Management Accounting Report: UCK Furniture, Financial Analysis, UK

VerifiedAdded on 2023/01/12

|18

|3698

|77

Report

AI Summary

This management accounting report focuses on UCK Furniture, a UK-based furniture manufacturer and seller. It defines management accounting and its role in decision-making, emphasizing the analysis of financial information for organizational improvement. The report details various management accounting systems like cost accounting, price optimization, job costing, and inventory management, explaining their benefits for UCK Furniture. It further explores essential reporting systems such as budget, performance, inventory management, and accounting receivable reports. The report also delves into costing methods like marginal and absorption costing, providing calculations and comparisons. Additionally, it discusses budgetary control and flexible budgeting as planning tools. The report concludes by highlighting the interdependencies between management accounting systems and reporting, showcasing how these are crucial for achieving organizational goals and objectives. The analysis aims to assist managers in making informed decisions for the financial stability and enhanced performance of UCK Furniture.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is defined as an activity of analysing financial information

available in financial records with an aim of making an effective decision for future

improvement in financial position of an organisation (Arroyo, 2012). It requires support from

finance department for recording accurate and reliable data that truly indicates the financial

position while overviewing financial statement of an organisation. It makes easy for stakeholders

to decide rather to stay with company or not according to their profitability. The present

assignment report is based on UCK Furniture which is engaged in manufacturing and selling

various designs of furniture in United Kingdom. The report explains the management accounting

concept with its different systems useful for chosen organisation. Along with this, the report also

describes the different costing methods along with calculation of net profitability, planning tools

to control budget and techniques to resolve financial issues faced by an organisation.

TASK 1

P1:

Management accounting is considered as a process of framing plans and making

decisions to enhance the performance level of an organisation by analysing the financial

statements prepared on annual basis (Badolato, Donelson and Ege, 2014). It is useful for

stakeholders to get information about the company’s present financial position on the basis of

which further investment decision should be made. It consists of various systems that

management of UCK furniture can adopt in order to maintain financial stability in competitive

market for longer period of time. These systems include:

COST ACCOUNTING SYSTEM

It is a system which used in manufacturing industries for purpose to evaluate flow of

inventory through various stage of production. Cost accounting involves various cost of product

in organisation which are measuring, recording and reporting cost with updated information of

cost (Christ and Burritt, 2013). Cost accounting system is a framework used by firms to estimate

the cost of their products for analysing profitability, stock valuation, control cost and accounts

for various manufacturing cost. Cost accounting system helps UCK Furniture to estimate the

closing value for material inventory, work-in-progress and finished goods inventory in preparing

Management accounting is defined as an activity of analysing financial information

available in financial records with an aim of making an effective decision for future

improvement in financial position of an organisation (Arroyo, 2012). It requires support from

finance department for recording accurate and reliable data that truly indicates the financial

position while overviewing financial statement of an organisation. It makes easy for stakeholders

to decide rather to stay with company or not according to their profitability. The present

assignment report is based on UCK Furniture which is engaged in manufacturing and selling

various designs of furniture in United Kingdom. The report explains the management accounting

concept with its different systems useful for chosen organisation. Along with this, the report also

describes the different costing methods along with calculation of net profitability, planning tools

to control budget and techniques to resolve financial issues faced by an organisation.

TASK 1

P1:

Management accounting is considered as a process of framing plans and making

decisions to enhance the performance level of an organisation by analysing the financial

statements prepared on annual basis (Badolato, Donelson and Ege, 2014). It is useful for

stakeholders to get information about the company’s present financial position on the basis of

which further investment decision should be made. It consists of various systems that

management of UCK furniture can adopt in order to maintain financial stability in competitive

market for longer period of time. These systems include:

COST ACCOUNTING SYSTEM

It is a system which used in manufacturing industries for purpose to evaluate flow of

inventory through various stage of production. Cost accounting involves various cost of product

in organisation which are measuring, recording and reporting cost with updated information of

cost (Christ and Burritt, 2013). Cost accounting system is a framework used by firms to estimate

the cost of their products for analysing profitability, stock valuation, control cost and accounts

for various manufacturing cost. Cost accounting system helps UCK Furniture to estimate the

closing value for material inventory, work-in-progress and finished goods inventory in preparing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial statement of company. UCK Furniture can plan properly and take effective decision

with the help of cost accounting system.

PRICE OPTIMISATION SYSTEM

Price optimisation system: It is a mathematical analysis of the company which shows

the customer's approach in terms of different services and product cost direct with different

channel. Optimisation means to evaluate the best way out of all by which UCK Furniture gets the

profit and that will be evaluate by price distribution. Also defines the best result of pricing to

achieve the goals and objective of the company and adheres the profit (Dekker, 2016).

JOB COSTING SYSTEM

It involves primary expenses of material, labour and overheads. It is a system for

assigning and accumulating manufacturing cost of single unit of outputs. Job costing system is

evaluating the accounts of cost and revenue by individual job. Job costing system is also known

as job order costing which help to create unique products with tracking their cost. In job costing

system an accountant keeps all record of each job of cost and maintaining those data which help

easily operating business. Job costing system help UCK Furniture manager to calculate profit

earned on individual job. UCK Furniture can keep tracking records of individual or team job

performance by analysing their efficiency, cost control and productivity with job costing system

(Englund and Gerdin, 2014).

INVENTOTY MANAGEMENT SYSTEM

It is a system to maintain and record each inventories in every firm. Inventory

management system is the process that managing company's inventories in ordering, storing,

purchasing, shipping, receiving, tracking, warehousing, turnover and recording. It includes

management of raw material, work-in-process and finish products for a company. Inventory

management system help to control inventory of a firm by generating maximum profit from least

amount of inventory used to produce finished good with best quality and full customer

satisfaction. UCK Furniture should follow inventory management system which help the

company to minimise their inventory cost with maximise sales of product and generate profit.

Inventory management system can help UCK Furniture to manage their overall product cost by

less wastage of raw material (Hiebl, 2014).

with the help of cost accounting system.

PRICE OPTIMISATION SYSTEM

Price optimisation system: It is a mathematical analysis of the company which shows

the customer's approach in terms of different services and product cost direct with different

channel. Optimisation means to evaluate the best way out of all by which UCK Furniture gets the

profit and that will be evaluate by price distribution. Also defines the best result of pricing to

achieve the goals and objective of the company and adheres the profit (Dekker, 2016).

JOB COSTING SYSTEM

It involves primary expenses of material, labour and overheads. It is a system for

assigning and accumulating manufacturing cost of single unit of outputs. Job costing system is

evaluating the accounts of cost and revenue by individual job. Job costing system is also known

as job order costing which help to create unique products with tracking their cost. In job costing

system an accountant keeps all record of each job of cost and maintaining those data which help

easily operating business. Job costing system help UCK Furniture manager to calculate profit

earned on individual job. UCK Furniture can keep tracking records of individual or team job

performance by analysing their efficiency, cost control and productivity with job costing system

(Englund and Gerdin, 2014).

INVENTOTY MANAGEMENT SYSTEM

It is a system to maintain and record each inventories in every firm. Inventory

management system is the process that managing company's inventories in ordering, storing,

purchasing, shipping, receiving, tracking, warehousing, turnover and recording. It includes

management of raw material, work-in-process and finish products for a company. Inventory

management system help to control inventory of a firm by generating maximum profit from least

amount of inventory used to produce finished good with best quality and full customer

satisfaction. UCK Furniture should follow inventory management system which help the

company to minimise their inventory cost with maximise sales of product and generate profit.

Inventory management system can help UCK Furniture to manage their overall product cost by

less wastage of raw material (Hiebl, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2.

There are various management accounting reporting which are essential to prepare by the

manufacturing companies such as UCK Furniture in order to maintain records that truly indicates

the financial performance of an organisation. These reporting systems includes:

BUDGET REPORT

It is a report that compare a company’s actual performance to prepare estimate budget for

company during accounting period. Budget report also referred as a financial report of a

company in which financial data is prepared and recorded in a budget report. Budget report is

mainly prepared for a person, family, business, government and country. A budget report is an

internal report used by management to compare the estimate budget of a company. A budget

report can help UCK Furniture to organise their expenditure and saving of money which able to

save unexpected cost. UCK Furniture can control over flotation of money which help company

to invest in right place where they get more benefits with the help of preparing a budget report

(Honggowati and et.al., 2017).

PERFORMANCE REPORT

It is the report which addresses outcome of a work performance for an individual in

company. A business performance report is a valuable business tools that provides an overview

of business performance. Its combine all information and analysis the expenses, revenue and

profit of upcoming year in the company. The performance report is designed to assist the

management for develop their business which help a company in collecting and analysing data

from various source like customer feedback. It helps to improve business performance which

help an organisation identify their problem which was facing in the business. A performance

report can help UCK Furniture improve their business productivity and accuracy by analysing

company's performance which also make effective decision making and minimizing cost (Kober,

Subraamanniam and Watson, 2012).

INVENTORY MANAGEMENT REPORT

It is s report by management to accessing the report of inventory. It helps to record the

inventory of raw material which is prepared a finished good. Inventory management report is

prepared to look wastage and usage of inventory to make the final product. It helps to find out

There are various management accounting reporting which are essential to prepare by the

manufacturing companies such as UCK Furniture in order to maintain records that truly indicates

the financial performance of an organisation. These reporting systems includes:

BUDGET REPORT

It is a report that compare a company’s actual performance to prepare estimate budget for

company during accounting period. Budget report also referred as a financial report of a

company in which financial data is prepared and recorded in a budget report. Budget report is

mainly prepared for a person, family, business, government and country. A budget report is an

internal report used by management to compare the estimate budget of a company. A budget

report can help UCK Furniture to organise their expenditure and saving of money which able to

save unexpected cost. UCK Furniture can control over flotation of money which help company

to invest in right place where they get more benefits with the help of preparing a budget report

(Honggowati and et.al., 2017).

PERFORMANCE REPORT

It is the report which addresses outcome of a work performance for an individual in

company. A business performance report is a valuable business tools that provides an overview

of business performance. Its combine all information and analysis the expenses, revenue and

profit of upcoming year in the company. The performance report is designed to assist the

management for develop their business which help a company in collecting and analysing data

from various source like customer feedback. It helps to improve business performance which

help an organisation identify their problem which was facing in the business. A performance

report can help UCK Furniture improve their business productivity and accuracy by analysing

company's performance which also make effective decision making and minimizing cost (Kober,

Subraamanniam and Watson, 2012).

INVENTORY MANAGEMENT REPORT

It is s report by management to accessing the report of inventory. It helps to record the

inventory of raw material which is prepared a finished good. Inventory management report is

prepared to look wastage and usage of inventory to make the final product. It helps to find out

the estimate cost of product and control unnecessary wastage. Inventory management report help

to build balance focus between inventory investment and customer services. An inventory

management report can help UCK Furniture to prepare a report where company manger can

identify reducing wastage of inventory which help them save capital. UCK Furniture can make

their product performance report where summarized document prepared with the help of

inventory management report.

ACCOUNTING RECEIVABLE REPORT

It is a record that show the invoice of unpaid balance along with duration from which

they have been outstanding. The accounting receivable report is the primary tools used by

collecting overdue payment of client in the company. It contains every detail and contact

information in company for checking their dues and schedule time for payments. Accounting

revisable report help to categorised the due payment on the basis of their given date of collecting

their invoice. UCK Furniture should preparer accounting receivable report for updating their

payment due by suppliers and customer. Account receivable report help UCK Furniture to

invoice the report of each client and keeping sloe paying client on top which may become easy

for company to evaluate report (Melnyk and et.al., 2014).

M1.

Management accounting systems Benefits

Cost accounting system It assists management in framing pricing

policy by examining the actual perception of

targeted customers while buying products and

services.

Inventory management system It facilitate management in identifying the

level of inventory the company have at

present which makes easy for them to order

further stock if required, to meet customers’

needs and requirements.

Cost accounting system It directs an organisation to analyse total cost

incurred in manufacturing process so that an

effective price can be charged after adding

to build balance focus between inventory investment and customer services. An inventory

management report can help UCK Furniture to prepare a report where company manger can

identify reducing wastage of inventory which help them save capital. UCK Furniture can make

their product performance report where summarized document prepared with the help of

inventory management report.

ACCOUNTING RECEIVABLE REPORT

It is a record that show the invoice of unpaid balance along with duration from which

they have been outstanding. The accounting receivable report is the primary tools used by

collecting overdue payment of client in the company. It contains every detail and contact

information in company for checking their dues and schedule time for payments. Accounting

revisable report help to categorised the due payment on the basis of their given date of collecting

their invoice. UCK Furniture should preparer accounting receivable report for updating their

payment due by suppliers and customer. Account receivable report help UCK Furniture to

invoice the report of each client and keeping sloe paying client on top which may become easy

for company to evaluate report (Melnyk and et.al., 2014).

M1.

Management accounting systems Benefits

Cost accounting system It assists management in framing pricing

policy by examining the actual perception of

targeted customers while buying products and

services.

Inventory management system It facilitate management in identifying the

level of inventory the company have at

present which makes easy for them to order

further stock if required, to meet customers’

needs and requirements.

Cost accounting system It directs an organisation to analyse total cost

incurred in manufacturing process so that an

effective price can be charged after adding

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

margin on it.

D.

Management accounting and reporting system are very much dependent on each other in

order to achieve organisational goals and objectives within pre-determined time period. For an

instance, price optimisation system assists in framing pricing policy that will be easily accepted

by targeted customers. For this, such system requires to gather information from cost accounting

report which contains details regarding total cost company incurred in manufacturing furniture

products. It expands the profitability and customers’ satisfaction level.

TASK 2

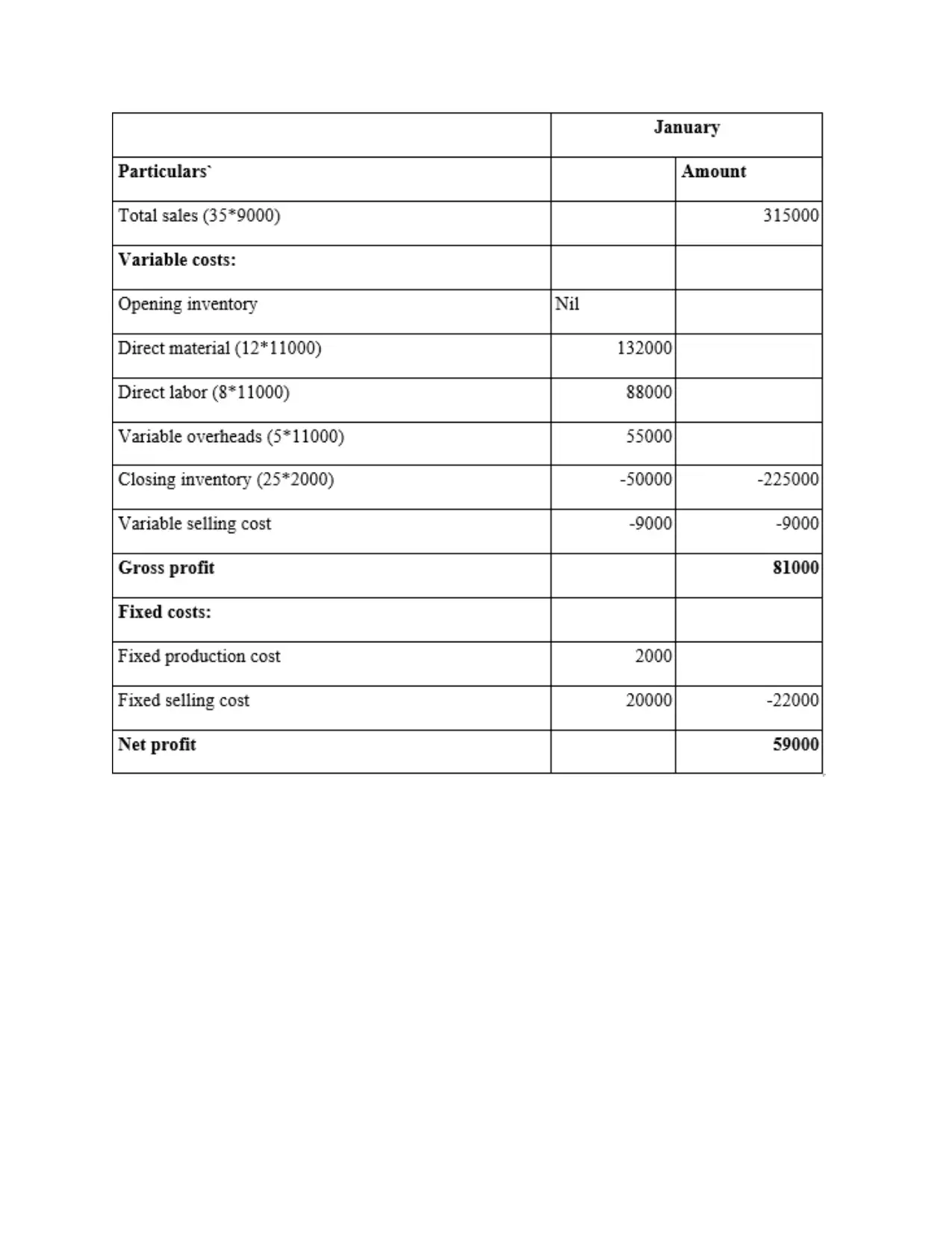

P3:

COST

Cost can be defining in terms of monetary they have been spent by company in order to

produce company's goodwill, revenue, effort, material, resources and good or services. It is

express as cash equivalence for an asset where all expenses incurred in company are cost. UCK

Furniture required cost to produce their goods and services. The expenditure of cost is required

in UCK Furniture to produce and sell their products which is prepared for customer.

MARGINAL COSTING

It is the change in total production cost that comes from making or producing one

additional unit. Marginal costing is effecting profit that change in volume or output by

differentiate between fixed and variable cost. It determines the economics of sale in organisation

to optimized product and overall operation. UCK Furniture should have utilized marginal cost

which help company to know their cost involve in production and quality of products (Nitzl,

2016).

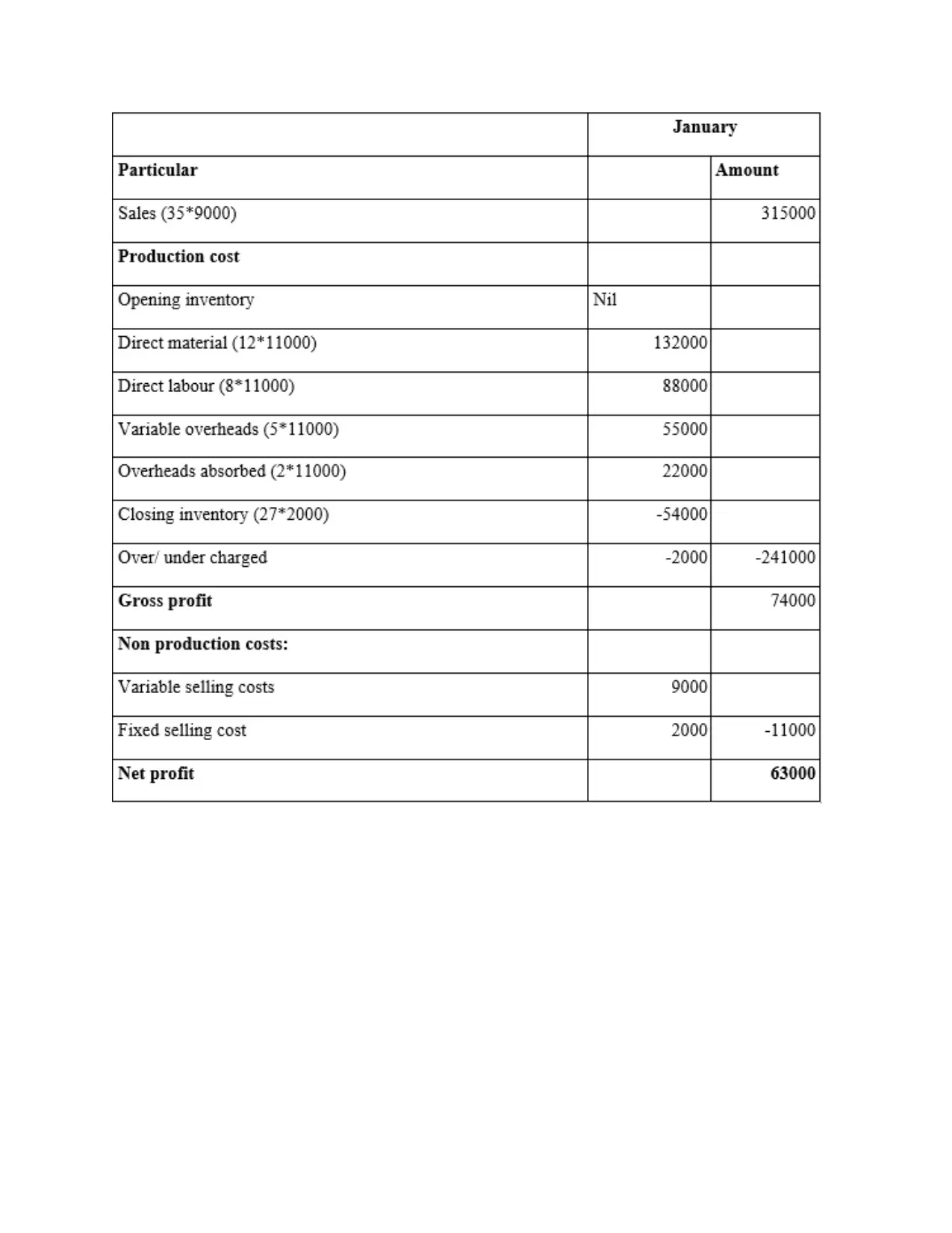

Cost card for this method for two months is as follows:

D.

Management accounting and reporting system are very much dependent on each other in

order to achieve organisational goals and objectives within pre-determined time period. For an

instance, price optimisation system assists in framing pricing policy that will be easily accepted

by targeted customers. For this, such system requires to gather information from cost accounting

report which contains details regarding total cost company incurred in manufacturing furniture

products. It expands the profitability and customers’ satisfaction level.

TASK 2

P3:

COST

Cost can be defining in terms of monetary they have been spent by company in order to

produce company's goodwill, revenue, effort, material, resources and good or services. It is

express as cash equivalence for an asset where all expenses incurred in company are cost. UCK

Furniture required cost to produce their goods and services. The expenditure of cost is required

in UCK Furniture to produce and sell their products which is prepared for customer.

MARGINAL COSTING

It is the change in total production cost that comes from making or producing one

additional unit. Marginal costing is effecting profit that change in volume or output by

differentiate between fixed and variable cost. It determines the economics of sale in organisation

to optimized product and overall operation. UCK Furniture should have utilized marginal cost

which help company to know their cost involve in production and quality of products (Nitzl,

2016).

Cost card for this method for two months is as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

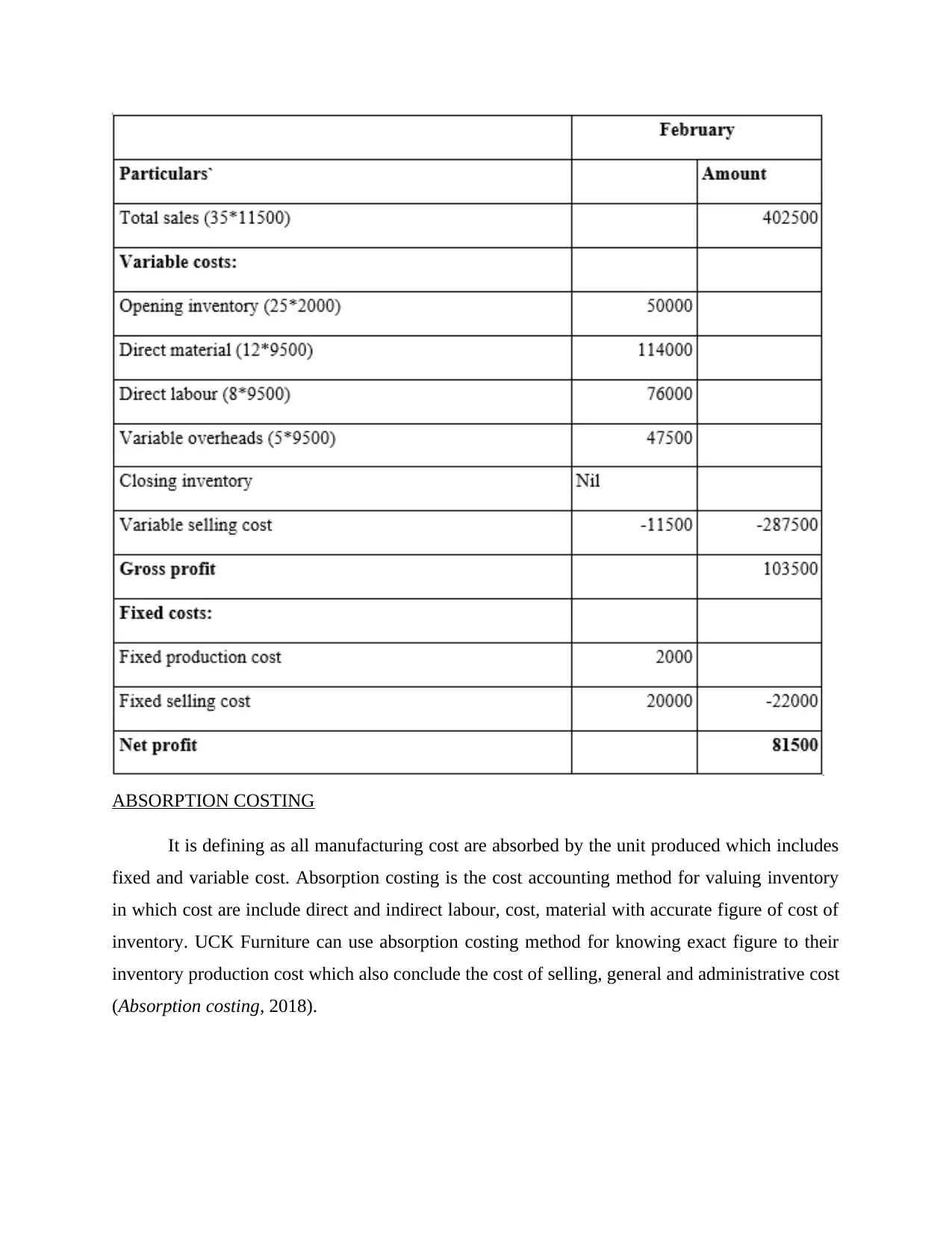

ABSORPTION COSTING

It is defining as all manufacturing cost are absorbed by the unit produced which includes

fixed and variable cost. Absorption costing is the cost accounting method for valuing inventory

in which cost are include direct and indirect labour, cost, material with accurate figure of cost of

inventory. UCK Furniture can use absorption costing method for knowing exact figure to their

inventory production cost which also conclude the cost of selling, general and administrative cost

(Absorption costing, 2018).

It is defining as all manufacturing cost are absorbed by the unit produced which includes

fixed and variable cost. Absorption costing is the cost accounting method for valuing inventory

in which cost are include direct and indirect labour, cost, material with accurate figure of cost of

inventory. UCK Furniture can use absorption costing method for knowing exact figure to their

inventory production cost which also conclude the cost of selling, general and administrative cost

(Absorption costing, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

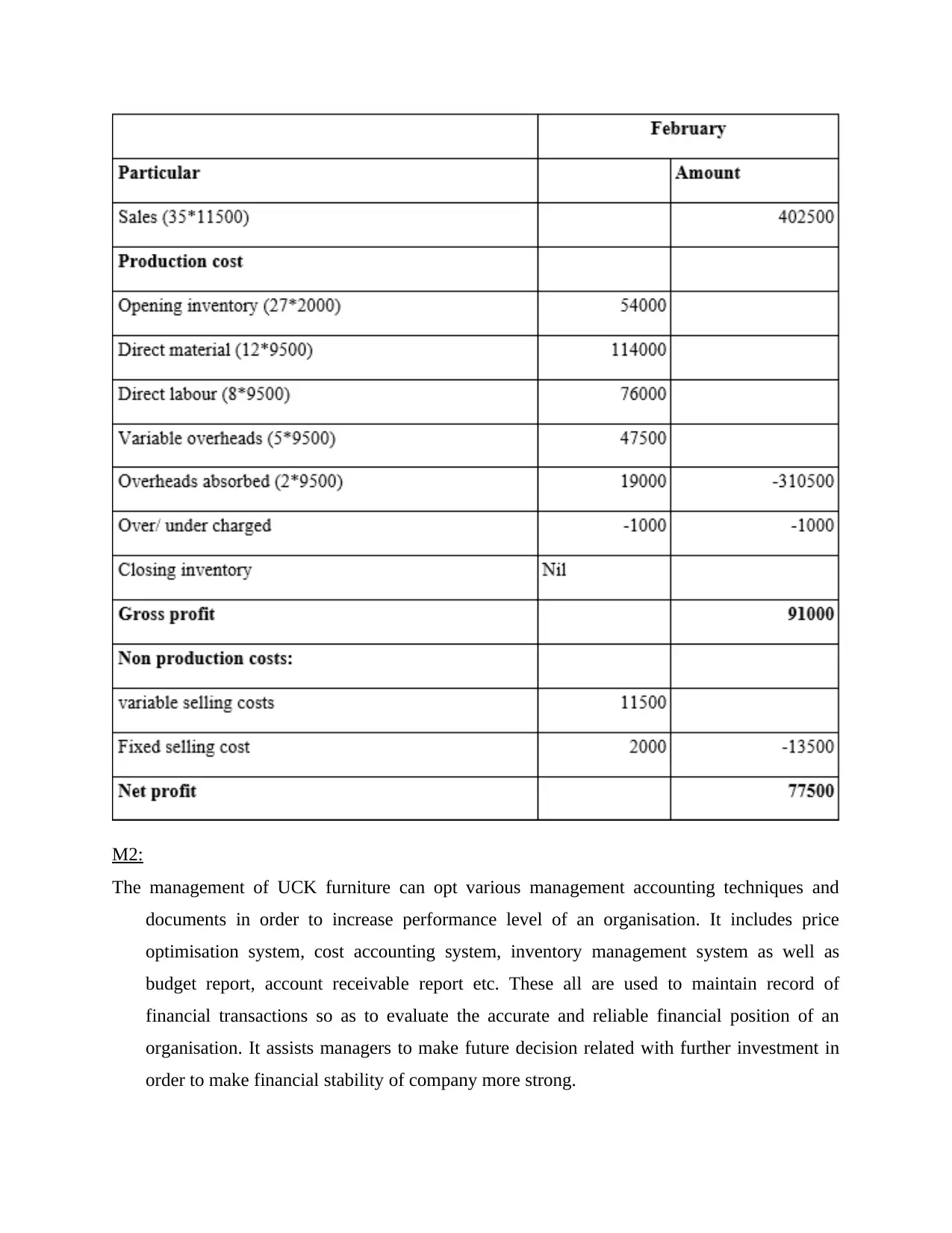

M2:

The management of UCK furniture can opt various management accounting techniques and

documents in order to increase performance level of an organisation. It includes price

optimisation system, cost accounting system, inventory management system as well as

budget report, account receivable report etc. These all are used to maintain record of

financial transactions so as to evaluate the accurate and reliable financial position of an

organisation. It assists managers to make future decision related with further investment in

order to make financial stability of company more strong.

The management of UCK furniture can opt various management accounting techniques and

documents in order to increase performance level of an organisation. It includes price

optimisation system, cost accounting system, inventory management system as well as

budget report, account receivable report etc. These all are used to maintain record of

financial transactions so as to evaluate the accurate and reliable financial position of an

organisation. It assists managers to make future decision related with further investment in

order to make financial stability of company more strong.

D2.

There are various techniques which is used to calculate net profit of UCK Furniture. While using

marginal costing method, 81000 comes as profit for January whereas 103500 comes as net

profit for the month of February. On the other hand, using absorption costing method, 74000

and 91000 comes as net profit for the month of January and February respectively. These

differences come due to inclusion of fixed cost.

TASK 3

P4.

BUDGET

A budget is a formal statement of estimated income and expenditure based on future plan

and objective. It is an instrument of management which is used in planning, programming and

control cost of business activity. UCK Furniture can get essential benefits for planning a budget

to know maximum expenditure and revenue incurred every year (Quattrone, 2016).

BUDGETARY CONTROL

It is a process by which budget is prepared for future period and then compared with

actual performance for finding changes in cost. Budgetary control helps to describe budget for

planning and controlling the cost of selling and producing goods or services. It helps a firm to

eliminate the waste and excess cost. UCK Furniture control on their wastage of cost by applying

budgetary control to minimise cost and invest in right place.

FLEXIBLE BUDGET

It is a financial plan to estimate revenue and expenses based in actual amount of output.

Flexible budget is a budget that varies from whole company or department need and demand. It

determines the accounting system for comparison to actual expenses in completed period where

all variable cost change to measure activity. UCK Furniture can calculate expenditure on

different level for increasing manager efficiency and effectiveness by flexible budget method

(Senftlechner, and Hiebl, 2015).

Advantage of flexible budget:

Have less workload or stress and has relatability.

There are various techniques which is used to calculate net profit of UCK Furniture. While using

marginal costing method, 81000 comes as profit for January whereas 103500 comes as net

profit for the month of February. On the other hand, using absorption costing method, 74000

and 91000 comes as net profit for the month of January and February respectively. These

differences come due to inclusion of fixed cost.

TASK 3

P4.

BUDGET

A budget is a formal statement of estimated income and expenditure based on future plan

and objective. It is an instrument of management which is used in planning, programming and

control cost of business activity. UCK Furniture can get essential benefits for planning a budget

to know maximum expenditure and revenue incurred every year (Quattrone, 2016).

BUDGETARY CONTROL

It is a process by which budget is prepared for future period and then compared with

actual performance for finding changes in cost. Budgetary control helps to describe budget for

planning and controlling the cost of selling and producing goods or services. It helps a firm to

eliminate the waste and excess cost. UCK Furniture control on their wastage of cost by applying

budgetary control to minimise cost and invest in right place.

FLEXIBLE BUDGET

It is a financial plan to estimate revenue and expenses based in actual amount of output.

Flexible budget is a budget that varies from whole company or department need and demand. It

determines the accounting system for comparison to actual expenses in completed period where

all variable cost change to measure activity. UCK Furniture can calculate expenditure on

different level for increasing manager efficiency and effectiveness by flexible budget method

(Senftlechner, and Hiebl, 2015).

Advantage of flexible budget:

Have less workload or stress and has relatability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.