018). A negotiated transfer price to be success require certain conditions, which include, some

sort of external market for the intermediate product ( that is present in the cushion division),

sharing of all the market information between the negotiators, independence in buying or selling

on the outer basis, and optimal support from the upper management. Thus, the agreed prices can

also be employed for the measurement of performance. Hence, when there is the existence of

outside market for the intermediate product, however is not perfectly competitive and wherein a

minor number of distinct products are transferred, them a negotiated-transfer- price approach

results best, as in the case of cushion division, as the outside market price can deliver as an

estimation of the opportunity cost(de Matta and Miller, 2015).

The approach of setting transfer of negotiated price, in this, the organization does not mention

riles for the identification of transfer prices. In this way, the divisional managers are motivated to

do the negotiation for a collectively agreeable transfer price (Löffler, 2018). This is typically

integrated with free sourcing. Business segments are enabled to negotiate the transfer prices,

generally among the lower and upper limit set out. There is the presence of implication that the

buying segment is entitled to but from the outer sources, in case it does not agree on a price.

Thus, this independence is engaged with risks, as the division manager compete to earn a higher

share for the available profit. Due to this aspect, the company might mention performance

management objectives that might analyze managers based on the total profit generated by both

divisions, despite the division they work in (Horst, 2018). This approach meets all four criteria

of transfer pricing; it conceals full costs and considers a profit for the profit centre.

Simultaneously, it is lower as compared to the external price, managers are motivated for the

internal transfer, and the autonomy, performance evaluation and goal congruence criteria are not

into risks, Negotiated transfer pricing benefits the firm, with imitating a free market wherein

divisional managers purchase and sell from one another in a way that fosters arms-length

transactions.

Dual-pricing

The dual prices of transfer pricing, states that selling divisions puts the transferred goods into

sale at a market or negotiated market price or at a cost with a certain profit margin. However, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

transfer price meant for the buying division is an amount based on cost. The difference in the

transfer prices for both of the division can be attributed by an exceptional centralized

account(Klassen, Lisowsky, and Mescall, 2017). Furthermore, this system would uphold cost

information for later buyer divisions and would foster internal transfers by offering a profit over

these transfers, particularly for selling divisions. It can be stated that dual prices lends

motivation, as well as inducement to the selling divisions as transferring of goods, are done at

market price, and this approach offers minimum cost to the buying division alongside (Cristea

and Nguyen, 2016). In this approach, the buying unit holds the transferred goods at cost, and on

the other hand, the selling unit is accounted for with the market price, wherein they can ensure a

certain profit. Generally, the motivation of employing dual transfer pricing is to permit the

selling price for surpassing the purchase price, leading to a corporate-level subsidy, thereby

motivating the managerial divisions to do participation in the transfer. For coping up with the

problem, of setting transfer prices, the company can implement the full exercise of dual pricing.

Herein, the agreed transfer price is employed for the aim of financial reporting of the individual

division outcomes (Davies and et al., 2018). While for, the purpose of management evaluation,

the application of variable cost is done to the outcomes of one or both divisions. Further, the

difference held in the management price and entity valueis considered as mark-up.

Similarly, the mark-up is accounted for by allotting it to a distinct account that is employed for

the purpose of reconciliation. The mark-up amount in the accounts of buying segment should be

equal the amount of the accounts of selling segment mark-up (Hamamura, 2019). By making

use of the dual pricing it enables the company to get the best of results, the setting of transfer

prices can be done to satisfy the regulatory as well as company financial constraints, and at the

same time the price employed by the management can be dependent on a closer approach

towards the marginal costs of long run. This allows the operations to the company to optimize

their pricing and output based decisions above the decentralized management (Andreou, 2016).

On the top of all, it is very important to identify the best transfer pricing approach or method that

can be implemented organization-wide, thereby helping in meeting regulatory needs and also

assisting in providing better insights as well as business benefits(Frost, Vogel, and Bagban,

2016). However, it is a complicated process, but if conducted right, then it can serve

commendable efficiency and higher business advantages.

transfer prices for both of the division can be attributed by an exceptional centralized

account(Klassen, Lisowsky, and Mescall, 2017). Furthermore, this system would uphold cost

information for later buyer divisions and would foster internal transfers by offering a profit over

these transfers, particularly for selling divisions. It can be stated that dual prices lends

motivation, as well as inducement to the selling divisions as transferring of goods, are done at

market price, and this approach offers minimum cost to the buying division alongside (Cristea

and Nguyen, 2016). In this approach, the buying unit holds the transferred goods at cost, and on

the other hand, the selling unit is accounted for with the market price, wherein they can ensure a

certain profit. Generally, the motivation of employing dual transfer pricing is to permit the

selling price for surpassing the purchase price, leading to a corporate-level subsidy, thereby

motivating the managerial divisions to do participation in the transfer. For coping up with the

problem, of setting transfer prices, the company can implement the full exercise of dual pricing.

Herein, the agreed transfer price is employed for the aim of financial reporting of the individual

division outcomes (Davies and et al., 2018). While for, the purpose of management evaluation,

the application of variable cost is done to the outcomes of one or both divisions. Further, the

difference held in the management price and entity valueis considered as mark-up.

Similarly, the mark-up is accounted for by allotting it to a distinct account that is employed for

the purpose of reconciliation. The mark-up amount in the accounts of buying segment should be

equal the amount of the accounts of selling segment mark-up (Hamamura, 2019). By making

use of the dual pricing it enables the company to get the best of results, the setting of transfer

prices can be done to satisfy the regulatory as well as company financial constraints, and at the

same time the price employed by the management can be dependent on a closer approach

towards the marginal costs of long run. This allows the operations to the company to optimize

their pricing and output based decisions above the decentralized management (Andreou, 2016).

On the top of all, it is very important to identify the best transfer pricing approach or method that

can be implemented organization-wide, thereby helping in meeting regulatory needs and also

assisting in providing better insights as well as business benefits(Frost, Vogel, and Bagban,

2016). However, it is a complicated process, but if conducted right, then it can serve

commendable efficiency and higher business advantages.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

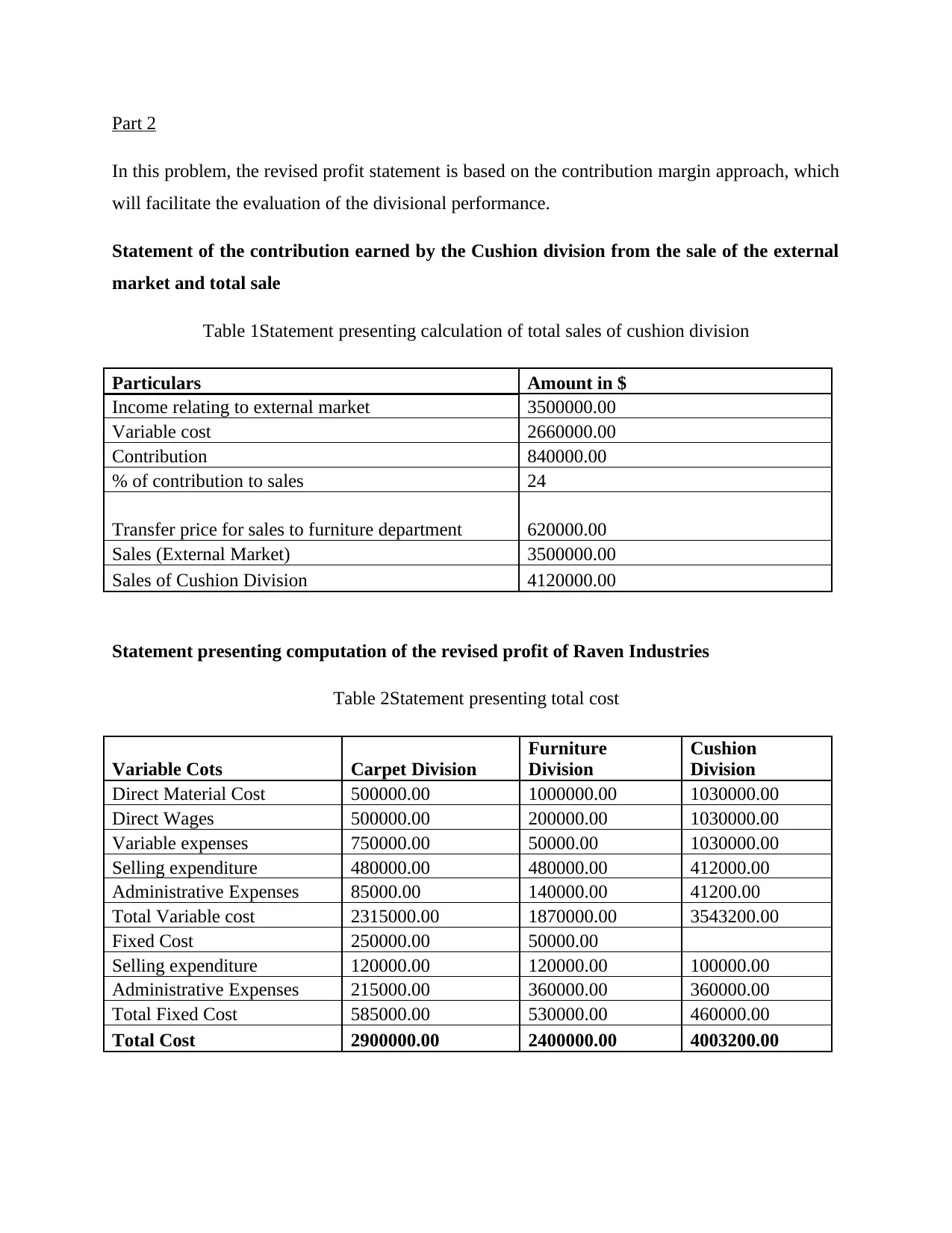

Part 2

In this problem, the revised profit statement is based on the contribution margin approach, which

will facilitate the evaluation of the divisional performance.

Statement of the contribution earned by the Cushion division from the sale of the external

market and total sale

Table 1Statement presenting calculation of total sales of cushion division

Particulars Amount in $

Income relating to external market 3500000.00

Variable cost 2660000.00

Contribution 840000.00

% of contribution to sales 24

Transfer price for sales to furniture department 620000.00

Sales (External Market) 3500000.00

Sales of Cushion Division 4120000.00

Statement presenting computation of the revised profit of Raven Industries

Table 2Statement presenting total cost

Variable Cots Carpet Division

Furniture

Division

Cushion

Division

Direct Material Cost 500000.00 1000000.00 1030000.00

Direct Wages 500000.00 200000.00 1030000.00

Variable expenses 750000.00 50000.00 1030000.00

Selling expenditure 480000.00 480000.00 412000.00

Administrative Expenses 85000.00 140000.00 41200.00

Total Variable cost 2315000.00 1870000.00 3543200.00

Fixed Cost 250000.00 50000.00

Selling expenditure 120000.00 120000.00 100000.00

Administrative Expenses 215000.00 360000.00 360000.00

Total Fixed Cost 585000.00 530000.00 460000.00

Total Cost 2900000.00 2400000.00 4003200.00

In this problem, the revised profit statement is based on the contribution margin approach, which

will facilitate the evaluation of the divisional performance.

Statement of the contribution earned by the Cushion division from the sale of the external

market and total sale

Table 1Statement presenting calculation of total sales of cushion division

Particulars Amount in $

Income relating to external market 3500000.00

Variable cost 2660000.00

Contribution 840000.00

% of contribution to sales 24

Transfer price for sales to furniture department 620000.00

Sales (External Market) 3500000.00

Sales of Cushion Division 4120000.00

Statement presenting computation of the revised profit of Raven Industries

Table 2Statement presenting total cost

Variable Cots Carpet Division

Furniture

Division

Cushion

Division

Direct Material Cost 500000.00 1000000.00 1030000.00

Direct Wages 500000.00 200000.00 1030000.00

Variable expenses 750000.00 50000.00 1030000.00

Selling expenditure 480000.00 480000.00 412000.00

Administrative Expenses 85000.00 140000.00 41200.00

Total Variable cost 2315000.00 1870000.00 3543200.00

Fixed Cost 250000.00 50000.00

Selling expenditure 120000.00 120000.00 100000.00

Administrative Expenses 215000.00 360000.00 360000.00

Total Fixed Cost 585000.00 530000.00 460000.00

Total Cost 2900000.00 2400000.00 4003200.00

Table 3 Revised Profit and Loss Statement

Particulars

Carpet

Division

Furniture

Division

Cushion

Division

Total Sales 3000000.00 3000000.00 4120000.00

Total Cost 2900000 2400000 4003200

Net Profit (Total Sales - Total

Cost) 100000.00 600000.00 116800.00

On the basis of the above analysis, for the evaluation of the performance of the division, the

contribution margin approach is the better technique.

Part 3

In the present problem, it is given that cushion division transfers its product to the furniture

division at the cost. Since transfer at cost does not generate any profit to the cushion department;

therefore, the manager of the cushion division does not want to make the transfer to the furniture

department.

Transfer price is a price implemented to measure the value of goods or services for the sales of

product or services from one department to the other department (Ghosh Ray, and Ghosh Ray,

2015). Transfer pricing is essential in order to the enhancement of the separate performance of

the department of the company, as it is implemented to analyze the revenue generating to the

selling department and the cost incurred by the purchasing department of the company (Menz,

Kunisch, and Collis, 2015). The main objective of the transfer price is to encourage the

department in such a manner which will not assist in the benefit of departments only, instead

helps in the improvising the overall profitability of the company. Along with this, a transfer price

should be determined in such a way by which central management of the company can easily

ascertain the participation by every department towards the profit of organizations (Arruñada,

and Hansen, 2015). Moreover, the advantages of the decentralization can be achieved only

through the maximum divisional autonomy. By considering the above aspect, the objective of

transfer price is not achieved if the department uses the cost method as a determination of the

transfer price (Norde, Özen, and Slikker, 2016).

Particulars

Carpet

Division

Furniture

Division

Cushion

Division

Total Sales 3000000.00 3000000.00 4120000.00

Total Cost 2900000 2400000 4003200

Net Profit (Total Sales - Total

Cost) 100000.00 600000.00 116800.00

On the basis of the above analysis, for the evaluation of the performance of the division, the

contribution margin approach is the better technique.

Part 3

In the present problem, it is given that cushion division transfers its product to the furniture

division at the cost. Since transfer at cost does not generate any profit to the cushion department;

therefore, the manager of the cushion division does not want to make the transfer to the furniture

department.

Transfer price is a price implemented to measure the value of goods or services for the sales of

product or services from one department to the other department (Ghosh Ray, and Ghosh Ray,

2015). Transfer pricing is essential in order to the enhancement of the separate performance of

the department of the company, as it is implemented to analyze the revenue generating to the

selling department and the cost incurred by the purchasing department of the company (Menz,

Kunisch, and Collis, 2015). The main objective of the transfer price is to encourage the

department in such a manner which will not assist in the benefit of departments only, instead

helps in the improvising the overall profitability of the company. Along with this, a transfer price

should be determined in such a way by which central management of the company can easily

ascertain the participation by every department towards the profit of organizations (Arruñada,

and Hansen, 2015). Moreover, the advantages of the decentralization can be achieved only

through the maximum divisional autonomy. By considering the above aspect, the objective of

transfer price is not achieved if the department uses the cost method as a determination of the

transfer price (Norde, Özen, and Slikker, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Since, in the decentralized department, each manager is responsible for the performance of their

division. Therefore they try to accelerate the performance of the division. It has been seen that

the company should apply the cost method only if there is spare capacity and no external market

is available for the sale of the product (Chenhall, and Moers, 2015). In the present case, the

cushion division can sale the product in the outside market and earn the return. Therefore the

company should apply the other technique of transfer pricing, which assists in the improvement

in the performance of the company.

Measurement of the divisional performance possible if the appropriate revenue and cost are

assigned to the division.It is recommended that the company should use the performance

measurement approach for the optimization of the performance and the effectiveness (Frost,

Vogel, and Bagban, 2016). It assists the divisional manager, to transfer the products and services

to other division in such a manner which will enhance the profitability. Further, if the company

provides any incentives or rewards whether financial or non-financial on the basis of

performance of the division, then it will provide the motivation to the employees to work in a

better manner (Bakaouka, and Milliou, 2018). Further, management can also ascertain about the

contribution by the department in the profitability of the company and can identify under the

developed department, and make plans accordingly.

However, sometimes company has to face the difficulty because of the performance

measurement. As in this every department wants to maximize their own profit only, they do not

consider the overall profitability of company. Along with this, if the consistent strategies are not

applied by the each department, then conflict may arise and which will deteriorate the

performance of company.

Finally, by considering the significant benefits of the performance measurement it can be

recommended to the Raven Industries to apply the performance measurement approach by which

the optimum performance and the effectiveness can be achieved (Colombo, and Scrimitore,

2018).

division. Therefore they try to accelerate the performance of the division. It has been seen that

the company should apply the cost method only if there is spare capacity and no external market

is available for the sale of the product (Chenhall, and Moers, 2015). In the present case, the

cushion division can sale the product in the outside market and earn the return. Therefore the

company should apply the other technique of transfer pricing, which assists in the improvement

in the performance of the company.

Measurement of the divisional performance possible if the appropriate revenue and cost are

assigned to the division.It is recommended that the company should use the performance

measurement approach for the optimization of the performance and the effectiveness (Frost,

Vogel, and Bagban, 2016). It assists the divisional manager, to transfer the products and services

to other division in such a manner which will enhance the profitability. Further, if the company

provides any incentives or rewards whether financial or non-financial on the basis of

performance of the division, then it will provide the motivation to the employees to work in a

better manner (Bakaouka, and Milliou, 2018). Further, management can also ascertain about the

contribution by the department in the profitability of the company and can identify under the

developed department, and make plans accordingly.

However, sometimes company has to face the difficulty because of the performance

measurement. As in this every department wants to maximize their own profit only, they do not

consider the overall profitability of company. Along with this, if the consistent strategies are not

applied by the each department, then conflict may arise and which will deteriorate the

performance of company.

Finally, by considering the significant benefits of the performance measurement it can be

recommended to the Raven Industries to apply the performance measurement approach by which

the optimum performance and the effectiveness can be achieved (Colombo, and Scrimitore,

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

On the basis of the above analysis, it has been ascertained that in the decentralized department,

the role of transfer price is very important. With this aspect, it has been analyzed that transfer

price at cost does not make happy the manager of cushion division, because this transfer does not

generate any earning to the division. However, it has been observed that it is not essential for the

department to apply only the cost method for the determination of transfer price. Instead of this,

negotiated price method is a better to approach, at which cushion division may transfer the

product to the furniture division.

On the basis of the above analysis, it has been ascertained that in the decentralized department,

the role of transfer price is very important. With this aspect, it has been analyzed that transfer

price at cost does not make happy the manager of cushion division, because this transfer does not

generate any earning to the division. However, it has been observed that it is not essential for the

department to apply only the cost method for the determination of transfer price. Instead of this,

negotiated price method is a better to approach, at which cushion division may transfer the

product to the furniture division.

REFERENCES

Books and Journals

Abdallah, W., 2016. Documentation of Transfer Pricing: A New Global Approach. International

Journal of Accounting and Taxation, 4(2), pp.37-55.

Arruñada, B. and Hansen, S., 2015. Organizing good public provision: Lessons from Managerial

Accounting. International Review of Law and Economics, 42, pp.185-191.

Bakaouka, E. and Million, C., 2018. Vertical licensing, input pricing, and entry. International

Journal of Industrial Organization, 59, pp.66-96.

Chenhall, R.H. and Moers, F., 2015.The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society, 47, pp.1-13.

Colombo, S. and Scrimitore, M., 2018.A managerial delegation under capacity commitment: A

tale of two sources. Journal of Economic Behavior & Organization, 150, pp.149-161.

Cooper, J., Fox, R., Loeprick, J. and Mohindra, K., 2017. Transfer pricing and developing

economies: A Handbook for policy makers and practitioners.The World Bank.15(1).pp.149-161.

Cristea, A.D. and Nguyen, D.X., 2016. Transfer pricing by multinational firms: New evidence

from foreign firm ownerships. American Economic Journal: Economic Policy, 8(3), pp.170-202.

Davies, R.B., Martin, J., Parenti, M. and Toubal, F., 2018.Knocking on tax haven’s door:

Multinational firms and transfer pricing. Review of Economics and Statistics, 100(1), pp.120-

134.

deMatta, R. and Miller, T., 2015. Formation of a strategic manufacturing and distribution

network with transfer prices. European Journal of Operational Research, 241(2), pp.435-448.

Frost, J., Vogel, R. and Bagban, K., 2016. Managing Interdependence in Multi-business

Organizations. Schmalenbach Business Review, 17(2), pp.225-260.

Books and Journals

Abdallah, W., 2016. Documentation of Transfer Pricing: A New Global Approach. International

Journal of Accounting and Taxation, 4(2), pp.37-55.

Arruñada, B. and Hansen, S., 2015. Organizing good public provision: Lessons from Managerial

Accounting. International Review of Law and Economics, 42, pp.185-191.

Bakaouka, E. and Million, C., 2018. Vertical licensing, input pricing, and entry. International

Journal of Industrial Organization, 59, pp.66-96.

Chenhall, R.H. and Moers, F., 2015.The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, organizations and

society, 47, pp.1-13.

Colombo, S. and Scrimitore, M., 2018.A managerial delegation under capacity commitment: A

tale of two sources. Journal of Economic Behavior & Organization, 150, pp.149-161.

Cooper, J., Fox, R., Loeprick, J. and Mohindra, K., 2017. Transfer pricing and developing

economies: A Handbook for policy makers and practitioners.The World Bank.15(1).pp.149-161.

Cristea, A.D. and Nguyen, D.X., 2016. Transfer pricing by multinational firms: New evidence

from foreign firm ownerships. American Economic Journal: Economic Policy, 8(3), pp.170-202.

Davies, R.B., Martin, J., Parenti, M. and Toubal, F., 2018.Knocking on tax haven’s door:

Multinational firms and transfer pricing. Review of Economics and Statistics, 100(1), pp.120-

134.

deMatta, R. and Miller, T., 2015. Formation of a strategic manufacturing and distribution

network with transfer prices. European Journal of Operational Research, 241(2), pp.435-448.

Frost, J., Vogel, R. and Bagban, K., 2016. Managing Interdependence in Multi-business

Organizations. Schmalenbach Business Review, 17(2), pp.225-260.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.