Management Accounting Report: Financial Analysis of Volkswagen

VerifiedAdded on 2023/01/18

|19

|5883

|56

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Volkswagen. It begins with an introduction to management accounting, its differences from financial accounting, and various management accounting systems such as inventory management, price optimization, cost accounting, and job costing. The report then explores the role of management accounting in effective control and planning. Different methods of management accounting reporting are discussed, including budget reports, cost managerial accounting reports, and performance reports. The report also delves into cost analysis techniques, including marginal and absorption costing, and examines the application of these techniques to financial reports. The report further explores planning tools used in budgetary control and analyzes how organizations like Volkswagen adapt management accounting systems to respond to financial problems and achieve sustainable success. The report provides a detailed overview of the accounting practices and financial strategies adopted by Volkswagen.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................4

Management accounting and different types of management accounting systems....................4

Different methods which are used for management accounting reporting.................................6

The benefits of management accounting systems and their application within the company....7

How management accounting systems and management accounting reporting is integrated

with organisational processes......................................................................................................8

LO 2.................................................................................................................................................8

Calculation of costs by using effective techniques of cost analysis............................................8

Management accounting techniques and financial reports.........................................................9

Financial reports that accurately apply and interpret the data for several business activities...10

LO 3...............................................................................................................................................10

Advantages and disadvantages of different types of planning tools used in budgetary control

...................................................................................................................................................10

Analyse the use of different planning tools and their application for preparing and forecasting

budgets......................................................................................................................................12

LO 4...............................................................................................................................................12

Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success..........................................................................................15

Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success............................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................4

Management accounting and different types of management accounting systems....................4

Different methods which are used for management accounting reporting.................................6

The benefits of management accounting systems and their application within the company....7

How management accounting systems and management accounting reporting is integrated

with organisational processes......................................................................................................8

LO 2.................................................................................................................................................8

Calculation of costs by using effective techniques of cost analysis............................................8

Management accounting techniques and financial reports.........................................................9

Financial reports that accurately apply and interpret the data for several business activities...10

LO 3...............................................................................................................................................10

Advantages and disadvantages of different types of planning tools used in budgetary control

...................................................................................................................................................10

Analyse the use of different planning tools and their application for preparing and forecasting

budgets......................................................................................................................................12

LO 4...............................................................................................................................................12

Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................12

Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success..........................................................................................15

Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success............................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting refers to the procedure of presenting accountancy data in order

to design the plans and policies which is adopted by the administration to operate its day to day

activities. It can be an activity of planning, organising, staffing, directing and dominant the fiscal

actionas of the business concern of the firm. It is essential to the administrator of the

organization to maintain the fiscal data and information and also assist in decision making

process. It is different form financial accounting because it will be prepared fro internal

stakeholders. Managerial accounting embrace many facets of account purpose at improving the

attribute of data which is delivered to management accounting about business concern trading

operations metrics (Alsharari, Dixon and Youssef, 2015). This report is based on Volkswagen

which is a German auto-maker and operate its business internationally. This firm was established

in 1937 and headquartered in Wolfsburg, Germany and operate its business in Automotive

industry. This assignment will discuss about management accounting and requirements of

different types of management accounting systems. Further, will discuss about different methods

of management accounting reporting, management accounting methods and proper financial

reporting documents. Advantages and disadvantages of various kind of designing tools that are

used in budgetary control and comparison of organisation which adopt management accounting

system to react to fiscal problems.

LO 1

Management accounting and different types of management accounting systems

Management accounting is a kind of accountancy which is helpful for the administrators

of the organisation to support the to manage the financial activities of the organisation in an

efficacious and efficient way and also support in the activity of determination devising in

different situations. In Volkswagen, the accounting financial manager manager of the company

can use it in manage the financial action like cost invest in manufacturing and others or have the

proper information of the finance which are invested by the company (Bennett and James, 2017).

There are number of accounting system which can be used by the firm in managing the finance

and decision making regarding it. Some of them are defined as beneath:

Inventory management system- In this system, the inventory of the organisations are

negotiated in an appropriate way. In addition to it, it traces the cost which which generates due to

Management accounting refers to the procedure of presenting accountancy data in order

to design the plans and policies which is adopted by the administration to operate its day to day

activities. It can be an activity of planning, organising, staffing, directing and dominant the fiscal

actionas of the business concern of the firm. It is essential to the administrator of the

organization to maintain the fiscal data and information and also assist in decision making

process. It is different form financial accounting because it will be prepared fro internal

stakeholders. Managerial accounting embrace many facets of account purpose at improving the

attribute of data which is delivered to management accounting about business concern trading

operations metrics (Alsharari, Dixon and Youssef, 2015). This report is based on Volkswagen

which is a German auto-maker and operate its business internationally. This firm was established

in 1937 and headquartered in Wolfsburg, Germany and operate its business in Automotive

industry. This assignment will discuss about management accounting and requirements of

different types of management accounting systems. Further, will discuss about different methods

of management accounting reporting, management accounting methods and proper financial

reporting documents. Advantages and disadvantages of various kind of designing tools that are

used in budgetary control and comparison of organisation which adopt management accounting

system to react to fiscal problems.

LO 1

Management accounting and different types of management accounting systems

Management accounting is a kind of accountancy which is helpful for the administrators

of the organisation to support the to manage the financial activities of the organisation in an

efficacious and efficient way and also support in the activity of determination devising in

different situations. In Volkswagen, the accounting financial manager manager of the company

can use it in manage the financial action like cost invest in manufacturing and others or have the

proper information of the finance which are invested by the company (Bennett and James, 2017).

There are number of accounting system which can be used by the firm in managing the finance

and decision making regarding it. Some of them are defined as beneath:

Inventory management system- In this system, the inventory of the organisations are

negotiated in an appropriate way. In addition to it, it traces the cost which which generates due to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the cost of storage of the goods in warehouses. The main objective of this management

accounting system is to make balance among the demand and supply of the goods of the

organisations. In Volkswagen, the management of the company can use this system under

guidance and with the help of it they can track the record of raw material to manufacturing a car.

The production function will take decision fro manufacturing new products as per the available

quantity of manufactured products like car in warehouse.

Price optimization system- This management accounting system is consisted in the

activity of setting price of goods and services on the base of customers feedback and analysis of

collected information of consumers (Chenhall and Moers, 2015). Generally, it is important for

sales division of the company because with the assistance of it, they set the price of the product

at a level is effective for both seller as well as purchaser. Apart form it, the organisations which

are not used this system of management accounting they face the problems in their business

related to finance like lack of sales and profitability etc. In Volkswagen, the administration of the

company implement this accounting system in their business with the purpose of setting the price

of their products. This help the company in maximising the sales and increasing the level of

profitability.

Cost accounting system- This accounting system is related with holding a brief record of

received cost in different operations. By using this system, the organisation can get information

about their actual financial position and make compression between their actual and estimated

cost. This management accounting system is beneficial for finance function of the company

because with the help of it they can formulate financial plan and make effective allocation of the

financial resources within the business activities. In Volkswagen, the financial team can apply

this system in the business because it help in keeping and managing the manufacturing cost at

minimum level. It is also crucial for the assignment of available finances into the different

production activities.

Job costing system- It is an another kind of management accounting system which is

affiliated to the assigning the manufacturing cost a specific unit of output. Generally, this

accounting system is important for those of organisations in which the portfolio of production is

bigger and their cost is differ from each other (Cooper, Ezzamel and Qu, 2017). So it is

important for determination of cost, loss, profitability of each job. In Volkswagen, the

accounting system is to make balance among the demand and supply of the goods of the

organisations. In Volkswagen, the management of the company can use this system under

guidance and with the help of it they can track the record of raw material to manufacturing a car.

The production function will take decision fro manufacturing new products as per the available

quantity of manufactured products like car in warehouse.

Price optimization system- This management accounting system is consisted in the

activity of setting price of goods and services on the base of customers feedback and analysis of

collected information of consumers (Chenhall and Moers, 2015). Generally, it is important for

sales division of the company because with the assistance of it, they set the price of the product

at a level is effective for both seller as well as purchaser. Apart form it, the organisations which

are not used this system of management accounting they face the problems in their business

related to finance like lack of sales and profitability etc. In Volkswagen, the administration of the

company implement this accounting system in their business with the purpose of setting the price

of their products. This help the company in maximising the sales and increasing the level of

profitability.

Cost accounting system- This accounting system is related with holding a brief record of

received cost in different operations. By using this system, the organisation can get information

about their actual financial position and make compression between their actual and estimated

cost. This management accounting system is beneficial for finance function of the company

because with the help of it they can formulate financial plan and make effective allocation of the

financial resources within the business activities. In Volkswagen, the financial team can apply

this system in the business because it help in keeping and managing the manufacturing cost at

minimum level. It is also crucial for the assignment of available finances into the different

production activities.

Job costing system- It is an another kind of management accounting system which is

affiliated to the assigning the manufacturing cost a specific unit of output. Generally, this

accounting system is important for those of organisations in which the portfolio of production is

bigger and their cost is differ from each other (Cooper, Ezzamel and Qu, 2017). So it is

important for determination of cost, loss, profitability of each job. In Volkswagen, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management of the company can implement it for making evaluation of the cost of each and

every activity of production.

Role of management accounting

There are several role which are played by management accounting system in financial

activities of Volkswagen. Some of them are defined as below:

Helpful in effective controlling- Management accounting id beneficial for entities to

develop effective control over various forms of operations and activities of the business. It can be

do by using effective information from internal report and managers become competent to focus

on that activities which are output in to low profit margins or higher costs (Eldenburg and et. al.,

2019). In Volkswagen, the manager can make control on different aspects in efficacious with the

help of management accounting.

Helpful in effectual planning- Management accounting plays a vital role in developing

effective planning of different kind of available origins. With the help of it, the administrators of

the respective company can monitor future activities that are beneficial for efficacious planning.

In Volkswagen, by using management accounting as a planning tool, different functions of the

firm can do better planning which help in generating internal report.

Different methods which are used for management accounting reporting

Management accounting reporting

These kind of account reportage indicates to those reports which are formulated by the

administration of the company with rte assistance of financial and on financial information to

take the intrinsic determinations for the administration. In Volkswagen, the administration of the

firm can use these kind of reporting systems to formulate several kind of administration

accounting reports. Some of them are mentioned as below:

Budget reports- These kind of reports refers to those those documents which consist the

information and data about the actualised income, deterioration & approximative income,

financial loss and others. These kind of reports are essential to measure the effective

performance with the comparison of actual financial gain or finical loss with the budgeted targets

(Fourie, Opperman and Kumar, 2015). In Volkswagen, the administration can prepare these kind

of reports to monitor their effective performance. With the help of it they can prepare their

budget and the firm can list its all expenses and revenues sources.

every activity of production.

Role of management accounting

There are several role which are played by management accounting system in financial

activities of Volkswagen. Some of them are defined as below:

Helpful in effective controlling- Management accounting id beneficial for entities to

develop effective control over various forms of operations and activities of the business. It can be

do by using effective information from internal report and managers become competent to focus

on that activities which are output in to low profit margins or higher costs (Eldenburg and et. al.,

2019). In Volkswagen, the manager can make control on different aspects in efficacious with the

help of management accounting.

Helpful in effectual planning- Management accounting plays a vital role in developing

effective planning of different kind of available origins. With the help of it, the administrators of

the respective company can monitor future activities that are beneficial for efficacious planning.

In Volkswagen, by using management accounting as a planning tool, different functions of the

firm can do better planning which help in generating internal report.

Different methods which are used for management accounting reporting

Management accounting reporting

These kind of account reportage indicates to those reports which are formulated by the

administration of the company with rte assistance of financial and on financial information to

take the intrinsic determinations for the administration. In Volkswagen, the administration of the

firm can use these kind of reporting systems to formulate several kind of administration

accounting reports. Some of them are mentioned as below:

Budget reports- These kind of reports refers to those those documents which consist the

information and data about the actualised income, deterioration & approximative income,

financial loss and others. These kind of reports are essential to measure the effective

performance with the comparison of actual financial gain or finical loss with the budgeted targets

(Fourie, Opperman and Kumar, 2015). In Volkswagen, the administration can prepare these kind

of reports to monitor their effective performance. With the help of it they can prepare their

budget and the firm can list its all expenses and revenues sources.

Cost managerial accounting reports- These are those types of reports which consist data

and information regarding different cost which are generated due to different activities of the

business. In Volkswagen, with the help of these kind of report, the firm can calculate cost which

are manufactured (Maas, Schaltegger and Crutzen, 2016). These reports also help in offering

elaborated information affiliated to cost like raw product overhead, labour, labour cost etc. Cost

reports allow administrators the capableness to view the cost value of goods verse the

merchandising price. It also assist the administrators to make control and plan profitability.

Performance reports- It refer to those documents which include the information

regarding the performance actions and activities of the organisation. In Volkswagen, with the

assistance of these kind of reports, the firm can measure the actual performance of the company

and it will help them in taking effective decision in forthcoming for the demands and cost

increment. These kind of reports are computed by the management each year to monitor the

performer of the company in the market.

Therefore, these kind of reporting system can be formulated by Volkswagen for the

effective operations of the business activities and operations. It is crucial for the company that

they must be prepare these kid of reports so that they can have information about the cost which

can be incurred by the business activities and monitor the performance of the company etc.

These reports are beneficial to have the information about the internal and external functions of

the firm like, stakeholder, workers, shareholders and other.

Difference between management accounting and Financial accounting

Basis Management accounting Financial accounting

Meaning It is a accounting system which

provides relevant data to the

administrator of the company

to form policies, plans and plan

of actions to operate the

business in effective manner.

It is an accounting method

which concentrator on the

preparation of the financial

statement of accompany to

offer the financial information

to the interested parties.

Objective To help in planing and

determination devising process

by providing brief information

To offer financial information

to externals.

and information regarding different cost which are generated due to different activities of the

business. In Volkswagen, with the help of these kind of report, the firm can calculate cost which

are manufactured (Maas, Schaltegger and Crutzen, 2016). These reports also help in offering

elaborated information affiliated to cost like raw product overhead, labour, labour cost etc. Cost

reports allow administrators the capableness to view the cost value of goods verse the

merchandising price. It also assist the administrators to make control and plan profitability.

Performance reports- It refer to those documents which include the information

regarding the performance actions and activities of the organisation. In Volkswagen, with the

assistance of these kind of reports, the firm can measure the actual performance of the company

and it will help them in taking effective decision in forthcoming for the demands and cost

increment. These kind of reports are computed by the management each year to monitor the

performer of the company in the market.

Therefore, these kind of reporting system can be formulated by Volkswagen for the

effective operations of the business activities and operations. It is crucial for the company that

they must be prepare these kid of reports so that they can have information about the cost which

can be incurred by the business activities and monitor the performance of the company etc.

These reports are beneficial to have the information about the internal and external functions of

the firm like, stakeholder, workers, shareholders and other.

Difference between management accounting and Financial accounting

Basis Management accounting Financial accounting

Meaning It is a accounting system which

provides relevant data to the

administrator of the company

to form policies, plans and plan

of actions to operate the

business in effective manner.

It is an accounting method

which concentrator on the

preparation of the financial

statement of accompany to

offer the financial information

to the interested parties.

Objective To help in planing and

determination devising process

by providing brief information

To offer financial information

to externals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

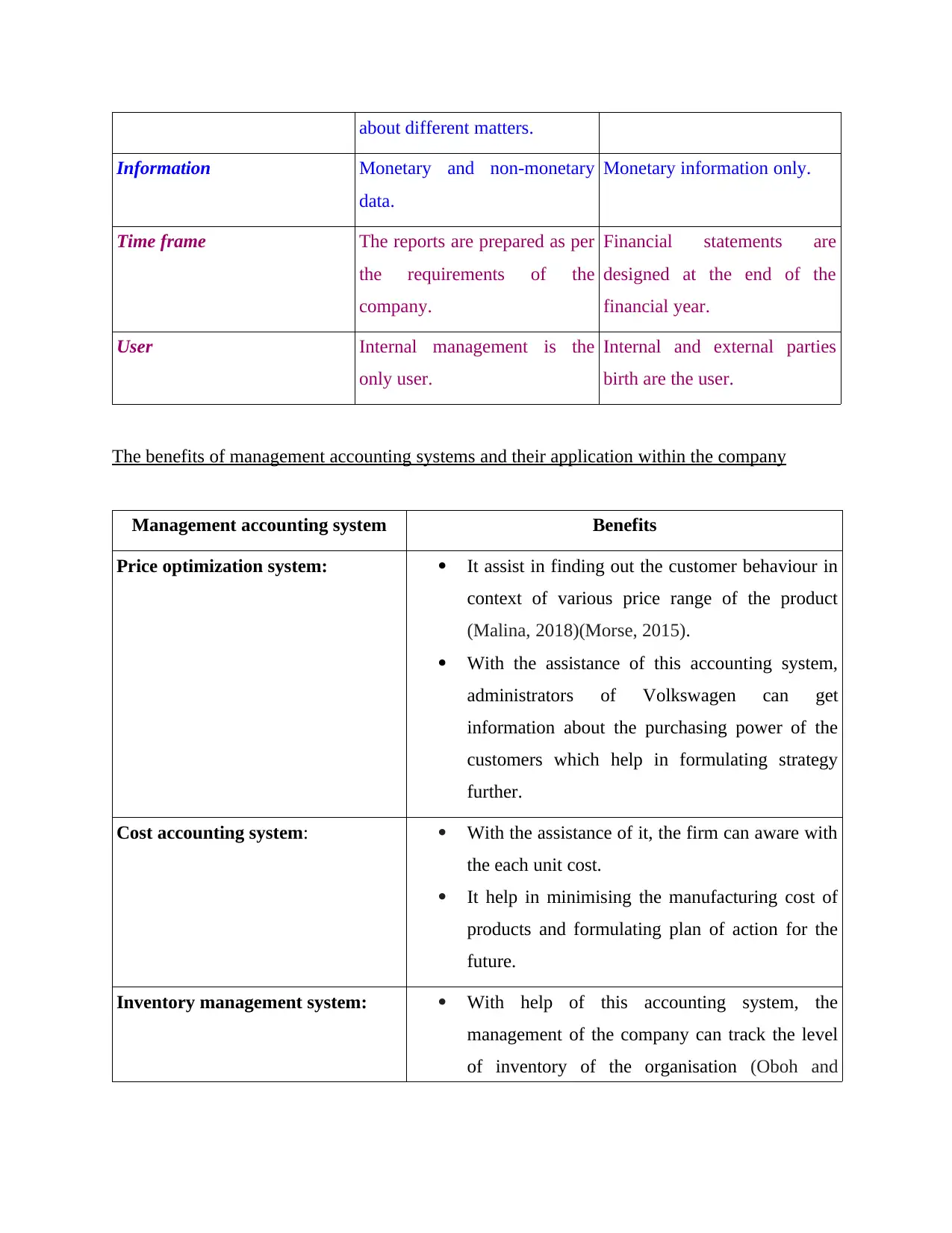

about different matters.

Information Monetary and non-monetary

data.

Monetary information only.

Time frame The reports are prepared as per

the requirements of the

company.

Financial statements are

designed at the end of the

financial year.

User Internal management is the

only user.

Internal and external parties

birth are the user.

The benefits of management accounting systems and their application within the company

Management accounting system Benefits

Price optimization system: It assist in finding out the customer behaviour in

context of various price range of the product

(Malina, 2018)(Morse, 2015).

With the assistance of this accounting system,

administrators of Volkswagen can get

information about the purchasing power of the

customers which help in formulating strategy

further.

Cost accounting system: With the assistance of it, the firm can aware with

the each unit cost.

It help in minimising the manufacturing cost of

products and formulating plan of action for the

future.

Inventory management system: With help of this accounting system, the

management of the company can track the level

of inventory of the organisation (Oboh and

Information Monetary and non-monetary

data.

Monetary information only.

Time frame The reports are prepared as per

the requirements of the

company.

Financial statements are

designed at the end of the

financial year.

User Internal management is the

only user.

Internal and external parties

birth are the user.

The benefits of management accounting systems and their application within the company

Management accounting system Benefits

Price optimization system: It assist in finding out the customer behaviour in

context of various price range of the product

(Malina, 2018)(Morse, 2015).

With the assistance of this accounting system,

administrators of Volkswagen can get

information about the purchasing power of the

customers which help in formulating strategy

further.

Cost accounting system: With the assistance of it, the firm can aware with

the each unit cost.

It help in minimising the manufacturing cost of

products and formulating plan of action for the

future.

Inventory management system: With help of this accounting system, the

management of the company can track the level

of inventory of the organisation (Oboh and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

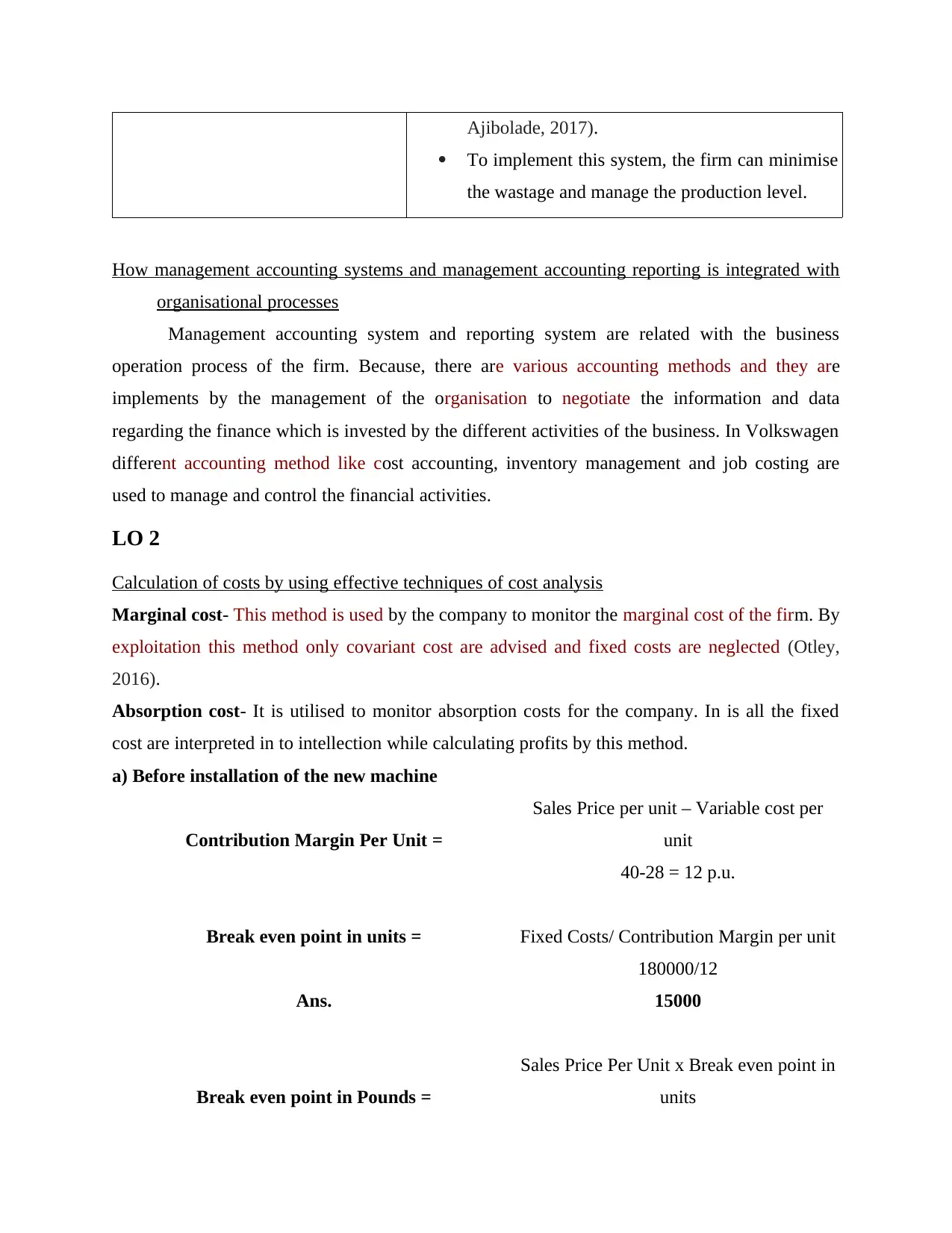

Ajibolade, 2017).

To implement this system, the firm can minimise

the wastage and manage the production level.

How management accounting systems and management accounting reporting is integrated with

organisational processes

Management accounting system and reporting system are related with the business

operation process of the firm. Because, there are various accounting methods and they are

implements by the management of the organisation to negotiate the information and data

regarding the finance which is invested by the different activities of the business. In Volkswagen

different accounting method like cost accounting, inventory management and job costing are

used to manage and control the financial activities.

LO 2

Calculation of costs by using effective techniques of cost analysis

Marginal cost- This method is used by the company to monitor the marginal cost of the firm. By

exploitation this method only covariant cost are advised and fixed costs are neglected (Otley,

2016).

Absorption cost- It is utilised to monitor absorption costs for the company. In is all the fixed

cost are interpreted in to intellection while calculating profits by this method.

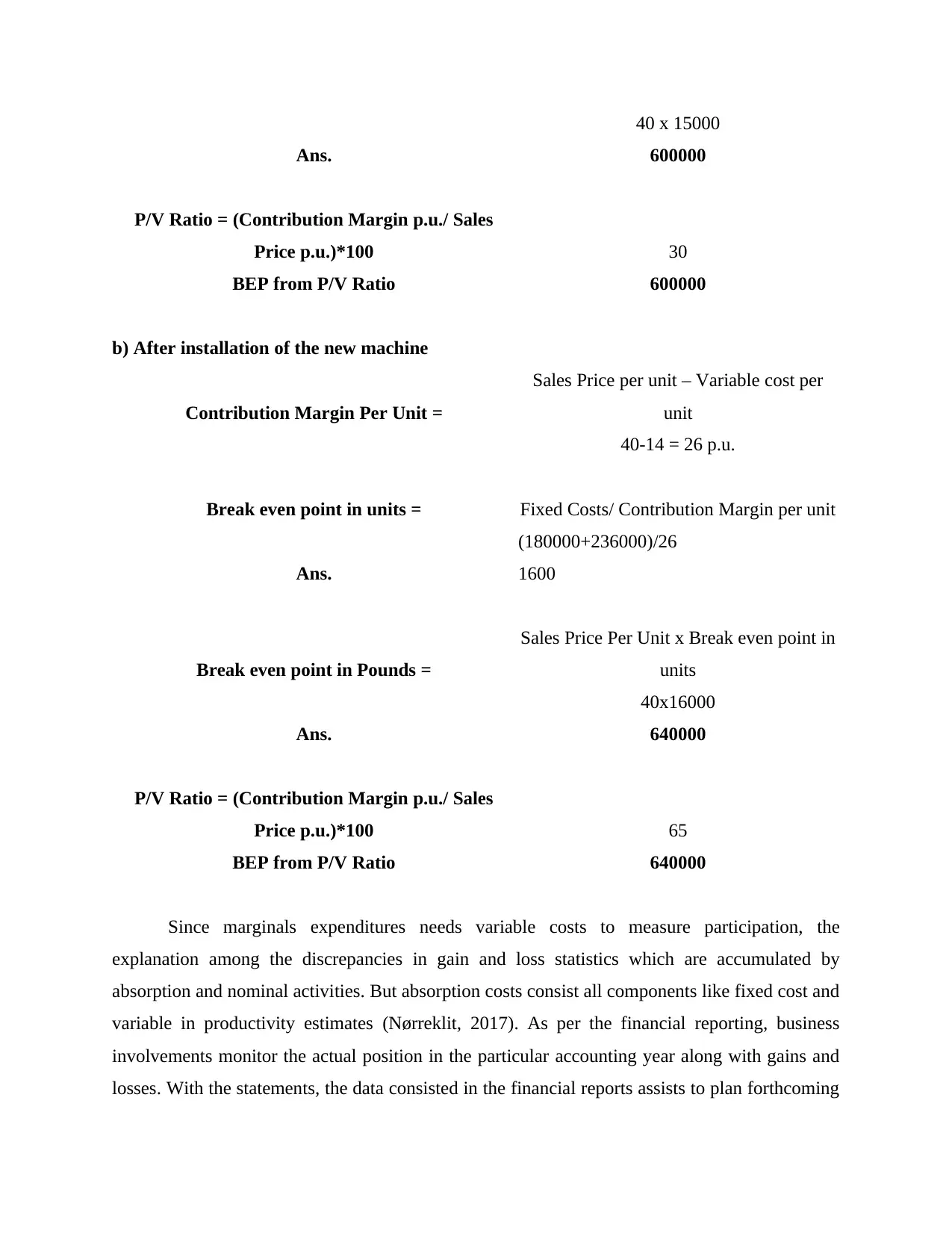

a) Before installation of the new machine

Contribution Margin Per Unit =

Sales Price per unit – Variable cost per

unit

40-28 = 12 p.u.

Break even point in units = Fixed Costs/ Contribution Margin per unit

180000/12

Ans. 15000

Break even point in Pounds =

Sales Price Per Unit x Break even point in

units

To implement this system, the firm can minimise

the wastage and manage the production level.

How management accounting systems and management accounting reporting is integrated with

organisational processes

Management accounting system and reporting system are related with the business

operation process of the firm. Because, there are various accounting methods and they are

implements by the management of the organisation to negotiate the information and data

regarding the finance which is invested by the different activities of the business. In Volkswagen

different accounting method like cost accounting, inventory management and job costing are

used to manage and control the financial activities.

LO 2

Calculation of costs by using effective techniques of cost analysis

Marginal cost- This method is used by the company to monitor the marginal cost of the firm. By

exploitation this method only covariant cost are advised and fixed costs are neglected (Otley,

2016).

Absorption cost- It is utilised to monitor absorption costs for the company. In is all the fixed

cost are interpreted in to intellection while calculating profits by this method.

a) Before installation of the new machine

Contribution Margin Per Unit =

Sales Price per unit – Variable cost per

unit

40-28 = 12 p.u.

Break even point in units = Fixed Costs/ Contribution Margin per unit

180000/12

Ans. 15000

Break even point in Pounds =

Sales Price Per Unit x Break even point in

units

40 x 15000

Ans. 600000

P/V Ratio = (Contribution Margin p.u./ Sales

Price p.u.)*100 30

BEP from P/V Ratio 600000

b) After installation of the new machine

Contribution Margin Per Unit =

Sales Price per unit – Variable cost per

unit

40-14 = 26 p.u.

Break even point in units = Fixed Costs/ Contribution Margin per unit

(180000+236000)/26

Ans. 1600

Break even point in Pounds =

Sales Price Per Unit x Break even point in

units

40x16000

Ans. 640000

P/V Ratio = (Contribution Margin p.u./ Sales

Price p.u.)*100 65

BEP from P/V Ratio 640000

Since marginals expenditures needs variable costs to measure participation, the

explanation among the discrepancies in gain and loss statistics which are accumulated by

absorption and nominal activities. But absorption costs consist all components like fixed cost and

variable in productivity estimates (Nørreklit, 2017). As per the financial reporting, business

involvements monitor the actual position in the particular accounting year along with gains and

losses. With the statements, the data consisted in the financial reports assists to plan forthcoming

Ans. 600000

P/V Ratio = (Contribution Margin p.u./ Sales

Price p.u.)*100 30

BEP from P/V Ratio 600000

b) After installation of the new machine

Contribution Margin Per Unit =

Sales Price per unit – Variable cost per

unit

40-14 = 26 p.u.

Break even point in units = Fixed Costs/ Contribution Margin per unit

(180000+236000)/26

Ans. 1600

Break even point in Pounds =

Sales Price Per Unit x Break even point in

units

40x16000

Ans. 640000

P/V Ratio = (Contribution Margin p.u./ Sales

Price p.u.)*100 65

BEP from P/V Ratio 640000

Since marginals expenditures needs variable costs to measure participation, the

explanation among the discrepancies in gain and loss statistics which are accumulated by

absorption and nominal activities. But absorption costs consist all components like fixed cost and

variable in productivity estimates (Nørreklit, 2017). As per the financial reporting, business

involvements monitor the actual position in the particular accounting year along with gains and

losses. With the statements, the data consisted in the financial reports assists to plan forthcoming

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

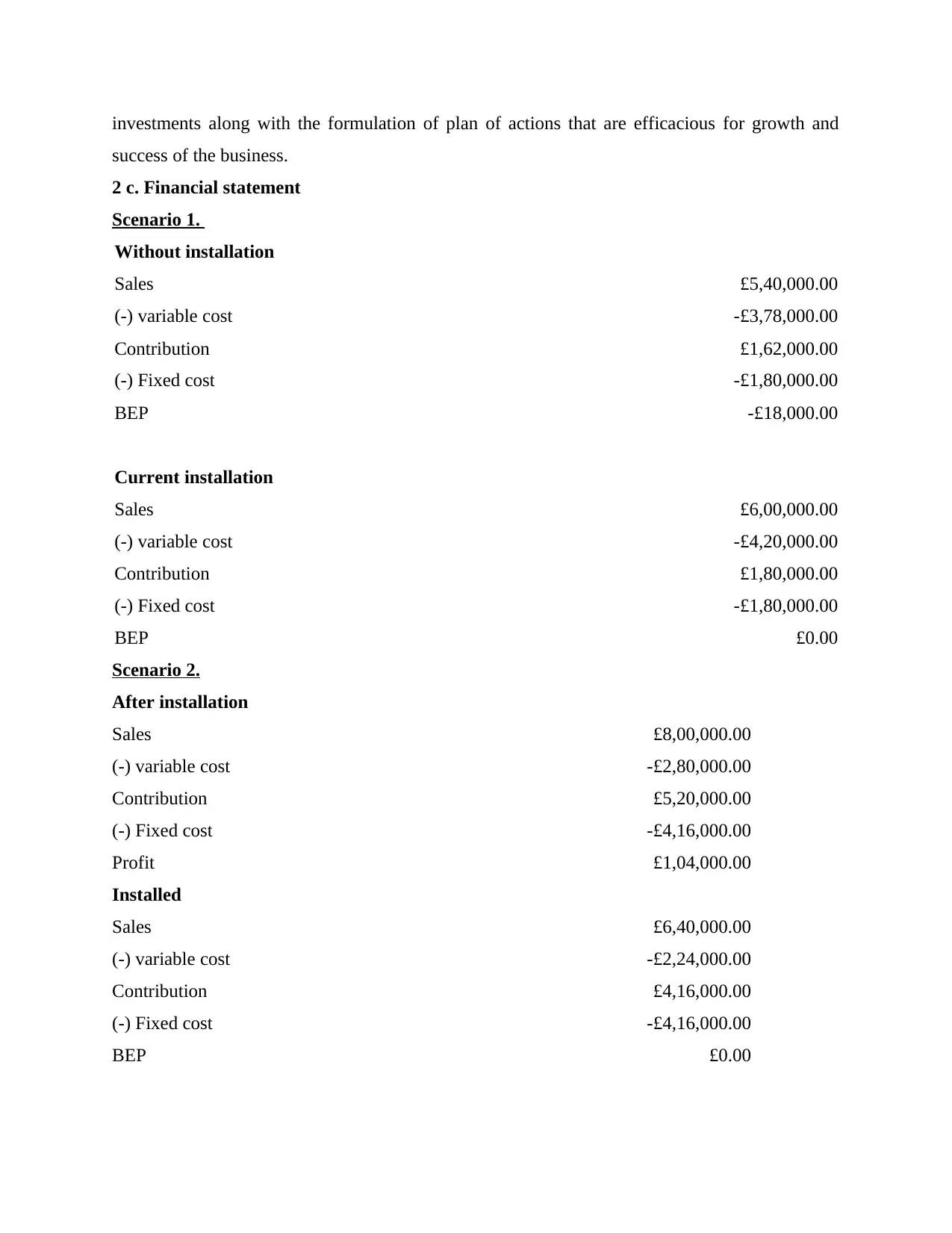

investments along with the formulation of plan of actions that are efficacious for growth and

success of the business.

2 c. Financial statement

Scenario 1.

Without installation

Sales £5,40,000.00

(-) variable cost -£3,78,000.00

Contribution £1,62,000.00

(-) Fixed cost -£1,80,000.00

BEP -£18,000.00

Current installation

Sales £6,00,000.00

(-) variable cost -£4,20,000.00

Contribution £1,80,000.00

(-) Fixed cost -£1,80,000.00

BEP £0.00

Scenario 2.

After installation

Sales £8,00,000.00

(-) variable cost -£2,80,000.00

Contribution £5,20,000.00

(-) Fixed cost -£4,16,000.00

Profit £1,04,000.00

Installed

Sales £6,40,000.00

(-) variable cost -£2,24,000.00

Contribution £4,16,000.00

(-) Fixed cost -£4,16,000.00

BEP £0.00

success of the business.

2 c. Financial statement

Scenario 1.

Without installation

Sales £5,40,000.00

(-) variable cost -£3,78,000.00

Contribution £1,62,000.00

(-) Fixed cost -£1,80,000.00

BEP -£18,000.00

Current installation

Sales £6,00,000.00

(-) variable cost -£4,20,000.00

Contribution £1,80,000.00

(-) Fixed cost -£1,80,000.00

BEP £0.00

Scenario 2.

After installation

Sales £8,00,000.00

(-) variable cost -£2,80,000.00

Contribution £5,20,000.00

(-) Fixed cost -£4,16,000.00

Profit £1,04,000.00

Installed

Sales £6,40,000.00

(-) variable cost -£2,24,000.00

Contribution £4,16,000.00

(-) Fixed cost -£4,16,000.00

BEP £0.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the preceding tables, it has been monitored that organization should use new

machines as they are capable to gain £1,04,000 and BEP is £0.00 when the organization sell

16000 units (Otley, 2016). Therefore, when the firm maximize its selling unit, there will be

maximization in the profit margins ration.

Financial reports that accurately apply and interpret the data for several business activities

The administration of Volkswagen frames financial reports with the assistance of

marginal and absorption techniques of cost accounting. Both the techniques have create

favourable and unfavourable impact. The marginal costing method is useful because it has the

feature of making control on the cost by devising the cost into fixed and variable cost. This

method negatively affect because it becomes unrealistic in the case of high fluctuation of

production (Renz and Herman, 2016). The absorption cost is crucial for preparing the income

statement because it consist both cost and unit cost. Apart form it, the disadvantage of it is that it

make complex the calculation cost volume profit analysis. In Volkswagen, the management of

the company can use the absorption technique because with the help of it the company can

effectively analyse and monitor cost and unit cost and with the help of it, the firm can effectively

prepare the income statement of the company.

LO 3

Advantages and disadvantages of different types of planning tools used in budgetary control

Budget is regarded as the precise statements which highlights approximation of financial

expending and revenues for certain time period. It aids organisation in obtaining profit by

figuring the cost of their business entities. In addition to this, it is also defined as the qualitative

statements which is formed for definitive period in order to approximate upcoming time

expenditure and revenue. All organisation has to formulate budgets as this aids them in getting

knowledge about the futuristics risk and profit. Therefore, the Volkswagen manager may able

make its budget by using last one as this assists them to gain more profit and run the entities in

effective and effectual way. Such as they make budget for its raw materials as this helps them to

get knowledge about how much they can spend into its raw materials (Schaltegger and Burritt,

2017). Budgetary Control is considered as the practice that is performed by managers in order to

decide the financial objectives and performance by doing comparison with actual expenses to get

machines as they are capable to gain £1,04,000 and BEP is £0.00 when the organization sell

16000 units (Otley, 2016). Therefore, when the firm maximize its selling unit, there will be

maximization in the profit margins ration.

Financial reports that accurately apply and interpret the data for several business activities

The administration of Volkswagen frames financial reports with the assistance of

marginal and absorption techniques of cost accounting. Both the techniques have create

favourable and unfavourable impact. The marginal costing method is useful because it has the

feature of making control on the cost by devising the cost into fixed and variable cost. This

method negatively affect because it becomes unrealistic in the case of high fluctuation of

production (Renz and Herman, 2016). The absorption cost is crucial for preparing the income

statement because it consist both cost and unit cost. Apart form it, the disadvantage of it is that it

make complex the calculation cost volume profit analysis. In Volkswagen, the management of

the company can use the absorption technique because with the help of it the company can

effectively analyse and monitor cost and unit cost and with the help of it, the firm can effectively

prepare the income statement of the company.

LO 3

Advantages and disadvantages of different types of planning tools used in budgetary control

Budget is regarded as the precise statements which highlights approximation of financial

expending and revenues for certain time period. It aids organisation in obtaining profit by

figuring the cost of their business entities. In addition to this, it is also defined as the qualitative

statements which is formed for definitive period in order to approximate upcoming time

expenditure and revenue. All organisation has to formulate budgets as this aids them in getting

knowledge about the futuristics risk and profit. Therefore, the Volkswagen manager may able

make its budget by using last one as this assists them to gain more profit and run the entities in

effective and effectual way. Such as they make budget for its raw materials as this helps them to

get knowledge about how much they can spend into its raw materials (Schaltegger and Burritt,

2017). Budgetary Control is considered as the practice that is performed by managers in order to

decide the financial objectives and performance by doing comparison with actual expenses to get

profit. Moreover, there are many planning tools which can be utilised by respective organisation

for budgetary control some of them are described below:

Cash budget: It is regarded as the budgetary planning tools that consists information

related to overall activities such as inflows as well as outflows of cash. This provide assistance to

its business owner in handling capital of networking. In boarded context, the cash budget

represents that how much cash is needed for operating its business (Schuster, 2015). Moreover,

cash budget is comprises of two of two section that are sources of cash as well as usages of cash.

Therefore, the Volkswagen accountants makes this particular budget as this aids its finance

division in order to develop effectual practices of management related to cash. Advantage: The sales budget provide assistance to Volkswagen for finding potential

deficit in quicker time period. It help in identify the amount of cash needed to fulfil

immediate short term obligations without usages of overdraft protection or lines of credit.

Disadvantage: The main drawbacks of this is that it totally depends on estimation and

also this may be lost in simple way. It may also cause distortions and do not equate to

profit. Cash inflows resulting from security deposits, fines, the scale of capital assess or

any Theo one -off, not suitable activity do not necessarily represent reliable ongoing

sources of revenue.

Sales budget: It is regarded as the kinds of budget that consists information in respect of

expected units of sales and incomes and expenses that may occurs within sells process. Based on

this information, the manager may able to set its plan of actions to accomplish the target desired

sales. Moreover, this is also known as coordination instrument among various department within

firm such as sales, production, advertising, finance and many others. So, Volkswagen accountant

may develop this particular budget that provide assistances to their production department in

order to take corrective actions. Moreover, it have some advantage and disadvantage which are

as follows: Advantage: The sales budget is beneficiary for Volkswagen in delegating resources for

producing many products and sales the in effective and efficient manner with the aim to

realise expected sales.

Disadvantage: The main drawback of sales budget, it is only completed according to the

last data . Moreover, in some cases the respective organisation can leads towards huge

financial losses.

for budgetary control some of them are described below:

Cash budget: It is regarded as the budgetary planning tools that consists information

related to overall activities such as inflows as well as outflows of cash. This provide assistance to

its business owner in handling capital of networking. In boarded context, the cash budget

represents that how much cash is needed for operating its business (Schuster, 2015). Moreover,

cash budget is comprises of two of two section that are sources of cash as well as usages of cash.

Therefore, the Volkswagen accountants makes this particular budget as this aids its finance

division in order to develop effectual practices of management related to cash. Advantage: The sales budget provide assistance to Volkswagen for finding potential

deficit in quicker time period. It help in identify the amount of cash needed to fulfil

immediate short term obligations without usages of overdraft protection or lines of credit.

Disadvantage: The main drawbacks of this is that it totally depends on estimation and

also this may be lost in simple way. It may also cause distortions and do not equate to

profit. Cash inflows resulting from security deposits, fines, the scale of capital assess or

any Theo one -off, not suitable activity do not necessarily represent reliable ongoing

sources of revenue.

Sales budget: It is regarded as the kinds of budget that consists information in respect of

expected units of sales and incomes and expenses that may occurs within sells process. Based on

this information, the manager may able to set its plan of actions to accomplish the target desired

sales. Moreover, this is also known as coordination instrument among various department within

firm such as sales, production, advertising, finance and many others. So, Volkswagen accountant

may develop this particular budget that provide assistances to their production department in

order to take corrective actions. Moreover, it have some advantage and disadvantage which are

as follows: Advantage: The sales budget is beneficiary for Volkswagen in delegating resources for

producing many products and sales the in effective and efficient manner with the aim to

realise expected sales.

Disadvantage: The main drawback of sales budget, it is only completed according to the

last data . Moreover, in some cases the respective organisation can leads towards huge

financial losses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.