Management Accounting Report: Unit 5 Analysis and Evaluation

VerifiedAdded on 2020/07/22

|17

|4206

|31

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its importance for organizational decision-making and financial control. It delves into various aspects, including management accounting versus financial accounting, cost accounting systems (normal, actual, and standard costing), inventory management, and job costing systems. The report also explores job cost reports, inventory management reports, operating budget reports, and performance reports. Furthermore, it analyzes marginal and absorption costing methods, highlighting their impact on net profit calculations. The report discusses the advantages of financial and operating budgets, including cash, capital expenditure, and balance sheet budgets. It also covers performance appraisal approaches such as the balanced scorecard and Just-In-Time methods to address financial obstacles, concluding with the importance of management accounting reports for effective business operations and achieving organizational goals.

UNIT-5 MNG ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 ...........................................................................................................................................1

P2 ...........................................................................................................................................3

TASK 2 ..........................................................................................................................................5

P3 ...........................................................................................................................................5

TASK 3............................................................................................................................................7

P4 ...........................................................................................................................................7

TASK 4 .........................................................................................................................................10

P5 .........................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 ...........................................................................................................................................1

P2 ...........................................................................................................................................3

TASK 2 ..........................................................................................................................................5

P3 ...........................................................................................................................................5

TASK 3............................................................................................................................................7

P4 ...........................................................................................................................................7

TASK 4 .........................................................................................................................................10

P5 .........................................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting and reports will help organisation and managers to cope up with

business activities and solve financial problems in the firm. The report focuses on essential

requirement of different management accounting system and methods of accounting reports.

Income statement is also made by using marginal and absorption costing method in order to

generate the net profit amount. Advantages and disadvantages of planning tools used for

controlling the budget will be discussed in this report. Finally, the performance appraisal

approaches such as balance scorecard and Just-In-Time method to address financial obstacles for

the firm is discussed.

TASK 1

P1

MANAGEMENT ACCOUNTING

It is a crucial process for any organisation which is also known as managerial and cost

accounting effectively. The report will help management to prepare internal financial reports,

analysing the cost of business operational activities and help towards decision making

efficiently. Management accounting also helps to make financial and costing data and also useful

to translate it into information (Adjei, 2016). This will help management to manage and control

business activities from which they are able to achieve better planning over firm. Management

accounting also increase the value of shareholders and customers which helps to manage the

resources accordingly and effectively.

Decision-making tool

It has been ascertained here that managers has important role in the organisation in terms

of making decisions relevant with financial and non-financial duties that management accounting

will help them to improve the decision making. This will be managed by the managers for the

long-time of period and with data driven inputs. For an example, cost analysis, cost techniques

and utilisation of information and data.

Management accounting helps to identify the performance metrics which is crucial for

managers.

Reports collect information relevant with financial and non-financial duties for managers.

Determine the deviation and provide valuable suggestions to measure them effectively.

1

Management accounting and reports will help organisation and managers to cope up with

business activities and solve financial problems in the firm. The report focuses on essential

requirement of different management accounting system and methods of accounting reports.

Income statement is also made by using marginal and absorption costing method in order to

generate the net profit amount. Advantages and disadvantages of planning tools used for

controlling the budget will be discussed in this report. Finally, the performance appraisal

approaches such as balance scorecard and Just-In-Time method to address financial obstacles for

the firm is discussed.

TASK 1

P1

MANAGEMENT ACCOUNTING

It is a crucial process for any organisation which is also known as managerial and cost

accounting effectively. The report will help management to prepare internal financial reports,

analysing the cost of business operational activities and help towards decision making

efficiently. Management accounting also helps to make financial and costing data and also useful

to translate it into information (Adjei, 2016). This will help management to manage and control

business activities from which they are able to achieve better planning over firm. Management

accounting also increase the value of shareholders and customers which helps to manage the

resources accordingly and effectively.

Decision-making tool

It has been ascertained here that managers has important role in the organisation in terms

of making decisions relevant with financial and non-financial duties that management accounting

will help them to improve the decision making. This will be managed by the managers for the

long-time of period and with data driven inputs. For an example, cost analysis, cost techniques

and utilisation of information and data.

Management accounting helps to identify the performance metrics which is crucial for

managers.

Reports collect information relevant with financial and non-financial duties for managers.

Determine the deviation and provide valuable suggestions to measure them effectively.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

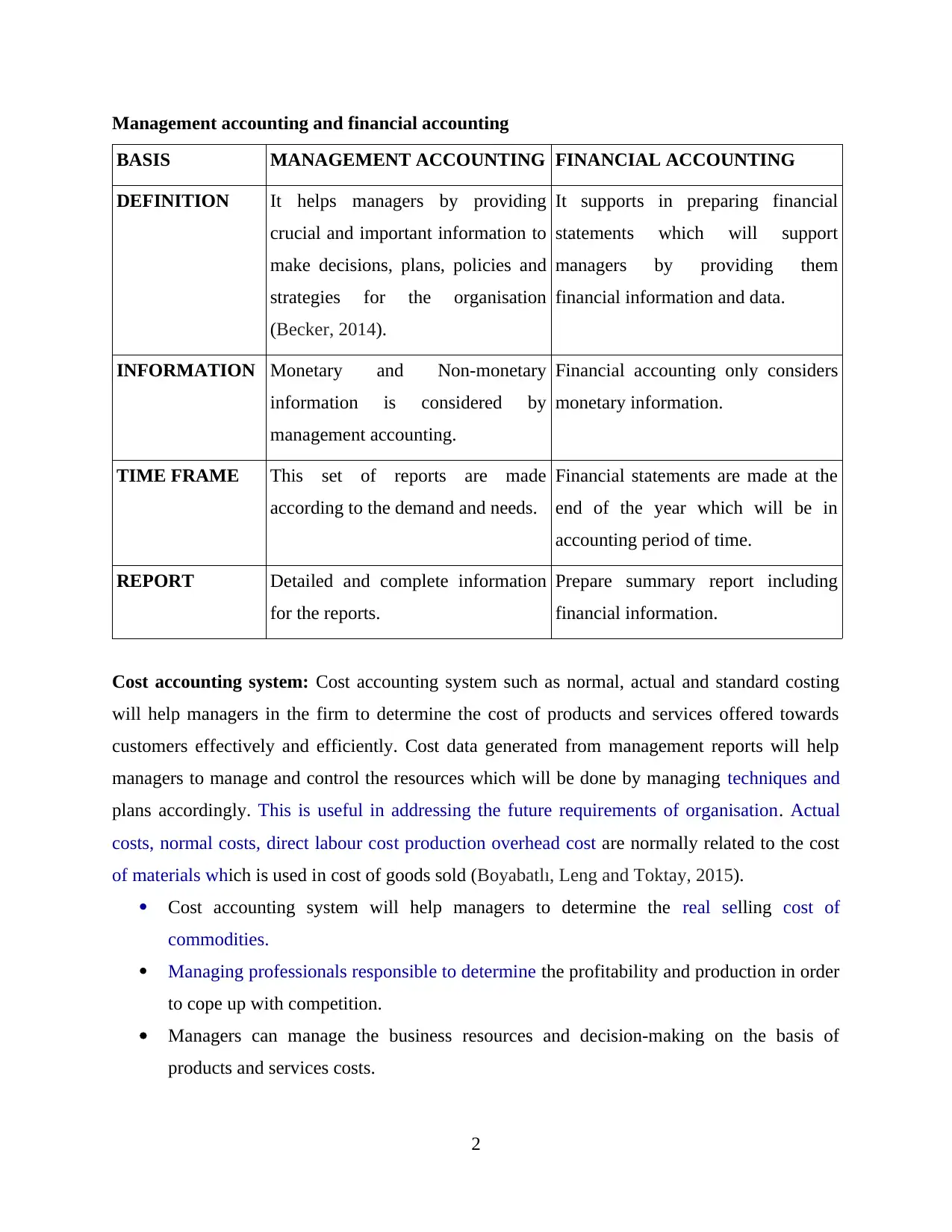

Management accounting and financial accounting

BASIS MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

DEFINITION It helps managers by providing

crucial and important information to

make decisions, plans, policies and

strategies for the organisation

(Becker, 2014).

It supports in preparing financial

statements which will support

managers by providing them

financial information and data.

INFORMATION Monetary and Non-monetary

information is considered by

management accounting.

Financial accounting only considers

monetary information.

TIME FRAME This set of reports are made

according to the demand and needs.

Financial statements are made at the

end of the year which will be in

accounting period of time.

REPORT Detailed and complete information

for the reports.

Prepare summary report including

financial information.

Cost accounting system: Cost accounting system such as normal, actual and standard costing

will help managers in the firm to determine the cost of products and services offered towards

customers effectively and efficiently. Cost data generated from management reports will help

managers to manage and control the resources which will be done by managing techniques and

plans accordingly. This is useful in addressing the future requirements of organisation. Actual

costs, normal costs, direct labour cost production overhead cost are normally related to the cost

of materials which is used in cost of goods sold (Boyabatlı, Leng and Toktay, 2015).

Cost accounting system will help managers to determine the real selling cost of

commodities.

Managing professionals responsible to determine the profitability and production in order

to cope up with competition.

Managers can manage the business resources and decision-making on the basis of

products and services costs.

2

BASIS MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

DEFINITION It helps managers by providing

crucial and important information to

make decisions, plans, policies and

strategies for the organisation

(Becker, 2014).

It supports in preparing financial

statements which will support

managers by providing them

financial information and data.

INFORMATION Monetary and Non-monetary

information is considered by

management accounting.

Financial accounting only considers

monetary information.

TIME FRAME This set of reports are made

according to the demand and needs.

Financial statements are made at the

end of the year which will be in

accounting period of time.

REPORT Detailed and complete information

for the reports.

Prepare summary report including

financial information.

Cost accounting system: Cost accounting system such as normal, actual and standard costing

will help managers in the firm to determine the cost of products and services offered towards

customers effectively and efficiently. Cost data generated from management reports will help

managers to manage and control the resources which will be done by managing techniques and

plans accordingly. This is useful in addressing the future requirements of organisation. Actual

costs, normal costs, direct labour cost production overhead cost are normally related to the cost

of materials which is used in cost of goods sold (Boyabatlı, Leng and Toktay, 2015).

Cost accounting system will help managers to determine the real selling cost of

commodities.

Managing professionals responsible to determine the profitability and production in order

to cope up with competition.

Managers can manage the business resources and decision-making on the basis of

products and services costs.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management system: Inventory management is all about managing and controlling

the resources which will be the stock of products and services, finished goods and raw materials.

Work in progress will be also aid in inventory management. This will help managers to manage

the resources which will help them to determine the availability, quality and quantity of stock

effectively. The inventory cost will include cost of storage, capital cost, insurance and tax and

facility cost efficiently (Busco and Quattrone, 2015).

Inventory management ascertains the economy scale of the organisation which in turn reflects in

presenting appropriate strategies, plans and policies for better management.

Job casting system: Job casting system can be defined as a process which will be fruitful

to the managers to identify the present cost of operations at work place to manage and control it

effectively. The process is also use to cost recording and accumulation. The job casting system is

used by those firms where the product production is 'One Off' and also various for a consumers

efficiently. The method is also used by the firms in case a customer put a specific demand

towards product or service which should be completed in a short period of time effectively.

Job casting system helps to determine the cost of decision-making, controlling and

planning of managers effectively.

The method also helps managers to measure the selling cost of an article and also

evaluate the profitability and deficits.

P2

Job cost reports: The job cost reports are useful for managers to evaluate and analyse

the cost of operations or a project accurately and efficiently. This will be helpful to managers in

determining generated profitability from the work of workers in the entity and the reports are

combined with revenue forecasts (Butler and Ghosh, 2015). Job cost reports will also help to

evaluate the cost of product and service when the work is in progress.

Inventory management reports: Inventory management system is important for the

firm in order to control and manage the various levels of inventory effectively and efficiently.

There are so many inventory levels managed and controlled by the managers such as quantity,

quality and availability of stock in terms of products and services offered by business to

customers in the market. Inventory management system should be physical which will help

managers to evaluate the stock activities.

3

the resources which will be the stock of products and services, finished goods and raw materials.

Work in progress will be also aid in inventory management. This will help managers to manage

the resources which will help them to determine the availability, quality and quantity of stock

effectively. The inventory cost will include cost of storage, capital cost, insurance and tax and

facility cost efficiently (Busco and Quattrone, 2015).

Inventory management ascertains the economy scale of the organisation which in turn reflects in

presenting appropriate strategies, plans and policies for better management.

Job casting system: Job casting system can be defined as a process which will be fruitful

to the managers to identify the present cost of operations at work place to manage and control it

effectively. The process is also use to cost recording and accumulation. The job casting system is

used by those firms where the product production is 'One Off' and also various for a consumers

efficiently. The method is also used by the firms in case a customer put a specific demand

towards product or service which should be completed in a short period of time effectively.

Job casting system helps to determine the cost of decision-making, controlling and

planning of managers effectively.

The method also helps managers to measure the selling cost of an article and also

evaluate the profitability and deficits.

P2

Job cost reports: The job cost reports are useful for managers to evaluate and analyse

the cost of operations or a project accurately and efficiently. This will be helpful to managers in

determining generated profitability from the work of workers in the entity and the reports are

combined with revenue forecasts (Butler and Ghosh, 2015). Job cost reports will also help to

evaluate the cost of product and service when the work is in progress.

Inventory management reports: Inventory management system is important for the

firm in order to control and manage the various levels of inventory effectively and efficiently.

There are so many inventory levels managed and controlled by the managers such as quantity,

quality and availability of stock in terms of products and services offered by business to

customers in the market. Inventory management system should be physical which will help

managers to evaluate the stock activities.

3

Operating budget reports: This report will be fruitful to the managers working in entity

to evaluate and determine the performance level of different units to execute and control the cost

of industrial activities under the budget. Operating budget analysis is also helpful to provide

rewards and incentives to employees according to their best performances in the firm effectively.

Accounts receivable ageing reports: This report will help managers in the firm to

ascertain and control the cash flow effectively and efficiently. This can be described as a critical

tool which breaks down the balance of customers at the time they owned the firm. Such reports

will also address the overlook at the past debts of the firm (D'Onza, Greco and Allegrini, 2016).

Performance reports: Performance report or analysis will help managers to evaluate the

performance of various departments which will include top level, middle level and bottom level

employees and their performances towards the work. The performance report will also help to

measure the profitability and production according to the work done by different departments.

This will help managers to measure the performance of employees at individual level which also

fill the requirement of increasing skills and knowledge in employees regarding the work

effectively.

IMPORTANCE

Management accounting reports are crucial and essential for the organisation in order to

manage the business activities and operations in the market towards customers effectively. This

will also help managers to increase their efficiency towards making effective decision regarding

operational and business activities. The inventory management, job casting, performance, cost

and accounts receivable reports will help managers to evaluate the actual position of the firm in

the market which will help them to manage the profitability and production accordingly and

effectively (Follmer and Johnson, 2017). This will also help to enhance the decision-making to

ascertain the cost of products and services offered by the firm under the budget. Strategies, plans

and policies are made by the managers with these reports which help to ensure the firm is

working in a proper and appropriate manner.

Thus, it can be addressed here, that this accounting reports are useful as well as important

for both managers and the firm in order to cope up with market and business activities. This will

help to increase the profitability and production which leads towards accomplishing the business

objectives and goals effectively and efficiently.

4

to evaluate and determine the performance level of different units to execute and control the cost

of industrial activities under the budget. Operating budget analysis is also helpful to provide

rewards and incentives to employees according to their best performances in the firm effectively.

Accounts receivable ageing reports: This report will help managers in the firm to

ascertain and control the cash flow effectively and efficiently. This can be described as a critical

tool which breaks down the balance of customers at the time they owned the firm. Such reports

will also address the overlook at the past debts of the firm (D'Onza, Greco and Allegrini, 2016).

Performance reports: Performance report or analysis will help managers to evaluate the

performance of various departments which will include top level, middle level and bottom level

employees and their performances towards the work. The performance report will also help to

measure the profitability and production according to the work done by different departments.

This will help managers to measure the performance of employees at individual level which also

fill the requirement of increasing skills and knowledge in employees regarding the work

effectively.

IMPORTANCE

Management accounting reports are crucial and essential for the organisation in order to

manage the business activities and operations in the market towards customers effectively. This

will also help managers to increase their efficiency towards making effective decision regarding

operational and business activities. The inventory management, job casting, performance, cost

and accounts receivable reports will help managers to evaluate the actual position of the firm in

the market which will help them to manage the profitability and production accordingly and

effectively (Follmer and Johnson, 2017). This will also help to enhance the decision-making to

ascertain the cost of products and services offered by the firm under the budget. Strategies, plans

and policies are made by the managers with these reports which help to ensure the firm is

working in a proper and appropriate manner.

Thus, it can be addressed here, that this accounting reports are useful as well as important

for both managers and the firm in order to cope up with market and business activities. This will

help to increase the profitability and production which leads towards accomplishing the business

objectives and goals effectively and efficiently.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

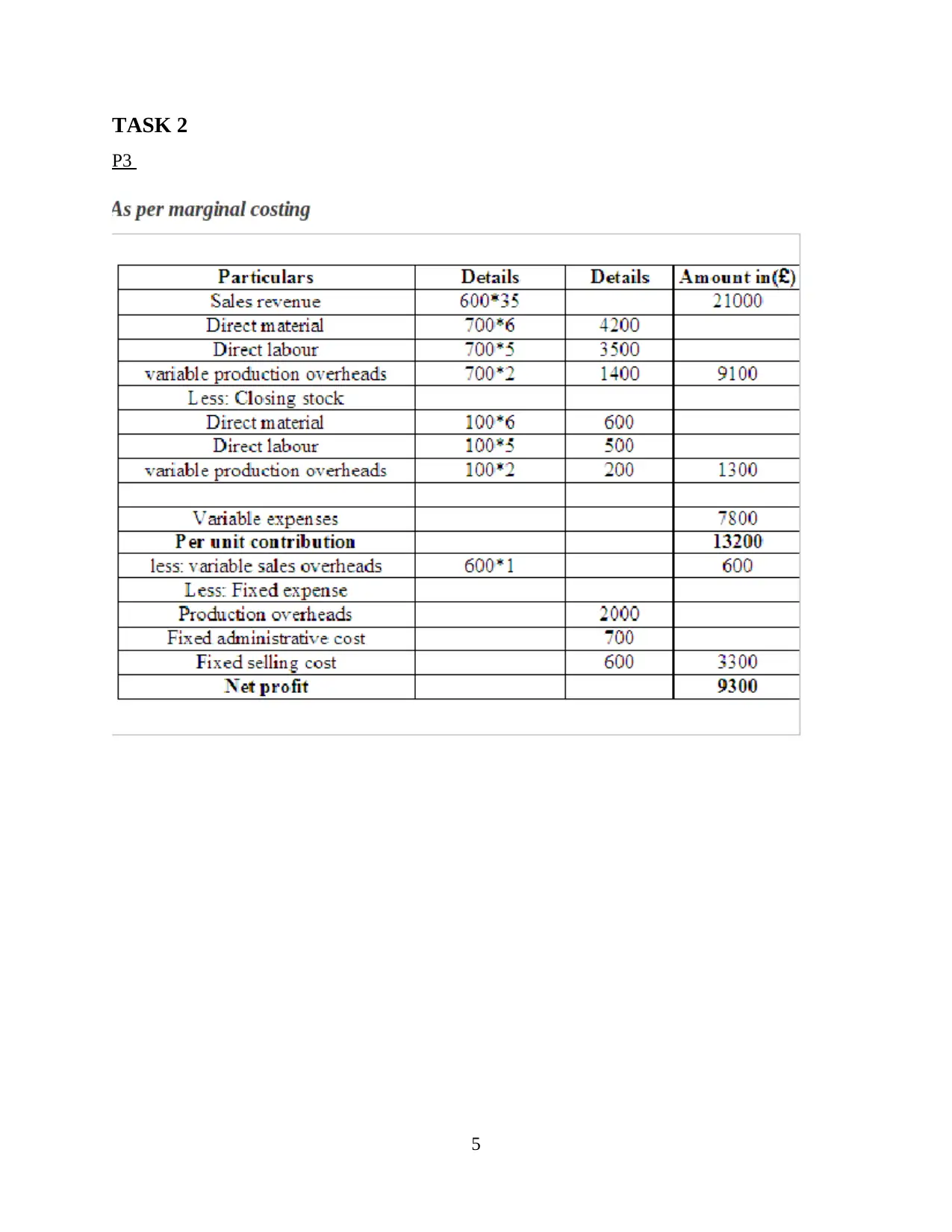

P3

5

P3

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

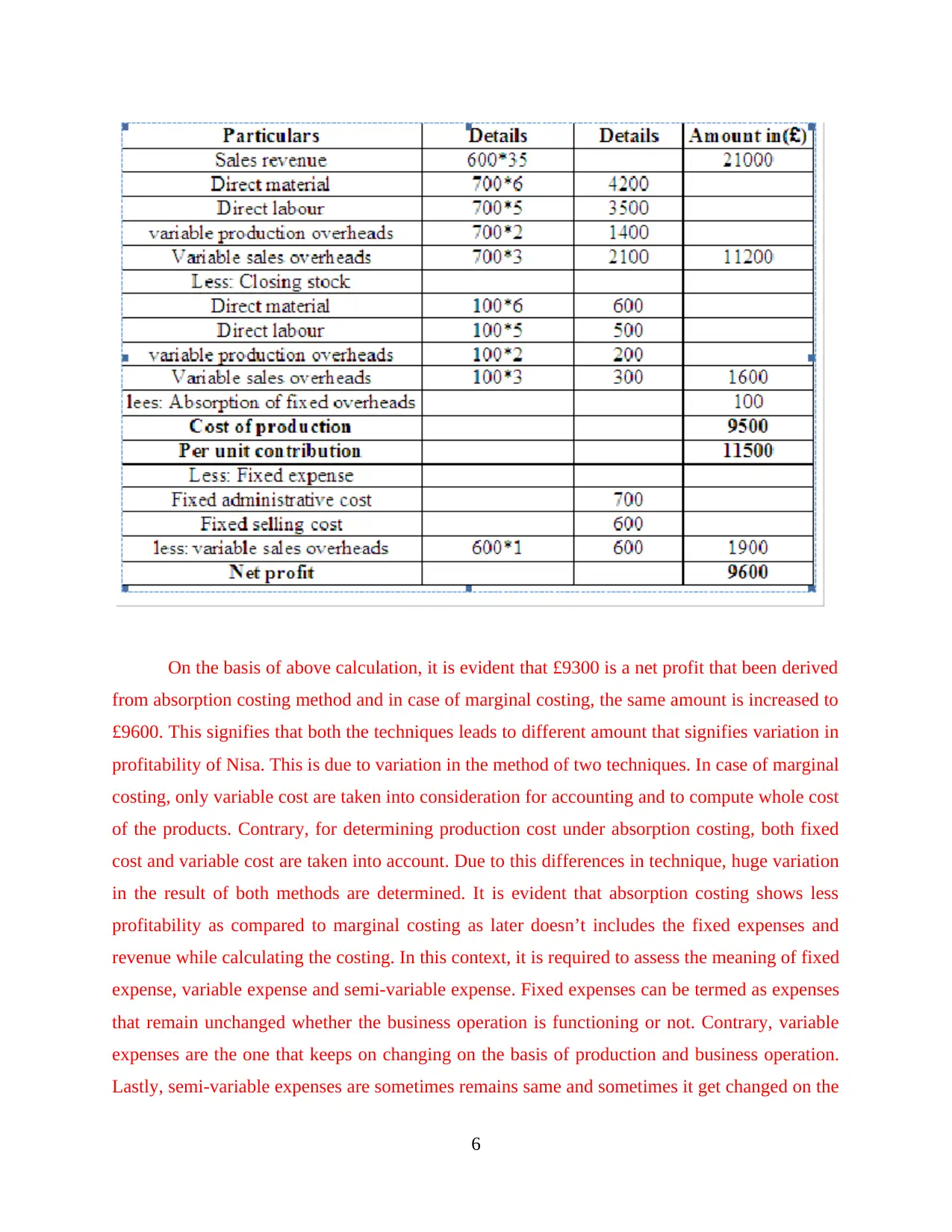

On the basis of above calculation, it is evident that £9300 is a net profit that been derived

from absorption costing method and in case of marginal costing, the same amount is increased to

£9600. This signifies that both the techniques leads to different amount that signifies variation in

profitability of Nisa. This is due to variation in the method of two techniques. In case of marginal

costing, only variable cost are taken into consideration for accounting and to compute whole cost

of the products. Contrary, for determining production cost under absorption costing, both fixed

cost and variable cost are taken into account. Due to this differences in technique, huge variation

in the result of both methods are determined. It is evident that absorption costing shows less

profitability as compared to marginal costing as later doesn’t includes the fixed expenses and

revenue while calculating the costing. In this context, it is required to assess the meaning of fixed

expense, variable expense and semi-variable expense. Fixed expenses can be termed as expenses

that remain unchanged whether the business operation is functioning or not. Contrary, variable

expenses are the one that keeps on changing on the basis of production and business operation.

Lastly, semi-variable expenses are sometimes remains same and sometimes it get changed on the

6

from absorption costing method and in case of marginal costing, the same amount is increased to

£9600. This signifies that both the techniques leads to different amount that signifies variation in

profitability of Nisa. This is due to variation in the method of two techniques. In case of marginal

costing, only variable cost are taken into consideration for accounting and to compute whole cost

of the products. Contrary, for determining production cost under absorption costing, both fixed

cost and variable cost are taken into account. Due to this differences in technique, huge variation

in the result of both methods are determined. It is evident that absorption costing shows less

profitability as compared to marginal costing as later doesn’t includes the fixed expenses and

revenue while calculating the costing. In this context, it is required to assess the meaning of fixed

expense, variable expense and semi-variable expense. Fixed expenses can be termed as expenses

that remain unchanged whether the business operation is functioning or not. Contrary, variable

expenses are the one that keeps on changing on the basis of production and business operation.

Lastly, semi-variable expenses are sometimes remains same and sometimes it get changed on the

6

basis of business activities. Considering this, it is highly required that manager must adopt the

best suitable approach for costing in order to determine the business profitability. However,

contradiction usually arises while choosing marginal or absorption costing method. It is evident

that fixed expenses are included in absorption costing, hence, it considers expenses like purchase

of fixed assess and aids in attaining actual effect of it on overall costing of business.

Considering this, it can be state that marginal and absorption method aids in assessing the

net income in different scenario and supports in managing the business activities in appropriate

manner.

TASK 3

P4

Financial budget

Financial budget can be described as the firm's expectations which refer to improve and

develop the cash revenues. This will be done for future time period and also assist in making

strategies as well as action plans to spend on such activities as an advantage to the firm.

Cash budget: Managers can control and manage the cash from cash budget which will in terms

of outgoing and incoming, monthly or yearly effectively. Cash budget is so important for the

managers in order to determine the availability of cash in the firm which is used for managing

the resources and production. Cash transactions, production cost and salary can be also managed

by preparing cash budget for the firm (Friis and Hansen, 2015).

Capital expenditure budget: Managers are able to focus on some major assets of the firm such

as land, machineries and plant which is useful as well as important. This can be done by

managing the capital expenditure budget. The budget can be attained from both long term bonds

as well as securities efficiently.

Balance sheet budget: Balance sheet budget can be managed by accomplishing all the demands

and requirements of firm which will increase the balance sheet. A suitable and appropriate

organisation of balance sheet budget will help managers to achieve and control the budget

network effectively.

OPERATING BUDGET

Revenue and sales budget: This budget is mainly focused on the revenue which is acquired by

the firm from managing and controlling the operational actions in the market towards customers

7

best suitable approach for costing in order to determine the business profitability. However,

contradiction usually arises while choosing marginal or absorption costing method. It is evident

that fixed expenses are included in absorption costing, hence, it considers expenses like purchase

of fixed assess and aids in attaining actual effect of it on overall costing of business.

Considering this, it can be state that marginal and absorption method aids in assessing the

net income in different scenario and supports in managing the business activities in appropriate

manner.

TASK 3

P4

Financial budget

Financial budget can be described as the firm's expectations which refer to improve and

develop the cash revenues. This will be done for future time period and also assist in making

strategies as well as action plans to spend on such activities as an advantage to the firm.

Cash budget: Managers can control and manage the cash from cash budget which will in terms

of outgoing and incoming, monthly or yearly effectively. Cash budget is so important for the

managers in order to determine the availability of cash in the firm which is used for managing

the resources and production. Cash transactions, production cost and salary can be also managed

by preparing cash budget for the firm (Friis and Hansen, 2015).

Capital expenditure budget: Managers are able to focus on some major assets of the firm such

as land, machineries and plant which is useful as well as important. This can be done by

managing the capital expenditure budget. The budget can be attained from both long term bonds

as well as securities efficiently.

Balance sheet budget: Balance sheet budget can be managed by accomplishing all the demands

and requirements of firm which will increase the balance sheet. A suitable and appropriate

organisation of balance sheet budget will help managers to achieve and control the budget

network effectively.

OPERATING BUDGET

Revenue and sales budget: This budget is mainly focused on the revenue which is acquired by

the firm from managing and controlling the operational actions in the market towards customers

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

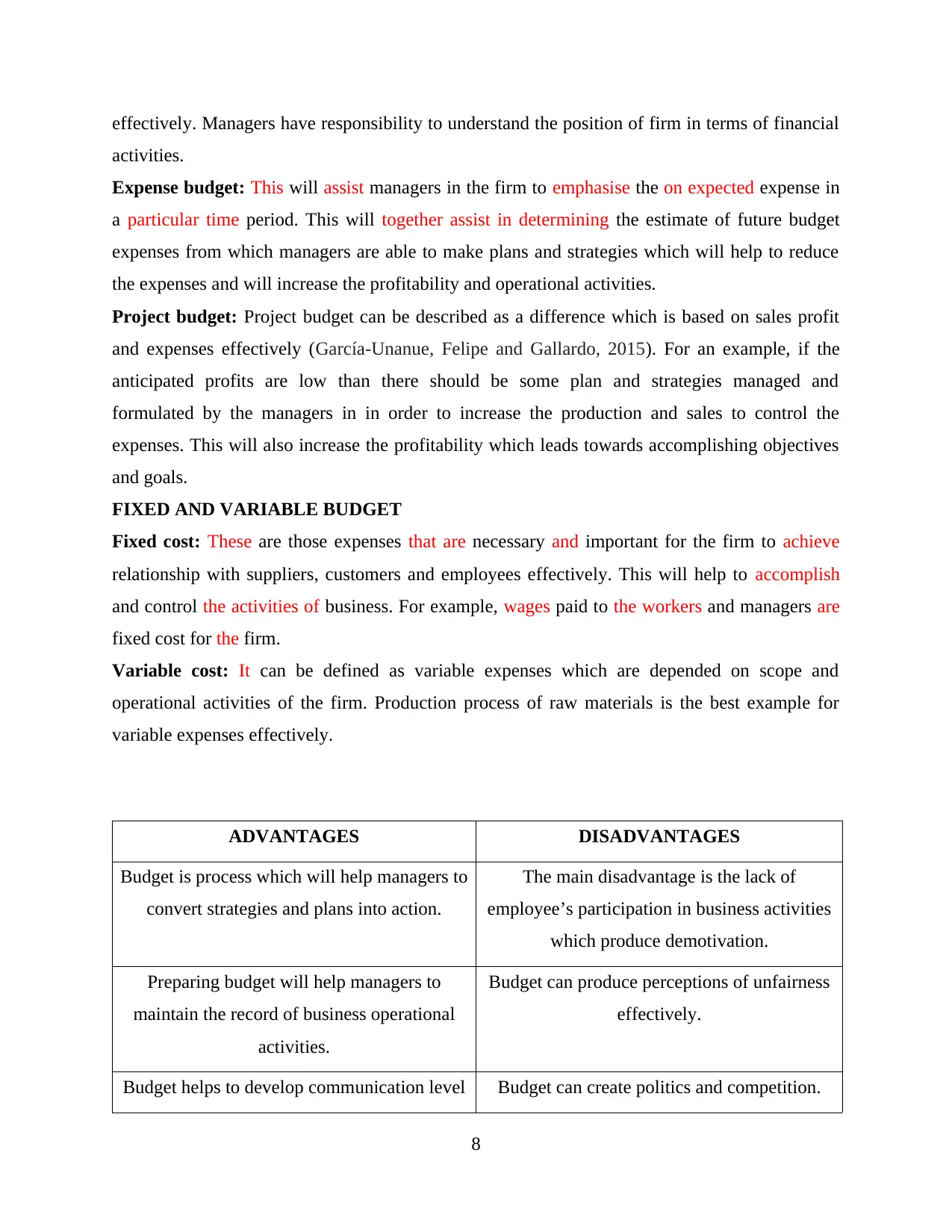

effectively. Managers have responsibility to understand the position of firm in terms of financial

activities.

Expense budget: This will assist managers in the firm to emphasise the on expected expense in

a particular time period. This will together assist in determining the estimate of future budget

expenses from which managers are able to make plans and strategies which will help to reduce

the expenses and will increase the profitability and operational activities.

Project budget: Project budget can be described as a difference which is based on sales profit

and expenses effectively (García-Unanue, Felipe and Gallardo, 2015). For an example, if the

anticipated profits are low than there should be some plan and strategies managed and

formulated by the managers in in order to increase the production and sales to control the

expenses. This will also increase the profitability which leads towards accomplishing objectives

and goals.

FIXED AND VARIABLE BUDGET

Fixed cost: These are those expenses that are necessary and important for the firm to achieve

relationship with suppliers, customers and employees effectively. This will help to accomplish

and control the activities of business. For example, wages paid to the workers and managers are

fixed cost for the firm.

Variable cost: It can be defined as variable expenses which are depended on scope and

operational activities of the firm. Production process of raw materials is the best example for

variable expenses effectively.

ADVANTAGES DISADVANTAGES

Budget is process which will help managers to

convert strategies and plans into action.

The main disadvantage is the lack of

employee’s participation in business activities

which produce demotivation.

Preparing budget will help managers to

maintain the record of business operational

activities.

Budget can produce perceptions of unfairness

effectively.

Budget helps to develop communication level Budget can create politics and competition.

8

activities.

Expense budget: This will assist managers in the firm to emphasise the on expected expense in

a particular time period. This will together assist in determining the estimate of future budget

expenses from which managers are able to make plans and strategies which will help to reduce

the expenses and will increase the profitability and operational activities.

Project budget: Project budget can be described as a difference which is based on sales profit

and expenses effectively (García-Unanue, Felipe and Gallardo, 2015). For an example, if the

anticipated profits are low than there should be some plan and strategies managed and

formulated by the managers in in order to increase the production and sales to control the

expenses. This will also increase the profitability which leads towards accomplishing objectives

and goals.

FIXED AND VARIABLE BUDGET

Fixed cost: These are those expenses that are necessary and important for the firm to achieve

relationship with suppliers, customers and employees effectively. This will help to accomplish

and control the activities of business. For example, wages paid to the workers and managers are

fixed cost for the firm.

Variable cost: It can be defined as variable expenses which are depended on scope and

operational activities of the firm. Production process of raw materials is the best example for

variable expenses effectively.

ADVANTAGES DISADVANTAGES

Budget is process which will help managers to

convert strategies and plans into action.

The main disadvantage is the lack of

employee’s participation in business activities

which produce demotivation.

Preparing budget will help managers to

maintain the record of business operational

activities.

Budget can produce perceptions of unfairness

effectively.

Budget helps to develop communication level Budget can create politics and competition.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

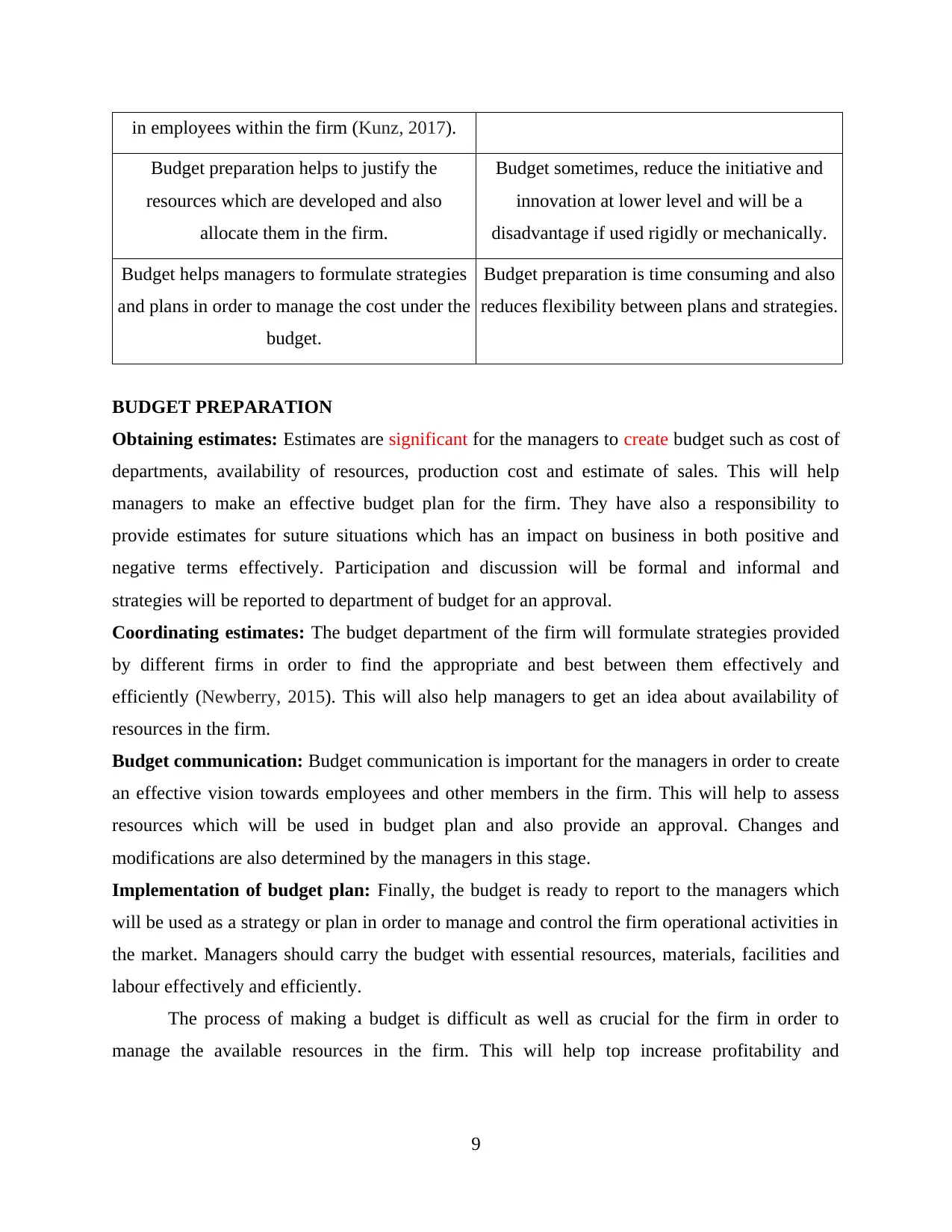

in employees within the firm (Kunz, 2017).

Budget preparation helps to justify the

resources which are developed and also

allocate them in the firm.

Budget sometimes, reduce the initiative and

innovation at lower level and will be a

disadvantage if used rigidly or mechanically.

Budget helps managers to formulate strategies

and plans in order to manage the cost under the

budget.

Budget preparation is time consuming and also

reduces flexibility between plans and strategies.

BUDGET PREPARATION

Obtaining estimates: Estimates are significant for the managers to create budget such as cost of

departments, availability of resources, production cost and estimate of sales. This will help

managers to make an effective budget plan for the firm. They have also a responsibility to

provide estimates for suture situations which has an impact on business in both positive and

negative terms effectively. Participation and discussion will be formal and informal and

strategies will be reported to department of budget for an approval.

Coordinating estimates: The budget department of the firm will formulate strategies provided

by different firms in order to find the appropriate and best between them effectively and

efficiently (Newberry, 2015). This will also help managers to get an idea about availability of

resources in the firm.

Budget communication: Budget communication is important for the managers in order to create

an effective vision towards employees and other members in the firm. This will help to assess

resources which will be used in budget plan and also provide an approval. Changes and

modifications are also determined by the managers in this stage.

Implementation of budget plan: Finally, the budget is ready to report to the managers which

will be used as a strategy or plan in order to manage and control the firm operational activities in

the market. Managers should carry the budget with essential resources, materials, facilities and

labour effectively and efficiently.

The process of making a budget is difficult as well as crucial for the firm in order to

manage the available resources in the firm. This will help top increase profitability and

9

Budget preparation helps to justify the

resources which are developed and also

allocate them in the firm.

Budget sometimes, reduce the initiative and

innovation at lower level and will be a

disadvantage if used rigidly or mechanically.

Budget helps managers to formulate strategies

and plans in order to manage the cost under the

budget.

Budget preparation is time consuming and also

reduces flexibility between plans and strategies.

BUDGET PREPARATION

Obtaining estimates: Estimates are significant for the managers to create budget such as cost of

departments, availability of resources, production cost and estimate of sales. This will help

managers to make an effective budget plan for the firm. They have also a responsibility to

provide estimates for suture situations which has an impact on business in both positive and

negative terms effectively. Participation and discussion will be formal and informal and

strategies will be reported to department of budget for an approval.

Coordinating estimates: The budget department of the firm will formulate strategies provided

by different firms in order to find the appropriate and best between them effectively and

efficiently (Newberry, 2015). This will also help managers to get an idea about availability of

resources in the firm.

Budget communication: Budget communication is important for the managers in order to create

an effective vision towards employees and other members in the firm. This will help to assess

resources which will be used in budget plan and also provide an approval. Changes and

modifications are also determined by the managers in this stage.

Implementation of budget plan: Finally, the budget is ready to report to the managers which

will be used as a strategy or plan in order to manage and control the firm operational activities in

the market. Managers should carry the budget with essential resources, materials, facilities and

labour effectively and efficiently.

The process of making a budget is difficult as well as crucial for the firm in order to

manage the available resources in the firm. This will help top increase profitability and

9

production which leads towards profitability and production (Song and Joo, 2015). Organisation

is also able to achieve the desired goals and objectives such as financial goals effectively.

IMPORTANCE OF BUDGET

Budget is important for the firm and managers in order to control the numerical form for

future time period and this will be done by making strategies and plans accordingly and

effectively. In addition, the budget will also help managers to manage and control their financial

and resources activities. The process for controlling the budget is discussed below:

Managers in the firm able to control and manage the business operational and financial activities.

Managers are able to evaluate and determine the standard of control system effectively.

It also helps to create guidelines about the firm resources and expectations.

It will also help managers to determine all the performance level of departments and employees.

Cost-based pricing: The cost-based pricing will help managers to determine the actual selling

cost of products and services offered by firm in the market towards customers effectively. Direct

cost pricing and full cost pricing are the two forms of cost-based pricing which will help

managers to control the cost of products in order to increase the profitability and production.

Cost plus pricing: Cost plus pricing is a stage where management and firm determine the cost of

direct labour, material and manufacturing overheads which will be aid in the price of products

later. This will help them to produce an effective price for products and services in the market

towards consumers (Verbeeten and Speklé, 2015).

Profit pricing: Profit pricing can be described as a strategy which is used to make money from

the products and services selling on each scale in the market effectively. In respect to this,

manufacturing cost will be evaluated and aid in the price of products.

Transfer price: In transfer price, the price division of an organisation transact with each other

for an example, labour between trade of suppliers and departments effectively. This will help

managers to manage and control the cost of products under the budget which leads towards

increasing profitability.

TASK 4

P5

Financial activities are the most important part for any organisation in order to manage

the different resources under the budget which helps to increase the profitability and

manufacturing. This will also help to reduce extra expenses which increase the cash in the firm

10

is also able to achieve the desired goals and objectives such as financial goals effectively.

IMPORTANCE OF BUDGET

Budget is important for the firm and managers in order to control the numerical form for

future time period and this will be done by making strategies and plans accordingly and

effectively. In addition, the budget will also help managers to manage and control their financial

and resources activities. The process for controlling the budget is discussed below:

Managers in the firm able to control and manage the business operational and financial activities.

Managers are able to evaluate and determine the standard of control system effectively.

It also helps to create guidelines about the firm resources and expectations.

It will also help managers to determine all the performance level of departments and employees.

Cost-based pricing: The cost-based pricing will help managers to determine the actual selling

cost of products and services offered by firm in the market towards customers effectively. Direct

cost pricing and full cost pricing are the two forms of cost-based pricing which will help

managers to control the cost of products in order to increase the profitability and production.

Cost plus pricing: Cost plus pricing is a stage where management and firm determine the cost of

direct labour, material and manufacturing overheads which will be aid in the price of products

later. This will help them to produce an effective price for products and services in the market

towards consumers (Verbeeten and Speklé, 2015).

Profit pricing: Profit pricing can be described as a strategy which is used to make money from

the products and services selling on each scale in the market effectively. In respect to this,

manufacturing cost will be evaluated and aid in the price of products.

Transfer price: In transfer price, the price division of an organisation transact with each other

for an example, labour between trade of suppliers and departments effectively. This will help

managers to manage and control the cost of products under the budget which leads towards

increasing profitability.

TASK 4

P5

Financial activities are the most important part for any organisation in order to manage

the different resources under the budget which helps to increase the profitability and

manufacturing. This will also help to reduce extra expenses which increase the cash in the firm

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.