Detailed Analysis of Management Accounting Report for Unilever PLC

VerifiedAdded on 2020/07/22

|19

|4789

|50

Report

AI Summary

This report examines the application of management accounting tools within Unilever PLC to enhance decision-making and improve operational efficiency. It covers various management accounting systems like cost accounting, inventory management, and job-costing, emphasizing their benefits. The report details management accounting reporting methods, including budget reports, job cost reports, and performance reports, and their role in cost control and performance evaluation. Furthermore, it provides calculations and comparisons of net profits under marginal and absorption costing, highlighting the implications of each method for financial outcomes. The analysis extends to the use of financial tools for evaluating financial problems and the role of management accounting in achieving sustainable development. The report concludes with a discussion of the benefits of management accounting systems within the context of Unilever PLC, emphasizing profitability, cost efficiency, and strategic decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types:.................................................................................1

M1 Benefits of management systems under the cited company context:...................................2

D1. How MA system and MA reporting integrates within the firm process:.............................2

P2. Various methods used for management accounting reporting:.............................................3

P3 Calculation of net profits under marginal and absorption costing:........................................4

M2 Application of techniques:....................................................................................................7

D2. Interpretation of data:...........................................................................................................8

TASK 3............................................................................................................................................8

Budget and its advantages and disadvantages.............................................................................8

Advantages: ..............................................................................................................................10

D3 How financial tools are used for evaluating financial problems:........................................11

TASK 4..........................................................................................................................................12

P5 How management accounting tools are used by the firm for responding financial problems:

...................................................................................................................................................12

M4 How management accounting can lead to attain sustainable development:.......................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types:.................................................................................1

M1 Benefits of management systems under the cited company context:...................................2

D1. How MA system and MA reporting integrates within the firm process:.............................2

P2. Various methods used for management accounting reporting:.............................................3

P3 Calculation of net profits under marginal and absorption costing:........................................4

M2 Application of techniques:....................................................................................................7

D2. Interpretation of data:...........................................................................................................8

TASK 3............................................................................................................................................8

Budget and its advantages and disadvantages.............................................................................8

Advantages: ..............................................................................................................................10

D3 How financial tools are used for evaluating financial problems:........................................11

TASK 4..........................................................................................................................................12

P5 How management accounting tools are used by the firm for responding financial problems:

...................................................................................................................................................12

M4 How management accounting can lead to attain sustainable development:.......................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the crucial tool which are used in order to make their business

decisions effective. These are the practices which are used by the management so that the they

could attain their pre-set objectives. Under this project research, Unilever plc having their

manufacturing units and it considers management accounting tools for lowering their products

costs. This will also provides sustainability so that their objectives can attain. Unilever plc needs

to make their business operations so effective so that competitive advantages can be attained by

lowering the costs of the product (Zimmerman and Yahya-Zadeh, 2011). Under this research

report, company will use various management accounting practices in their manufacturing

operations for lowering the product costs and with the help of this, company will take the

competitive advantages over the rivals. Under this research report, company will frame

management accounting reporting for making the decisions in an efficient manner. There are so

many business accounting tools which are used in order to get the business objectives effective.

TASK 1

P1. Management accounting and its types:

Management accounting is the procedure which is used in the firm for analysing firm

costs to make internal financial report, records and assist the managers to frame business

decisions effective and efficient in order to attain its pre set objectives. On the other way, this is

the act of framing sense of financial and costing data and converting those data and converting

that data into fruitful information for management and officers within the firm. There are various

management accounting systems which are used by the firms in order to make certain changes.

Cost accounting system: Under this system, management of the Unilever plc adopt cost

accounting system so that there pre-set objectives can be attained. This accounting system is

used by the firm in order to lower their operational expenses and also control them effectively.

This cost accounting is suitable for the manufacturing sector companies which main object are to

produce something in a effective price so that optimum profits can be gained (Ward, 2012). This

accounting system does not only considers various costs related matters but also make certain

assumptions on the basis of these resources. Which will be helpful for making business strategies

so effective.

1

Management accounting is the crucial tool which are used in order to make their business

decisions effective. These are the practices which are used by the management so that the they

could attain their pre-set objectives. Under this project research, Unilever plc having their

manufacturing units and it considers management accounting tools for lowering their products

costs. This will also provides sustainability so that their objectives can attain. Unilever plc needs

to make their business operations so effective so that competitive advantages can be attained by

lowering the costs of the product (Zimmerman and Yahya-Zadeh, 2011). Under this research

report, company will use various management accounting practices in their manufacturing

operations for lowering the product costs and with the help of this, company will take the

competitive advantages over the rivals. Under this research report, company will frame

management accounting reporting for making the decisions in an efficient manner. There are so

many business accounting tools which are used in order to get the business objectives effective.

TASK 1

P1. Management accounting and its types:

Management accounting is the procedure which is used in the firm for analysing firm

costs to make internal financial report, records and assist the managers to frame business

decisions effective and efficient in order to attain its pre set objectives. On the other way, this is

the act of framing sense of financial and costing data and converting those data and converting

that data into fruitful information for management and officers within the firm. There are various

management accounting systems which are used by the firms in order to make certain changes.

Cost accounting system: Under this system, management of the Unilever plc adopt cost

accounting system so that there pre-set objectives can be attained. This accounting system is

used by the firm in order to lower their operational expenses and also control them effectively.

This cost accounting is suitable for the manufacturing sector companies which main object are to

produce something in a effective price so that optimum profits can be gained (Ward, 2012). This

accounting system does not only considers various costs related matters but also make certain

assumptions on the basis of these resources. Which will be helpful for making business strategies

so effective.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system: This is used by the management in order to effectively

manage stocks of the firm. Stocks are the lifeline of any business as there is a need to manage

inventory so that the available resources can be used by the firm. The management accountant is

the main authority which uses resources in an effective manner so that maximum outcome can be

granted (van der Steen, 2011). This accounting system helps Unilever plc for managing

inventory in order to have their business operations effective. With the help of this,company is

able to track inventory levels, orders, sales and deliveries. This system is mostly used in

manufacturing sector to frame a work order, bills of materials and other manufacturing-related

documents.

Job-costing system: By applying this costing system, management is able to assign production

costs to each individual good or batches of products. Normally, this system is used by the firm at

the time when the goods produced are quite separate for each other. This assign overheads costs

to one or more cost pools. At the time of accounting period end, total amount in each cos pool is

assigned to different open jobs depends on few allocation methodology which is regularly apply.

This tools helps Unilever plc to assess the each job order costs so that they could fix prices for

them.

Price optimisation system: This is the implementation of mathematical assessment by a firm to

identify about the customers reaction at various prices for its goods and services via various

channels (Tappura and et. al., 2015). This is also implemented to identify the prices which the

cited firm will fix in order to attain its objectives like- optimising operating revenues.

M1 Benefits of management systems under the cited company context:

By implementing management accounting tools, Unilever plc is able to run effectively so

that its objectives can meet in a best manner. There are various tools which are used by the firm

in order to make their business objectives in an effective manner. Under this, it has been

identified that the business can run smoothly by applying management accounting practices.

Management accounting benefits are used to increase profitability, cost efficiency for making

product cheaper.

D1. How MA system and MA reporting integrates within the firm process:

Management accounting system helps the cited firm in order to make MA reporting in

order to make efficient decisions so that Unilever plc could attain pre-set objectives. This is the

definite process which is used by the firm for smooth running of the operations. But, only one of

2

manage stocks of the firm. Stocks are the lifeline of any business as there is a need to manage

inventory so that the available resources can be used by the firm. The management accountant is

the main authority which uses resources in an effective manner so that maximum outcome can be

granted (van der Steen, 2011). This accounting system helps Unilever plc for managing

inventory in order to have their business operations effective. With the help of this,company is

able to track inventory levels, orders, sales and deliveries. This system is mostly used in

manufacturing sector to frame a work order, bills of materials and other manufacturing-related

documents.

Job-costing system: By applying this costing system, management is able to assign production

costs to each individual good or batches of products. Normally, this system is used by the firm at

the time when the goods produced are quite separate for each other. This assign overheads costs

to one or more cost pools. At the time of accounting period end, total amount in each cos pool is

assigned to different open jobs depends on few allocation methodology which is regularly apply.

This tools helps Unilever plc to assess the each job order costs so that they could fix prices for

them.

Price optimisation system: This is the implementation of mathematical assessment by a firm to

identify about the customers reaction at various prices for its goods and services via various

channels (Tappura and et. al., 2015). This is also implemented to identify the prices which the

cited firm will fix in order to attain its objectives like- optimising operating revenues.

M1 Benefits of management systems under the cited company context:

By implementing management accounting tools, Unilever plc is able to run effectively so

that its objectives can meet in a best manner. There are various tools which are used by the firm

in order to make their business objectives in an effective manner. Under this, it has been

identified that the business can run smoothly by applying management accounting practices.

Management accounting benefits are used to increase profitability, cost efficiency for making

product cheaper.

D1. How MA system and MA reporting integrates within the firm process:

Management accounting system helps the cited firm in order to make MA reporting in

order to make efficient decisions so that Unilever plc could attain pre-set objectives. This is the

definite process which is used by the firm for smooth running of the operations. But, only one of

2

them can not attain firm's pre-set objectives. Hence, both management accounting system and

management accounting reporting are required to be integrated for attaining their pre-set

objectives.

P2. Various methods used for management accounting reporting:

There are various tools which are used by the firm in order for attaining firm's pre-set

objectives. This also has been seen that the management of the cited company will use these

reports so that they would able to control expenditures and reduce the cost of the productions so

that company would able to sustain in effective manner (Setthasakko, 2010). There are few

reports which are explained hereunder:

Budget report: This reports assist small firms owners to review their firm performance. But, in

that case of operations are big, in that case, managers review their division's performance and

and manage costs. The forecasted budget is usually depends on the actual costs from previous

years. With the help of this, actual figure is compared to the budged figure and then analyse it in

an effective manner. This also has been seen that the management of the Unilever company

needs to form budget reports so that they could control the costs or expenses and also compare

their actual results with the anticipated outcomes. If the variances occurred in a favourable

manner then it is presumed to be good. But if, variances occurred in an adverse manner, then the

authorised person will overcome these issues effectively.

Job cost reports: This reflects the expenses for a specific project. They are normally matched

with forecasting of revenue in order to firm can assess job profitability. Which assist in

determining greater earning areas of the firm so that company could concentrates its attempts

rather than of wasting time and monetary resources on jobs with less profit margins (Quinn,

2011). Job cost reports are implemented to review expenses at the time of project running

henceforth, the mangers are able to rectify areas of waste before the costs increase.

Accounting receivable report: Under this report, all the earnings arises or presumed to be arise

in near future, are recoded. Whole earnings is recorded under this report and at the end, make

report which can assist the firm to get the sustainable development.

Performance report: Under performance report, management accountant assess it's company's

performance by taking financial and non-financial data. With the help of this, firm is able to

make strategies in a great manner. With the help of this, various stakeholders uses these reports

so that they would able to get pre-set objectives.

3

management accounting reporting are required to be integrated for attaining their pre-set

objectives.

P2. Various methods used for management accounting reporting:

There are various tools which are used by the firm in order for attaining firm's pre-set

objectives. This also has been seen that the management of the cited company will use these

reports so that they would able to control expenditures and reduce the cost of the productions so

that company would able to sustain in effective manner (Setthasakko, 2010). There are few

reports which are explained hereunder:

Budget report: This reports assist small firms owners to review their firm performance. But, in

that case of operations are big, in that case, managers review their division's performance and

and manage costs. The forecasted budget is usually depends on the actual costs from previous

years. With the help of this, actual figure is compared to the budged figure and then analyse it in

an effective manner. This also has been seen that the management of the Unilever company

needs to form budget reports so that they could control the costs or expenses and also compare

their actual results with the anticipated outcomes. If the variances occurred in a favourable

manner then it is presumed to be good. But if, variances occurred in an adverse manner, then the

authorised person will overcome these issues effectively.

Job cost reports: This reflects the expenses for a specific project. They are normally matched

with forecasting of revenue in order to firm can assess job profitability. Which assist in

determining greater earning areas of the firm so that company could concentrates its attempts

rather than of wasting time and monetary resources on jobs with less profit margins (Quinn,

2011). Job cost reports are implemented to review expenses at the time of project running

henceforth, the mangers are able to rectify areas of waste before the costs increase.

Accounting receivable report: Under this report, all the earnings arises or presumed to be arise

in near future, are recoded. Whole earnings is recorded under this report and at the end, make

report which can assist the firm to get the sustainable development.

Performance report: Under performance report, management accountant assess it's company's

performance by taking financial and non-financial data. With the help of this, firm is able to

make strategies in a great manner. With the help of this, various stakeholders uses these reports

so that they would able to get pre-set objectives.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management report: This is the report which is made by the firm in order to track

the inventory level stocks and make them accordingly in order to make successful business

decisions. The company will form inventory management report in order to make their business

decision accordingly. The inventory management report helps the management to make their to

adopt effective inventory management plan so that these can be attained in an effective

management plan.

TASK 2

P3 Calculation of net profits under marginal and absorption costing:

Marginal costing: This is the costing method under which variable cost is considered. This cost

of production is the vary in the total cost arise from producing one extra item (Parker, 2012).

The aim of assessing marginal cost is to identify the point where a firm can attain economies of

scale. This is the extra cost incurred in the manufacturing of production of extra unit of a product

or services. This is most crucial in economic theory as a profits optimising firm company would

manufacture upto the marginal cost equal marginal revenue.

Absorption costing: Absorption cost is used in order to make costs. The costs which are

concerned to the manufacturing of goods, considered under absorption costing. Under this, all

costs whether these are variable or fixed, is considered. On the other words, absorption costing is

characterized as a tool for gathering the costs linked with the production process.

Here are net profits as per marginal and absorption costing are given hereunder:

Calculation as per Absorption costing.

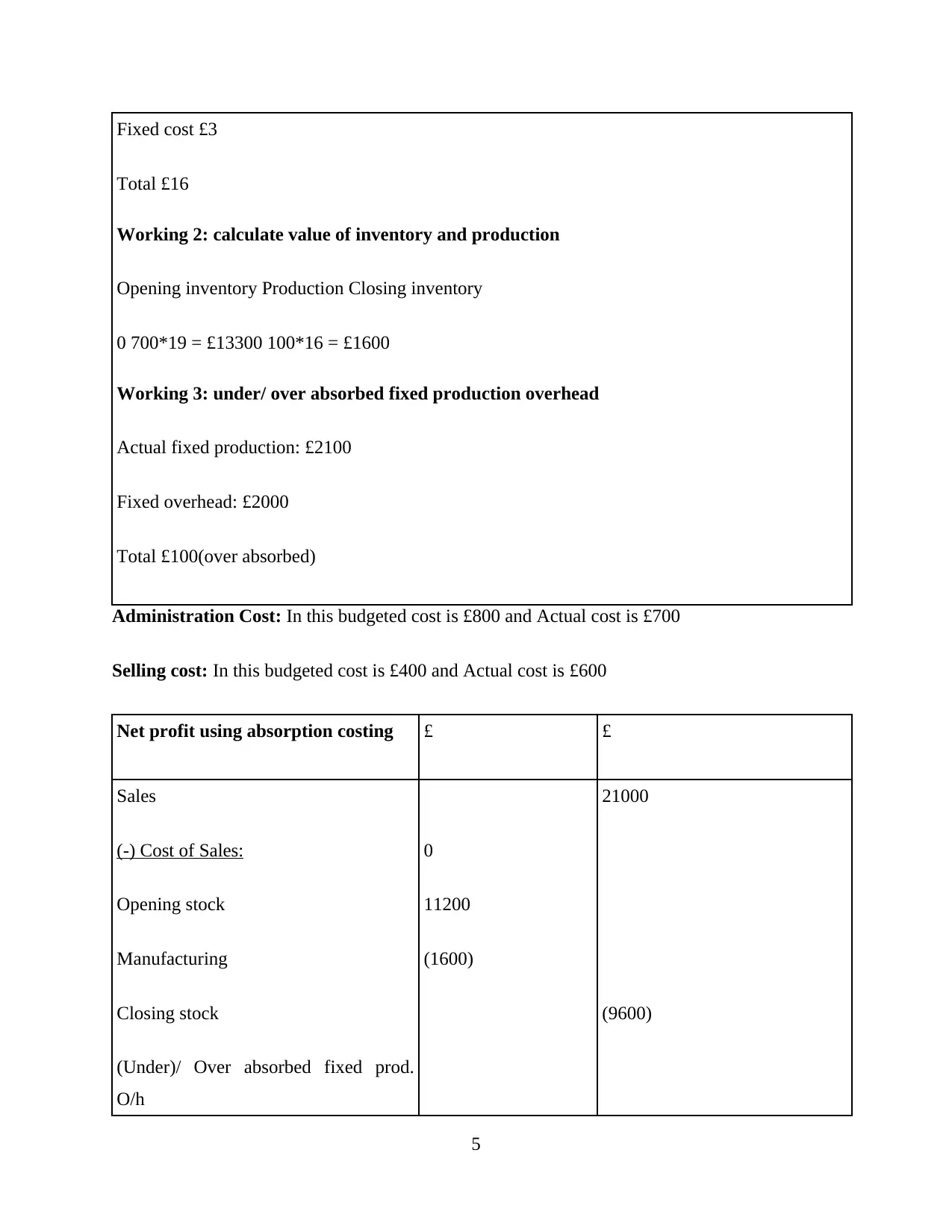

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

4

the inventory level stocks and make them accordingly in order to make successful business

decisions. The company will form inventory management report in order to make their business

decision accordingly. The inventory management report helps the management to make their to

adopt effective inventory management plan so that these can be attained in an effective

management plan.

TASK 2

P3 Calculation of net profits under marginal and absorption costing:

Marginal costing: This is the costing method under which variable cost is considered. This cost

of production is the vary in the total cost arise from producing one extra item (Parker, 2012).

The aim of assessing marginal cost is to identify the point where a firm can attain economies of

scale. This is the extra cost incurred in the manufacturing of production of extra unit of a product

or services. This is most crucial in economic theory as a profits optimising firm company would

manufacture upto the marginal cost equal marginal revenue.

Absorption costing: Absorption cost is used in order to make costs. The costs which are

concerned to the manufacturing of goods, considered under absorption costing. Under this, all

costs whether these are variable or fixed, is considered. On the other words, absorption costing is

characterized as a tool for gathering the costs linked with the production process.

Here are net profits as per marginal and absorption costing are given hereunder:

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

0

11200

(1600)

21000

(9600)

5

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this budgeted cost is £800 and Actual cost is £700

Selling cost: In this budgeted cost is £400 and Actual cost is £600

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

0

11200

(1600)

21000

(9600)

5

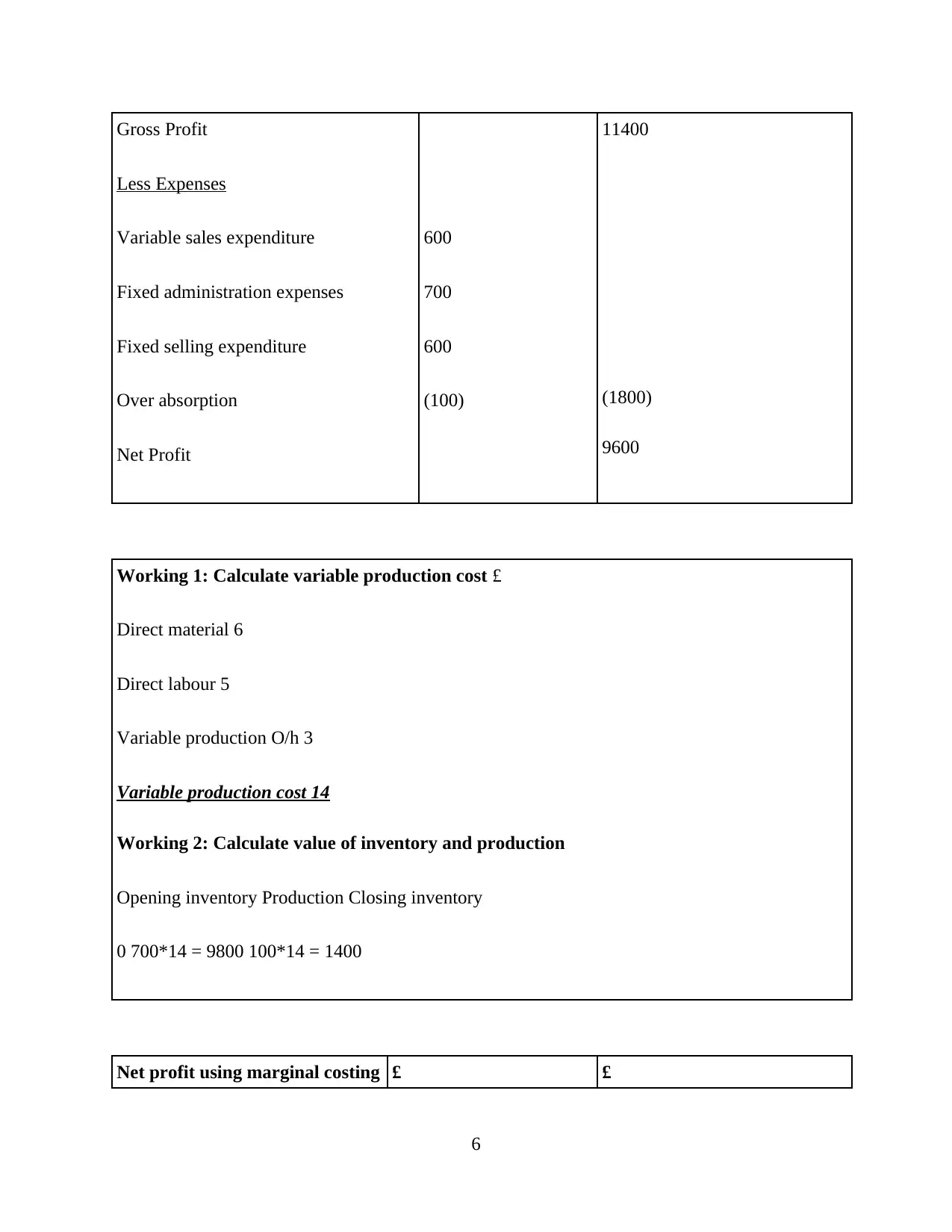

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

700

600

(100)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

6

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

600

700

600

(100)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

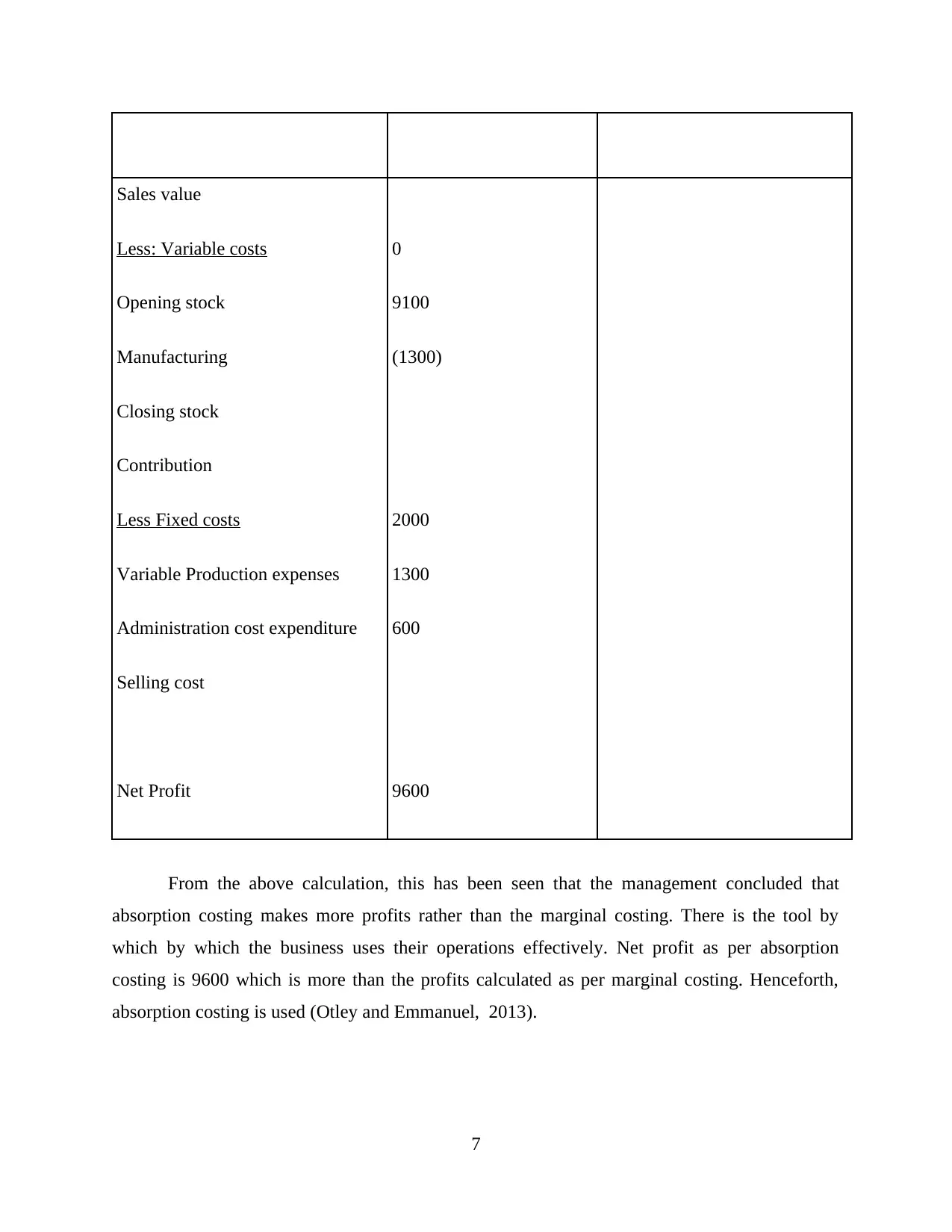

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

9600

From the above calculation, this has been seen that the management concluded that

absorption costing makes more profits rather than the marginal costing. There is the tool by

which by which the business uses their operations effectively. Net profit as per absorption

costing is 9600 which is more than the profits calculated as per marginal costing. Henceforth,

absorption costing is used (Otley and Emmanuel, 2013).

7

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

9600

From the above calculation, this has been seen that the management concluded that

absorption costing makes more profits rather than the marginal costing. There is the tool by

which by which the business uses their operations effectively. Net profit as per absorption

costing is 9600 which is more than the profits calculated as per marginal costing. Henceforth,

absorption costing is used (Otley and Emmanuel, 2013).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 Application of techniques:

In the cited question, Unilever plc is needed to implement management accounting tools in order

to get the maximum outcomes. Such also need to frame the running so smooth that carry the

operations in effective manner. Above mentioned tools are used by the firm fo getting

sustainable development.

D2. Interpretation of data:

The profits attained accordingly marginal costing and absorption costing reflects various

value. This basically assists the firm for making the business sustainable (Malmi, 2010). As per

the absorption costing, firm earn 9600 profits. On the other hand, as per the marginal costing,

company earns 9300.

TASK 3

Budget and its advantages and disadvantages

Budget is the report or statement made on the basis past financial data for a set of period.

Budget is a tool which is used by the firm in order to make thier business effectively. This is the

report which is used in order to make decisions effectively. A budget assists the manager to

make plans in an effective manner (Macintosh and Quattrone, 2010). There are is a need to make

planning, priortizinring, regular enhancement, forecasting so that there business can run

effectively. The budget process is the main thing which helps the firm to make their business

plans accordingly, and on the basis of that business, manager would able to achieve its pre-set

targets. However, the budgeted results is compared with the actual outcome so that they would to

analyse them and find out the variables effectively. The manager of the Unilever plc would

makes efforts for eliminating that variances in a proper manner. There are so many budgets

which helps the overall firms for assisting the firm to get pre-set objectives. Some of them are

opertaing budget, sales budget, cash budget and so on.

Operating budget: This is the budget which is used by the firm for attaining firm's pre-set

targets. All the expenses which are related to the operations, need to consider. The outcome

which is extracted by using operating budget needs to be considered by the firm for analysing the

actual budget and then frame policies in order to eliminate these variances.

Advantages:

8

In the cited question, Unilever plc is needed to implement management accounting tools in order

to get the maximum outcomes. Such also need to frame the running so smooth that carry the

operations in effective manner. Above mentioned tools are used by the firm fo getting

sustainable development.

D2. Interpretation of data:

The profits attained accordingly marginal costing and absorption costing reflects various

value. This basically assists the firm for making the business sustainable (Malmi, 2010). As per

the absorption costing, firm earn 9600 profits. On the other hand, as per the marginal costing,

company earns 9300.

TASK 3

Budget and its advantages and disadvantages

Budget is the report or statement made on the basis past financial data for a set of period.

Budget is a tool which is used by the firm in order to make thier business effectively. This is the

report which is used in order to make decisions effectively. A budget assists the manager to

make plans in an effective manner (Macintosh and Quattrone, 2010). There are is a need to make

planning, priortizinring, regular enhancement, forecasting so that there business can run

effectively. The budget process is the main thing which helps the firm to make their business

plans accordingly, and on the basis of that business, manager would able to achieve its pre-set

targets. However, the budgeted results is compared with the actual outcome so that they would to

analyse them and find out the variables effectively. The manager of the Unilever plc would

makes efforts for eliminating that variances in a proper manner. There are so many budgets

which helps the overall firms for assisting the firm to get pre-set objectives. Some of them are

opertaing budget, sales budget, cash budget and so on.

Operating budget: This is the budget which is used by the firm for attaining firm's pre-set

targets. All the expenses which are related to the operations, need to consider. The outcome

which is extracted by using operating budget needs to be considered by the firm for analysing the

actual budget and then frame policies in order to eliminate these variances.

Advantages:

8

By applying budgetary tools, firm would able to attain their operations related objectives

in an effective way.

Operating budget helps the managers to control operating related expenses effectively so

that operational profits could enhanced. This is the main task which are useful for making

their business sustainable.

This also stimulates coordination and communication.

Disadvantages:

Operating budget does not easily to reconcile personal/individual and corporate goals.

This is not always to produce reliable outcomes in an order to get the reliable outcomes.

Managers might overestimate costs which is not able to produce outcome business

outcome effectively (Lukka and Modell, 2010).

Sales budget: Sales budget is the main budget which is used in order to predict the sales figure

and the basis of that figure, company would able to make certain strategies for attianing its pre-

set objectives. Sales budget are required to make their business plans effective and in this

manner, the company makes certain tools that will be done in an effective manner. However,

company needs to make thier business operations so effective. There are so many tools which is

used in the make their sales budget in an effective manner.

Advantages:

Sales budget is helpful for estimating sales outcome and then react in order to attain

firm's objectives.

Sales budget also assist the firm to control the sales related expenses in an effective

manner so that the sales price can be lowered and also make certain changes in the cost

price.

It also enhance the allocation of available resources.

Disadvantages:

Budget could be oversight as pressure instrument improvement which is imposed by the

management, hence, wrongful strategies would be made after analysing sales budget.

Sales budget also extract the policy for considering better spendings or ignoring

opportunity. Hence, this will create difficulty (Hutaibat, 2012).

9

in an effective way.

Operating budget helps the managers to control operating related expenses effectively so

that operational profits could enhanced. This is the main task which are useful for making

their business sustainable.

This also stimulates coordination and communication.

Disadvantages:

Operating budget does not easily to reconcile personal/individual and corporate goals.

This is not always to produce reliable outcomes in an order to get the reliable outcomes.

Managers might overestimate costs which is not able to produce outcome business

outcome effectively (Lukka and Modell, 2010).

Sales budget: Sales budget is the main budget which is used in order to predict the sales figure

and the basis of that figure, company would able to make certain strategies for attianing its pre-

set objectives. Sales budget are required to make their business plans effective and in this

manner, the company makes certain tools that will be done in an effective manner. However,

company needs to make thier business operations so effective. There are so many tools which is

used in the make their sales budget in an effective manner.

Advantages:

Sales budget is helpful for estimating sales outcome and then react in order to attain

firm's objectives.

Sales budget also assist the firm to control the sales related expenses in an effective

manner so that the sales price can be lowered and also make certain changes in the cost

price.

It also enhance the allocation of available resources.

Disadvantages:

Budget could be oversight as pressure instrument improvement which is imposed by the

management, hence, wrongful strategies would be made after analysing sales budget.

Sales budget also extract the policy for considering better spendings or ignoring

opportunity. Hence, this will create difficulty (Hutaibat, 2012).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.