Report on Management Accounting Unit 5 (L02) Cost Analysis

VerifiedAdded on 2022/12/15

|14

|1550

|433

Report

AI Summary

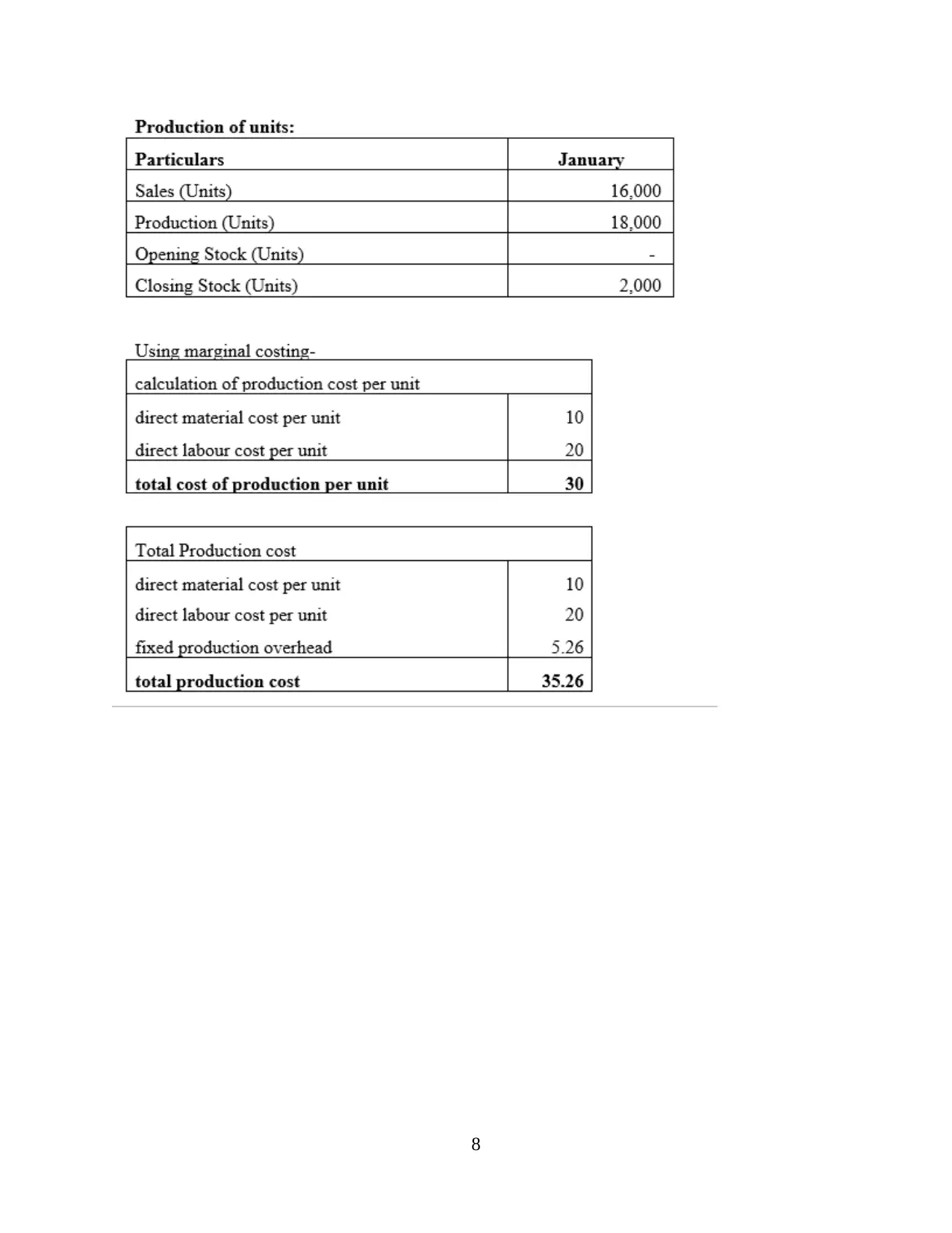

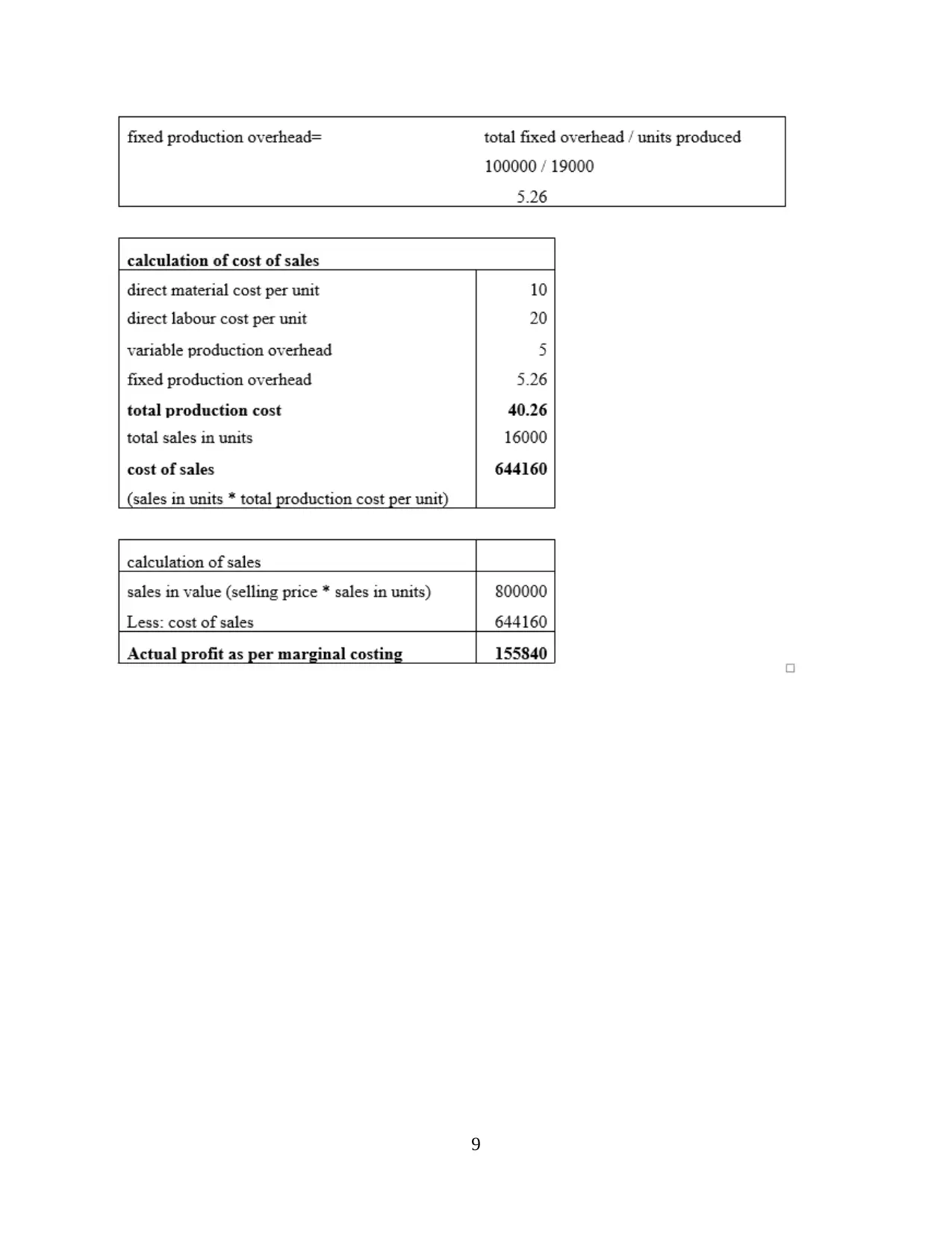

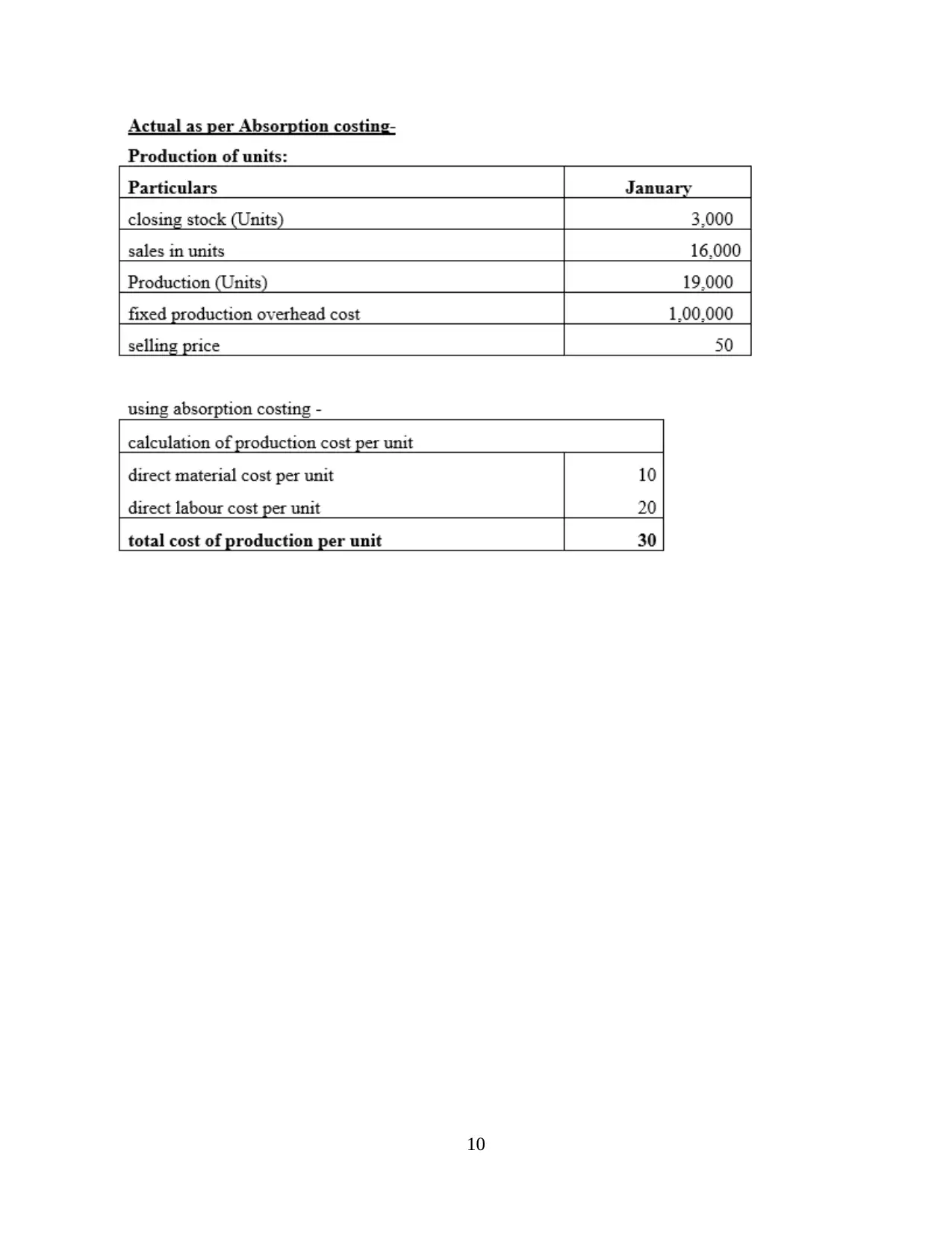

This report provides a comprehensive overview of management accounting, specifically focusing on Unit 5 (L02). It explores microeconomic techniques such as cost analysis, cost-volume-profit analysis, flexible budgeting, and cost variances. The report delves into product costing, including absorption costing and marginal costing, and examines fixed and variable costs, cost allocation, and normal and standard costing. Furthermore, it addresses the cost of inventory, covering definitions, types of costs, inventory valuation methods (FIFO, LIFO, weighted average), and the benefits of reducing inventory costs. The document also includes references to books and journals related to management accounting. The report emphasizes the importance of cost data in setting prices and provides a detailed analysis of various costing methods and their applications in business operations.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.