Management Accounting Assignment: Value Chain and Costing

VerifiedAdded on 2023/01/18

|11

|1447

|85

Homework Assignment

AI Summary

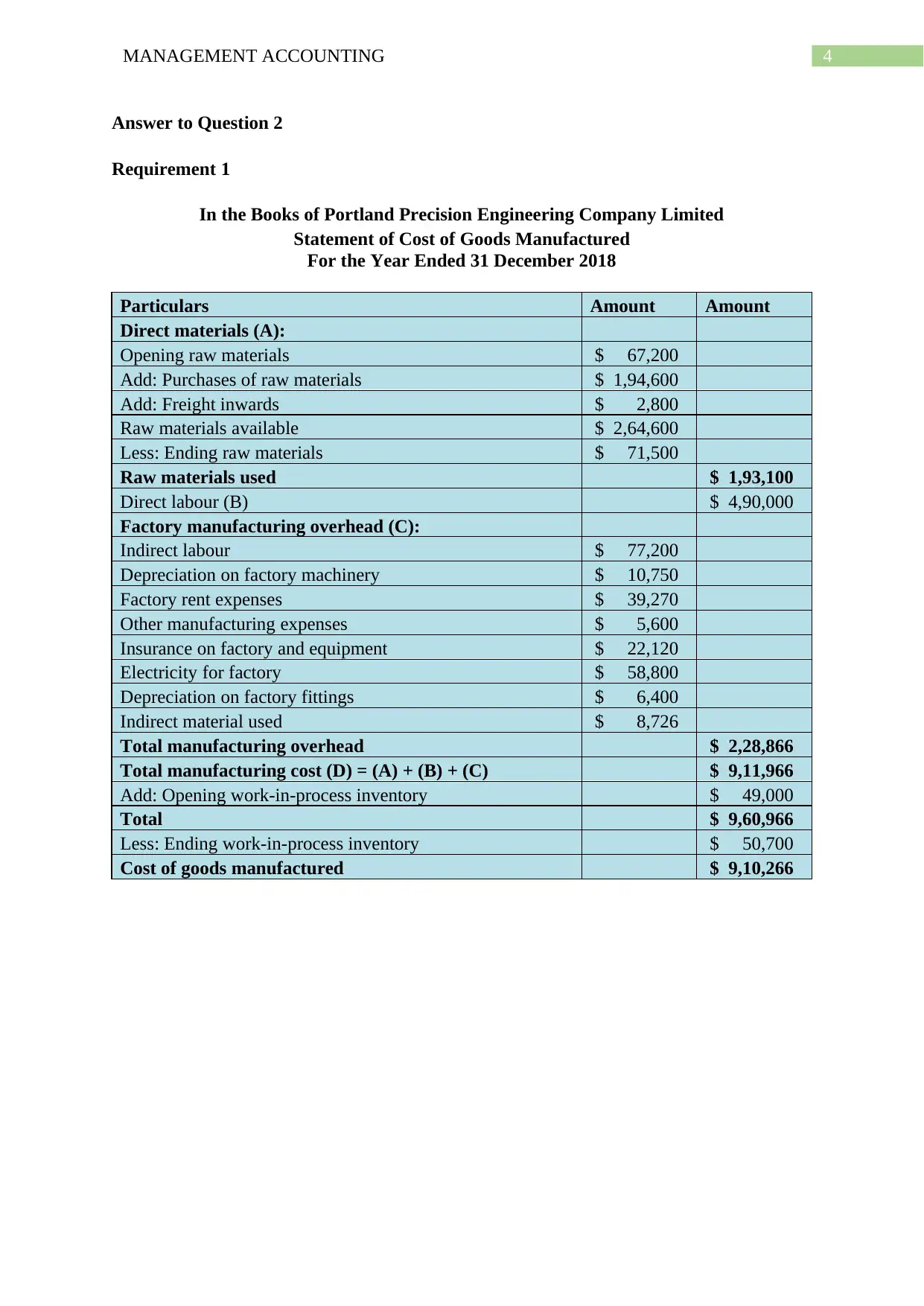

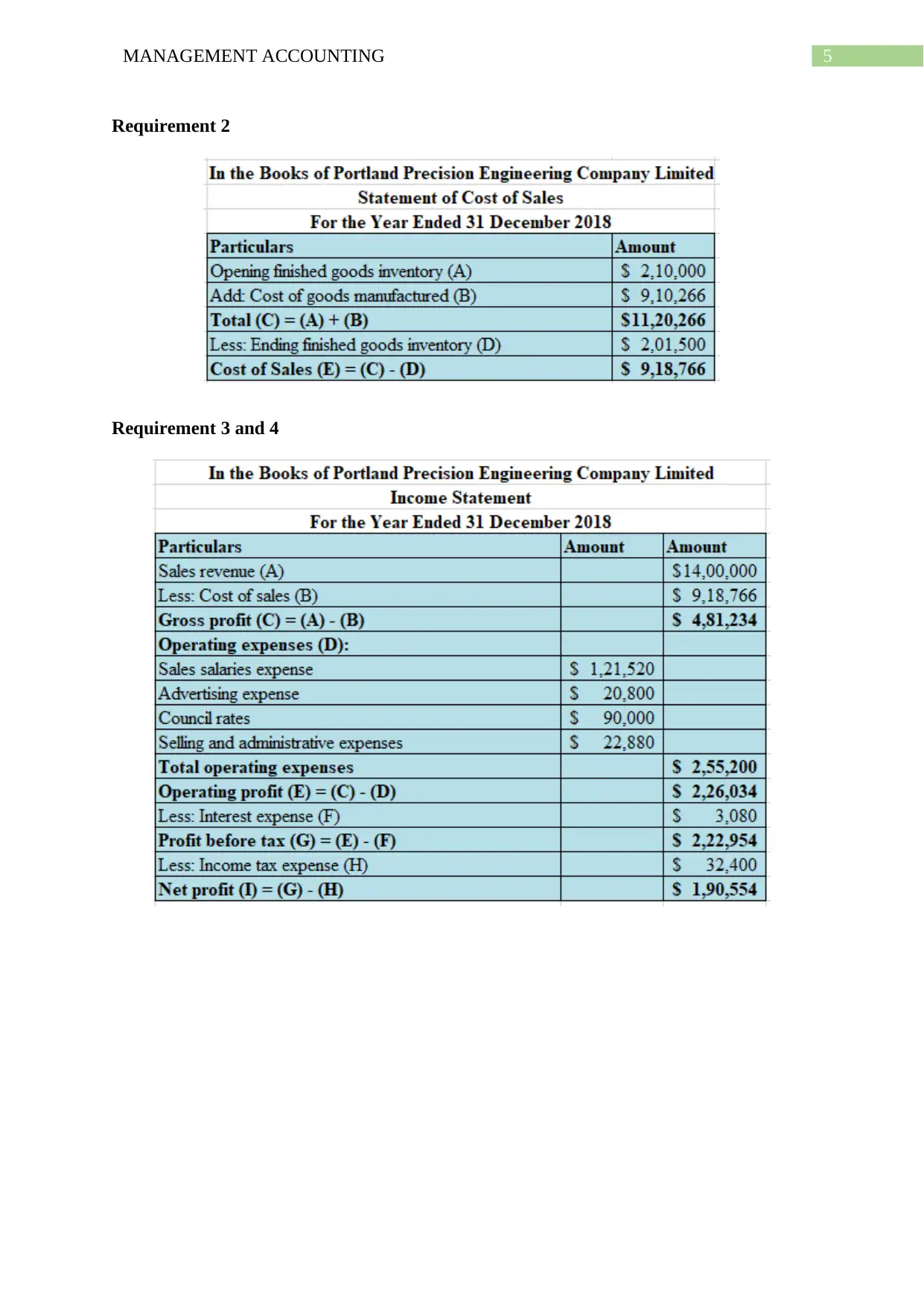

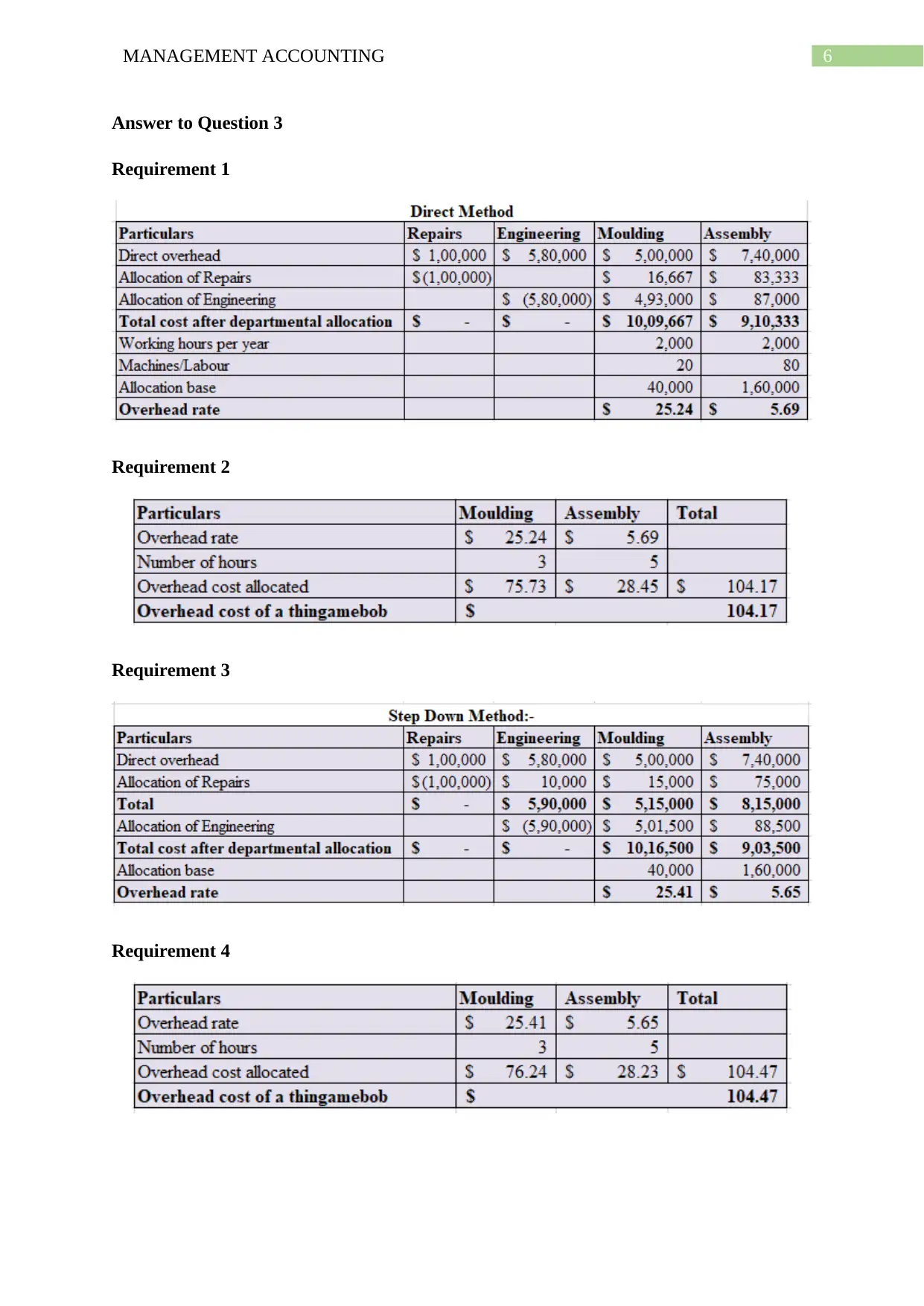

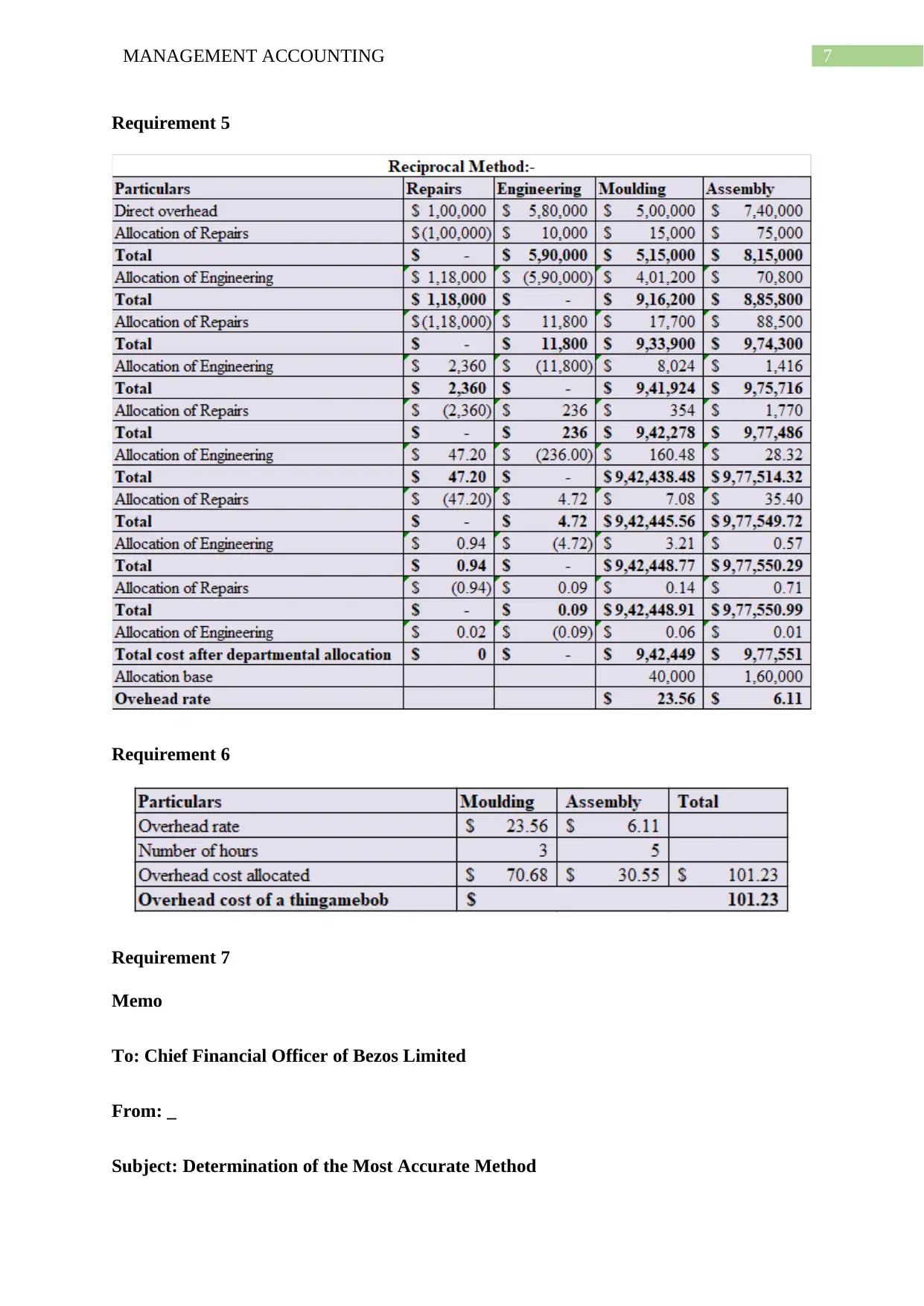

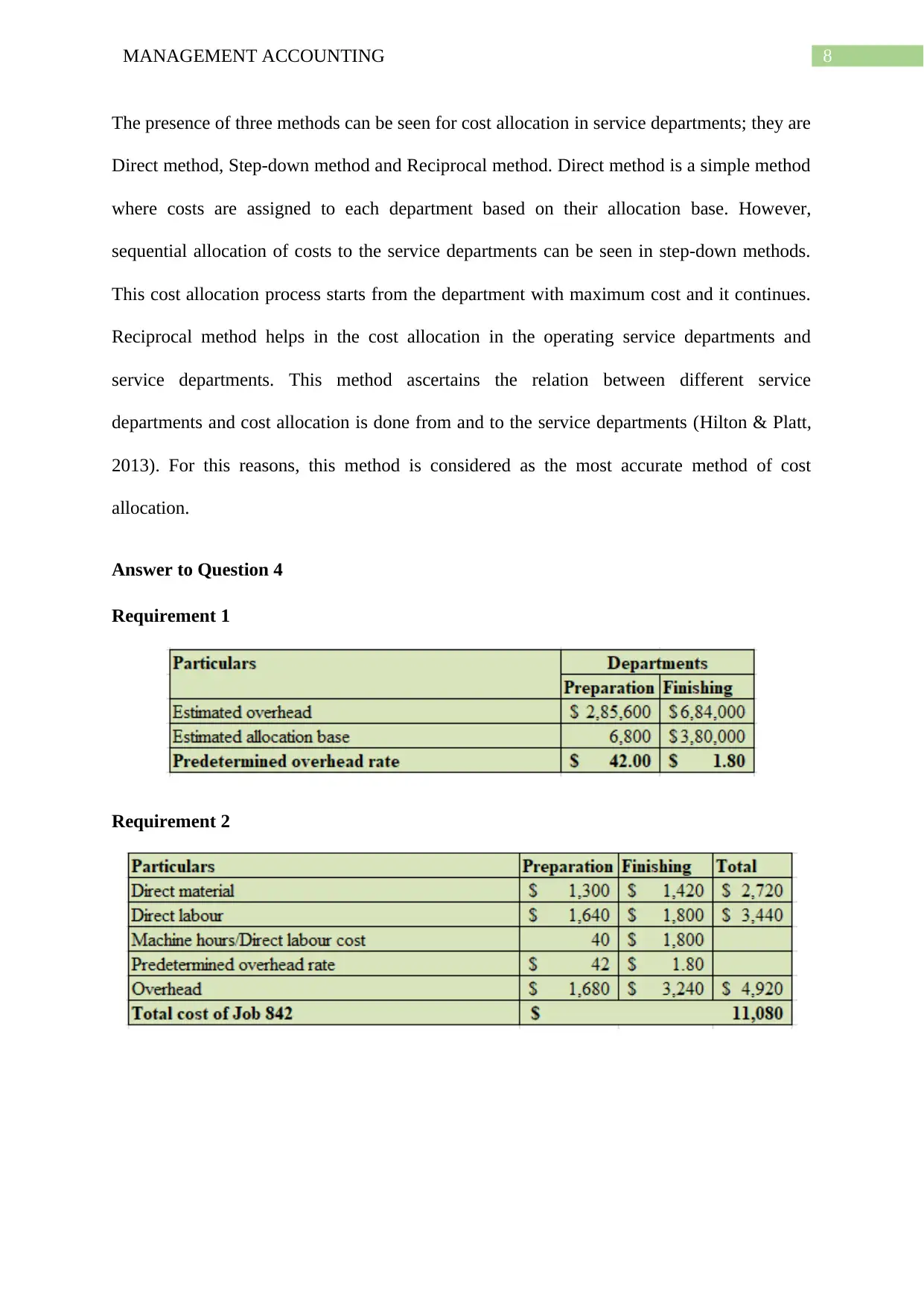

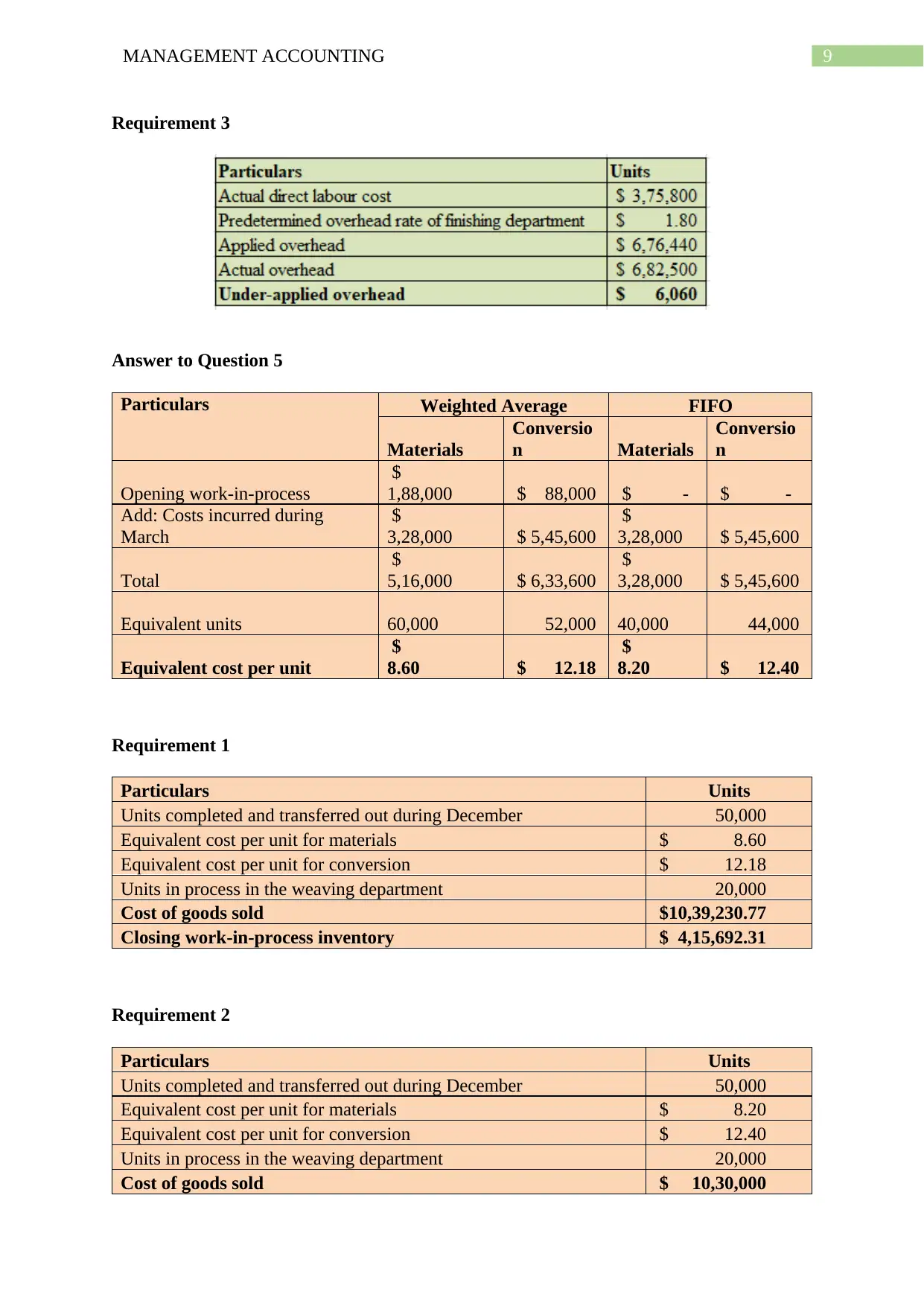

This management accounting assignment solution encompasses several key areas of the subject. It begins with a value chain analysis of BHP Billiton, examining its primary and secondary activities to identify management accounting issues and improve operational efficiency. The solution then presents a detailed cost of goods manufactured statement for Portland Precision Engineering Company Limited, calculating the cost of sales, gross profit, and net profit. Following this, the assignment addresses cost allocation methods, comparing the direct, step-down, and reciprocal methods and justifying the selection of the most accurate method. The solution further explores cost accounting concepts, including weighted average and FIFO methods, by calculating equivalent units and equivalent cost per unit, and preparing the cost of goods sold and closing work-in-process inventory. The assignment includes several requirements, from preparing financial statements to determining the most appropriate cost allocation method. The provided solution is comprehensive and offers insights into various aspects of management accounting.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.