Analysis of Management Accounting Systems and Reporting at Unilever

VerifiedAdded on 2021/02/21

|20

|5636

|142

Report

AI Summary

This report delves into the realm of management accounting, examining its essential requirements, diverse reporting methods, and its crucial integration within organizational processes, with a specific focus on the case of Unilever. The report explores various management accounting systems, including inventory management, price optimization, job costing, and cost accounting, highlighting their applications and benefits within Unilever's operations. It further investigates different management accounting reporting techniques such as variance analysis, budgeting, performance reports, activity-based costing, and standard costing, emphasizing their roles in performance evaluation and strategic decision-making. The report also addresses how management accounting systems are integrated within organizational processes, with data flowing from various processes to support effective management accounting and reporting. The benefits of implementing these systems, such as improved inventory management and cost optimization, are discussed in the context of Unilever. The report concludes by providing a thorough analysis of how Unilever adapts its management accounting systems to address financial challenges, demonstrating the critical role of management accounting in driving organizational success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Essential requirements of different types of management accounting systems...........................1

Different techniques and methods used for management accounting reporting..........................3

Management accounting system and management accounting reporting is integrated within

organisational processes...............................................................................................................5

Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs:...........................................................................................7

ACTIVITY 2....................................................................................................................................8

Use of planning tools used in management accounting...............................................................8

Uses of different planing tools in forecasting budget................................................................10

Comparison of how organisations are adapting management accounting systems to respond to

financial problems......................................................................................................................11

CONCLUSION..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Essential requirements of different types of management accounting systems...........................1

Different techniques and methods used for management accounting reporting..........................3

Management accounting system and management accounting reporting is integrated within

organisational processes...............................................................................................................5

Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs:...........................................................................................7

ACTIVITY 2....................................................................................................................................8

Use of planning tools used in management accounting...............................................................8

Uses of different planing tools in forecasting budget................................................................10

Comparison of how organisations are adapting management accounting systems to respond to

financial problems......................................................................................................................11

CONCLUSION..............................................................................................................................14

INTRODUCTION

Management accounting implies to utilisation of professional knowledge, expertise skills,

methods and theories in presenting accounting or financial information in systematic manner

which assist managerial personnel of business organisation in framing policies and plans,

controlling various operations or functions of organisation, activities related to decision making,

proper utilisation of organisation's resources, safeguarding financial assets and reporting to top

management (Aksoylu and Aykan, 2013). This report demonstrates an understanding of

management accounting systems, different methods used for management accounting reporting,

benefits of management accounting systems and their application within an organisational

context, advantages and disadvantages of different types of planning tools used for budgetary

control, use of different planning tools and their application for preparing and forecasting

budgets and Compare how organisations are adapting management accounting systems to

respond to financial problems in the context of Unilever, a British-Dutch transnational retail and

consumer goods company. Company is engaged in selling various consumer products like food

and beverages, beauty products, home care products and personal care products. This report also

contains calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs, how management accounting systems and

management accounting reporting is integrated within organisational processes and analysis

about way to respond to various financial problems, management accounting can lead

organisations to sustainable success.

ACTIVITY 1

Essential requirements of different types of management accounting systems.

Management accounting simply refers to a systematic process of presentation and

redefining financial and accounting information or data in way that it help in evaluating and

analysing performance of managerial personnels, formulating plan and strategies, systematic

comparison, forecasting, budgeting etc. Financial data and outcomes generated from

management accounting system provide assistance in developing internal rules or policies and

operating day to day to activities or functions. Management accounting system is future oriented

approach which provide a framework for planning and decision-making. Under management

accounting system qualitative information regarding performance of managerial personnels and

1

Management accounting implies to utilisation of professional knowledge, expertise skills,

methods and theories in presenting accounting or financial information in systematic manner

which assist managerial personnel of business organisation in framing policies and plans,

controlling various operations or functions of organisation, activities related to decision making,

proper utilisation of organisation's resources, safeguarding financial assets and reporting to top

management (Aksoylu and Aykan, 2013). This report demonstrates an understanding of

management accounting systems, different methods used for management accounting reporting,

benefits of management accounting systems and their application within an organisational

context, advantages and disadvantages of different types of planning tools used for budgetary

control, use of different planning tools and their application for preparing and forecasting

budgets and Compare how organisations are adapting management accounting systems to

respond to financial problems in the context of Unilever, a British-Dutch transnational retail and

consumer goods company. Company is engaged in selling various consumer products like food

and beverages, beauty products, home care products and personal care products. This report also

contains calculation of costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs, how management accounting systems and

management accounting reporting is integrated within organisational processes and analysis

about way to respond to various financial problems, management accounting can lead

organisations to sustainable success.

ACTIVITY 1

Essential requirements of different types of management accounting systems.

Management accounting simply refers to a systematic process of presentation and

redefining financial and accounting information or data in way that it help in evaluating and

analysing performance of managerial personnels, formulating plan and strategies, systematic

comparison, forecasting, budgeting etc. Financial data and outcomes generated from

management accounting system provide assistance in developing internal rules or policies and

operating day to day to activities or functions. Management accounting system is future oriented

approach which provide a framework for planning and decision-making. Under management

accounting system qualitative information regarding performance of managerial personnels and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other staff is also considered on priority basis. Management accounting system is not required as

per statute. It is done as per specific and particular problem of business organisation on weekly,

monthly, quarterly or yearly basis. Also there is no specific format for presentation of

information obtained form management accounting system but information is required to be

presented in format which is easily understandable. Various kind of management accounting

systems are adopted by management for different – different purpose. But overall focus of these

different methods is to evaluate or analyse financial performance and to achieve organisational

objectives or goals. Following are some major management accounting system used by Unilever,

as follows:

Inventory management system: This is most popular and widely used management

accounting system which assist management in effective inventory management. This system of

management accounting provider support to whole production and supply chain in order to

maximise profit by optimising various inventory cost (Boiral, 2016). By applying inventory

system managerial personnel in a business organisation can note down each and every factor or

aspect concerned with inventory like raw material, work in progress, finished goods etc. and

ensure availability of inventory in production process. In Unilever, company is engaged in

selling various retail products and having wide variety of product. So in company, management

uses inventory management system to monitor, maintain and manage its various inventory leads

to reduction in inventory storage cost and other related expenses. Due to which company is

ultimately able to enhance their profits in long run.

Price optimisation system: This in an significant system of management accounting

which is used by business organisations to set or determine price of its various products

according to the latest responses and variation in demands of consumers. This system is also

assist organisation to analyse and set best optimised price products that provide assistance in

capturing production expense or cost and enhance overall profit to achieve predetermine

objective. So price optimisation system is imperative aspect of pricing decisions to ensure

profitability. Unilever is known for selling products at lower price as compare to its competitors,

it is possible for company only due to effective price optimisation system. In company managers

by analysing various trends and sceneries determine the optimum prices of products which help

is providing products at lower prices to gain competitive advantages.

2

per statute. It is done as per specific and particular problem of business organisation on weekly,

monthly, quarterly or yearly basis. Also there is no specific format for presentation of

information obtained form management accounting system but information is required to be

presented in format which is easily understandable. Various kind of management accounting

systems are adopted by management for different – different purpose. But overall focus of these

different methods is to evaluate or analyse financial performance and to achieve organisational

objectives or goals. Following are some major management accounting system used by Unilever,

as follows:

Inventory management system: This is most popular and widely used management

accounting system which assist management in effective inventory management. This system of

management accounting provider support to whole production and supply chain in order to

maximise profit by optimising various inventory cost (Boiral, 2016). By applying inventory

system managerial personnel in a business organisation can note down each and every factor or

aspect concerned with inventory like raw material, work in progress, finished goods etc. and

ensure availability of inventory in production process. In Unilever, company is engaged in

selling various retail products and having wide variety of product. So in company, management

uses inventory management system to monitor, maintain and manage its various inventory leads

to reduction in inventory storage cost and other related expenses. Due to which company is

ultimately able to enhance their profits in long run.

Price optimisation system: This in an significant system of management accounting

which is used by business organisations to set or determine price of its various products

according to the latest responses and variation in demands of consumers. This system is also

assist organisation to analyse and set best optimised price products that provide assistance in

capturing production expense or cost and enhance overall profit to achieve predetermine

objective. So price optimisation system is imperative aspect of pricing decisions to ensure

profitability. Unilever is known for selling products at lower price as compare to its competitors,

it is possible for company only due to effective price optimisation system. In company managers

by analysing various trends and sceneries determine the optimum prices of products which help

is providing products at lower prices to gain competitive advantages.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: This kind of management accounting system is applied by business

organisation in respect of process related to predicting or forecasting useful and relevant

information concerned with cost of particular job or task within a business organisation. This

system is generally used production manager or cost accountants to identify band allocated

reaggregate cost of producing to a particular jobs or task irrespective of their nature. The job

costing system simply emphasises on cost or expanses incurred for or related with each and

every job and assign them to such job. In Unilever this system is adopted at lower level where it

is difficult to classify miscellaneous costs as per their nature then cost are classified by

accountant as per job costing system to reduce complexity in analysis of performance of various

operations or activities. Following are the some major information that is necessary for

implementation of job costing system, as follows:

Direct martial: This system required to track and monitor cost of direct material which

help to classify value of raw material related with a particular job or task. In Unilever, managers

by using information recorded by accountants, classifies and assign them to particular task.

Direct Labour: In Unilever management asses the cost of workers or employees engaged

in accomplishment of particular task to perform job costing system.

Cost accounting system: This system is used by management to assess and evaluate

detailed cost of each kind of product at every level of production and selling. This system help to

identify any variation in cost which help to optimise overall cost in order to achieve overall

objectives of organisation and probability (Bromiley and et.al, 2015). In Unilever cost

accounting system is used for detailed assessment of cost of food and beverages, cleaning agents

etc. which assist management to take significant business decisions.

Different techniques and methods used for management accounting reporting.

In big organisations like Unilever in order to keep a systematic record financial

transactions and events in proper way various reporting methods and reports are essential.

Manager and accountants are responsible preparation of different reports as per requirement.

These reports are ultimately used by top management to analyse and evaluate the overall

performance of business organisation. These reports are also used by management to prepare

strategies and action plans. These reports are also used by internal managers to implement

predetermined strategies to ensure accomplishment of goals effectively. In Unilever reporting is

done by manages to form a effective and appropriate strategy which assist organisation to gain

3

organisation in respect of process related to predicting or forecasting useful and relevant

information concerned with cost of particular job or task within a business organisation. This

system is generally used production manager or cost accountants to identify band allocated

reaggregate cost of producing to a particular jobs or task irrespective of their nature. The job

costing system simply emphasises on cost or expanses incurred for or related with each and

every job and assign them to such job. In Unilever this system is adopted at lower level where it

is difficult to classify miscellaneous costs as per their nature then cost are classified by

accountant as per job costing system to reduce complexity in analysis of performance of various

operations or activities. Following are the some major information that is necessary for

implementation of job costing system, as follows:

Direct martial: This system required to track and monitor cost of direct material which

help to classify value of raw material related with a particular job or task. In Unilever, managers

by using information recorded by accountants, classifies and assign them to particular task.

Direct Labour: In Unilever management asses the cost of workers or employees engaged

in accomplishment of particular task to perform job costing system.

Cost accounting system: This system is used by management to assess and evaluate

detailed cost of each kind of product at every level of production and selling. This system help to

identify any variation in cost which help to optimise overall cost in order to achieve overall

objectives of organisation and probability (Bromiley and et.al, 2015). In Unilever cost

accounting system is used for detailed assessment of cost of food and beverages, cleaning agents

etc. which assist management to take significant business decisions.

Different techniques and methods used for management accounting reporting.

In big organisations like Unilever in order to keep a systematic record financial

transactions and events in proper way various reporting methods and reports are essential.

Manager and accountants are responsible preparation of different reports as per requirement.

These reports are ultimately used by top management to analyse and evaluate the overall

performance of business organisation. These reports are also used by management to prepare

strategies and action plans. These reports are also used by internal managers to implement

predetermined strategies to ensure accomplishment of goals effectively. In Unilever reporting is

done by manages to form a effective and appropriate strategy which assist organisation to gain

3

competitive advantages. Following are some significant methods and techniques used by

company for management accounting reporting, as follows:

Variance analysis: It is a kind of management accounting reporting system under which

variance are calculated to track any particular weakness related to different processes. Here

variance refers to gap between actual and budgeted or standard amount. A variance may be

favourable or unfavourable. An unfavourable variance in any cost or expense points out towards

area of weakness. Under this reporting methods a detailed analysis of variances are presented to

asses the performance and efficiency (Malinić and Todorović, 2012). This analysis is done

though computing variance of factors such as labour cost, material cost, manufacturing overhead

cost and other production related cost. In Unilever, variance analysis is done by various

departments which help company to identify and resolve any problem at early stage. In company,

management prepare or modifies strategies by using outputs of variance analysis.

Budgeting: This is most popular and widely accepted technique of management

accounting reporting under which income and expense of business organisation is forecasting as

per past performance and trends to prepare a projection report to asses the performance of

organisation in near future. Budgets are prepared by managerial personnels as per organisation's

requirements like sales budgets, purchase budget etc. In Unilever this technique is used by

management to forecast organisation's performance in near future. Different budgets are analysed

by company's management to evaluate whether implemented strategy require any modification.

Performance Report: This reporting technique is used to analyse the overall

performance of an organisation as a whole and as well as for each employee during a particular

period. Department wise performance reports are prepared in big organisation like Unilever.

Managers by using these reports prepare a framework for strategic decisions making. In

Unilever, employees and workers are generally awarded for their obligations to company and

also under performers are identified. Performance-related managerial accounting reports also

help to deeply monitor the working of a company.

Activity based costing (ABC): Under activity based costing, management identifies and

allocate various cost or expenses to overhead functions and then allocate them to different costs.

This system of reporting identifies relationship between various overheads, costs, functions and

products, Through such relationship its allocated indirect costs to product less promptly than

other traditional methods. Some costs and expenses are complex to allocate through this

4

company for management accounting reporting, as follows:

Variance analysis: It is a kind of management accounting reporting system under which

variance are calculated to track any particular weakness related to different processes. Here

variance refers to gap between actual and budgeted or standard amount. A variance may be

favourable or unfavourable. An unfavourable variance in any cost or expense points out towards

area of weakness. Under this reporting methods a detailed analysis of variances are presented to

asses the performance and efficiency (Malinić and Todorović, 2012). This analysis is done

though computing variance of factors such as labour cost, material cost, manufacturing overhead

cost and other production related cost. In Unilever, variance analysis is done by various

departments which help company to identify and resolve any problem at early stage. In company,

management prepare or modifies strategies by using outputs of variance analysis.

Budgeting: This is most popular and widely accepted technique of management

accounting reporting under which income and expense of business organisation is forecasting as

per past performance and trends to prepare a projection report to asses the performance of

organisation in near future. Budgets are prepared by managerial personnels as per organisation's

requirements like sales budgets, purchase budget etc. In Unilever this technique is used by

management to forecast organisation's performance in near future. Different budgets are analysed

by company's management to evaluate whether implemented strategy require any modification.

Performance Report: This reporting technique is used to analyse the overall

performance of an organisation as a whole and as well as for each employee during a particular

period. Department wise performance reports are prepared in big organisation like Unilever.

Managers by using these reports prepare a framework for strategic decisions making. In

Unilever, employees and workers are generally awarded for their obligations to company and

also under performers are identified. Performance-related managerial accounting reports also

help to deeply monitor the working of a company.

Activity based costing (ABC): Under activity based costing, management identifies and

allocate various cost or expenses to overhead functions and then allocate them to different costs.

This system of reporting identifies relationship between various overheads, costs, functions and

products, Through such relationship its allocated indirect costs to product less promptly than

other traditional methods. Some costs and expenses are complex to allocate through this

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

technique. Indirect cost like staff salaries, management costs are some time tuff to allocate to a

particular product. This method is mostly used in manufacturing industry as its increases the

reliability of data. In Unilever this reporting method is not used at wide level but for some

activities like food and beverages processing this technique is used to determine the performance

of organisation.

Standard costing: Standard costing is method of reporting under which business

organisation determines an estimates expense or cost as against actual cost incurred during a

particular period of time. Later, manager make comparison of actual and standard cost to asses

the performance or efficiency. Such estimated or standard cost is fixed by managerial personnels

based on their skill, industry trends, previous performance etc. In Unilever management

generally use industry trends or competitors data to set standard cost. Managers by comparing

standard cost with actual cost evaluates the overall performance of company.

Management accounting system and management accounting reporting is integrated within

organisational processes

In present business scenarios every organisation emphasises on management accounting

system and reporting for which different processes are implemented by organisation in order to

integrate management accounting system and reporting within organisational processes. Data

and information used in management accounting and reporting is obtained though the outputs of

various other organisational processes, such as accounting process provide a basic information

and data for management accounting system and reporting (McLean, McGovern and Davie,

2015). In Unilever management is aware about the importance of management accounting

system so the implement process which directly provides support to management in order to

implement management accounting system and reporting. In Unilever, managers of different

department and store are generated in managing data to provide relevant information for

management accounting and reporting. In company inventory and stock is marinated through

various processes which ultimately assist in effective inventory management.

Benefits of management accounting systems:

Different type of management accounting system is used by management to implement

an overall effective management accounting system and to solve different problems. Following

are some key benefits of management accounting system, in the context of Unilever, as follows:

Different accounting Benefits

5

particular product. This method is mostly used in manufacturing industry as its increases the

reliability of data. In Unilever this reporting method is not used at wide level but for some

activities like food and beverages processing this technique is used to determine the performance

of organisation.

Standard costing: Standard costing is method of reporting under which business

organisation determines an estimates expense or cost as against actual cost incurred during a

particular period of time. Later, manager make comparison of actual and standard cost to asses

the performance or efficiency. Such estimated or standard cost is fixed by managerial personnels

based on their skill, industry trends, previous performance etc. In Unilever management

generally use industry trends or competitors data to set standard cost. Managers by comparing

standard cost with actual cost evaluates the overall performance of company.

Management accounting system and management accounting reporting is integrated within

organisational processes

In present business scenarios every organisation emphasises on management accounting

system and reporting for which different processes are implemented by organisation in order to

integrate management accounting system and reporting within organisational processes. Data

and information used in management accounting and reporting is obtained though the outputs of

various other organisational processes, such as accounting process provide a basic information

and data for management accounting system and reporting (McLean, McGovern and Davie,

2015). In Unilever management is aware about the importance of management accounting

system so the implement process which directly provides support to management in order to

implement management accounting system and reporting. In Unilever, managers of different

department and store are generated in managing data to provide relevant information for

management accounting and reporting. In company inventory and stock is marinated through

various processes which ultimately assist in effective inventory management.

Benefits of management accounting systems:

Different type of management accounting system is used by management to implement

an overall effective management accounting system and to solve different problems. Following

are some key benefits of management accounting system, in the context of Unilever, as follows:

Different accounting Benefits

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

systems

Inventory management

system

it assist business organisation in effective utilisation of

inventory and goods.

It ensures availability of goods any time in company.

It help management in company to track the on-line and

real time movement of inventory and stock.

It provide benefit to company by reducing storage and

extra inventory cost.

Job Costing system It ensures proper and effective allocation of different cost

to various cost and job.

It help to identify any inefficient and excessive cost

making job or task which leads to increase in overall

profitability (Takeda and Boyns, 2014).

It help to define the performance of each task or job within

organisation for strategy formulation.

Cost accounting system It provide assistance in evaluating the cost of various

product in Unilever which help to gain competitive

advantages.

It assist in assessing the overall performance in term of

each unit within respective company.

It assist management in framing policies regarding overall

cost reduction to increase profitability in company

It help managers in Unilever to take decision regarding

whether it is cost effective to open or shout down company

store.

Price optimization system It helps Unilever to optimise their while maintaining same

profit margin.

Company with help of this system minimise product price

to gain competitive advantages.

6

Inventory management

system

it assist business organisation in effective utilisation of

inventory and goods.

It ensures availability of goods any time in company.

It help management in company to track the on-line and

real time movement of inventory and stock.

It provide benefit to company by reducing storage and

extra inventory cost.

Job Costing system It ensures proper and effective allocation of different cost

to various cost and job.

It help to identify any inefficient and excessive cost

making job or task which leads to increase in overall

profitability (Takeda and Boyns, 2014).

It help to define the performance of each task or job within

organisation for strategy formulation.

Cost accounting system It provide assistance in evaluating the cost of various

product in Unilever which help to gain competitive

advantages.

It assist in assessing the overall performance in term of

each unit within respective company.

It assist management in framing policies regarding overall

cost reduction to increase profitability in company

It help managers in Unilever to take decision regarding

whether it is cost effective to open or shout down company

store.

Price optimization system It helps Unilever to optimise their while maintaining same

profit margin.

Company with help of this system minimise product price

to gain competitive advantages.

6

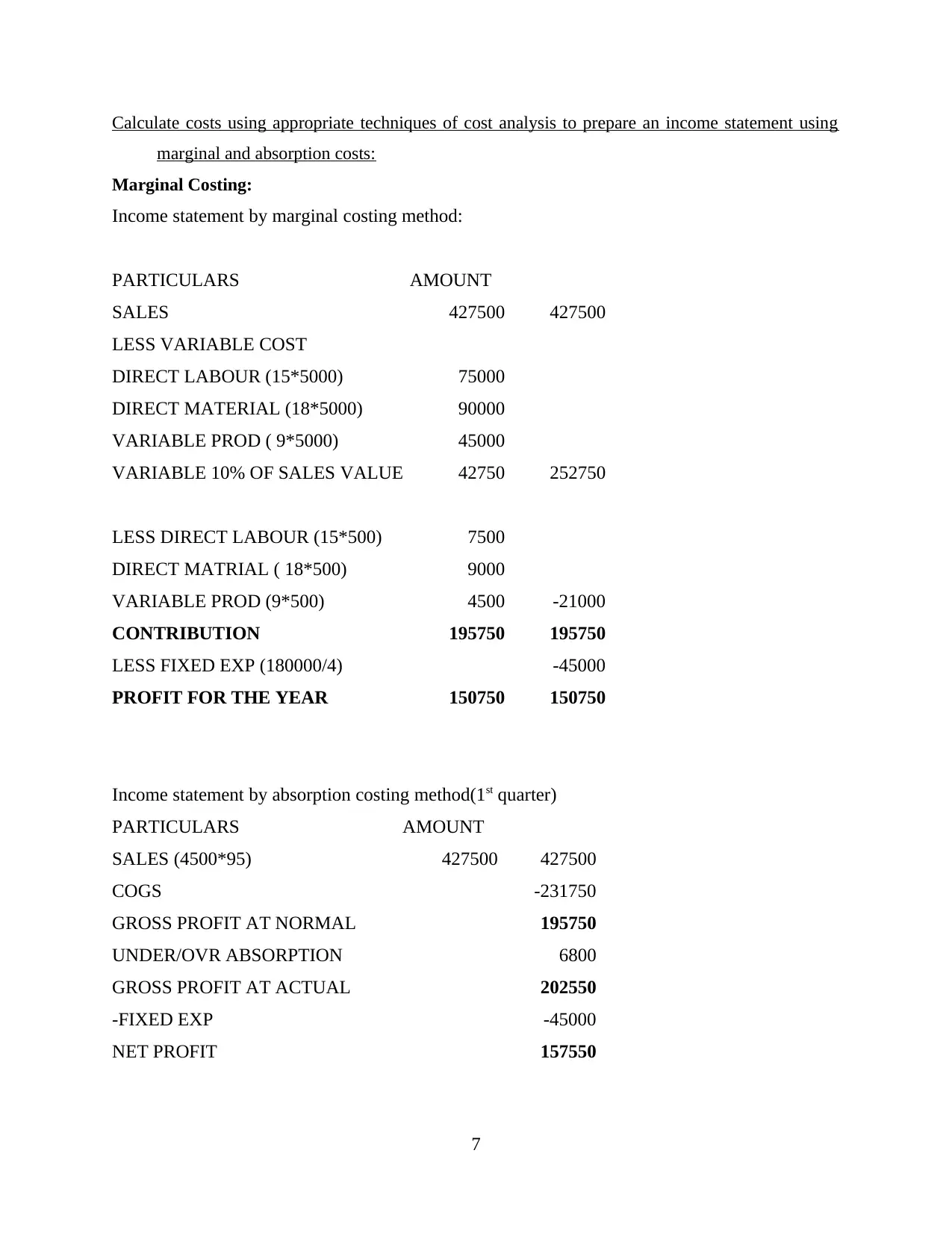

Calculate costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs:

Marginal Costing:

Income statement by marginal costing method:

PARTICULARS AMOUNT

SALES 427500 427500

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method(1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

-FIXED EXP -45000

NET PROFIT 157550

7

marginal and absorption costs:

Marginal Costing:

Income statement by marginal costing method:

PARTICULARS AMOUNT

SALES 427500 427500

LESS VARIABLE COST

DIRECT LABOUR (15*5000) 75000

DIRECT MATERIAL (18*5000) 90000

VARIABLE PROD ( 9*5000) 45000

VARIABLE 10% OF SALES VALUE 42750 252750

LESS DIRECT LABOUR (15*500) 7500

DIRECT MATRIAL ( 18*500) 9000

VARIABLE PROD (9*500) 4500 -21000

CONTRIBUTION 195750 195750

LESS FIXED EXP (180000/4) -45000

PROFIT FOR THE YEAR 150750 150750

Income statement by absorption costing method(1st quarter)

PARTICULARS AMOUNT

SALES (4500*95) 427500 427500

COGS -231750

GROSS PROFIT AT NORMAL 195750

UNDER/OVR ABSORPTION 6800

GROSS PROFIT AT ACTUAL 202550

-FIXED EXP -45000

NET PROFIT 157550

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

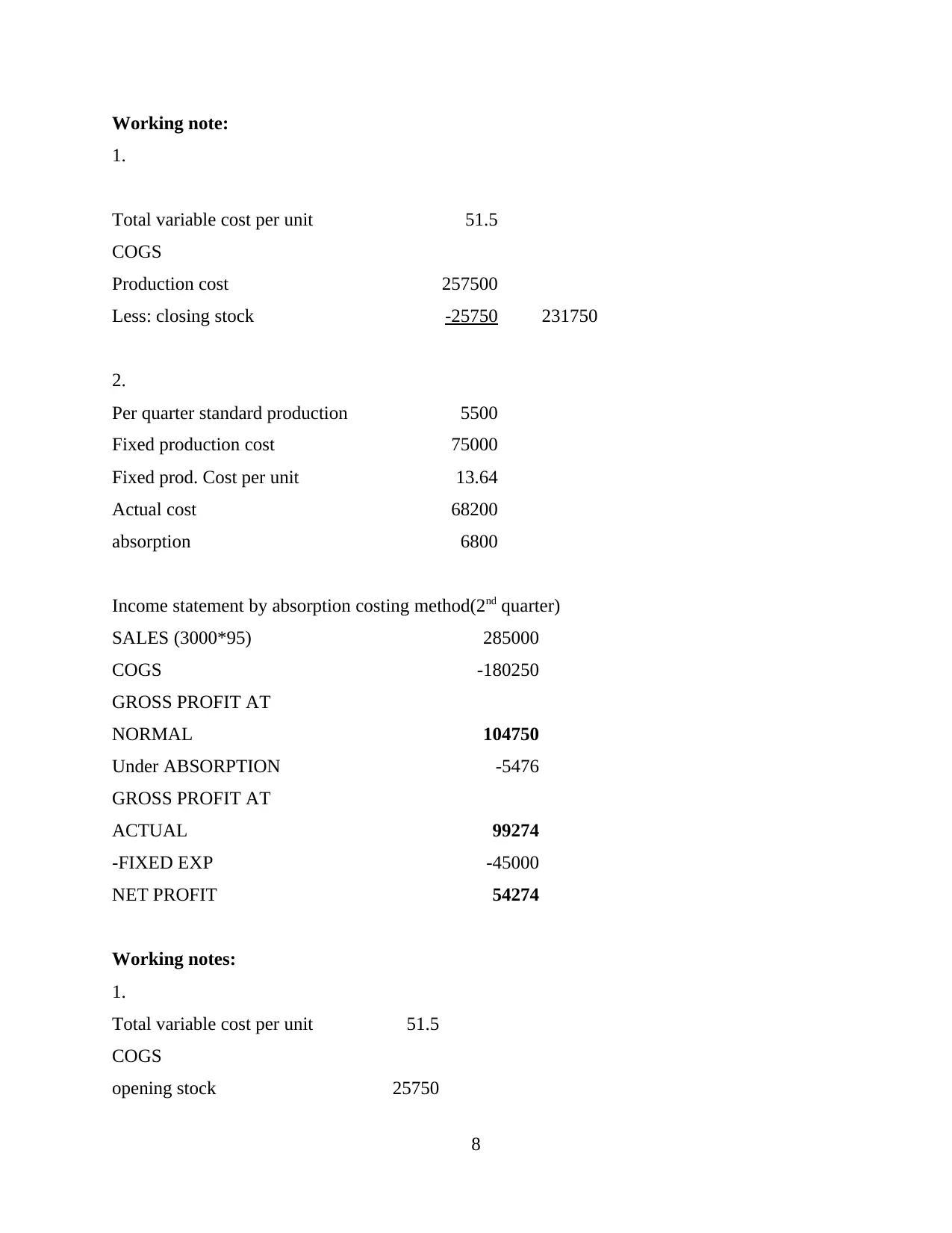

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method(2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

8

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method(2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

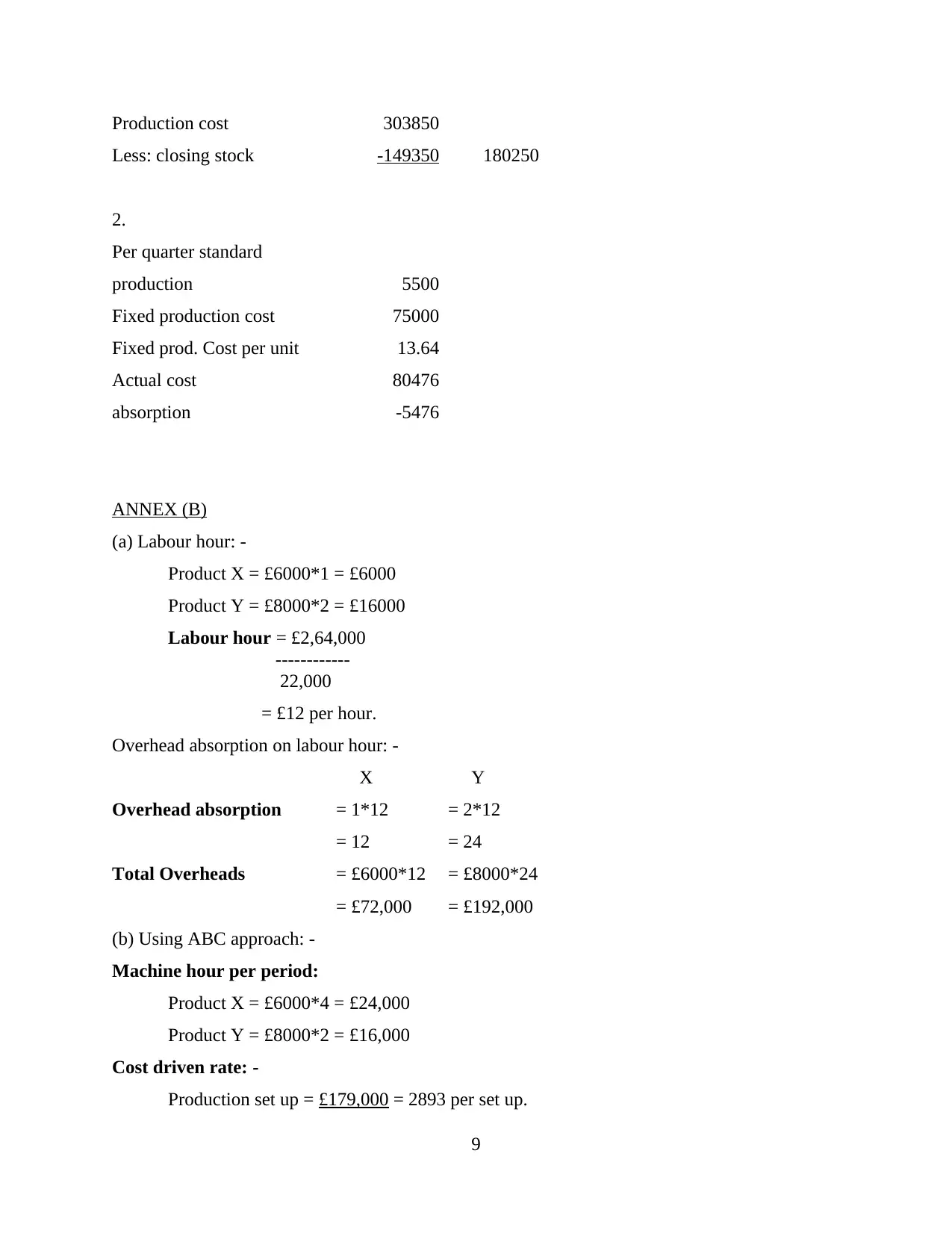

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

9

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

9

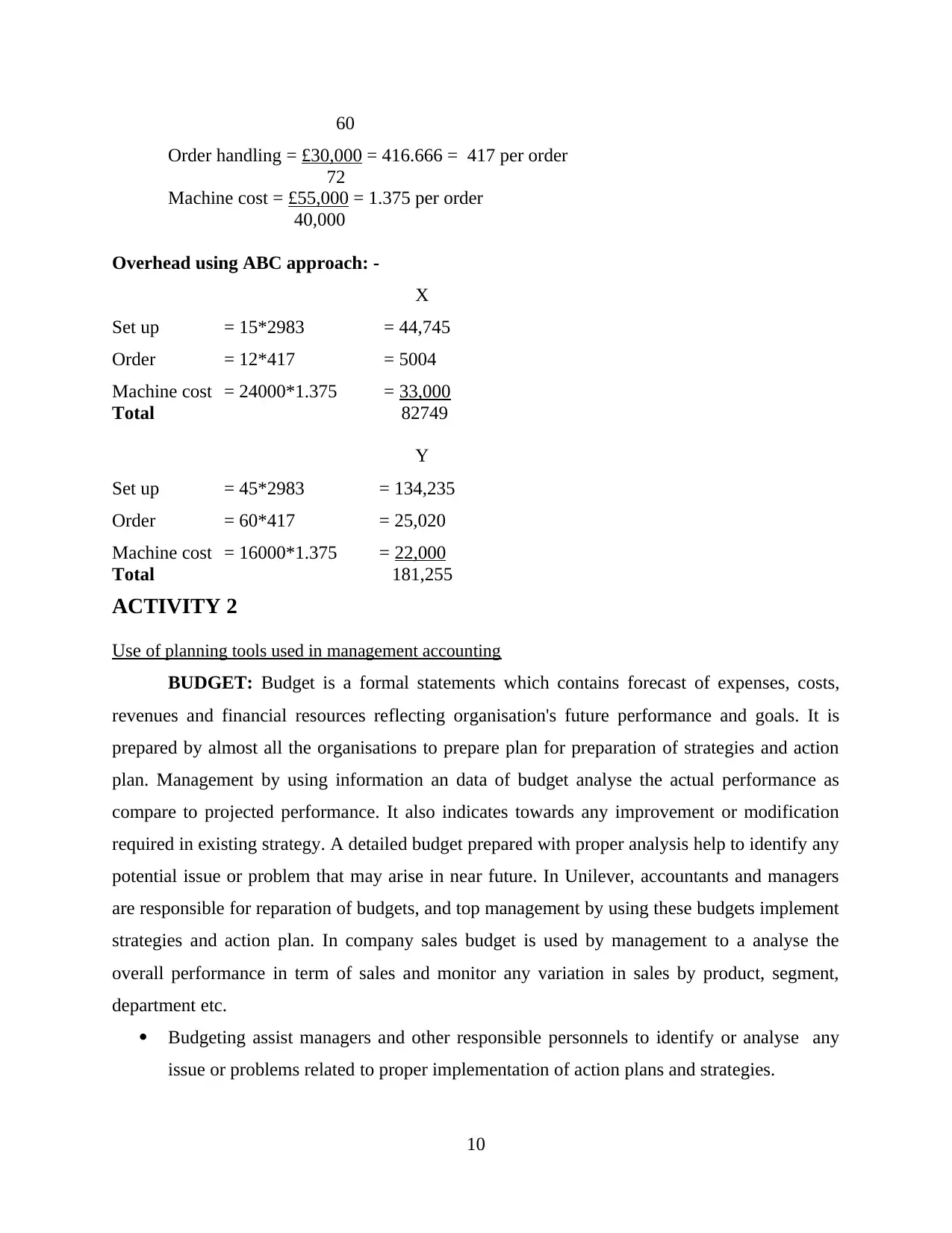

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

ACTIVITY 2

Use of planning tools used in management accounting

BUDGET: Budget is a formal statements which contains forecast of expenses, costs,

revenues and financial resources reflecting organisation's future performance and goals. It is

prepared by almost all the organisations to prepare plan for preparation of strategies and action

plan. Management by using information an data of budget analyse the actual performance as

compare to projected performance. It also indicates towards any improvement or modification

required in existing strategy. A detailed budget prepared with proper analysis help to identify any

potential issue or problem that may arise in near future. In Unilever, accountants and managers

are responsible for reparation of budgets, and top management by using these budgets implement

strategies and action plan. In company sales budget is used by management to a analyse the

overall performance in term of sales and monitor any variation in sales by product, segment,

department etc.

Budgeting assist managers and other responsible personnels to identify or analyse any

issue or problems related to proper implementation of action plans and strategies.

10

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

ACTIVITY 2

Use of planning tools used in management accounting

BUDGET: Budget is a formal statements which contains forecast of expenses, costs,

revenues and financial resources reflecting organisation's future performance and goals. It is

prepared by almost all the organisations to prepare plan for preparation of strategies and action

plan. Management by using information an data of budget analyse the actual performance as

compare to projected performance. It also indicates towards any improvement or modification

required in existing strategy. A detailed budget prepared with proper analysis help to identify any

potential issue or problem that may arise in near future. In Unilever, accountants and managers

are responsible for reparation of budgets, and top management by using these budgets implement

strategies and action plan. In company sales budget is used by management to a analyse the

overall performance in term of sales and monitor any variation in sales by product, segment,

department etc.

Budgeting assist managers and other responsible personnels to identify or analyse any

issue or problems related to proper implementation of action plans and strategies.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.