HNBS 305: Management Accounting Project for UCK Furniture Analysis

VerifiedAdded on 2020/07/23

|10

|2986

|55

Project

AI Summary

This project report delves into the core elements of management accounting, focusing on cost calculation techniques and budgetary control within the context of UCK Furniture. The report begins by outlining various cost analysis methods, including marginal and absorption costing, and prepares an income statement. It then explores budgetary control tools, analyzing their advantages and disadvantages, along with practical applications such as the high-low method and cash budgeting. The report further examines how organizations adapt management accounting systems to address financial challenges and improve performance. It provides comparative analyses and evaluates planning tools. The report concludes by summarizing key findings and recommendations for UCK Furniture, offering a comprehensive overview of management accounting principles and their practical application. The financial position is found in a positive situation.

MANAGEMENT

ACCOUNTING

[PROJECT-2]

ACCOUNTING

[PROJECT-2]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Calculate cost using appropriate techniques of analysing cost and prepare income

statement.....................................................................................................................................1

1.2 Accurately apply a range of management accounting techniques and financial reporting...2

1.3 Produce financial reports accurately apply and interpret data for a range of business

activities......................................................................................................................................2

TASK 2 ...........................................................................................................................................3

2.1 Advantages and disadvantages of various type of planning tools using in budgetary

control.........................................................................................................................................3

2.2 High low method to determine the expenses if the numbers for July and August is 650 and

750...............................................................................................................................................5

2.3 Purpose of budget and preparing cash budget.......................................................................5

TASK 3............................................................................................................................................6

3.1 Compare how organisations are adapting management accounting system to respond

financial problems.......................................................................................................................6

3.2 how management accounting can help to improve the financial performance of both

companies to attain sustainable success......................................................................................7

3.3 evaluate the planning tools used in management accounting to reduce the financial

problems......................................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Calculate cost using appropriate techniques of analysing cost and prepare income

statement.....................................................................................................................................1

1.2 Accurately apply a range of management accounting techniques and financial reporting...2

1.3 Produce financial reports accurately apply and interpret data for a range of business

activities......................................................................................................................................2

TASK 2 ...........................................................................................................................................3

2.1 Advantages and disadvantages of various type of planning tools using in budgetary

control.........................................................................................................................................3

2.2 High low method to determine the expenses if the numbers for July and August is 650 and

750...............................................................................................................................................5

2.3 Purpose of budget and preparing cash budget.......................................................................5

TASK 3............................................................................................................................................6

3.1 Compare how organisations are adapting management accounting system to respond

financial problems.......................................................................................................................6

3.2 how management accounting can help to improve the financial performance of both

companies to attain sustainable success......................................................................................7

3.3 evaluate the planning tools used in management accounting to reduce the financial

problems......................................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Calculating the cost and preparing the budgets are the essential elements of management

accounting (Chiwamit, Modell and Yang, 2014). This report defines the cost calculating

techniques to determine the cost and profit for UCK furnitures. Planning tools are also defined

which are used in budgetary control process. Ways are compared that how business are

implementing management accounting system to respond financial problems. Practical examples

are defined in this context subject to evaluating the cost and budgetary control. Evaluation

methods are also described in respect of financial problems

TASK 1

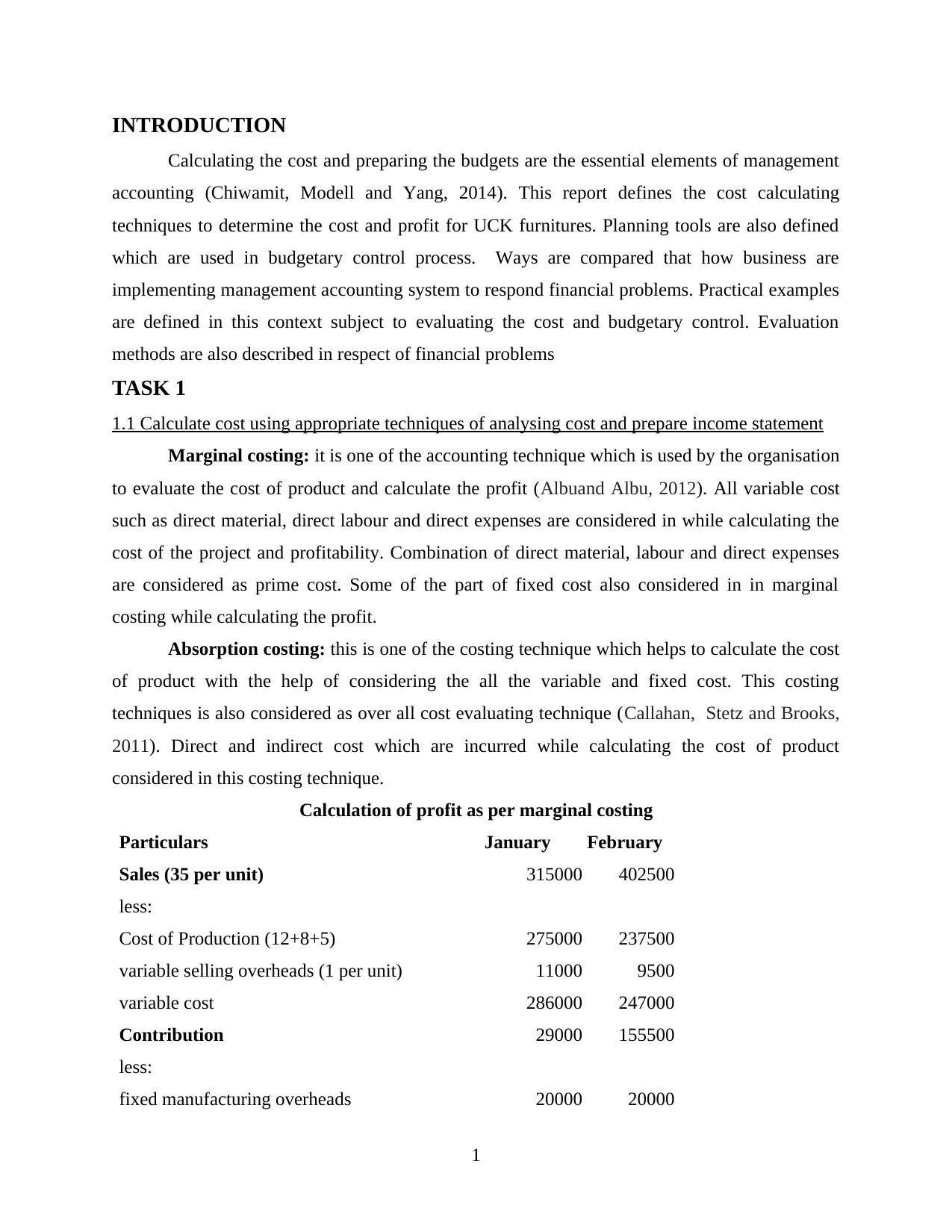

1.1 Calculate cost using appropriate techniques of analysing cost and prepare income statement

Marginal costing: it is one of the accounting technique which is used by the organisation

to evaluate the cost of product and calculate the profit (Albuand Albu, 2012). All variable cost

such as direct material, direct labour and direct expenses are considered in while calculating the

cost of the project and profitability. Combination of direct material, labour and direct expenses

are considered as prime cost. Some of the part of fixed cost also considered in in marginal

costing while calculating the profit.

Absorption costing: this is one of the costing technique which helps to calculate the cost

of product with the help of considering the all the variable and fixed cost. This costing

techniques is also considered as over all cost evaluating technique (Callahan, Stetz and Brooks,

2011). Direct and indirect cost which are incurred while calculating the cost of product

considered in this costing technique.

Calculation of profit as per marginal costing

Particulars January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

1

Calculating the cost and preparing the budgets are the essential elements of management

accounting (Chiwamit, Modell and Yang, 2014). This report defines the cost calculating

techniques to determine the cost and profit for UCK furnitures. Planning tools are also defined

which are used in budgetary control process. Ways are compared that how business are

implementing management accounting system to respond financial problems. Practical examples

are defined in this context subject to evaluating the cost and budgetary control. Evaluation

methods are also described in respect of financial problems

TASK 1

1.1 Calculate cost using appropriate techniques of analysing cost and prepare income statement

Marginal costing: it is one of the accounting technique which is used by the organisation

to evaluate the cost of product and calculate the profit (Albuand Albu, 2012). All variable cost

such as direct material, direct labour and direct expenses are considered in while calculating the

cost of the project and profitability. Combination of direct material, labour and direct expenses

are considered as prime cost. Some of the part of fixed cost also considered in in marginal

costing while calculating the profit.

Absorption costing: this is one of the costing technique which helps to calculate the cost

of product with the help of considering the all the variable and fixed cost. This costing

techniques is also considered as over all cost evaluating technique (Callahan, Stetz and Brooks,

2011). Direct and indirect cost which are incurred while calculating the cost of product

considered in this costing technique.

Calculation of profit as per marginal costing

Particulars January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

less:

fixed manufacturing overheads 20000 20000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

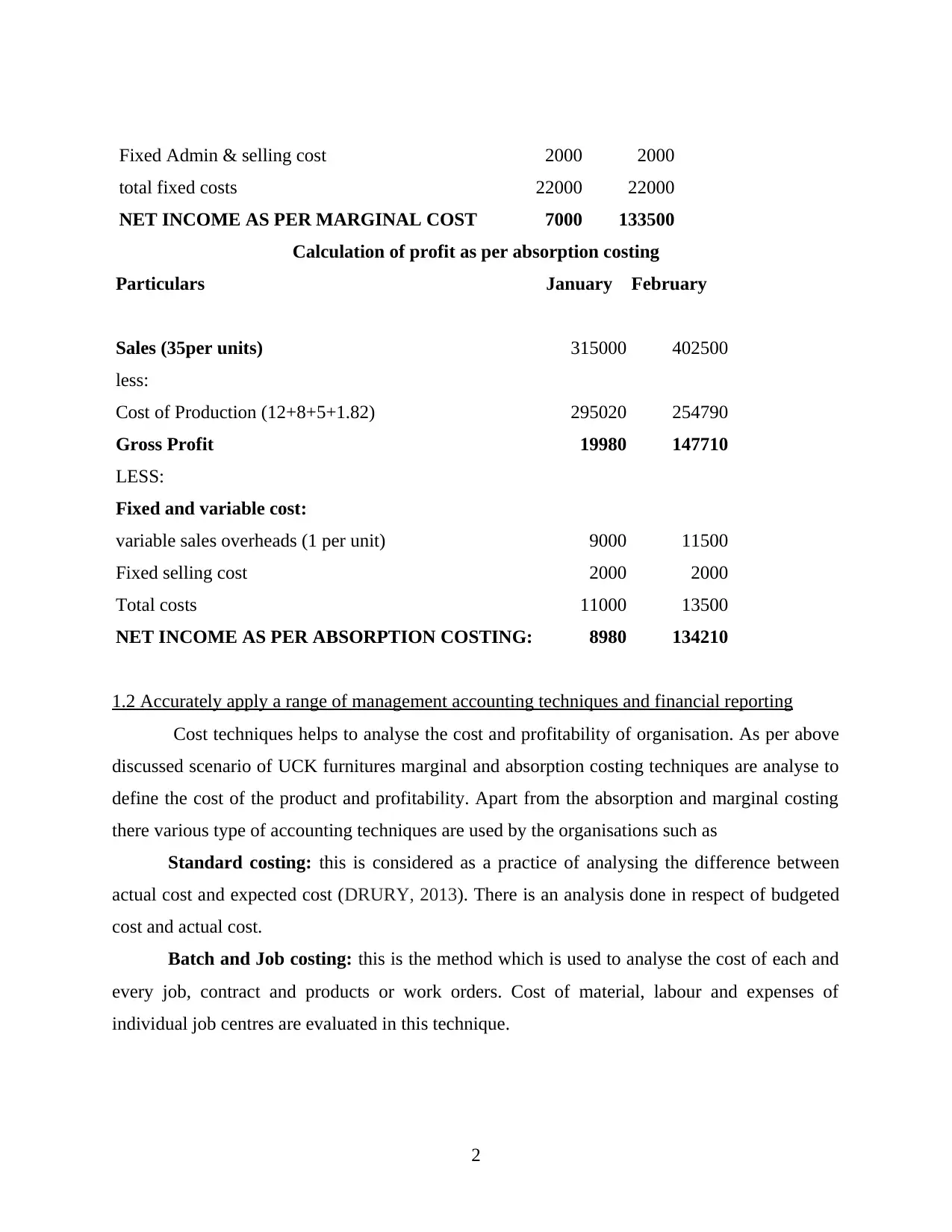

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

Calculation of profit as per absorption costing

Particulars January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

1.2 Accurately apply a range of management accounting techniques and financial reporting

Cost techniques helps to analyse the cost and profitability of organisation. As per above

discussed scenario of UCK furnitures marginal and absorption costing techniques are analyse to

define the cost of the product and profitability. Apart from the absorption and marginal costing

there various type of accounting techniques are used by the organisations such as

Standard costing: this is considered as a practice of analysing the difference between

actual cost and expected cost (DRURY, 2013). There is an analysis done in respect of budgeted

cost and actual cost.

Batch and Job costing: this is the method which is used to analyse the cost of each and

every job, contract and products or work orders. Cost of material, labour and expenses of

individual job centres are evaluated in this technique.

2

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

Calculation of profit as per absorption costing

Particulars January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

1.2 Accurately apply a range of management accounting techniques and financial reporting

Cost techniques helps to analyse the cost and profitability of organisation. As per above

discussed scenario of UCK furnitures marginal and absorption costing techniques are analyse to

define the cost of the product and profitability. Apart from the absorption and marginal costing

there various type of accounting techniques are used by the organisations such as

Standard costing: this is considered as a practice of analysing the difference between

actual cost and expected cost (DRURY, 2013). There is an analysis done in respect of budgeted

cost and actual cost.

Batch and Job costing: this is the method which is used to analyse the cost of each and

every job, contract and products or work orders. Cost of material, labour and expenses of

individual job centres are evaluated in this technique.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimising techniques: this is one of the method which helps to analyse the

behaviour of customer to respond various prices for products and services through various

channels.

1.3 Produce financial reports accurately apply and interpret data for a range of business activities

As per the above analysis there are some essential elements are evaluated. Financial

position is found in positive situation (Fourie and et. al., 2015). With the help of cost techniques

cost of the products evaluated such as marginal costing and absorption costing.

Pros of marginal costing: this costing technique is beneficial in order to determine the

cost of manufacturing products by considering all the variable aspects and cost.

Limitation: Fixed expenses and overheads remain avoided while calculating the

profitability of organisation.

Pros of absorption costing: this is also considered as overall cost measurement and cost

evaluating technique (Quinn, 2014). All the fixed aspects are covered in absorption costing

technique while calculating cost and profit of product.

Demerits: this technique is not considered effective as decision making perspective.

TASK 2

2.1 Advantages and disadvantages of various type of planning tools using in budgetary control

Budget: It is the process of preparing budget through identifying the cost incurred in past

project activities in order to support future business activities (Zaleha Abdul Rasid, Ruhana Isa

and Khairuzzaman Wan Ismail, 2014). The main objective of preparing budget is to ensure

employees to execute business activities well without fearing the shortage situation of funds

which directly encourage them to perform well.

Budgetary control: It is the process of controlling the wastage of funds through guiding

and directing the employees to utilise available funds in an optimum manner that will help in

bringing positive outcome to company (Budgetary control, 2017). It helps manager to find out

the deviation if any, through comparing actual performance with desired performance so that

they can implement corrective measures to eliminate such deviations without wasting time.

Objectives of Budgetary control:

There are many objectives of budgetary control which are as follows:

It helps in defining the aim or objectives of company clearly to the employees which

enables managers to formulate plans and policies to achieve same objectives.

3

behaviour of customer to respond various prices for products and services through various

channels.

1.3 Produce financial reports accurately apply and interpret data for a range of business activities

As per the above analysis there are some essential elements are evaluated. Financial

position is found in positive situation (Fourie and et. al., 2015). With the help of cost techniques

cost of the products evaluated such as marginal costing and absorption costing.

Pros of marginal costing: this costing technique is beneficial in order to determine the

cost of manufacturing products by considering all the variable aspects and cost.

Limitation: Fixed expenses and overheads remain avoided while calculating the

profitability of organisation.

Pros of absorption costing: this is also considered as overall cost measurement and cost

evaluating technique (Quinn, 2014). All the fixed aspects are covered in absorption costing

technique while calculating cost and profit of product.

Demerits: this technique is not considered effective as decision making perspective.

TASK 2

2.1 Advantages and disadvantages of various type of planning tools using in budgetary control

Budget: It is the process of preparing budget through identifying the cost incurred in past

project activities in order to support future business activities (Zaleha Abdul Rasid, Ruhana Isa

and Khairuzzaman Wan Ismail, 2014). The main objective of preparing budget is to ensure

employees to execute business activities well without fearing the shortage situation of funds

which directly encourage them to perform well.

Budgetary control: It is the process of controlling the wastage of funds through guiding

and directing the employees to utilise available funds in an optimum manner that will help in

bringing positive outcome to company (Budgetary control, 2017). It helps manager to find out

the deviation if any, through comparing actual performance with desired performance so that

they can implement corrective measures to eliminate such deviations without wasting time.

Objectives of Budgetary control:

There are many objectives of budgetary control which are as follows:

It helps in defining the aim or objectives of company clearly to the employees which

enables managers to formulate plans and policies to achieve same objectives.

3

It helps in making proper communication and coordination among different departments

in order to operate business activities in an effective manner.

It guides and directs employees to utilise resources in an optimum manner that will brings

profitable result to company (Nørreklit, 2014).

Through budgetary control, the manager can assign roles and responsibility to their

employees.

Budgetary control methods and its advantages and disadvantages:

There are various methods of budgetary control with the help of which the manager can

control and eliminate irrelevant cost incurred in business activities. Such methods includes:

Incremental Budgeting: It is the process of preparing budget through analysing previous

period budget which help them in identifying that how much extra amount required ion

executing future business activities (Melnyk and et. al., 2014). Its main objective is to spend

adequate resources with a hope of getting positive outcome but if results goes wrong then it will

make negative impact on the financial position of company.

Advantages:

It helps manager to operate their departments consistently in order to achive desired

objective within given time frame.

The chances of arising conflicts are minimum as the managers treats every department

equally. It is simple to operate and easy to understand.

Disadvantages:

It will not provide any incentive ton employees for generating new ideas and innovation

and reducing cost.

It allocate funds at maximum due to which if the result may gone wrong then it will badly

damage the financial position of company. The managers spends huge amount of budget which restricts them to focus on preparing

next year budget.

Zero Based Budgeting: It is the process of allocating funds after identifying and

analysing the programs rather than observing previous period budget which help them in

bringing more efficiency in result (Messner, 2016). The managers can adopt such budgetary

4

in order to operate business activities in an effective manner.

It guides and directs employees to utilise resources in an optimum manner that will brings

profitable result to company (Nørreklit, 2014).

Through budgetary control, the manager can assign roles and responsibility to their

employees.

Budgetary control methods and its advantages and disadvantages:

There are various methods of budgetary control with the help of which the manager can

control and eliminate irrelevant cost incurred in business activities. Such methods includes:

Incremental Budgeting: It is the process of preparing budget through analysing previous

period budget which help them in identifying that how much extra amount required ion

executing future business activities (Melnyk and et. al., 2014). Its main objective is to spend

adequate resources with a hope of getting positive outcome but if results goes wrong then it will

make negative impact on the financial position of company.

Advantages:

It helps manager to operate their departments consistently in order to achive desired

objective within given time frame.

The chances of arising conflicts are minimum as the managers treats every department

equally. It is simple to operate and easy to understand.

Disadvantages:

It will not provide any incentive ton employees for generating new ideas and innovation

and reducing cost.

It allocate funds at maximum due to which if the result may gone wrong then it will badly

damage the financial position of company. The managers spends huge amount of budget which restricts them to focus on preparing

next year budget.

Zero Based Budgeting: It is the process of allocating funds after identifying and

analysing the programs rather than observing previous period budget which help them in

bringing more efficiency in result (Messner, 2016). The managers can adopt such budgetary

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

control methods to nay type of cost such as capital expenditure, operating expenses, marketing

cost etc.

Advantages:

It ensures to get profitable result in future business activities.

It helps in improving efficiency level in operation activities through challenging

assumptions. It helps in reducing cost through avoiding automatic budget increases.

Disadvantages:

It consumes huge cost and time as budget is re-prepared from scratch annually.

Required specialised training to employees in order to accomplish goals.

Requires more resources hence the chances of miss-utilisation of resources is more. Activity Based Budgeting: It is a method through which the manager can fixed budget on

each activities in order to get maximum possible outcome to company (Schaltegger and

Burritt, 2017). Each activity are carefully analysed which help in identifying the

requirements needed to achieve desired outcome.

Advantages:

As planning related with revenue and expenses are formulates ta last level which help in

providing useful information regarding execution of project activities. It helps management to control over the budgeting process and align the budget with

overall company objectives.

Disadvantages:

It involves huge cost when compared with traditional budgeting.

It is based on assumption due to which the expected result may fial to ahcive due to

uncertainties.

It requires more resources in analysing budget variances as compared to other budgeting

techniques.

2.2 High low method to determine the expenses if the numbers for July and August is 650 and

750

Computation of variable cost per unit using calculated as high and low activity level:

Total cost= (Expenses of high activity- expenses of low activity)/(Highest activity hours spent -

lowest hours spent)

5

cost etc.

Advantages:

It ensures to get profitable result in future business activities.

It helps in improving efficiency level in operation activities through challenging

assumptions. It helps in reducing cost through avoiding automatic budget increases.

Disadvantages:

It consumes huge cost and time as budget is re-prepared from scratch annually.

Required specialised training to employees in order to accomplish goals.

Requires more resources hence the chances of miss-utilisation of resources is more. Activity Based Budgeting: It is a method through which the manager can fixed budget on

each activities in order to get maximum possible outcome to company (Schaltegger and

Burritt, 2017). Each activity are carefully analysed which help in identifying the

requirements needed to achieve desired outcome.

Advantages:

As planning related with revenue and expenses are formulates ta last level which help in

providing useful information regarding execution of project activities. It helps management to control over the budgeting process and align the budget with

overall company objectives.

Disadvantages:

It involves huge cost when compared with traditional budgeting.

It is based on assumption due to which the expected result may fial to ahcive due to

uncertainties.

It requires more resources in analysing budget variances as compared to other budgeting

techniques.

2.2 High low method to determine the expenses if the numbers for July and August is 650 and

750

Computation of variable cost per unit using calculated as high and low activity level:

Total cost= (Expenses of high activity- expenses of low activity)/(Highest activity hours spent -

lowest hours spent)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total expense per units = (9820-7410)/(795-505)=8.31

Total expenses for July:

650*8.31=5401.5

For August:

750*8.31= 6232.5

2.3 Purpose of budget and preparing cash budget

(3) Cash budget of UCK furnitures for the month of September

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Purchase -16800

Selling and administration expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash in the end of September

month 6848

TASK 3

3.1 Compare how organisations are adapting management accounting system to respond

financial problems

UCK furniture adapted management accounting technique to respond financial problems

such as preparing cash budget, income statement. With the help of management accounting

system there are some techniques used to evaluate the cost of product such as marginal and

absorption costing. With the help of budgetary control tools mangers and accountants become

eligible to make cash budget and income statement (Mistry, Sharma and Low, 2014). There are

some performance management tools are defined in this context subject to evaluating the

6

Total expenses for July:

650*8.31=5401.5

For August:

750*8.31= 6232.5

2.3 Purpose of budget and preparing cash budget

(3) Cash budget of UCK furnitures for the month of September

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Purchase -16800

Selling and administration expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash in the end of September

month 6848

TASK 3

3.1 Compare how organisations are adapting management accounting system to respond

financial problems

UCK furniture adapted management accounting technique to respond financial problems

such as preparing cash budget, income statement. With the help of management accounting

system there are some techniques used to evaluate the cost of product such as marginal and

absorption costing. With the help of budgetary control tools mangers and accountants become

eligible to make cash budget and income statement (Mistry, Sharma and Low, 2014). There are

some performance management tools are defined in this context subject to evaluating the

6

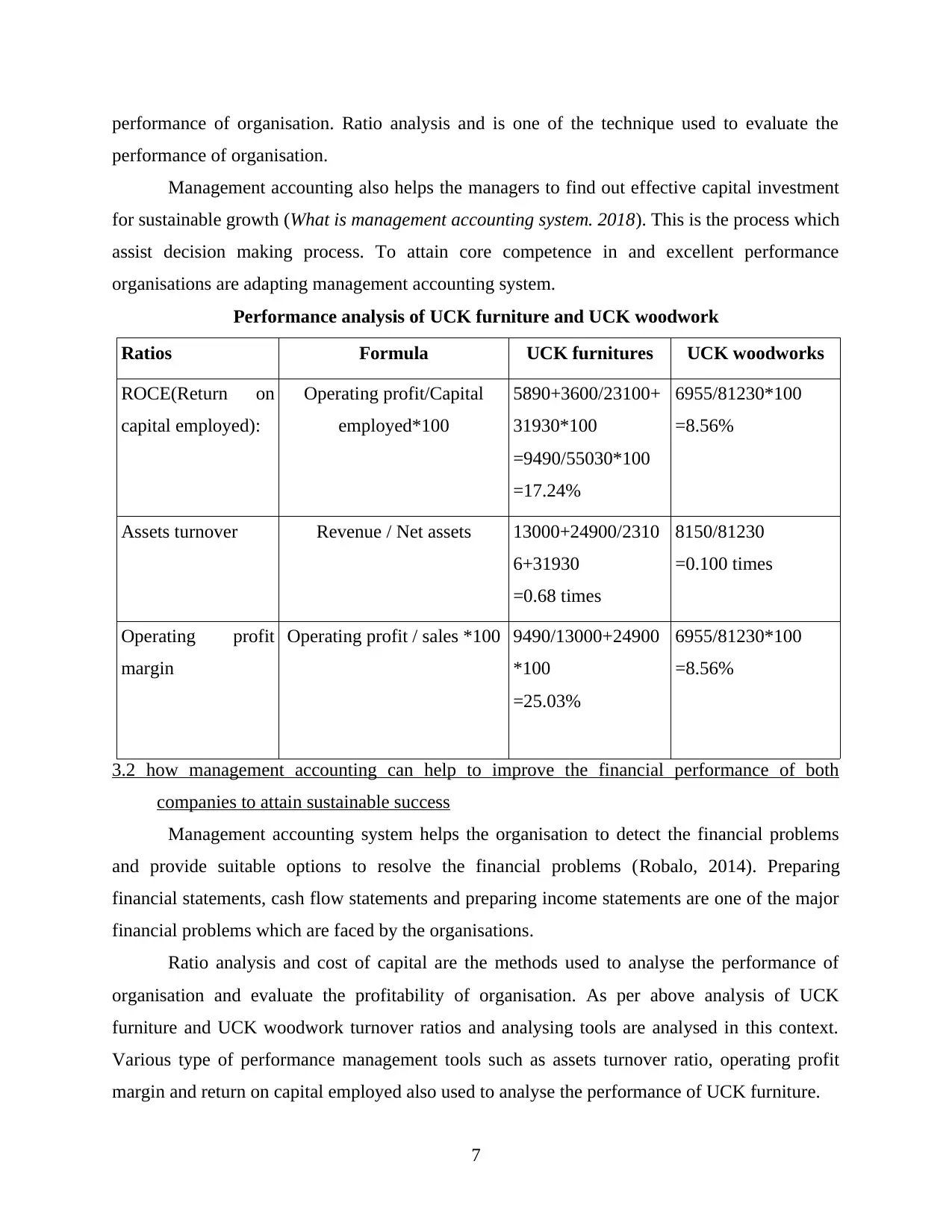

performance of organisation. Ratio analysis and is one of the technique used to evaluate the

performance of organisation.

Management accounting also helps the managers to find out effective capital investment

for sustainable growth (What is management accounting system. 2018). This is the process which

assist decision making process. To attain core competence in and excellent performance

organisations are adapting management accounting system.

Performance analysis of UCK furniture and UCK woodwork

Ratios Formula UCK furnitures UCK woodworks

ROCE(Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+

31930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/2310

6+31930

=0.68 times

8150/81230

=0.100 times

Operating profit

margin

Operating profit / sales *100 9490/13000+24900

*100

=25.03%

6955/81230*100

=8.56%

3.2 how management accounting can help to improve the financial performance of both

companies to attain sustainable success

Management accounting system helps the organisation to detect the financial problems

and provide suitable options to resolve the financial problems (Robalo, 2014). Preparing

financial statements, cash flow statements and preparing income statements are one of the major

financial problems which are faced by the organisations.

Ratio analysis and cost of capital are the methods used to analyse the performance of

organisation and evaluate the profitability of organisation. As per above analysis of UCK

furniture and UCK woodwork turnover ratios and analysing tools are analysed in this context.

Various type of performance management tools such as assets turnover ratio, operating profit

margin and return on capital employed also used to analyse the performance of UCK furniture.

7

performance of organisation.

Management accounting also helps the managers to find out effective capital investment

for sustainable growth (What is management accounting system. 2018). This is the process which

assist decision making process. To attain core competence in and excellent performance

organisations are adapting management accounting system.

Performance analysis of UCK furniture and UCK woodwork

Ratios Formula UCK furnitures UCK woodworks

ROCE(Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+

31930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/2310

6+31930

=0.68 times

8150/81230

=0.100 times

Operating profit

margin

Operating profit / sales *100 9490/13000+24900

*100

=25.03%

6955/81230*100

=8.56%

3.2 how management accounting can help to improve the financial performance of both

companies to attain sustainable success

Management accounting system helps the organisation to detect the financial problems

and provide suitable options to resolve the financial problems (Robalo, 2014). Preparing

financial statements, cash flow statements and preparing income statements are one of the major

financial problems which are faced by the organisations.

Ratio analysis and cost of capital are the methods used to analyse the performance of

organisation and evaluate the profitability of organisation. As per above analysis of UCK

furniture and UCK woodwork turnover ratios and analysing tools are analysed in this context.

Various type of performance management tools such as assets turnover ratio, operating profit

margin and return on capital employed also used to analyse the performance of UCK furniture.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.3 evaluate the planning tools used in management accounting to reduce the financial problems

Planning tools are used to interpret financial problems and sort out the complex business

situations (Renz and Herman, Eds., 2016). Various type of planning tools such as budgetary

control, project analysis and evaluation standard costing, analysation of cost variances and ratio

analysis are used to reduce financial risk and uncertainties.

CONCLUSION

This report is prepared to analyse the costing techniques to evaluate the cost and

profitability. Use of planning tools illustrated in this context which are used in budgetary control

process. Ways are compared in respect of adapting management accounting system with in the

organisation. Use of management accounting system to financial problems illustrated in this

context. Budgets are prepared to resolve the financial problems such as cash budget, and sales

budget. Performance of UCK Furnitures and UCK woodwork organisations evaluated with the

use of performance management tools.

8

Planning tools are used to interpret financial problems and sort out the complex business

situations (Renz and Herman, Eds., 2016). Various type of planning tools such as budgetary

control, project analysis and evaluation standard costing, analysation of cost variances and ratio

analysis are used to reduce financial risk and uncertainties.

CONCLUSION

This report is prepared to analyse the costing techniques to evaluate the cost and

profitability. Use of planning tools illustrated in this context which are used in budgetary control

process. Ways are compared in respect of adapting management accounting system with in the

organisation. Use of management accounting system to financial problems illustrated in this

context. Budgets are prepared to resolve the financial problems such as cash budget, and sales

budget. Performance of UCK Furnitures and UCK woodwork organisations evaluated with the

use of performance management tools.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.