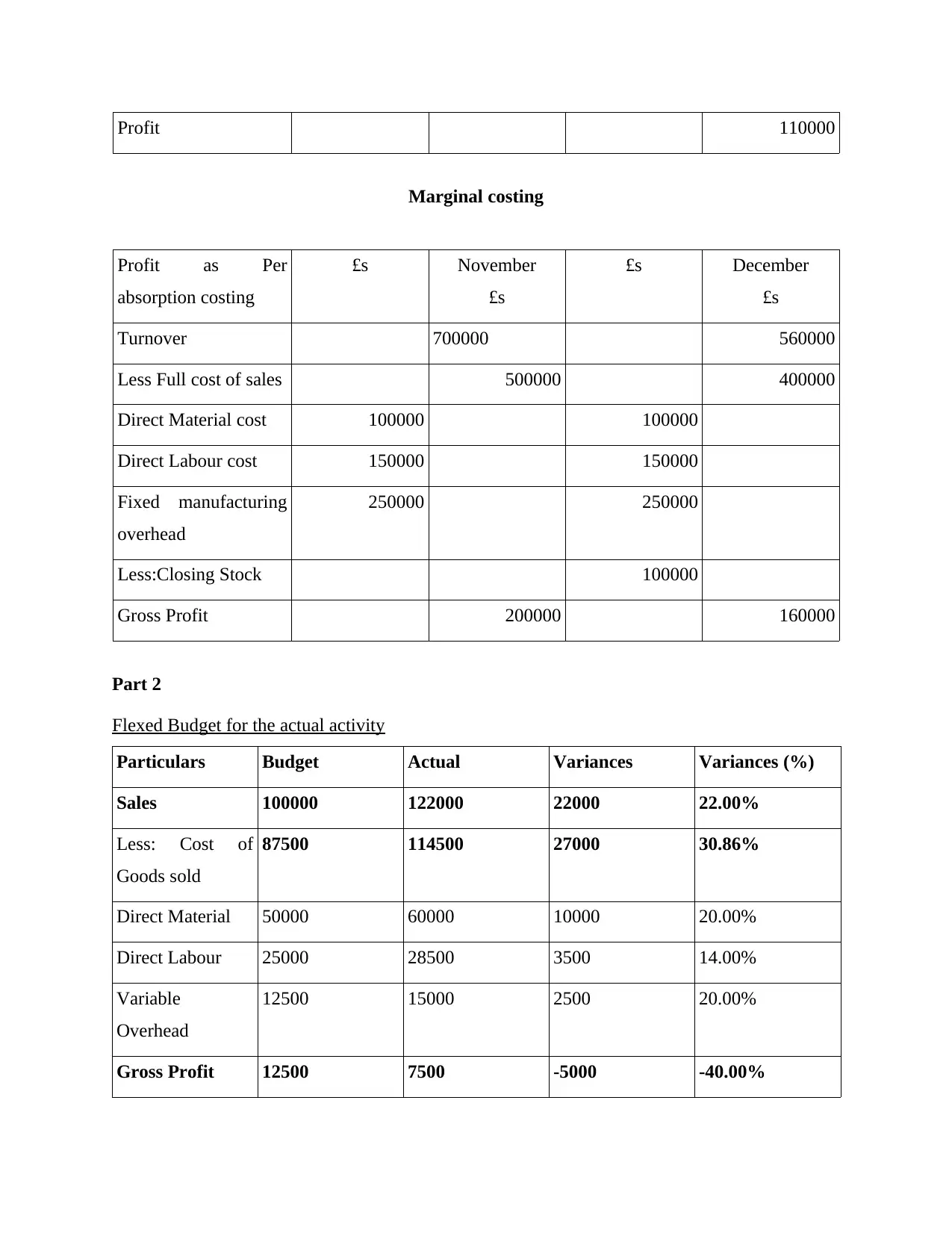

Financial Analysis: Management Accounting for Warwick Fabrics UK Ltd

VerifiedAdded on 2023/06/17

|14

|3920

|343

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within a financial consultancy context, specifically focusing on Arrow Financial Services and its client, Warwick Fabrics UK Ltd. It covers essential components of management accounting systems, including cost accounting, inventory management, job costing, and price optimization. The report also examines various methods used in management accounting reporting, such as accounts receivable reports, budget reports, inventory management reports, and performance reports. Practical application is demonstrated through the preparation of income statements under absorption and marginal costing methods, along with flexed budget analysis. Furthermore, the report discusses the advantages and disadvantages of planning tools used for budgetary control, offering a comprehensive overview of how organizations can leverage management accounting to address financial issues. Desklib provides access to similar solved assignments and resources for students.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and essential requirement of different kind of management

accounting systems-.....................................................................................................................3

P2. Various method that used in management accounting reporting:.........................................5

TASK 2............................................................................................................................................6

P3. Preparation of income statements under the absorption and marginal costing-....................6

Absorption costing ..........................................................................................................................7

Flexed Budget for the actual activity...........................................................................................8

TASK 3............................................................................................................................................9

P4. Advantages and disadvantages of planning tools used for budgetary control:......................9

TASK 4..........................................................................................................................................10

P5. Comparison of organisations to solve the financial issues .................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and essential requirement of different kind of management

accounting systems-.....................................................................................................................3

P2. Various method that used in management accounting reporting:.........................................5

TASK 2............................................................................................................................................6

P3. Preparation of income statements under the absorption and marginal costing-....................6

Absorption costing ..........................................................................................................................7

Flexed Budget for the actual activity...........................................................................................8

TASK 3............................................................................................................................................9

P4. Advantages and disadvantages of planning tools used for budgetary control:......................9

TASK 4..........................................................................................................................................10

P5. Comparison of organisations to solve the financial issues .................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting (MA) is called managerial accounting and cost accounting. It is

a process that is discussed as controlling, directing, administration of the operational and

functional activities of the business processing unit to prepare the financial reports and statement

from business transaction or records that assist in decision-making process to management

(Yahyavisaeen, Amirhosseini, and Poorzamani, 2015). It control the business operation and

apply the systematic approaches of management accounting process to management can take the

decision regards the achieving the business goal. For this report a financial consultancy company

that is Arrow financial services is selected that is UK origin company and provides the financial

consulting services to its valued customers. In further to another Client company of the this

particular company Warwick fabrics UK Ltd is choose for better understanding this report. This

is manufacturer of the cloth and supplier of fabrics that is located in Gloucester, united kingdom.

This reports covers the management accounting system and reporting, budgeting control system

and different planning tools and techniques that are implementing in the business to resolve the

financial problem of the business. It also covers practical problem on the basis of the stores and

production level of the company.

TASK 1

P1. Management accounting and essential requirement of different kind of management

accounting systems-

Management accounting: It consist of the detailed planning, monitoring and handling

the business activity or action to betterment in the business productivity and performance. This

process of management accounting includes the decision making system in the business from its

current business affairs and deals. Management accounting is combines the application of the

financial and non monitory information and data to handle the business concern and its

components. The company Warwick fabrics UK Ltd is manufacturer of the textiles fabrics is

used the management accounting system to conduct the business activities and deals (Sahu and

Kumari, 2015).

Management accounting system: management accounting system are appropriate and

systematic process of analyse the business final account and other statement and used the data

from the daily operation and records in the enterprises. These analysed data and information are

Management accounting (MA) is called managerial accounting and cost accounting. It is

a process that is discussed as controlling, directing, administration of the operational and

functional activities of the business processing unit to prepare the financial reports and statement

from business transaction or records that assist in decision-making process to management

(Yahyavisaeen, Amirhosseini, and Poorzamani, 2015). It control the business operation and

apply the systematic approaches of management accounting process to management can take the

decision regards the achieving the business goal. For this report a financial consultancy company

that is Arrow financial services is selected that is UK origin company and provides the financial

consulting services to its valued customers. In further to another Client company of the this

particular company Warwick fabrics UK Ltd is choose for better understanding this report. This

is manufacturer of the cloth and supplier of fabrics that is located in Gloucester, united kingdom.

This reports covers the management accounting system and reporting, budgeting control system

and different planning tools and techniques that are implementing in the business to resolve the

financial problem of the business. It also covers practical problem on the basis of the stores and

production level of the company.

TASK 1

P1. Management accounting and essential requirement of different kind of management

accounting systems-

Management accounting: It consist of the detailed planning, monitoring and handling

the business activity or action to betterment in the business productivity and performance. This

process of management accounting includes the decision making system in the business from its

current business affairs and deals. Management accounting is combines the application of the

financial and non monitory information and data to handle the business concern and its

components. The company Warwick fabrics UK Ltd is manufacturer of the textiles fabrics is

used the management accounting system to conduct the business activities and deals (Sahu and

Kumari, 2015).

Management accounting system: management accounting system are appropriate and

systematic process of analyse the business final account and other statement and used the data

from the daily operation and records in the enterprises. These analysed data and information are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

really helpful in order to make the business decision and redefine the organisational rule and

policies in structured manner. Warwick fabrics UK Ltd applies the management accounting

tools in the business function to better manage the short term operation. There are a lot of

management accounting system available to be utilize in the business. Some of them are

discussed below:

Cost accounting system: This is the main accounting system of management that is

described as structure of outlay which is recognize the accurate cost of production for a

processing unit. This is the system that used to evaluating the cost of the material, direct labour,

and other overhead and monitor the total works cost at the processing unit of manufacture. This

system is based on the cost and production value techniques to handle the overall cost. In the

relevance with Warwick fabrics UK Ltd company used this process to maintain the overall cost

of manufacturing, fabrication and designing section cost. So it help in the ascertaining the total

cost of production as well as profit from the processing unit of enterprises. This tools is also

helpful in devising the cost accompanying scheme, cost structure and annual budget (O’Grady

and Akroyd, 2016).

Inventory management system: It is a basic system of management accounting process

that defines as ascertain the level of the stock in the manufacturing unit, stores, and warehouses.

It further ensure the accessibility of the stock material at right time of consumption in making the

goods and services. The stock comprises the stage of the stock such as raw material

consumption, work in progress (WIP) and last stage of goods finished stock. This system play a

significant role in deciding the price tag for the particular product. The selected company

Warwick fabrics UK Ltd is using this particular tools in the system to ascertain the quality and

quantity of the stock available at the warehouse. This process monitor the stored quantity of the

goods to improved flow of the goods and services. There are antithetic concepts to confirm the

value of goods such as LIFO, FIFO and weighted average method (Nanshun and Ya, 2013).

Job costing system: This is the another method of the management accounting system

that refers to simply allocation of the cost on the particular task or projects. It is relevant with

grouping of the cost component that is related with particular product. It aid in evaluating the

different job allocation cost to improve the final capacity of particular manufacturing unit. It is

cost accounting method that is based on the estimation of the cost of the completed projects and

policies in structured manner. Warwick fabrics UK Ltd applies the management accounting

tools in the business function to better manage the short term operation. There are a lot of

management accounting system available to be utilize in the business. Some of them are

discussed below:

Cost accounting system: This is the main accounting system of management that is

described as structure of outlay which is recognize the accurate cost of production for a

processing unit. This is the system that used to evaluating the cost of the material, direct labour,

and other overhead and monitor the total works cost at the processing unit of manufacture. This

system is based on the cost and production value techniques to handle the overall cost. In the

relevance with Warwick fabrics UK Ltd company used this process to maintain the overall cost

of manufacturing, fabrication and designing section cost. So it help in the ascertaining the total

cost of production as well as profit from the processing unit of enterprises. This tools is also

helpful in devising the cost accompanying scheme, cost structure and annual budget (O’Grady

and Akroyd, 2016).

Inventory management system: It is a basic system of management accounting process

that defines as ascertain the level of the stock in the manufacturing unit, stores, and warehouses.

It further ensure the accessibility of the stock material at right time of consumption in making the

goods and services. The stock comprises the stage of the stock such as raw material

consumption, work in progress (WIP) and last stage of goods finished stock. This system play a

significant role in deciding the price tag for the particular product. The selected company

Warwick fabrics UK Ltd is using this particular tools in the system to ascertain the quality and

quantity of the stock available at the warehouse. This process monitor the stored quantity of the

goods to improved flow of the goods and services. There are antithetic concepts to confirm the

value of goods such as LIFO, FIFO and weighted average method (Nanshun and Ya, 2013).

Job costing system: This is the another method of the management accounting system

that refers to simply allocation of the cost on the particular task or projects. It is relevant with

grouping of the cost component that is related with particular product. It aid in evaluating the

different job allocation cost to improve the final capacity of particular manufacturing unit. It is

cost accounting method that is based on the estimation of the cost of the completed projects and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

task at central manufactured system. In addition to it can use other method of the cost to

appraise the production like process costing and batch costing.

Price optimisation system: This is the particular method of management accounting

process that is determine the cost of product and setting the price on the goods and services by

adding the profit margin. This system also confirm the value of the goods on basis of the

customer reaction. And it ascertain how customer will approaches the price structure of the

goods and services. So they can adjust the price or tag of the particular goods by make the

alteration the price. Warwick fabrics UK Ltd is using this tool to set the price on the goods to

maintain the profit level of the goods. There are different price strategies to be adopt by the

company to decide the price tag of the certain goods (Ling, 2013).

P2. Various method that used in management accounting reporting:

Management accounting reporting: This is the basic process that is defined as

aggregation of the financial information and data by the management of firm in order to prepare

the financial statement and reports for the specific time of period to make the financial decision.

These are internal reports for the management of the business that supply the particular by head

of the department of the processing unit of the business. Warwick fabrics UK Ltd uses the

different kind of reports in the making the future decision and strategies planning. Following

reports are created by the company defined as under:

Account receivable reports: This report can be generated by those company which are

involving in the trading of goods and services on credit basis. This reports is directed with

providing the internal data and information to management about the overdue payment from the

customers. So management and staff are analyse the credit amount and its duration to pay off.

Main motive behind this to ascertain the credit amount for the outstanding with the debtors. It

may help in tighten the credit limit for the customer who are not paying on time (Jersan, Dun-

hou and Chung, 2014).

Budget report: This reports contents the projection of the data related to particular

processing unit and compare with the actual performance of the unit. It derives the value from

the certain internal papers used by the management in order to estimates the projected data and

make a comparison with actual output and identify the clear variances between them.

Management of the Warwick fabrics UK Ltd is using this tool in the cost accounting to ascertain

the budgeted data and actual performance in the processing unit at the particular level.By

appraise the production like process costing and batch costing.

Price optimisation system: This is the particular method of management accounting

process that is determine the cost of product and setting the price on the goods and services by

adding the profit margin. This system also confirm the value of the goods on basis of the

customer reaction. And it ascertain how customer will approaches the price structure of the

goods and services. So they can adjust the price or tag of the particular goods by make the

alteration the price. Warwick fabrics UK Ltd is using this tool to set the price on the goods to

maintain the profit level of the goods. There are different price strategies to be adopt by the

company to decide the price tag of the certain goods (Ling, 2013).

P2. Various method that used in management accounting reporting:

Management accounting reporting: This is the basic process that is defined as

aggregation of the financial information and data by the management of firm in order to prepare

the financial statement and reports for the specific time of period to make the financial decision.

These are internal reports for the management of the business that supply the particular by head

of the department of the processing unit of the business. Warwick fabrics UK Ltd uses the

different kind of reports in the making the future decision and strategies planning. Following

reports are created by the company defined as under:

Account receivable reports: This report can be generated by those company which are

involving in the trading of goods and services on credit basis. This reports is directed with

providing the internal data and information to management about the overdue payment from the

customers. So management and staff are analyse the credit amount and its duration to pay off.

Main motive behind this to ascertain the credit amount for the outstanding with the debtors. It

may help in tighten the credit limit for the customer who are not paying on time (Jersan, Dun-

hou and Chung, 2014).

Budget report: This reports contents the projection of the data related to particular

processing unit and compare with the actual performance of the unit. It derives the value from

the certain internal papers used by the management in order to estimates the projected data and

make a comparison with actual output and identify the clear variances between them.

Management of the Warwick fabrics UK Ltd is using this tool in the cost accounting to ascertain

the budgeted data and actual performance in the processing unit at the particular level.By

analyzing the assorted aspects of budget they can make proper business conclusion for the

improvement the function of the firm.

Inventory management report: This report is used by the business firm to track the

record of the stock. This reports contents with the raw data of stock at the processing unit's stores

and warehouse. It also records the inward and outward movement of the stock from a particular

location of the unit. By maintaining this report of cost management can better know the actual

situation of the inventory. In addition to, this report is also useful to canvass the actual position

of stock whether it is in transit or at warehouse. Warwick fabrics UK Ltd is generating this

reports to know the actual status of the stock of raw material, finished goods or at stored location

(Ionescu and Tudoran, 2013).

Performance report: This is reports covers the information related to overall

performance of the structure. It consists of the financial goals that required to attain in the

financial year. Performance reports are basically concluded the actual data and compare with

budgeted information to find out the variances that occur in the business. Warwick fabrics UK

Ltd is used this reports to evaluate the business performance by analyzing the performed task

that is well executed by the workers of the organization. With the help of this reports,

management can know the efficiency of the employees. This reports is used by the management

in order to give incentives to those worker who work as per abilities and beyond it.

TASK 2.

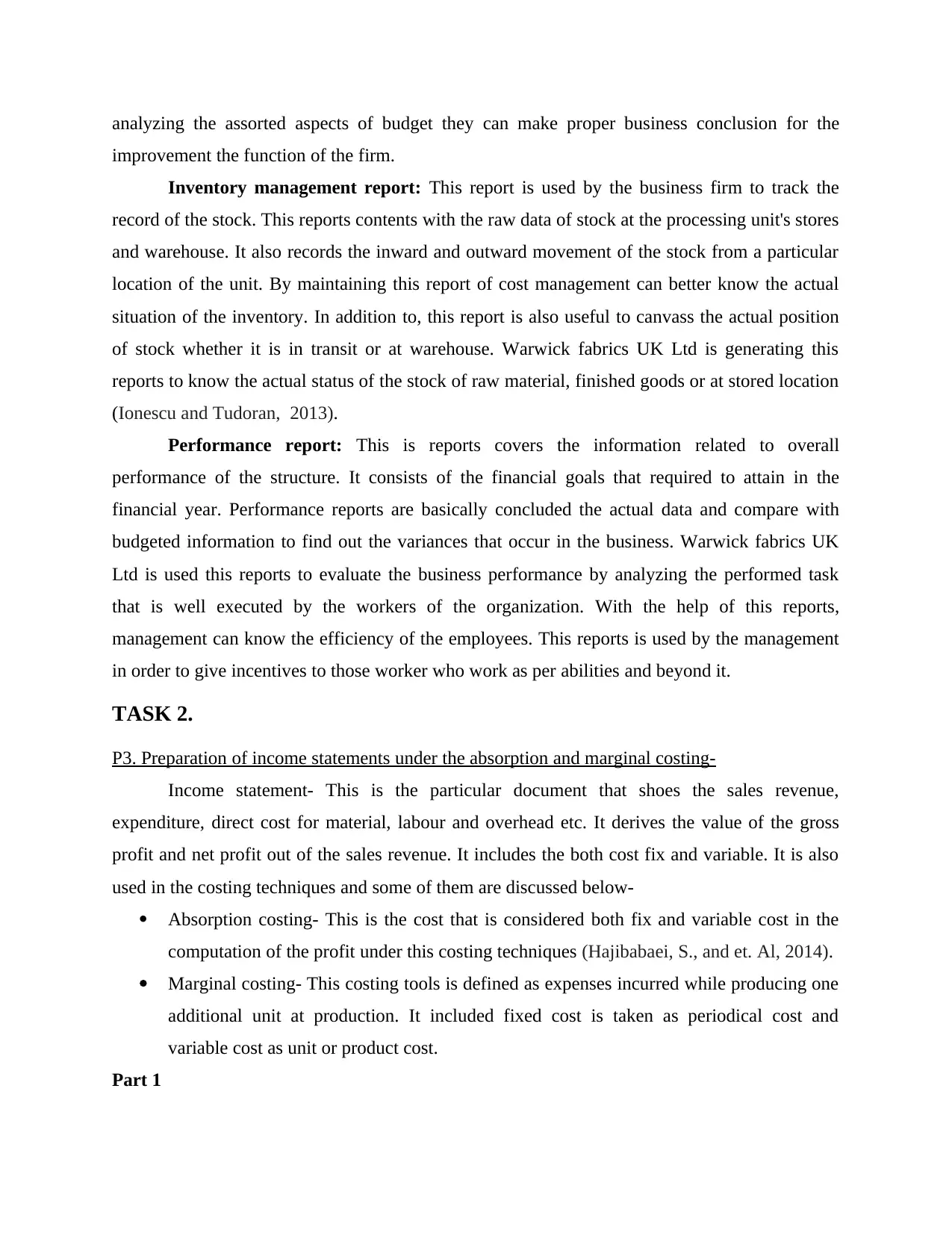

P3. Preparation of income statements under the absorption and marginal costing-

Income statement- This is the particular document that shoes the sales revenue,

expenditure, direct cost for material, labour and overhead etc. It derives the value of the gross

profit and net profit out of the sales revenue. It includes the both cost fix and variable. It is also

used in the costing techniques and some of them are discussed below-

Absorption costing- This is the cost that is considered both fix and variable cost in the

computation of the profit under this costing techniques (Hajibabaei, S., and et. Al, 2014).

Marginal costing- This costing tools is defined as expenses incurred while producing one

additional unit at production. It included fixed cost is taken as periodical cost and

variable cost as unit or product cost.

Part 1

improvement the function of the firm.

Inventory management report: This report is used by the business firm to track the

record of the stock. This reports contents with the raw data of stock at the processing unit's stores

and warehouse. It also records the inward and outward movement of the stock from a particular

location of the unit. By maintaining this report of cost management can better know the actual

situation of the inventory. In addition to, this report is also useful to canvass the actual position

of stock whether it is in transit or at warehouse. Warwick fabrics UK Ltd is generating this

reports to know the actual status of the stock of raw material, finished goods or at stored location

(Ionescu and Tudoran, 2013).

Performance report: This is reports covers the information related to overall

performance of the structure. It consists of the financial goals that required to attain in the

financial year. Performance reports are basically concluded the actual data and compare with

budgeted information to find out the variances that occur in the business. Warwick fabrics UK

Ltd is used this reports to evaluate the business performance by analyzing the performed task

that is well executed by the workers of the organization. With the help of this reports,

management can know the efficiency of the employees. This reports is used by the management

in order to give incentives to those worker who work as per abilities and beyond it.

TASK 2.

P3. Preparation of income statements under the absorption and marginal costing-

Income statement- This is the particular document that shoes the sales revenue,

expenditure, direct cost for material, labour and overhead etc. It derives the value of the gross

profit and net profit out of the sales revenue. It includes the both cost fix and variable. It is also

used in the costing techniques and some of them are discussed below-

Absorption costing- This is the cost that is considered both fix and variable cost in the

computation of the profit under this costing techniques (Hajibabaei, S., and et. Al, 2014).

Marginal costing- This costing tools is defined as expenses incurred while producing one

additional unit at production. It included fixed cost is taken as periodical cost and

variable cost as unit or product cost.

Part 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost Cards

November

Sales = 70* 10000 = £ 700000

Direct Materials = £100000

Direct Labour = £ 150000

Fixed Overheads = £ 250000

December

Sales = 70* 8000 = £ 560000

Direct Materials = £100000

Direct Labour = £ 150000

Fixed Overheads = £ 250000

Inventory = £ 2000 units

Absorption costing

Profit as Per

absorption costing

£s November

£s

£s December

£s

Turnover 700000 560000

Less Full cost of sales 500000 400000

Direct Material cost 100000 100000

Direct Labour cost 150000 150000

Fixed manufacturing

overhead

250000 250000

Less:Closing Stock 100000

Gross Profit 200000 160000

Less: Under

absorption

0 50000

November

Sales = 70* 10000 = £ 700000

Direct Materials = £100000

Direct Labour = £ 150000

Fixed Overheads = £ 250000

December

Sales = 70* 8000 = £ 560000

Direct Materials = £100000

Direct Labour = £ 150000

Fixed Overheads = £ 250000

Inventory = £ 2000 units

Absorption costing

Profit as Per

absorption costing

£s November

£s

£s December

£s

Turnover 700000 560000

Less Full cost of sales 500000 400000

Direct Material cost 100000 100000

Direct Labour cost 150000 150000

Fixed manufacturing

overhead

250000 250000

Less:Closing Stock 100000

Gross Profit 200000 160000

Less: Under

absorption

0 50000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit 110000

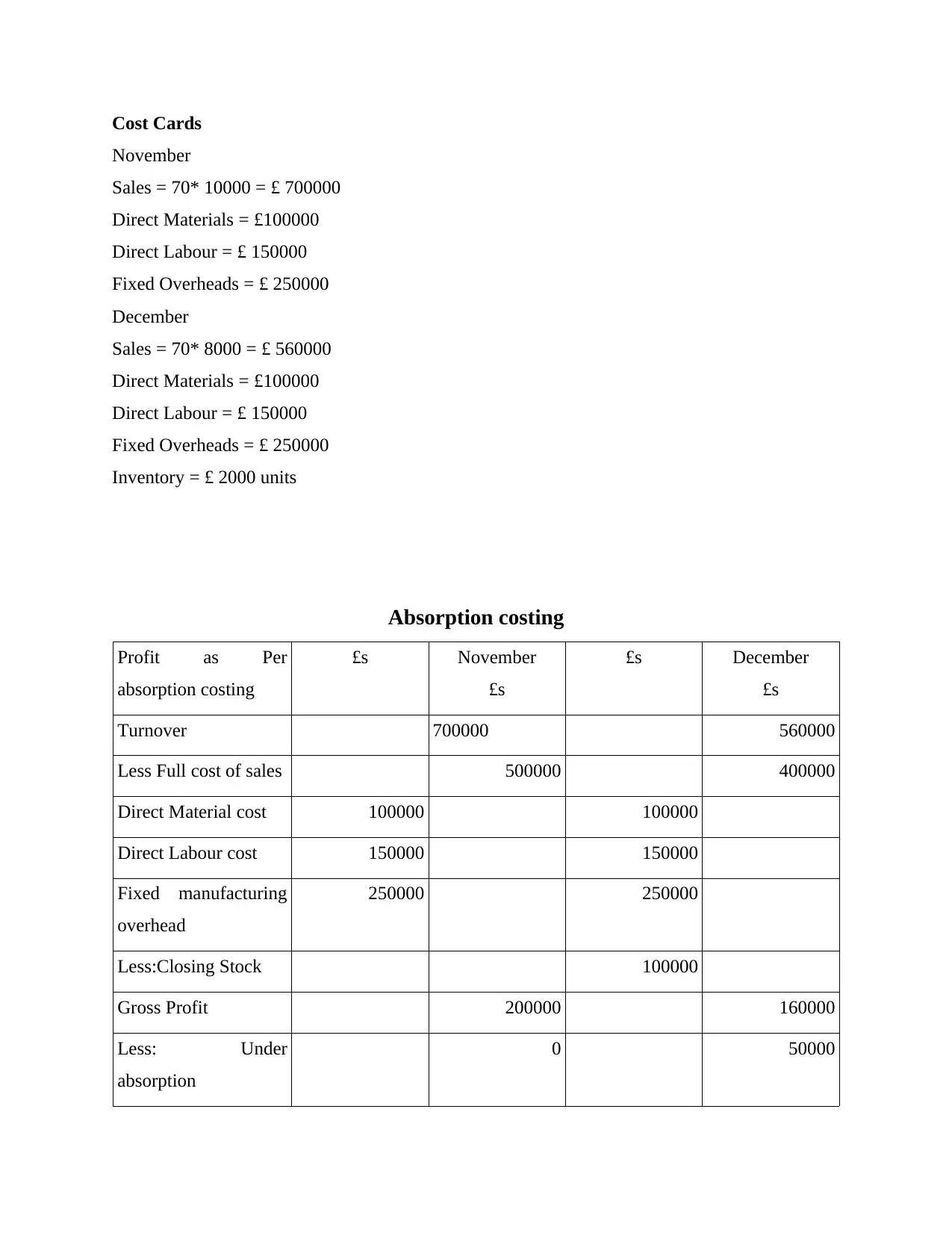

Marginal costing

Profit as Per

absorption costing

£s November

£s

£s December

£s

Turnover 700000 560000

Less Full cost of sales 500000 400000

Direct Material cost 100000 100000

Direct Labour cost 150000 150000

Fixed manufacturing

overhead

250000 250000

Less:Closing Stock 100000

Gross Profit 200000 160000

Part 2

Flexed Budget for the actual activity

Particulars Budget Actual Variances Variances (%)

Sales 100000 122000 22000 22.00%

Less: Cost of

Goods sold

87500 114500 27000 30.86%

Direct Material 50000 60000 10000 20.00%

Direct Labour 25000 28500 3500 14.00%

Variable

Overhead

12500 15000 2500 20.00%

Gross Profit 12500 7500 -5000 -40.00%

Marginal costing

Profit as Per

absorption costing

£s November

£s

£s December

£s

Turnover 700000 560000

Less Full cost of sales 500000 400000

Direct Material cost 100000 100000

Direct Labour cost 150000 150000

Fixed manufacturing

overhead

250000 250000

Less:Closing Stock 100000

Gross Profit 200000 160000

Part 2

Flexed Budget for the actual activity

Particulars Budget Actual Variances Variances (%)

Sales 100000 122000 22000 22.00%

Less: Cost of

Goods sold

87500 114500 27000 30.86%

Direct Material 50000 60000 10000 20.00%

Direct Labour 25000 28500 3500 14.00%

Variable

Overhead

12500 15000 2500 20.00%

Gross Profit 12500 7500 -5000 -40.00%

Less: Fixed

Overhead

10000 11000 1000 10.00%

Net Profit 2500 -3500 -6000 -240.00%

TASK 3.

P4. Advantages and disadvantages of planning tools used for budgetary control:

The budgetary control refers to a process of the discern different actual result with

budgeted information and data for a business over a period of time. It set the standard business

target to the business activities and compared with actual situation to determine the variances.

Cash budget- This is the budgeting control system that is defined as future estimation of the

cash receipt and cash payment during a certain period of time. It forecast the cash inflow and

outflow assorted future activities are included accumulation of budgeted cash sales, receipts from

debtors, expenses etc.

Advantages- This budget is helpful in to understand the liquidity position of the company

on regular basis (Goudarzvand Ghegini and Esmaeili, 2015).

Disadvantage- This is based on the forecasting the future data and information which may be

true or wrong. so future result can be lead the outflow of the cash.

Operating budget- This is annual budget that includes estimation of the total value of fund and

resources needed to perform the business operation. Company Warwick fabrics UK Ltd used

this budget in the business processing unit of manufacturer the fabrics to ascertain the total sum

of the resources required.

Advantages: Management can handle the fund and resources such as expenditure,

budgeted income, sales revenue, direct expenses etc.

Disadvantage: In the limitation of the this budget it require long term planning and

decision making regards the financial operation. It may lead extra costing by the management.

Overhead

10000 11000 1000 10.00%

Net Profit 2500 -3500 -6000 -240.00%

TASK 3.

P4. Advantages and disadvantages of planning tools used for budgetary control:

The budgetary control refers to a process of the discern different actual result with

budgeted information and data for a business over a period of time. It set the standard business

target to the business activities and compared with actual situation to determine the variances.

Cash budget- This is the budgeting control system that is defined as future estimation of the

cash receipt and cash payment during a certain period of time. It forecast the cash inflow and

outflow assorted future activities are included accumulation of budgeted cash sales, receipts from

debtors, expenses etc.

Advantages- This budget is helpful in to understand the liquidity position of the company

on regular basis (Goudarzvand Ghegini and Esmaeili, 2015).

Disadvantage- This is based on the forecasting the future data and information which may be

true or wrong. so future result can be lead the outflow of the cash.

Operating budget- This is annual budget that includes estimation of the total value of fund and

resources needed to perform the business operation. Company Warwick fabrics UK Ltd used

this budget in the business processing unit of manufacturer the fabrics to ascertain the total sum

of the resources required.

Advantages: Management can handle the fund and resources such as expenditure,

budgeted income, sales revenue, direct expenses etc.

Disadvantage: In the limitation of the this budget it require long term planning and

decision making regards the financial operation. It may lead extra costing by the management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Master budget: This is detailed budget contents the summery of various budget such as cash,

sales, fix and flexible budget and other relevant budget. Company is using this tools to

summarised the financial information and data to understand capital and resources from related

department.

Advantages: It is used in well planning to allocate the funds and resources in the different

head by the help of the assorted type of budget planning.

Disadvantages: It fails to give accurate information taken up from subsidiary budgets

which may lead the cost maximisation in the particular projects (Gajevszky, 2013).

Warwick fabrics UK Ltd uses the different kind of budgetary control system in the

business in an effective and efficient manner. The business of management deals with current set

of manner that helps them to manage their sections. Warwick fabrics UK Ltd uses this report to

provide the information regarding the late customer who are entertain with the credit amount.

TASK 4.

P5. Comparison of organisations to solve the financial issues

In the current business market, enterprises of production and manufacture are facing the

difficulties due to lack of the fund and other resources of the business. In context to the Warwick

fabrics United Kingdom that are totally depends on the management how they settle these issue

or problem. Warwick fabrics UK Ltd is using this tool to analysis the total production cost by

allocating the estimated on the different task and projects. Some financial issues and problem are

described as follow:

Less sales: This is the particular issue of the company Warwick fabrics UK Ltd that is

facing the problem related to decrements in the sales. It this concern, It is required to settle the

issue as soon as possible otherwise It may cause the decrements in the profit too. This is most

common issue to business that is business is facing. Currently, company is stuck at the financial

problem (Eslami Eshlaghi and Khamseh, 2019).

Higher expenses: In this particular financial problem, company's expenses are higher

and profit is lower. The reason behind it, inappropriate management of the operating and

functional resources at the processing unit that may create the financial crises. This is crucial for

institution to get over from this financial problem early.

Methods for deducting financial issues:

sales, fix and flexible budget and other relevant budget. Company is using this tools to

summarised the financial information and data to understand capital and resources from related

department.

Advantages: It is used in well planning to allocate the funds and resources in the different

head by the help of the assorted type of budget planning.

Disadvantages: It fails to give accurate information taken up from subsidiary budgets

which may lead the cost maximisation in the particular projects (Gajevszky, 2013).

Warwick fabrics UK Ltd uses the different kind of budgetary control system in the

business in an effective and efficient manner. The business of management deals with current set

of manner that helps them to manage their sections. Warwick fabrics UK Ltd uses this report to

provide the information regarding the late customer who are entertain with the credit amount.

TASK 4.

P5. Comparison of organisations to solve the financial issues

In the current business market, enterprises of production and manufacture are facing the

difficulties due to lack of the fund and other resources of the business. In context to the Warwick

fabrics United Kingdom that are totally depends on the management how they settle these issue

or problem. Warwick fabrics UK Ltd is using this tool to analysis the total production cost by

allocating the estimated on the different task and projects. Some financial issues and problem are

described as follow:

Less sales: This is the particular issue of the company Warwick fabrics UK Ltd that is

facing the problem related to decrements in the sales. It this concern, It is required to settle the

issue as soon as possible otherwise It may cause the decrements in the profit too. This is most

common issue to business that is business is facing. Currently, company is stuck at the financial

problem (Eslami Eshlaghi and Khamseh, 2019).

Higher expenses: In this particular financial problem, company's expenses are higher

and profit is lower. The reason behind it, inappropriate management of the operating and

functional resources at the processing unit that may create the financial crises. This is crucial for

institution to get over from this financial problem early.

Methods for deducting financial issues:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

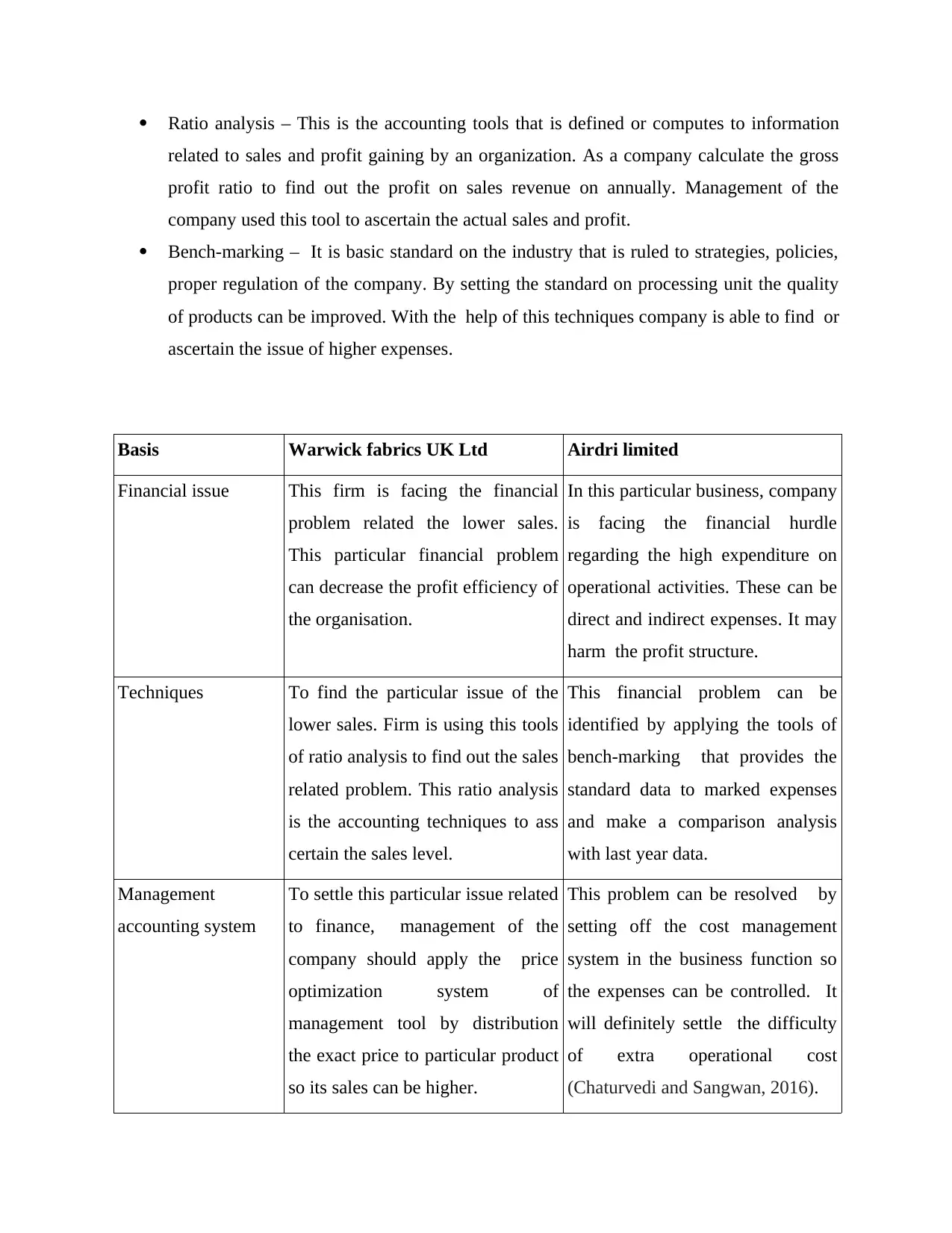

Ratio analysis – This is the accounting tools that is defined or computes to information

related to sales and profit gaining by an organization. As a company calculate the gross

profit ratio to find out the profit on sales revenue on annually. Management of the

company used this tool to ascertain the actual sales and profit.

Bench-marking – It is basic standard on the industry that is ruled to strategies, policies,

proper regulation of the company. By setting the standard on processing unit the quality

of products can be improved. With the help of this techniques company is able to find or

ascertain the issue of higher expenses.

Basis Warwick fabrics UK Ltd Airdri limited

Financial issue This firm is facing the financial

problem related the lower sales.

This particular financial problem

can decrease the profit efficiency of

the organisation.

In this particular business, company

is facing the financial hurdle

regarding the high expenditure on

operational activities. These can be

direct and indirect expenses. It may

harm the profit structure.

Techniques To find the particular issue of the

lower sales. Firm is using this tools

of ratio analysis to find out the sales

related problem. This ratio analysis

is the accounting techniques to ass

certain the sales level.

This financial problem can be

identified by applying the tools of

bench-marking that provides the

standard data to marked expenses

and make a comparison analysis

with last year data.

Management

accounting system

To settle this particular issue related

to finance, management of the

company should apply the price

optimization system of

management tool by distribution

the exact price to particular product

so its sales can be higher.

This problem can be resolved by

setting off the cost management

system in the business function so

the expenses can be controlled. It

will definitely settle the difficulty

of extra operational cost

(Chaturvedi and Sangwan, 2016).

related to sales and profit gaining by an organization. As a company calculate the gross

profit ratio to find out the profit on sales revenue on annually. Management of the

company used this tool to ascertain the actual sales and profit.

Bench-marking – It is basic standard on the industry that is ruled to strategies, policies,

proper regulation of the company. By setting the standard on processing unit the quality

of products can be improved. With the help of this techniques company is able to find or

ascertain the issue of higher expenses.

Basis Warwick fabrics UK Ltd Airdri limited

Financial issue This firm is facing the financial

problem related the lower sales.

This particular financial problem

can decrease the profit efficiency of

the organisation.

In this particular business, company

is facing the financial hurdle

regarding the high expenditure on

operational activities. These can be

direct and indirect expenses. It may

harm the profit structure.

Techniques To find the particular issue of the

lower sales. Firm is using this tools

of ratio analysis to find out the sales

related problem. This ratio analysis

is the accounting techniques to ass

certain the sales level.

This financial problem can be

identified by applying the tools of

bench-marking that provides the

standard data to marked expenses

and make a comparison analysis

with last year data.

Management

accounting system

To settle this particular issue related

to finance, management of the

company should apply the price

optimization system of

management tool by distribution

the exact price to particular product

so its sales can be higher.

This problem can be resolved by

setting off the cost management

system in the business function so

the expenses can be controlled. It

will definitely settle the difficulty

of extra operational cost

(Chaturvedi and Sangwan, 2016).

CONCLUSION

From the above report it is concluded that management accounting and its requirement in

the business organisation play a crucial role to enhance the capacity and productivity by applying

the tools. Certain MA tools like cost and price optimisation techniques are help in the setting the

price to its product and services and also control the cost and allocation of the effective manner.

These MA reports are help in the decision making system of the processing unit. In further to

this, budgetary control that help in forecast the business condition as income and expenses at

particular level of production. It resolve the financial issues and problem with the help of these.

From the above report it is concluded that management accounting and its requirement in

the business organisation play a crucial role to enhance the capacity and productivity by applying

the tools. Certain MA tools like cost and price optimisation techniques are help in the setting the

price to its product and services and also control the cost and allocation of the effective manner.

These MA reports are help in the decision making system of the processing unit. In further to

this, budgetary control that help in forecast the business condition as income and expenses at

particular level of production. It resolve the financial issues and problem with the help of these.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.