Management Accounting Project: UCK Furniture Financial Analysis

VerifiedAdded on 2021/01/01

|11

|2679

|309

Project

AI Summary

This Management Accounting Project examines the financial performance of UCK Furniture. It begins by calculating net profit using various costing methods, including absorption and marginal costing, and analyzes their advantages and disadvantages. The project then explores different management accounting techniques and data interpretation. Task 2 focuses on the advantages and disadvantages of planning tools, analyzing monthly expenditures and calculating a cash budget. Finally, the project analyzes financial problems using accounting systems and financial ratios like ROCE, and explores measures to reduce these problems, comparing the performance of UCK Furniture and UCK Woodworks. The project highlights the importance of financial planning and control for business success.

Management Accounting

Project 2

Project 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Calculation of net profit by using various costing methods............................................1

1.2: Various types of management accounting techniques....................................................3

1.3: Data interpretation by using costing method...................................................................3

TASK 2............................................................................................................................................4

2.1: Advantage and disadvantage of various types of planning tools....................................4

2.2: Analysis of every expenditure for the month of July and August...................................4

2.3: Calculation of cash budget..............................................................................................5

TASK 3............................................................................................................................................5

3.1: Calculation of accounting system to analyse financial problems....................................5

3.2: Analysing the measures to reduce financial problems in both the company..................6

3.3: Analysis of planning tools used in company...................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Calculation of net profit by using various costing methods............................................1

1.2: Various types of management accounting techniques....................................................3

1.3: Data interpretation by using costing method...................................................................3

TASK 2............................................................................................................................................4

2.1: Advantage and disadvantage of various types of planning tools....................................4

2.2: Analysis of every expenditure for the month of July and August...................................4

2.3: Calculation of cash budget..............................................................................................5

TASK 3............................................................................................................................................5

3.1: Calculation of accounting system to analyse financial problems....................................5

3.2: Analysing the measures to reduce financial problems in both the company..................6

3.3: Analysis of planning tools used in company...................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is utmost crucial aspects for every business organisation. It is

helpful for the better results and development of the UCK group everyday financial transactions.

The main aim of managers is to make use of appropriate resources that are helpful for the

company for the longer period of time. This project module aims to delivery better under

understanding of costing methods those are useful for calculating net profit for the UCK

furniture. Advantage and disadvantage of adapting various types of planning tools that are used

for the budgetary control are mentioned under this report. Use of management accounting

systems in order to resolve financial issues are examining and discussed effectively under this

report (Bromwich and Scapens, 2016).

TASK 1

1.1: Calculation of net profit by using various costing methods

It is crucial for companies like UCK Furniture to make use of better resources so that

maximum profits can be attain in near future time. The role of manager is to organise necessary

information that are needed for the calculation of net earnings generated by UCK furniture

within an accounting period of time. Basically, they are related with the production of products

and wide verities of furniture as per the demand of the people. In this process certain costs are

incurred those are needed to be paid by the project manager on its daily manufacturing. Some of

them are either directly or indirectly make impacts on goodwill as well as productivity at the

same time (Amoako, 2013). It is said that cost is the value that is paid by the manager in order to

attain something. It happens to be more reliable in which overall calculation of total costs for

production of product in context to record information about cost of inventory in appropriate

format such as profit and loss statement, balances sheet and cash flow statement.

This would be useful for delivering better understanding of cost behaviour and other vital

financial aspects those are suitable for the company in longer period of time. Costing consist of

detail information about fixed cost in which all those cost that are applied in the same or

irrespective with the level of activities are taken into account in proper manner. There are various

types of costing methods that are helpful for finance managers in respect to calculate total net

profit during the time. Some of them are discussed underneath:

1

Management accounting is utmost crucial aspects for every business organisation. It is

helpful for the better results and development of the UCK group everyday financial transactions.

The main aim of managers is to make use of appropriate resources that are helpful for the

company for the longer period of time. This project module aims to delivery better under

understanding of costing methods those are useful for calculating net profit for the UCK

furniture. Advantage and disadvantage of adapting various types of planning tools that are used

for the budgetary control are mentioned under this report. Use of management accounting

systems in order to resolve financial issues are examining and discussed effectively under this

report (Bromwich and Scapens, 2016).

TASK 1

1.1: Calculation of net profit by using various costing methods

It is crucial for companies like UCK Furniture to make use of better resources so that

maximum profits can be attain in near future time. The role of manager is to organise necessary

information that are needed for the calculation of net earnings generated by UCK furniture

within an accounting period of time. Basically, they are related with the production of products

and wide verities of furniture as per the demand of the people. In this process certain costs are

incurred those are needed to be paid by the project manager on its daily manufacturing. Some of

them are either directly or indirectly make impacts on goodwill as well as productivity at the

same time (Amoako, 2013). It is said that cost is the value that is paid by the manager in order to

attain something. It happens to be more reliable in which overall calculation of total costs for

production of product in context to record information about cost of inventory in appropriate

format such as profit and loss statement, balances sheet and cash flow statement.

This would be useful for delivering better understanding of cost behaviour and other vital

financial aspects those are suitable for the company in longer period of time. Costing consist of

detail information about fixed cost in which all those cost that are applied in the same or

irrespective with the level of activities are taken into account in proper manner. There are various

types of costing methods that are helpful for finance managers in respect to calculate total net

profit during the time. Some of them are discussed underneath:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed and variable cost: It is known as one of the effective cost that would remain

constant and unchanged with an increment or reduction in total number of products or services

sold or manufactured by the company. While variable cost is said to be corporate expenses those

are changed in relation with the production capacity. Certain examples are fuel, repair, salary etc.

Historical cost: This seems to be effective measure of total value that is being utilise in

accounting for the evaluation of cost of assets on balance sheet. It is entirely based on nominal or

real cost of production.

Absorption costing: It is known as one of the effective method which is used during

production of product and services. It consists of both variable and fixed cost because of this it

need to be full costing (Klemstine and Maher, 2014). It is not taken into account as that much

effective in decision making.

Marginal costing: It refers as the utmost effective method which will be used by the

managers in production of one additional units of product. It includes only variable cost because

of this, it is known as period costing. In steed of this, management used to make use of this

costing method more effective for future decision making.

NET INCOME AS PER ABSORPTION COSTING:

Particular January February

Sales (35per units) 315000 402500

Deduct:

Cost of Production 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable expenses:

Variable sales overheads (@1 per unit) 9000 11500

Fixed selling expenses 2000 2000

Total costs 11000 13500

NET INCOME 8980 134210

Calculation of net profit by using marginal costing

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

2

constant and unchanged with an increment or reduction in total number of products or services

sold or manufactured by the company. While variable cost is said to be corporate expenses those

are changed in relation with the production capacity. Certain examples are fuel, repair, salary etc.

Historical cost: This seems to be effective measure of total value that is being utilise in

accounting for the evaluation of cost of assets on balance sheet. It is entirely based on nominal or

real cost of production.

Absorption costing: It is known as one of the effective method which is used during

production of product and services. It consists of both variable and fixed cost because of this it

need to be full costing (Klemstine and Maher, 2014). It is not taken into account as that much

effective in decision making.

Marginal costing: It refers as the utmost effective method which will be used by the

managers in production of one additional units of product. It includes only variable cost because

of this, it is known as period costing. In steed of this, management used to make use of this

costing method more effective for future decision making.

NET INCOME AS PER ABSORPTION COSTING:

Particular January February

Sales (35per units) 315000 402500

Deduct:

Cost of Production 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable expenses:

Variable sales overheads (@1 per unit) 9000 11500

Fixed selling expenses 2000 2000

Total costs 11000 13500

NET INCOME 8980 134210

Calculation of net profit by using marginal costing

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

2

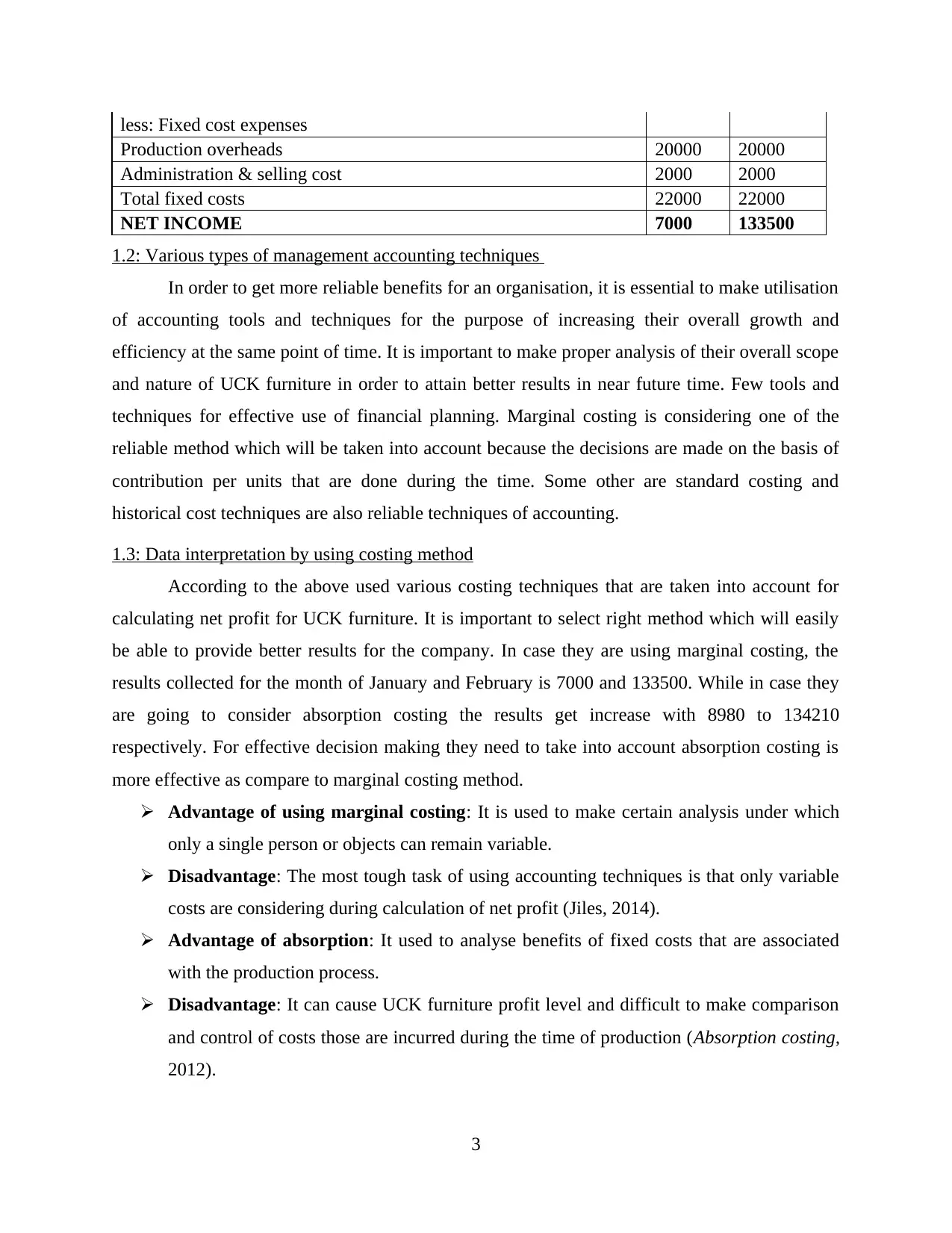

less: Fixed cost expenses

Production overheads 20000 20000

Administration & selling cost 2000 2000

Total fixed costs 22000 22000

NET INCOME 7000 133500

1.2: Various types of management accounting techniques

In order to get more reliable benefits for an organisation, it is essential to make utilisation

of accounting tools and techniques for the purpose of increasing their overall growth and

efficiency at the same point of time. It is important to make proper analysis of their overall scope

and nature of UCK furniture in order to attain better results in near future time. Few tools and

techniques for effective use of financial planning. Marginal costing is considering one of the

reliable method which will be taken into account because the decisions are made on the basis of

contribution per units that are done during the time. Some other are standard costing and

historical cost techniques are also reliable techniques of accounting.

1.3: Data interpretation by using costing method

According to the above used various costing techniques that are taken into account for

calculating net profit for UCK furniture. It is important to select right method which will easily

be able to provide better results for the company. In case they are using marginal costing, the

results collected for the month of January and February is 7000 and 133500. While in case they

are going to consider absorption costing the results get increase with 8980 to 134210

respectively. For effective decision making they need to take into account absorption costing is

more effective as compare to marginal costing method.

Advantage of using marginal costing: It is used to make certain analysis under which

only a single person or objects can remain variable.

Disadvantage: The most tough task of using accounting techniques is that only variable

costs are considering during calculation of net profit (Jiles, 2014).

Advantage of absorption: It used to analyse benefits of fixed costs that are associated

with the production process.

Disadvantage: It can cause UCK furniture profit level and difficult to make comparison

and control of costs those are incurred during the time of production (Absorption costing,

2012).

3

Production overheads 20000 20000

Administration & selling cost 2000 2000

Total fixed costs 22000 22000

NET INCOME 7000 133500

1.2: Various types of management accounting techniques

In order to get more reliable benefits for an organisation, it is essential to make utilisation

of accounting tools and techniques for the purpose of increasing their overall growth and

efficiency at the same point of time. It is important to make proper analysis of their overall scope

and nature of UCK furniture in order to attain better results in near future time. Few tools and

techniques for effective use of financial planning. Marginal costing is considering one of the

reliable method which will be taken into account because the decisions are made on the basis of

contribution per units that are done during the time. Some other are standard costing and

historical cost techniques are also reliable techniques of accounting.

1.3: Data interpretation by using costing method

According to the above used various costing techniques that are taken into account for

calculating net profit for UCK furniture. It is important to select right method which will easily

be able to provide better results for the company. In case they are using marginal costing, the

results collected for the month of January and February is 7000 and 133500. While in case they

are going to consider absorption costing the results get increase with 8980 to 134210

respectively. For effective decision making they need to take into account absorption costing is

more effective as compare to marginal costing method.

Advantage of using marginal costing: It is used to make certain analysis under which

only a single person or objects can remain variable.

Disadvantage: The most tough task of using accounting techniques is that only variable

costs are considering during calculation of net profit (Jiles, 2014).

Advantage of absorption: It used to analyse benefits of fixed costs that are associated

with the production process.

Disadvantage: It can cause UCK furniture profit level and difficult to make comparison

and control of costs those are incurred during the time of production (Absorption costing,

2012).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

2.1: Advantage and disadvantage of various types of planning tools

Planning is an essential aspect that assist an organisation in attaining future aims and

objectives in effective manner. It is utilising to management in discharged of their basic

operations during forecasting, planning and communicating overall financial transaction. This

used to analyse various ways for effective control of business operations through undertaking a

appraisal of physical and financial targets of the company. All the effective activities that are

needed to be taken into account for overall expenses that are related with the UCK furniture. The

primary motive of the company is helpful to make ensure that expenses cannot reverse their total

earning those are incurred through the company before making budgets. Some crucial planning

tools are:

Forecasting tool: It is important for an organisation to make use of strategies in order to

determine future cost and expenses those are going to be incurred by the UCK group. This will

be helpful to control additional cost that are done at the time of production process.

Advantage: The utmost crucial benefit of quantitative forecasting approach those are

related with projections that depends on strength of past data.

Disadvantage: It is based on proper estimation so that it is hard to make better outcomes.

Contingency tool: It is known as organisational theory that used to claim that there are no

any other ways that make company to take better decision. This is simply helpful for analysing

business risks that are occur in the department (Huber and Scheytt, 2013).

Advantage: This seems to be control losses that are major concern for an organisation. It

is more comprehensive for the managers to use this tool.

Disadvantage: Because of the uncertainty, it is hard to control and deal with unseen risks

that are arises in an organisation.

2.2: Analysis of every expenditure for the month of July and August

In order to get better outcomes in accordance with the variable cost incurred by UCK

furniture. It will be examining that high and low activity procedure is taken into account as more

reliable task. To calculate total expense incurred during the month of July and August are

discussed underneath:

(Total expenses of high activity – Expenses from low activity)

4

2.1: Advantage and disadvantage of various types of planning tools

Planning is an essential aspect that assist an organisation in attaining future aims and

objectives in effective manner. It is utilising to management in discharged of their basic

operations during forecasting, planning and communicating overall financial transaction. This

used to analyse various ways for effective control of business operations through undertaking a

appraisal of physical and financial targets of the company. All the effective activities that are

needed to be taken into account for overall expenses that are related with the UCK furniture. The

primary motive of the company is helpful to make ensure that expenses cannot reverse their total

earning those are incurred through the company before making budgets. Some crucial planning

tools are:

Forecasting tool: It is important for an organisation to make use of strategies in order to

determine future cost and expenses those are going to be incurred by the UCK group. This will

be helpful to control additional cost that are done at the time of production process.

Advantage: The utmost crucial benefit of quantitative forecasting approach those are

related with projections that depends on strength of past data.

Disadvantage: It is based on proper estimation so that it is hard to make better outcomes.

Contingency tool: It is known as organisational theory that used to claim that there are no

any other ways that make company to take better decision. This is simply helpful for analysing

business risks that are occur in the department (Huber and Scheytt, 2013).

Advantage: This seems to be control losses that are major concern for an organisation. It

is more comprehensive for the managers to use this tool.

Disadvantage: Because of the uncertainty, it is hard to control and deal with unseen risks

that are arises in an organisation.

2.2: Analysis of every expenditure for the month of July and August

In order to get better outcomes in accordance with the variable cost incurred by UCK

furniture. It will be examining that high and low activity procedure is taken into account as more

reliable task. To calculate total expense incurred during the month of July and August are

discussed underneath:

(Total expenses of high activity – Expenses from low activity)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

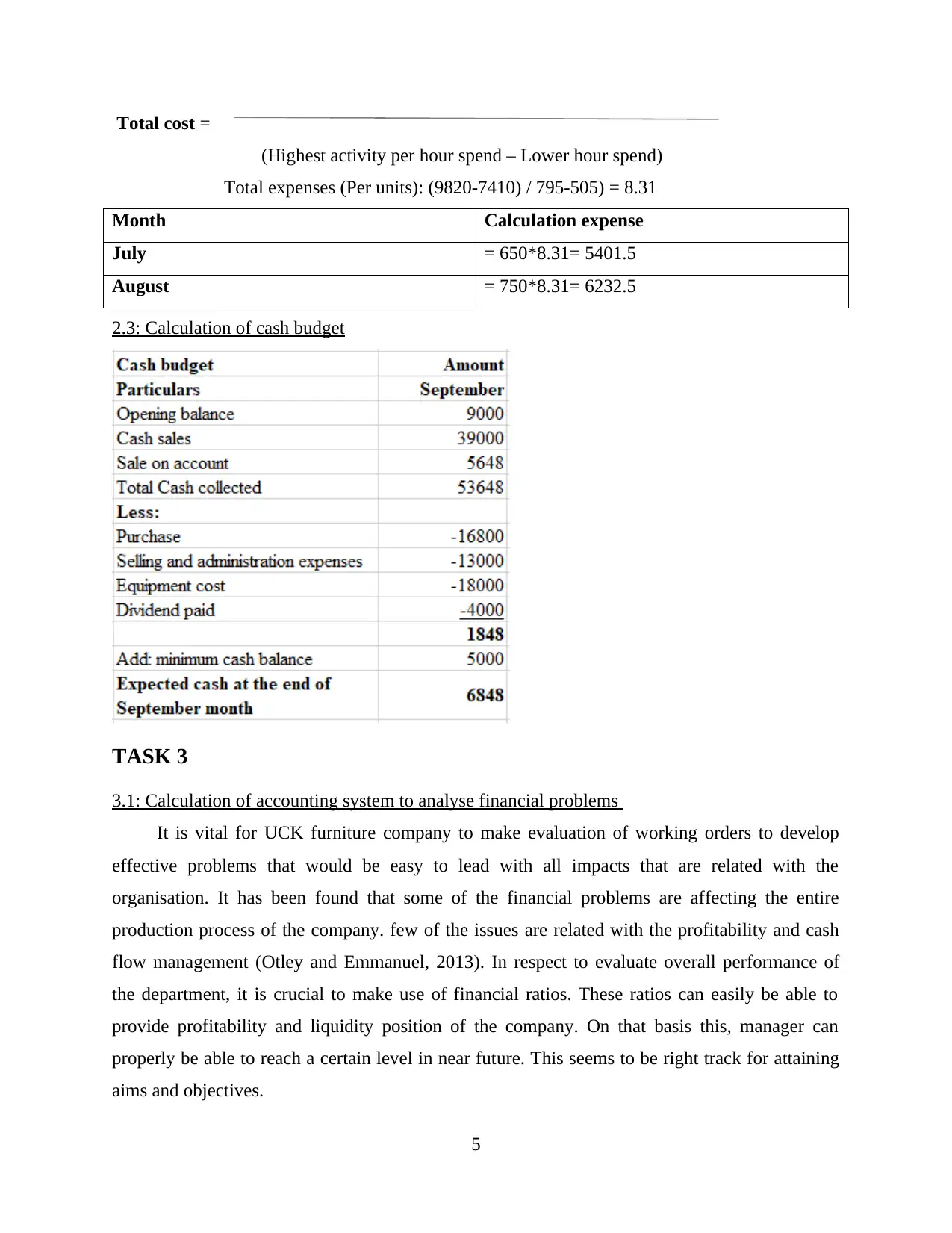

Total cost =

(Highest activity per hour spend – Lower hour spend)

Total expenses (Per units): (9820-7410) / 795-505) = 8.31

Month Calculation expense

July = 650*8.31= 5401.5

August = 750*8.31= 6232.5

2.3: Calculation of cash budget

TASK 3

3.1: Calculation of accounting system to analyse financial problems

It is vital for UCK furniture company to make evaluation of working orders to develop

effective problems that would be easy to lead with all impacts that are related with the

organisation. It has been found that some of the financial problems are affecting the entire

production process of the company. few of the issues are related with the profitability and cash

flow management (Otley and Emmanuel, 2013). In respect to evaluate overall performance of

the department, it is crucial to make use of financial ratios. These ratios can easily be able to

provide profitability and liquidity position of the company. On that basis this, manager can

properly be able to reach a certain level in near future. This seems to be right track for attaining

aims and objectives.

5

(Highest activity per hour spend – Lower hour spend)

Total expenses (Per units): (9820-7410) / 795-505) = 8.31

Month Calculation expense

July = 650*8.31= 5401.5

August = 750*8.31= 6232.5

2.3: Calculation of cash budget

TASK 3

3.1: Calculation of accounting system to analyse financial problems

It is vital for UCK furniture company to make evaluation of working orders to develop

effective problems that would be easy to lead with all impacts that are related with the

organisation. It has been found that some of the financial problems are affecting the entire

production process of the company. few of the issues are related with the profitability and cash

flow management (Otley and Emmanuel, 2013). In respect to evaluate overall performance of

the department, it is crucial to make use of financial ratios. These ratios can easily be able to

provide profitability and liquidity position of the company. On that basis this, manager can

properly be able to reach a certain level in near future. This seems to be right track for attaining

aims and objectives.

5

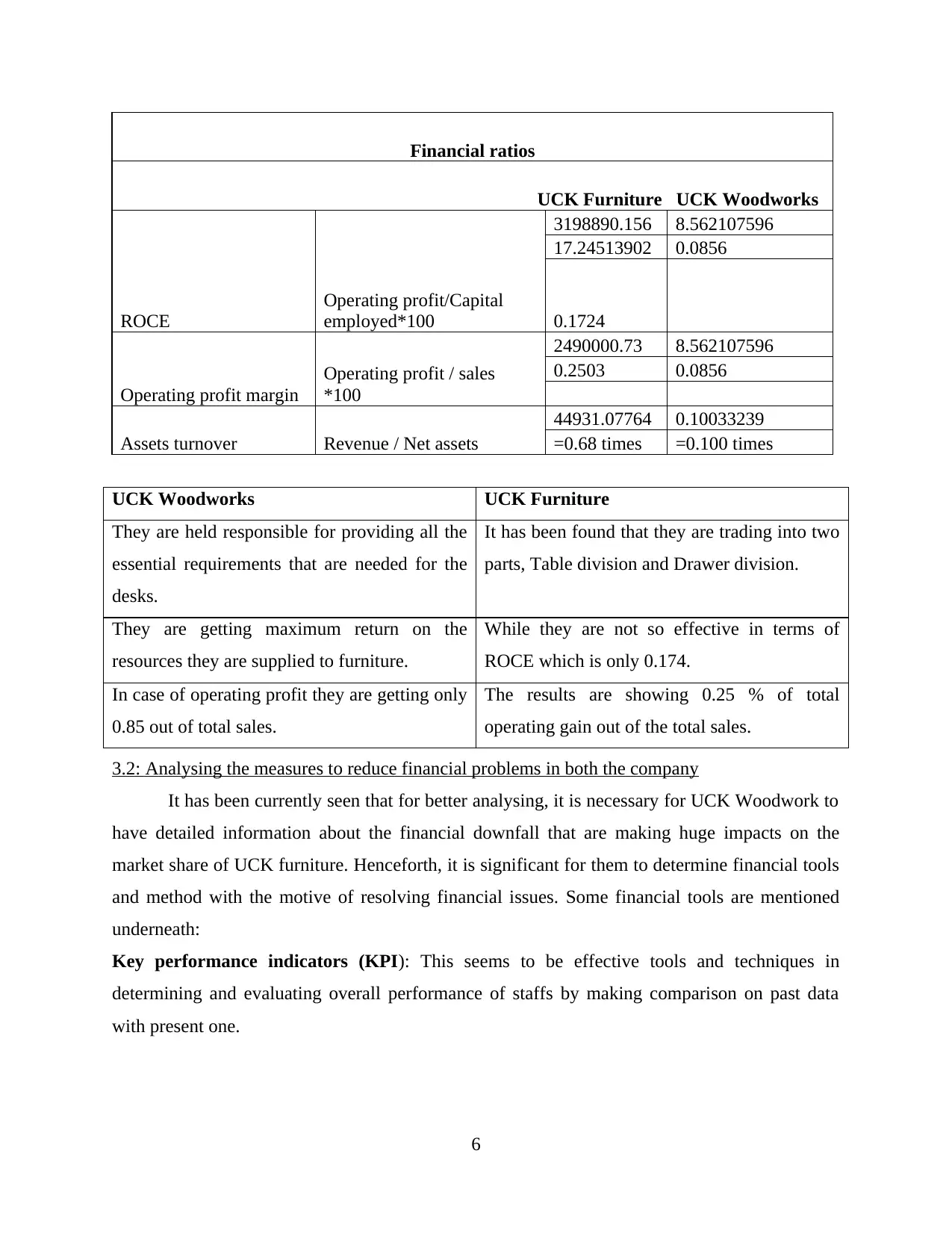

Financial ratios

UCK Furniture UCK Woodworks

ROCE

Operating profit/Capital

employed*100

3198890.156 8.562107596

17.24513902 0.0856

0.1724

Operating profit margin

Operating profit / sales

*100

2490000.73 8.562107596

0.2503 0.0856

Assets turnover Revenue / Net assets

44931.07764 0.10033239

=0.68 times =0.100 times

UCK Woodworks UCK Furniture

They are held responsible for providing all the

essential requirements that are needed for the

desks.

It has been found that they are trading into two

parts, Table division and Drawer division.

They are getting maximum return on the

resources they are supplied to furniture.

While they are not so effective in terms of

ROCE which is only 0.174.

In case of operating profit they are getting only

0.85 out of total sales.

The results are showing 0.25 % of total

operating gain out of the total sales.

3.2: Analysing the measures to reduce financial problems in both the company

It has been currently seen that for better analysing, it is necessary for UCK Woodwork to

have detailed information about the financial downfall that are making huge impacts on the

market share of UCK furniture. Henceforth, it is significant for them to determine financial tools

and method with the motive of resolving financial issues. Some financial tools are mentioned

underneath:

Key performance indicators (KPI): This seems to be effective tools and techniques in

determining and evaluating overall performance of staffs by making comparison on past data

with present one.

6

UCK Furniture UCK Woodworks

ROCE

Operating profit/Capital

employed*100

3198890.156 8.562107596

17.24513902 0.0856

0.1724

Operating profit margin

Operating profit / sales

*100

2490000.73 8.562107596

0.2503 0.0856

Assets turnover Revenue / Net assets

44931.07764 0.10033239

=0.68 times =0.100 times

UCK Woodworks UCK Furniture

They are held responsible for providing all the

essential requirements that are needed for the

desks.

It has been found that they are trading into two

parts, Table division and Drawer division.

They are getting maximum return on the

resources they are supplied to furniture.

While they are not so effective in terms of

ROCE which is only 0.174.

In case of operating profit they are getting only

0.85 out of total sales.

The results are showing 0.25 % of total

operating gain out of the total sales.

3.2: Analysing the measures to reduce financial problems in both the company

It has been currently seen that for better analysing, it is necessary for UCK Woodwork to

have detailed information about the financial downfall that are making huge impacts on the

market share of UCK furniture. Henceforth, it is significant for them to determine financial tools

and method with the motive of resolving financial issues. Some financial tools are mentioned

underneath:

Key performance indicators (KPI): This seems to be effective tools and techniques in

determining and evaluating overall performance of staffs by making comparison on past data

with present one.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial governance: It is known as all the rules and regulations that are made by the

government in order to run their business in more effective and efficient manner for the long

period of time (Speklé and Verbeeten, 2014).

3.3: Analysis of planning tools used in company

There are various tools that are discussed in the above report. All of them are having

certain benefits and limitations. This will assist the department to make better understanding of

business and their future growth. Some of them are:

Contingency tools are more reliable and effective tools that is used for the purpose of

hedging all those business risk that are making huge impacts on the overall performance of the

company. while forecasting tools can be helpful for estimating future losses by preparing specific

kind of budget such as sales and operations. This will guide the manager to operate in better

manner in the department.

CONCLUSION

This project report used to conclude that there is various crucial method which are taken into

account for calculating net income of UCK furniture. Utilisation of planning tools with the merit

and demerit are also discussed those are beneficial for the company for the long time basis. All

the analysis is done to make better growth and sustainability in near future time.

7

government in order to run their business in more effective and efficient manner for the long

period of time (Speklé and Verbeeten, 2014).

3.3: Analysis of planning tools used in company

There are various tools that are discussed in the above report. All of them are having

certain benefits and limitations. This will assist the department to make better understanding of

business and their future growth. Some of them are:

Contingency tools are more reliable and effective tools that is used for the purpose of

hedging all those business risk that are making huge impacts on the overall performance of the

company. while forecasting tools can be helpful for estimating future losses by preparing specific

kind of budget such as sales and operations. This will guide the manager to operate in better

manner in the department.

CONCLUSION

This project report used to conclude that there is various crucial method which are taken into

account for calculating net income of UCK furniture. Utilisation of planning tools with the merit

and demerit are also discussed those are beneficial for the company for the long time basis. All

the analysis is done to make better growth and sustainability in near future time.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Amoako, G.K., 2013. Accounting practices of SMEs: A case study of Kumasi Metropolis in

Ghana. International Journal of Business and Management. 8(24). p.73.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research. 31. pp.1-9.

Huber, C. and Scheytt, T., 2013. The dispositif of risk management: Reconstructing risk

management after the financial crisis. Management Accounting Research. 24(2). pp.88-

99.

Jiles, L., 2014. Management accounting career readiness: Shaping your curriculum. Strategic

Finance. 96(2). p.38.

Klemstine, C. F. and Maher, M., 2014. Management Accounting Research (RLE Accounting): A

Review and Annotated Bibliography. Routledge.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Speklé, R. F. and Verbeeten, F. H., 2014. The use of performance measurement systems in the

public sector: Effects on performance. Management Accounting Research. 25(2). pp.131-

146.

Online

Absorption costing. 2012.[Online]. Available through:

<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Marginal%20and

%20absorption%20costing.aspx>.

8

Books and Journals:

Amoako, G.K., 2013. Accounting practices of SMEs: A case study of Kumasi Metropolis in

Ghana. International Journal of Business and Management. 8(24). p.73.

Bromwich, M. and Scapens, R.W., 2016. Management accounting research: 25 years

on. Management Accounting Research. 31. pp.1-9.

Huber, C. and Scheytt, T., 2013. The dispositif of risk management: Reconstructing risk

management after the financial crisis. Management Accounting Research. 24(2). pp.88-

99.

Jiles, L., 2014. Management accounting career readiness: Shaping your curriculum. Strategic

Finance. 96(2). p.38.

Klemstine, C. F. and Maher, M., 2014. Management Accounting Research (RLE Accounting): A

Review and Annotated Bibliography. Routledge.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Speklé, R. F. and Verbeeten, F. H., 2014. The use of performance measurement systems in the

public sector: Effects on performance. Management Accounting Research. 25(2). pp.131-

146.

Online

Absorption costing. 2012.[Online]. Available through:

<http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Marginal%20and

%20absorption%20costing.aspx>.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.