Management Accounting Assignment: Value Chain & Budgeting

VerifiedAdded on 2022/12/28

|16

|3320

|24

Homework Assignment

AI Summary

This assignment delves into the core principles of management accounting, focusing on value chain analysis and budgeting techniques. The first part of the assignment examines the value chain concept within the context of Sydney Ferries, an Australian transportation service, analyzing its competitive strategies such as cost leadership and differentiation. It identifies the key stages of the value chain, including inbound and outbound logistics, and marketing. The second part focuses on Takulah company, preparing a comprehensive master budget for the third quarter ending September. This includes sales, production, direct materials, direct labor, manufacturing overhead, finished goods inventory, and selling and administrative expenses budgets. The assignment also covers expected cash collections, providing a detailed overview of planning and controlling business operations through financial forecasting and analysis.

MANAGEMENT

ACCOUNTING BACHELOR

OF PROFESSIONAL

ACCOUNTING

ACCOUNTING BACHELOR

OF PROFESSIONAL

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question: 1...................................................................................................................................3

Question: 2...................................................................................................................................6

CONCLUSION..............................................................................................................................13

REFERENCES............................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question: 1...................................................................................................................................3

Question: 2...................................................................................................................................6

CONCLUSION..............................................................................................................................13

REFERENCES............................................................................................................................1

INTRODUCTION

The concept of management accounting refers to the responsibilities of management accountant,

which involves planning and controlling business activities and then making wise decisions for

efficiently and effectively achieving the organizational goals (Schwartz, 2016). Management

accounting is one of the division of accounting which involves measurement, analysing,

interpretation and informing managers about business status to the concerned managers with the

help of preparation of various budgets and reports relation to various business activity. The

present report has two parts where first part is based on value chain concept with reference to

Australian service organization, that is, Sydney ferries which is an Australian based

transportation service network. The second part of this report is based on budget preparation for

the third quarter ending 30th September for Takulah company in order to plan and control their

business operations.

MAIN BODY

Question: 1

a) Value chain is an important concept in every manufacturing and service organization which

indicated a comprehensive range of activities that is being performed for producing a unit of

product or delivering service (Zamora, 2016). It is referred to as value chain because the set of

activities so undertaken are meant for adding value to the product or service. By performing each

and every activity of the value chain, a producer can enhance its product's value. As per Michael

Porter's value chain analysis, there are five stages in value creating chain, that is, inbound

logistics, operational activities, outbound logistics, sales and marketing activities and after sale

service.

Benefits of value chain

With the help of value chain, the overall production activities can be bifurcated into

various stages which helps in saving costs by identifying the most expensive activities of

producing products and services and taking steps for minimizing these costly affairs.

Through value chain, a producer can minimize wasteful activities and enhance

profitability by looking into its supply chain, and identifying ways for minimizing

wastages in order to achieve efficiency (Jaligot and et.al., 2016).

For example, when a company recognizes that their subsidiary can produce a product at

lower costs, then they may go for outsourcing the product to its subsidiary, where they

The concept of management accounting refers to the responsibilities of management accountant,

which involves planning and controlling business activities and then making wise decisions for

efficiently and effectively achieving the organizational goals (Schwartz, 2016). Management

accounting is one of the division of accounting which involves measurement, analysing,

interpretation and informing managers about business status to the concerned managers with the

help of preparation of various budgets and reports relation to various business activity. The

present report has two parts where first part is based on value chain concept with reference to

Australian service organization, that is, Sydney ferries which is an Australian based

transportation service network. The second part of this report is based on budget preparation for

the third quarter ending 30th September for Takulah company in order to plan and control their

business operations.

MAIN BODY

Question: 1

a) Value chain is an important concept in every manufacturing and service organization which

indicated a comprehensive range of activities that is being performed for producing a unit of

product or delivering service (Zamora, 2016). It is referred to as value chain because the set of

activities so undertaken are meant for adding value to the product or service. By performing each

and every activity of the value chain, a producer can enhance its product's value. As per Michael

Porter's value chain analysis, there are five stages in value creating chain, that is, inbound

logistics, operational activities, outbound logistics, sales and marketing activities and after sale

service.

Benefits of value chain

With the help of value chain, the overall production activities can be bifurcated into

various stages which helps in saving costs by identifying the most expensive activities of

producing products and services and taking steps for minimizing these costly affairs.

Through value chain, a producer can minimize wasteful activities and enhance

profitability by looking into its supply chain, and identifying ways for minimizing

wastages in order to achieve efficiency (Jaligot and et.al., 2016).

For example, when a company recognizes that their subsidiary can produce a product at

lower costs, then they may go for outsourcing the product to its subsidiary, where they

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

can avail products at lower costs and offer lower prices to customers, which is helpful in

getting competitive advantage in the market.

b)

i) Here in this report, the Australian service organization, that is, Sydney ferries, has been

chosen. It's operations are mainly into service sector. The network of Sydney ferries aims at

providing transport services over nine routes. It a public transportation services mainly serving

the citizens of Sydney.

ii) Sydney ferries has the following competitive strategy:

Cost leadership: It is the strategy of producing goods and delivering services with the

lowest possible costs. This lower cost is helpful in setting lower prices which results in

competitive advantage for a company by selling products and providing services at lower

price than its competitors (Hishe, Asfaw and Giday, 2016). In case of Sydney ferries,

they by serving large number passengers need at one point of time, are able to reduce

their overall operating costs and this reduction in operating costs leads to lower fares

charge from passengers.

Differentiation strategy: This strategy aims to differentiate the product or services from

that of competitor's offering. This strategy is effective in attracting large number of

customers through the element of unique feature of the product or service. Sydney ferries

has 31 Fleet or vessels operating in seven different classes which satisfies different

customers need in different manner (Mudambi and Puck, 2016). Their differentiating

strategy is to provide the best possible experiences at the affordable price to the

customers. The customers can avail trustworthy and safe services from them.

Focus strategy: this strategy aims at covering or focusing on a niche market by designing

and offering a product or service for specific group of customers. Under this strategy all

the efforts and resources are utilized for the particular segment of customers. Sydney

ferries is mainly targeting and focusing commuters and leisure travellers. Commuters are

those travelling for the purpose of education and work (Hishe, Asfaw and Giday, 2016).

Also, their niche segment according to geographical area, they are only focusing on the

citizens of Sydney.

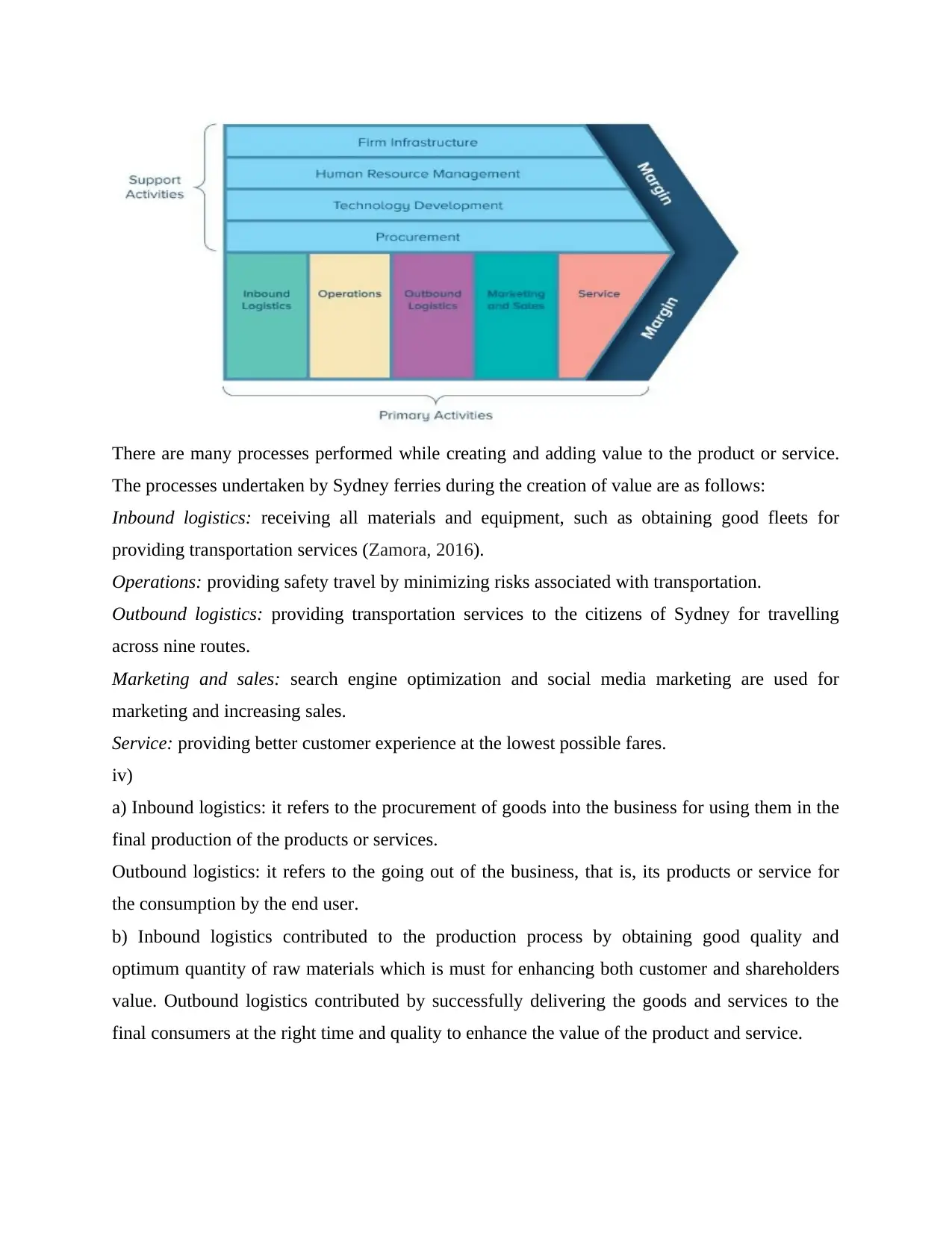

iii) Value chain model of Sydney ferries:

getting competitive advantage in the market.

b)

i) Here in this report, the Australian service organization, that is, Sydney ferries, has been

chosen. It's operations are mainly into service sector. The network of Sydney ferries aims at

providing transport services over nine routes. It a public transportation services mainly serving

the citizens of Sydney.

ii) Sydney ferries has the following competitive strategy:

Cost leadership: It is the strategy of producing goods and delivering services with the

lowest possible costs. This lower cost is helpful in setting lower prices which results in

competitive advantage for a company by selling products and providing services at lower

price than its competitors (Hishe, Asfaw and Giday, 2016). In case of Sydney ferries,

they by serving large number passengers need at one point of time, are able to reduce

their overall operating costs and this reduction in operating costs leads to lower fares

charge from passengers.

Differentiation strategy: This strategy aims to differentiate the product or services from

that of competitor's offering. This strategy is effective in attracting large number of

customers through the element of unique feature of the product or service. Sydney ferries

has 31 Fleet or vessels operating in seven different classes which satisfies different

customers need in different manner (Mudambi and Puck, 2016). Their differentiating

strategy is to provide the best possible experiences at the affordable price to the

customers. The customers can avail trustworthy and safe services from them.

Focus strategy: this strategy aims at covering or focusing on a niche market by designing

and offering a product or service for specific group of customers. Under this strategy all

the efforts and resources are utilized for the particular segment of customers. Sydney

ferries is mainly targeting and focusing commuters and leisure travellers. Commuters are

those travelling for the purpose of education and work (Hishe, Asfaw and Giday, 2016).

Also, their niche segment according to geographical area, they are only focusing on the

citizens of Sydney.

iii) Value chain model of Sydney ferries:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are many processes performed while creating and adding value to the product or service.

The processes undertaken by Sydney ferries during the creation of value are as follows:

Inbound logistics: receiving all materials and equipment, such as obtaining good fleets for

providing transportation services (Zamora, 2016).

Operations: providing safety travel by minimizing risks associated with transportation.

Outbound logistics: providing transportation services to the citizens of Sydney for travelling

across nine routes.

Marketing and sales: search engine optimization and social media marketing are used for

marketing and increasing sales.

Service: providing better customer experience at the lowest possible fares.

iv)

a) Inbound logistics: it refers to the procurement of goods into the business for using them in the

final production of the products or services.

Outbound logistics: it refers to the going out of the business, that is, its products or service for

the consumption by the end user.

b) Inbound logistics contributed to the production process by obtaining good quality and

optimum quantity of raw materials which is must for enhancing both customer and shareholders

value. Outbound logistics contributed by successfully delivering the goods and services to the

final consumers at the right time and quality to enhance the value of the product and service.

The processes undertaken by Sydney ferries during the creation of value are as follows:

Inbound logistics: receiving all materials and equipment, such as obtaining good fleets for

providing transportation services (Zamora, 2016).

Operations: providing safety travel by minimizing risks associated with transportation.

Outbound logistics: providing transportation services to the citizens of Sydney for travelling

across nine routes.

Marketing and sales: search engine optimization and social media marketing are used for

marketing and increasing sales.

Service: providing better customer experience at the lowest possible fares.

iv)

a) Inbound logistics: it refers to the procurement of goods into the business for using them in the

final production of the products or services.

Outbound logistics: it refers to the going out of the business, that is, its products or service for

the consumption by the end user.

b) Inbound logistics contributed to the production process by obtaining good quality and

optimum quantity of raw materials which is must for enhancing both customer and shareholders

value. Outbound logistics contributed by successfully delivering the goods and services to the

final consumers at the right time and quality to enhance the value of the product and service.

c) For inbound logistics, direct material budget is prepared on a monthly or quarterly basis and

submitted to finance manager while for outbound logistics, selling and distribution budget is

prepared on a quarterly basis and submitted to marketing manager.

Question: 2

1. Sales budget:A Sales budget is prepared to plan and forecast future expected sales revenue.

This is done to provide and make arrangements for important resources in order to meet these

sales figures without getting fail (Barr and McClellan, 2018). The forecasting of revenue from

sales is possible through proper estimation of demand for goods and services in the near future.

The business which successfully estimate and achieve and satisfy this demand can ensure its long

term sustainability and profitability. It helps in setting inventory levels, arranging Sales person in

order to maximize profits. Takulah's Sales budget for the third quarter of 2019 starting from July

till September are as follows:

Sales budget for the quarter ending 30th September 2019

S.

No.

Particulars July August September October November

1 Expected sales in

units

22000 50000 32000 26000 15000

2 Selling price per

unit

$15 $15 $15 $15 $15

3 Total sales $330000 $750000 $480000 $390000 $225000

Interpretation: Sales revenue of Takulah is increasing initially but from September it is

continuously decreasing.

2. Production budget: This budget is prepared to estimate the number of units to be produced so

that the expected sales can be achieved and resources for successfully achieving production

target can be provided in advance, so that the continuous manufacturing can be ensured (Rogelj

and et.al., 2016). This budget is prepared in alignment with Sales budget and desired level of

finished goods inventory in hand at the end of the period.

Production budget for the quarter ending 30th September 2019

S. Particulars July August Septemb October Novemb

submitted to finance manager while for outbound logistics, selling and distribution budget is

prepared on a quarterly basis and submitted to marketing manager.

Question: 2

1. Sales budget:A Sales budget is prepared to plan and forecast future expected sales revenue.

This is done to provide and make arrangements for important resources in order to meet these

sales figures without getting fail (Barr and McClellan, 2018). The forecasting of revenue from

sales is possible through proper estimation of demand for goods and services in the near future.

The business which successfully estimate and achieve and satisfy this demand can ensure its long

term sustainability and profitability. It helps in setting inventory levels, arranging Sales person in

order to maximize profits. Takulah's Sales budget for the third quarter of 2019 starting from July

till September are as follows:

Sales budget for the quarter ending 30th September 2019

S.

No.

Particulars July August September October November

1 Expected sales in

units

22000 50000 32000 26000 15000

2 Selling price per

unit

$15 $15 $15 $15 $15

3 Total sales $330000 $750000 $480000 $390000 $225000

Interpretation: Sales revenue of Takulah is increasing initially but from September it is

continuously decreasing.

2. Production budget: This budget is prepared to estimate the number of units to be produced so

that the expected sales can be achieved and resources for successfully achieving production

target can be provided in advance, so that the continuous manufacturing can be ensured (Rogelj

and et.al., 2016). This budget is prepared in alignment with Sales budget and desired level of

finished goods inventory in hand at the end of the period.

Production budget for the quarter ending 30th September 2019

S. Particulars July August Septemb October Novemb

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

No. er er

1 Forecasted sales revenue 22000 50000 32000 26000 15000

2 Planned ending Finished Goods

Inventory (25% of succeeding

month's budgeted sales)

50000 *

25%

=12500

32000 *

25%

=8000

26000 *

25%

=6500

15000 *

25%

=3750

3 Total required production (1+2) 34500 58000 38500 29750

4 Less: opening finished goods

inventory

- -12500 -8000 -6500

5 Total units to be manufactured 34500 45500 30500 23250

3. Direct Material Budget: This budget is prepared for the particular period in order to estimate

the required quantity of direct material for successfully carrying out production of units as per

production budget (Chiu and et.al., 2018). It indicates per unit requirement of material along with

the total cost of direct material. It helps also in providing for desired inventory of materials in

hand at the end of each period under consideration.

Direct Materials budgets

S.

No.

Particulars July August September October

1 Units to be manufactured as

per production budget

34500 45500 30500 23250

2 Direct material per unit 5 pounds 5 pounds 5 pounds 5 pounds

3 Direct material required for

production

172500 227500 152500 116250

4 Add: direct material on hand

at the end of each month

(15% of succeeding month's

production)

227500 *

15%

=34125

152500 *

15%

=22875

116250 * 15%

=17438

5 Less: direct material at the - -34125 -22875

1 Forecasted sales revenue 22000 50000 32000 26000 15000

2 Planned ending Finished Goods

Inventory (25% of succeeding

month's budgeted sales)

50000 *

25%

=12500

32000 *

25%

=8000

26000 *

25%

=6500

15000 *

25%

=3750

3 Total required production (1+2) 34500 58000 38500 29750

4 Less: opening finished goods

inventory

- -12500 -8000 -6500

5 Total units to be manufactured 34500 45500 30500 23250

3. Direct Material Budget: This budget is prepared for the particular period in order to estimate

the required quantity of direct material for successfully carrying out production of units as per

production budget (Chiu and et.al., 2018). It indicates per unit requirement of material along with

the total cost of direct material. It helps also in providing for desired inventory of materials in

hand at the end of each period under consideration.

Direct Materials budgets

S.

No.

Particulars July August September October

1 Units to be manufactured as

per production budget

34500 45500 30500 23250

2 Direct material per unit 5 pounds 5 pounds 5 pounds 5 pounds

3 Direct material required for

production

172500 227500 152500 116250

4 Add: direct material on hand

at the end of each month

(15% of succeeding month's

production)

227500 *

15%

=34125

152500 *

15%

=22875

116250 * 15%

=17438

5 Less: direct material at the - -34125 -22875

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

beginning of each month

6 Required purchase of direct

material in pounds (3+4-5)

206625 216250 147063

7 Material cost per pound $0.5 $0.5 $0.5

8 Total Direct material cost $103313 $108125 $73532

4. Direct labour budget: The purpose of this budget is to identify the number of hour required

for manufacturing units as per the production budget by multiplying the per unit time required

with the total number of budgeted production units. Then number of hours are multiplied with

the per hour cost pertaining to labours in order to estimate the total cost related to direct labour.

Direct labour Budget

S. No. Particulars July August September

1 Budgeted units of production 34500 45500 30500

2 Per unit requirement of

labour hour

0.06 0.06 0.06

3 Production labour hour 2070 2730 1830

4 Per hour rate of labour $15 $15 $15

5 Total cost pertaining to

labour hour

$31050 $40950 $27450

*As the total worked labour hour is less than the minimum required hour, that is 2000 hour per

month, but the calculation is done for September just to support the master budget.

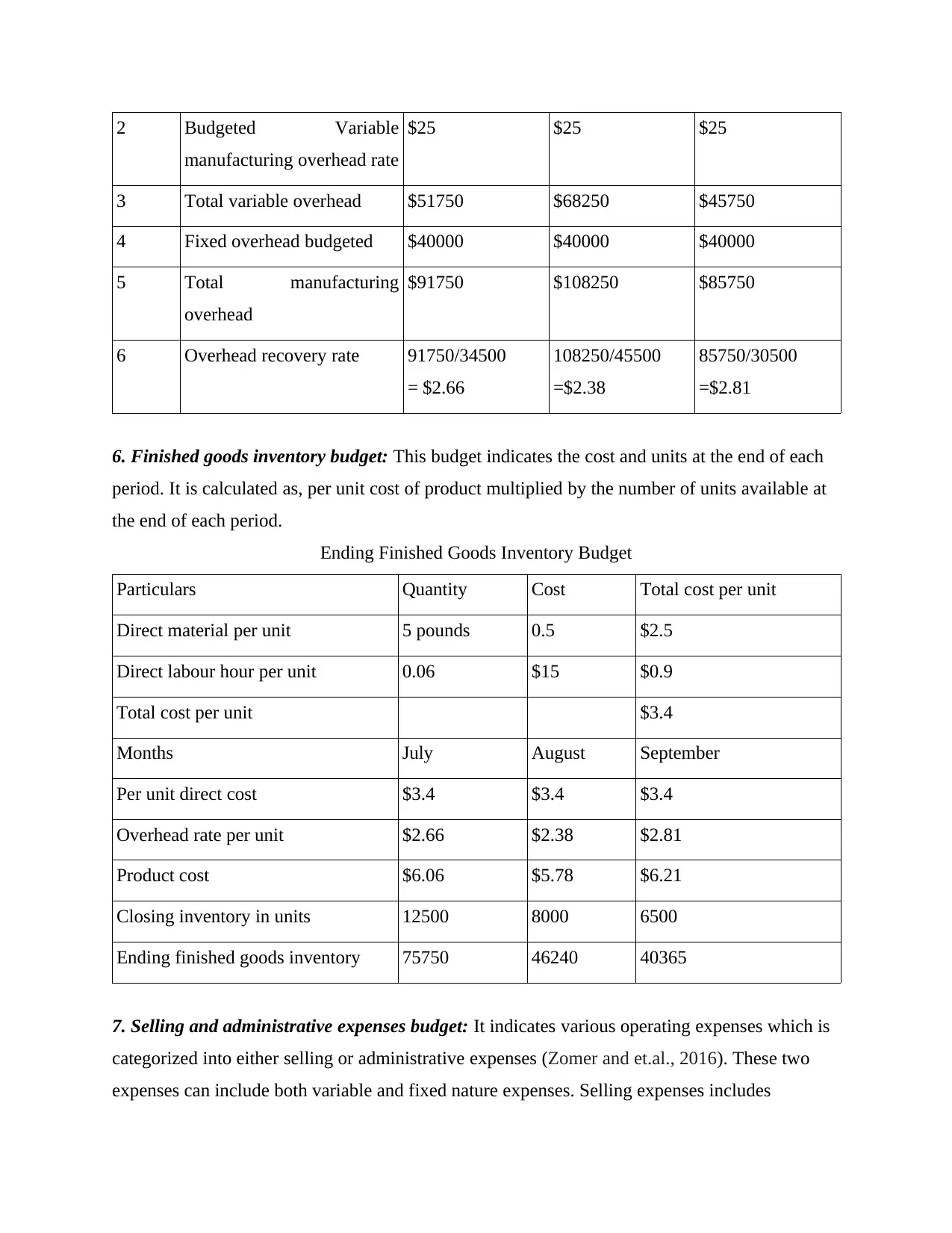

5. Manufacturing overhead budget: A budget is prepared to estimate the cost of production

which will be incurred by the producer in manufacturing units. The cost of direct

materials and direct labour are not taken into consideration here. It involves rental

expenses, machine related expenses, supplies, wages and insurance.

Manufacturing Overhead Budget

S. No. Particulars July August September

1 Budgeted Labour hours 2070 2730 1830

6 Required purchase of direct

material in pounds (3+4-5)

206625 216250 147063

7 Material cost per pound $0.5 $0.5 $0.5

8 Total Direct material cost $103313 $108125 $73532

4. Direct labour budget: The purpose of this budget is to identify the number of hour required

for manufacturing units as per the production budget by multiplying the per unit time required

with the total number of budgeted production units. Then number of hours are multiplied with

the per hour cost pertaining to labours in order to estimate the total cost related to direct labour.

Direct labour Budget

S. No. Particulars July August September

1 Budgeted units of production 34500 45500 30500

2 Per unit requirement of

labour hour

0.06 0.06 0.06

3 Production labour hour 2070 2730 1830

4 Per hour rate of labour $15 $15 $15

5 Total cost pertaining to

labour hour

$31050 $40950 $27450

*As the total worked labour hour is less than the minimum required hour, that is 2000 hour per

month, but the calculation is done for September just to support the master budget.

5. Manufacturing overhead budget: A budget is prepared to estimate the cost of production

which will be incurred by the producer in manufacturing units. The cost of direct

materials and direct labour are not taken into consideration here. It involves rental

expenses, machine related expenses, supplies, wages and insurance.

Manufacturing Overhead Budget

S. No. Particulars July August September

1 Budgeted Labour hours 2070 2730 1830

2 Budgeted Variable

manufacturing overhead rate

$25 $25 $25

3 Total variable overhead $51750 $68250 $45750

4 Fixed overhead budgeted $40000 $40000 $40000

5 Total manufacturing

overhead

$91750 $108250 $85750

6 Overhead recovery rate 91750/34500

= $2.66

108250/45500

=$2.38

85750/30500

=$2.81

6. Finished goods inventory budget: This budget indicates the cost and units at the end of each

period. It is calculated as, per unit cost of product multiplied by the number of units available at

the end of each period.

Ending Finished Goods Inventory Budget

Particulars Quantity Cost Total cost per unit

Direct material per unit 5 pounds 0.5 $2.5

Direct labour hour per unit 0.06 $15 $0.9

Total cost per unit $3.4

Months July August September

Per unit direct cost $3.4 $3.4 $3.4

Overhead rate per unit $2.66 $2.38 $2.81

Product cost $6.06 $5.78 $6.21

Closing inventory in units 12500 8000 6500

Ending finished goods inventory 75750 46240 40365

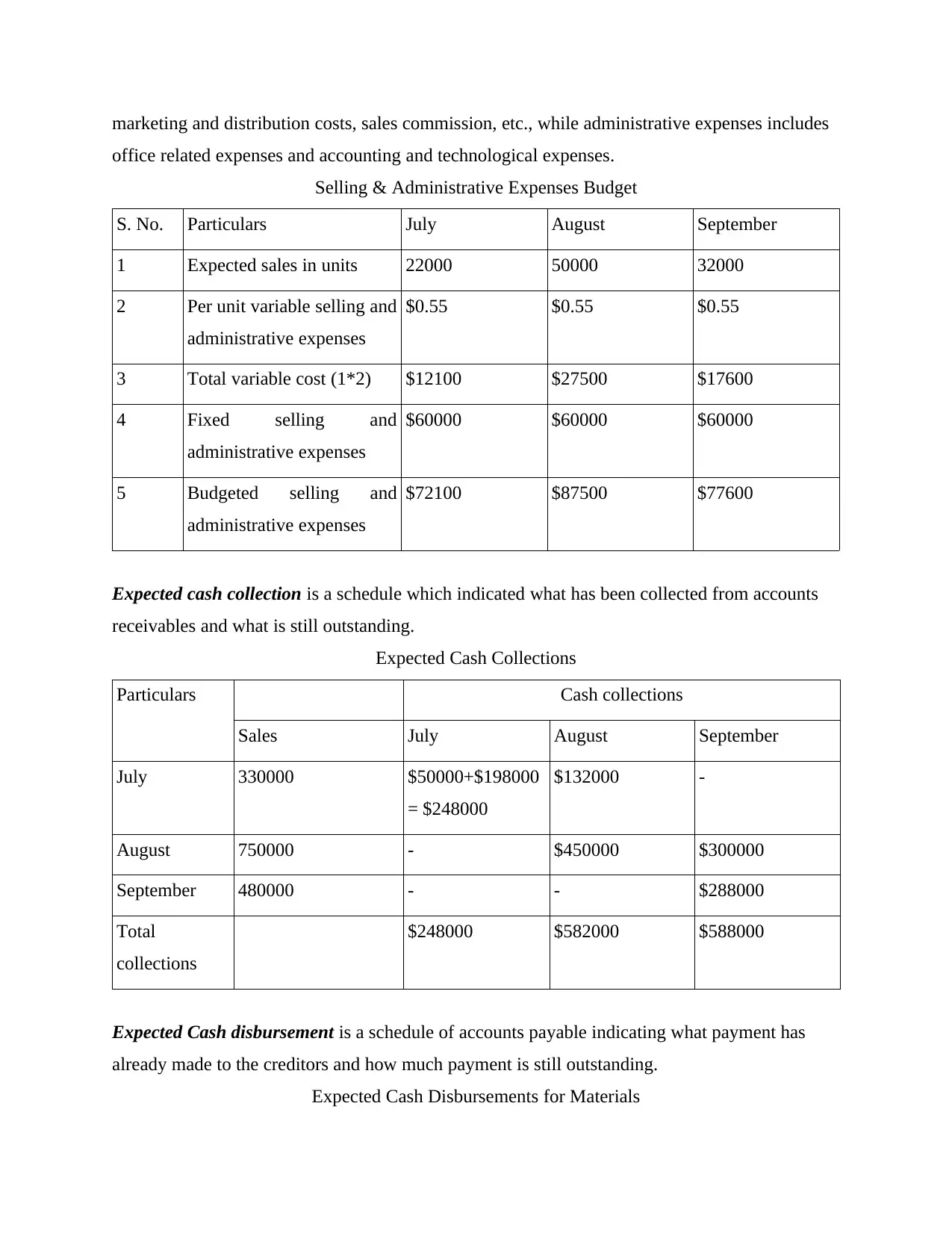

7. Selling and administrative expenses budget: It indicates various operating expenses which is

categorized into either selling or administrative expenses (Zomer and et.al., 2016). These two

expenses can include both variable and fixed nature expenses. Selling expenses includes

manufacturing overhead rate

$25 $25 $25

3 Total variable overhead $51750 $68250 $45750

4 Fixed overhead budgeted $40000 $40000 $40000

5 Total manufacturing

overhead

$91750 $108250 $85750

6 Overhead recovery rate 91750/34500

= $2.66

108250/45500

=$2.38

85750/30500

=$2.81

6. Finished goods inventory budget: This budget indicates the cost and units at the end of each

period. It is calculated as, per unit cost of product multiplied by the number of units available at

the end of each period.

Ending Finished Goods Inventory Budget

Particulars Quantity Cost Total cost per unit

Direct material per unit 5 pounds 0.5 $2.5

Direct labour hour per unit 0.06 $15 $0.9

Total cost per unit $3.4

Months July August September

Per unit direct cost $3.4 $3.4 $3.4

Overhead rate per unit $2.66 $2.38 $2.81

Product cost $6.06 $5.78 $6.21

Closing inventory in units 12500 8000 6500

Ending finished goods inventory 75750 46240 40365

7. Selling and administrative expenses budget: It indicates various operating expenses which is

categorized into either selling or administrative expenses (Zomer and et.al., 2016). These two

expenses can include both variable and fixed nature expenses. Selling expenses includes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

marketing and distribution costs, sales commission, etc., while administrative expenses includes

office related expenses and accounting and technological expenses.

Selling & Administrative Expenses Budget

S. No. Particulars July August September

1 Expected sales in units 22000 50000 32000

2 Per unit variable selling and

administrative expenses

$0.55 $0.55 $0.55

3 Total variable cost (1*2) $12100 $27500 $17600

4 Fixed selling and

administrative expenses

$60000 $60000 $60000

5 Budgeted selling and

administrative expenses

$72100 $87500 $77600

Expected cash collection is a schedule which indicated what has been collected from accounts

receivables and what is still outstanding.

Expected Cash Collections

Particulars Cash collections

Sales July August September

July 330000 $50000+$198000

= $248000

$132000 -

August 750000 - $450000 $300000

September 480000 - - $288000

Total

collections

$248000 $582000 $588000

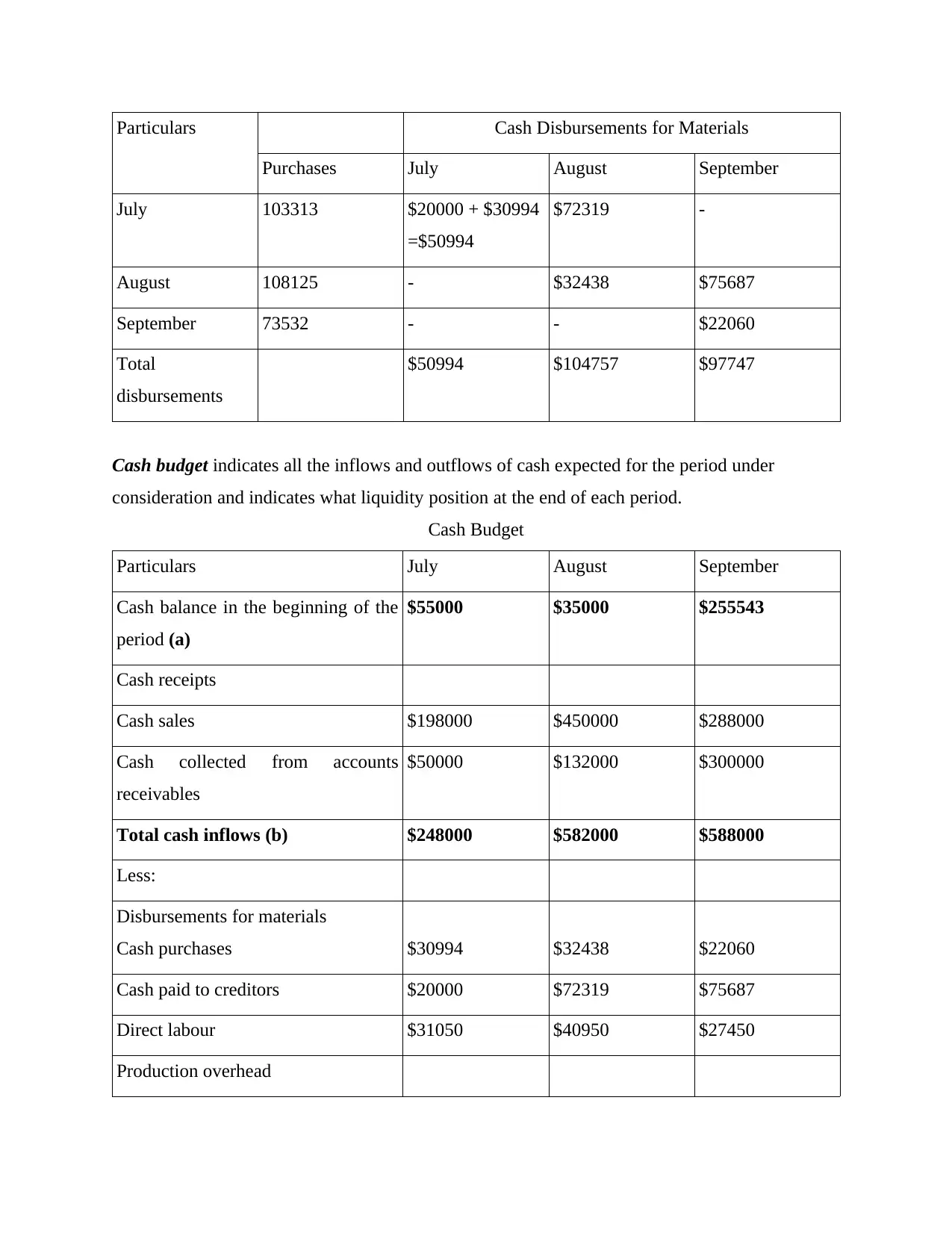

Expected Cash disbursement is a schedule of accounts payable indicating what payment has

already made to the creditors and how much payment is still outstanding.

Expected Cash Disbursements for Materials

office related expenses and accounting and technological expenses.

Selling & Administrative Expenses Budget

S. No. Particulars July August September

1 Expected sales in units 22000 50000 32000

2 Per unit variable selling and

administrative expenses

$0.55 $0.55 $0.55

3 Total variable cost (1*2) $12100 $27500 $17600

4 Fixed selling and

administrative expenses

$60000 $60000 $60000

5 Budgeted selling and

administrative expenses

$72100 $87500 $77600

Expected cash collection is a schedule which indicated what has been collected from accounts

receivables and what is still outstanding.

Expected Cash Collections

Particulars Cash collections

Sales July August September

July 330000 $50000+$198000

= $248000

$132000 -

August 750000 - $450000 $300000

September 480000 - - $288000

Total

collections

$248000 $582000 $588000

Expected Cash disbursement is a schedule of accounts payable indicating what payment has

already made to the creditors and how much payment is still outstanding.

Expected Cash Disbursements for Materials

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Cash Disbursements for Materials

Purchases July August September

July 103313 $20000 + $30994

=$50994

$72319 -

August 108125 - $32438 $75687

September 73532 - - $22060

Total

disbursements

$50994 $104757 $97747

Cash budget indicates all the inflows and outflows of cash expected for the period under

consideration and indicates what liquidity position at the end of each period.

Cash Budget

Particulars July August September

Cash balance in the beginning of the

period (a)

$55000 $35000 $255543

Cash receipts

Cash sales $198000 $450000 $288000

Cash collected from accounts

receivables

$50000 $132000 $300000

Total cash inflows (b) $248000 $582000 $588000

Less:

Disbursements for materials

Cash purchases $30994 $32438 $22060

Cash paid to creditors $20000 $72319 $75687

Direct labour $31050 $40950 $27450

Production overhead

Purchases July August September

July 103313 $20000 + $30994

=$50994

$72319 -

August 108125 - $32438 $75687

September 73532 - - $22060

Total

disbursements

$50994 $104757 $97747

Cash budget indicates all the inflows and outflows of cash expected for the period under

consideration and indicates what liquidity position at the end of each period.

Cash Budget

Particulars July August September

Cash balance in the beginning of the

period (a)

$55000 $35000 $255543

Cash receipts

Cash sales $198000 $450000 $288000

Cash collected from accounts

receivables

$50000 $132000 $300000

Total cash inflows (b) $248000 $582000 $588000

Less:

Disbursements for materials

Cash purchases $30994 $32438 $22060

Cash paid to creditors $20000 $72319 $75687

Direct labour $31050 $40950 $27450

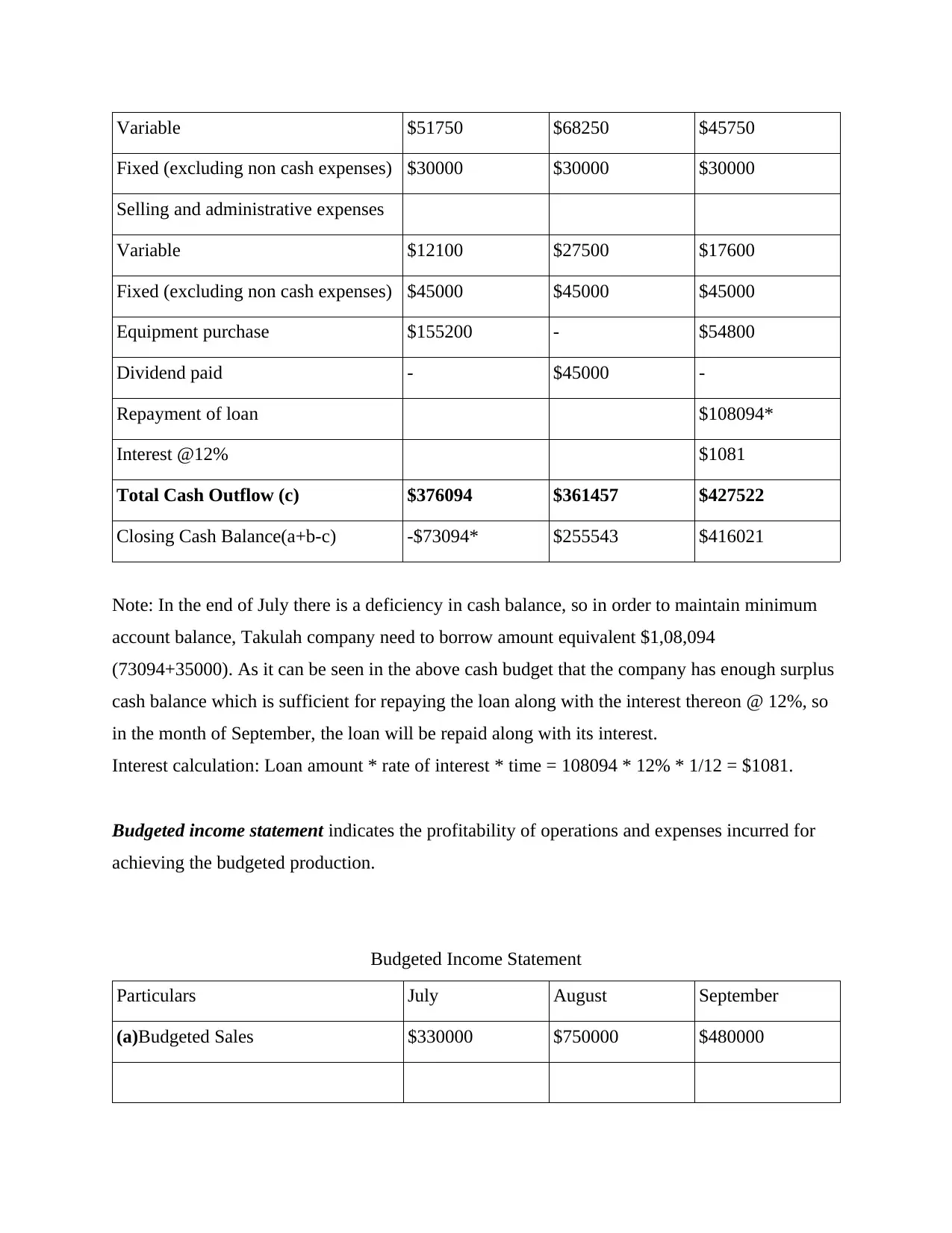

Production overhead

Variable $51750 $68250 $45750

Fixed (excluding non cash expenses) $30000 $30000 $30000

Selling and administrative expenses

Variable $12100 $27500 $17600

Fixed (excluding non cash expenses) $45000 $45000 $45000

Equipment purchase $155200 - $54800

Dividend paid - $45000 -

Repayment of loan $108094*

Interest @12% $1081

Total Cash Outflow (c) $376094 $361457 $427522

Closing Cash Balance(a+b-c) -$73094* $255543 $416021

Note: In the end of July there is a deficiency in cash balance, so in order to maintain minimum

account balance, Takulah company need to borrow amount equivalent $1,08,094

(73094+35000). As it can be seen in the above cash budget that the company has enough surplus

cash balance which is sufficient for repaying the loan along with the interest thereon @ 12%, so

in the month of September, the loan will be repaid along with its interest.

Interest calculation: Loan amount * rate of interest * time = 108094 * 12% * 1/12 = $1081.

Budgeted income statement indicates the profitability of operations and expenses incurred for

achieving the budgeted production.

Budgeted Income Statement

Particulars July August September

(a)Budgeted Sales $330000 $750000 $480000

Fixed (excluding non cash expenses) $30000 $30000 $30000

Selling and administrative expenses

Variable $12100 $27500 $17600

Fixed (excluding non cash expenses) $45000 $45000 $45000

Equipment purchase $155200 - $54800

Dividend paid - $45000 -

Repayment of loan $108094*

Interest @12% $1081

Total Cash Outflow (c) $376094 $361457 $427522

Closing Cash Balance(a+b-c) -$73094* $255543 $416021

Note: In the end of July there is a deficiency in cash balance, so in order to maintain minimum

account balance, Takulah company need to borrow amount equivalent $1,08,094

(73094+35000). As it can be seen in the above cash budget that the company has enough surplus

cash balance which is sufficient for repaying the loan along with the interest thereon @ 12%, so

in the month of September, the loan will be repaid along with its interest.

Interest calculation: Loan amount * rate of interest * time = 108094 * 12% * 1/12 = $1081.

Budgeted income statement indicates the profitability of operations and expenses incurred for

achieving the budgeted production.

Budgeted Income Statement

Particulars July August September

(a)Budgeted Sales $330000 $750000 $480000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.